Asthma Spacers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

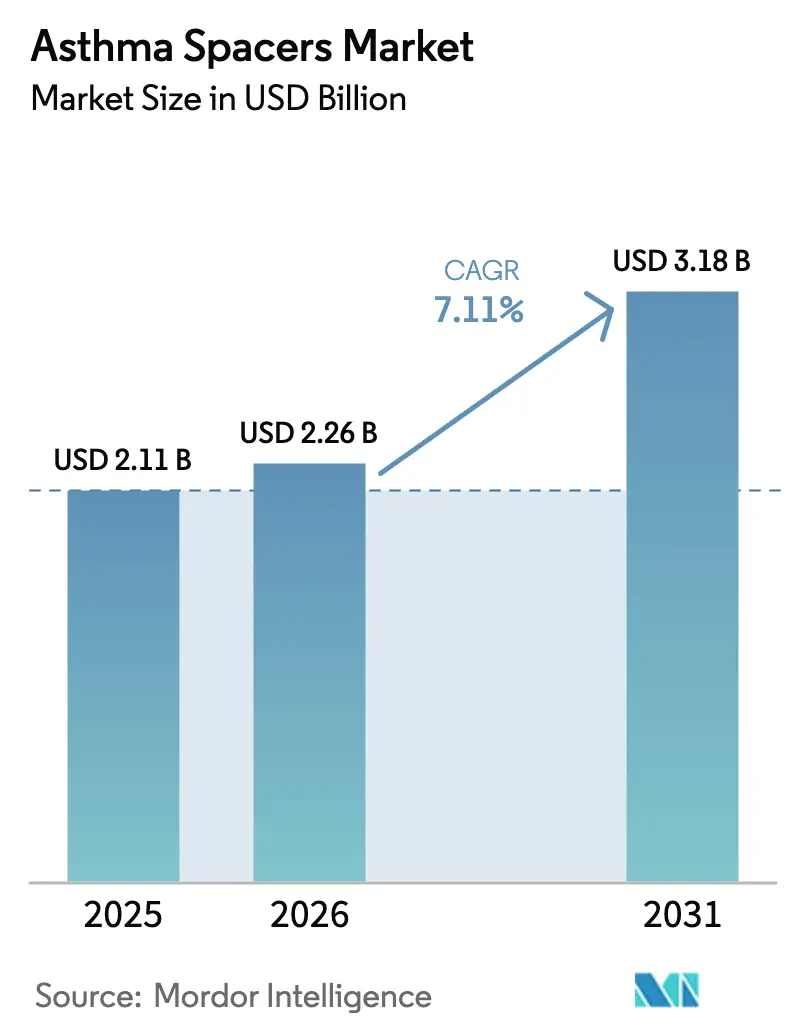

| Market Size (2026) | USD 2.26 Billion |

| Market Size (2031) | USD 3.18 Billion |

| Growth Rate (2026 - 2031) | 7.11% CAGR |

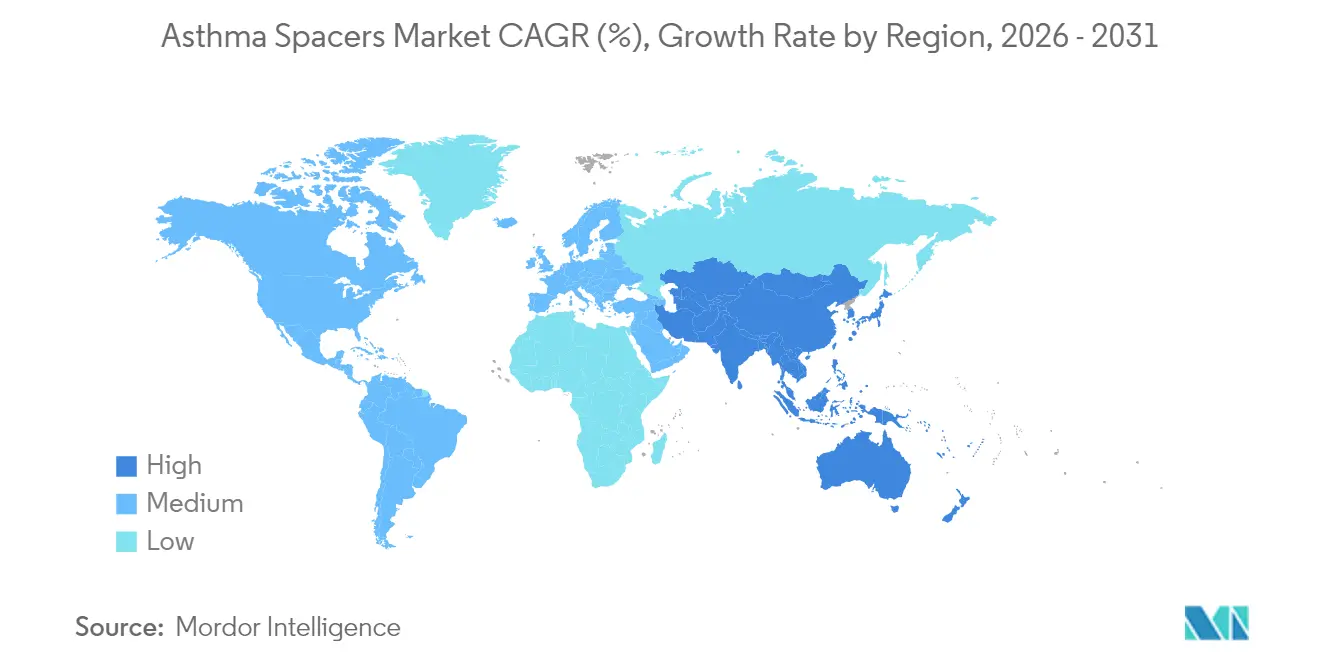

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asthma Spacers Market Analysis by Mordor Intelligence

The asthma spacers market size was valued at USD 2.11 billion in 2025 and estimated to grow from USD 2.26 billion in 2026 to reach USD 3.18 billion by 2031, at a CAGR of 7.11% during the forecast period (2026-2031). Growth rests on the rising role of spacer devices in improving medication delivery efficiency, supported by evolving regulatory guidance that simplifies device innovation pathways. Increasing global asthma prevalence, heightened clinician awareness of spacer-assisted inhalation, and continuous product enhancements in anti-static and smart technologies further support revenue expansion. North American market maturity, Asia-Pacific’s rapid incidence growth, and supply chain challenges that elevate the value proposition of dose-saving devices reinforce demand momentum. Sustainability mandates and digital health integration add new layers of competitiveness, prompting both incumbents and emerging firms to invest in reusable materials and connected features.

Key Report Takeaways

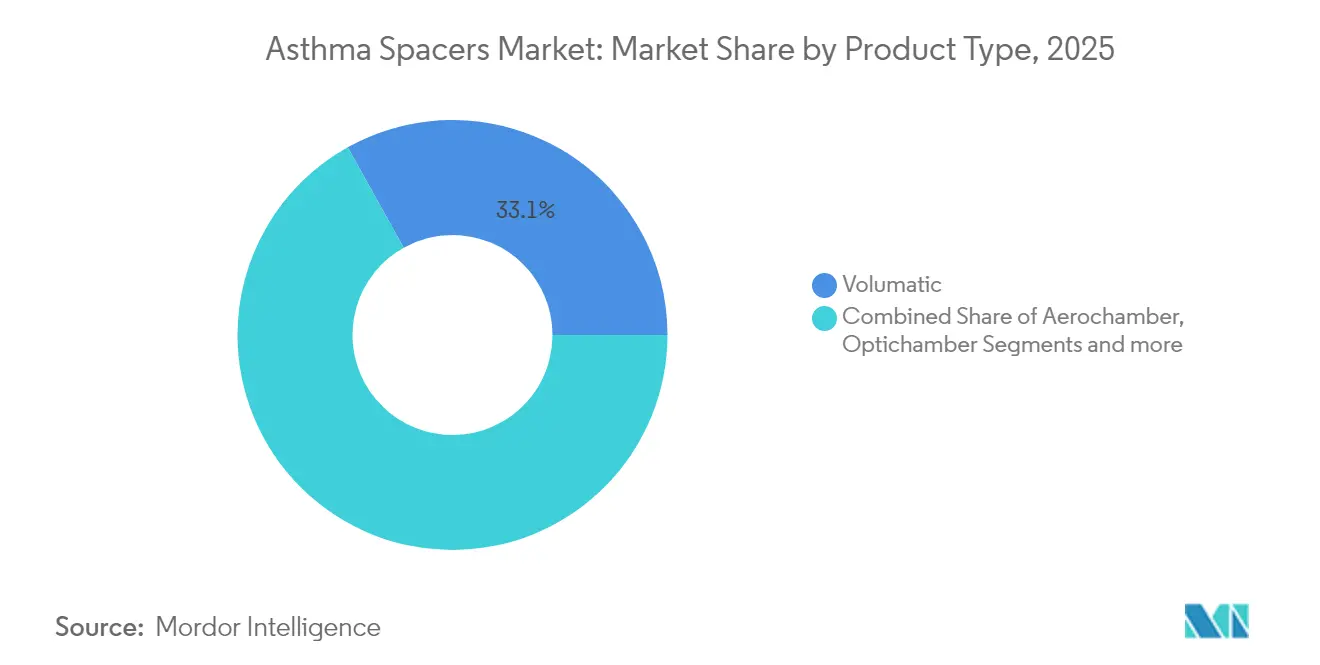

- By product type, Volumatic spacers led with 33.10% asthma spacers market share in 2025, while Optichamber is projected to grow at a 7.88% CAGR through 2031.

- By material, polycarbonate commanded 40.85% share of the asthma spacers market size in 2025, whereas metal spacers are set to expand at an 8.01% CAGR to 2031.

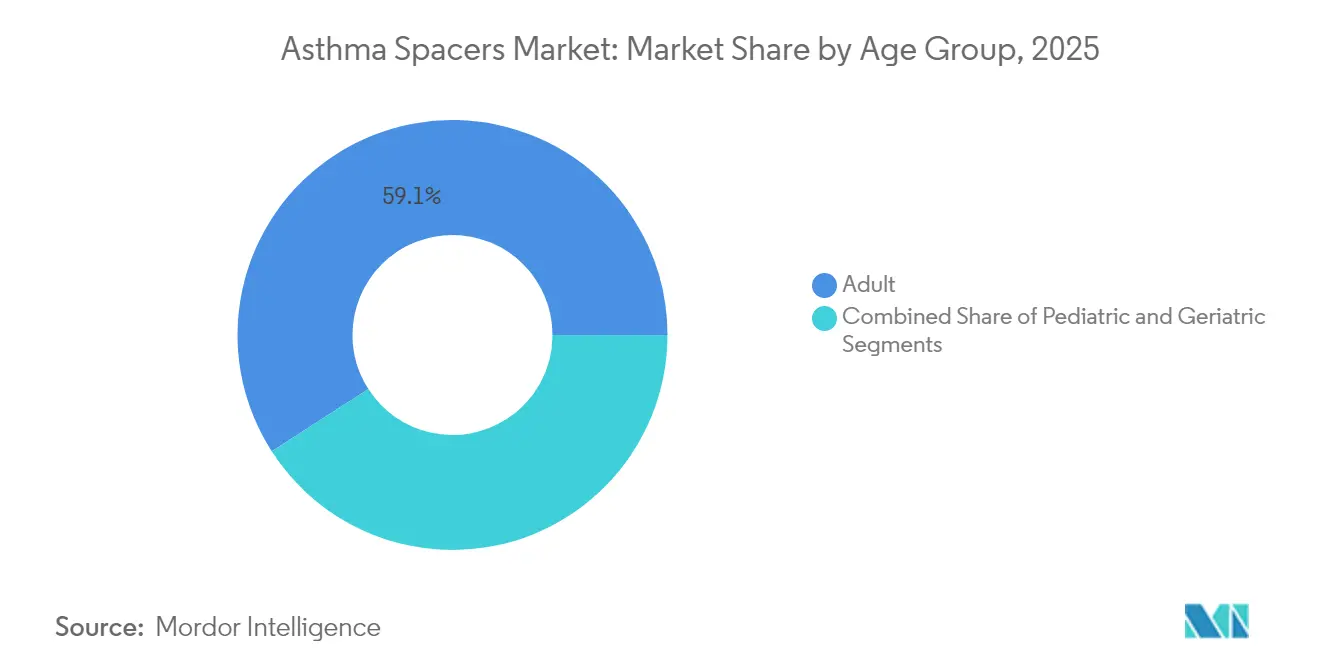

- By age group, adult patients accounted for 59.10% revenue in 2025; the pediatric segment is the fastest growing at an 7.92% CAGR up to 2031.

- By distribution channel, hospital pharmacies held 56.10% of the asthma spacers market in 2025, but e-commerce is advancing at an 8.09% CAGR through 2031.

- By geography, North America captured 40.80% of global revenue in 2025; Asia-Pacific is poised for the highest regional CAGR of 8.11% over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Asthma Spacers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of chronic respiratory diseases | +2.1% | Global, with highest impact in APAC and MEA | Long term (≥ 4 years) |

| Growing awareness of spacer-assisted inhalation | +1.8% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Intensifying R&D in anti-static & smart spacers | +1.5% | North America & EU core, spill-over to APAC | Medium term (2-4 years) |

| Eco-friendly inhaler initiatives favouring spacers | +0.9% | EU primary, North America secondary | Long term (≥ 4 years) |

| Tele-respiratory care & digital adherence tools | +0.7% | North America & EU, selective APAC markets | Short term (≤ 2 years) |

| Home-based respiratory therapy expansion | +0.6% | Global, accelerated in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising prevalence of chronic respiratory diseases

Asthma cases are projected to rise from 260 million in 2021 to 275 million by 2050, with modifiable factors responsible for nearly 30% of the disease burden [1]Aleksandr Aravkin. "Global, regional, and national burden of asthma and atopic dermatitis, 1990–2021, and projections to 2050: a systematic analysis of the Global Burden of Disease Study 2021," IHME, healthdata.org The increase sustains long-term demand for spacers as healthcare systems seek cost-effective ways to enhance inhaled therapy outcomes. Asia-Pacific faces distinct pressure, with only 7.6% of patients achieving well-controlled asthma across nine countries, signaling substantial upside for devices that support adherence. Although China’s incidence rate fell over three decades, demographic shifts imply absolute case numbers could reach 4.5 million by 2046 [2]Xi Chen, "Temporal trends and future projections of incidence rate and mortality for asthma in China: an analysis of the Global Burden of Disease Study 2021," Frontiers in Medicine, frontiersin.org. Globally, chronic respiratory diseases remain the third leading cause of death, underscoring the need for optimized inhaler technology.

Growing awareness of spacer-assisted inhalation

Clinical studies report 21-25% better bronchodilator response when anti-static chambers are used during nocturnal bronchospasm episodes. Education campaigns now emphasize correct inhaler technique, particularly for children, leading to fewer errors and longer inhalation time. Professional guidelines recommend spacers for all children using pressurized metered-dose inhalers and for patients prescribed high-dose corticosteroids. Reimbursement frameworks in developed markets increasingly prefer proven, cost-effective accessories, turning guidelines into standardized purchase drivers.

Intensifying R&D in anti-static & smart spacers

Product innovation centers on superior materials and digital connectivity. Trudell Medical’s Z STAT chamber shows improved drug delivery versus conventional designs. Adherium’s FDA-cleared Smartinhaler integrates with leading inhalation therapies to track adherence in real time. Wearable solutions, such as the AI Asthma Guard smartwatch, leverage physiologic and environmental signals to predict attacks [3]Hajar Almuhanna, "AI Asthma Guard: Predictive Wearable Technology for Asthma Management in Vulnerable Populations," MDPI, mdpi.com. Advanced cyclone prototypes selectively allow particles under 5 µm to pass, potentially raising lung deposition efficiency.

Eco-friendly inhaler initiatives favoring spacers

Europe’s Packaging and Packaging Waste Regulation requires recyclable design by 2030, indirectly benefiting reusable spacer models. Partnerships—for example, DevPro Biopharma and Bespak—explore low-global-warming albuterol formulations where spacers enhance effectiveness. Healthcare buyers increasingly consider lifecycle impacts; spacers’ durability aligns with circular economy targets and helps clinicians meet environmental pledges.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium pricing of branded anti-static chambers | -1.2% | Global, most acute in LMIC markets | Short term (≤ 2 years) |

| Limited reimbursement & user awareness in LMICs | -0.8% | LMIC markets, particularly Sub-Saharan Africa and South Asia | Long term (≥ 4 years) |

| Sustainability regulations on single-use plastics | -0.5% | EU primary, expanding to North America | Medium term (2-4 years) |

| "For-children" perception curbing adult uptake | -0.4% | Global, particularly pronounced in APAC cultural contexts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Premium pricing of branded anti-static chambers

Advanced anti-static spacers cost 40-60% more than basic models, limiting affordability in price-sensitive markets where out-of-pocket health expenses dominate. The differential keeps high-end devices concentrated in developed economies, while conventional spacer formats prevail elsewhere. As manufacturing volumes rise and patents expire, generic competitors could narrow the price gap and reduce this constraint.

Limited reimbursement & user awareness in LMICs

In many low- and middle-income countries, spacers lack formal reimbursement classifications, restricting uptake. Billing guidelines, such as Montana’s HCPC-based protocol, illustrate complexity even in advanced systems. Cultural reservations toward asthma diagnoses in several Asian populations further depress adult adoption. Expanding clinician training and advocacy campaigns seek to shift perceptions, but coverage gaps remain a hurdle.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Optichamber builds momentum amid Volumatic leadership

Volumatic devices generated 33.10% of revenue in 2025, anchoring the asthma spacers market through clinician familiarity and broad hospital adoption. Optichamber’s 7.88% CAGR underscores preference for anti-static performance, particularly in outpatient and home settings where self-administered accuracy matters most. Aerochamber maintains strong pediatric positioning, while Inspirease targets users needing breath-actuated support. Product diversification limits direct price competition and encourages targeted marketing strategies.

Second-generation smart spacers integrate acoustic or pressure sensors to verify patient technique, expanding therapy adherence data. Manufacturers that bundle analytics with consumables aim to secure recurring revenue streams beyond initial device sales. Hospitals increasingly embed device selection into formularies, weighing real-world outcomes evidence over legacy brand loyalty. As reimbursement frameworks reward proven effectiveness, premium products with clinical validation capture higher margins despite cost-constrained procurement climates.

By Material: Polycarbonate strength meets metal sustainability appeal

Polycarbonate accounted for 40.85% of 2025 revenue, reflecting cost-effective manufacturing, transparency for visual dose confirmation, and acceptable anti-static coatings. Metal spacers, though representing a smaller base, post an 8.01% CAGR as hospitals and regulators champion reusable solutions with lower environmental footprint. The asthma spacers market size for metal formats is forecast to widen as lifecycle value analyses favor durable devices within green procurement policies.

Innovations in composite and specialty plastics occupy a transitional space, offering enhanced chemical resistance or ergonomic comfort. Suppliers experiment with antimicrobial treatments to reduce infection risk in reusable units. European tenders increasingly score bids on sustainability metrics, driving material choices. In the United States, hospital groups weigh long-run cost savings from fewer replacements against higher upfront acquisition prices for metal designs.

By Age Group: Pediatric demand accelerates beyond adult base

Adults retained 59.10% revenue contribution in 2025, reflecting broader prevalence and purchasing power. The pediatric segment records an 7.92% CAGR, supported by guideline-mandated spacer use with pressurized inhalers. Growing caregiver education and school-based asthma programs further boost uptake. The asthma spacers market share held by pediatric devices is expected to climb steadily as adherence benefits become widely publicized.

Geriatric adoption remains modest yet growing, driven by comorbid respiratory conditions and caregiver involvement. Device makers address arthritic dexterity issues by adding larger actuators and visual cues. Insurers begin to recognize spacers as preventive tools that lower hospital admissions, encouraging coverage for elderly patients. Demographic segmentation inspires tailored marketing: child-friendly designs use bright colors and playful shapes, whereas adult lines emphasize discretion and portability.

By Distribution Channel: E-commerce advances as hybrid models emerge

Hospital pharmacies dominated distribution with 56.10% share in 2025, capturing initial prescriptions and forming long-term user habits. E-commerce grows at an 8.09% CAGR thanks to telehealth, direct-to-consumer marketing, and subscription refill services. The asthma spacers market size for online sales is expected to nearly double by 2030, though overall channel fragmentation persists.

Retail pharmacies remain vital for insurance processing and impulse replacements, yet face pressure from mail-order portals. Manufacturers deploy omnichannel strategies: hospital detailing drives clinical endorsement, retail merchandising ensures shelf presence, and branded websites foster loyalty through tutorial content and app integration. Channel partners invest in data analytics to predict reorder cycles and personalize promotions.

Geography Analysis

North America generated 40.80% of global sales in 2025, buoyed by widespread insurance coverage, strong clinician awareness, and the FDA’s clear regulatory pathway that shortens innovation cycles. Supply chain disruptions in 2024 exposed inhaler vulnerabilities, elevating spacers as a conservation tool that maximizes existing inventory efficacy. Adoption of smart devices is highest in the United States, where adherence analytics feed directly into tele-respiratory platforms, enhancing reimbursement prospects.

Asia-Pacific is the fastest-growing territory with an 8.11% CAGR to 2031. Rising asthma prevalence, rapid urbanization, and improved medical infrastructure stimulate demand. Economic burden studies reveal per-patient costs spanning USD 108 to USD 1,010, highlighting a wide affordability range that manufacturers must navigate. Governments in China, India, and Indonesia launch awareness drives, creating fertile ground for pediatric spacer programs. Nonetheless, cultural resistance to chronic disease labeling persists, requiring localized educational content and community-based training.

Europe presents a stable yet dynamically regulated environment. The EU’s incoming recyclable packaging mandate favors reusable spacers and pressures single-use plastic components. The European Medicines Agency’s 2024 guidance streamlines approval for devices that contain ancillary medicinal substances, accelerating next-generation spacer entries. Temporary salbutamol shortages across several member states reaffirmed the importance of efficient drug delivery, thereby maintaining spacer demand through supply shocks.

South America and the Middle East & Africa register moderate adoption, constrained by reimbursement gaps and lower clinician familiarity. Pilot projects in Brazil and Saudi Arabia demonstrate that targeted training improves inhaler technique and lowers emergency visits, foreshadowing incremental penetration as payer systems mature. Donor-funded health programs increasingly bundle spacers with inhaled corticosteroids, leveraging device efficacy to stretch limited medicine budgets.

Competitive Landscape

Competition is moderate, with several multinational and regional players sharing revenue. Trudell Medical, Cipla, and GSK anchor the high-value tier through strong clinical evidence portfolios and global distribution. No single actor exceeds one-third market share, giving buyers multiple sourcing options and keeping price negotiations active. Digital capabilities emerge as new differentiators, evidenced by Adherium’s Smartinhaler platform that secures data partnerships with pulmonology clinics.

M&A activity centers on expanding respiratory portfolios. GSK’s USD 1.4 billion purchase of Aiolos Bio strengthens biologics capabilities, while Molex’s acquisition of Vectura Group enhances device-drug integration competencies. Joint ventures between pharmaceutical companies and electronics specialists explore predictive analytics, aiming to position connected spacers within broader chronic-care ecosystems. Intellectual property battles around anti-static coatings and aerosol optimization technologies remain active, though patent expiries in 2027-2028 could open space for value-priced entrants.

Regional manufacturers leverage cost advantages to supply domestic hospitals, particularly in India and China. These firms focus on basic polycarbonate designs, gradually adding anti-static treatments as local guidelines tighten. In mature markets, premium brands emphasize evidence-based superiority and sustainability credentials to command higher price points. Strategic emphasis on education campaigns persists; companies sponsor clinician workshops to reinforce correct device usage that correlates to better clinical outcomes and repeat purchases.

Asthma Spacers Industry Leaders

-

PARI GmbH

-

Koninklijke Philips N.V.

-

HAAG-STREIT GROUP

-

Cipla Inc.

-

Truedell Medical International

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Theravance Biopharma finalized the sale of its residual Trelegy Ellipta interest to GSK for USD 225 million, retaining up to USD 150 million in milestones through 2026.

- March 2025: The National Asthma Council Australia and Trudell Medical Australia released a new spacer-use resource highlighting that only 10% of patients execute correct inhaler technique.

- June 2024: Boehringer Ingelheim, AstraZeneca, and GSK capped out-of-pocket asthma inhaler costs at USD 35 per month for eligible US patients.

- April 2024: Adherium launched an FDA-cleared Smartinhaler compatible with AstraZeneca’s Airsupra and AbbVie’s Breztri, enabling real-time adherence monitoring.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our review defines the asthma spacer market as all single- and multi-use holding chambers that attach to pressurized metered-dose inhalers to slow aerosol velocity and improve pulmonary drug deposition across hospital, pharmacy, and online channels. According to Mordor Intelligence, the valuation for 2025 stands at USD 2.11 billion, and the study forecasts USD 2.99 billion by 2030.

Scope exclusion: Disposable mouthpieces sold with dry-powder inhalers and devices intended solely for COPD training are left outside our boundary.

Segmentation Overview

-

By Product Type

- Aerochamber

- Optichamber

- Volumatic

- Inspirease

-

By Material

- Polycarbonate

- Metal

- Others

-

By Age Group

- Paediatric

- Adult

- Geriatric

-

By Distribution Channel

- Hospital Pharmacy

- Retail Pharmacy

- E-Commerce

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

-

Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed respiratory therapists, pediatric pulmonologists, and supply-chain managers in North America, Europe, India, and Brazil. These discussions clarified real-world usage frequency, typical life span of reusable chambers, and discounting structures agreed with group purchasing organizations, which in turn refined our unit multiplier and price decay curves.

Desk Research

We first mapped demand drivers using publicly available epidemiology from the World Health Organization, the Global Initiative for Asthma, and the U.S. CDC, which quantify diagnosed patient pools and attack frequency. Trade statistics from UN Comtrade helped us approximate cross-border flows of plastic medical parts that correlate with spacer assembly volumes, while procurement notices on Tenders Info revealed hospital purchase patterns across Southeast Asia.

Company 10-K filings, investor decks, and quarterly calls added average selling price trends, and D&B Hoovers furnished revenue splits for leading spacer manufacturers that guide channel mix assumptions. Patent abstracts sourced through Questel highlighted anti-static material adoption curves that influence replacement rates. The sources listed are illustrative; many other credible references were consulted for corroboration.

Market-Sizing & Forecasting

We build the 2025 baseline through a top-down prevalence-to-treated-cohort calculation, multiplying country-level asthma cases by inhaler penetration and spacer attachment rates, which are then validated against selective bottom-up roll-ups of manufacturer shipments and sampled ASP x volume checks. Key variables include diagnosed asthma prevalence, share of pressurized inhalers within total therapy, mean spacer replacement interval, anti-static spacer uptake, average retail ASP, and regional reimbursement coverage ratios. A multivariate regression model projects these drivers forward; scenario analysis around pollution growth and pediatric diagnosis rates frames upside and downside cases. Gaps in bottom-up data, for example, in fragmented Latin American retail, are bridged with regional shipment proxies and primary interview insights before final convergence.

Data Validation & Update Cycle

Model outputs pass anomaly screening, variance checks against external benchmarks, and a two-level analyst review. We refresh every twelve months, and material events such as regulatory bans or large tender wins trigger interim updates. Prior to client delivery, an analyst re-runs the latest data pull so users receive the freshest view.

Why Mordor's Asthma Spacers Baseline Stands Up to Scrutiny

Published estimates seldom align because firms pick differing device mixes, pricing ladders, and refresh cadences. We state these factors up front so buyers understand why numbers diverge.

Key gap drivers include whether single-patient hospital spacers are counted, how fast anti-static upgrades are assumed, the currency year chosen for ASP conversion, and how frequently models are back-tested with clinicians.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.11 B (2025) | Mordor Intelligence | - |

| USD 1.80 B (2023) | Global Consultancy A | Excludes emerging-market retail and hospital single-use units |

| USD 1.86 B (2024) | Trade Journal B | Blends spacers with nebulizer mouthpieces, diluting device-specific value |

| USD 2.10 B (2024) | Industry Association C | Uses static ASPs without accounting for anti-static premium or currency shifts |

In summary, our disciplined scope selection, variable transparency, and annual refresh give decision-makers a balanced, reproducible starting point, while the gap analysis shows why Mordor Intelligence provides the steadier compass amid varied public figures.

Key Questions Answered in the Report

What is the current size of the asthma spacers market?

The asthma spacers market reached USD 2.26 billion in 2026 and is projected to hit USD 3.18 billion by 2031 at a 7.11% CAGR.

Which product type holds the largest asthma spacers market share today?

Volumatic spacers led with 33.10% market share in 2025.

Why is the Asia-Pacific region growing fastest in the asthma spacers market?

Rising asthma prevalence, expanding healthcare access, and greater clinician focus on inhaler technique are driving an 8.11% regional CAGR through 2031.

How are sustainability regulations influencing spacer demand?

European packaging rules favor reusable devices, prompting hospitals to prefer metal or durable polycarbonate spacers that lower environmental impact.

What role do smart spacers play in market growth?

Digital adherence monitoring and tele-respiratory integration enhance treatment outcomes, allowing smart spacers to command premium pricing and expand overall market value.

Which distribution channel is expanding quickest for spacer sales?

E-commerce is growing at an 8.09% CAGR as telemedicine and direct-to-consumer models gain traction.

Page last updated on: