Neurodegenerative Disease Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

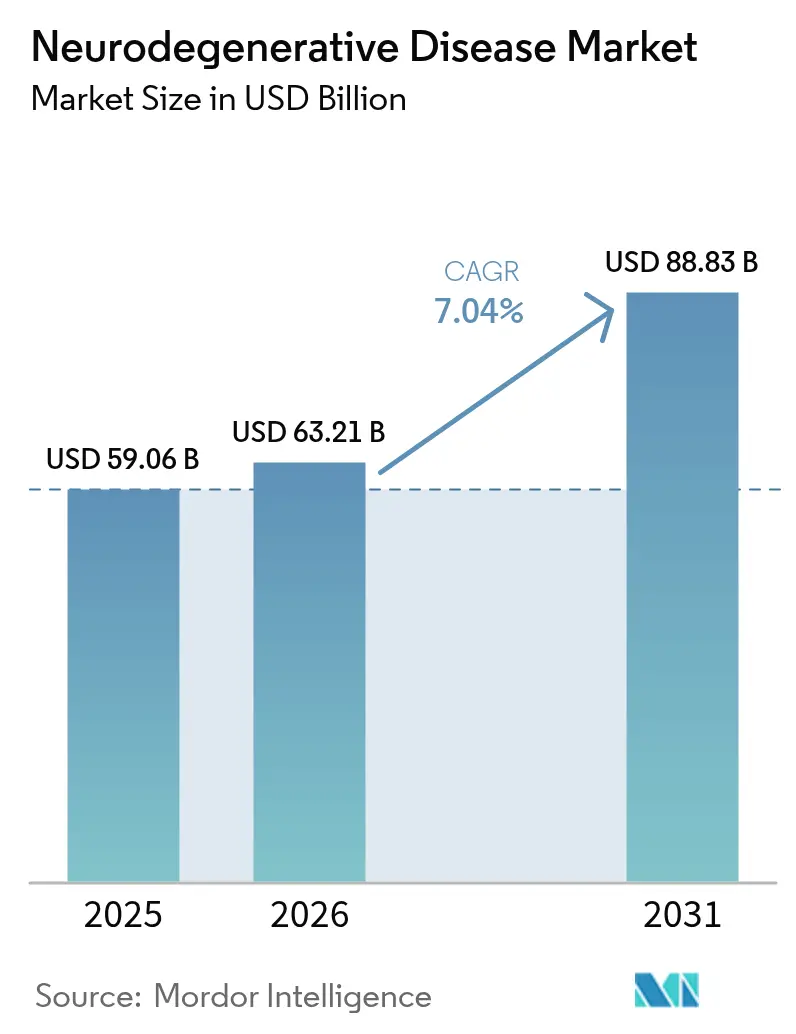

| Market Size (2026) | USD 63.21 Billion |

| Market Size (2031) | USD 88.83 Billion |

| Growth Rate (2026 - 2031) | 7.04% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Neurodegenerative Disease Market Analysis by Mordor Intelligence

The Neurodegenerative Disease Market size is expected to grow from USD 59.06 billion in 2025 to USD 63.21 billion in 2026 and is forecast to reach USD 88.83 billion by 2031 at 7.04% CAGR over 2026-2031.

Robust demand is fuelled by an aging global population, fresh approvals for disease-modifying biologics, and sharper diagnostic tools that enable earlier intervention. Competitive pressure intensifies as incumbents defend blockbuster franchises while biotechnology newcomers push gene and RNA therapies toward late-stage trials. Payer appetite for premium pricing remains intact in the United States, yet parallel generic erosion in symptomatic drugs reshapes revenue mixes. Taken together, these forces put the neurodegenerative disease market on a durable growth path that balances near-term stability with long-term innovation. At the same time, Asia-Pacific governments are mandating nationwide dementia screening, spurring double-digit test volumes that lift reagent demand. Competitive intensity is escalating as AI-enabled discovery platforms compress target-identification timelines and draw venture capital toward niche, genetically defined indications.

Key Report Takeaways

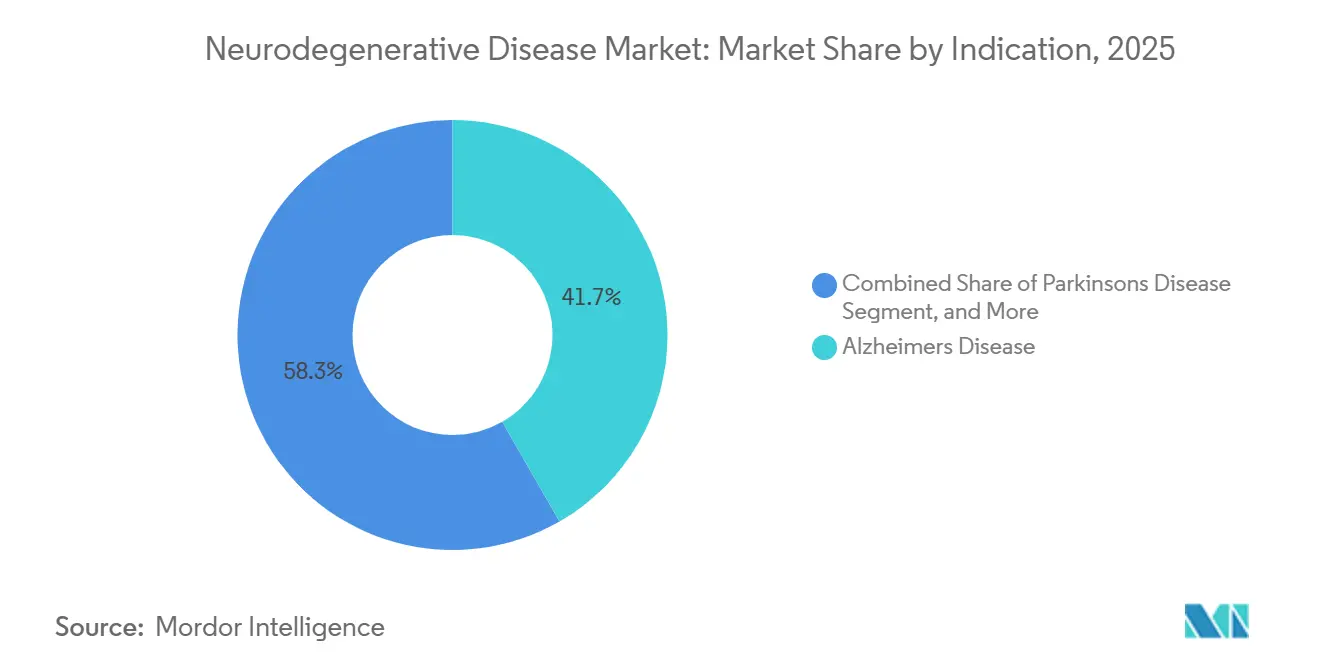

- By indication, Alzheimer’s disease held 41.72% of the Neurodegenerative disease market share in 2025, while amyotrophic lateral sclerosis is projected to record a 9.36% CAGR through 2031.

- By drug class, cholinesterase inhibitors accounted for 27.98% share of the Neurodegenerative disease market size in 2025; gene and cell therapies are poised to grow at a 9.21% CAGR between 2026 and 2031.

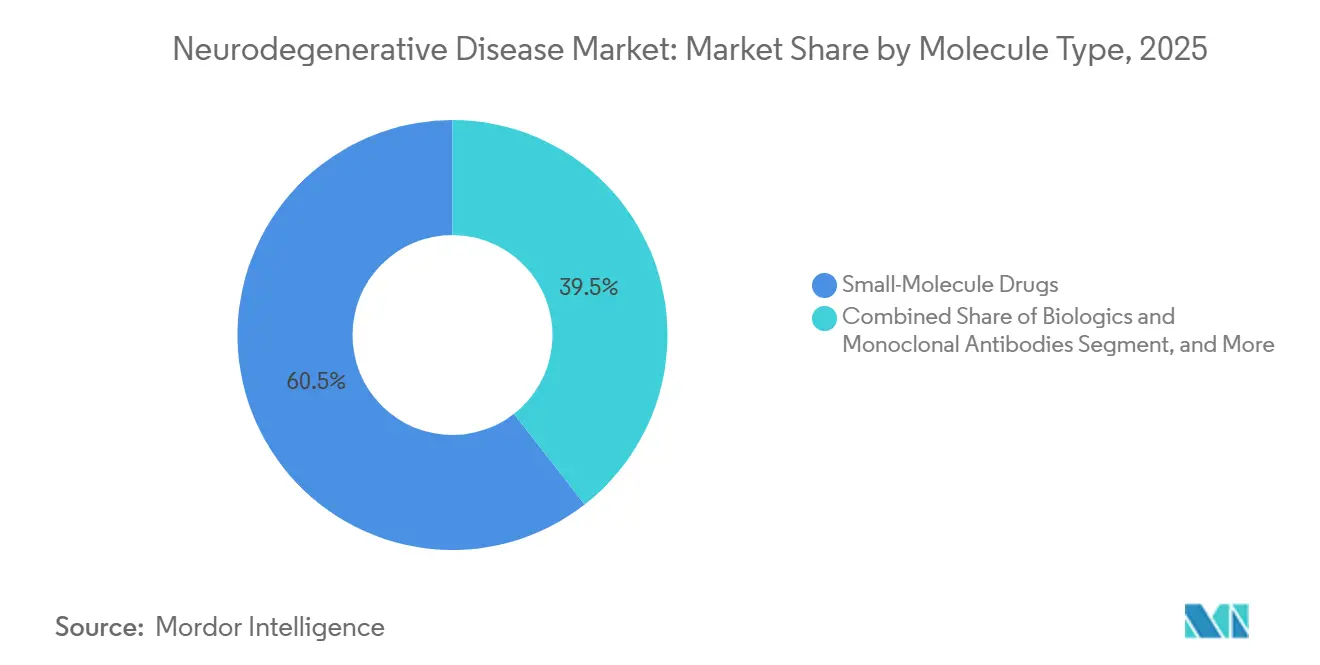

- By molecule type, small-molecule drugs commanded 60.55% share in 2025, whereas RNA-based therapeutics show the fastest 9.14% CAGR outlook to 2031.

- By route of administration, oral formulations dominated with 76.88% share in 2025, and transdermal or intranasal delivery is forecast to expand at a 9.88% CAGR over the same period.

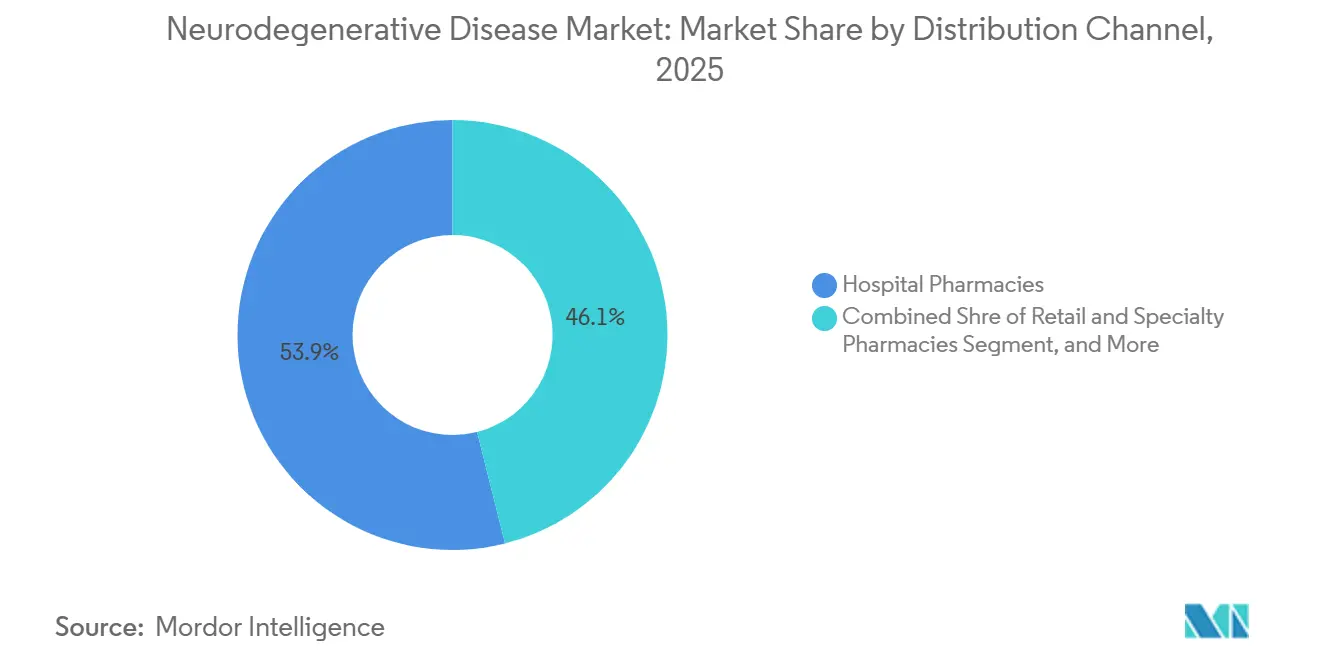

- By distribution channel, hospital pharmacies led with 53.92% share in 2025; online pharmacies are expected to advance at a 10.08% CAGR to 2031.

- By geography, North America generated 41.96% of revenue in 2025, while Asia-Pacific is on track for an 8.31% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Neurodegenerative Disease Market Trends and Insights

Driver Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Aging population escalating disease burden | +1.2% | Global, peak intensity in Japan, South Korea, Germany, Italy | Long term (≥ 4 years) |

| Launch and reimbursement of disease-modifying therapies | +1.5% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Advancements in neuro-imaging and blood-based biomarkers | +0.9% | North America and Europe, urban China and India | Medium term (2-4 years) |

| Expanding neuroscience R&D investments | +1.1% | United States, United Kingdom, Switzerland, China | Long term (≥ 4 years) |

| AI-enabled de-novo target discovery | +0.8% | North America and Europe, hubs in Singapore and Israel | Short term (≤ 2 years) |

| Brain-targeted delivery platforms | +0.7% | North America and Europe, trial sites in Australia and Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging Population Escalating Disease Burden

People aged 65 and older will comprise 16.5% of the world’s population by 2030, with Japan already at 29.1% in 2024.[1]U.S. Food & Drug Administration, “Biomarker Qualification for Neurodegenerative Diseases,” fda.gov National health-care systems are responding with community screening mandates; Japan began compulsory annual cognitive checks for citizens over 75 in April 2025, channeling roughly 1.2 million residents into diagnostic pathways that rely on plasma p-tau assays before costly PET imaging.[2]National Institutes of Health, “ClinicalTrials.gov Trends in Neurodegenerative Trials,” clinicaltrials.gov South Korea enacted a parallel program in January 2026, while German insurers started reimbursing plasma p-tau217 in November 2025. Rising prevalence drives payer willingness to fund early intervention, a strategy supported by Alzheimer’s Disease International, which reported dementia-related costs exceeding USD 1.3 trillion in high-income countries during 2024.

Launch and Reimbursement of Disease-Modifying Therapies

The 2024 approvals of donanemab and subcutaneous lecanemab shifted commercial narratives from symptom relief to disease alteration. Their launch proved payers will reimburse high-cost biologics when evidence shows amyloid plaque clearance and cognitive stabilization. More than 15 additional anti-amyloid or anti-tau antibodies now populate Phase III pipelines, signaling a therapeutic arms race. Biogen, Roche, and Johnson & Johnson deploy adaptive trial designs and fluid biomarker surrogate endpoints to shorten development timelines. Investor confidence surges, with neuroscience IPO proceeds rising despite macro uncertainty. Over the medium term, combination regimens pairing antibodies with small-molecule anti-inflammatories are expected to widen clinical benefit windows, further enlarging revenue opportunities across the neurodegenerative disease market.

Full FDA approvals for Eisai’s lecanemab in July 2024 and Eli Lilly’s donanemab in October 2024 validated the anti-amyloid class after showing 27% and 35% cognitive-decline slowing, respectively. Japan’s PMDA approved lecanemab in September 2024 and set annual reimbursement at JPY 2.98 million (USD 20,100) three months later.

Advancements In Neuroimaging and Biomarker Diagnostics

Precision diagnostics underpin personalized treatment algorithms. Amyloid PET, CSF p-tau assays, and emerging plasma-based tests enable stratification of preclinical populations, lifting trial success odds and facilitating earlier prescribing. Lantheus’ 2024 acquisition of Life Molecular Imaging secured proprietary tracers that now integrate into commercial treatment pathways. Diagnostic reimbursement codes expand in the United States, while Europe adopts joint clinical-assessment frameworks to streamline coverage decisions. Plasma p-tau217 reached 89% sensitivity and 91% specificity for Alzheimer’s pathology in a 2024 Lancet Neurology study.[3]Biotechnology Innovation Organization, “Clinical Development Success Rates,” bio.org Roche launched its CE-marked Elecsys p-tau181 test in January 2025 at roughly USD 150, one-tenth the cost of amyloid-PET.

Expanding Neuroscience R&D Investments

Roche’s USD 50 billion commitment through 2030 exemplifies the sector’s massive capital influx. Similar, though smaller, pledges by Eli Lilly, Novartis, and Takeda concentrate on biologics manufacturing and AI-enabled target discovery. Venture capital funding rebounds after a 2024 dip, emphasizing platform technologies such as protein degraders and gene-editing modalities. Academic-industry consortia proliferate, pooling datasets and accelerating IND filings. Governments weigh in through tax incentives and expedited pathways, underscoring neuroscience as a strategic research frontier. Eli Lilly allocated USD 3.2 billion to new neuroscience programs and, in July 2023, acquired Versantis Bio for USD 1.9 billion to repurpose bimagrumab for Parkinson's-related sarcopenia. Pennsylvania earmarked USD 5 million for neurodegenerative research in December 2025, while Ireland’s FutureNeuro committed EUR 17.9 million in May 2024 to chronic-disease diagnostics.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High attrition rates in late-stage trials | -1.3% | Global, highest in North America and Europe | Medium term (2-4 years) |

| Premium pricing of advanced therapies | -0.9% | Global, acute in United States, mitigated in Europe | Short term (≤ 2 years) |

| Limited biomarker infrastructure | -0.6% | Latin America, Middle East, Africa, rural Asia-Pacific | Long term (≥ 4 years) |

| Viral-vector manufacturing bottlenecks | -0.8% | Global, affecting launches in North America, Europe, Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Patent Expirations of Key Neurology Brands

Eli Lilly terminated zagotenemab in December 2024, writing off USD 1.2 billion after missing cognitive endpoints. Roche ended its gantenerumab Alzheimer’s prevention study in March 2024 on the grounds of futility. Regulators now allow surrogate endpoints, but confirmatory trials must prove clinical benefit within nine years, compressing commercialization windows.

Aricept’s loss of exclusivity in 2026 erases USD 2.8 billion in branded revenue, triggering price compression across generic donepezil competitors. Similar erosion hits Namzaric by 2029, overlapping with premium launches of antibodies and gene therapies. Portfolio managers hedge by layering life-cycle extensions, fixed-dose combos, new delivery systems, and OTC switches, but margin dilution remains inevitable. Emerging markets, where intellectual property enforcement lags, see even steeper price declines, challenging multinational revenue-recapture strategies. This constraint suppresses near-term top-line growth while nudging firms to accelerate higher-value innovation, thereby indirectly sustaining the broader neurodegenerative disease market.

Premium Pricing of Advanced Biologics & Gene Therapies

Lecanemab lists at USD 26,500 per year, and donanemab is expected to cost near USD 32,000, swelling Medicare Part B spending by 38% between 2023 and 2024. Novartis’ Zolgensma commands USD 2.1 million per patient; outcomes-based contracts tie payments to motor milestones. Germany negotiated a 12% discount on lecanemab in May 2025, linking price to real-world evidence of benefit beyond 18 months.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Indication: Alzheimer’s Disease Dominates Despite ALS Growth

Alzheimer’s disease commanded 41.72% of the neurodegenerative disease market share in 2025, buoyed by high prevalence and multiple labeled therapies. The 2025 surge in Leqembi revenue, topping JPY 23.1 billion (USD 154 million), reaffirmed commercial headroom for disease-modifying antibodies. Parkinson’s and multiple sclerosis sustain volume through entrenched dopaminergic and immunomodulatory regimens, yet incremental innovation remains slower. ALS, albeit small, posts a 9.36% CAGR, supported by gene-silencing candidates and expanded newborn-screening programs. Huntington’s benefits from Pridopidine’s European nod, adding a tangible disease-modifying option for the first time. Over the forecast, Alzheimer’s still anchors the neurodegenerative disease market, but diversified revenue flow from rare indications mitigates concentration risk.

A second layer of growth emerges as regulators widen accelerated-approval eligibility to lysosomal storage diseases with neurodegenerative components. Denali’s tividenofusp alfa breakthrough tag illustrates this trend, channelling capital toward previously neglected orphan indications. Collectively, these shifts broaden the therapeutic canvas, raising the ceiling for total neurodegenerative disease market size and creating cross-segment synergies in biomarker standardization.

By Drug Class: Cholinesterase Inhibitors Anchor, Gene Therapies Ascend

Cholinesterase inhibitors accounted for 27.98% of the neurodegenerative disease market in 2025, reflecting entrenched first-line use. Yet pipeline velocity now favors gene and cell therapies, which are set to grow 9.21% annually as vector design and manufacturing scale improve. Solid Biosciences’ SGT-212 clearance for Friedreich ataxia validates systemic AAV delivery for neuro-cardiac phenotypes, opening paths to adjacent forms of ataxia. Meanwhile, monoclonal antibodies extend beyond amyloid to target alpha-synuclein and TDP-43, supported by learnings in dosing optimization. NMDA antagonists and dopamine agonists remain staples but face generic exposure; sponsors defend share through long-acting injectables and digital adherence tools. RNA therapeutics occupy a strategic middle ground, with lower COGS than biologics and greater specificity than small molecules, further fragmenting drug-class leadership in the neurodegenerative disease market.

By Molecule Type: Small Molecules Lead, RNA Therapeutics Gain Traction

Small molecules retained 60.55% share in 2025, sustained by oral preference and mature supply chains. However, antisense oligonucleotides and siRNA platforms are predicted to post 9.14% CAGR, and they benefit from chemical modifications that extend dosing intervals to quarterly or bi-annual regimens. Ionis and Alnylam showcase proof-of-concept in spinal muscular atrophy and ATTR amyloidosis; lessons transfer into Parkinson’s and Huntington’s, reducing clinical risk. Biologics, including bispecific antibodies, expand via subcutaneous reformulations that cut infusion times and site-of-care costs. Meanwhile, hybrid constructs - antibody-RNA conjugates - blur category lines and demand nuanced regulatory guidance.

Manufacturing investments focus on modular, single-use bioreactors adaptable to both viral vectors and mRNA payloads. Such flexibility lowers capex per campaign, encouraging broader experimentation across molecule types and sustaining innovation-led growth in the neurodegenerative disease market.

By Route of Administration: Novel Delivery Gains Traction

Oral dosing dominated with 76.88% share in 2025, but patient and caregiver surveys reveal growing acceptance of minimally invasive alternatives once clinical benefit is demonstrated. Intranasal glutathione and transdermal rotigotine pilot programs record high adherence, validating 9.88% CAGR forecasts for these routes. Regulatory agencies expedite device-drug combination reviews, recognizing unmet needs in motor-symptom fluctuation control. Subcutaneous antibody auto-injectors halve clinic-time burden, enlarging eligible patient pools and smoothing supply chain logistics. Focused-ultrasound-mediated BBB openings remain experimental but show potential for periodic, non-systemic gene-editing payload delivery. Collectively, route innovation diversifies delivery choices and enhances the patient-centricity of the neurodegenerative disease industry.

By Distribution Channel: Digital Transformation Accelerates

Hospital pharmacies controlled 53.92% of the neurodegenerative disease market share in 2025 as initiation protocols for antibodies and gene therapies demand specialist oversight. Yet telemedicine proliferation propels online pharmacy CAGR to 10.08%, with e-prescription integrations enabling direct-to-home fulfilment for maintenance dosing. Specialty pharmacies fortify cold-chain capacity and deploy nurse-led adherence programs; CareMed’s alliance with Eisai typifies such models. Retail chains upgrade consultation rooms for in-store cognitive testing, bridging diagnosis and dispensing. Payers pilot value-based contracts tied to digital-biomarker outcomes uploaded via patient apps, further embedding tech into distribution workflows. This omni-channel evolution underpins an increasingly accessible neurodegenerative disease market.

Geography Analysis

North America accounted for 41.96% of worldwide revenue in 2025, as the FDA’s accelerated approval pathway and Medicare reimbursement are driving rapid uptake of novel biologics. Breakthrough tags for posdinemab and tividenofusp alfa in January 2025 exemplify regulatory agility. Venture capital funnels toward Boston and San Francisco hubs, while Roche’s USD 50 billion U.S. expansion secures domestic biologics capacity. Canada broadens early-access programs, and Mexico leverages near-shoring to attract packaging operations, creating a contiguous North American supply ecosystem that boosts the neurodegenerative disease market.

Asia-Pacific holds the fastest 8.31% CAGR outlook through 2031. Japan’s rapid adoption of Leqembi set a regional precedent for reimbursing expensive antibodies despite budget scrutiny. China is accelerating NDA reviews through its priority-review channel, with local firms co-developing biosimilars and RNA therapies to lower entry prices. South Korea funds AI-guided screening tools, and Australia integrates genomic testing into public health benefits. Collectively, infrastructure expansion and policy harmonization expand patient access and diversify revenue drivers within the neurodegenerative disease market.

Europe posts steady growth anchored by EMA’s centralized procedures that balance risk and access. The agency’s Pridopidine reversal signals an openness to re-evaluation based on post-hoc analyses. Germany, France, and the United Kingdom remain premium markets but negotiate outcome-based rebates to contain spending. Southern Europe increases deployment of regional dementia plans co-funded by EU cohesion funds, supporting earlier diagnosis and slowing disease progression. While differing national HTA assessments fragment launch sequencing, collective purchasing through EU4 consortia mitigates pricing gaps and sustains the continental contribution to the neurodegenerative disease market.

Competitive Landscape

Market structure remains moderately concentrated, with top multinationals leveraging patent estates and distribution muscle, yet no single firm exceeds a one-third share. Biogen, Roche, Eli Lilly, Eisai, and Novartis collectively hold an estimated 62% of branded revenue, leaving ample headroom for venture-backed entrants. Strategic alliances dominate deal flow, typified by Biogen–Neomorph’s USD 1.45 billion protein-degrader pact and Novartis–BioAge’s USD 530 million longevity collaboration. M&A activity rebounded with AbbVie’s USD 8.7 billion Cerevel take-out and Johnson & Johnson’s USD 14.6 billion Intra-Cellular Therapies acquisition, reflecting appetite for de-risked Phase II assets.

Emerging platforms leverage AI to unearth novel targets and accelerate chemistry workflows, challenging incumbents’ scale advantage. Solid Biosciences’ FDA clearance and Annovis Bio’s phase-3 acceptance underscore regulators’ willingness to green-light smaller sponsors with compelling science. Meanwhile, big pharma diversifies into diagnostics and digital health to lock in end-to-end value capture, as shown by Lantheus’ imaging play and Eli Lilly’s tele-health rollout. Overall, dynamic collaboration, selective consolidation, and cross-sector convergence define competitive choreography within the neurodegenerative disease market.

Neurodegenerative Disease Industry Leaders

Boehringer Ingelheim International GmbH

UCB SA

Novartis AG

Merck & Co Inc.

Teva Pharmaceuticals, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: NRG Therapeutics dosed first participants in a Phase 1 ALS/Parkinson’s trial for NRG5051.

- January 2026: Ipsen entered a global option deal with Origami Therapeutics for protein degraders addressing genetic neurodegeneration.

- December 2025: SciNeuro Pharmaceuticals closed USD 53 million financing to advance Lp-PLA2, beta-amyloid, and LRRK2 programs.

- June 2025: Roche advanced its Parkinson’s candidate into Phase III following positive mid-stage data.

- December 2024: Lantheus closed its USD 1.27 billion purchase of Life Molecular Imaging.

- November 2024: Johnson & Johnson announced a USD 14.6 billion acquisition of Intra-Cellular Therapies.

Global Neurodegenerative Disease Market Report Scope

As per the scope of the report, neurodegenerative disease is a broad term used to denote a range of conditions that primarily affect the neurons in the brain. Neurodegenerative diseases are incurable, and neuron degradation leads to neurons' gradual death.

The market is segmented by indication type, drug type, and geography. By indication type, the market is segmented into Parkinson's disease, Alzheimer's disease, multiple sclerosis, Huntington's disease, and other indication types. By drug class, the market is segmented into N-methyl-D-aspartate receptor antagonists, cholinesterase inhibitors, dopamine agonists, immunomodulatory drugs, and other drug types. By molecule type, the market is segmented into small-molecule drugs, biologics & monoclonal antibodies, RNA-based therapeutics, and others. By route of administration, the market is segmented into oral, parenteral (IV/SC), transdermal/intranasal, intrathecal delivery, and focused-ultrasound mediated delivery. By distribution channel, the market is segmented into hospital pharmacies, retail & specialty pharmacies, and online pharmacies. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the market sizes and forecasts in 17 countries across the major regions. For each segment, the market size is provided in terms of value (USD).

| Parkinsons Disease |

| Alzheimers Disease |

| Amyotrophic Lateral Sclerosis (ALS) |

| Multiple Sclerosis |

| Huntington Disease |

| Frontotemporal Dementia |

| Spinal Muscular Atrophy (SMA) |

| Other Rare Neurodegenerative Disorders |

| NMDA Receptor Antagonists |

| Cholinesterase Inhibitors |

| Dopamine Agonists |

| Immunomodulators / Monoclonal Antibodies |

| Gene & Cell Therapies |

| Antisense Oligonucleotides & RNAi |

| Other Drug Classes |

| Small-Molecule Drugs |

| Biologics & Monoclonal Antibodies |

| RNA-based Therapeutics |

| Others |

| Oral |

| Parenteral (IV/SC) |

| Transdermal/Intranasal |

| Intrathecal Delivery |

| Focused-Ultrasound Mediated Delivery |

| Hospital Pharmacies |

| Retail & Specialty Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Indication | Parkinsons Disease | |

| Alzheimers Disease | ||

| Amyotrophic Lateral Sclerosis (ALS) | ||

| Multiple Sclerosis | ||

| Huntington Disease | ||

| Frontotemporal Dementia | ||

| Spinal Muscular Atrophy (SMA) | ||

| Other Rare Neurodegenerative Disorders | ||

| By Drug Class | NMDA Receptor Antagonists | |

| Cholinesterase Inhibitors | ||

| Dopamine Agonists | ||

| Immunomodulators / Monoclonal Antibodies | ||

| Gene & Cell Therapies | ||

| Antisense Oligonucleotides & RNAi | ||

| Other Drug Classes | ||

| By Molecule Type | Small-Molecule Drugs | |

| Biologics & Monoclonal Antibodies | ||

| RNA-based Therapeutics | ||

| Others | ||

| By Route of Administration | Oral | |

| Parenteral (IV/SC) | ||

| Transdermal/Intranasal | ||

| Intrathecal Delivery | ||

| Focused-Ultrasound Mediated Delivery | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail & Specialty Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the Neurodegenerative disease market in 2026?

It reached USD 63.21 billion in 2026 and is projected to climb to USD 88.83 billion by 2031.

Which indication dominates sales?

Alzheimer’s disease leads with 41.72% share of global revenue in 2025.

What is the fastest-growing region between 2026 and 2031?

Asia-Pacific is forecast to expand at an 8.31% CAGR due to aging demographics and improved access.

Are gene therapies gaining traction?

Yes, gene and cell therapies are the fastest-growing drug class with a projected 9.21% CAGR.

How are digital channels affecting drug distribution?

Online pharmacies show a 10.08% CAGR as telemedicine and e-prescriptions improve access to complex therapies.

What keeps late-stage failure rates high?

Biological complexity and difficulty in measuring clinical endpoints drive Phase III attrition rates above 85%.

Page last updated on: