Brain Tumor Therapeutics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

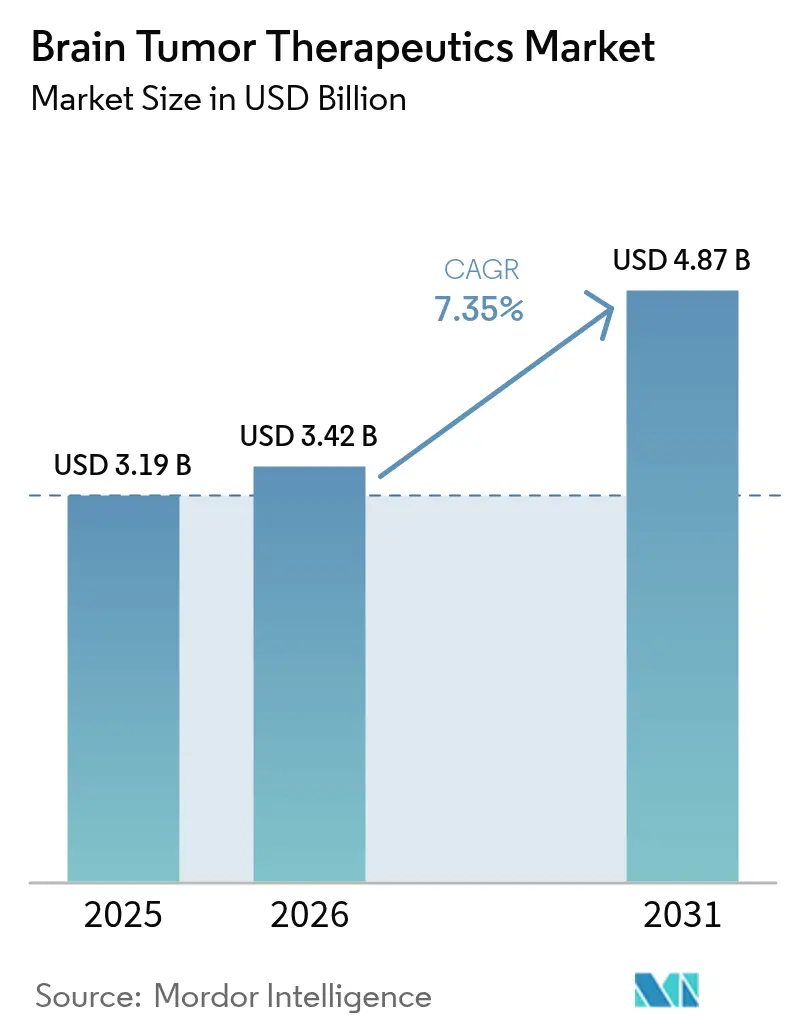

| Market Size (2026) | USD 3.42 Billion |

| Market Size (2031) | USD 4.87 Billion |

| Growth Rate (2026 - 2031) | 7.35% CAGR |

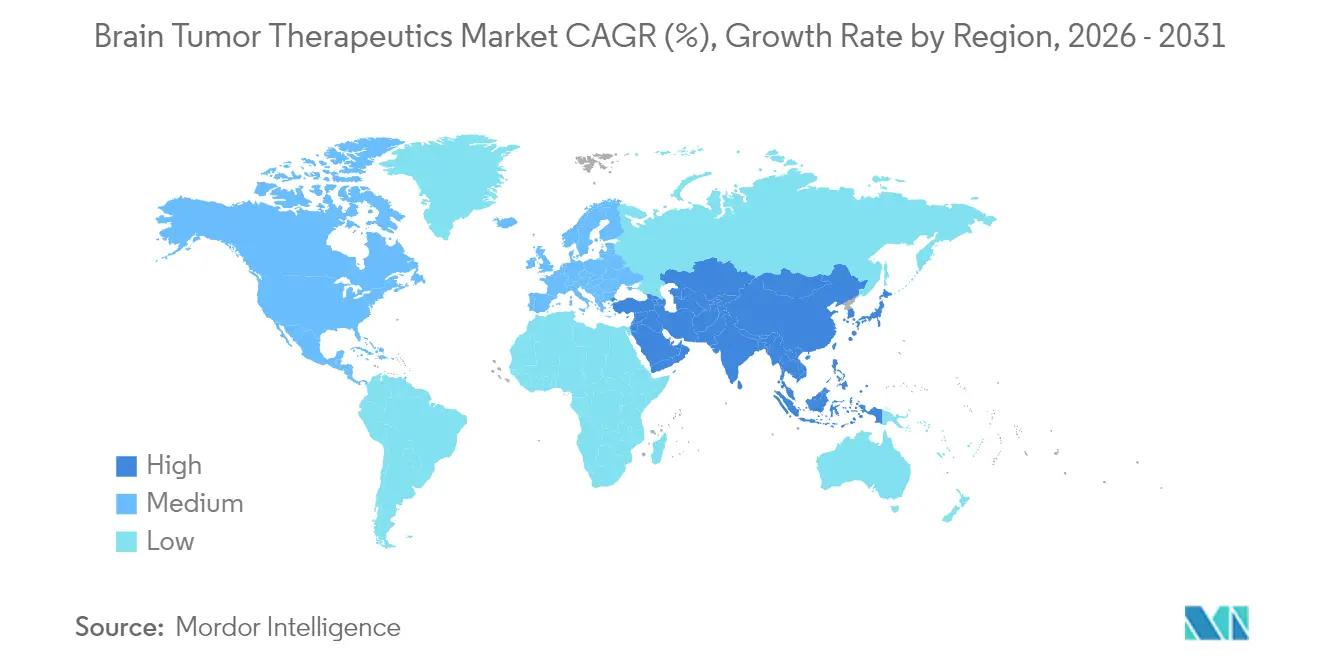

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

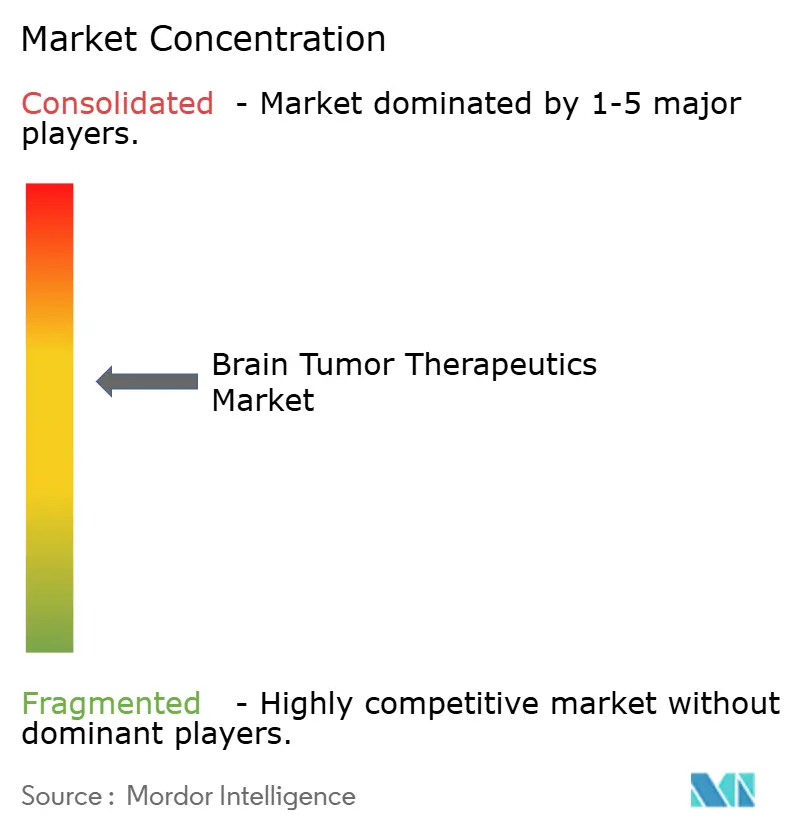

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brain Tumor Therapeutics Market Analysis by Mordor Intelligence

The brain tumor therapeutics market size is expected to grow from USD 3.19 billion in 2025 to USD 3.42 billion in 2026 and is forecast to reach USD 4.87 billion by 2031 at 7.35% CAGR over 2026-2031. Robust growth reflects the convergence of precision-medicine breakthroughs, fast-track approvals, and a steady pipeline of late-stage assets that shorten the bench-to-bedside journey. The commercial roll-out of Boron Neutron Capture Therapy (BNCT) alongside AI-enabled drug-repurposing tools is shifting therapeutic expectations, particularly for glioma and other high-grade tumors. Intravenous regimens still dominate clinical practice because they allow tight pharmacokinetic control, yet oral targeted agents are gaining traction as blood–brain barrier solutions improve. Investors continue to funnel record sums into neuro-oncology, with large biopharma groups allocating more than USD 53 billion to neurological assets in the past two years. However, radio-isotope supply chain disruptions and elevated therapy costs temper near-term momentum.

Key Report Takeaways

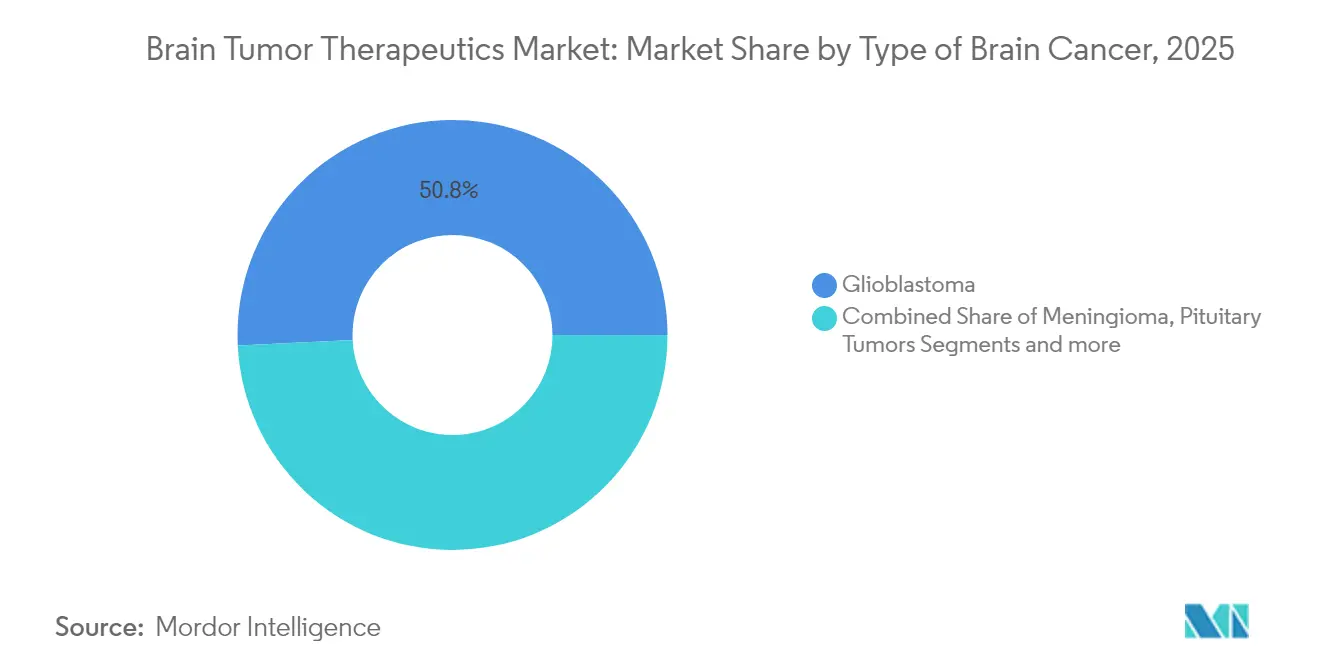

- By cancer type, glioblastoma led with 50.78% of brain tumor therapeutics market share in 2025, while it is also poised for the fastest 8.02% CAGR through 2031.

- By therapy, immunotherapy held 32.10% revenue share in 2025; targeted small-molecule treatments are projected to post the highest 8.10% CAGR to 2031.

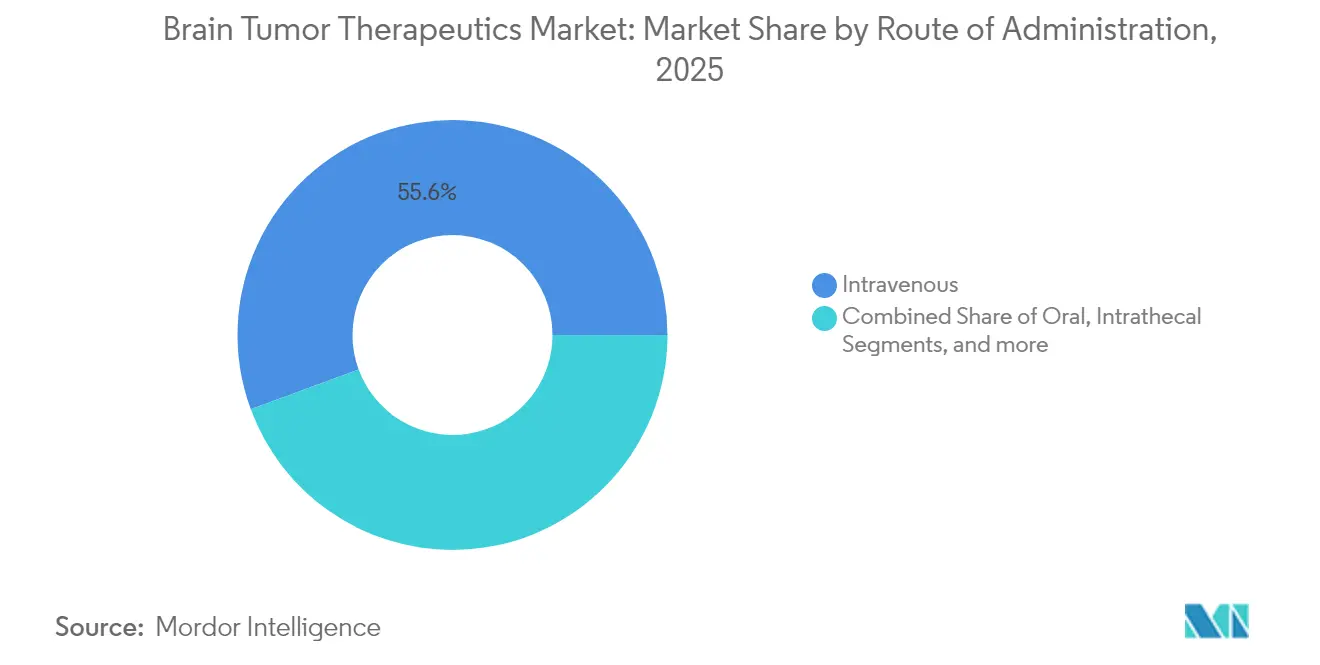

- By route of administration, the intravenous segment commanded 55.62% share of the brain tumor therapeutics market size in 2025.

- By geography, North America accounted for 39.88% revenue share in 2025, whereas Asia-Pacific is forecast to rise at an 8.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Brain Tumor Therapeutics Market*

| Driver | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of primary & metastatic brain tumors | +1.8% | Global | Medium term (2-4 years) |

| Late-stage pipeline expansion & accelerated FDA approvals | +2.1% | North America & EU, spill-over to APAC | Short term (≤ 2 years) |

| Precision-medicine shift toward biomarker-guided therapies | +1.6% | Global; early gains in US, Germany, Japan | Medium term (2-4 years) |

| Government-sponsored brain cancer initiatives & funding boosts | +1.2% | North America & EU core | Long term (≥ 4 years) |

| BNCT commercial roll-out momentum | +0.9% | APAC core; spill-over to MEA | Long term (≥ 4 years) |

| AI-enabled drug-repurposing accelerates orphan-tumor candidates | +1.4% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Late-stage pipeline expansion & accelerated FDA approvals

Regulatory speed continues to reshape the brain tumor therapeutics market. Vorasidenib’s 2024 approval for grade 2 IDH-mutant glioma doubled median progression-free survival versus placebo, validating biomarker-guided development paths[1]Drugs.com, “FDA Approves Vorasidenib for Low-Grade Glioma,” drugs.com. Breakthrough therapy designations are compressing timelines, while investigational device exemptions now cover novel radiotherapy platforms such as Alpha DaRT’s radium-224 seeds for recurrent glioblastoma. Collective momentum shortens commercialization cycles and encourages multi-arm master trials that match molecular subsets with targeted agents.

Precision-medicine shift toward biomarker-guided therapies

Routine testing for IDH mutation, MGMT promoter methylation, and 1p/19q codeletion now guides regimen selection in leading centers. Liquid biopsy platforms provide real-time molecular readouts, allowing therapy switches before radiographic progression. Machine-learning algorithms integrating multi-omics profiles already predict immunotherapy responses with 90%+ accuracy, a capability that is refining eligibility criteria for checkpoint blockade.

Commercial roll-out of compact BNCT platforms

Japan has moved Boron Neutron Capture Therapy from experimental use to routine hospital service by installing compact accelerator-based neutron sources that replace the large research reactors used in earlier trials. More than 500 patients have already received the therapy, establishing a first real-world safety and efficacy record for the modality . Clinical programs are now extending beyond recurrent head-and-neck tumors to brain malignancies, helped by next-generation boron carriers such as peptide-conjugated compounds that accumulate more selectively in tumor tissue. Parallel Monte Carlo studies show that redesigned neutron generators can reach thermal-to-epithermal flux ratios that match IAEA treatment guidelines, a technical milestone that opens the door to broader disease applications and installation in regional cancer centers.

AI-assisted drug repurposing for orphan brain tumors

Machine-learning platforms that screen legacy compound libraries against multi-omics cancer datasets are compressing the discovery timeline for rare brain-tumor therapeutics from decades to only a few years. Pattern-recognition algorithms have already highlighted new uses for familiar molecules, including the repositioning of the anthelmintic mebendazole for glioblastoma, now protected in a recent patent filing. Model accuracy keeps improving as training sets combine genomic, transcriptomic and real-world treatment-outcome data, allowing developers to forecast drug response at the tumor-subtype level with high confidence. The approach is especially valuable for ultra-rare brain tumors whose small patient pools make conventional prospective trials impractical; AI-guided repurposing supplies clinically actionable candidates while minimizing both cost and time.

Restraints Impact Analysis of Brain Tumor Therapeutics Market*

| Restraint | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of novel therapeutics & combination regimens | -1.4% | Global | Short term (≤ 2 years) |

| Blood–brain barrier limits small-molecule & biologic penetration | -1.1% | Global | Medium term (2-4 years) |

| Tumor micro-environment driven immunotherapy resistance | -0.8% | Global | Medium term (2-4 years) |

| Radio-isotope supply shortages for BNCT facilities | -0.6% | APAC core; emerging in North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High cost of novel therapeutics & combination regimens

First-in-class cell and gene therapies often exceed USD 400,000 per course, while multi-agent combinations can add another USD 300,000 annually, straining payer budgets. Health systems now link reimbursement to real-world outcomes, creating coverage delays that limit early adoption in lower-income settings.

Blood–brain barrier limits small-molecule & biologic penetration

Only 2% of systemic molecules reach therapeutic concentrations in the brain, forcing reliance on high doses that raise systemic toxicity. Focused ultrasound, convection-enhanced delivery, and nanoparticle carriers are progressing, yet capital intensity and specialized training slow rollout beyond tertiary centers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Brain Tumor Therapeutics Market Segment Analysis

By Type of Brain Cancer:

Glioblastoma drives innovation despite therapeutic hurdlesGlioblastoma held 50.78% of brain tumor therapeutics market share in 2025 and is projected to grow at an 8.02% CAGR, sustaining the largest slice of the brain tumor therapeutics market size through 2031. High mortality, limited standard-of-care options, and the emergence of tumor-treating fields help maintain investor focus.

Continued device-drug pairings, peptide vaccines, and IDH-selective inhibitors illustrate capital concentration in this segment. Meningioma follows in value terms thanks to refined radiosurgery protocols, whereas pituitary tumors benefit from novel endocrine modulators that normalize hormone levels more predictably. Pediatric-leaning subtypes such as medulloblastoma and ependymoma now integrate risk-adapted radiotherapy with molecular diagnostics, improving five-year survival yet leaving relapsed disease an urgent research priority.

By Therapy:

Targeted small molecules overtake immunotherapy in growth paceImmunotherapy commanded 32.10% revenue in 2025 and remains integral for high-mutational-burden tumors. Nonetheless, the precision-led approval wave now positions targeted small-molecule therapy as the fastest-growing category at an anticipated 8.10% CAGR, reflecting the brain tumor therapeutics market’s appetite for orally dosed, biomarker-matched agents.

Chemotherapy endures as adjuvant or salvage therapy, but dose-dense regimens face replacement as mutation-specific inhibitors gain reimbursement. Gene and cell therapies introduce curative potential yet confront scalability and cost. Meanwhile, radiotherapeutic adjuncts such as BNCT are expanding beyond head and neck indications, reinforcing multi-modal protocols.

By Route of Administration:

Intravenous remains dominant amid delivery innovationThe intravenous segment covered 55.62% of the brain tumor therapeutics market size in 2025 and should rise at an 7.90% CAGR through 2031. Clinicians rely on IV delivery for precise dose titration and real-time toxicity management in narrow therapeutic index drugs.

Oral targeted agents are scaling thanks to improved permeability and patient convenience, while intrathecal and intraventricular methods see niche use in leptomeningeal spread. Convection-enhanced delivery trials demonstrate 100-fold higher tumor concentrations versus systemic infusion, yet technical complexity confines it to referral centers.

Geography Analysis

North America Brain Tumor Therapeutics Market

North America maintained 39.88% market share in 2025 and enjoys unrivaled clinical-trial density, genomic testing adoption, and payer mechanisms that expedite new product uptake. The region’s large installed base of Gamma Knife and BNCT systems supports combination regimens, and philanthropic funding from the Biden Cancer Moonshot sustains translational research programs.

Europe Brain Tumor Therapeutics Market

Europe follows with steady contributions as EMA centralized approvals streamline access across member states, and public–private partnerships co-finance orphan-tumor projects. Germany, France, and Italy collectively host more than 120 ongoing brain tumor interventional studies, while pan-European registries supply real-world evidence to health technology assessment agencies.

APAC Brain Tumor Therapeutics Market

Asia-Pacific, the fastest-growing region at 8.12% CAGR, benefits from China’s regulatory modernization, where 60+ innovative drugs won clearance under accelerated pathways in 2024. Japan’s early BNCT adoption makes the country a regional referral hub, and Australian institutions leverage favorable ethics timelines to recruit international patients. Improving reimbursement frameworks in South Korea and Singapore further broaden patient access to leading-edge regimens.

Regulatory Landscape

Regulatory activity in brain tumor therapeutics is increasingly anchored in biomarker-defined labels and expedited pathways for high-unmet-need neuro-oncology indications. In the United States, the FDA approval of VORANIGO (vorasidenib) in August 2024 for grade 2 IDH1/IDH2-mutant glioma (including patients aged 12 years and older) reinforced mutation-guided development and supported standardized IDH testing in treatment pathways. The FDA has also used accelerated approval in ultra-rare brain tumors, including the August 2025 accelerated approval of Modeyso (dordaviprone) for recurrent H3 K27M-mutant diffuse midline glioma (patients aged 1 year and older), increasing the emphasis on confirmatory study commitments in commercialization planning.

In Europe, centralized review continues to shape access across member states through European Commission decisions supported by EMA assessments. The European Commission granted marketing authorization for Voranigo in September 2025, and in April 2026 granted conditional marketing authorization for Ojemda (tovorafenib) for pediatric low-grade glioma with specific BRAF alterations (from 6 months of age), illustrating how conditional authorization can enable earlier access on less comprehensive datasets for unmet medical need. Separately, proposed US legislative activity (S. 4739) directs the FDA Commissioner to issue guidance within one year of enactment aimed at minimizing exclusion of brain tumor patients from clinical trials for other indications, signaling a policy push toward broader trial access and eligibility modernization.

Competitive Landscape

Competition is intense yet moderately concentrated, with global pharmaceutical leaders and nimble biotechs racing to secure first-in-class labels. Novartis, Roche, and Bristol-Myers Squibb leverage diversified pipelines and precision-oncology expertise to anchor the high-value glioma franchise. Novocure captured the tumor-treating fields niche after demonstrating overall-survival gains in multiple randomized trials.

Acquisition activity is brisk. Merck’s USD 30 million purchase of Modifi Biosciences delivered a DNA-damage enhancer designed to circumvent temozolomide resistance. Bristol-Myers Squibb’s USD 4.1 billion move for RayzeBio secured an actinium-225 radiopharmaceutical platform, though global isotope shortages threaten supply consistency[4]Fierce Pharma, “Radiopharmaceutical Supply Headwinds Stall Clinical Programs,” fiercepharma.com.

Developers also chase rare-tumor white space, where competitive density remains low and regulators offer priority review vouchers. Companies with adaptive trial capabilities and patient-advocacy alliances secure faster enrollment and differentiated real-world datasets that bolster reimbursement dossiers.

Brain Tumor Therapeutics Industry Leaders

Bayer AG

F. Hoffmann-La Roche Ltd

Eisai Inc.

Novartis AG

Merck & Co. Inc.

- *Disclaimer: Major Players sorted in no particular order

Brain Tumor Therapeutics Market Companies Covered in this Report

- Amgen

- AstraZeneca

- Bayer

- Bristol-Myers Squibb

- Eisai

- Roche

- GlaxoSmithKline

- Johnson & Johnson

- Merck

- Novartis

- Pfizer

- Novocure Ltd.

- Celldex Therapeutic

- Kintara Therapeutics

- DelMar Pharmaceuticals

- Abbvie

- Daiichi Sankyo Co., Ltd.

- Sumitomo Heavy Industries (BNCT Systems)

- Neutron Therapeutics

- TAE Life Sciences

Market Opportunities and Future Outlook

The move toward genotype-defined subpopulations (IDH, H3 K27M, BRAF) is expanding commercial whitespace in earlier-line and pediatric settings where conventional chemotherapy and radiotherapy leave high relapse risk. Recent approvals such as VORANIGO (vorasidenib) for grade 2 IDH-mutant glioma (FDA, August 2024; European Commission authorization, September 2025) and Modeyso (dordaviprone) for recurrent H3 K27M-mutant diffuse midline glioma (FDA accelerated approval, August 2025) are increasing the routine use of molecular profiling in care pathways, which improves patient identification for targeted agents and supports development of adjacent companion diagnostic and testing services.

Glioblastoma continues to be a key opportunity area because standard regimens face blood-brain barrier limitations and immunotherapy resistance, driving demand for modalities with differentiated delivery or immune activation. In 2026, clinical and translational outputs highlighted multiple approaches under active investigation, including a July 2026 Journal of Clinical Oncology publication from IN8bio reporting Phase 1 data for INB-200 (DeltEx DRI) with progression-free survival of 16.1 months in repeat-dose glioblastoma patients versus 6.9 months for standard of care, alongside academic work on personalized neoantigen vaccine strategies and viral immunotherapy concepts. At the same time, the roll-out of BNCT infrastructure, particularly in Japan where more than 500 patients have received BNCT across real-world use, supports a longer-term pathway for radiotherapy adjunct uptake, while also emphasizing supply-chain constraints around radioisotopes that create openings for alternative production, logistics, and facility-side reliability solutions.

Recent Industry Developments in Brain Tumor Therapeutics Market

- July 2026: IN8bio published Phase 1 data for its gamma-delta T cell therapy candidate INB-200 (DeltEx DRI) in the Journal of Clinical Oncology, reporting progression-free survival of 16.1 months in repeat-dose glioblastoma patients compared with 6.9 months for standard of care. The readout supports the clinical rationale for cell-therapy approaches that address glioblastoma resistance mechanisms and backs continued partnering interest around scalable manufacturing and combination strategies.

- March 2025: Bayer entered into a global license agreement with Suzhou Puhe BioPharma for the oral PRMT5 inhibitor BAY 3713372, designed for brain penetration and under investigation for primary brain tumors and central nervous system metastases. The deal expands the set of brain-penetrant small-molecule candidates in development and points to continued large-pharma investment aimed at overcoming blood-brain barrier constraints.

- August 2024: The FDA approved VORANIGO (vorasidenib) for adults and pediatric patients aged 12 years and older with grade 2 astrocytoma or oligodendroglioma with IDH1 or IDH2 mutations. This approval established a targeted option in a biomarker-defined glioma population and reinforced broader adoption of molecular testing as a gatekeeper for treatment selection.

Brain Tumor Therapeutics Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers revenues generated from therapies used to treat brain tumors, where the intent is to shrink, control, or eliminate tumor growth in the brain. It includes approved drug treatments and established therapy modalities used in neuro-oncology care across major geographies.

Scope exclusions: diagnostic imaging and biopsy services, along with supportive or palliative medicines not intended to treat the tumor, are excluded.

Segments Covered in This Report

- By Type of Brain Cancer

- Glioblastoma

- Meningioma

- Pituitary Tumors

- Ependymoma

- Medulloblastoma

- Other Rare Tumors

- By Therapy

- Chemotherapy

- Immunotherapy

- Gene & Cell Therapy

- Targeted Small-Molecule Therapy

- Tumor-Treating Fields (TTF) & Electro-therapy

- Radiotherapy Adjuncts

- By Route of Administration

- Oral

- Intravenous

- Intrathecal / Intraventricular

- Convection-Enhanced Delivery

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the disease and treatment context, then to build a consistent demand pool that can be tracked over time. We relied on public sources such as the World Health Organization, the US National Cancer Institute and SEER-style cancer statistics, the International Agency for Research on Cancer (GLOBOCAN), and peer-reviewed clinical literature indexed on PubMed to understand incidence, subtype mix, and lines of therapy.

For pricing and access signals, we also reviewed FDA and EMA public drug labels, national reimbursement or formulary references where available, and audited company filings and investor materials discussing key oncology products. In a few places, paid company financials and an intelligence subscription, plus a patent database subscription, were used to cross-check pipeline direction and avoid missing material launches. The examples above are not exhaustive, and many other public sources were referenced for data collection, validation, and additional research clarification.

Primary Interviews and Surveys

Primary interviews and surveys were used to pressure-test the desk assumptions, especially around treatment sequencing, real-world adoption, and how quickly newer modalities move from specialist centers to broader use. We spoke with a mix of neuro-oncology clinicians, hospital and specialty pharmacy stakeholders, payers, and industry participants across major regions, so the final model reflects both clinical practice and commercial reality.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 14% | APAC: 50% |

| Mid tier: 57% | Functional/Unit leaders: 26% | EMEA: 31% |

| Smaller Players: 15% | Managers: 60% | Americas: 19% |

Market-Sizing & Forecasting

Market sizing was built using a top-down demand pool reconstruction, where epidemiology is translated into treated patients and then into therapy value by applying therapy mix and typical pricing levels. For brain tumor therapeutics, the key inputs include incidence and prevalence by major tumor types, the share of patients receiving systemic therapy, the split of first-line versus later-line treatment, the adoption curve of newer targeted and immunotherapy options, and average treatment duration patterns, which often differ for glioblastoma versus slower-growing tumors.

To keep the totals realistic, we corroborated results with selective bottom-up approximations such as sampled product revenue disclosures where available, channel checks with hospital and specialty pharmacies, and sanity checks on price ranges from public labels and reimbursement references. Where data was thin for smaller geographies, gaps were handled by using region-level treatment rate proxies and then adjusting them through expert feedback on access and referral pathways.

For forecasting, scenario analysis was used with a base case informed by expected diagnosis growth, likely approval timing for late-stage assets, and expected changes in treatment mix. These variables were reviewed with primary experts so the forecast reflects adoption lags rather than relying on clinical-trial optimism alone.

Data Validation & Update Cycle

Validation was done through multiple passes so the final numbers align with real market signals, not just one dataset. We compared outputs against independent checks such as cancer case trends, therapy utilization patterns discussed in clinical sources, and observed pricing direction for key modalities, and then investigated any sharp jumps before sign-off.

Where variances remained, assumptions were revisited and follow-up outreach was triggered to clarify the specific driver, for example a shift in treatment duration or faster adoption of a modality in a given region. Reports are refreshed annually, and interim updates are made when material events happen, such as major approvals, safety warnings, or reimbursement changes. Before delivery, an analyst performs a final refresh pass so clients receive the latest updated view.

Mordor Intelligence's Brain Tumor Therapeutics Market Size Compared Against Other Published Estimates

Published market sizes for brain tumor therapeutics often differ because the counted therapy set is not always the same, and the treated patient pool can be built using different clinical assumptions. Differences also show up when one publisher uses faster adoption curves for newer modalities, or when currency timing and pricing updates are not aligned to the same year.

Supportive medicines such as anti-emetics sit outside Mordor Intelligence's scope, which is one practical reason its 2025 total can look higher than drug-only figures yet lower than studies that quietly add broader oncology supportive spend. Another common gap driver is whether device-based tumor treating fields and radiotherapy adjunct revenues are counted, along with how quickly later-line use is assumed to expand beyond specialist centers.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.19 B (2025) | |

| Global Consultancy A | USD 2.79 B (2025) | Uses a narrower drugs-only view in many sections and does not clearly account for device-based therapy revenues, which can compress the total even when tumor incidence assumptions are similar. |

| Industry Publisher B | USD 2.29 B (2025) | Focuses on brain tumor drugs and typically excludes non-drug modalities, and it can also understate value when treatment duration and later-line uptake are simplified to one average across tumor types. |

The spread in published values is mainly explained by what is counted as a therapy revenue stream and how treatment duration and adoption are handled for high-grade tumors versus slower-growing ones. With clear inclusions, traceable inputs, and practical cross-checks, the model gives a number that can be repeated and adjusted as new approvals and utilization patterns emerge.

Key Questions Answered in the Report

What is the current value of the brain tumor therapeutics market?

The market generated USD 3.42 billion in 2026 and is on track to reach USD 4.87 billion by 2031, growing at a 7.35% CAGR.

Which cancer type contributes the most revenue?

Glioblastoma contributes the highest revenue, accounting for 50.78% of the 2025 market and expanding at an 8.02% CAGR through 2031.

Why are targeted small-molecule therapies gaining pace?

Biomarker-matched small molecules, such as IDH inhibitors, deliver oral convenience and improved efficacy, making them the fastest-growing therapy class at 8.10% CAGR.

Which region offers the most rapid growth opportunity?

Asia-Pacific is the fastest-growing region with an 8.12% CAGR, supported by accelerated approvals in China and BNCT adoption in Japan.

What factors limit treatment success despite new approvals?

High therapy costs, blood–brain barrier penetration limits, and supply constraints for radio-isotopes restrain broader patient access and consistent treatment outcomes.

How concentrated is the competitive landscape?

The market earns a concentration score of 6, indicating moderate dominance by the top five firms while allowing room for innovative biotechs to secure share.

Page last updated on: