Neurological Disorder Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

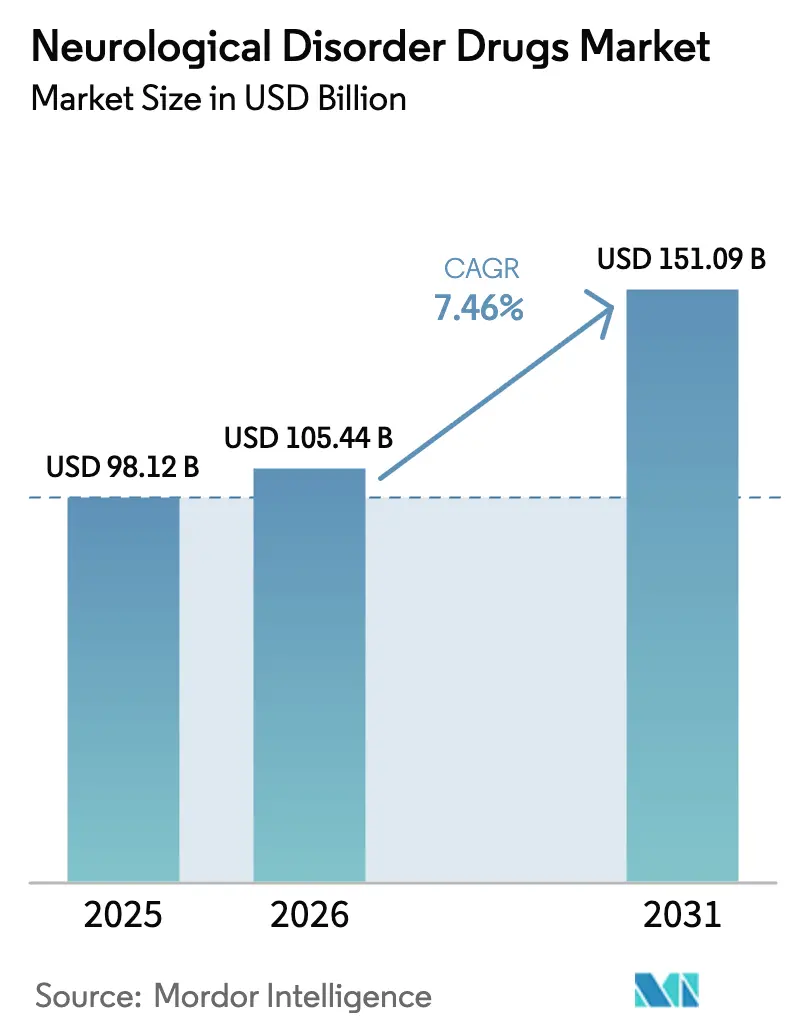

| Market Size (2026) | USD 105.44 Billion |

| Market Size (2031) | USD 151.09 Billion |

| Growth Rate (2026 - 2031) | 7.46% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Neurological Disorder Drugs Market Analysis by Mordor Intelligence

The neurological disorder drugs market size was valued at USD 98.12 billion in 2025 and estimated to grow from USD 105.44 billion in 2026 to reach USD 151.09 billion by 2031, at a CAGR of 7.46% during the forecast period (2026-2031). Demographic ageing, breakthrough disease-modifying approvals, and artificial-intelligence-enabled discovery pipelines are the three structural forces widening access to advanced therapeutics across every major indication. Regulatory agencies are sustaining the growth trajectory by applying accelerated approval pathways, a stance illustrated by the full approvals of Leqembi and Donanemab for Alzheimer’s disease. Digital health adoption is simultaneously reshaping distribution economics, while patent-cliff pressures between 2025 and 2029 are opening space for biosimilars that can reach patients faster across cost-sensitive geographies. In parallel, capacity expansions in sterile injectable manufacturing are becoming a competitive differentiator as supply chain resilience joins safety and efficacy as a front-line purchase criterion.

Key Report Takeaways

- By indication, Alzheimer’s disease led with 28.67% of the neurological disorder drugs market share in 2025; rare & orphan neurological disorders are forecast to expand at an 8.01% CAGR through 2031.

- By drug class, antiepileptics commanded 24.01% share of the neurological disorder drugs market size in 2025; CGRP monoclonal antibodies are projected to rise at an 8.29% CAGR to 2031.

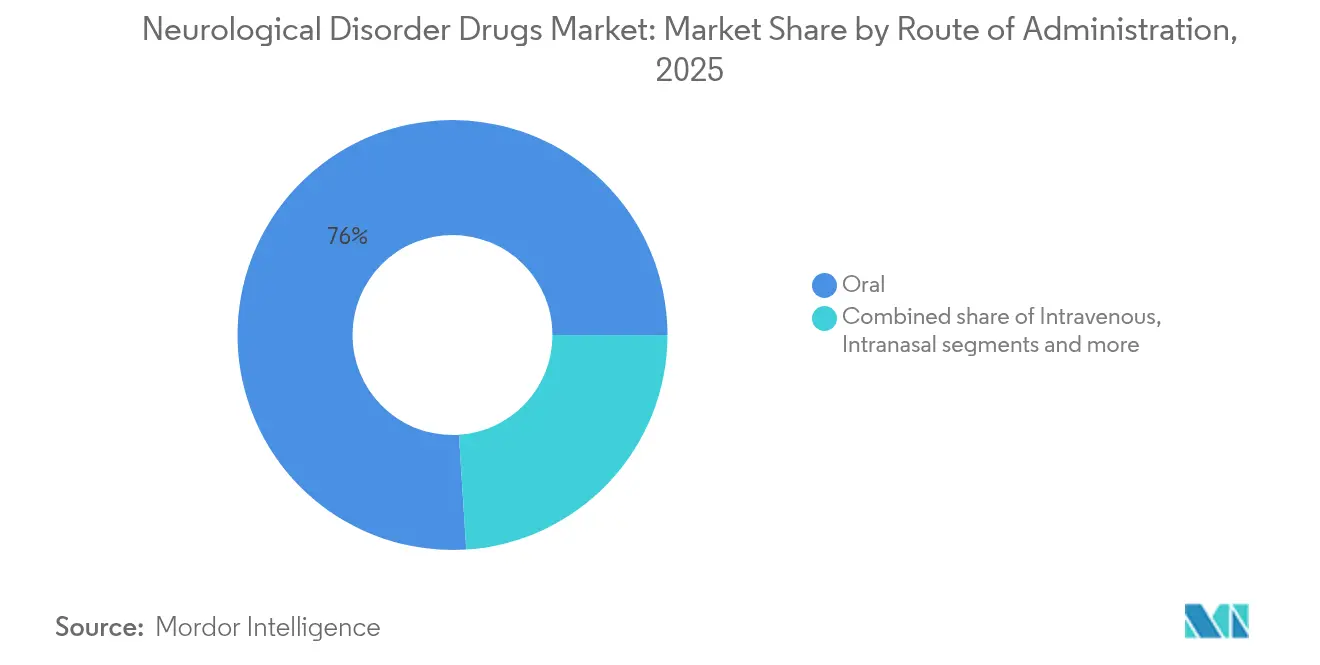

- By route of administration, oral formulations accounted for 76.02% share in 2025, while intranasal delivery platforms are set to grow at an 8.35% CAGR through 2031.

- By distribution channel, hospital pharmacies captured 53.21% share in 2025; online pharmacies are advancing at a 8.54% CAGR to 2031.

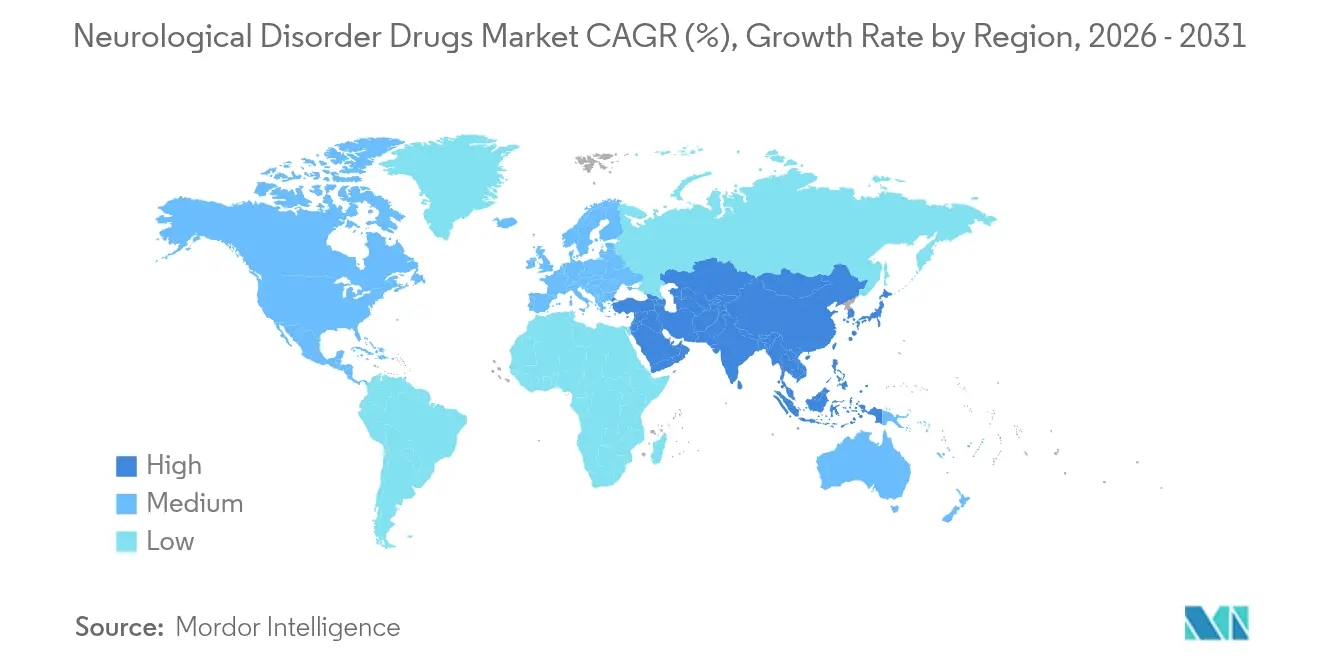

- North America held 39.35% share of the neurological disorder drugs market size in 2025, whereas Asia-Pacific is progressing at a 8.70% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Neurological Disorder Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing population & rising prevalence of CNS disorders | +1.8% | Global; strongest in North America & Europe | Long term (≥ 4 years) |

| Breakthrough disease-modifying approvals (Leqembi, Donanemab) | +1.2% | North America & EU; expanding to APAC | Medium term (2-4 years) |

| Expansion of orphan-drug incentives | +0.9% | Global; highest in North America | Medium term (2-4 years) |

| AI-enabled neuro-drug discovery | +0.7% | Global; led by US & EU hubs | Long term (≥ 4 years) |

| Novel BBB & intranasal delivery platforms | +0.6% | Global; early uptake in developed markets | Medium term (2-4 years) |

| Venture funding surge in psychedelic-assisted neurotherapeutics | +0.4% | North America & EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Ageing Population & Rising Prevalence of CNS Disorders

Longer life expectancy is increasing the absolute number of patients with chronic neurological illnesses, a trend most visible in high-income economies where individuals aged ≥ 60 will represent more than 30% of the population by 2050[1]Source: Department of Ageing, “Ageing and Health,” World Health Organization, who.int . Europe already reports 6.9 million Alzheimer’s cases, a figure that could double before mid-century, prompting insurers to reimburse earlier and costlier interventions. Similar prevalence curves are appearing in Parkinson’s disease, epilepsy, and multiple sclerosis, allowing manufacturers that expand regional production to secure first-mover volume advantages. Governments are also financing preventive screening that paradoxically lifts diagnosed prevalence and enlarges the addressable pool for therapeutics. The direct economic burden is pushing regulators to accelerate approvals, tightening the feedback loop between scientific discovery and bedside adoption and thereby supporting sustained expansion of the neurological disorder drugs market.

Breakthrough Disease-Modifying Approvals Drive Market Confidence

Leqembi’s full approval and Donanemab’s positive Phase III data have proven that amyloid-targeting pathways can achieve clinical and commercial success, validating high-risk neurodegenerative targets. Revenue ramp-ups have signaled strong payer acceptance despite high list prices, emboldening capital markets to back next-generation disease-modifying candidates across Huntington’s disease, ALS, and frontotemporal dementia. The European Medicines Agency revised its earlier stance on Leqembi, highlighting regulators’ willingness to re-assess benefit-risk when unmet need is compelling. Companies are reacting by accelerating time-to-submission strategies and intensifying global Phase III enrolment, moves that shorten commercialization cycles and further enlarge the neurological disorder drugs market.

Expansion of Orphan-Drug Incentives Accelerates Rare-Disease Development

Targeted laws such as the ACT for ALS Act and enhanced tax credits now underwrite early research, enabling smaller biotechs to advance niche neurological programs otherwise deemed uneconomic. Successful launches of Ztalmy and Skyclarys confirm that rare neurology can deliver blockbuster-level returns when exclusivity and pricing converge. Big Pharma is responding with acquisition mandates that secure first-in-class assets and specialized medical-science liaisons for ultra-orphan engagement. Improved registry data are also de-risking trial design by clarifying natural history endpoints, thereby pushing the neurological disorder drugs market toward precision-sized sub-markets that still carry premium margins.

AI-Enabled Neuro-Drug Discovery Transforms Pipeline Development

Machine-learning models now match genomic and proteomic signatures to druggable targets, aiding discovery in pathologies notorious for complex etiology. The EMA’s draft reflection paper on AI has given developers a framework for validating algorithms, effectively mainstreaming computational approaches. Cerevance’s NETSseq platform, already partnered with Merck, exemplifies how AI shortens target-ID cycles and reduces false positives[2]Source: Editorial Desk, “Cerevance Achieves First Milestone in Collaboration with Merck,” Cerevance, cerevance.com . As productivity improves, pipeline breadth is rising without proportional cost escalation, expanding the investable universe within the neurological disorder drugs market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High late-stage attrition & R&D costs in CNS | -1.4% | Global; highest in US & EU | Long term (≥ 4 years) |

| Wave of blockbuster patent expiries (2025-29) | -1.1% | Global; concentrated in developed markets | Short term (≤ 2 years) |

| Supply shortage of cGMP neuro-APIs & sterile injectables | -0.8% | Global; acute in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Late-Stage Attrition & R&D Costs Create Development Barriers

Neurology maintains the lowest Phase III success rate among major therapeutic areas, hovering near 30% compared with 58% for oncology. Complex endpoints, placebo effects, and heterogeneous pathophysiology drive median program costs above USD 2 billion, throttling smaller companies reliant on single assets. Investors, still wary from high-profile Alzheimer’s failures, require co-development risk-sharing that dilutes upside. Large firms mitigate through diversified portfolios, but the absolute spend siphons resources from early exploratory programs, dampening near-term asset flow into the neurological disorder drugs industry.

Patent Cliff Pressures Intensify Competitive Dynamics

Blockbusters across epilepsy, multiple sclerosis, and migraine will relinquish exclusivity before 2029, slicing in branded sales and triggering generic erosion. Payors already implement automatic substitution when chronic therapies fall below copay thresholds, pressuring innovators to launch line-extensions or fixed-dose combinations. While biosimilars expand access, they compress price corridors and can restrain top-line growth inside the neurological disorder drugs market—at least until next-wave disease-modifying agents backfill revenue gaps.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Indication: Alzheimer’s Scale Paired with Rare-Disease Velocity

Alzheimer’s disease generated 28.67% of neurological disorder drugs market revenue in 2025 on the back of high-ticket disease-modifying launches. The platform is widening as payers approve biomarker-confirmed early-stage use, anchoring premium ASPs and elevating the overall neurological disorder drugs market size. In the same period, rare & orphan neurologic diseases grew fastest, advancing at an 8.01% CAGR owing to orphan-drug exclusivity and public-grant co-funding. The differential growth rates signal portfolio-balancing value: broad-based Alzheimer’s drugs produce predictable volume while smaller, high-exclusivity disorders deliver margin upside.

Pipeline readouts in Huntington’s and Rett syndrome illustrate how niche indications can pivot to non-dilutive financing, allowing firms to monetize science before peak-sales maturity. Across Parkinson’s and epilepsy, incremental innovation—such as extended-release L-dopa and third-generation sodium-channel blockers—sustains mid-single-digit growth but cedes relative share to high-impact disease-modifiers. Migraine continues its biologics-driven transformation, as CGRP inhibitors expand prophylaxis beyond triptan non-responders, reinforcing multi-brand coexistence under roomier clinical guidelines. Collectively, indication diversity hedges exposure to single-asset risk and keeps the neurological disorder drugs market on a stable expansion path.

By Drug Class: Antiepileptics Anchor, CGRP Biologics Accelerate

Antiepileptics retained 24.01% of the neurological disorder drugs market share in 2025 thanks to entrenched prescribing patterns and broad insurance coverage. Their generics bulk still provides high patient volume, but revenue concentration is shifting as branded precision molecules secure orphan reimbursement. CGRP monoclonal antibodies, however, recorded the highest 8.29% CAGR, scaling an addressable pool of 36 million chronic migraine patients who previously cycled through four or more preventive classes.

Cholinesterase inhibitors and NMDA antagonists remain Alzheimer’s mainstays, yet real-world evidence indicates gradual slot replacement by Leqembi and Donanemab, reaffirming the transition from symptomatic to disease-modifying therapy. Dopamine agonists preserve relevance in Parkinson’s motor-symptom control, but non-motor endpoints drive demand for combination protocols. Immunomodulators, notably S1P receptor modulators, widen multiple-sclerosis remission durability, while biosimilar interferons introduce cost offsets that allow payors to fund novel agents. This compositional shift underscores how diversified drug-class dynamics reinforce resilience across the neurological disorder drugs market.

By Route of Administration: Oral Dominance Faces Direct-to-Brain Innovation

Oral drugs represented 76.02% of neurological disorder drugs market volume in 2025, reflecting patient preference and straightforward manufacturing economics. Convenience factors lock in strong adherence, keeping the oral segment’s neurological disorder drugs market size above USD 74.58 billion. Intranasal delivery, however, is posting an 8.35% CAGR as nanoparticle excipients improve nose-to-brain transit, delivering rapid-onset seizure rescue and new-generation migraine prophylaxis without systemic exposure.

Intravenous therapies still underpin hospital-based acute care in stroke thrombolysis and status epilepticus, fields where bioavailability trumps convenience. Depot subcutaneous injections and transdermal systems fill the “Others” category, layering differentiation on chronically dosed agents through extended release and wearable patches. Technology convergence is allowing formulators to re-platform old APIs into novel devices, deepening lifecycle management and diversifying the revenue base within the neurological disorder drugs market.

By Distribution Channel: Hospitals Hold Scale, Online Platforms Gain Velocity

Hospital pharmacies controlled 53.21% of 2025 sales because many neurological biologics require cold-chain handling and infusion monitoring. Their structural role anchors formulary inclusion and centralizes patient management for complex therapies. Online pharmacies, scaling at 8.54% CAGR, benefit from tele-neurology uptake and chronic refill automation, particularly for epilepsy and migraine maintenance drugs where adherence drives outcomes.

Retail outlets remain vital for face-to-face counseling and immediate access to acute rescue medications, especially in emerging markets where e-commerce penetration lags. Hybrid distribution models are emerging: digitally enabled hospital systems push e-prescriptions directly to home-delivery partners, integrating smart-pack adherence sensors that feed data back to clinicians. As service differentiation matures, competitive advantage will hinge on ecosystem coordination, extending the neurological disorder drugs market beyond product sales into longitudinal patient-support platforms.

Geography Analysis

North America generated 39.35% of the neurological disorder drugs market size in 2025, underpinned by early uptake of FDA-approved disease-modifying agents and broad private-payer coverage. The region’s payer tolerance for premium therapies, combined with strong clinical-trial infrastructure, sustains double-digit launch trajectories for high-impact assets. Public policy also fuels demand: Medicare’s revised coverage decision for amyloid-targeting drugs effectively opens a multi-billion-dollar reimbursement channel, accelerating top-line momentum for asset holders.

Europe follows as the second-largest arena, though its reimbursement committees mandate cost-effectiveness thresholds that temper launch pricing. The EMA’s conditional endorsements typically require real-world evidence collection, compelling manufacturers to run outcome registries that can be leveraged globally. Despite tighter price discipline, pan-EU orphan-drug incentives—ten-year exclusivity and R&D tax credits—create vibrant sub-markets for rare neurological indications. Digital-health pilots in Germany’s DiGA program and France’s ETAPES tele-monitoring scheme are catalyzing remote-care integration, indirectly boosting prescription fills through adherence tools.

Asia-Pacific is the fastest-growing cluster, advancing at a 8.70% CAGR thanks to rapid urbanization, rising incomes, and regulatory harmonization. China’s National Reimbursement Drug List now incorporates several foreign neurological biologics, substantially reducing patient copays and unlocking volume. Japan’s Sakigake pathway continues to entice global developers with expedited review, while Australia’s Therapeutic Goods Administration aligns labeling changes within weeks of FDA actions, streamlining regional launches. Local manufacturing incentives in India and South Korea attract CDMO investment, shortening supply chains and building indigenous capacity that keeps margin erosion under control. The collective momentum positions Asia-Pacific as a strategic focal point for scaling the neurological disorder drugs market over the next decade.

Competitive Landscape

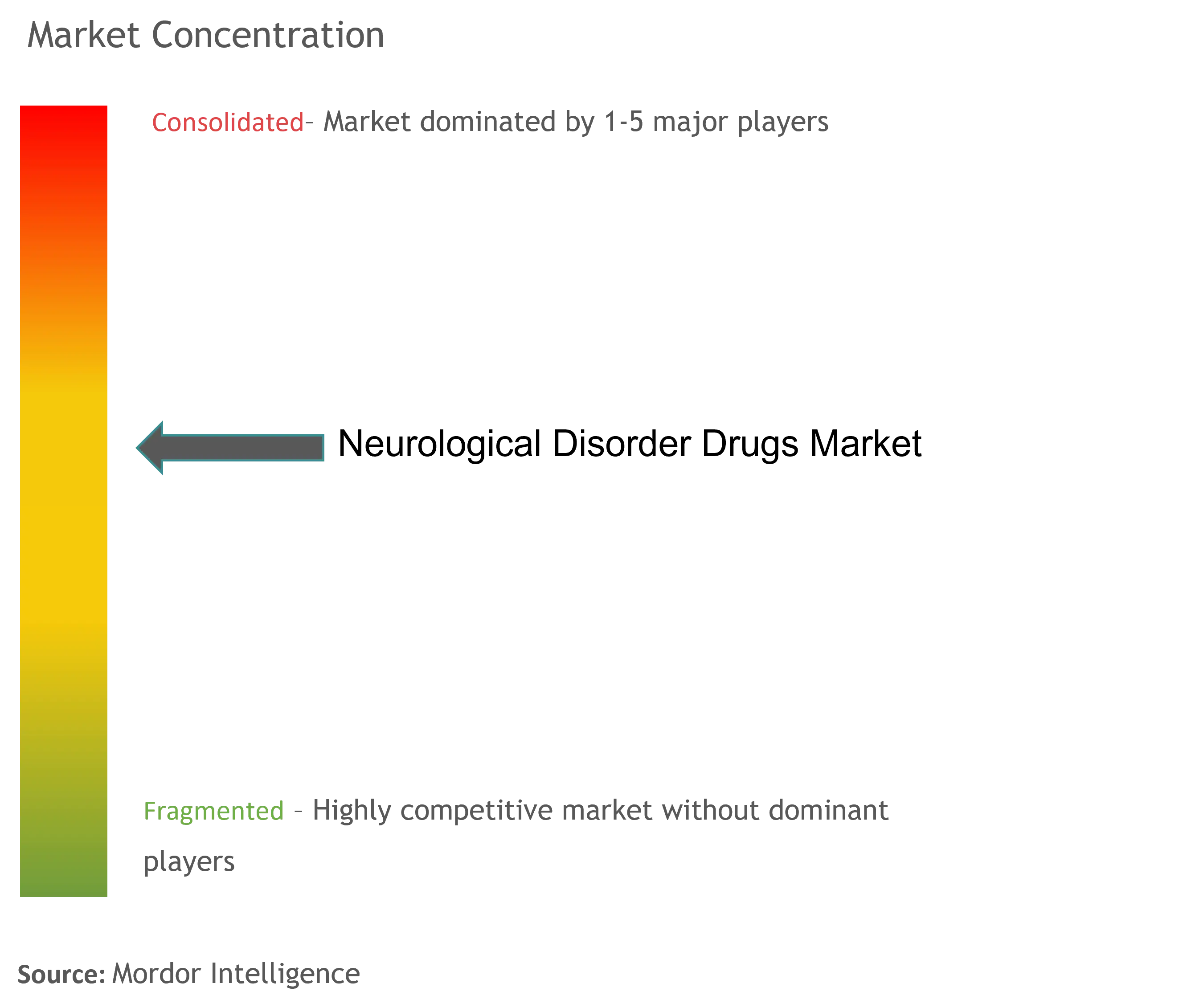

The neurological disorder drugs market depicts moderate concentration, with the top five companies controlling an estimated half of global revenue. Incumbents such as Biogen, Eli Lilly, and Roche deploy diversified portfolios spanning Alzheimer’s, multiple sclerosis, and rare epilepsy, mitigating single-asset risk. Their regulatory expertise allows parallel filings across continents, compressing time-to-revenue. Mid-caps including Acadia Pharmaceuticals and Neurocrine Biosciences leverage focused franchises and specialty sales forces, achieving outsized growth in movement disorders and tardive dyskinesia.

Strategic activity revolves around bolt-on acquisitions that infuse platform technologies—intranasal delivery, gene-editing, and digital therapeutics—into established pipelines. Lilly’s acquisition of intranasal-delivery firm Disarm showcases vertical integration aimed at route-of-administration differentiation, while Amgen’s Uplizna expansion into IgG4-related disease validates indications outside classic neurology yet dependent on neuro-immunology expertise. Collaborations with AI specialists such as Cerevance streamline target discovery, allowing pharma to outsource early risk while retaining downstream commercialization rights.

Price competition intensifies once molecules lose exclusivity; Takeda and Teva maintain competitive biosimilar units ready to cannibalize their own expiring blockbusters, thus defending share. Manufacturing resilience is emerging as a moat: companies with dual-continent sterile-fill plants weather API shortages better, protecting hospital contracts. Commercial models now integrate telehealth companion apps, with UCB’s epilepsy platform synchronizing refill reminders and seizure logs, creating sticky patient ecosystems that extend beyond the pill. This evolution keeps the neurological disorder drugs market dynamically balanced between scale advantages and niche innovation.

Neurological Disorder Drugs Industry Leaders

Pfizer Inc

Bayer AG

Johnson & Johnson Private Limited

Novartis AG

F. Hoffmann-La Roche Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Teva Pharmaceuticals presents real-world outcomes data for UZEDY (risperidone) showing 9.0% relapse rates compared to 15.4% for oral antipsychotics, with Phase 3 SOLARIS data demonstrating no incidence of post-injection delirium/sedation syndrome in over 3,400 injections.

- April 2025: Amgen’s UPLIZNA receives FDA approval as first treatment for IgG4-related disease, with Phase III MITIGATE trial showing 87% reduction in disease flares and 57.4% complete remission rate at 52 weeks

Global Neurological Disorder Drugs Market Report Scope

As per the scope of this report, neurological disorder drugs are used to treat a neurological or neuromuscular disorder of the nervous system, such as Parkinson's disease, Alzheimer's disease, and traumatic brain injuries.

The Neurological Disorder Drugs Market is segmented by Disorders (Epilepsy, Alzheimer's Disease, Parkinson's Disease, Multiple Sclerosis, Cerebrovascular Disease, and Other Disorders), Drug Type (Cholinesterase Inhibitors, NMDA Receptor Antagonists, Antiepileptic, Antipsychotic & Antidepressant, and Other Drugs Type), Distribution Channel (Hospital Pharmacies, Online Pharmacies, Retail Pharmacies) and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report also covers the estimated market sizes and trends for 17 countries across significant regions globally. The report offers the value (in USD million) for the above segments.

| Alzheimer’s Disease |

| Parkinson’s Disease |

| Epilepsy |

| Multiple Sclerosis |

| Migraine |

| ADHD & Other Psychiatric CNS |

| Rare & Orphan Neurological Disorders |

| Cholinesterase Inhibitors |

| NMDA Receptor Antagonists |

| Dopamine Agonists & Precursors |

| Antiepileptics |

| CGRP & Other Novel Biologics |

| Immunomodulators |

| Neuroprotective / Disease-Modifying Agents |

| Oral |

| Intravenous |

| Intranasal |

| Others |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Indication | Alzheimer’s Disease | |

| Parkinson’s Disease | ||

| Epilepsy | ||

| Multiple Sclerosis | ||

| Migraine | ||

| ADHD & Other Psychiatric CNS | ||

| Rare & Orphan Neurological Disorders | ||

| By Drug Class | Cholinesterase Inhibitors | |

| NMDA Receptor Antagonists | ||

| Dopamine Agonists & Precursors | ||

| Antiepileptics | ||

| CGRP & Other Novel Biologics | ||

| Immunomodulators | ||

| Neuroprotective / Disease-Modifying Agents | ||

| By Route of Administration | Oral | |

| Intravenous | ||

| Intranasal | ||

| Others | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the neurological disorder drugs market in 2026?

The market is valued at USD 105.44 billion in 2026 and is forecast to reach USD 151.09 billion by 2031.

Which therapeutic area holds the biggest revenue share?

Alzheimer's disease contributes 28.67% of 2025 sales, making it the single largest indication.

What is the fastest-growing drug class?

CGRP monoclonal antibodies for migraine prevention are expanding at an 8.29% CAGR through 2031.

Which region is growing fastest?

Asia-Pacific is set to register a 8.70% CAGR as health-care infrastructure matures and access widens.

How will patent expiries affect pricing?

Patents expiring between 2025 and 2029 will invite generic entry, compressing prices but broadening patient access.

What delivery technology shows most promise?

Intranasal nose-to-brain platforms are posting the highest growth, offering rapid CNS penetration and improved patient convenience.

Page last updated on: