Central Nervous System Therapeutics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

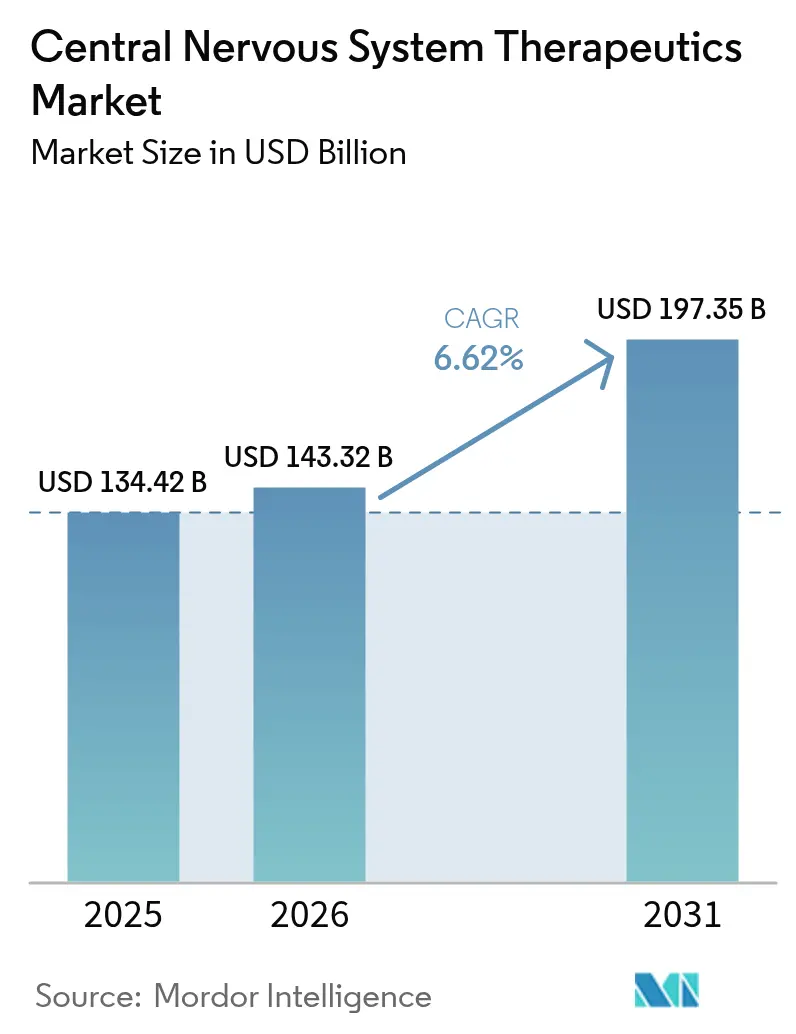

| Market Size (2026) | USD 143.32 Billion |

| Market Size (2031) | USD 197.35 Billion |

| Growth Rate (2026 - 2031) | 6.62% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Central Nervous System Therapeutics Market Analysis by Mordor Intelligence

Central nervous system therapeutics market size in 2026 is estimated at USD 143.32 billion, growing from 2025 value of USD 134.42 billion with 2031 projections showing USD 197.35 billion, growing at 6.62% CAGR over 2026-2031. Breakthrough approvals such as KarXT for schizophrenia and donanemab for Alzheimer’s disease mark a decisive shift from symptomatic control toward precision medicine that targets causal neurobiology. Intensifying payer support for disease-modifying regimens, expanding biomarker-guided diagnosis, and AI-enabled trial design collectively reinforce the expansion trajectory. Competitive momentum is heightened by high-value acquisitions that secure differentiated assets, even as generic erosion squeezes margins for mature franchises. The resulting landscape rewards companies capable of blending robust clinical evidence with real-world value propositions.

Key Report Takeaways

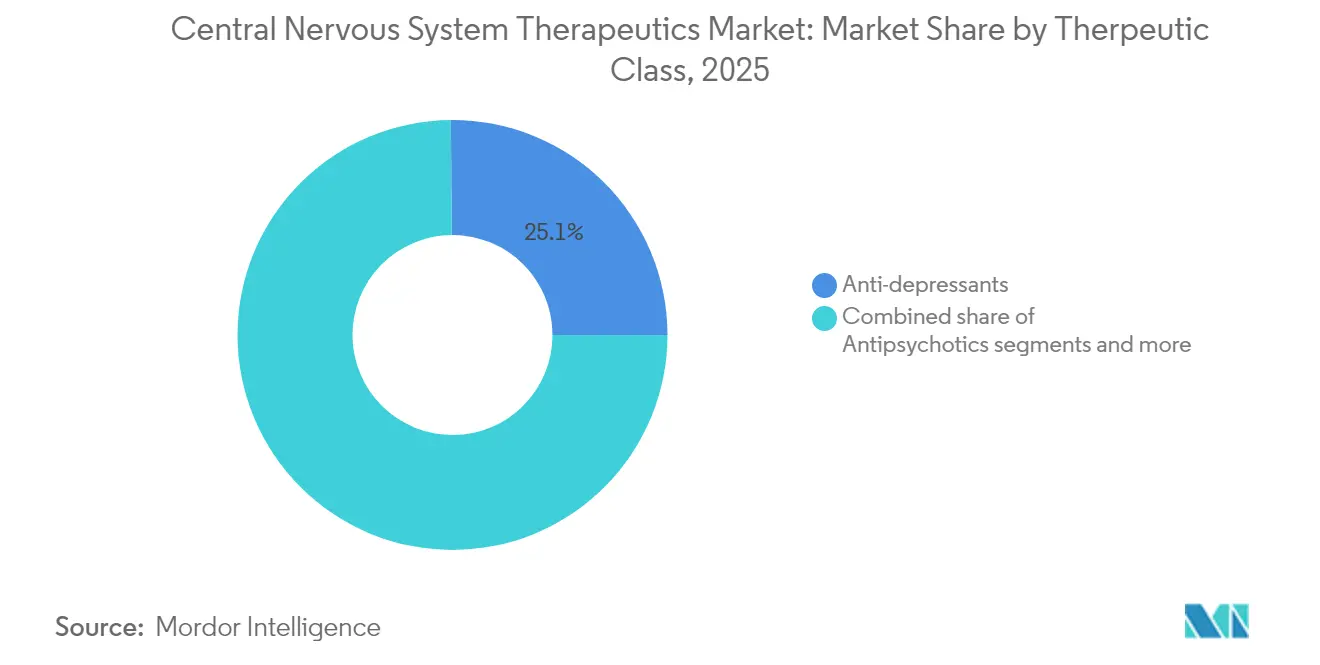

- By therapeutic class, antidepressants led with 25.12% revenue share in 2025; disease-modifying therapies are projected to grow at a 6.83% CAGR through 2031.

- By disease, depression accounted for 27.55% of the central nervous system therapeutics market share in 2025, while Alzheimer’s disease is set to climb at a 7.05% CAGR to 2031.

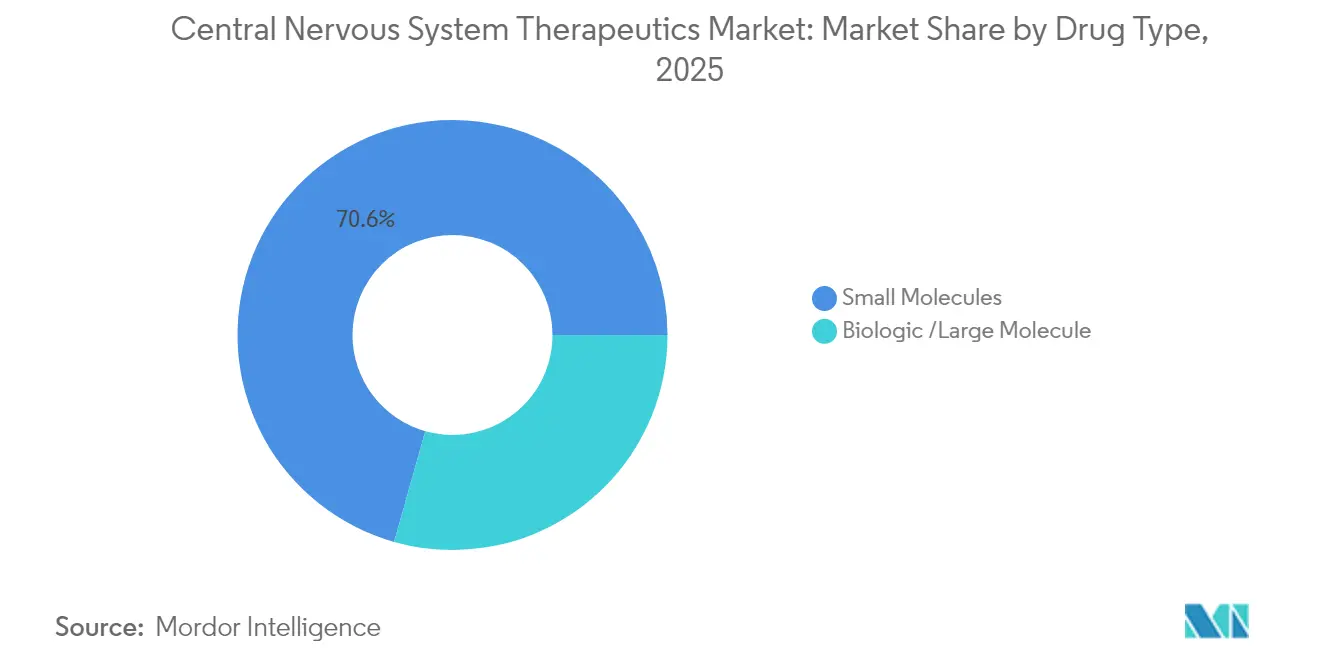

- By drug type, small molecules commanded 70.62% share of the central nervous system therapeutics market size in 2025; biologics are forecast to rise at a 7.52% CAGR during 2026-2031.

- By route of administration, oral formulations held 82.11% of the central nervous system therapeutics market size in 2025 and alternative routes are advancing at a 7.28% CAGR through 2031.

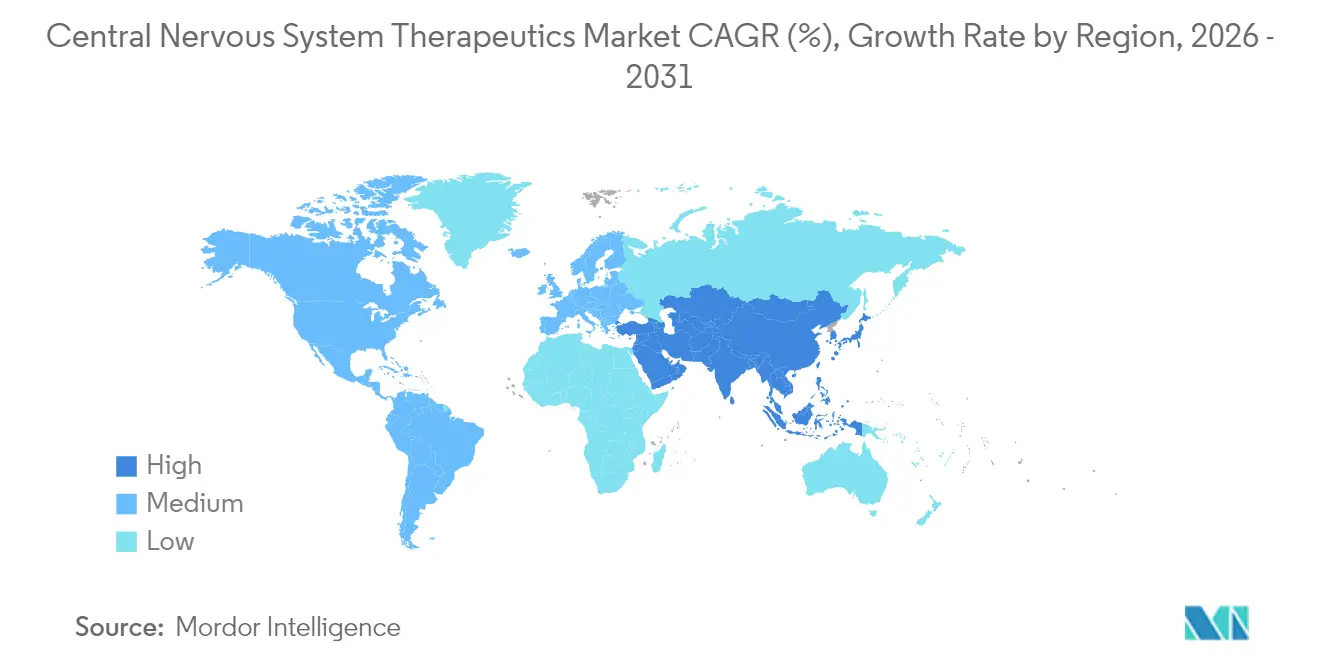

- By geography, North America retained 45.01% of the central nervous system therapeutics market share in 2025, whereas Asia-Pacific is expanding at a 7.78% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Central Nervous System Therapeutics Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging population & rising CNS disorder prevalence | +1.0% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

| Growing generic penetration post-LOE | +0.8% | Global, led by North America & Europe | Medium term (2-4 years) |

| Favorable reimbursement for breakthrough CNS drugs | +0.7% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Improved neuroimaging & biomarker-based diagnosis | +0.5% | North America & EU core, spillover to APAC | Long term (≥ 4 years) |

| Psychedelic-assisted therapy clinical wins | +0.5% | North America & EU regulatory frameworks | Short term (≤ 2 years) |

| Venture funding into CNS-focused digital twins | +0.4% | Global, concentrated in North America & EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging Population & Rising CNS Disorder Prevalence

Neurological disorders affected 3.4 billion people in 2024, making them the leading global source of disability-adjusted life years00038-3/fulltext). Incidence accelerates beyond age 65, driving sustained demand for the central nervous system therapeutics market. Annual caregiving costs for cognitive decline reached USD 1.1 trillion in developed economies, motivating payers to endorse interventions that delay institutionalization. Early diagnosis paired with disease-modifying drugs is therefore viewed as fiscally prudent by insurers. As demographic aging is irreversible over the forecast horizon, this demand vector remains the single most durable growth catalyst for the central nervous system therapeutics market.

Growing Generic Penetration Post-LOE

Lyrica generics captured 85% of prescription volume within 18 months of US exclusivity loss, illustrating how quickly price erosion strikes blockbuster CNS brands. Lower cost options widen patient access in emerging economies, swelling treated populations and cementing the central nervous system therapeutics market as a core expenditure line for public payers. Simultaneously, originators accelerate next-generation assets and novel delivery modes that command premium pricing and resist substitution, keeping innovation cycles active.

Favorable Reimbursement for Breakthrough CNS Drugs

The FDA’s Total Care for Exceptional Therapies pathway trims approval timelines by 40% for high-need CNS drugs. Medicare’s coverage of lecanemab despite modest benefit signals willingness to reimburse disease-modifying agents with clear societal value. Value-based contracts that tether payments to functional outcomes are spreading to private insurance and Asian markets, improving revenue predictability for innovators and reinforcing confidence in the central nervous system therapeutics market.

Improved Neuroimaging & Biomarker-Based Diagnosis

Blood-based tests now achieve 90% accuracy for Alzheimer’s disease, enabling earlier therapeutic intervention. PET imaging of tau and neuroinflammation supplies objective endpoints that shrink trial sizes and bolster statistical power. Regulators increasingly accept biomarker data in lieu of long-term clinical outcomes, compressing development costs. Integration of AI with multimodal imaging creates predictive models that match patients with optimal therapies, elevating success rates for pipeline programs within the central nervous system therapeutics market.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High clinical trial failure rates in neurology | -0.9% | Global, particularly impacting North America & EU | Long term (≥ 4 years) |

| Generic erosion of blockbusters (e.g., Lyrica) | -0.7% | Global, led by North America & Europe | Medium term (2-4 years) |

| Stringent CNS safety labeling requirements | -0.5% | Global regulatory frameworks | Medium term (2-4 years) |

| Supply-chain scarcity of specialized excipients | -0.3% | Global, concentrated in Asia-Pacific manufacturing | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Clinical Trial Failure Rates in Neurology

A 92% attrition rate afflicts neurological pipelines, the worst among therapeutic areas. Complex pathophysiology, blood-brain-barrier permeability hurdles, and heterogeneous patient presentations thwart translation of preclinical signals. High-profile setbacks such as emraclidine and dalzanemdor underscore persistent risk. Capital-intensive trials deter smaller firms, fostering consolidation as deep-pocketed pharmas acquire distressed assets, yet overall innovation velocity suffers, tempering the growth outlook for the central nervous system therapeutics market.

Stringent CNS Safety Labeling Requirements

Sixty percent of newly approved neurological drugs enter the market under FDA Risk Evaluation and Mitigation Strategies. EMA mandates expanded neuropsychiatric monitoring, extending development timelines by up to 18 months. Additional data collection inflates trial budgets and disproportionately burdens small developers. Though essential for patient protection, heightened vigilance elevates barriers to entry and lengthens payback periods, dampening near-term enthusiasm within the central nervous system therapeutics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapeutic Class: Disease-Modifying Therapies Scale Rapidly

The disease-modifying cohort is on track to expand at a 6.83% CAGR, outpacing all other categories inside the central nervous system therapeutics market. Antidepressants remain the volume leader at 25.12% 2025 share, sustained by widespread prescribing in primary care. Investor interest has pivoted, however, toward agents that alter disease course, exemplified by Bristol Myers Squibb’s USD 14 billion outlay for KarXT. These transactions channel capital into regenerative pathways, immunomodulation, and synaptic repair platforms.

Antipsychotics receive renewed momentum following KarXT, while antiepileptics confront steep generic penetration. Analgesics suffer margin squeeze, yet specialty migraine biologics retain pricing strength. Neurodegeneration assets attract premium valuations despite modest efficacy because any delay in progression yields sizeable societal savings. Convergence is emerging as firms test combo regimens pairing symptomatic relief with disease modification, blurring historic therapeutic silos within the central nervous system therapeutics market.

By Diseases: Alzheimer’s Disease Sets the Growth Pace

Depression kept 27.55% of 2025 revenues, but Alzheimer’s disease is forecast to post a 7.05% CAGR, the fastest among indications. Reimbursement of lecanemab and pipeline agents such as donanemab creates a multibillion-dollar addressable segment that was previously untapped. Mental-health indications also benefit from digital therapeutics that extend reach beyond traditional clinical settings.

Neurovascular disorders and rare epilepsies remain underserved niches offering orphan-drug pricing power. Infection-linked neurological sequelae and oncology crossover therapies are slowly enlarging, aided by heightened research into latent viral impacts on the CNS. These diverse disease-level dynamics reinforce multi-modal portfolio strategies inside the central nervous system therapeutics market.

By Drug Type: Biologics and Gene Therapies Quickening

Small molecules retained 70.62% of 2025 sales, yet biologics are charting a 7.52% CAGR thanks to growing acceptance of monoclonal antibodies and gene therapies. FDA nods for SOD1-ALS and AADC deficiency confirm feasibility of genetic interventions in neurology. Antibody-drug conjugates and targeted degraders merge biologic precision with small-molecule convenience, diversifying toolkits for innovators.

Investors reward platforms that surmount the blood-brain barrier, such as receptor-mediated transcytosis vectors. Meanwhile, small-molecule research shifts toward highly brain-penetrant chemistries and allosteric modulators. This complementary evolution sustains balanced growth across modalities in the central nervous system therapeutics market.

By Route of Administration: Alternatives to Oral Gain Ground

Oral dosage forms commanded 82.11% share in 2025, favored for convenience and supply-chain familiarity. Long-acting injectables and intranasal sprays, however, are registering a 7.28% CAGR by improving adherence and enabling rapid symptom control. Transdermal and implantable systems promise steady plasma levels with fewer systemic effects, creating clinical value that offsets higher costs.

Emerging intrathecal and intraventricular devices offer targeted drug deposition for spinal or intracranial pathologies. Digital device-drug hybrids that auto-adjust dosing based on biomarker feedback are entering trials, opening a future where route of administration becomes personalized rather than fixed, further enriching the central nervous system therapeutics market.

Geography Analysis

North America accounted for 45.01% of 2025 revenue, underpinned by Medicare coverage expansions and dense clinical-trial infrastructure. The United States leads with sophisticated payer frameworks that adopt value-based contracts, whereas Canada provides stable uptake through universal coverage. Mexico is emerging on the back of growing middle-class insurance penetration. Pricing pressures from generic proliferation and buyer consolidation temper revenue per patient but are offset by the premium commanded by innovative launches, sustaining leadership for the central nervous system therapeutics market.

Asia-Pacific is the growth heartbeat, projected at 7.78% CAGR, driven by China’s regulatory liberalization, Japan’s fast-track approvals, and India’s expanding access programs. Rapid urbanization correlates with higher incidence of mood and anxiety disorders, unlocking volume. Japan and South Korea anchor regional clinical trials, while Southeast Asian nations import affordable generics to widen coverage. Government recognition of neurological disease burden is translating into reimbursement reforms that uplift market value, positioning the region as a pivotal expansion arena for the central nervous system therapeutics market.

Europe delivers steady gains through EMA-coordinated pathways and universal healthcare. Germany and the United Kingdom dominate launches due to robust assessment agencies, whereas southern European markets contribute scale. The new Clinical Trials Information System streamlines submissions, slightly trimming timelines. Cost-effectiveness scrutiny remains stringent, sometimes delaying premium products, yet predictable reimbursement decisions create long-tail revenue stability. Collectively, these continental patterns diversify growth drivers and risk profiles for stakeholders in the central nervous system therapeutics market.

Competitive Landscape

The central nervous system therapeutics market is moderately fragmented, featuring pharmaceutical majors alongside agile biotechs. Consolidation accelerated in 2024 when Bristol Myers Squibb paid USD 14 billion for Karuna Therapeutics[1]Source: Bristol Myers Squibb, “Karuna Therapeutics acquisition,” bms.com and AbbVie invested USD 2 billion in Gilgamesh Pharmaceuticals. These valuations underscore investor appetite for assets with novel mechanisms and solid Phase 2 data. Large companies are pursuing platform acquisitions that unlock multi-indication pipelines rather than single-asset deals.

Digital and data-science capabilities are now central to differentiation. Unlearn.AI’s USD 50 million raise to expand digital twins for neurology trials illustrates how AI startups can influence drug-development economics[2]Source: Unlearn.AI, “Unlearn raises USD 50 million Series B,” unlearn.ai . Established players integrate such tools to shorten cycle times and de-risk investment. Simultaneously, gene-therapy specialists obtain priority review vouchers that attract big-pharma partnerships, enriching cash and expertise pools while maintaining scientific autonomy.

Rare-disease focus and psychedelic medicine represent white-space frontiers. Gene-editing firms pursuing Huntington’s disease and antisense companies targeting ALS have attracted multibillion-dollar transactions with Novartis and Biogen. Psychedelic-assisted therapy platforms benefit from increasing regulatory openness, drawing mainstream capital. Competitive intensity is expected to heighten as proof-of-concept readouts convert scientific curiosity into commercial reality within the central nervous system therapeutics market.

Central Nervous System Therapeutics Industry Leaders

Biogen

Novartis AG

Merck KGaA

Eli Lilly and Company

Johnson & Johnson

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Biogen received conditional Health Canada approval for QALSODY (tofersen) as the first SOD1-ALS therapy

- January 2025: Eisai updated the EU regulatory status of lecanemab, with the European Commission requesting additional safety data

Global Central Nervous System Therapeutics Market Report Scope

As per the scope, the central nervous system (CNS) consists of the brain and spinal cord. It controls things like thought, movement, and emotion, as well as breathing, heart rate, hormones, and body temperature. The drugs that act on the functions of the brain and spinal cord are central nervous system therapeutics. The central nervous system therapeutics market is segmented by Disease (Neurovascular Diseases, Trauma, Mental Health, Degenerative Disease, Infectious Diseases, Cancer, and Others), Drug Class (Analgesics, Antidepressants, Anesthetics, Anti-Parkinson Drugs, Anti-Epileptics, and Other Drug Classes), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Antidepressants |

| Antipsychotics |

| Antiepileptics |

| Analgesics (Neuropathic & Migraine) |

| Disease-Modifying (MS, ALS, etc.) |

| Neurodegeneration (AD, PD) |

| Others |

| Neurovascular Diseases | |

| Trauma | |

| Mental Health | Anxiety Disorders |

| Epilepsy | |

| Psychotic Disorders | |

| Other Mental Health Disorders | |

| Degenerative Diseases | Alzheimer's Disease |

| Parkinson's Disease | |

| Multiple Sclerosis | |

| Amyotrophic Lateral Sclerosis | |

| Other Degenerative Diseases | |

| Infectious Diseases | |

| Cancer | |

| Other Diseases |

| Small Molecule |

| Biologic /Large Molecule |

| Oral |

| Parenteral |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Therapeutic Class (Value) | Antidepressants | |

| Antipsychotics | ||

| Antiepileptics | ||

| Analgesics (Neuropathic & Migraine) | ||

| Disease-Modifying (MS, ALS, etc.) | ||

| Neurodegeneration (AD, PD) | ||

| Others | ||

| By Diseses | Neurovascular Diseases | |

| Trauma | ||

| Mental Health | Anxiety Disorders | |

| Epilepsy | ||

| Psychotic Disorders | ||

| Other Mental Health Disorders | ||

| Degenerative Diseases | Alzheimer's Disease | |

| Parkinson's Disease | ||

| Multiple Sclerosis | ||

| Amyotrophic Lateral Sclerosis | ||

| Other Degenerative Diseases | ||

| Infectious Diseases | ||

| Cancer | ||

| Other Diseases | ||

| By Drug Type (Value) | Small Molecule | |

| Biologic /Large Molecule | ||

| By Route of Administration (Value) | Oral | |

| Parenteral | ||

| Others | ||

| By Geography (Value) | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current valuation and growth outlook for the central nervous system therapeutics space?

The segment is valued at USD 143.32 billion in 2026 and is projected to climb to USD 197.35 billion by 2031, reflecting a 6.62% CAGR.

Which therapeutic class is expanding the fastest?

Disease-modifying therapies are forecast to grow at a 6.83% CAGR through 2031 as payers and clinicians prioritize treatments that slow or alter disease progression.

Why is Alzheimer's disease drawing heightened investment?

Regulatory acceptance of amyloid-targeting drugs such as lecanemab and donanemab has created a new treatment category, positioning Alzheimers as the fastest-growing indication at a 7.05% CAGR.

How do biologics compare with small molecules in future growth?

Although small molecules still hold over 70% revenue share, biologics including gene and antibody therapiesare advancing at a 7.52% CAGR thanks to improvements in brain delivery technologies.

Which region is expected to contribute most to incremental revenues?

Asia-Pacific is projected to record a 7.78% CAGR to 2031, driven by China's regulatory reforms, Japans fast-track pathways, and expanding healthcare access across emerging economies.

What competitive trend is reshaping deal activity?

Large pharmaceutical companies are acquiring or partnering with biotech firms that possess differentiated mechanisms, exemplified by multi-billion-dollar transactions for schizophrenia, gene, and psychedelic programs.

Page last updated on: