Alzheimer's Therapeutics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 7.48 Billion |

| Market Size (2031) | USD 11.06 Billion |

| Growth Rate (2026 - 2031) | 8.12% CAGR |

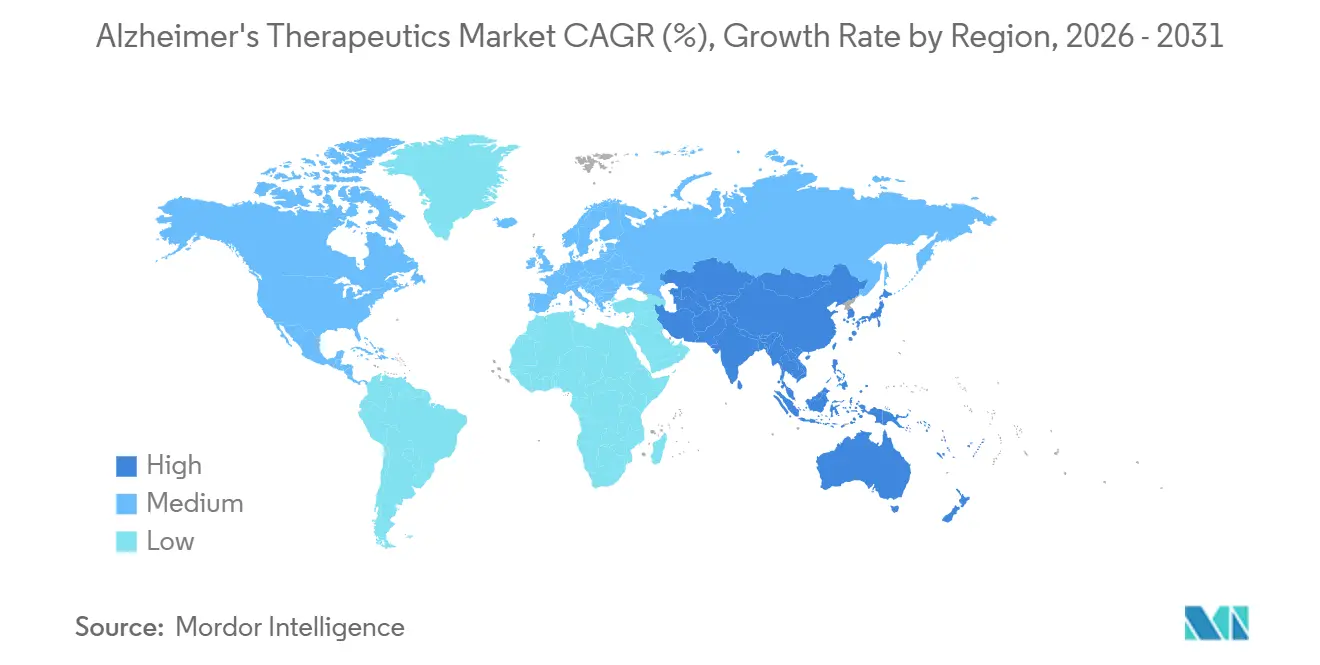

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Alzheimer's Therapeutics Market Analysis by Mordor Intelligence

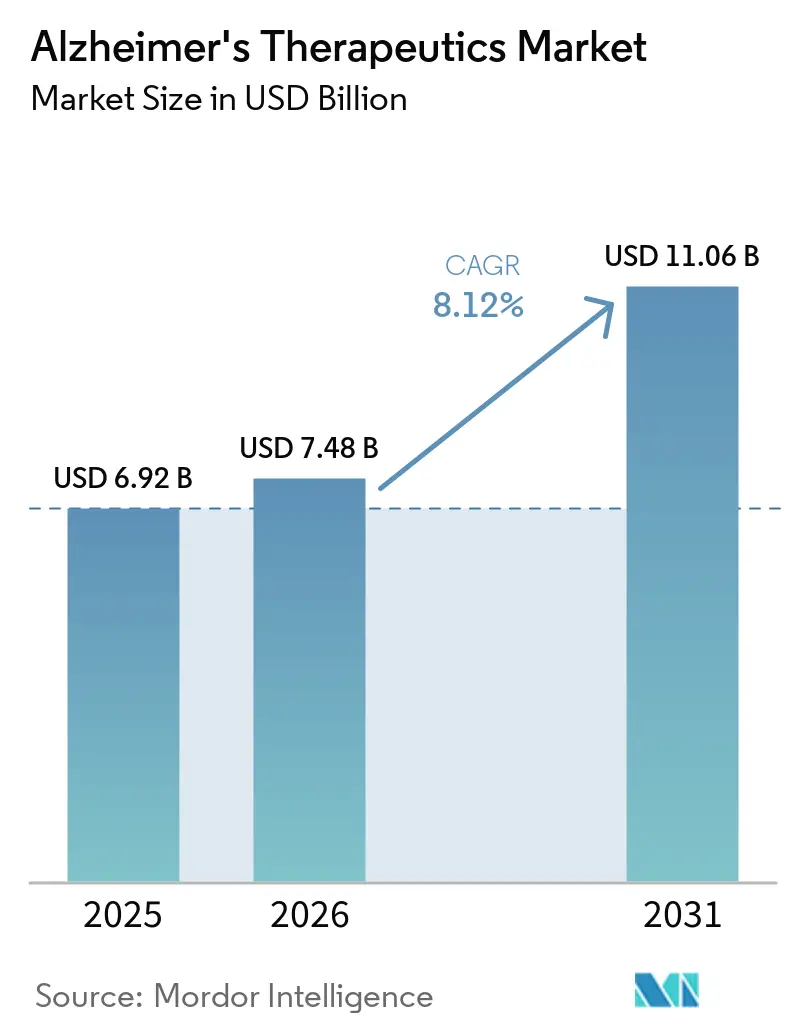

The Alzheimer's Therapeutics Market size is projected to expand from USD 6.92 billion in 2025 and USD 7.48 billion in 2026 to USD 11.06 billion by 2031, registering a CAGR of 8.12% between 2026 to 2031.

Demand is being sustained by aging populations in major healthcare systems, with 7.4 million Americans aged 65 and older living with Alzheimer's dementia in 2026, while global dementia cases stand at 55 million and are expected to nearly triple by 2050. The cost burden is also intensifying, as U.S. health and long-term care costs for Alzheimer's and related dementias are projected to reach USD 409 billion in 2026, which keeps payer attention fixed on treatments that can slow progression rather than only manage symptoms. The competitive base of the Alzheimer's therapeutics market is now centered on a small number of approved disease-modifying programs, but the presence of 158 novel agents across 192 active clinical trials keeps long-range competition open and strategically important. Blood-based biomarker guidance issued in 2025 is also reducing dependence on amyloid PET in specialized care settings, which can widen the diagnosed and treatment-eligible population without requiring the same pace of imaging expansion. As a result, the Alzheimer's therapeutics market is increasingly shaped by how quickly health systems can convert diagnostic capacity into treatment starts, especially in regions where demand is rising faster than infusion and monitoring infrastructure.

Key Report Takeaways

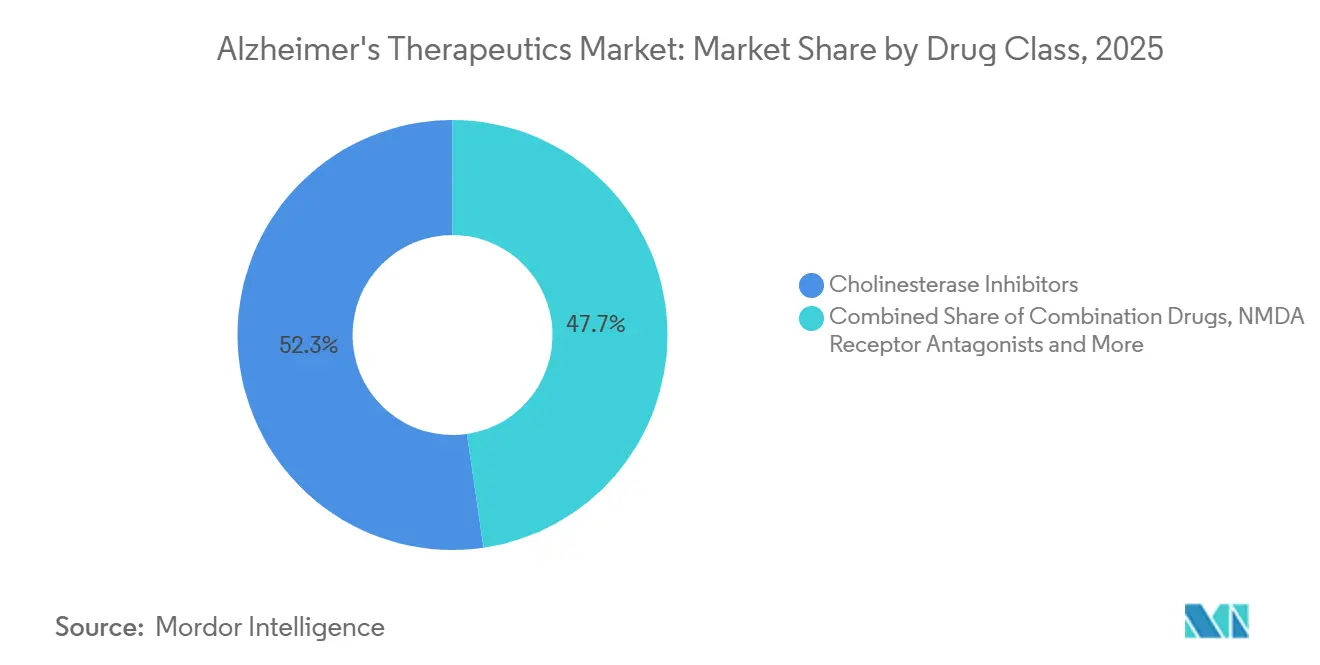

- By drug class, cholinesterase inhibitors held 52.31% share in 2025, while combination drugs are projected to expand at a 10.38% CAGR through 2031.

- By type of treatment, symptomatic treatments accounted for 62.24% share in 2025, while disease-modifying therapies are expected to record the highest CAGR at 10.52% through 2031.

- By route of administration, oral therapies held 68.52% share in 2025, while injectables are forecast to grow at a 9.25% CAGR through 2031.

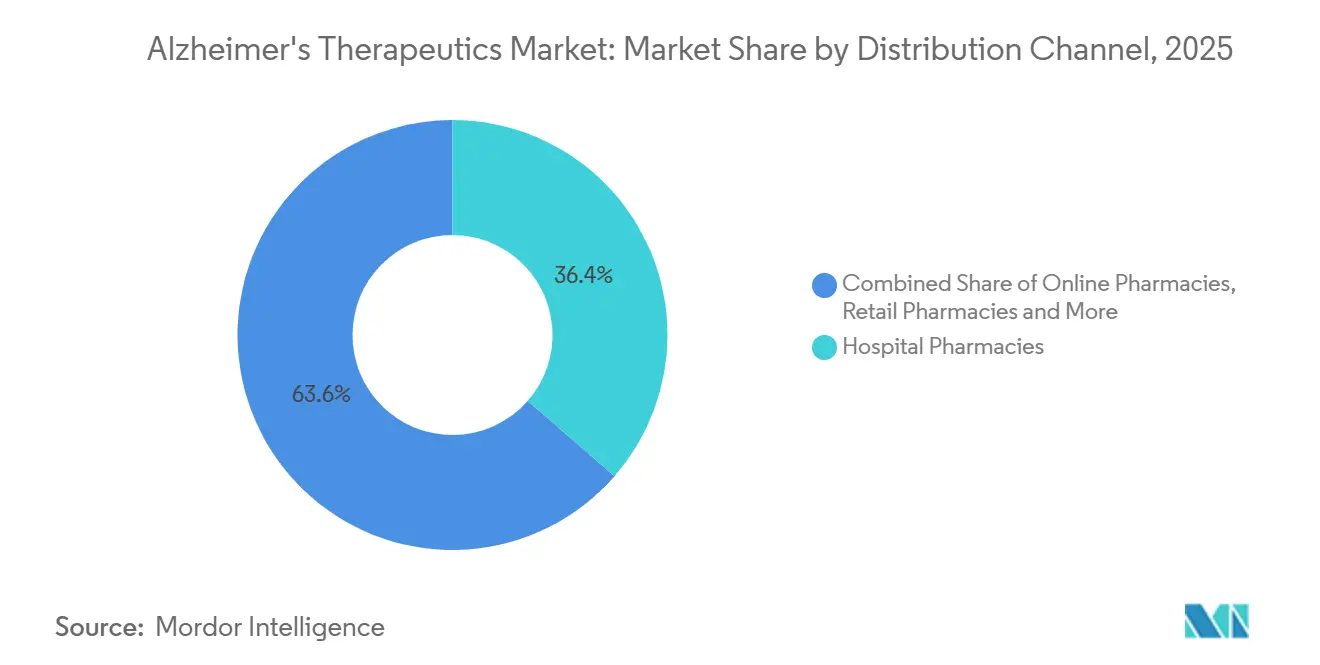

- By distribution channel, hospital pharmacies held 36.42% share in 2025, while online pharmacies are projected to expand at an 11.25% CAGR through 2031.

- By patient stage, mild dementia accounted for 46.24% share in 2025, while mild cognitive impairment is projected to advance at a 10.15% CAGR through 2031.

- By end user, hospitals held 41.82% share in 2025, while home care settings are forecast to grow at an 11.25% CAGR through 2031.

- By geography, North America held 40.24% share in 2025, while Asia-Pacific is projected to grow at an 11.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Alzheimer's Therapeutics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Alzheimer's Prevalence And Aging Population | +2.5% | Global, concentrated in North America, Europe, and East Asia | Long term (≥ 4 years) |

| Disease-Modifying Therapy Adoption Expands Treatable Patient Pool | +1.8% | North America and EU with early spillover to Japan and China | Medium term (2-4 years) |

| Biomarker-Led Patient Identification Improves Therapy Eligibility | +1.2% | North America, Europe, and emerging APAC | Medium term (2-4 years) |

| Hospital-Based Infusion And Monitoring Infrastructure Supports Premium Therapies | +0.8% | North America, with early gains in Japan and South Korea | Short term (≤ 2 years) |

| Payer And Registry Pathways Normalize Real-World Evidence Based Access | +0.6% | North America primarily, EU developing | Medium term (2-4 years) |

| Repurposed Metabolic And Neuroprotective Assets Broaden The Pipeline | +0.4% | Global, with R&D concentrated in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Alzheimer's Prevalence and Aging Population

Alzheimer's disease accounts for 60-80% of all dementia cases, and the burden is rising as populations age across both mature and emerging healthcare systems. A 2025 global burden analysis projected that Alzheimer's disease and other dementias could affect 191 million people by 2050, with especially strong growth across East Asia, South Asia, and sub-Saharan Africa. In the United States, all baby boomers will be aged 65 or older by 2030, which places the largest insured patient pool at a point of rising incidence while newer treatments are scaling. At the same time, more than 60% of current dementia cases are already located in lower- and middle-income countries, where diagnostic access and reimbursement remain much weaker[1]Alzheimer's Disease International, “Dementia Statistics,” Alzheimer's Disease International, alzint.org. This means the disease burden ceiling is much higher than the revenue ceiling in the Alzheimer's therapeutics market. It also means companies that build lower-cost oral pathways or simpler blood-test-led access models can reach demand that IV-focused treatment models cannot serve efficiently.

Disease-Modifying Therapy Adoption Expands Treatable Patient Pool

Traditional regulatory progress for anti-amyloid therapies has created the first commercially viable disease-modification category in the Alzheimer's therapeutics market, after years of clinical disappointment. By early 2025, 80% of surveyed neurologists reported discussing anti-amyloid therapies with patients, and the average number of patients per prescribing neurologist had increased nearly 5-fold from the prior year. That shift shows that specialist adoption moved from caution to active clinical planning. It also creates a more familiar treatment pathway for future agents that will not need to start from a cold market. The Alzheimer care model is therefore moving toward earlier intervention, which expands the commercial value of diagnosed patients. In practical terms, the Alzheimer's therapeutics market can now grow through both new product entry and deeper physician willingness to treat eligible patients.

Biomarker-Led Patient Identification Improves Therapy Eligibility

One of the clearest structural shifts in the Alzheimer's therapeutics market is the move away from heavy reliance on amyloid PET and cerebrospinal fluid confirmation. The 2025 clinical practice guideline from the Alzheimer's Association endorsed blood-based biomarkers with at least 90% sensitivity and specificity as substitutes for amyloid PET in specialized care settings. That guidance gives health systems a practical standard for designing lower-friction diagnostic pathways. It also supports earlier screening of patients who might otherwise wait for memory clinic access or imaging slots. A simpler screening flow can raise treatment starts faster than prevalence growth alone would suggest. For the Alzheimer's therapeutics market, this means diagnostic efficiency is becoming a direct commercial lever rather than only a clinical support step.

Hospital-Based Infusion and Monitoring Infrastructure Supports Premium Therapies

Premium biologic uptake still depends heavily on the physical care network that surrounds each therapy in the Alzheimer's therapeutics market. Mass General Brigham launched a unified Alzheimer Therapeutics Program across multiple infusion sites and standardized MRI monitoring across all network imaging centers, which shows how large systems are formalizing repeatable delivery models. As more centers establish amyloid testing, infusion capacity, and MRI follow-up, the operational barriers to prescribing begin to fall within those local systems. Early embedded therapies also gain a practical advantage because clinicians and administrators tend to stay with the workflow they already built. This strengthens hospital-based prescribing patterns even before broader home-based dosing becomes common. Since hospital pharmacies held 36.42% of distribution in 2025, these institutional nodes remain central revenue gateways in the Alzheimer's therapeutics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Treatment And Monitoring Cost Limits Broad Access | -1.5% | Global, most acute in Europe, South America, and MEA | Long term (≥ 4 years) |

| Safety Monitoring Burden And Adverse Event Risk Restrict Uptake | -0.9% | Global, disproportionate in rural North America and APAC | Medium term (2-4 years) |

| Clinical Trial Failure And Attrition Increase Capital Risk | -0.6% | Global, concentrated in R&D-intensive North America and Europe | Long term (≥ 4 years) |

| Narrow Specialist Capacity Slows Diagnosis To Treatment Conversion | -0.7% | Rural North America, Europe, South America, and MEA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Treatment and Monitoring Cost Limits Broad Access

The access problem in the Alzheimer's therapeutics market extends beyond drug price into the full cost of diagnosis, monitoring, and delivery. NICE rejected both leading anti-amyloid drugs for routine NHS use, and a separate capacity analysis estimated that GBP 14 billion (USD 18.8 billion) would be needed over 10 years to bring England to G7-average diagnostic readiness for treatment eligibility assessment. In the United States, CMS continues to tie Medicare reimbursement for anti-amyloid monoclonal antibodies to registry participation under its Coverage with Evidence Development framework[2]Centers for Medicare & Medicaid Services, “Monoclonal Antibodies Directed Against Amyloid for the Treatment of Alzheimer's Disease,” CMS, cms.gov. That requirement adds process and staffing burdens for providers that do not already operate high-resource dementia programs. The result is uneven access, where insured patients close to specialist centers can move much faster than the wider age-eligible population. Even with online pharmacies growing at 11.25% CAGR, that channel cannot remove the high-touch infrastructure burden attached to parenteral DMT care in the Alzheimer's therapeutics market.

Safety Monitoring Burden and Adverse Event Risk Restrict Uptake

Safety oversight remains a major brake on adoption in the Alzheimer's therapeutics market, especially for anti-amyloid antibodies that require ongoing imaging review. Clinical guidance for anti-amyloid use calls for brain MRI before treatment and at defined points before later infusions, with added scans when abnormalities are detected. This monitoring protocol narrows prescribing to sites with dependable MRI access and staff familiar with amyloid-related imaging abnormality management. Rural and underserved patients therefore face longer waits between diagnosis, treatment discussion, and therapy initiation. The same burden also raises delivery cost for hospitals and public payers that must fund repeated imaging and specialist oversight. The injectable segment can keep expanding in the Alzheimer's therapeutics market, but this safety workload will continue to limit how quickly uptake can spread beyond established centers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Established Base Anchors Revenue, Combination Therapies Accelerate

Cholinesterase inhibitors held 52.31% of the Alzheimer's therapeutics market share in 2025, reflecting long prescribing history, generic availability, and broad affordability. NMDA receptor antagonists represented the second-largest position because they remain a standard option in moderate and severe disease management. Amyloid immunotherapies still formed a smaller revenue base, but they have started to influence treatment mix more directly than before. Combination drugs are projected to grow at a 10.38% CAGR from 2026 to 2031, which is the fastest pace within this segmentation. The Alzheimer's therapeutics market still relies on mature symptomatic classes for revenue stability even as newer categories gain traction.

The 2026 development pipeline contained 20 active combination therapy trials, equal to 11% of all active trials, which shows how strongly developers are leaning into multi-mechanism strategies. Eisai's study of E2814 with concurrent lecanemab is the clearest example of this approach now in motion. Repurposed assets accounted for 35% of all pipeline agents in 2026, which widened the field beyond traditional neurology pharmacology. That breadth supports a larger search for value across tau, neuroinflammation, metabolism, and related pathways. Other classes contribute useful depth, but near-term revenue in the Alzheimer's therapeutics market remains concentrated in established symptomatic products and early commercial DMT adoption.

By Type of Treatment: Symptomatic Treatments Dominate, Disease Modification Accelerates

Symptomatic treatments held 62.24% of the market in 2025, while disease-modifying therapies are projected to expand at a 10.52% CAGR through 2031. This split shows that the Alzheimer's therapeutics market still depends on long-established prescriptions for current revenue generation. Cholinesterase inhibitors and NMDA antagonists retain wide reach in systems where DMT reimbursement is not yet mature. Disease-modifying therapies are rising faster because they shift care toward earlier intervention rather than symptom control alone. The Alzheimer's therapeutics market size for disease-modifying therapies is therefore set to expand faster than the overall sector as care pathways become more standardized.

Clinical adoption accelerated sharply in 2025 as neurologists became more willing to discuss anti-amyloid treatment with patients. That change matters because DMT eligibility is tied to early pathology and functional stage rather than late-stage symptom burden. Earlier identification can extend treatment duration and increase the value of each treated patient over time. Symptomatic therapies are therefore shifting into a complementary role instead of remaining the only realistic option in many treatment journeys. If maintenance dosing keeps moving closer to the home, the Alzheimer's therapeutics market should face fewer care setting barriers in disease modification.

By Route of Administration: Oral Accessibility Leads, Injectables Rise with DMT Scaling

The oral route held 68.52% of the market in 2025, while injectables are projected to advance at a 9.25% CAGR through 2031. Oral products lead because they fit routine community prescribing and require no specialized delivery environment. Injectable growth is being driven by anti-amyloid antibodies whose targets currently rely on systemic administration. Transdermal products maintain a modest but relevant place for patients who struggle with swallowing or gastrointestinal tolerance. The Alzheimer's therapeutics market still leans toward convenience in installed use, but growth is moving toward more complex delivery formats.

The shift toward subcutaneous maintenance dosing can reduce dependence on repeated infusion visits. That transition can improve adherence while also releasing capacity at hospital infusion centers. It may also support wider participation from home-delivery and specialty pharmacy services as the treatment model matures. Pipeline oral DMT candidates could later rebalance route economics if they show strong clinical proof. Until then, the Alzheimer's therapeutics market size linked to injectable therapies should continue rising as disease-modifying products scale.

By Distribution Channel: Hospital Networks Lead While Digital Dispensing Expands

Hospital pharmacies held 36.42% of the market in 2025, while online pharmacies are projected to grow at an 11.25% CAGR through 2031. Hospital leadership reflects the central role of infusion protocols, monitoring, and specialist supervision in DMT delivery. Retail pharmacies remained the second-largest channel because they serve the broad base of symptomatic oral therapy users. Online pharmacies are gaining through mail-order convenience and stable refill behavior in long-term oral treatment. The Alzheimer's therapeutics market is therefore operating through two channel models with very different complexity and margin structures.

One channel model is built around hospital and specialty outpatient care for biologics that require monitoring and controlled administration. The second model centers on high-volume oral dispensing through retail and digital platforms. As premium therapies expand, hospital pharmacy importance is unlikely to weaken quickly even if online growth remains faster. Specialty home-delivery services may gradually bridge the gap for maintenance-phase injectable care. That split keeps channel design, reimbursement support, and patient logistics central to planning in the Alzheimer's therapeutics market.

By Patient Stage: Mild Dementia Leads Revenue While Mild Cognitive Impairment Gains Speed

Mild dementia held 46.24% of the market in 2025, while mild cognitive impairment is projected to grow at a 10.15% CAGR through 2031. Mild dementia leads because it combines the broadest currently treated population with stronger day-to-day treatment adherence than later stages. Mild cognitive impairment is expanding faster because approved anti-amyloid therapies focus on patients earlier in the disease course. Moderate and severe stages still represent large patient numbers, but they generate less DMT revenue under current treatment boundaries. The Alzheimer's therapeutics market is increasingly shaped by how quickly systems can identify patients before they move beyond the approved treatment window.

The 2025 Alzheimer's Disease Facts and Figures report noted that 34% to 59% of Americans aged 65 and older live in areas with potential dementia specialist shortfalls. That shortfall directly slows conversion from early symptoms to confirmed treatment eligibility. Every patient diagnosed at mild cognitive impairment rather than moderate dementia becomes a longer-duration candidate for therapy. Blood-based screening and telehealth-enabled diagnostic pathways therefore matter as much as new product launches for this stage mix. In the Alzheimer's therapeutics industry, earlier stage capture will keep deciding where high-value growth lands.

By End User: Hospitals Anchor Initiation, Home Care Gains Importance

Hospitals held 41.82% of the market in 2025, while home care settings are projected to grow at an 11.25% CAGR through 2031. Hospitals lead because they anchor infusion therapy, biomarker workups, and MRI-based safety monitoring. Memory clinics are also becoming more important where multidisciplinary assessment is needed to confirm DMT candidacy. Home care is growing faster because maintenance dosing is moving closer to the patient and caregiver. The Alzheimer's therapeutics market still begins in hospitals even when later care shifts outward.

Home-based administration can lower delivery cost and reduce the burden of repeated facility visits for patients and caregivers. That makes it more attractive to payers that are evaluating total care cost rather than only unit drug price. Long-term care facilities and assisted living settings continue to support stable symptomatic medication use. Research centers remain relevant through trial enrollment and early access pathways. As site-of-care options widen, the Alzheimer's therapeutics market will redistribute end-user revenue, but hospitals should remain the main entry point for DMT initiation.

Geography Analysis

North America held 40.24% of the Alzheimer's therapeutics market share in 2025, making it the largest regional revenue base. The United States drove this position with 7.4 million people aged 65 and older living with Alzheimer's dementia in 2026, while national health and long-term care costs are projected at USD 409 billion[3]Alzheimer's Association, “Alzheimer's Facts and Figures Report 2026,” Alzheimer's Association, alz.org. The region also benefits from broader insurance depth and a defined Medicare pathway for anti-amyloid antibodies under Coverage with Evidence Development. Canada and Mexico remain smaller opportunities because specialist access and reimbursement breadth are more limited. Europe presents a more divided picture because lecanemab secured European Commission approval in 2025 while donanemab faced a less favorable benefit-risk outcome in Europe.

Asia-Pacific is projected to grow at an 11.15% CAGR from 2026 to 2031, which makes it the fastest regional growth zone in the Alzheimer's therapeutics market. Japan and China are positioned at the front of this expansion because they already have clearer paths for early DMT commercialization. The region also benefits from the growing role of blood-based diagnostics, which can reduce dependence on scarce PET infrastructure. South Korea, India, and Australia remain earlier in adoption, yet each has room to expand through better specialist access and earlier patient identification. The Alzheimer's therapeutics market in Asia-Pacific can scale quickly once diagnosis, monitoring, and reimbursement begin to move in the same direction.

South America and the Middle East and Africa remain smaller revenue contributors in the Alzheimer's therapeutics market, and symptomatic oral treatments still account for most demand. Brazil and Argentina lead South American activity, while the GCC countries offer the strongest near-term potential within MEA because healthcare spending and specialist capacity are relatively stronger. More than 60% of global dementia cases already occur in lower- and middle-income countries, yet most DMT revenue still accrues in high-income healthcare systems. Affordable oral drugs, broader awareness programs, and simpler diagnostic pathways will therefore determine how much of the Alzheimer's therapeutics market can open in these regions through 2031.

Competitive Landscape

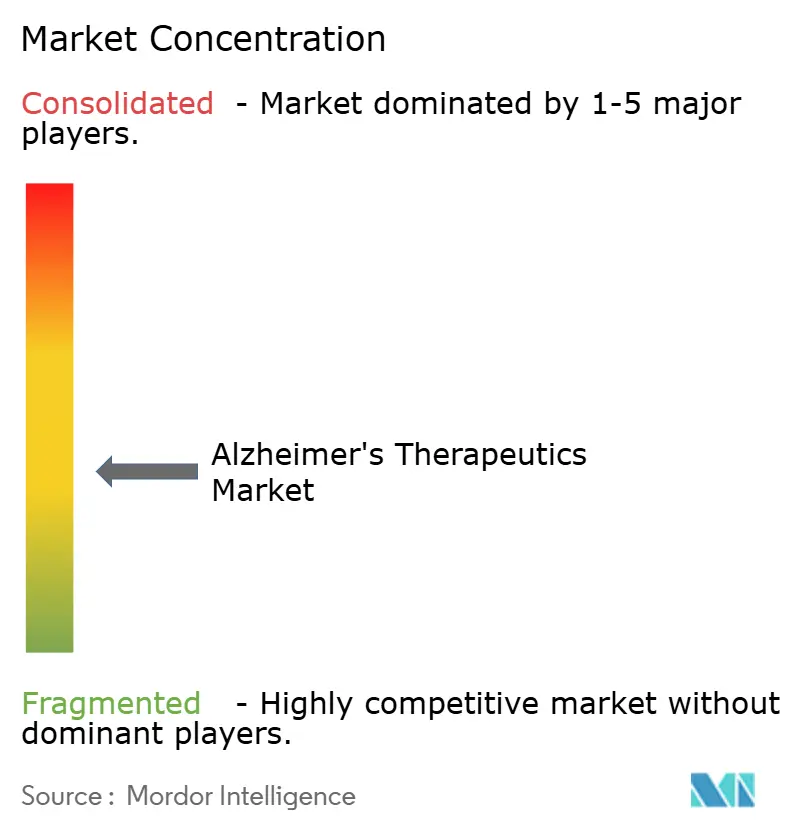

The Alzheimer's therapeutics market is moderately concentrated at the DMT level, but it remains fragmented across symptomatic drugs and the broader development pipeline. The 2026 pipeline included 158 novel agents across 192 active clinical trials, which kept long-range competition broad despite leadership by a small number of approved programs. A 2026 analysis of pharmaceutical innovation patterns found that currently approved Alzheimer therapies came from large firms, while smaller firms were more active in early-stage innovation. This structure gives larger players an advantage in late-stage validation, manufacturing scale, and commercial rollout. It also leaves meaningful white space for smaller developers that can prove value in novel mechanisms or more practical delivery models.

Competitive strategy is moving beyond amyloid-only exposure in the Alzheimer's therapeutics market. Tau programs, neuroinflammation targets, and delivery technologies that improve brain access are drawing more strategic attention. Eisai's ongoing study of E2814 with concurrent lecanemab is the clearest combination example now in active development. Sanofi also strengthened its position by announcing the acquisition of Vigil Neuroscience in 2025 to add an investigational medicine for Alzheimer's disease. These moves show that leading companies want broader exposure to the next treatment cycle instead of relying on one mechanism alone.

Commercial white space remains strongest in oral disease modification, earlier diagnosis, and simpler risk management inside the Alzheimer's therapeutics market. A therapy that can show disease modification without infusion and intensive MRI follow-up would gain a clear access advantage. Late-stage failure risk remains high, which is why portfolio diversity still matters even for well-resourced companies. The Alzheimer's therapeutics market is likely to reward companies that align clinical proof, workable care delivery, and payer acceptance at the same time.

Alzheimer's Therapeutics Industry Leaders

AbbVie Inc.

Biogen Inc.

Eisai Co., Ltd.

Eli Lilly and Company

F. Hoffmann-La Roche Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Fosun Pharma signed an exclusive global option agreement with South Korea's AriBio for oral Alzheimer's candidate AR1001, paying a USD 60 million option fee with potential milestone value exceeding USD 4.7 billion; the agreement, the largest Alzheimer's licensing deal in South Korean biotech history, reflects accelerating Chinese pharma investment in the global Alzheimer's drug pipeline.

- February 2026: China's NMPA designated the subcutaneous autoinjector formulation of lecanemab (LEQEMBI) for Priority Review, with potential approval enabling once-weekly at-home dosing, a shift that could substantially expand the accessible patient population in a market of an estimated 17 million eligible patients.

Global Alzheimer's Therapeutics Market Report Scope

As per the scope of the report, Alzheimer's therapeutics refer to the treatments and interventions developed to prevent, slow, or manage the symptoms of Alzheimer's disease. The Alzheimer's therapeutics market is segmented by drug class, type of treatment, route of administration, distribution channel, patient stage, end user, and geography. By drug class, the market includes cholinesterase inhibitors, NMDA receptor antagonists, amyloid immunotherapies, combination therapies, and other drug classes. By type of treatment, it is divided into symptomatic treatment and disease-modifying therapies. Based on the route of administration, the segmentation includes oral, injectable, and transdermal options. The distribution channel segmentation comprises hospital pharmacies, retail pharmacies, online pharmacies, and other channels. By patient stage, the market is categorized into mild cognitive impairment, mild dementia, moderate dementia, and severe dementia. The end-user segmentation includes hospitals, memory clinics, home care settings, and other users.

Geographically, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Cholinesterase Inhibitors |

| NMDA Receptor Antagonists |

| Amyloid Immunotherapies |

| Combination Therapies |

| Other Drug Classes |

| Symptomatic Treatment |

| Disease Modifying Therapies |

| Oral |

| Injectable |

| Transdermal |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| Other Distribution Channels |

| Mild Cognitive Impairment |

| Mild Dementia |

| Moderate Dementia |

| Severe Dementia |

| Hospitals |

| Memory Clinics |

| Home Care Settings |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | Cholinesterase Inhibitors | |

| NMDA Receptor Antagonists | ||

| Amyloid Immunotherapies | ||

| Combination Therapies | ||

| Other Drug Classes | ||

| By Type of Treatment | Symptomatic Treatment | |

| Disease Modifying Therapies | ||

| By Route of Administration | Oral | |

| Injectable | ||

| Transdermal | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| Other Distribution Channels | ||

| By Patient Stage | Mild Cognitive Impairment | |

| Mild Dementia | ||

| Moderate Dementia | ||

| Severe Dementia | ||

| By End User | Hospitals | |

| Memory Clinics | ||

| Home Care Settings | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of Alzheimer's therapeutics by 2031?

The Alzheimer's therapeutics market is forecast to reach USD 11.06 billion by 2031 from USD 7.48 billion in 2026, growing at an 8.12% CAGR.

Which treatment category is growing the fastest in Alzheimer care?

Disease-modifying therapies are the fastest-growing treatment type, with a projected 10.52% CAGR through 2031.

Which drug class currently generates the most revenue?

Cholinesterase inhibitors led all drug classes with 52.31% share in 2025 because of long prescribing history, generic availability, and low treatment cost.

Why is mild cognitive impairment becoming more commercially important?

Mild cognitive impairment is projected to grow at a 10.15% CAGR through 2031 because approved anti-amyloid therapies focus on patients earlier in the disease course.

Which region is expanding the fastest through 2031?

Asia-Pacific is the fastest-growing regional cluster, with an 11.15% CAGR through 2031, helped by earlier diagnosis efforts and expanding DMT access pathways.

What is the biggest barrier to wider use of anti-amyloid therapies?

Cost and monitoring remain the biggest barriers, because treatment access depends on diagnostics, MRI follow-up, specialist capacity, and payer approval, not only the drug itself.

Page last updated on: