Lithium-ion Battery Separator Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 11.44 Billion |

| Market Size (2031) | USD 23.29 Billion |

| Growth Rate (2026 - 2031) | 15.28% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

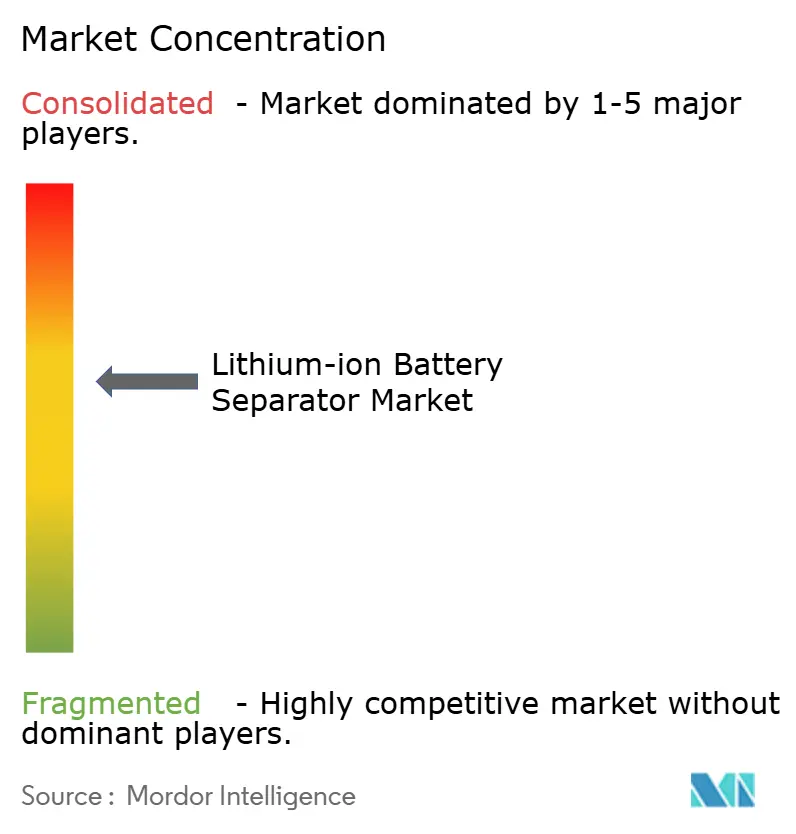

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Lithium-ion Battery Separator Market Analysis by Mordor Intelligence

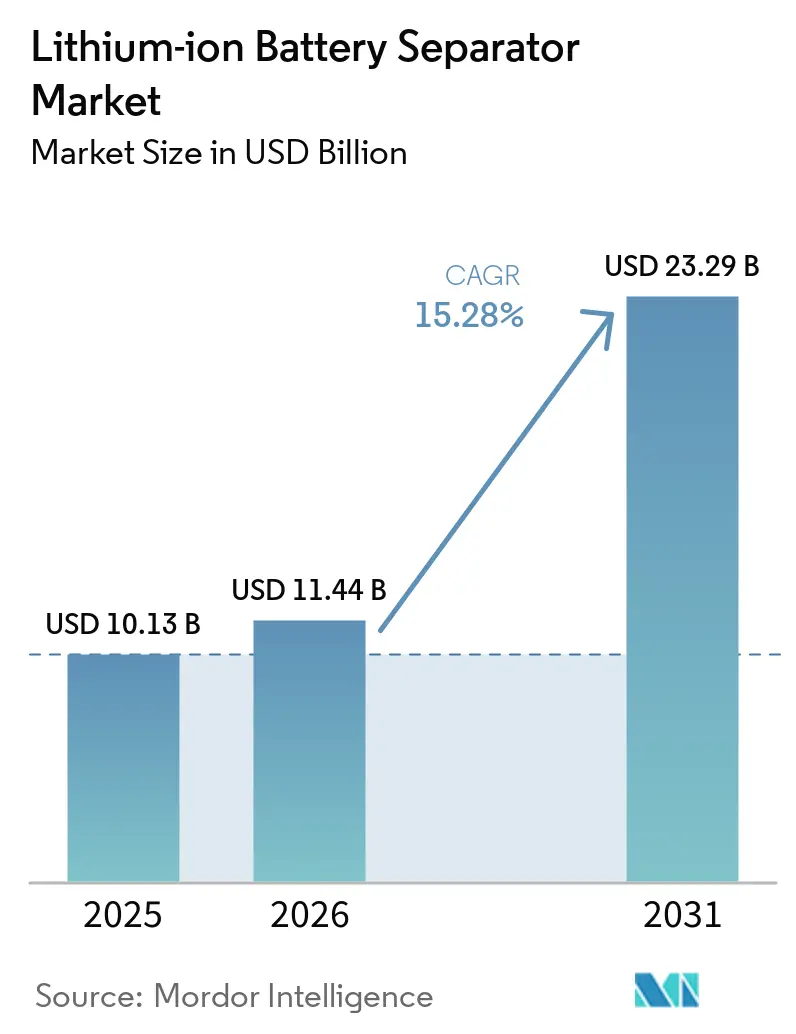

The Lithium-ion Battery Separator Market size was valued at USD 10.13 billion in 2025 and is estimated to grow from USD 11.44 billion in 2026 to reach USD 23.29 billion by 2031, at a CAGR of 15.28% during the forecast period (2026-2031).

New demand stems from electric vehicles and utility-scale storage, which increasingly specify ultra-thin, ceramic-coated membranes that tolerate high-nickel chemistries and aggressive fast-charge profiles. Wet-process polyolefin separators still dominate, yet coated variants are growing rapidly as automakers elevate thermal-propagation safeguards. Capital is flowing to regions with domestic-content mandates; Asahi Kasei’s CAD 1.56 billion Ontario complex exemplifies the first-mover incentives now reshaping the supply map. Meanwhile, North American tax credits, Europe’s Battery Regulation, and China’s gigafactory build-out are fragmenting global trade flows and rewarding suppliers that certify regional provenance while mastering cost-effective resin integration.

Key Report Takeaways

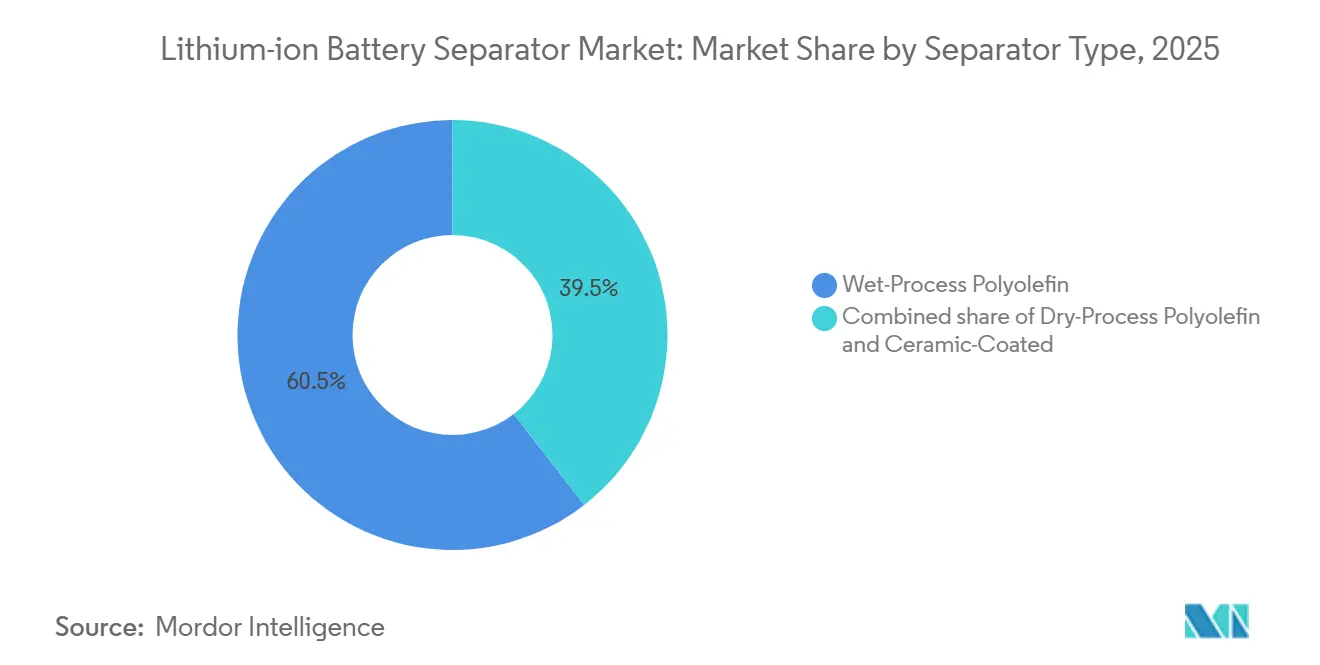

- By separator type, wet-process polyolefin led with 60.5% of the lithium-ion battery separator market share in 2025; ceramic-coated designs are forecast to post the fastest 22.9% CAGR through 2031.

- By material, polypropylene commanded 48.2% share in 2025, while non-woven composites are projected to grow at a 20.3% CAGR during 2026-2031.

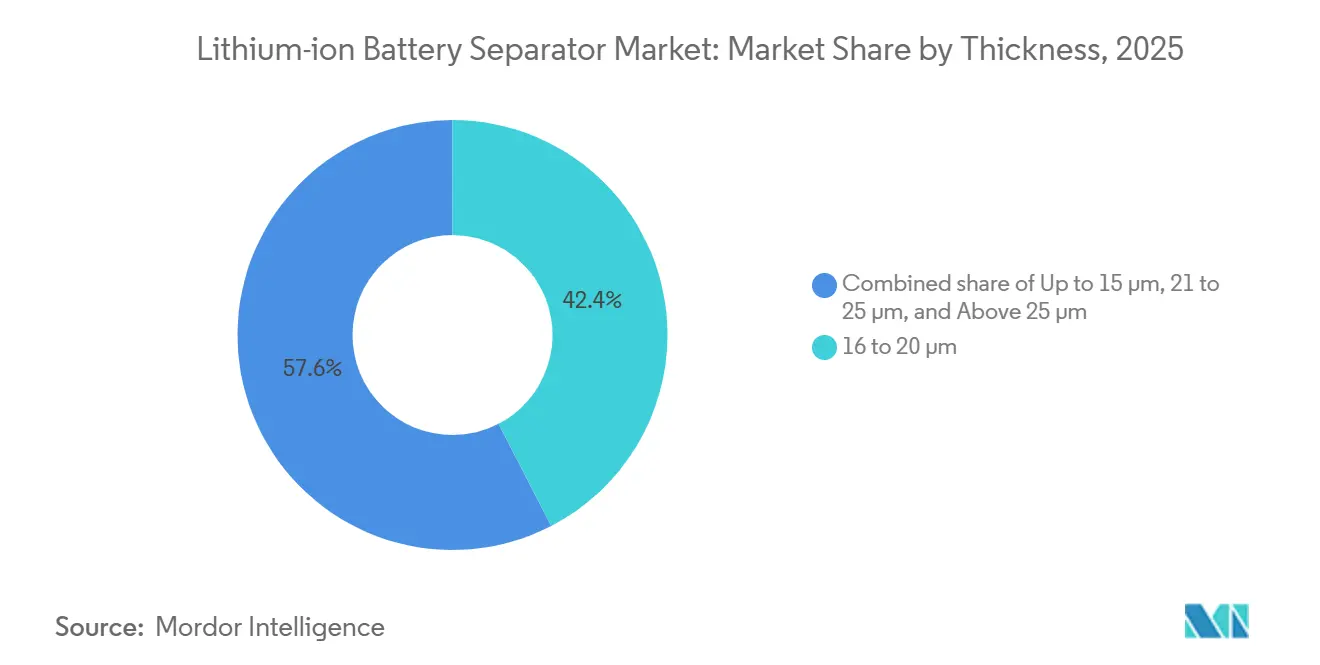

- By thickness, the 16 to 20 µm segment held the largest share of 42.4% in 2025, while the up-to-15 µm gauge recorded the strongest growth trajectory at 25.5% CAGR through 2031.

- By battery form factor, pouch cells led with 44.8% of the lithium-ion battery separator market share in 2025; prismatic cells are forecast to post the fastest 20.8% CAGR through 2031.

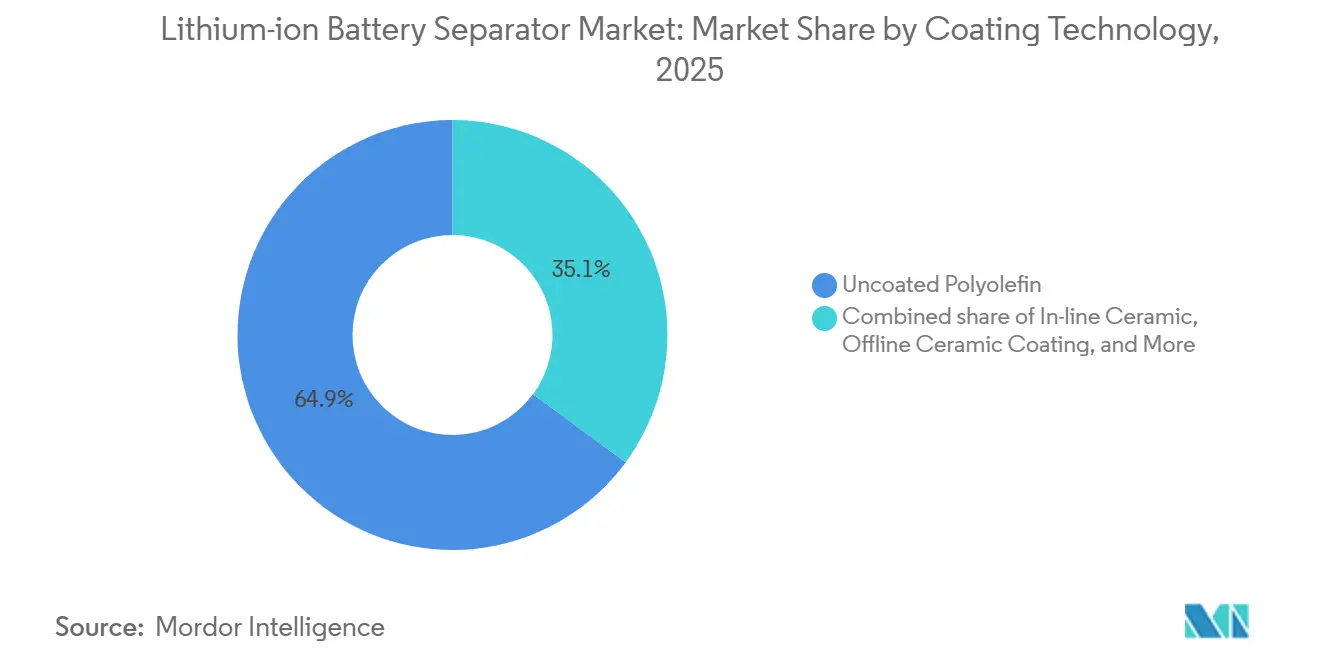

- By coating technology, uncoated polyolefin commanded 64.9% share in 2025, while in-line ceramic coating is projected to grow at 24.1% CAGR during 2026-2031.

- By application, automotive EVs accounted for 56.3% of demand in 2025, and stationary energy storage represents the fastest segment with a 21% CAGR outlook.

- By geography, Asia-Pacific captured 50% of 2025 revenue, whereas North America is projected to expand at the highest 22% CAGR under the Inflation Reduction Act incentives.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Lithium-ion Battery Separator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining lithium-ion battery prices | +2.5% | Global, strongest in China and North America | Medium term (2-4 years) |

| Accelerating global EV adoption | +4.0% | China, Europe, North America | Long term (≥ 4 years) |

| Rapid growth in stationary energy-storage projects | +2.0% | North America, Europe, Australia | Medium term (2-4 years) |

| Government incentives for domestic battery supply chains | +2.5% | North America, Europe, India | Short term (≤ 2 years) |

| OEM push for ultra-thin separators for high-Ni cathodes | +1.5% | Asia-Pacific, spill-over to North America | Medium term (2-4 years) |

| Localization mandates driving regional separator gigafactories | +2.0% | North America, Europe, Southeast Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Declining Lithium-Ion Battery Prices

Pack costs fell to USD 115 kWh⁻¹ in 2025, freeing headroom for OEMs to specify better separators without raising bill-of-material totals. Savings stem from lower lithium-carbonate prices and excess cathode capacity in China, cutting input costs by 35% year-over-year. Cell makers are channeling these gains into ceramic coatings that add only USD 0.10 m⁻² yet curb warranty risk from thermal events. Thinner membranes also reclaim internal volume lost to lower-energy LFP chemistries, bolstering range targets without bigger packs.[1]Russell Gold, “Utilities Bet on Long-Life Batteries,” wsj.com Persistent price pressure may squeeze gross margins below 15%, driving producers toward proprietary formulations that justify premium pricing.

Accelerating Global EV Adoption

Worldwide EV sales climbed to 14.2 million units in 2025, a 22% gain that lifts separator demand in lockstep with battery capacity. Growing 80-100 kWh packs in midsize cars translates into an extra 1.2 billion m² of wet-process film each year. Chinese automakers are shifting from pouch to prismatic cells, prioritizing separators with high puncture resistance under 2 MPa compression loads. General Motors and Ford will follow with prismatic designs for model-year 2027, requiring local separator content to satisfy a 60% IRA threshold. CAFE and Euro 7 regulations ensure sustained growth well beyond 2030.

Rapid Growth in Stationary Energy-Storage Projects

Grid batteries reached 45 GWh of new installations in 2025 as utilities firm up wind and solar output. Long life cycles push buyers toward dry-process films with narrower pore dispersion to survive 6,000-8,000 deep cycles. The U.S. DOE Long Duration Storage Shot seeks USD 0.05 kWh⁻¹ by 2030, encouraging extrusion upgrades that deliver sub-USD 1.50 m⁻² membranes. Australia and India echo this trend with local-content subsidies that call for domestically made separators. Producers that master thick 21-25 µm gauges can protect cells against field thermal abuse over 20 years, winning critical utility approval.

Government Incentives for Domestic Battery Supply Chains

U.S. Advanced Manufacturing Production Credits worth USD 10 kWh⁻¹ have triggered USD 2.8 billion of announced capacity since 2024. Entek and Celgard alone will add 3.3 billion m² of domestic wet-process lines by 2027. Europe’s Battery Regulation attaches carbon-footprint reporting and recycled-content targets that nudge Asian producers to build local coating plants. India’s PLI scheme mirrors this approach, while South Korea’s K-Battery plan co-funds R&D on composite membranes. Early movers capture share as OEM sourcing teams lock multi-year contracts to secure compliant components.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Polyolefin resin supply–demand imbalance | -1.5% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Stringent safety and quality certification timelines | -0.8% | Global, bottlenecks in North America and Europe | Medium term (2-4 years) |

| Solvent-recovery cost challenges in wet-process lines | -0.5% | North America, Europe, emerging Asia-Pacific | Medium term (2-4 years) |

| Limited recyclability pathways for spent separators | -0.4% | Global, with regulatory pressure in Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Polyolefin Resin Supply–Demand Imbalance

Unplanned outages at crackers in Saudi Arabia and China lifted feedstock prices 18% in Q1 2025, starving separator plants of high-melt-flow polypropylene that makes up just 3% of global output. Celgard and Entek rationed resin to auto clients, sidelining consumer-electronics orders to protect contracts. Scrap from edge-trim cannot be recycled without molecular degradation, keeping virgin-resin dependence high. Strategic tolling deals with resin majors are now critical to future capacity expansions. Backward integration remains costly, but firms that secure supply enjoy higher plant utilization and steadier margins.

Stringent Safety & Quality Certification Timelines

UL 1642 and IEC 62133 testing can stretch 18 months for new coatings, delaying commercialization for startups. Labs at Underwriters Laboratories and TÜV Rheinland hold nine-month backlogs amid a 40% jump in 2025 submissions. Automakers add 500-cycle aging and humidity trials, driving costs, and favoring incumbents with established data packages. ISO 9001 and IATF 16949 audits reinforce hurdles by requiring documented controls for each process step. China’s 2024 GB/T 31485 revision forced domestic producers to retrofit ceramic lines, underscoring the global compliance burden.[2]Journal of Materials Chemistry A, “Thermal-Propagation Standards for EV Batteries,” pubs.rsc.org

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Separator Type: Ceramic Coatings Gain on Safety Mandates

Wet-process polyolefin films captured 60.5% of 2025 revenue, the largest slice of the lithium-ion battery separator market. Ceramic-coated variants are projected to expand at a 22.9% CAGR, reflecting OEM urgency to curb thermal runaway in high-nickel cells. Dry-process films, roughly a quarter of volume, equip grid batteries that value cycle life over energy density.

Uncoated films keep cost leadership, yet growing liability concerns push tier-one cell makers toward alumina-coated membranes that pass IEC 62133 propagation limits. Asahi Kasei’s Hipore and Toray’s Setela demonstrate how sub-15 µm thickness can coexist with ceramic layers that stay intact above 150 °C. Commodity-grade uncoated sheets remain preferred for power tools and industrial packs where price outweighs gravimetric efficiency.

By Material: Non-Woven Composites Challenge Polyolefin Hegemony

Polypropylene retained 48.2% of 2025 revenue, yet non-woven and specialty composites are advancing at 20.3% CAGR to nibble share. Multilayer PP/PE/PP designs hold about 15% of high-end auto demand, balancing quick shutdown with mechanical strength.

Aramid-fiber and glass-mat substrates deliver 60% higher puncture resistance, appealing to ultra-high-energy designs that chase 300 Wh kg⁻¹ goals. Polyethylene keeps traction in cylindrical cells thanks to its lower melting point, though tensile limits deter use in compressed prismatic stacks. Functional coatings such as polyvinylidene fluoride improve ionic wet-out, hinting at a diversified feedstock future that could cap polypropylene dominance after 2028.

By Thickness: Ultra-Thin Membranes Enable Energy-Density Gains

Films in the 16-20 µm band represented 42.4% of sales, anchoring the lithium-ion battery separator market size for mainstream EV packs. Up-to-15 µm gauges are forecast to rise at a 25.5% CAGR, the fastest among all thickness classes, as automakers target 250- to 300-Wh kg⁻¹ cells.

CATL’s Qilin platform illustrates benefits: a 12 µm ceramic-coated film freed volume for extra active material and lifted cell energy density to 255 Wh kg⁻¹. Thicker 21-25 µm sheets are essential for stationary storage where cycle life matters more than pack mass. Above 25 µm finds niche use in aerospace batteries that prize safety margins under extreme conditions.

By Battery Form Factor: Prismatic Cells Reshape Specifications

Pouch cells held 44.8% of the 2025 unit demand, reflecting legacy smartphone and early EV adoption. Prismatic formats will grow at 20.8% CAGR as Chinese and European OEMs deploy cell-to-pack architectures that cut module parts.

BYD’s Blade and CATL’s Qilin both rely on prismatic LFP cells with ceramic-coated films that block propagation between tightly packed cells. Cylindrical interest is rebounding on Tesla’s 4680, driving demand for films that survive tabless electrodes and 5× faster charging. Cold-climate EVs still favor pouch flexibility and multilayer structures that keep ionic pathways open below –20 °C.

By Coating Technology: In-Line Processes Cut Handling Steps

Uncoated films occupied 64.9% of 2025 sales, but in-line ceramic coating is projected to climb 24.1% CAGR on cost and yield gains. SK IE Technology’s Jeungpyeong line applies 2-3 µm alumina at 100 m min⁻¹ with 98.5% uniformity, illustrating scale benefits.

Offline ceramic remains essential for small producers, yet it adds a three-day lead time and higher contamination risk. Functional polymer coatings deliver faster electrolyte soak and shave 20% from formation times without a weight penalty, enticing solid-state developers.

By Application: Automotive EV Demand Outpaces Consumer Electronics

Automotive EVs absorbed 56.3% of 2025 volume and will expand at 19.2% CAGR as pack capacities rise to 100 kWh in many mid-segment models. Consumer electronics contribute about one-quarter of demand but show slower growth as device refresh cycles lengthen.

Stationary energy storage posts a faster 21% CAGR, favoring dry-process films that hold up over 8,000 cycles. Industrial and power-tool migration from nickel chemistries will lift separator shipments, but it remains a sub-10% niche through 2031.

Geography Analysis

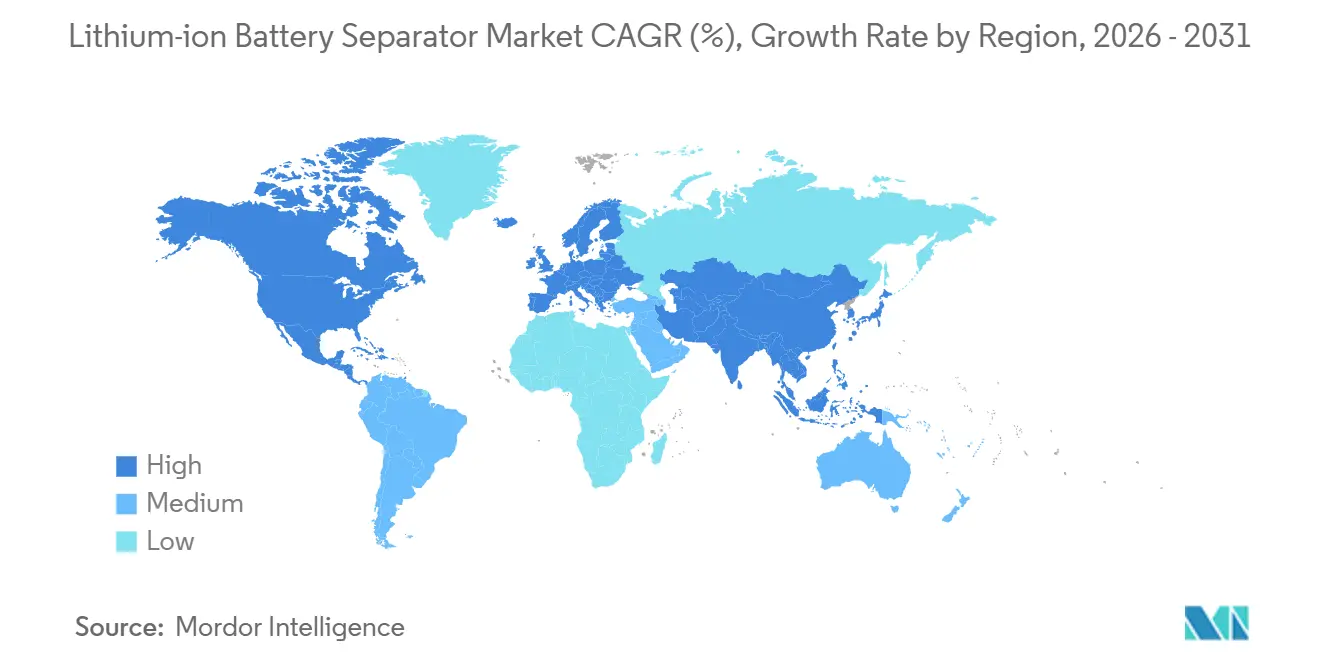

Asia-Pacific led the lithium-ion battery separator market with 50.0% of 2025 revenue, powered by China’s extrusion capacity and South Korea’s ceramic-coating expertise. Utilization hovered near 80% as domestic EV growth cooled to 22%, giving exporters the slack to chase foreign contracts. Japan and Korea now build coating lines in the United States and Europe to hedge logistics risk, while retaining core extrusion in Asia to leverage lower energy and labor inputs.[3]Chemical & Engineering News, “IRA Spurs U.S. Separator Investments,” cen.acs.org

North America ranks as the fastest-growing region with a 22.0% CAGR, lifted by the Inflation Reduction Act’s 60% domestic-content threshold by 2027. Entek’s USD 850 million Indiana plant, coming online in 2026, will supply 1.2 billion m² a year, trimming U.S. reliance on imports and anchoring the local Lithium-ion battery separator market size to major cell programs at GM and Stellantis. Mexico’s near-shoring wave adds another 1.1 billion m² by 2028, serving Gigafactory Mexico and other auto hubs.

Europe controls roughly 20% of current demand and grows at 18% CAGR as the Battery Regulation enforces 50% regional value by 2027. Plants in Poland and Hungary that feed Volkswagen and Stellantis packs will elevate the lithium-ion battery separator market share above 30% of regional consumption by 2031. India, Vietnam and Indonesia constitute emerging hubs as policy makers tie mineral permits to downstream processing, but combined share stays below 10% until late in the forecast.

Competitive Landscape

The top five suppliers, Asahi Kasei, Toray, SK IE Technology, Celgard, and Entek, controlled about 65% of global capacity in 2025, giving the lithium-ion battery separator market a moderate concentration profile. Chinese challengers Shenzhen Senior and Cangzhou Mingzhu doubled output since 2024, putting price pressure on commodity-grade films. Incumbents counter by integrating backward into polypropylene sourcing and forward into ceramic coating to lock in margin.

Intellectual-property filings underscore strategy: Asahi Kasei lodged 47 separator patents in 2025 focused on trilayer architectures, while SK IE Technology booked 32 grants tied to high-speed slot-die coating. Toray’s Setela exploits 200-nm alumina on an aramid base to hit 3C fast-charge without lithium plating, winning orders from Toyota and Nissan. Emerging players such as Dreamweaver (electrospun aramid) and Suzhou GreenPower (solvent-free dry coating) target white-space niches where incumbents have fewer patents.[4]Lindsay Chappell, “Patent Rush in Separator Tech,” wsj.com

Standards updates now influence competitive dynamics almost as much as cost. IEC 62133’s 2024 revision inserted propagation limits that tilt awards toward ceramic-coated films, while UL 1642 ramps abuse-test stringency in 2026. Firms with pre-qualified portfolios clear customer audits faster, maintaining higher bid-win ratios even when Chinese prices are undercut by up to 12%.

Lithium-ion Battery Separator Industry Leaders

Asahi Kasei Corporation

Toray Industries Inc.

SK IE Technology Co. Ltd

Entek International LLC

Ube Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Cangzhou Mingzhu unveiled the Phase II rollout of its expansion project, focusing on ultra-thin wet-process lithium battery separators, with an emphasis on producing premium 5-micron separators.

- December 2025: Asahi Kasei divested its Daramic lead-acid battery separator business to focus on expanding its lithium-ion battery separator segment. The company is prioritizing its Hipore™ wet-process separators, which are designed for automotive and electronics applications. This move aligns with Asahi Kasei's portfolio transformation strategy and its increased investment in high-growth functional materials.

- October 2025: I Squared Capital acquired a majority stake in ENTEK Technology Holdings, a U.S.-based battery separator manufacturer, with an investment of approximately $800 million. The investment will fund the construction of the first large-scale wet-process lithium-ion separator gigafactory in Terre Haute, Indiana. This initiative aims to strengthen domestic supply chains and support the electric vehicle, energy storage, and defense battery markets.

- January 2024: Noco-noco and Greenfuel Energy Solutions signed a memorandum of understanding (MOU) to integrate Noco-noco’s X-SEPA™ separator technology into electric vehicle batteries. This collaboration aims to improve battery efficiency and lifespan, targeting the two- and three-wheeler markets in India and Africa. The partnership supports electrification adoption by enhancing performance with advanced separator technology.

Global Lithium-ion Battery Separator Market Report Scope

The battery separator works as a membrane between the anode and cathode. It is a key component within the lithium-ion battery cell. In lithium-ion batteries, separators create a barrier to prevent a short circuit between the cathode and anode.

The global lithium-ion battery separator market is segmented by separator type, material, thickness, battery form factor, coating technology, application, and geography. By separator type, the market is segmented into wet-process polyolefin, dry-process polyolefin, and ceramic-coated separators. By material, the market is segmented into polypropylene (PP), polyethylene (PE), multilayer PP/PE/PP, and non-woven & other specialty separator materials. By thickness, the market is segmented into up to 15 µm, 16 to 20 µm, 21 to 25 µm, and above 25 µm separator films. By battery form factor, the market is segmented into pouch, cylindrical, and prismatic cell formats. By coating technology, the market is categorized into in-line ceramic coating, offline ceramic coating, functional polymer-coated separators, and uncoated separators. By application, the market is segmented into automotive electric vehicles (EVs), consumer electronics, stationary energy storage systems, and industrial & power tools. The report also provides market sizes and forecasts for the global lithium-ion battery separator market across major countries in key regions, including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. For each segment, the market sizing and forecasts are presented in terms of value (USD).

| Wet-Process Polyolefin |

| Dry-Process Polyolefin |

| Ceramic-Coated |

| Polypropylene (PP) |

| Polyethylene (PE) |

| Multilayer PP/PE/PP |

| Non-woven and Others |

| Up to 15 µm |

| 16 to 20 µm |

| 21 to 25 µm |

| Above 25 µm |

| Pouch Cells |

| Cylindrical Cells |

| Prismatic Cells |

| In-line Ceramic Coating |

| Offline Ceramic Coating |

| Functional Polymer Coatings |

| Uncoated Polyolefin |

| Automotive EV |

| Consumer Electronics |

| Stationary Energy Storage |

| Industrial and Power Tools |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia and New Zealand | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Separator Type | Wet-Process Polyolefin | |

| Dry-Process Polyolefin | ||

| Ceramic-Coated | ||

| By Material | Polypropylene (PP) | |

| Polyethylene (PE) | ||

| Multilayer PP/PE/PP | ||

| Non-woven and Others | ||

| By Thickness | Up to 15 µm | |

| 16 to 20 µm | ||

| 21 to 25 µm | ||

| Above 25 µm | ||

| By Battery Form Factor | Pouch Cells | |

| Cylindrical Cells | ||

| Prismatic Cells | ||

| By Coating Technology | In-line Ceramic Coating | |

| Offline Ceramic Coating | ||

| Functional Polymer Coatings | ||

| Uncoated Polyolefin | ||

| By Application | Automotive EV | |

| Consumer Electronics | ||

| Stationary Energy Storage | ||

| Industrial and Power Tools | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia and New Zealand | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the Lithium ion battery separator market be by 2031?

It is projected to reach USD 23.29 billion by 2031 as volumes scale with electric-vehicle and grid-storage demand.

Which separator type is growing the fastest?

Ceramic-coated wet-process films are forecast to expand at 22.9% CAGR because they improve safety in high-nickel batteries.

Why is North America the fastest-growing region for separators?

Inflation Reduction Act domestic-content rules are driving new U.S. and Mexican separator plants, pushing regional CAGR to 22.0%.

What thickness trend dominates next-generation EV batteries?

Ultra-thin films under 15 µm enable higher energy density and are expected to rise at 25.5% CAGR through 2031.

Who are the leading separator suppliers today?

Asahi Kasei, Toray, SK IE Technology, Celgard, and Entek together hold about 65% of global capacity.

Page last updated on: