Smart Inhalers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

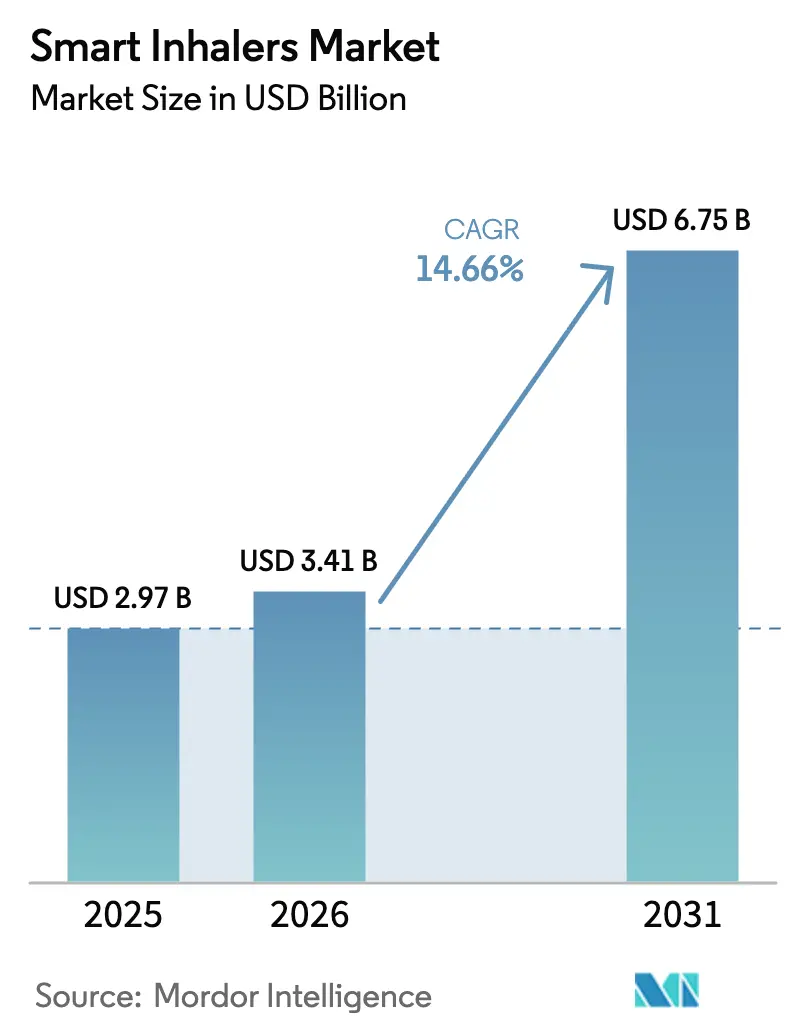

| Market Size (2026) | USD 3.41 Billion |

| Market Size (2031) | USD 6.75 Billion |

| Growth Rate (2026 - 2031) | 14.66% CAGR |

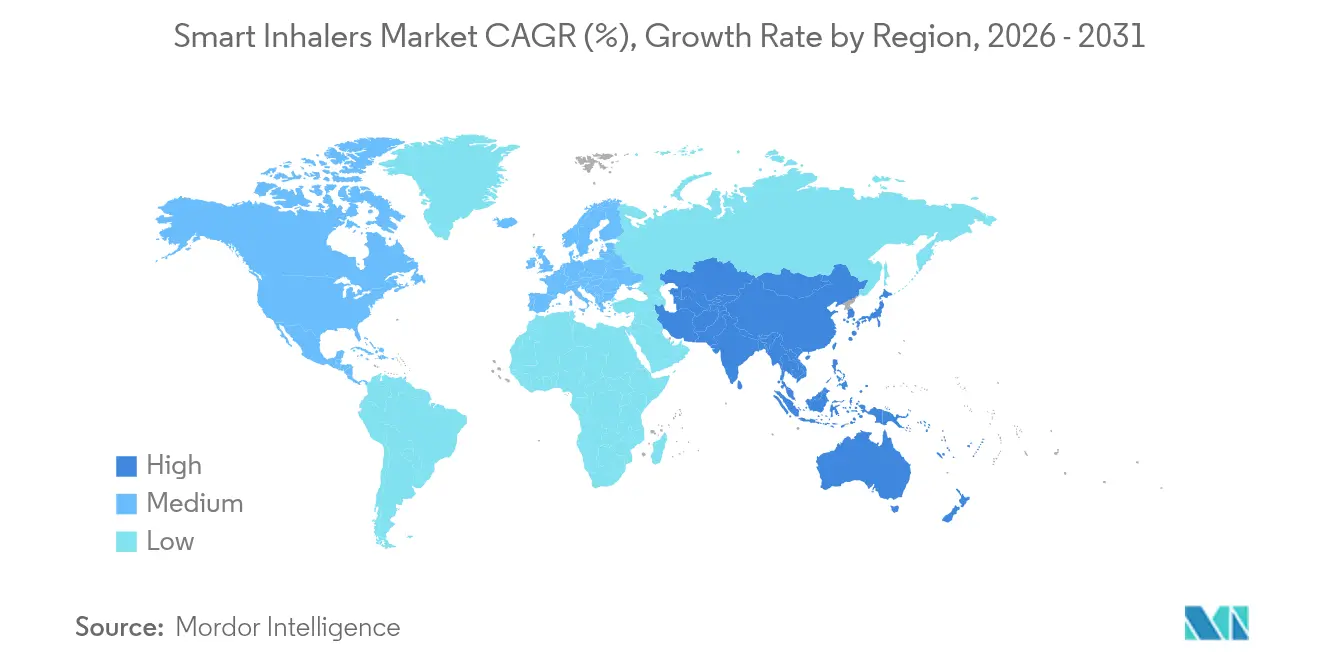

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Inhalers Market Analysis by Mordor Intelligence

Smart Inhalers Market size in 2026 is estimated at USD 3.41 billion, growing from 2025 value of USD 2.97 billion with 2031 projections showing USD 6.75 billion, growing at 14.66% CAGR over 2026-2031. Demand reflects the convergence of digital-health priorities with the long-term management of asthma and COPD, where adherence gaps have historically limited therapeutic success. FDA guidance issued in 2024 clarifies validation requirements for connected drug-delivery devices, shortening approval timelines and encouraging product launches.[1]Source: U.S. Food and Drug Administration, “Essential Drug Delivery Outputs for Devices,” fda.gov Environmental sustainability mandates are redirecting R&D toward propellant-free or near-zero global-warming-potential formulations, a shift embodied by AstraZeneca’s next-generation Breztri program. At the same time, AI-enabled analytics within inhalers generate real-time adherence data that clinicians convert into proactive interventions, reducing exacerbation-related hospitalizations.

Key Report Takeaways

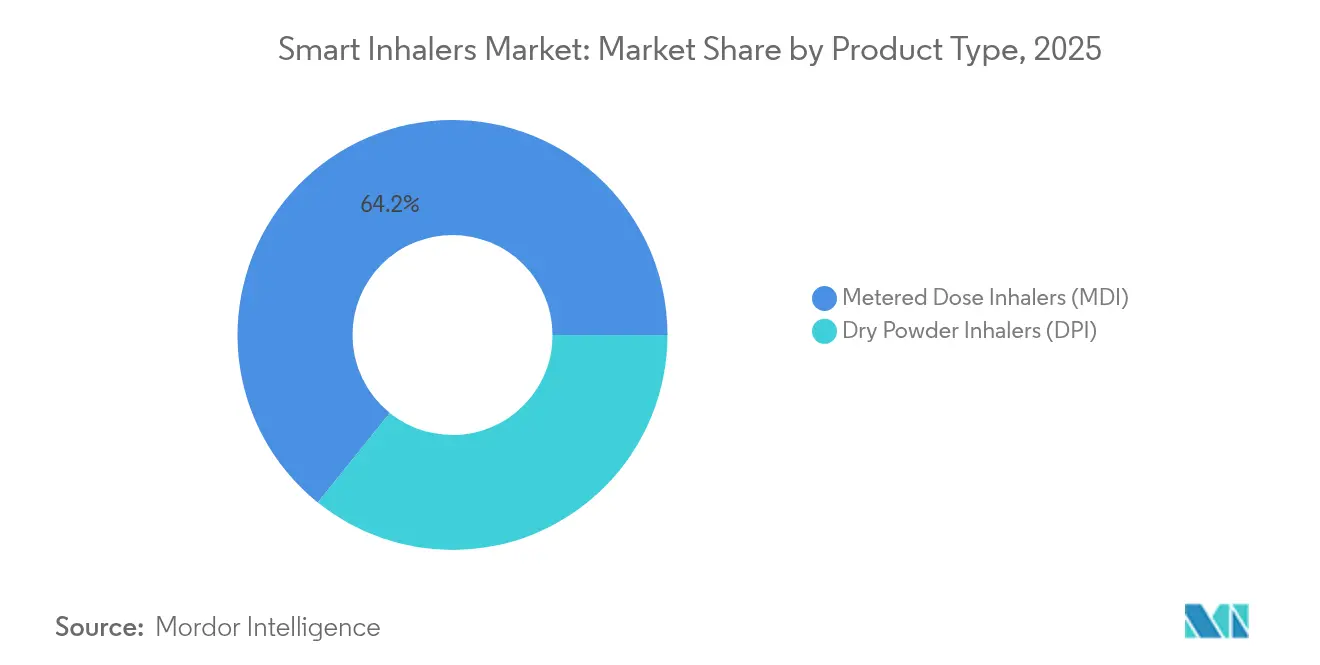

- By product type, Metered Dose Inhalers held 64.22% of the smart inhalers market share in 2025, while Dry Powder Inhalers are forecast to expand at a 15.69% CAGR to 2031.

- By indication, COPD accounted for 50.71% revenue in 2025; asthma is projected to grow fastest at a 15.01% CAGR through 2031.

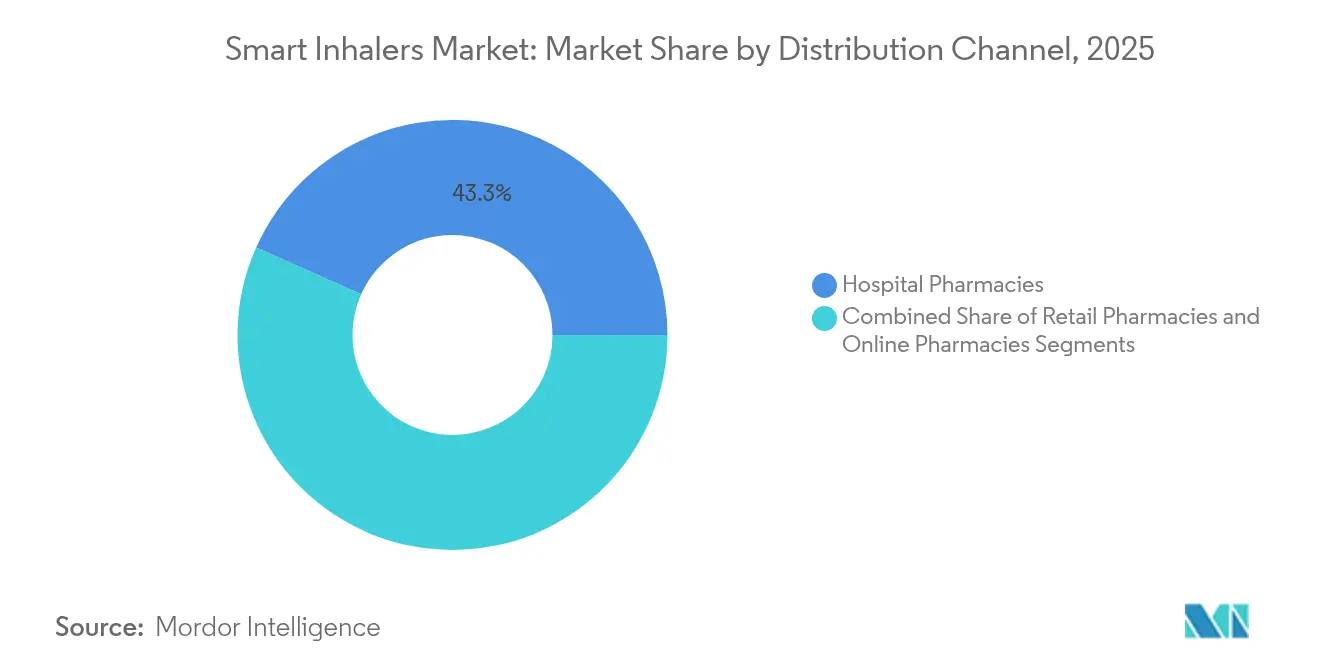

- By distribution channel, hospital pharmacies led with 43.33% share in 2025, whereas online pharmacies are set to post a 15.36% CAGR by 2031.

- By geography, North America commanded 41.02% of the smart inhalers market size in 2025, while Asia-Pacific will register the fastest 16.02% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Smart Inhalers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Prevalence of Respiratory Diseases | +3.2% | Global, with highest impact in Asia-Pacific and aging populations | Long term (≥ 4 years) |

| Technological Advances in Tele-Health and RPM | +2.8% | North America & EU leading, expanding to APAC | Medium term (2-4 years) |

| Improved Medication Adherence Analytics | +2.1% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Government Digital-Health Incentives | +1.9% | North America, EU, Japan leading policy frameworks | Short term (≤ 2 years) |

| Shift Toward Value-Based and Preventive Healthcare Models | +1.7% | North America & EU, expanding to emerging markets | Long term (≥ 4 years) |

| Expansion of Digital Health Ecosystem and Interoperability Standards | +1.4% | Global, with regulatory harmonization focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Prevalence of Respiratory Diseases

COPD now affects 454 million people, and asthma impacts 262 million, trends driven by ageing populations and urban air pollution. Real-world surveys in China show high adherence in only 40.9% of COPD patients, underscoring an unmet therapeutic need.[2]Source: Jie Zhang, “COPD Adherence in Northern China,” BioMed Central, eurjmedres.biomedcentral.com Smart inhalers give clinicians objective dose-timing data, making them essential rather than optional for long-term disease control. Elderly users benefit from audible and visual reminders that offset cognitive decline, ensuring correct technique. Consequently, payers increasingly recognise the devices as preventive tools that lower overall healthcare costs.

Technological Advances in Tele-Health and RPM

Partnerships such as AstraZeneca–ArtiQ fuse AI spirometry with inhaler telemetry, allowing lung-function assessments at home. IoT-enabled platforms like Pneulytics create continuous data streams that clinicians integrate with electronic health records for personalised care. The rollout of 5G networks adds bandwidth for real-time inhalation-flow analytics, while edge computing minimises latency. Together, these elements convert smart inhalers from isolated devices into nodes within a comprehensive chronic-care ecosystem.

Improved Medication Adherence Analytics

Meta-analyses record asthma-control improvements of three points and adherence gains from 30% to 68% when electronic-monitoring modules are added to inhalers. ProAir Digihaler data covering 53,083 events pinpointed 29% of patients with sustained SABA overuse—information invisible to conventional monitoring. Machine-learning algorithms now adjust spray-nozzle settings in real time, as demonstrated by Oklahoma State University’s AI prototype, delivering personalised doses. Such analytics shift respiratory care from reactive to predictive.

Government Digital-Health Incentives

Regulatory frameworks and reimbursement policies create favorable market conditions that accelerate smart inhaler adoption across healthcare systems. The FDA’s 2024 software-function guidance and Essential Drug-Delivery Outputs framework standardise approval pathways, trimming market-entry risks. Japan’s digital-health strategy is expanding connected-device reimbursement at a 7.29% CAGR, setting a regional benchmark. Meanwhile, Medicare’s 2026 rule extends coverage to digital therapeutics, unlocking a large insured population in the United States.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of Traditional Inhalers | -2.1% | Global, with stronger impact in cost-sensitive markets | Medium term (2-4 years) |

| High Upfront Cost of Smart Devices | -1.8% | Emerging markets and uninsured populations | Short term (≤ 2 years) |

| Data-Privacy and Cyber-Security Concerns | -1.3% | EU and privacy-conscious markets | Medium term (2-4 years) |

| Patchy Reimbursement for Digital Therapeutics | -1.1% | US and fragmented healthcare systems | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Availability of Traditional Inhalers

The entrenched market position of conventional inhalers creates switching resistance that slows smart inhaler adoption despite superior clinical outcomes. Low-priced generics enjoy deep physician familiarity and robust supply chains, slowing conversion to digital formats. FDA bioequivalence guidance continues to bring cheaper MDIs and DPIs to market, reinforcing incumbent share.[3]Source: U.S. Food and Drug Administration, “Budesonide; Formoterol; Glycopyrrolate Inhalation Aerosol,” fda.gov Provider inertia also matters: only 27% of patients change inhaler types at discharge despite documented technique errors. Limited digital infrastructure in some health systems further tilts preference toward conventional devices.

High Upfront Cost of Smart Devices

Sensor modules, wireless chips, and cloud-platform licences elevate price points beyond those of legacy inhalers. AstraZeneca’s voluntary USD 35 monthly cap on certain respiratory medicines illustrates industry pressure to ease affordability gaps. Budget-constrained hospitals often prioritise essential drugs over smart hardware, especially in emerging markets. The digital divide also restricts elderly and low-income patients who lack compatible smartphones or data plans. Healthcare systems operating under budget constraints prioritize essential medications over technology-enhanced delivery systems, limiting institutional adoption of smart inhalers despite long-term cost benefits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: MDIs Dominate Despite DPI Innovation Surge

Metered Dose Inhalers captured 64.22% of the smart inhalers market share in 2025, reflecting decades of clinical habit and wide formulary inclusion. However, Dry Powder Inhalers headline future growth with a 15.69% CAGR thanks to eco-friendly propellant-free designs and easier digital-sensor integration. The Smart inhalers market continues to pivot as payers link procurement criteria to carbon-reduction targets, a policy trend reinforced by AstraZeneca’s near-zero-GWP Breztri transition.

Dry-powder platforms also achieve superior adherence in real-world studies, posting a 0.67 mean proportion of days covered versus 0.62 for MDIs in Korea. Clinicians favour breath-actuated dosing because built-in flow sensors capture inspiratory profiles without propellant interference, allowing richer data analytics. As a result, DPIs are expected to lift their contribution to the Smart inhalers market size at double-digit rates throughout the decade.

By Indication: COPD Leadership Challenged by Asthma Innovation

COPD applications represented USD 1.51 billion of the Smart inhalers market size in 2025 and are expanding steadily on the back of high comorbidity rates. Nevertheless, asthma is advancing faster at 15.01% CAGR, propelled by pediatric uptake and regulator-endorsed single-maintenance-and-reliever-therapy (SMART) protocols. The 2024 FDA clearance of anti-inflammatory rescue therapy Airsupra underscores an innovation cycle favouring data-rich inhalers.

Asthma patients, often digital natives, engage readily with mobile-application dashboards that gamify adherence. COPD users derive value from AI-driven exacerbation prediction models that flag declining inhalation volume weeks before flare-ups. Together, the two indications will keep the Smart inhalers market on a high-growth trajectory through 2030.

By Distribution Channel: Hospital Dominance Faces Digital Disruption

Hospital pharmacies retained 43.33% of global revenue in 2025, benefiting from integrated electronic health-record (EHR) systems that import inhaler-generated data for multidisciplinary review. Value-based purchasing contracts encourage bulk procurement of connected devices for population-health programs, reinforcing institutional scale in the Smart inhalers market.

Online pharmacies, however, are forecast to grow at 15.36% CAGR as telemedicine normalises physician-patient engagement and electronic prescriptions. Direct-to-consumer fulfilment coupled with in-app coaching narrows the adherence gap without requiring in-person visits. Retail outlets sit between the two, adding self-service kiosks that upload inhaler metrics to cloud dashboards. Collectively, these shifts illustrate how omnichannel models will recalibrate competitive stakes across the Smart inhalers industry.

Geography Analysis

North America controlled 41.02% of revenue in 2025 owing to structured reimbursement frameworks and early digital-therapeutics uptake. The United States benefits from Medicare policies that now classify connected respiratory devices as durable medical equipment, encouraging widespread deployment. Canada’s single-payer system pilots population-wide adherence programs, while Mexico is rolling out digitised clinics that will extend device penetration beyond urban centres.

Asia-Pacific is the fastest-expanding territory, with a 16.02% CAGR projected to 2031. Japan leads on the back of ministry-backed digital-health incentives and an ageing population keen on at-home monitoring. China’s scale and state-backed telehealth rollouts create fertile ground for low-cost, cloud-synced inhalers. India’s urban middle class demands app-connected devices, and private insurers are beginning to reimburse smart solutions.

Europe advances through regulatory harmonisation under the European Health Data Space, which specifies FHIR-based interoperability rules. Germany, the United Kingdom, and France spearhead adoption via e-prescription mandates that embed device data into national EHRs. Southern European states follow as infrastructure gaps close. Collectively, regional policy frameworks ensure the Smart inhalers market maintains a balanced geographic revenue mix.

Competitive Landscape

The Smart inhalers market features moderate fragmentation. Legacy pharmaceutical companies such as AstraZeneca and GSK are pairing drug portfolios with proprietary sensor platforms to protect brand equity. Digital-health specialists like Propeller Health and Adherium license software-as-a-medical-device algorithms that overlay inhaler telemetry with weather and pollution indices for contextual alerts.

Strategic acquisitions are reshaping capabilities: Molex’s Phillips Medisize purchased Vectura Group to blend drug-formulation expertise with miniaturised electronics, a move designed to deliver turnkey connected devices. Meanwhile, component suppliers such as Aptar partner with Propeller to build interoperable platforms that span multiple therapeutic areas.

Start-ups target white-space niches: AI labs are refining inhalers that automatically tune spray-nozzle geometry based on each user’s breathing profile, promising precision dosing. As cybersecurity scrutiny rises, blockchain-validated data pathways are emerging to secure patient telemetry. Vendors that master both clinical efficacy and data stewardship are likely to consolidate share over the next five years.

Smart Inhalers Industry Leaders

Teva Pharmaceutical Industries Ltd.

AstraZeneca

GlaxoSmithKline plc.

Novartis AG

Boehringer Ingelheim International GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2024: Leicester launches NHS trial of smart inhalers for children, equipping 300 youngsters with app-connected devices for adherence feedback.

- April 2024: Adherium unveiled an FDA-cleared Smartinhaler compatible with Airsupra and Breztri, widening interoperability across leading brands.

- July 2023: Teva launched its GoResp Digihaler, a digitally enabled inhaler, in the United Kingdom. It is used by patients with asthma and COPD.

- June 2023: Phil Inc., a life science product commercialization and patient access platform company, announced a collaborative agreement with Teva Pharmaceuticals to launch a new program to improve accessibility for the Digihaler family of smart inhalers in support of asthma management.

Global Smart Inhalers Market Report Scope

As per the scope of the report, the smart inhalers market involves technologically advanced inhalation devices designed to monitor and enhance the treatment of respiratory conditions. These devices typically integrate sensors, connectivity features, and data analytics to provide real-time feedback, promote medication adherence, and enable personalized management of respiratory diseases such as asthma and COPD.

The smart inhalers market is segmented by product type, indication, distribution channel, and geography. By product type, the market is segmented into dry powder inhalers (DPI) and metered dosage inhalers (MDI)). By indication, the market is segmented into asthma, chronic obstructive pulmonary disorders (COPD), and others. By distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, and e-commerce. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report offers market sizes and forecasts in terms of value (USD) for the above segments.

| Metered Dose Inhalers (MDI) |

| Dry Powder Inhalers (DPI) |

| Asthma |

| Chronic Obstructive Pulmonary Disease (COPD) |

| Other Indications |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Metered Dose Inhalers (MDI) | |

| Dry Powder Inhalers (DPI) | ||

| By Indication | Asthma | |

| Chronic Obstructive Pulmonary Disease (COPD) | ||

| Other Indications | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the smart inhalers market?

The smart inhalers market size stands at USD 3.41 billion in 2026 and is projected to reach USD 6.75 billion by 2031.

Which product category is growing fastest?

Dry Powder Inhalers are the fastest-growing product type, forecast to post a 15.69% CAGR through 2031 as sustainability mandates gain traction.

Why is Asia-Pacific considered the growth hotspot?

Government digital-health incentives in Japan, expansive telehealth infrastructure in China, and rising urban affluence in India combine to drive a regional 16.02% CAGR.

How do smart inhalers improve patient outcomes?

Built-in sensors capture dose timing and inhalation flow, enabling AI algorithms to predict exacerbations and prompting timely interventions that curb emergency visits.

What are the main hurdles to wider adoption?

High device costs, data-privacy concerns, and the entrenched availability of low-priced traditional inhalers continue to moderate uptake despite clinical advantages.

Page last updated on: