Plasma Fractionation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

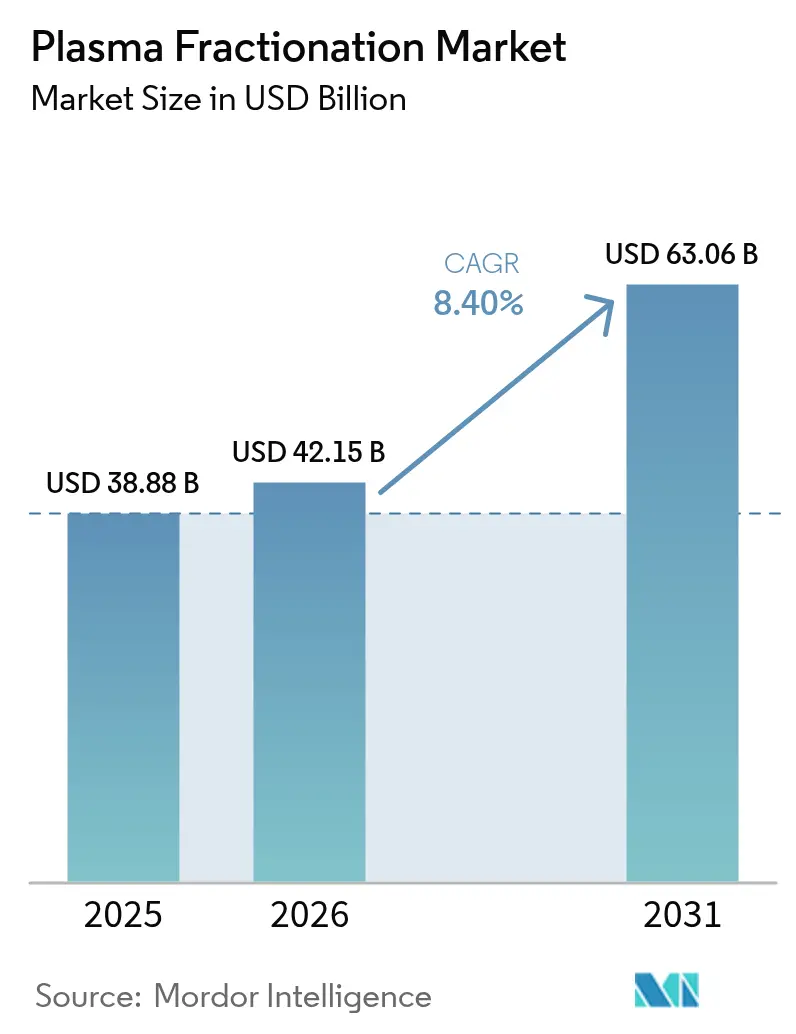

| Market Size (2026) | USD 42.15 Billion |

| Market Size (2031) | USD 63.06 Billion |

| Growth Rate (2026 - 2031) | 8.40% CAGR |

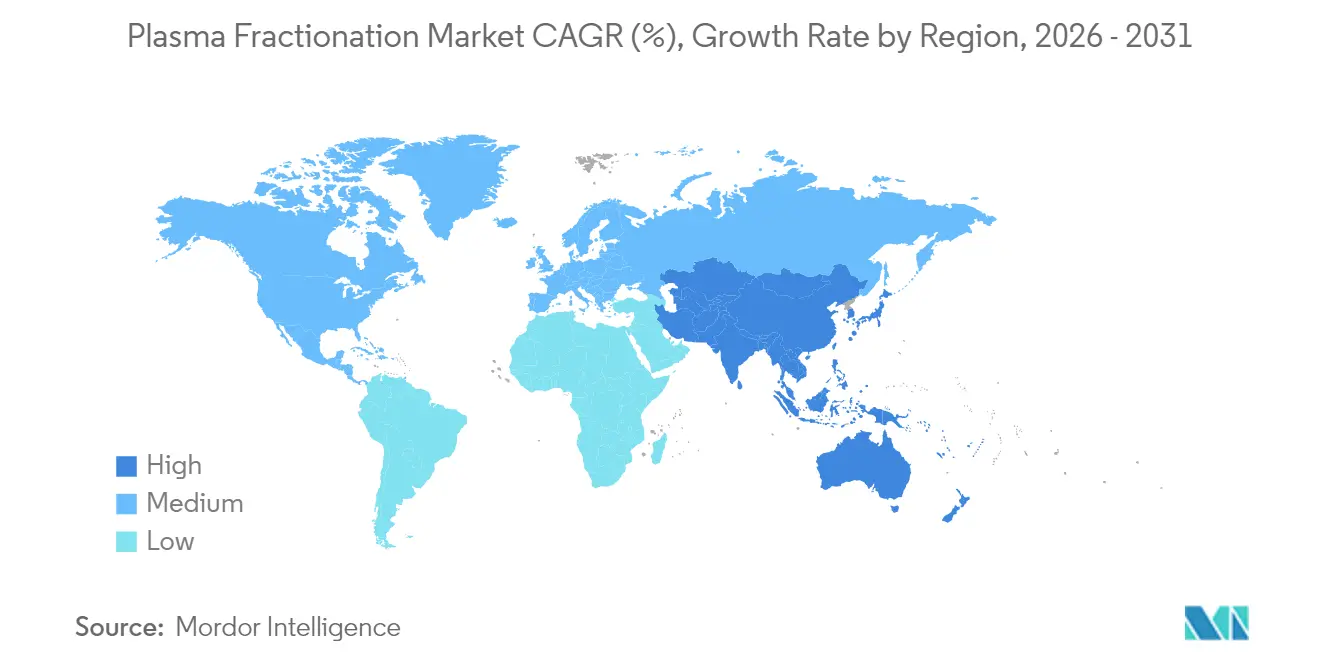

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Plasma Fractionation Market Analysis by Mordor Intelligence

Plasma fractionation market size in 2026 is estimated at USD 42.15 billion, growing from 2025 value of USD 38.88 billion with 2031 projections showing USD 63.06 billion, growing at 8.4% CAGR over 2026-2031. Rising demand for plasma-derived medicinal products in neurology, immunology and critical-care medicine underpins this expansion, while supply security remains a strategic priority for manufacturers. Asia-Pacific is advancing fastest as governments and private operators build domestic plasma collection capacity; at the same time, North America continues to dominate volumes thanks to favorable donor compensation models. Product innovation is accelerating around high-concentration immunoglobulins, next-generation virus-removal filters and automated collection devices, helping companies lower cost per liter and improve manufacturing yields. Competitive intensity is shaped by vertical integration, with leading players operating hundreds of donation centers to secure raw material and cushion supply shocks in the plasma fractionation market.

Key Report Takeaways

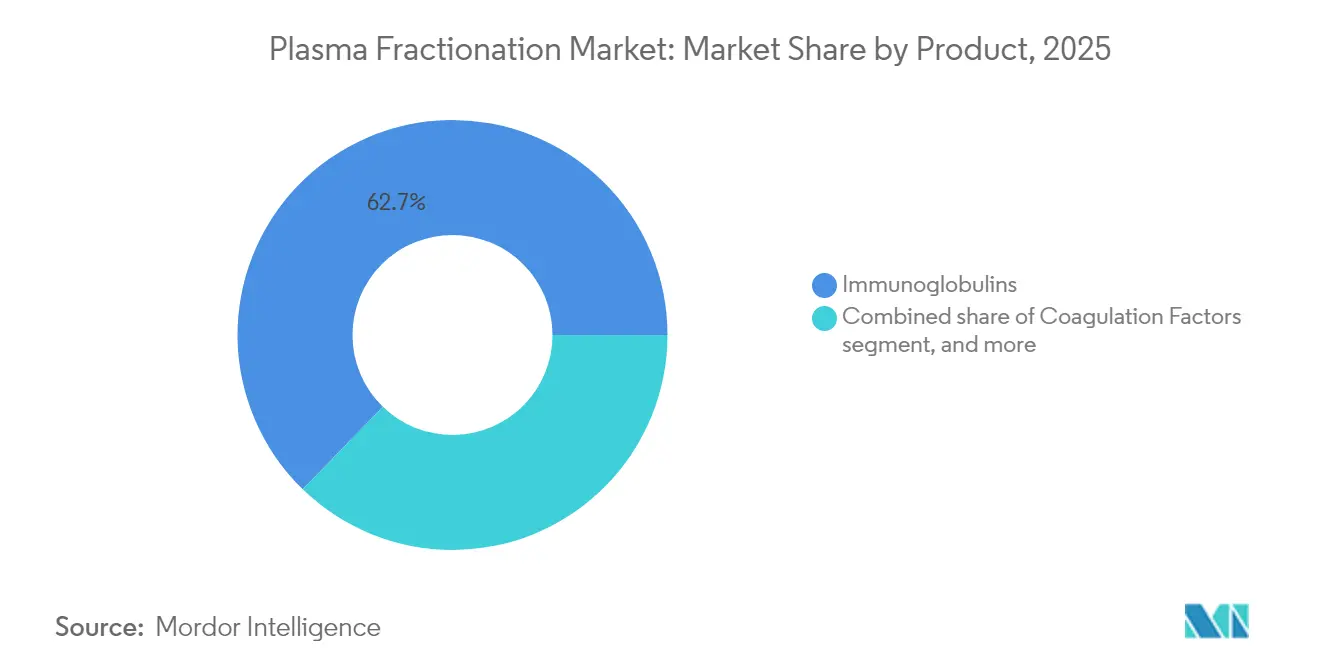

- By product, immunoglobulins led with 62.74% revenue share in 2025; coagulation factors are projected to expand at a 8.97% CAGR to 2031.

- By application, neurology accounted for a 41.66% share in 2025; pulmonology is forecast to expand at a 10.12% CAGR through 2031.

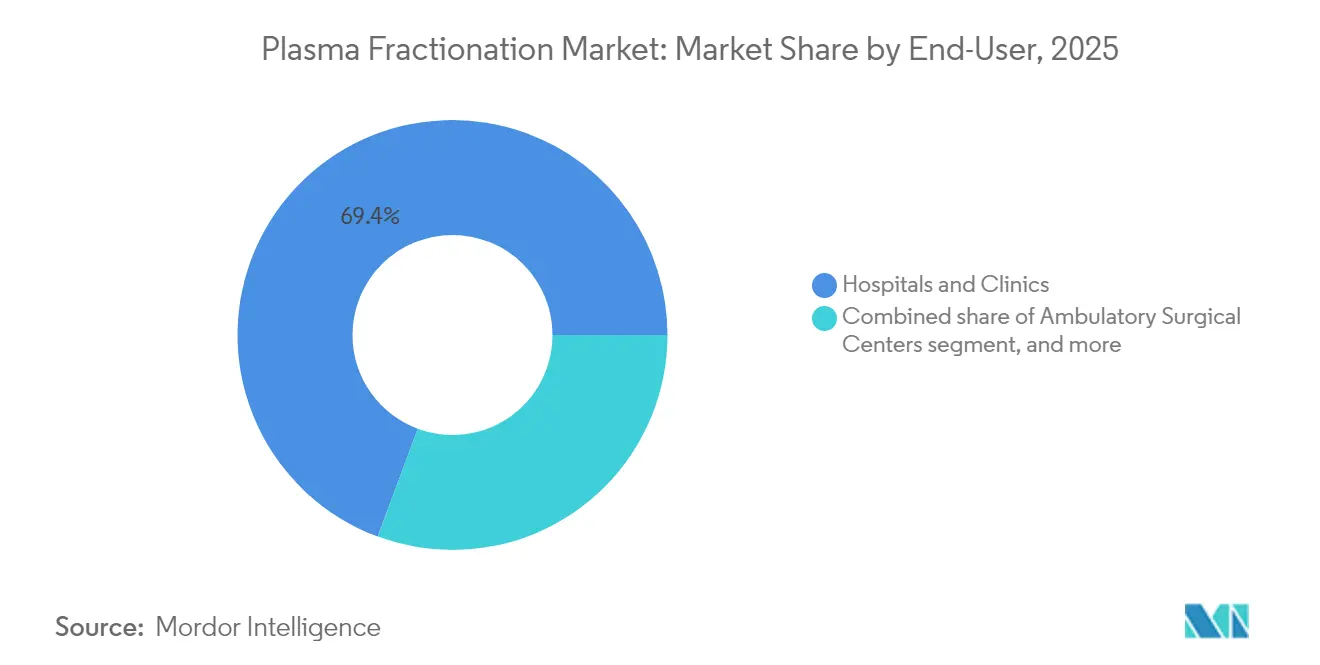

- By end-user, hospitals and clinics held 69.35% share in 2025; other end-users are set to grow at an 10.93% CAGR through 2031.

- By sector, private fractionators commanded 67.41% share in 2025 and are advancing at an 8.18% CAGR through 2031.

- By geography, North America captured 53.05% share in 2025; Asia-Pacific is projected to register a 9.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Plasma Fractionation Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of private donor plasma collection centers | +2.1 | North America; emerging Asia-Pacific | Medium term (2-4 years) |

| Rising adoption of subcutaneous immunoglobulin (SCIG) | +1.8 | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Increasing utilization of albumin in critical-care management | +1.2 | Asia-Pacific (China, India, Indonesia) | Short term (≤ 2 years) |

| Favourable government funding for hemophilia treatment programs | +0.9 | Global, strongest in developed markets | Medium term (2-4 years) |

| Accelerated regulatory approvals for hyperimmune globulins | +1.0 | Global, priority in North America & Europe | Short term (≤ 2 years) |

| Growth of contract fractionation services in emerging economies | +0.7 | Latin America, Africa, South-East Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of Private Donor Plasma Collection Centers

Global operators continue to accelerate site roll-outs to secure supply, reshaping the plasma fractionation market. CSL Plasma deployed the RIKA Plasma Donation System in Houston, trimming session times by 15 minutes and improving donor throughput. Canadian Blood Services is opening new centers—including Thunder Bay in early 2025—to increase domestic collections[1]CBC News, “Canadian Blood Services to Open Thunder Bay Plasma Centre,” cbc.ca. Emerging economies are following suit; Indonesia’s first fractionation plant in Karawang will process 600,000 liters a year, converting discarded plasma into medicines. These moves collectively ease the raw-material bottleneck as global IG demand grows 8-9% annually. Larger, technology-enabled centers also allow companies to diversify sourcing and mitigate region-specific donor constraints, reinforcing supply resilience across the plasma fractionation market.

Rising Adoption of Subcutaneous Immunoglobulin (SCIG)

Patient preference for home therapy and pressure to lower infusion costs are driving rapid uptake of SCIG. XEMBIFY, the first FDA-cleared 20% SCIG for treatment-naïve primary immunodeficiency patients, offers ≥98% IgG purity and favorable tolerability. HYQVIA pairs 10% IG with recombinant hyaluronidase to achieve 93.3% bioavailability while requiring fewer infusion sites. These high-concentration products, alongside smart infusion pumps, facilitate self-administration and free hospital capacity. Payers view SCIG favorably because it reduces chair time and ancillary costs, supporting broader reimbursement. Consequently, specialty pharmacies and infusion centers are scaling distribution networks, reinforcing a structural shift toward decentralized care within the plasma fractionation market.

Increasing Albumin Utilization in Critical Care

Consensus guidance now recommends human serum albumin for fluid resuscitation in septic shock and perioperative management. Clinical experts in China, India and Indonesia emphasize albumin’s oncotic properties to stabilize hemodynamics and mitigate complications[2]HealthManagement.org Staff, “Expert Consensus on Albumin Use,” healthmanagement.org. As healthcare infrastructure improves, Asia-Pacific hospitals are adopting standardized protocols, translating into higher albumin volumes. Local production initiatives, exemplified by Indonesia’s Karawang facility, aim to meet rising demand and reduce import dependence. Short-term growth is further supported by new evidence linking albumin supplementation to lower mortality in complex liver disease, widening its therapeutic scope. These trends collectively lift regional consumption, contributing to sustained expansion of the plasma fractionation market.

Government Funding for Hemophilia Treatment Programs

Public reimbursement schemes are broadening access to prophylactic replacement therapy, stabilizing demand for coagulation factors. Real-world data show comparable annualized bleeding rates between standard half-life and extended half-life products (1.7 vs 1.8 in hemophilia A; 2.1 vs 1.4 in hemophilia B), steering payers toward value-based procurement models. Pilot programs in Europe and Asia now incorporate quality-of-life metrics when allocating budgets, reinforcing steady uptake despite rising recombinant competition. Funding also covers comprehensive care centers that coordinate physiotherapy, psychosocial support and genetic counseling, driving holistic patient management. Such initiatives provide a predictable demand base, enabling manufacturers to optimize production lines and maintain economies of scale within the plasma fractionation market.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply constraints due to donor compensation caps | −1.7 | Europe (spillover worldwide) | Short term (≤ 2 years) |

| Competition from long-acting recombinant coagulation factors | −1.3 | North America & Europe; spreading globally | Long term (≥ 4 years) |

| High batch failure rates with chromatography-intensive lines | −1.0 | Global, heightened in older facilities | Medium term (2-4 years) |

| Limited reimbursement for IVIG in low-income Asian countries | −0.8 | South Asia, parts of ASEAN | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Supply Constraints Due to Donor Compensation Caps

Europe’s ethical ceilings on donor payments threaten supply stability, with forecasts pointing to a 4-8 million-liter shortfall by 2025. Imports already cover 40% of European demand, underscoring vulnerability to external shocks. The proposed Substances of Human Origin regulation seeks a balance between donor protection and material sufficiency, but near-term collection gaps persist. Australia, operating on voluntary donation, imported USD 399.2 million worth of immunoglobulin in 2022-23 as domestic volumes lagged 8% annual demand growth[3]ABC News, “Australia’s Growing Reliance on Imported Plasma,” abc.net.au. These limitations compel fractionators to diversify sourcing, optimize yield per liter and invest in collection technology—yet they still temper growth projections for the plasma fractionation market.

Competition from Long-Acting Recombinant Coagulation Factors

Extended half-life recombinant factors and emerging gene therapies are redefining hemophilia management economics. Etranacogene dezaparvovec offers the prospect of durable correction with a single infusion, challenging lifetime plasma-derived factor consumption. Non-factor agents such as emicizumab further reduce bleeding episodes with subcutaneous dosing, enhancing adherence and patient convenience. With comparable clinical outcomes and supportive reimbursement in advanced markets, recombinant portfolios erode the addressable pool for plasma-derived coagulation factors. Although legacy products retain a role in inhibitor-positive or resource-constrained settings, competitive intensity weighs on segment profitability and moderates overall growth of the plasma fractionation market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Immunoglobulins Retain Leadership, Coagulation Factors Accelerate

Immunoglobulins held 62.74% of the plasma fractionation market share in 2025, reflecting their broad therapeutic footprint in immunology and neurology. Launches of high-concentration formulations like Yimmugo are expected to lift segment revenues, with Grifols projecting USD 1 billion in U.S. sales over seven years. The plasma fractionation market benefits from stable double-digit demand for immunoglobulins, underpinned by expanding indications such as chronic inflammatory demyelinating polyneuropathy. At the same time, manufacturing upgrades—most notably Asahi Kasei Medical’s Planova FG1 filter—raise throughput and lower virus breakthrough risk, supporting volume growth.

Coagulation factors, while representing a smaller revenue base, are forecast to expand at a 8.97% CAGR, the fastest among product lines. Extended prophylaxis protocols foster rising per-patient consumption, and new delivery platforms improve adherence. Nevertheless, recombinant alternatives and non-factor therapies introduce pricing pressure. Albumin retains a sizeable share due to its role in critical care, especially across Asia-Pacific where protocol updates recommend early administration in septic shock. Protease inhibitors, centred on alpha-1 antitrypsin, are gaining momentum in pulmonology as standardized pathways for severe deficiency enter clinical practice. Taken together, product diversification and technological advancement continue to define competitive positioning in the plasma fractionation market.

By Application: Neurology Dominates, Pulmonology Rises Quickly

Neurology applications accounted for 41.66% of 2025 revenues, anchored by intravenous and subcutaneous immunoglobulin use in CIDP and multifocal motor neuropathy. HYQVIA’s 93.3% bioavailability exemplifies modality evolution, offering fewer sites and lower infusion frequency. As disease awareness improves, diagnosis rates climb, further cementing neurology’s primacy in the plasma fractionation market. Growth is reinforced by real-world data demonstrating sustained functional gains and reduced relapse frequency with maintenance dosing.

Pulmonology marks the fastest-growing segment, slated to post a 10.12% CAGR to 2031. Alpha-1 antitrypsin replacement therapy drives this surge, with European consensus guidelines streamlining patient selection and dosing. Research linking arterial stiffness to cardiovascular risk in deficiency patients underscores wider systemic benefits, potentially unlocking new reimbursement pathways. Immunology remains a core indication set, while hematology confronts recombinant competition. Critical-care adoption of albumin in trauma and surgical contexts bolsters cross-department utilization, broadening application diversity. Collectively, these dynamics ensure the plasma fractionation market stays responsive to shifting clinical priorities.

By End-User: Hospitals Command Volumes, Alternative Sites Grow

Hospitals and clinics captured 69.35% of global revenues in 2025, reflecting their central role in administering intravenous therapies and managing acute indications. Complex infusion protocols, adverse-event monitoring and reimbursement pathways keep hospital pharmacies at the heart of the plasma fractionation market. As hospitals adopt integrated care pathways, utilization rates of albumin and coagulation factors rise, sustaining volume leadership. Investments in automated blood-component processors, including the Reveos system, enable transfusion services to cut processing steps by 65% and free resources for higher-value activities.

The “other end-users” category—which encompasses home care, specialty pharmacies and infusion suites—is projected to grow at 10.93% CAGR, powered by SCIG adoption and payer encouragement of home-based models. Improved training programs and remote monitoring technologies, such as connected pumps, enhance safety and adherence. Ambulatory surgical centers represent a niche yet expanding destination for albumin use in hemodynamic stabilization. Blood banks and plasma collection centers, while upstream, influence downstream availability by securing the raw material that sustains the plasma fractionation market.

By Sector: Private Fractionators Drive Scale and Innovation

Private players commanded 67.41% of 2025 revenues and exhibit the fastest growth trajectory at 8.18% CAGR. Octapharma’s plan to lift production capacity by 50% before 2028 typifies aggressive expansion strategies. These firms leverage flexible capital allocation, advanced IT infrastructure and global sourcing networks to optimize cost per liter and maintain quality. Vertically integrated models spanning donation through final fill-and-finish help private operators manage margins amid pricing pressure, securing competitive advantage in the plasma fractionation market.

Public fractionators remain pivotal in regions prioritizing self-sufficiency, albeit with more conservative investment horizons. Collaborations—such as Indonesia’s joint venture between the national sovereign wealth fund and SK Plasma—illustrate hybrid models that blend state oversight with private technological expertise. Technology-transfer agreements and contract manufacturing bolster public capacity without duplicating expensive R&D pipelines. Over the forecast period, blended ecosystems of private and public entities will continue to evolve, balancing access, affordability and strategic autonomy across the plasma fractionation market.

Geography Analysis

North America remains the epicenter of the plasma fractionation market, holding 53.05% of revenue in 2025. The United States alone accounts for 70% of global source plasma, supported by donor compensation that sustains a dense network of nearly 1,200 centers. The Congressional Plasma Caucus spotlights bipartisan support for uninterrupted immunoglobulin access, while technological upgrades like CSL’s RIKA system shorten donation times and improve throughput. Advanced regulatory processes facilitate rapid approval of next-generation filters and formulations, reinforcing the region’s supply chain robustness.

Asia-Pacific represents the fastest-growing arena, anticipated to record a 9.18% CAGR to 2031. Governments in Indonesia, China and India are investing in domestic fractionation plants to reduce reliance on imports. Indonesia’s Karawang facility will convert 600,000 liters annually into high-value products, exemplifying a shift toward self-sufficiency. Nonetheless, supply imbalances persist: Australia imported USD 399.2 million worth of immunoglobulin in 2022-23, with demand growing 8% each year. Strategic transactions, such as CSL’s divestiture of its Wuhan plasma portfolio to Rongsheng Pharmaceutical for USD 185 million, realign footprints for better local market fit.

Europe faces structural headwinds from donor compensation caps, leading to 40% dependence on U.S. plasma. Proposed SoHO regulations aim to boost donor retention while preserving ethical standards, yet near-term scarcity remains a reality. Manufacturing expertise and established distribution channels temper risk, but capacity utilization hinges on raw material flows. Latin America, the Middle East and Africa collectively contribute a modest share today, yet rising healthcare expenditure and wider insurance coverage are opening access to plasma-derived therapies. Long-term upside lies in infrastructure investment and public-private partnerships, gradually enlarging regional slices of the plasma fractionation market.

Mordor Intelligence provides coverage of the plasma fractionation market across other key regional markets. Detailed country-level analysis extends to India incorporating local coverage and market participation, as required.

Competitive Landscape

The plasma fractionation market is moderately concentrated: CSL Behring, Grifols and Takeda control an estimated 70% of global capacity, leveraging vertically integrated operations to secure raw material and maintain quality leadership. Cost-efficient sourcing is central; CSL operates approximately 350 donation centers worldwide, while Grifols’ Operational Improvement Plan reduced cost per liter by 22% in 2024. Takeda’s dual supply-chain hubs in the U.S. and Europe provide geographic redundancy, enabling agile response to regional demand spikes.

Innovation differentiates competitors. Asahi Kasei Medical’s Planova FG1 filter delivers seven-fold higher flux, slashing virus-filtration bottlenecks and trimming batch cycles. Grifols advanced ESG scoring to 70 in the 2024 Corporate Sustainability Assessment, appealing to ethically inclined institutional investors. CSL’s Program REACH modernizes donor engagement with mobile scheduling and loyalty analytics, boosting repeat donations and data accuracy.

Governance reforms signal strategic evolution. Grifols separated management from family ownership in 2024, appointing Nacho Abia as CEO to sharpen operational focus and investor communication. Regional challengers are emerging: Kedrion opened a production hub in Bolognana, Italy, to scale hyperimmune globulin output, while Australian start-up Aegros is raising USD 20 million to commercialize high-yield fractionation technology. These developments hint at gradual dilution of incumbent share, although scale advantages remain formidable in the plasma fractionation market.

Plasma Fractionation Industry Leaders

CSL Behring

Grifols S.A

Octapharma

Kedrion S.p.A

Bio Products Laboratory Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: ADMA Biologics reported preliminary FY 2024 revenue of USD 417-425 million and projected FY 2025 revenue above USD 485 million.

- October 2024: Asahi Kasei Medical introduced Planova FG1, offering seven-times higher flux than earlier filters.

- October 2024: Terumo Blood and Cell Technologies launched the Reveos Automated Blood Processing System in the U.S., cutting processing steps by 65%.

- October 2024: Grifols achieved a Corporate Sustainability Assessment score of 70 points.

- October 2024: CSL Plasma deployed the RIKA Plasma Donation System in Houston, reducing donation time by 15 minutes.

Global Plasma Fractionation Market Report Scope

As per the scope of the report, plasma fractionation is defined as the general process of separating the various components of blood plasma obtained via blood fractionation. Plasma contains multiple proteins, including immunoglobulins, albumin, and coagulation proteins. The Plasma Fractionation Market is segmented by product (immunoglobulins, platelets, coagulation factor concentrate, albumin, and other products), application (Neurology, Immunology, Hematology, and other applications), end-user (hospitals and clinics, clinical research laboratories, and other end-users), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major global regions. The report offers the value in (USD million) for the above segments.

| Immunoglobulins | Intravenous Immunoglobulin (IVIG) |

| Subcutaneous Immunoglobulin (SCIG) | |

| Other Immunoglobulins | |

| Coagulation Factors | |

| Albumin | |

| Protease Inhibitors (C1-Esterase, Alpha-1 Antitrypsin) | |

| Other Plasma-Derived Products |

| Neurology |

| Immunology |

| Hematology |

| Pulmonology |

| Critical Care & Trauma |

| Other Applications |

| Hospitals & Clinics |

| Ambulatory Surgical Centers |

| Plasma Collection Centers & Blood Banks |

| Other End-Users |

| Private Fractionators |

| Public Fractionators |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Immunoglobulins | Intravenous Immunoglobulin (IVIG) |

| Subcutaneous Immunoglobulin (SCIG) | ||

| Other Immunoglobulins | ||

| Coagulation Factors | ||

| Albumin | ||

| Protease Inhibitors (C1-Esterase, Alpha-1 Antitrypsin) | ||

| Other Plasma-Derived Products | ||

| By Application | Neurology | |

| Immunology | ||

| Hematology | ||

| Pulmonology | ||

| Critical Care & Trauma | ||

| Other Applications | ||

| By End-User | Hospitals & Clinics | |

| Ambulatory Surgical Centers | ||

| Plasma Collection Centers & Blood Banks | ||

| Other End-Users | ||

| By Sector | Private Fractionators | |

| Public Fractionators | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the plasma fractionation market?

The plasma fractionation market size stands at USD 42.15 billion in 2026 and is projected to reach USD 63.06 billion by 2031.

Which product segment holds the largest share of the plasma fractionation market?

Immunoglobulins lead, accounting for 62.74% of revenues in 2025.

Which region is expected to grow fastest in plasma fractionation?

Asia-Pacific is forecast to record a 9.18% CAGR from 2026 to 2031.

Who are the leading companies in the plasma fractionation industry?

CSL Behring, Grifols and Takeda together hold about 70.0% of global capacity.

Why are subcutaneous immunoglobulins gaining popularity?

SCIG products allow home-based self-administration, reduce hospital dependence and maintain comparable efficacy to intravenous formulations.

Page last updated on: