Albumin Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 8.43 Billion |

| Market Size (2031) | USD 12.19 Billion |

| Growth Rate (2026 - 2031) | 7.66% CAGR |

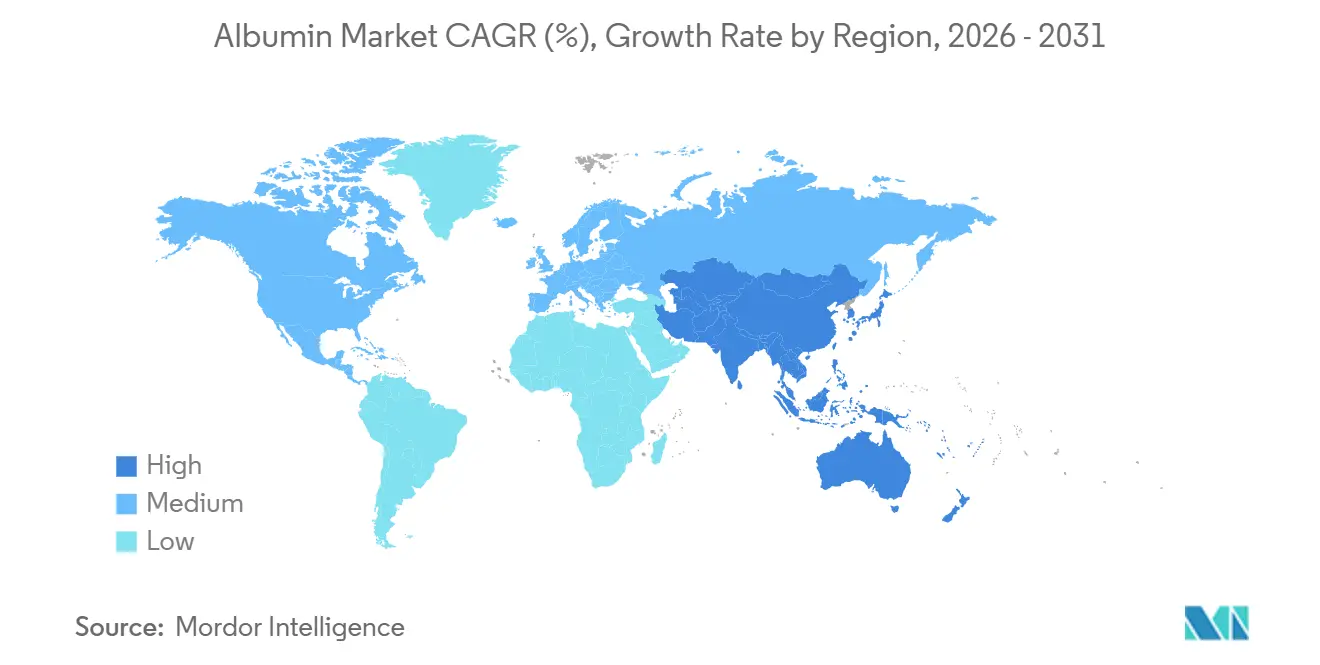

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Albumin Market Analysis by Mordor Intelligence

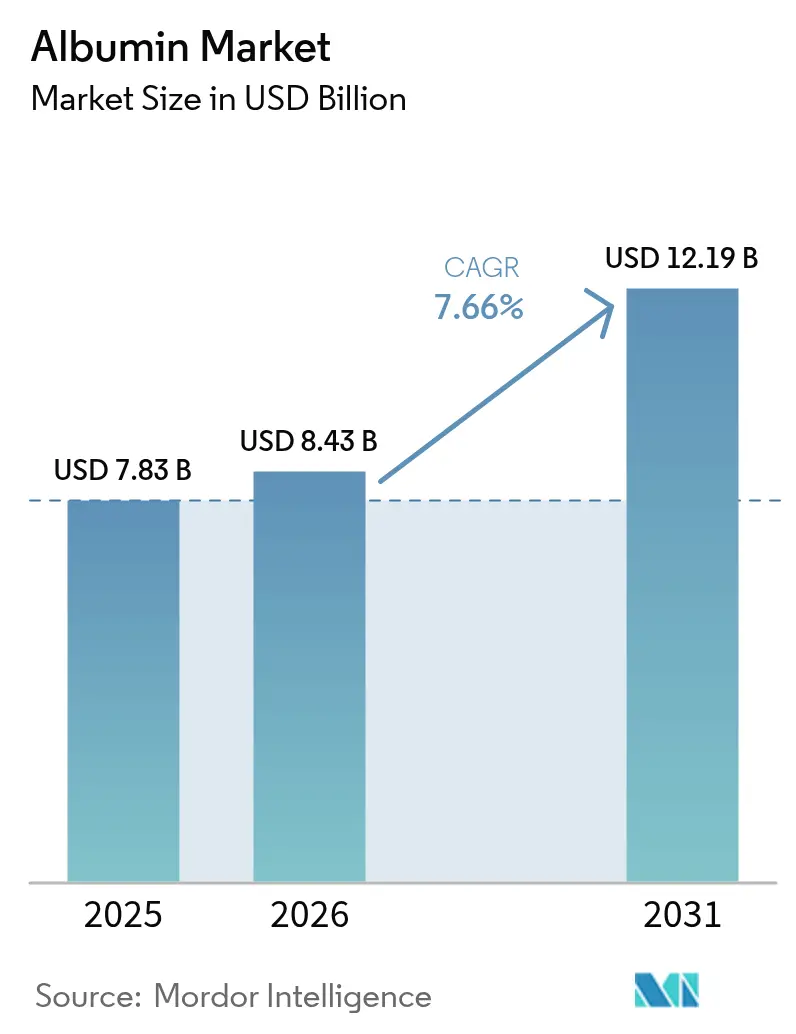

The Albumin Market size is expected to grow from USD 7.83 billion in 2025 to USD 8.43 billion in 2026 and is forecast to reach USD 12.19 billion by 2031 at 7.66% CAGR over 2026-2031.

The growth path reflects a shift from supply-constrained plasma-derived inputs toward recombinant platforms that address pathogen risk, improve consistency, and support new use cases in vaccines, biologics, and advanced drug delivery. Vaccine programs, cell-culture research, and oncology drug reformulations are expanding the addressable base as policymakers tighten quality controls on blood-product supply and bioprocessors seek animal-component-free ingredients. The albumin market is also seeing a dual-source structure emerge, with plasma-derived products serving legacy care settings, while recombinant formats are penetrating high-value applications where batch consistency and regulatory predictability carry weight. Regulatory updates in the United States and Europe are reshaping production choices, supporting sustained demand for pathogen-free inputs and aligning with industry efforts to reduce variability in manufacturing workflows.

Key Report Takeaways

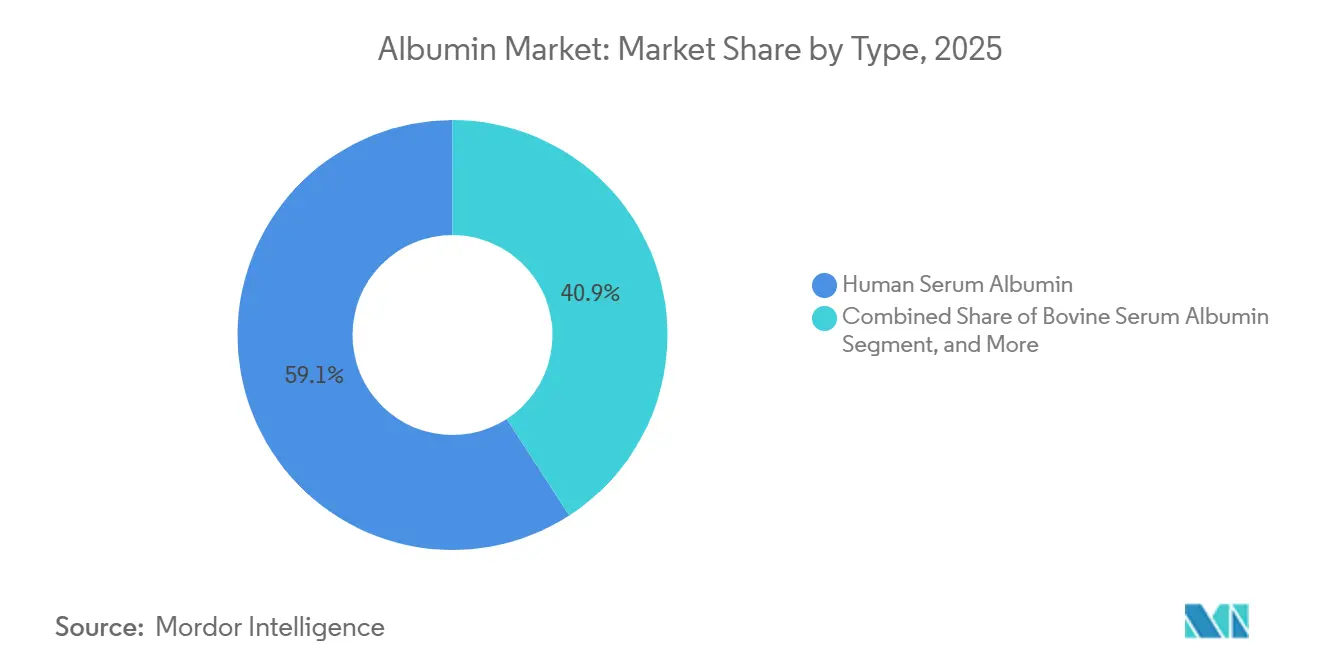

- By type, human serum albumin led with 59.14% revenue share in 2025, while recombinant albumin is forecast to expand at an 11.80% CAGR through 2031.

- By source, plasma-derived albumin held an 82.02% share in 2025, and recombinant sources are projected to grow at a 10.65% CAGR through 2031.

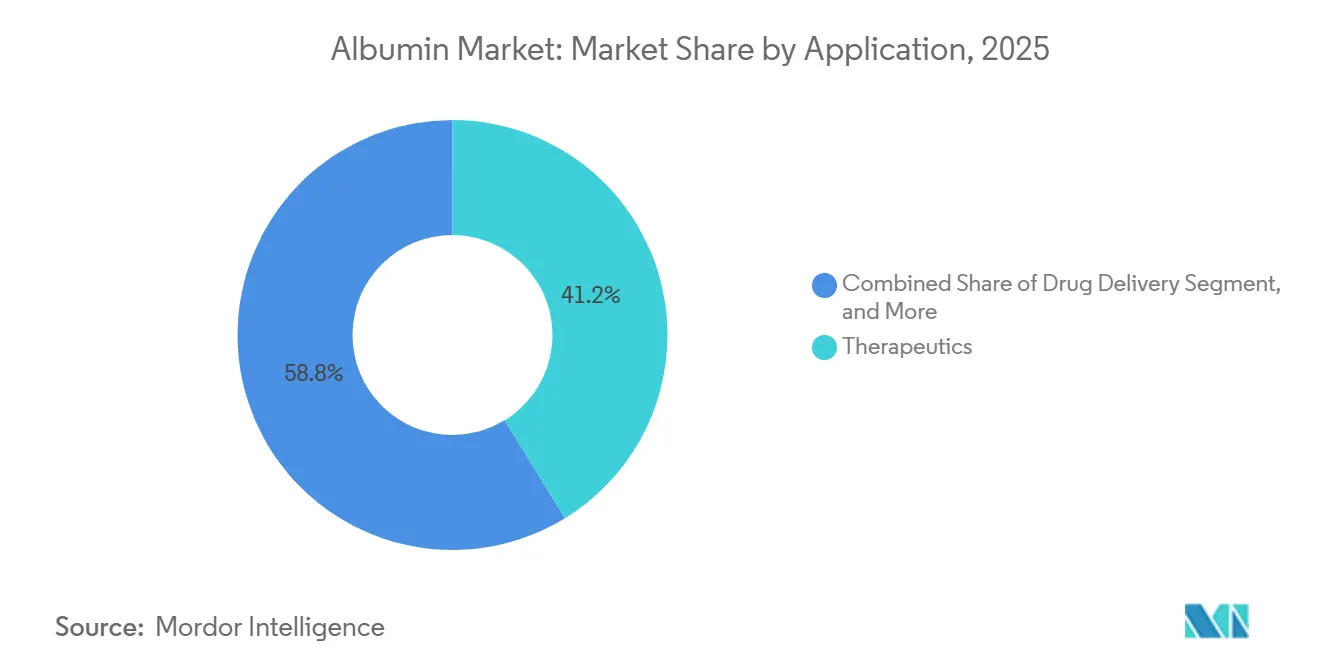

- By application, therapeutics accounted for a 41.23% share in 2025, while drug delivery is projected to grow at a 9.40% CAGR through 2031.

- By end user, pharmaceutical & biotechnology companies held a 45.00% share in 2025, and research institutes & CROs are projected to grow at a 11.05% CAGR through 2031.

- By geography, North America captured a 35.50% share in 2025, and Asia-Pacific is projected to grow at an 8.03% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Albumin Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Growing demand for albumin-based stabilizers in vaccine manufacturing | +1.2% | Global, with concentration in North America and Europe for mRNA platforms, Asia-Pacific for viral-vector vaccines | Medium term (2-4 years) |

| Expanding use of albumin as an excipient in biologic drug formulations | +1.5% | Global, led by North America and Europe where biologics approvals are concentrated | Long term (≥ 4 years) |

| Rising plasma-fractionation capacity in Asia-Pacific (China and India) | +1.3% | Asia-Pacific core, with spill-over to Middle East and Africa as regional supply chains mature | Medium term (2-4 years) |

| Uptake of recombinant albumin in cell-culture media for cultivated-meat R&D | +0.8% | North America, Europe, Singapore, early-stage commercial in Asia-Pacific | Long term (≥ 4 years) |

| Adoption of albumin nanoparticles in next-gen targeted drug-delivery platforms | +1.0% | Global, with North America and Europe leading clinical trials, Asia-Pacific following | Medium term (2-4 years) |

| Regulatory push for safer blood-product handling (EU MDR and U.S. cGMP upgrades) | +0.9% | Europe and North America primary, cascading to Asia-Pacific as harmonization advances | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Albumin-Based Stabilizers in Vaccine Manufacturing

Vaccine manufacturers are increasing the use of albumin stabilizers to protect antigens during lyophilization and distribution, which gained momentum when ERVEBO for Ebola, a live vaccine, incorporated rice-derived recombinant albumin in its formulation. This practice aligns with efforts to reduce cold-chain sensitivity and maintain stability for critical immunization programs serving high-risk populations. Recombinant albumin removes donor-derived pathogen risks, which is a core advantage for programs that support immunocompromised patients and regions with fragile logistics. China’s significant albumin needs and the advancement of rice-derived recombinant human serum albumin through late-stage clinical trials are prompting greater attention to domestic supply options that bypass plasma sourcing constraints. Public-health agencies encourage the use of defined, animal-component-free excipients where feasible because they reduce variability and ease post-approval changes to regulated filings. This demand pattern supports a steady expansion of albumin use in vaccine stabilization as programs for viral-vector and protein-subunit platforms broaden their portfolios in the forecast window.

Expanding Use of Albumin as an Excipient in Biologic Drug Formulations

Albumin’s role as a stabilizer and solubility enhancer in biologic formulations is expanding as developers focus on product integrity across manufacturing, storage, and administration. Subcutaneous and high-concentration injectable formats benefit from albumin’s ability to reduce aggregation and oxidation, thereby helping maintain consistent performance throughout shelf life. Ophthalmology injectables, such as Lucentis, are examples in which excipient choices support durability in prefilled presentations that must withstand refrigerated storage without loss of activity. The regulatory track record of albumin in human use supports predictable filings, which shorten development timelines for specific formulations compared with newer excipients that lack extensive safety histories. Recombinant albumin’s batch-to-batch consistency further reduces variability and documentation burden, which is essential for lifecycle management. As biologics programs focus on supply resilience and lean change-control workflows, albumin’s position as a proven excipient is becoming more central across select high-value therapy classes.

Rising Plasma-Fractionation Capacity in Asia-Pacific (China and India)

Asia-Pacific is expanding domestic fractionation footprints to meet therapeutic albumin demand and to reduce reliance on imports. In January 2026, ViNS Bioproducts committed Rs. 150 crore (USD 18 million) to PlasmaGen to expand production capacity in India, signaling policy support for greater self-sufficiency in plasma-derived medicines.[1]The Economic Times, “ViNS Bioproducts Invests Rs 150 Crore in PlasmaGen to Expand Plasma Protein Production,” The Economic Times, economictimes.indiatimes.com The United States remains the largest single source of plasma for fractionation, with regulatory frameworks that permit frequent plasma donations, which support steady global supply flows to import-dependent regions. Collection policies in parts of Europe and Asia limit supply elasticity, which can raise volatility in downstream pricing and heighten the need for diversified sourcing. These dynamics are drawing attention to recombinant routes, which scale through fermentation or plant-based expression rather than donor networks. Even with new Asia-Pacific facilities, domestic collections may lag demand growth, preserving a role for imports and dual-sourcing strategies. Recombinant producers that close cost gaps through yield gains have an opening to serve vaccine, excipient, and research-grade needs across these markets.

Uptake of Recombinant Albumin in Cell-Culture Media for Cultivated-Meat R&D

Cultivated-meat programs are moving away from fetal bovine serum toward recombinant albumin to remove animal components and stabilize cost structures during scale-up. Rice-based expression systems for recombinant human serum albumin now yield multi-gram amounts per kilogram of grain with high purity, supporting feasibility for use as a growth supplement in defined media. Regulatory momentum is visible in the United States, where the FDA and USDA cleared the way for the commercialization of cell-cultured poultry products in 2023, setting precedents for food-safety frameworks and ingredient scrutiny. Recombinant albumin provides a consistent alternative to serum as developers iterate media formulations for muscle and fat cell lines. The cost profile remains a challenge at pilot scale, but recombinant inputs align with labeling and safety expectations for future consumer acceptance. Suppliers that secure reliable capacity and high-quality systems are well positioned to serve early adopters in this field.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Safety concerns around pathogen transmission from plasma-derived albumin | -0.9% | Global, with heightened scrutiny in Europe and North America following periodic safety incidents | Short term (≤ 2 years) |

| Price volatility due to plasma-collection bottlenecks | -1.1% | North America and Europe primary, Asia-Pacific secondary as import dependence persists | Medium term (2-4 years) |

| Rapid shift toward chemically-defined, protein-free media in bioprocessing | -1.3% | Global, led by North America and Europe where mAb production is concentrated | Long term (≥ 4 years) |

| Competition from plant-derived albumin mimetics in food and cosmetics | -0.5% | Europe and North America for cosmetics, Asia-Pacific for food applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Safety Concerns Around Pathogen Transmission from Plasma-Derived Albumin

Plasma-derived albumin carries a residual risk of pathogen transmission despite validated steps such as solvent-detergent treatment, pasteurization, and nanofiltration that reduce viral load. Donor screening and deferral criteria reduce risk, yet window periods for certain infections can still lead to recalls or added oversight in cases that demand investigation. The FDA maintains standards for blood and blood components in 21 CFR Part 640, which frames collection, processing, and testing requirements for the U.S. plasma supply. FDA’s 2024 draft guidance on cattle-derived materials for human use underscores ongoing BSE risk management. It strengthens expectations for traceability and sourcing controls, which add cost and complexity when animal derivatives are used. These constraints motivate vaccine and biologics makers to consider recombinant albumin for patient safety and compliance reasons. As a result, plasma-based albumin retains demand in well-established care settings, while high-growth applications turn to animal-component-free options to mitigate risk.

Rapid Shift Toward Chemically Defined, Protein-Free Media in Bioprocessing

Monoclonal antibody production and other biologics workflows are moving quickly to chemically defined, protein-free media to minimize variability and reduce regulatory burden. Suppliers now offer complete media solutions without albumin that deliver consistent performance at large bioreactor scales, which simplifies quali.y controls and supports global filings, This migration reduces consumption of Bovine Serum Albumin in industrial cell culture. It shifts demand toward niche research use and select therapeutic contexts that still prefer albumin’s functional attributes. For manufacturers, standardized media reduces lot-release testing tied to animal components and lowers contamination risks during scale-up. Regulators also encourage animal-component-free processes where equivalent outcomes can be shown. The near-term effect is a contraction in commodity BSA volumes for bioprocessing, which shapes where and how suppliers invest in production capacity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Recombinant Platforms Challenge Plasma Dominance

Human Serum Albumin accounted for 59.14% in 2025, reflecting its central role in volume expansion, burn care, and the management of hypoalbuminemia in clinical practice. These uses remain anchored in established protocols, where clinicians rely on known safety and reimbursement pathways to support steady utilization. Recombinant Albumin is set to grow at an 11.80% CAGR through 2031, driven by gains in vaccines, biologics formulations, and specialized cell-culture media, where batch consistency and pathogen-free sourcing are preferred. In this context, the albumin market is splitting between legacy therapeutic settings and advanced applications where supply predictability and defined excipients matter. Bovine Serum Albumin is seeing slower growth as chemically defined media replace protein supplements in mainstream monoclonal antibody manufacturing. However, it retains roles in diagnostics and lab protocols that are less sensitive to regulatory pressure to eliminate animal components. The evolution of type preferences is driving suppliers to align production with compliant, scalable routes that meet both clinical and non-clinical needs.

By Source: Plasma Supply Constraints Accelerate Recombinant Adoption

Plasma-derived albumin held 82.02% of the supply in 2025, supported by extensive U.S. collection networks and established fractionation hubs in North America and Europe. The United States supplies a large share of global plasma, which promotes domestic fractionation output and exports to import-dependent regions. Regulatory frameworks in the United States that allow frequent plasma donations help maintain capacity, while policy limits in parts of Europe and Asia constrain collection volumes and slow response to demand spikes. These constraints reinforce price swings for plasma-derived inputs and increase interest in dual sourcing strategies. Recombinant albumin from yeast, rice, and other expression platforms is projected to grow at a 10.65% CAGR from 2026 to 2031 as manufacturers seek to limit supply shocks and compliance complexity for tightly regulated applications.

By Application: Drug Delivery Outpaces Legacy Therapeutics

Therapeutics led with 41.23% of demand in 2025 as clinicians continued to rely on albumin solutions for volume expansion in critical care and for support in severe burns and hypoalbuminemia. Intravenous presentations at 20% and 25% concentrations are embedded in emergency and perioperative protocols and have established reimbursement pathways in significant markets. Drug Delivery is projected to grow at a 9.40% CAGR from 2026 to 2031 as albumin-based nanoparticles advance in oncology and other areas where targeted payload delivery and solvent-free formulations matter. Abraxane is a reference example that uses human albumin to deliver paclitaxel without Cremophor EL, thereby reducing solvent toxicity and improving tumor penetration in specific settings. Vaccine Ingredient uses are rising as developers integrate albumin for stability in freeze-dried formulations and during storage, with the ERVEBO program providing a proof point for the use of recombinant albumin in an approved vaccine.

By End-User: Research Institutes Outpace Pharma Incumbents

Pharmaceutical & Biotechnology Companies accounted for 45.00% of demand in 2025, driven by consistent use in therapeutic infusions and as excipients in certain biologics and vaccines. Hospitals & Clinics sustain large volumes through protocols in intensive care units, surgery suites, and emergency medicine. Research Institutes & CROs are set to grow at an 11.05% CAGR as they expand work on cultivated meat, regenerative medicine, and stem cell systems that require highly consistent, animal-component-free proteins for experimental and translational programs. Developers studying cell-culture media for food applications have also flagged albumin as a key cost driver and a focus for recombinant substitution, which supports a broad set of research-led orders in the near term. Diagnostic Centers continue to use albumin for assay development, although competitive alternatives are displacing some volumes in basic workflows.

Geography Analysis

North America captured 35.50% in 2025, supported by the United States’ large plasma-collection footprint and established fractionation base that ensures a steady therapeutic albumin supply. The region’s high-acuity care settings and mature reimbursement systems help sustain demand for infusions used in critical care, surgery, and emergency medicine. U.S. regulators set standards for blood and blood components that influence global practices, and these frameworks enable frequent plasma donations that support both domestic demand and exports. North America’s research and biopharma ecosystems also contribute to growth in vaccine stabilization and drug-delivery reformulations that utilize albumin-based technologies. As a result, the albumin market in the region combines legacy therapeutic use with growing innovation-led demand.

Asia-Pacific is projected to grow at an 8.03% CAGR through 2031 as countries invest in plasma-protein infrastructure and encourage the development of recombinant routes for albumin supply. Domestic needs in China and India are central to regional growth, with initiatives to reduce import dependence and to bring more of the value chain onshore. Late-stage development of rice-derived recombinant human serum albumin in China adds a future source of supply that can support vaccines, excipients, and other regulated uses once approvals are secured. India’s investments in fractionation capacity, such as ViNS Bioproducts’ 2026 funding for PlasmaGen, reflect this goal of greater self-sufficiency in albumin and related plasma proteins. The albumin market in the region benefits from strong policy support, which should attract both plasma-derived and recombinant suppliers to scale capabilities in step with local demand.

Competitive Landscape

The albumin market features moderate concentration across plasma-derived supply, with the top multinational fractionators maintaining a large installed base of centers and fractionation assets. Global leaders such as CSL Behring, Grifols, Takeda, Baxter’s spin-off Vantive, and Octapharma sustain extensive networks that enable consistent output and international distribution. Recombinant-focused players include Albumedix within Novonesis, along with plant-expression pioneers that are advancing rice-derived rHSA through clinical pathways in China. The albumin market is therefore developing along two capability sets, one optimized for donor collection and fractionation scale, and the other for controlled expression platforms that emphasize consistency and regulatory fit.

Strategic moves reflect this bifurcation. Plasma networks continue to adjust site footprints and donor engagement practices to keep yields aligned with demand and to manage cost structures linked to donor compensation and testing requirements. On the recombinant side, capacity expansions are tied to fermentation or agricultural cycles that improve yields and cost position. Partnerships and licensing arrangements are used to access markets that require local production or tailored quality systems, which is important for vaccine stabilizers and specific excipient grades.

Albumin Industry Leaders

Baxter International Inc.

Bristol-Myers Squibb Company

Merck KGaA

Grifols (Biotest AG)

Thermo Fisher Scientific Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: ViNS Bioproducts invested INR 150 crore (USD 18 million) in PlasmaGen to expand plasma-protein production capacity in India, targeting albumin, immunoglobulins, and coagulation factors to reduce import dependence and meet rising therapeutic demand.

- May 2025: Grifols reported topline data from its Phase 3 PRECIOSA clinical trial evaluating long-term albumin treatment with Albutein in patients with decompensated cirrhosis and ascites.

- December 2024: Grifols reported topline data from its Phase 3 PRECIOSA clinical trial evaluating long-term albumin treatment with Albutein in patients with decompensated cirrhosis and ascites.

Global Albumin Market Report Scope

As per the scope of the report, albumin is a water-soluble globular protein produced in the liver and accounts for 50% of blood plasma proteins. It plays a vital role in regulating blood volume and transporting molecules, such as hormones, bile salts, and ions. It is commonly used as a blood volumiser in rare diseases, burns, shock, liver conditions, and other situations involving blood loss, trauma, or surgery.

The albumin market is segmented by type, source, application, end-user, and geography. By type, the market is segmented into human serum albumin, bovine serum albumin, and recombinant albumin. By source, the market is segmented into plasma-derived recombinant (yeast, rice, transgenic plants). By application, the market is segmented into drug delivery, therapeutics, culture media ingredients, vaccine ingredients, and other applications. By end user, the market is segmented into pharmaceutical & biotechnology companies, research institutes & CROs, hospitals & clinics, diagnostic centers, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle-East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers market size and forecasts in value (USD) for the above segments.

| Human Serum Albumin |

| Bovine Serum Albumin |

| Recombinant Albumin |

| Plasma-derived |

| Recombinant (Yeast, Rice, Transgenic Plants) |

| Drug Delivery |

| Therapeutics |

| Culture-Media Ingredient |

| Vaccine Ingredient |

| Diagnostics |

| Other Applications |

| Pharmaceutical & Biotechnology Companies |

| Research Institutes & CROs |

| Hospitals & Clinics |

| Diagnostic Centers |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Human Serum Albumin | |

| Bovine Serum Albumin | ||

| Recombinant Albumin | ||

| By Source | Plasma-derived | |

| Recombinant (Yeast, Rice, Transgenic Plants) | ||

| By Application | Drug Delivery | |

| Therapeutics | ||

| Culture-Media Ingredient | ||

| Vaccine Ingredient | ||

| Diagnostics | ||

| Other Applications | ||

| By End-user | Pharmaceutical & Biotechnology Companies | |

| Research Institutes & CROs | ||

| Hospitals & Clinics | ||

| Diagnostic Centers | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected growth of the albumin market to 2031?

The albumin market is projected to grow from USD 8.43 billion in 2026 to USD 12.19 billion by 2031 at a 7.66% CAGR.

Which type is growing fastest within the albumin market?

Recombinant Albumin is forecast to grow at an 11.80% CAGR through 2031, driven by vaccine stabilization, biologics formulation, and advanced delivery use cases.

What factors are shaping albumin sourcing strategies for biopharma?

Regulatory focus on safety and traceability, the need for batch consistency, and supply predictability are pushing adoption of recombinant sources alongside plasma-derived supply.

Where is demand growing fastest geographically for albumin?

Asia-Pacific is projected to post an 8.03% CAGR through 2031 as China and India expand fractionation and recombinant capabilities, while North America remains the largest regional base by share.

What applications are expanding fastest for albumin use?

Drug delivery and vaccine stabilization are expanding fastest due to solvent-free nanoparticle formats and defined excipients that improve stability and regulatory clarity.

How are bioprocessing trends affecting albumin demand?

The shift to chemically defined, protein-free media is reducing industrial BSA use while pharmaceutical applications for HSA continue to expand, increasing the need for differentiated grades.

Page last updated on: