Advanced Therapy Medicinal Products Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

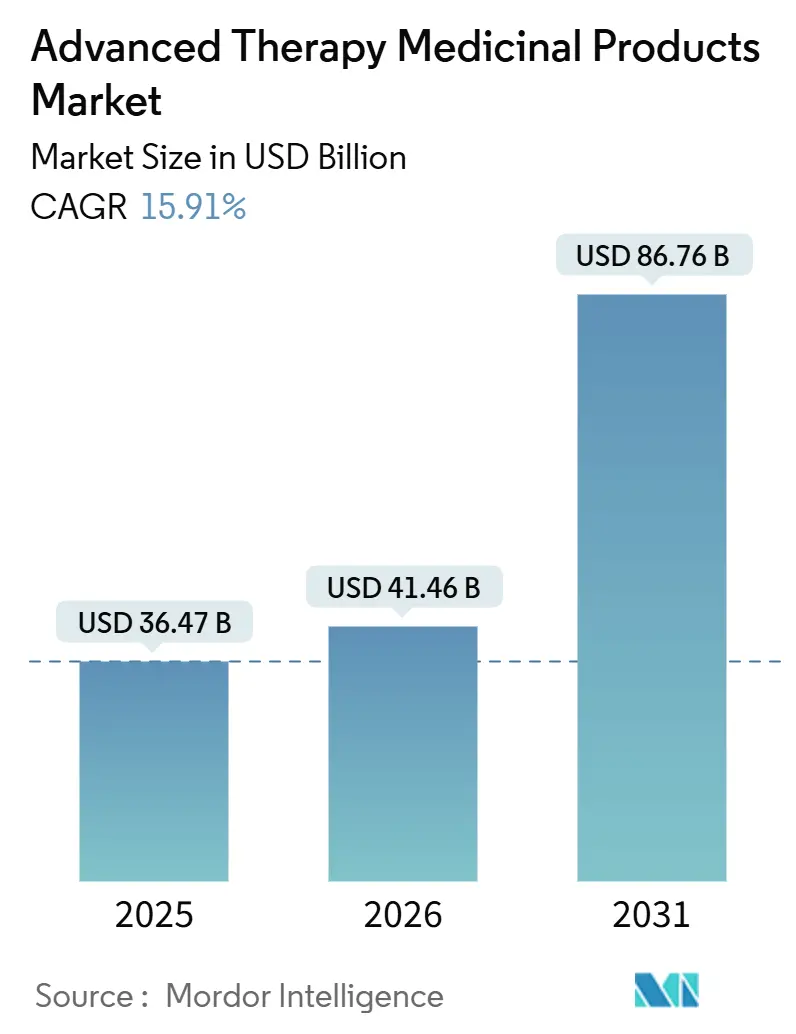

| Market Size (2026) | USD 41.46 Billion |

| Market Size (2031) | USD 86.76 Billion |

| Growth Rate (2026 - 2031) | 15.91% CAGR |

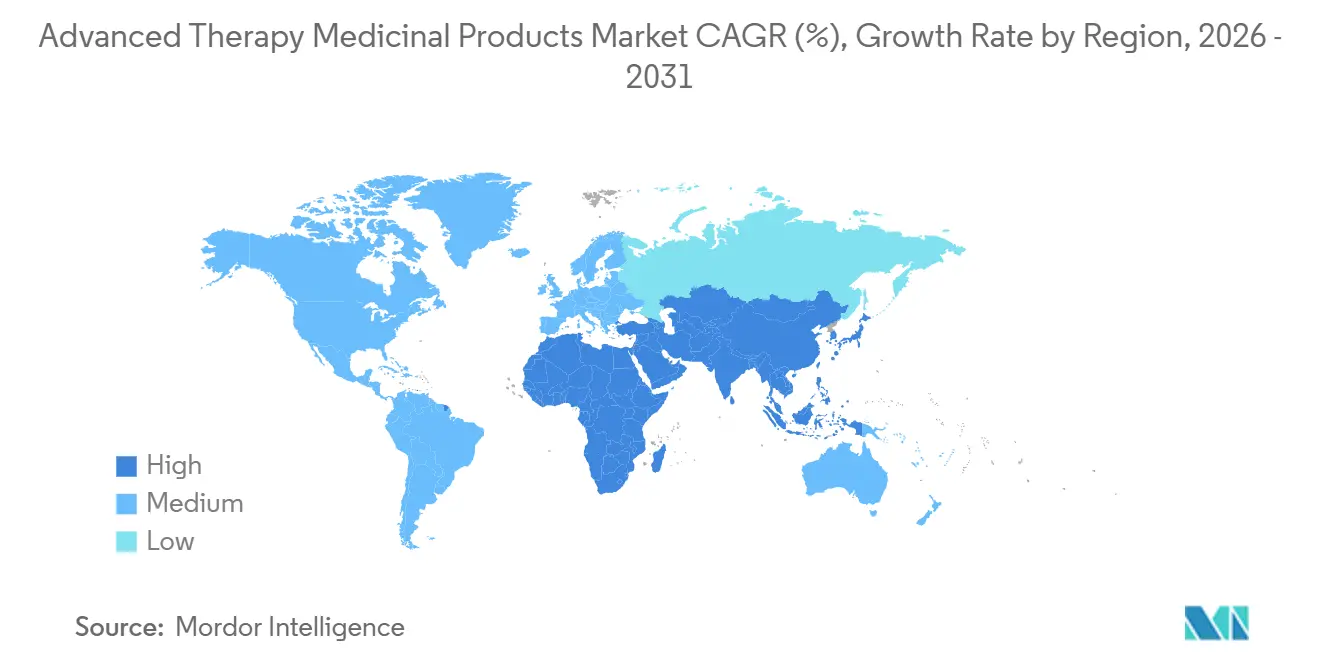

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

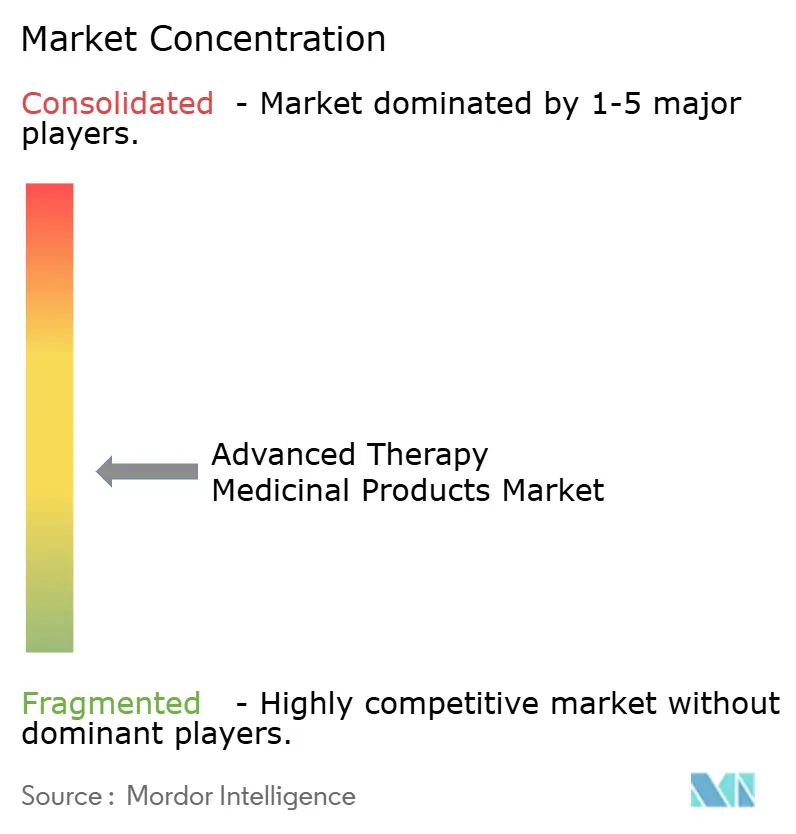

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Advanced Therapy Medicinal Products Market Analysis by Mordor Intelligence

The Advanced Therapy Medicinal Products Market size is projected to be USD 36.47 billion in 2025, USD 41.46 billion in 2026, and reach USD 86.76 billion by 2031, growing at a CAGR of 15.91% from 2026 to 2031.

Escalating regulatory fast-track designations, surging venture investment, and robust clinical success in CAR-T oncology programs are accelerating modality roll-outs. Viral-vector supply constraints and reimbursement innovation are shaping competitive strategies, while allogeneic off-the-shelf platforms promise to curb manufacturing lead times and broaden global access. Contract manufacturers are scaling modular plants to halve autologous turnaround, and Asia-Pacific health agencies are shortening review cycles to entice pipeline sponsors into local trials.

Key Report Takeaways

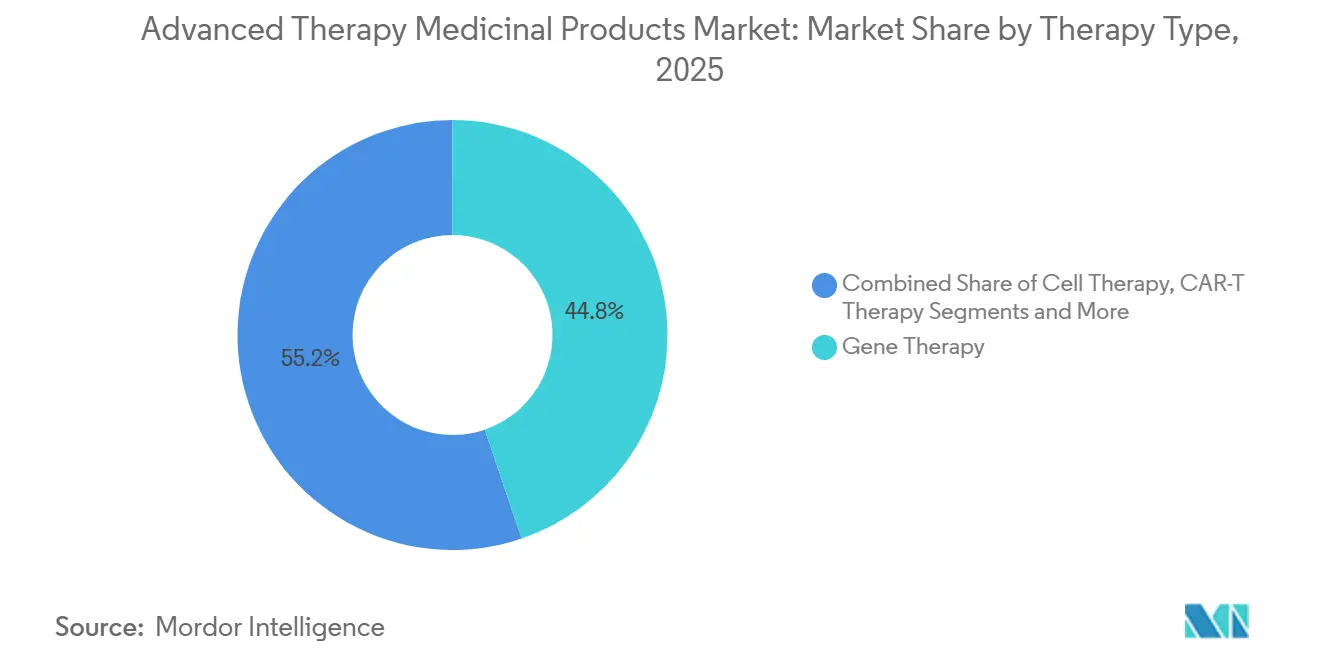

- By therapy type, gene therapy held 44.79% of the advanced therapy medicinal products market share in 2025, whereas CAR-T therapy is forecast to advance at a 20.01% CAGR to 2031.

- By cell source, autologous platforms contributed 61.73% of 2025 revenue, while allogeneic constructs are projected to rise at a 17.53% CAGR through 2031.

- By vector type, viral vectors captured 69.23% of 2025 spending, but gene-editing systems are set to expand at an 18.57% CAGR to 2031.

- By application, oncology accounted for 55.43% of demand in 2025, yet rare genetic disorders are poised to grow at a 19.45% CAGR between 2026 and 2031.

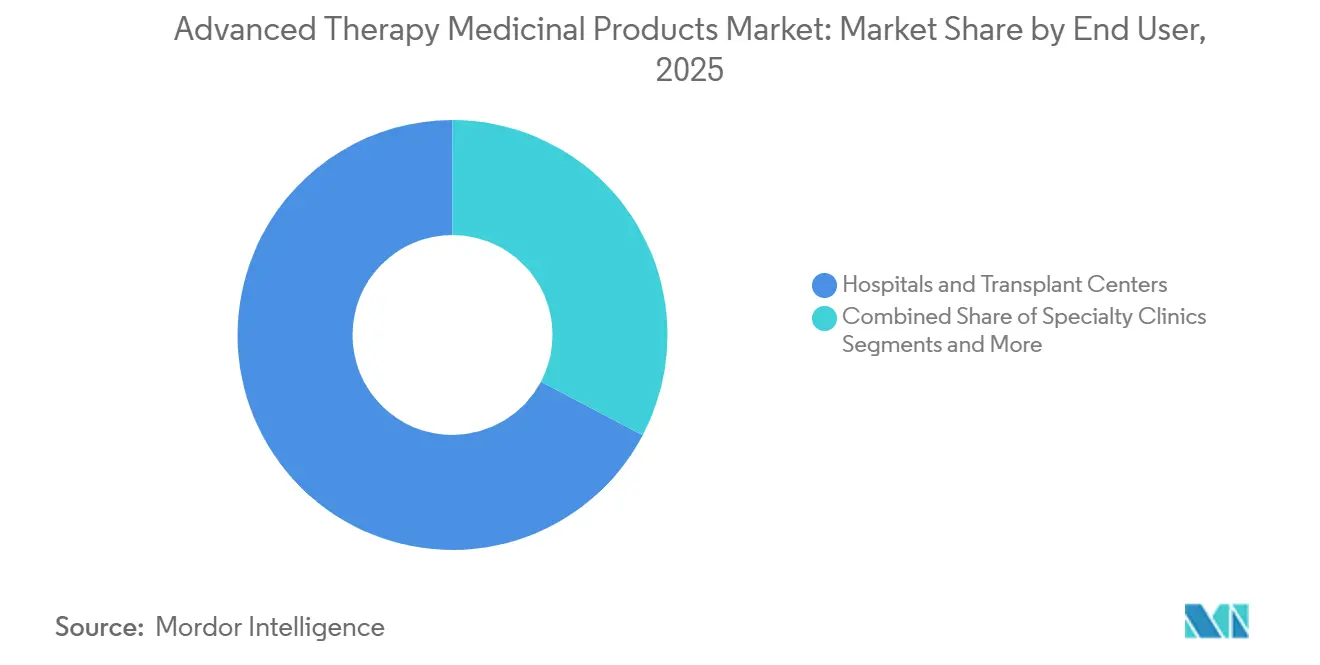

- By end user, hospitals and transplant centers generated 67.28% of 2025 outlays, whereas contract manufacturing organizations are anticipated to climb at an 18.26% CAGR to 2031.

- By manufacturing platform, ex-vivo modified systems made up 49.84% of 2025 production value, while point-of-care facilities are projected to advance at a 16.78% CAGR through 2031.

- By geography, North America delivered 39.22% of global revenue in 2025, but Asia-Pacific is forecast to post the fastest 18.46% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Advanced Therapy Medicinal Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fast-track regulatory designations rising | +2.8% | North America, Europe | Short term (≤ 2 years) |

| Venture-capital and big-pharma deal surge | +2.5% | North America, Europe, Asia-Pacific spill | Medium term (2–4 years) |

| Growing orphan and oncology prevalence | +2.3% | Global | Long term (≥ 4 years) |

| Outcome-based reimbursement pilots | +1.9% | North America, Europe, Australia | Medium term (2–4 years) |

| Decentralized GMP micro-facilities | +1.7% | Europe, North America, emerging Asia-Pac | Medium term (2–4 years) |

| AI-driven vector engineering | +1.5% | North America, Europe, Asia-Pacific R&D | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Fast-Track Designations and Approvals Surging Post-2024

Regulators are condensing review windows for high-need therapies, enabling first movers to secure orphan markets quickly. The EMA PRIME program accepted 11 advanced candidates in 2024, a 38% rise on 2023.[1] Emer Cooke, “PRIME: Priority Medicines,” European Medicines Agency, ema.europa.euJapan’s Sakigake pathway similarly granted four allogeneic designations, allowing conditional approval on Phase II data.[2]Yasuhiro Fujiwara, “Sakigake Designation System,” Pharmaceuticals and Medical Devices Agency, pmda.go.jp These mechanisms reduce the time-to-market to roughly six years, but new FDA guidance extends post-marketing surveillance for lentiviral products to 15 years, stretching the compliance budgets of smaller innovators.

Escalating VC and Big-Pharma Deal Values in ATMP Pipelines

Disclosed transaction value climbed to USD 12.3 billion in 2024, buoyed by Bristol-Myers Squibb’s USD 4.8 billion Mirati buy-out and Gilead’s USD 850 million Legend Biotech stake. Beam Therapeutics’ USD 520 million Series D in 2025 exemplifies venture appetite for next-gen base-editing. Capital concentration in the United States and Europe accelerates multi-indication programs yet leaves many Asia-Pacific teams reliant on out-licensing.

Rising Prevalence of Orphan and Oncology Indications Addressable by ATMPs

Roughly 300 million individuals live with rare diseases, and refractory cancer incidence continues to climb. CRISPR Therapeutics’ exa-cel gained U.S. approval in late-2024 for sickle cell disease, while bluebird bio’s Lyfgenia reached 89% transfusion independence in β-thalassemia trials. Multiple myeloma prevalence is forecast to rise 18% through 2031, underpinning demand for CAR-T lines such as Abecma and Tecartus.

Payer Shift Toward Outcome-Based Reimbursement Pilots for One-Time Cures

CMS launched its Cell and Gene Therapy Access Model in January 2025, letting state Medicaid agencies amortize payments over five years. Eight European health systems negotiated a 22% discount by tying payments to five-year outcomes, highlighting payers’ pivot toward risk-sharing. Novartis’ Zolgensma now carries outcome-linked contracts in 14 countries.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost and reimbursement uncertainty | −1.8% | Global, severe in emerging markets | Medium term (2–4 years) |

| Complex cold-chain logistics and brief shelf life | −1.2% | Global, acute in Asia-Pacific and MEA | Short term (≤ 2 years) |

| Long-term insertional-oncogenesis monitoring burden | −0.9% | North America, Europe | Long term (≥ 4 years) |

| Shortage of GMP-grade plasmids and LNP raw materials | −1.1% | North America, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost and Reimbursement Uncertainty for Curative One-Off Therapies

List prices of USD 1.5 million–3 million per patient strain payer budgets, limiting access outside wealthy regions. Bluebird bio’s Lyfgenia debuted at USD 3.1 million, and exa-cel lists at USD 2.2 million. U.S. private insurers often leave gene therapies off formularies, and middle-income economies lack subsidy frameworks, slowing adoption.

Complex Cold-Chain Logistics and Short Shelf-Life Challenges

Autologous products must remain below −150 °C and reach clinics within 48 hours. Novartis reported 12% product loss from shipping failures in 2024. Only 38% of Indian hospitals possess the required freezers, constraining penetration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapy Type: CAR-T Momentum Challenges Gene Therapy Dominance

The advanced therapy medicinal products market size for CAR-T constructs is forecast to advance at a 20.01% CAGR, narrowing the lead of gene therapy, which held 44.79% in 2025. Breyanzi’s 2024 approval for second-line diffuse large B-cell lymphoma improved progression-free survival by 34% compared to chemotherapy. Cell therapy options, such as Temcell, posted USD 180 million in Japanese sales, while tissue-engineered products remain a niche market because payers still debate their cost-effectiveness. Combination ATMPs blending gene editing with hypoimmune cell engineering are entering first-in-human studies. Overall, rapidly expanding CAR-T pipelines recalibrate the therapeutic mix and are poised to capture a growing share of the advanced therapy medicinal products market.

Gene therapy remains critical for treating monogenic disorders, but it contends with vector supply limitations and immunogenicity hurdles. Demand centers in Europe leverage hospital-exemption options to accelerate adoption, whereas U.S. payers insist on long-term durability data. Academic-industry coalitions such as Penn-Novartis are refining CRISPR edits to improve engraftment, signaling iterative innovation inside the advanced therapy medicinal products market.

By Cell Source: Allogeneic Platforms Reshape Manufacturing Economics

Allogeneic constructs are projected to outpace autologous workflows with a 17.53% CAGR through 2031, challenging the incumbent 61.73% autologous share. Century Therapeutics’ iPSC-CAR-NK program showed zero graft-versus-host events across 24 patients, and Sana Biotechnology’s SC291 posted 78% complete responses.

Global adoption hinges on inventory-based distribution, which reduces patient wait times to 48 hours and cuts manufacturing costs by 60%. Yet shorter persistence still drives some clinicians toward autologous regimens, sustaining segments of the advanced therapy medicinal products market size. Regulatory agencies now demand 10-year monitoring of gene-edited allogeneic constructs, adding clarity to risk management.

By Vector Type: Gene-Editing Gains Ground Against Viral Workhorses

Gene-editing systems are accelerating at an 18.57% CAGR and are poised to chip away at viral vectors’ 69.23% 2025 foothold. Beam Therapeutics reported 0.3% off-target edits with its base-editor in sickle cell trials, and exa-cel’s Cas9 approach achieved 91% transfusion independence.[3]David Liu, “Gene Editing Clinical Trials,” Nature, nature.com

Non-viral delivery, particularly with lipid nanoparticles, is emerging as a promising approach for mRNA-based CAR-T prototypes. Even so, adeno-associated virus serotype 9 continues to underpin durable in-vivo expression, preserving a sizable slice of the advanced therapy medicinal products market share. AI-guided guide-RNA design shortens optimization cycles and lowers discovery costs, further boosting gene-editing competitiveness.

By Application: Rare Diseases Approach Oncology Scale

Oncology kept 55.43% of 2025 demand, yet rare genetic disorders are forecast to log the strongest 19.45% CAGR as orphan designations lock in exclusivity and premium pricing. CMS’s reimbursement model now funds one-time sickle cell cures, helping the segment gain momentum. Cardiovascular, musculoskeletal, and ophthalmology pipelines demonstrate clinical progress but still await broad payer alignment to accelerate uptake in the advanced therapy medicinal products market.

By End User: CMOs Expand Industrial Footprint

Contract manufacturing organizations are set to rise at an 18.26% CAGR, eroding hospitals’ 67.28% 2025 hold. Lonza’s closed-system reactors cut autologous cycles in half and improve sterility by 72%. Catalent’s 200,000-square-foot Maryland plant adds 120 AAV batches annually. Specialty clinics are opening CAR-T infusion units, while academic centers continue to publish translational breakthroughs that feed commercial pipelines.

By Manufacturing Platform: Decentralization Spurs Point-of-Care Growth

Point-of-care suites are forecast to climb at a 16.78% CAGR, challenging ex-vivo facilities’ 49.84% share. Twelve European transplant centers now produce Kymriah on-site within seven days, bypassing international shipping. Automated devices such as CliniMACS Prodigy enable same-day CAR-T manufacture in 45 hospitals. FDA draft guidance requires site-specific validation, adding six to twelve months before full deployment, yet European payers incentivize local production to cut logistics risk, further diversifying the advanced therapy medicinal products market.

Geography Analysis

North America retained 39.22% of 2025 revenue thanks to FDA acceleration programs and a dense network of academic CAR-T hubs. Ten U.S. ATMP approvals in 2024, including exa-cel and BEAM-101, underline regulatory momentum. Canada’s harmonized standards enabled simultaneous Lyfgenia launch, while Mexico’s cost-effective trial infrastructure attracted Poseida’s Phase II allogeneic study. Payer fragmentation remains a hurdle as 42% of U.S. private insurers exclude gene therapies, tempering near-term growth.

Asia-Pacific is projected to lead expansion with an 18.46% CAGR. China’s NMPA cleared nine domestic CAR-T brands in 2024 and contributed most of Carvykti’s USD 680 million sales. India earmarked USD 120 million for ATMP development in 2025, prioritizing hemoglobinopathies, while South Korea’s Invossa secured USD 42 million sales under national insurance coverage. ASEAN regulatory divergence, however, still tacks 12–18 months onto regional launches, marginally delaying the advanced therapy medicinal products market ramp-up.

Europe continues to refine outcome-based reimbursement. Germany’s pooled procurement initiative locked in a 22% gene-therapy discount in 2025, and France now spreads Zolgensma payments over five years. EMA’s PRIME admissions accentuate the region’s clinical depth. Middle East and Africa markets remain embryonic as cold-chain gaps and high out-of-pocket expenses limit diffusion. South America’s first two CAR-T approvals in Brazil signal gradual emergence, yet reimbursement lags constrain immediate volume.

Competitive Landscape

The top five companies include Bristol-Myers Squibb, Gilead Sciences, Novartis, bluebird bio, and Vericel Corporation, which held major shares of global 2025 revenue, denoting moderate concentration. Breyanzi and Abecma collectively earned USD 2.1 billion in 2024. Gilead’s Yescarta and Tecartus added USD 1.8 billion, buttressed by vertically integrated Kite Pharma plants. Adaptimmune’s SPEAR T-cells achieved 43% responses in synovial sarcoma, evidencing competitive pressure from smaller entrants. Patent filings for allogeneic CAR-T platforms surged 47% in 2024, reinforcing the sector’s pivot to scalable inventory models.

Manufacturing agility and payer alignment dominate strategy. Lonza’s modular suites reduced turnaround to 14 days, and Novartis maintains bilateral outcome contracts across 14 nations. AI-mediated vector design accelerates pipeline throughput, while 15-year surveillance mandates raise barriers for start-ups. White-space opportunities persist in neurological and cardiovascular diseases, where late-stage ATMPs remain sparse within the advanced therapy medicinal products market.

Advanced Therapy Medicinal Products Industry Leaders

Novartis AG

Gilead Sciences, Inc.

Bristol-Myers Squibb Company

Bluebird Bio, Inc.

Vericel Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Cipla launched Ciplostem, an allogeneic MSC therapy for knee osteoarthritis cleared by India’s DCGI.

- December 2025: FDA approved Waskyra, the first cell-based gene therapy for Wiskott-Aldrich syndrome.

- November 2025: India unveiled BIRSA 101, its inaugural indigenous CRISPR gene therapy for sickle cell disease.

- January 2025: Immuneel Therapeutics introduced Qartemi, an autologous CAR-T for adult B-cell non-Hodgkin lymphoma.

Global Advanced Therapy Medicinal Products Market Report Scope

As per the scope of this report, advanced therapies are novel modes of disease treatment that are based on genes, tissues, or cells. These therapies offer new avenues for disease and injury treatment, thus revolutionizing the pharmaceutical industry. The Global Advanced Therapy Medicinal Products market is segmented by Therapy Type, cell source, vector type, application, end user, manufacturing platform, and geography. By Therapy type, the market is segmented by Cell Therapy, Gene Therapy, CAR-T Therapy, Tissue-Engineered Product, and Combination ATMPs. By Cell Source, the market is segmented into Autologous and Allogeneic. By Vector Type, the market is segmented by Viral Vectors, Non-viral Vectors, and Gene-editing. By Application, the market is segmented into oncology, Rare Genetic Disorders, Cardiovascular, musculoskeletal and orthopedic, Ophthalmology, Neurological Disorders, and Others. By End User, the market is segmented into hospitals and transplant centers, Specialty Clinics, academic and research institutes, and Contract Manufacturing Organizations. By Manufacturing Platform, the market is segmented into in-vivo modified, Ex-vivo Modified, Point-of-Care Facilities, and Centralized GMP Facilities. By Geography, the market is segmented by North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The Market Forecasts are Provided in Terms of Value (USD). The market report also covers the estimated market sizes and trends of 17 countries across major regions globally. The report offers values in USD million for the above segments.

| Cell Therapy |

| Gene Therapy |

| CAR-T Therapy |

| Tissue-Engineered Product |

| Combination ATMPs |

| Autologous |

| Allogeneic |

| Viral Vectors |

| Non-viral Vectors |

| Gene-editing |

| Oncology |

| Rare Genetic Disorders |

| Cardiovascular |

| Musculoskeletal & Orthopedic |

| Ophthalmology |

| Neurological Disorders |

| Others |

| Hospitals & Transplant Centers |

| Specialty Clinics |

| Academic & Research Institutes |

| Contract Manufacturing Organizations |

| In-vivo Modified |

| Ex-vivo Modified |

| Point-of-Care Facilities |

| Centralised GMP Facilities |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Therapy Type | Cell Therapy | |

| Gene Therapy | ||

| CAR-T Therapy | ||

| Tissue-Engineered Product | ||

| Combination ATMPs | ||

| By Cell Source | Autologous | |

| Allogeneic | ||

| By Vector Type | Viral Vectors | |

| Non-viral Vectors | ||

| Gene-editing | ||

| By Application | Oncology | |

| Rare Genetic Disorders | ||

| Cardiovascular | ||

| Musculoskeletal & Orthopedic | ||

| Ophthalmology | ||

| Neurological Disorders | ||

| Others | ||

| By End User | Hospitals & Transplant Centers | |

| Specialty Clinics | ||

| Academic & Research Institutes | ||

| Contract Manufacturing Organizations | ||

| By Manufacturing Platform | In-vivo Modified | |

| Ex-vivo Modified | ||

| Point-of-Care Facilities | ||

| Centralised GMP Facilities | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current global value of advanced therapy medicinal products and how fast is it expanding?

The market is valued at USD 41.46 billion in 2026 and is projected to reach USD 86.76 billion by 2031, advancing at a 15.91% CAGR.

Which treatment modality is forecast to grow the fastest through 2031?

CAR-T therapy shows the strongest momentum, with a projected 20.01% CAGR that outpaces all other modalities.

How are payers addressing the multi-million-dollar price tags of one-time gene therapies?

Programs such as the CMS Cell and Gene Therapy Access Model and pooled European purchasing agreements spread payments over five years and link them to real-world outcomes.

Why are allogeneic ''off-the-shelf'' cell sources garnering attention?

Why are allogeneic "off-the-shelf" cell sources garnering attention?

Which region is expected to see the fastest revenue growth by 2031?

Asia-Pacific is forecast to expand at an 18.46% CAGR, bolstered by multiple domestic CAR-T approvals in China and Japan's Sakigake fast-track pathway.

What logistical hurdle most commonly delays autologous therapies?

Maintaining −150 °C cold-chain shipping within a 48-hour window remains challenging, leading to product-loss rates of about 12% in 2024 shipments.

Page last updated on: