Blood Brain Barrier Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

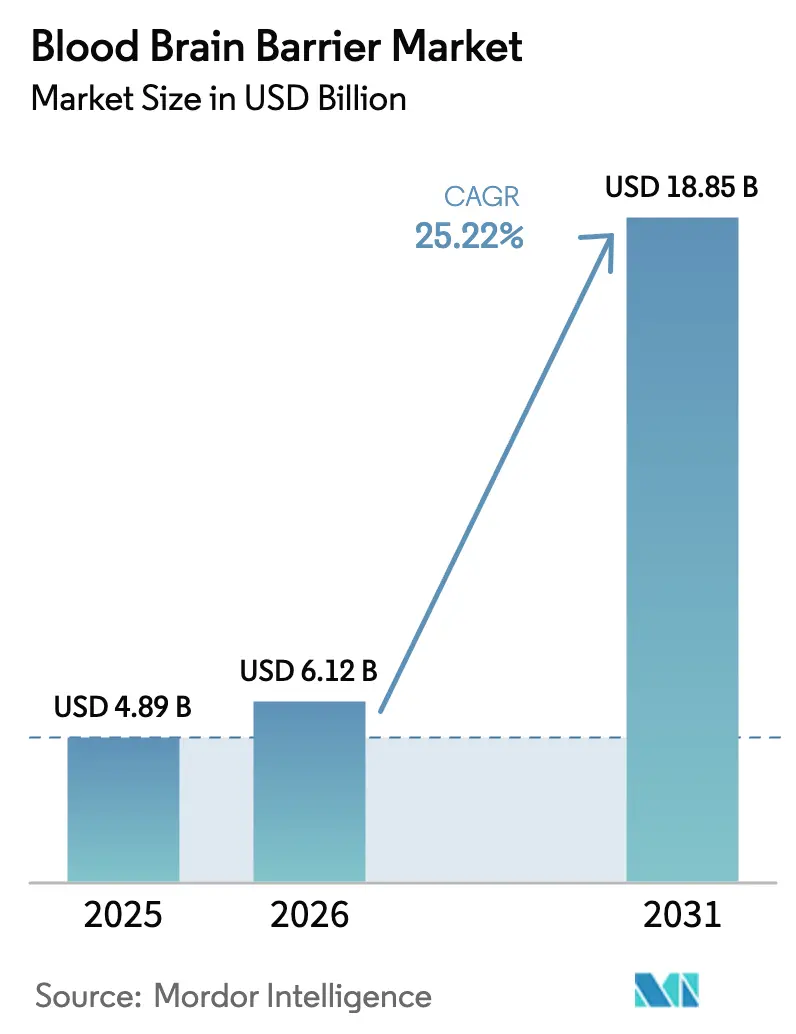

| Market Size (2026) | USD 6.12 Billion |

| Market Size (2031) | USD 18.85 Billion |

| Growth Rate (2026 - 2031) | 25.22% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Blood Brain Barrier Market Analysis by Mordor Intelligence

Blood Brain Barrier Market size in 2026 is estimated at USD 6.12 billion, growing from 2025 value of USD 4.89 billion with projections showing USD 18.85 billion, growing at 25.22% CAGR over 2026-2031.

This momentum is powered by biopharma’s pivot from broad systemic therapies toward precision CNS payloads that breach endothelial tight junctions via receptor-mediated transcytosis, focused ultrasound, and nanocarrier platforms. Large-molecule programs that once stalled in preclinical stages now enter pivotal trials for Alzheimer’s disease, Parkinson’s disease, and glioblastoma, expanding the accessible patient pool. Capital deployment into BBB-modulation startups has tightened the discovery-to-commercialization loop, while regulatory incentives, including FDA breakthrough therapy and EMA PRIME designations, have shortened approval timelines. Competitive intensity is growing as big-cap pharma licenses specialized shuttle technologies, yet the landscape remains fragmented, creating room for mid-cap innovators.

Key Report Takeaways

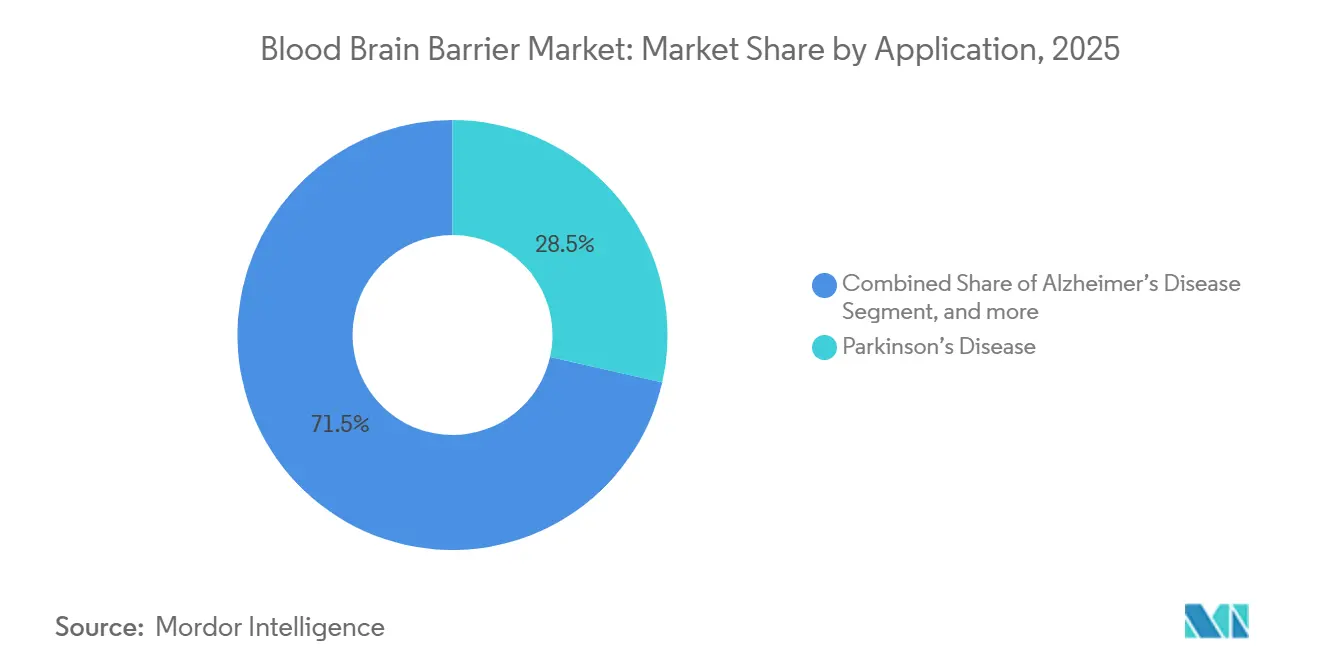

- By application, Parkinson’s disease held 28.54% of the blood brain barrier market share in 2025, while brain cancer is forecast to expand at a 27.43% CAGR through 2031.

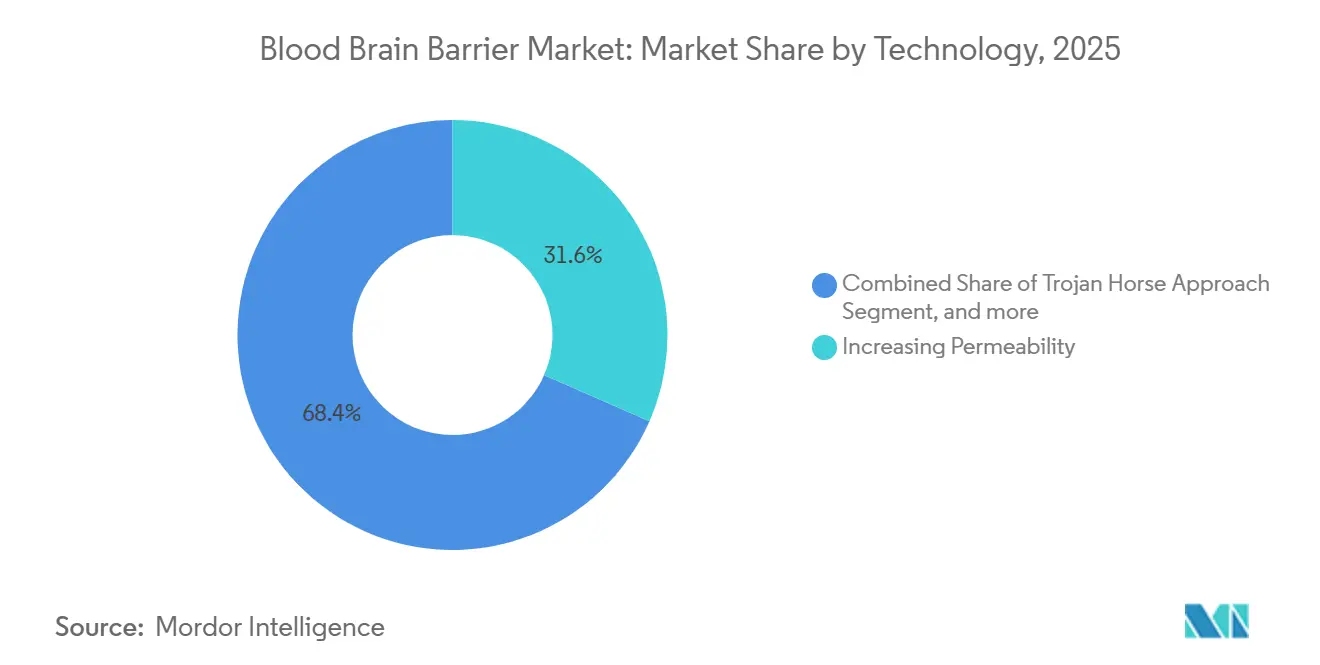

- By technology, increasing permeability methods captured 31.57% of the blood brain barrier market share in 2025; bispecific antibody receptor-mediated transcytosis is projected to grow at a 26.99% CAGR to 2031.

- By end user, hospitals led with a 46.87% revenue share in 2025, whereas surgical centers are advancing at a 27.65% CAGR through 2031.

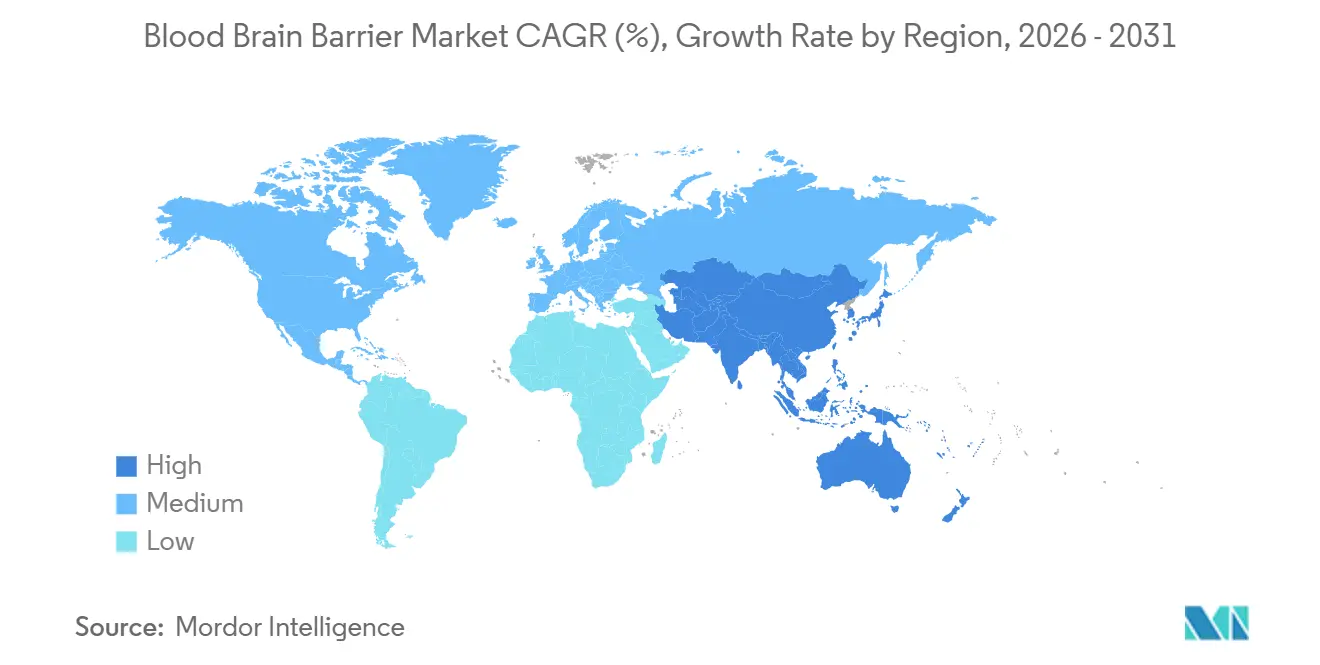

- By geography, North America accounted for 42.54% of blood brain barrier market share in 2025, while Asia-Pacific is set to expand at 26.43% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Blood Brain Barrier Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Neurological Disease Burden | 6.2% | Global, with highest prevalence in North America and Europe | Long term (≥ 4 years) |

| Rising R&D Investments in CNS Delivery Technologies | 5.8% | North America, Europe, Asia-Pacific core | Medium term (2-4 years) |

| Advances in Drug Delivery Nanotechnology | 4.9% | Global, with manufacturing hubs in North America and Asia-Pacific | Medium term (2-4 years) |

| Expansion of Focused-Ultrasound BBB Modulation Clinics | 3.7% | North America and Europe, spillover to Asia-Pacific | Short term (≤ 2 years) |

| Orphan-Drug and Rare-Disease Regulatory Incentives | 2.4% | North America, Europe (EMA), Japan | Short term (≤ 2 years) |

| Growing Adoption of Digital Biomarker Platforms for BBB Integrity | 1.6% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Neurological Disease Burden

Neurological disorders continue to rise, with Parkinson’s disease affecting more than 10 million people worldwide and Alzheimer’s disease projected to reach 152 million cases by 2050. Existing symptomatic regimens fall short of altering disease progression, prompting stakeholders to consider disease-modifying biologics that require active transport across the BBB. Glioblastoma maintains a median survival of 15 months under standard treatment, yet a 2025 Phase II protocol that paired focused ultrasound with immune-checkpoint inhibitors improved progression-free survival by 40%. Multiple sclerosis and epilepsy are fueling parallel antibody-shuttle programs, underscoring the expanding therapeutic canvas.

Rising R&D Investments in CNS Delivery Technologies

Global pharmaceutical spending on CNS delivery surged to USD 18.2 billion in 2025, up 22% from 2024. Roche directed USD 1.1 billion to its trontinemab program, Bristol-Myers Squibb committed USD 850 million to a tau-targeted pipeline, and the U.S. NIH allocated USD 320 million to BBB-modulation grants. Japan’s AMED launched a JPY 36 billion (USD 240 million) fund to accelerate the development of domestic shuttle technologies. This influx is derisking early platforms and compressing timelines to first-in-human trials.

Advances in Drug Delivery Nanotechnology

Lipid nanoparticles, polymeric micelles, and exosome carriers now deliver brain bioavailability rates above 5%, fivefold better than unmodified biologics. Pfizer reported 12% brain uptake for a Huntington’s disease candidate versus 0.8% for its unconjugated counterpart. In January 2025, Eli Lilly partnered with Precision NanoSystems to scale siRNA lipid-nanoparticle production, investing USD 180 million. The FDA’s March 2025 draft guidance on nanocarrier characterization has further reduced regulatory risk.

Expansion of Focused Ultrasound BBB Modulation Clinics

Global installations of focused ultrasound systems rose to 120 in December 2025 from 68 a year earlier[1]Focused Ultrasound Foundation, “Annual Registry 2025,” fusfoundation.org. Insightec placed 45 new Exablate Neuro units in 2025, mainly at U.S. academic centers and European oncology hubs. Combination protocols, such as trastuzumab plus ultrasound for HER2-positive brain metastases, achieved a 58% objective response in a 2025 multicenter trial. Carthera’s CE-marked SonoCloud-9 device and a new CMS billing code are accelerating outpatient adoption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Biological Complexity of BBB Limiting Drug Entry | -3.8% | Global | Long term (≥ 4 years) |

| High Development and Manufacturing Costs | -2.9% | Global, highest pressure in emerging markets | Medium term (2–4 years) |

| Safety Concerns Around Vascular Adverse Events | -1.8% | Global | Short term (≤ 2 years) |

| Limited Large-Scale CGMP Capacity for BBB-Shuttle Biologics | -2.1% | North America, Europe, Asia-Pacific | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Biological Complexity of the BBB Limiting Drug Entry

Tight junctions, efflux transporters, and enzymatic degradation restrict brain uptake of 98% of small molecules and nearly all biologics[2]Source: Nature Reviews Drug Discovery, “Barriers to CNS Drug Uptake,” nature.com. Even transferrin-receptor shuttles reach only 0.3% of plasma levels in brain tissue, as shown in a 2025 pharmacokinetic analysis of trontinemab. Efflux pumps, such as P-gp, expel lipophilic agents, and Phase II attrition in CNS trials exceeds 75%.

High Development and Manufacturing Costs

Building CGMP suites for bispecific antibodies demands more than USD 500 million per site, and the cost-of-goods can reach USD 15,000 per gram. Bioasis required CAD 420 million (USD 310 million) to scale a 2,000-liter bioreactor for its xB3 platform. This financial burden hinders programs targeting small, rare-disease populations and delays global rollout where pricing headroom is limited.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Oncology Gains as Neurodegeneration Matures

Brain cancer applications are expected to expand at a 27.43% CAGR through 2031, outpacing other segments in the blood brain barrier market. A 2025 glioblastoma trial combining focused ultrasound with pembrolizumab achieved a 12-month overall survival of 42%, more than doubling the monotherapy arm. Parkinson’s disease accounted for 28.54% of blood brain barrier market share in 2025, supported by established dopaminergic regimens and emerging gene-therapy vectors. Alzheimer’s disease pipelines gained momentum after lecanemab’s 2024 accelerated approval, galvanizing investment in bispecific anti-amyloid constructs. Multiple sclerosis and epilepsy programs employ antibody-shuttle conjugates to target intrathecal pathologies, while orphan indications such as Hunter’s syndrome and lysosomal storage disorders advance in late-stage trials.

Next-generation applications fuse BBB-shuttle strategies with cell and gene therapies. Exosome-encapsulated CRISPR-Cas9 constructs entered Phase I for Huntington’s disease in 2025, illustrating convergence across modalities. As patient stratification sharpens through digital biomarkers, precision delivery is expected to elevate clinical efficacy, supporting the blood brain barrier market size for neuro-oncology and neurodegeneration.

By Technology: Bispecific Antibodies Challenge Permeability Methods

Increasing permeability techniques—focused ultrasound, osmotic disruption, and bradykinin agonists—held 31.57% share in 2025, anchoring the blood brain barrier market size for immediate clinical adoption. Bispecific antibody shuttles are projected to grow at 26.99% CAGR, driven by transferrin- and insulin-receptor platforms now entering pivotal studies. Armagen’s AGT-181 demonstrated a 4.2-fold brain-uptake gain in 2025 Phase Ib results. Trojan-horse chemistries, exemplified by Angiochem’s ANG1005, which achieved a 38% response in leptomeningeal metastases, illustrate strong late-stage traction.

Hybrid protocols that pair ultrasound with bispecific antibodies are emerging, aiming to maximize brain exposure while minimizing systemic toxicity. Passive diffusion stays relevant for lipophilic small molecules but remains constrained by efflux transporters. Exosome and peptide-mediated pathways remain early-stage yet promise adaptable cargo capacity, maintaining technology diversity within the blood brain barrier market.

By End-User: Surgical Centers Gain as Outpatient Procedures Scale

Hospitals retained 46.87% revenue share in 2025, reflecting their multidisciplinary infrastructure for complex neuro-oncology interventions within the blood brain barrier market. Surgical centers will likely expand at 27.65% CAGR as focused ultrasound migrates to outpatient suites, lowering overhead and improving patient throughput. A 2025 ASCO survey found that 42% of U.S. neuro-oncology centers planned to adopt ultrasound in ambulatory settings by 2027. Research institutes continue to seed early-phase studies, backed by 68 NIH-funded BBB programs in 2025.

Specialty neurology clinics are adopting serum- and CSF-based BBB-integrity assays, expanding the end-user ecosystem. As procedure times fall and reimbursement clarity improves, outpatient growth will underpin incremental volumes, reinforcing the blood brain barrier market size across delivery settings.

Geography Analysis

North America commanded 42.54% of blood brain barrier market share in 2025, supported by 58 installed focused ultrasound systems in the United States and sustained NIH funding above USD 320 million. Canada is scaling national registry studies, while Mexico attracts lower-cost clinical trials. The United States hosts pivotal programs such as Roche’s trontinemab and Denali’s enzyme transport vehicle candidates, ensuring pipeline depth.

Asia-Pacific is set to grow at 26.43% CAGR to 2031, as China’s NMPA approved 12 BBB-crossing INDs in 2025 and Japan strengthened orphan-drug incentives[3]Source: National Medical Products Administration, “Annual Report 2025,” nmpa.gov.cn. South Korea’s Samsung Biologics committed USD 680 million to expand bispecific antibody capacity, reinforcing regional CGMP depth. India and Australia pursue academic-industry consortia to pilot nanocarrier programs, laying the groundwork for regional commercialization.

Europe maintains steady adoption through EMA’s PRIME scheme and national reimbursement policies. Germany’s Charité installed eight focused ultrasound systems, and the United Kingdom’s NICE issued supportive guidance for recurrent brain tumors. France, Italy, and Spain expand ultrasound capacity through EU research funding. South America and the Middle East remain nascent but active; Brazil’s University of São Paulo teamed with Insightec for three oncology installations, and the UAE is positioning itself as a regional trial hub.

Competitive Landscape

The blood brain barrier market remains fragmented, with no firm exceeding 8% share, but consolidation is accelerating as large-cap pharmaceutical companies license shuttle platforms to complement existing CNS portfolios. Roche, Pfizer, Johnson & Johnson, and Bristol-Myers Squibb collectively announced more than USD 4 billion in BBB-related deals during 2025. Denali’s enzyme transport vehicle generated a USD 1.15 billion out-licensing pact with Takeda. Device makers Insightec and Carthera have shifted toward per-procedure leasing, easing capital constraints for hospital adoption.

Patent velocity is high: the USPTO issued 142 BBB-related patents in 2025, covering bispecific constructs, ultrasound transducers, and nanoparticle surface chemistries. Academic spin-outs such as Codiak BioSciences are trialing exosome-encapsulated antibodies for frontotemporal dementia. As head-to-head trials benchmark brain uptake, safety, and patient-reported outcomes, differentiation will hinge on integrated delivery platforms rather than single-asset positioning, shaping future blood brain barrier market trajectories.

Blood Brain Barrier Industry Leaders

F. Hoffmann-La Roche AG

Bristol-Myers Squibb

Sanofi

Pfizer Inc.

Eli Lilly and Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: InnoSer, one of the leading preclinical contract research organizations (CRO), and Carthera, a clinical-stage MedTech company, announced a strategic collaboration. The partnership will offer access to Carthera’s preclinical SonoCloud platform, an innovative ultrasound-based medical device developed to support the treatment of a wide range of brain disorders, helping researchers explore new strategies for CNS-targeted therapeutics.

- November 2025: Manifold Bio, a platform therapeutics company pioneering AI-guided drug discovery coupled with direct-to-vivo measurement, announced a strategic research collaboration and license agreement with Roche (SIX: RO, ROG; OTCQX: RHHBY). The partnership will apply Manifold's proprietary tissue-targeting shuttle portfolio and mDesign AI-driven in vivo discovery engine to create multiple next-generation BBB shuttles for the treatment of neurological and neurodegenerative diseases.

- August 2025: Lantern Pharma Inc., a pioneering artificial intelligence company transforming oncology drug discovery and development, announced the public release of its AI module for predicting blood-brain barrier (BBB) permeability of small molecules with unprecedented accuracy and scalability – predictBBB.ai.

Global Blood Brain Barrier Market Report Scope

As per the scope of the report, the blood-brain barrier is a selective, protective barrier formed by endothelial cells in brain blood vessels. It restricts the passage of most substances from the bloodstream into the brain tissue. This barrier helps maintain the brain's stable environment and protects it from toxins and pathogens.

The Blood Brain Barrier Market is Segmented by Application (Alzheimer's Disease, Parkinson's Disease, Epilepsy, Multiple Sclerosis, Hunter's Syndrome, Brain Cancer, and Other Applications), Technology (Bispecific Antibody RMT Approach, Trojan Horse Approach, Increasing Permeability, Passive Diffusion, and Other Technologies), End-User (Hospitals, Surgical Centers, Research Institutes, and Other End-Users), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Alzheimer's Disease |

| Parkinson's Disease |

| Epilepsy |

| Multiple Sclerosis |

| Hunter's Syndrome |

| Brain Cancer |

| Other Applications |

| Bispecific Antibody Rmt Approach |

| Trojan Horse Approach |

| Increasing Permeability |

| Passive Diffusion |

| Other Technologies |

| Hospitals |

| Surgical Centers |

| Research Institutes |

| Other End-Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest Of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest Of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest Of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest Of South America |

| By Application | Alzheimer's Disease | |

| Parkinson's Disease | ||

| Epilepsy | ||

| Multiple Sclerosis | ||

| Hunter's Syndrome | ||

| Brain Cancer | ||

| Other Applications | ||

| By Technology | Bispecific Antibody Rmt Approach | |

| Trojan Horse Approach | ||

| Increasing Permeability | ||

| Passive Diffusion | ||

| Other Technologies | ||

| By End-User | Hospitals | |

| Surgical Centers | ||

| Research Institutes | ||

| Other End-Users | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest Of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest Of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest Of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest Of South America | ||

Key Questions Answered in the Report

What is the current size of the blood brain barrier market?

The blood brain barrier market stands at USD 6.12 billion in 2026 and is projected to reach USD 18.85 billion by 2031.

Which therapeutic area leads demand for BBB-crossing technologies?

Parkinson's disease holds the largest application share at 28.54%, though brain cancer shows the fastest projected growth.

Which technology is growing fastest for BBB delivery?

Bispecific antibody receptor-mediated transcytosis platforms are forecast to expand at 26.99% CAGR through 2031.

What region is expected to grow most rapidly?

Asia-Pacific is projected to grow at 26.43% CAGR, driven by China and Japan.

How fragmented is the competitive landscape?

No firm controls more than 8% share, and the top five hold roughly 35%, indicating moderate fragmentation.

Which end-user segment is gaining momentum?

Surgical centers are advancing at 27.65% CAGR as focused ultrasound shifts to outpatient settings.

Page last updated on: