Therapeutic Plasma Exchange Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.33 Billion |

| Market Size (2031) | USD 1.91 Billion |

| Growth Rate (2026 - 2031) | 7.42% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

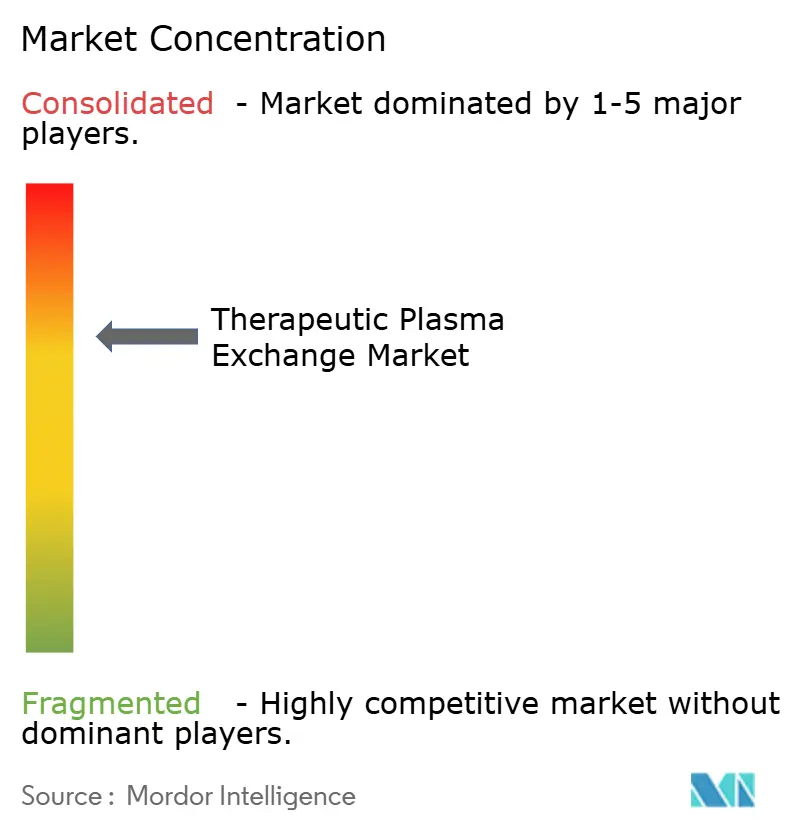

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Therapeutic Plasma Exchange Market Analysis by Mordor Intelligence

Therapeutic plasma exchange market size in 2026 is estimated at USD 1.33 billion, growing from 2025 value of USD 1.24 billion with 2031 projections showing USD 1.91 billion, growing at 7.42% CAGR over 2026-2031. This expansion reflects rising prevalence of severe autoimmune and neurological diseases, growing clinical validation across new indications, and a decisive shift from hospital-centric procedures toward decentralized and home-based care models. Portable apheresis devices shorten treatment times, reduce infection exposure, and align with patients’ preference for receiving chronic therapies in familiar environments. Reimbursement upgrades in the United States and Western Europe have removed major financial barriers for frequent procedures, while government-backed localization programs in Asia-Pacific multiply production capacity for both machines and consumables. Technological convergence of membrane filtration with selective adsorption columns is reshaping equipment design as providers demand systems capable of multiplex functionality. At the same time, alternative drug classes such as FcRn inhibitors are intensifying competitive pressure, spurring equipment manufacturers to bundle software, disposables, and service contracts into integrated value propositions.

Key Report Takeaways

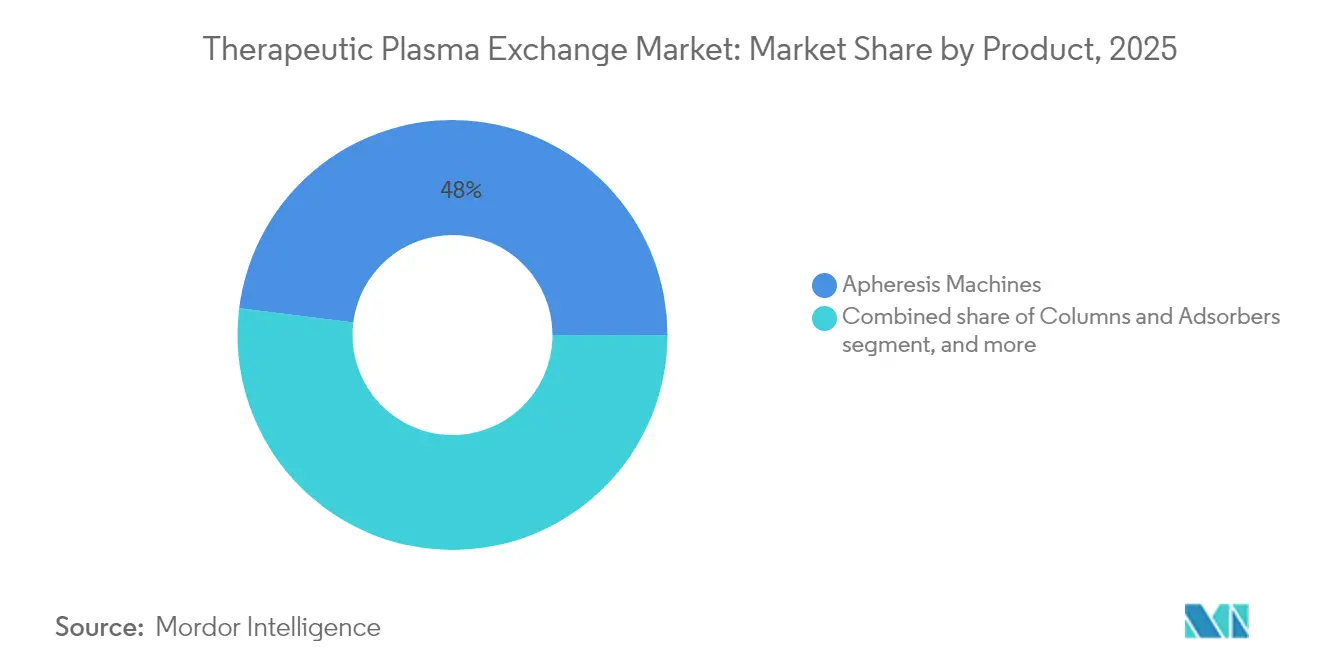

- By product type, apheresis machines led with 48.02% of therapeutic plasma exchange market share in 2025. Columns and adsorbers are poised for a 9.49% CAGR through 2031.

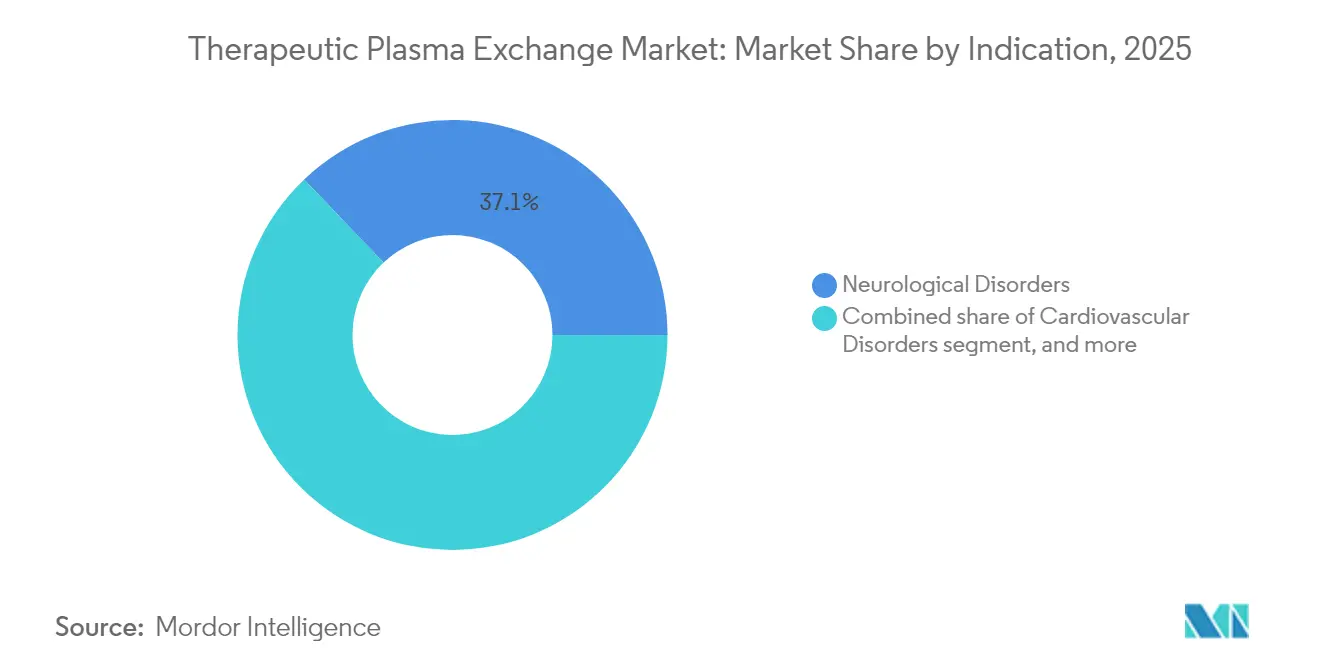

- By indication, neurological disorders accounted for 37.12% of the therapeutic plasma exchange market size in 2025, whereas transplant rejection applications are forecast to expand at 9.63% CAGR.

- By end-user, home-care settings captured 61.78% share of the therapeutic plasma exchange market in 2025 and are advancing at a 10.29% CAGR to 2031.

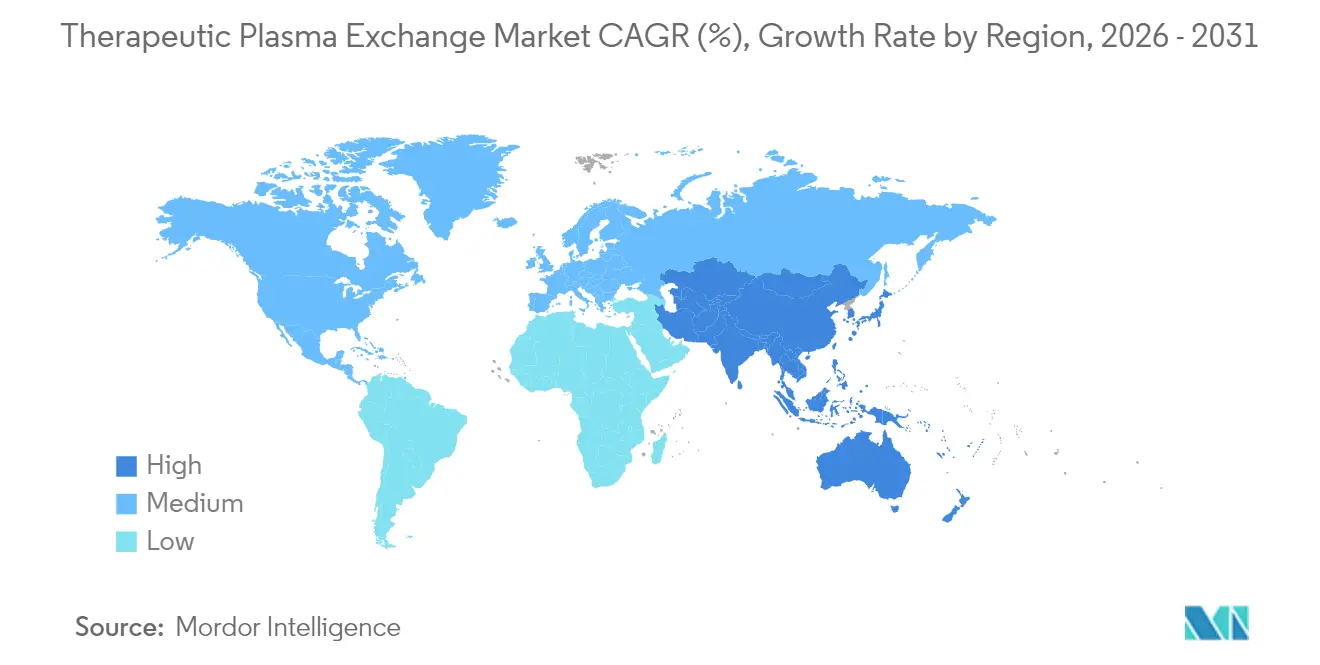

- By geography, North America held 40.66% share of the therapeutic plasma exchange market in 2025, while Asia-Pacific is projected to register the fastest regional CAGR at 8.31% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Therapeutic Plasma Exchange Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising burden of autoimmune and neurological disorders | +2.1% | Global, concentrated in North America & Europe | Long term (≥ 4 years) |

| Increasing clinical evidence supporting expanded indications | +1.8% | Global, early adoption in developed markets | Medium term (2-4 years) |

| Favorable reimbursement policies in developed nations | +1.4% | North America & Europe; selective APAC markets | Short term (≤ 2 years) |

| Growing adoption of therapeutic plasma exchange in cardiac surgery | +0.9% | Global, early gains in specialized cardiac centers | Medium term (2-4 years) |

| Surge in adoption of adsorption columns in Asian hospitals | +1.2% | Asia-Pacific, especially China & Japan | Medium term (2-4 years) |

| Emergence of portable apheresis devices for out-of-hospital care | +1.6% | Global, with rapid uptake in home-care markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Autoimmune and Neurological Disorders

Global incidence of chronic autoimmune diseases continues to climb, with Guillain–Barré syndrome and myasthenia gravis patients showing 92% and 81.25% response rates respectively when treated with therapeutic plasma exchange. Healthcare systems increasingly recognize plasma exchange as a rescue therapy for refractory flares, a trend amplified by aging populations in high-income countries where disease severity is greater. Early evidence also suggests plasma exchange may mitigate long-COVID symptoms by removing inflammatory mediators, thereby widening the patient pool. Collectively these epidemiological and clinical factors generate sustained procedure demand and underpin multi-year equipment replacement cycles.

Increasing Clinical Evidence Supporting Expanded Indications

The American Society for Apheresis assigned therapeutic plasma exchange a Category I-III recommendation across 87 diseases in its 2024 guidelines, highlighting broadening indication scope[1]American Society for Apheresis, “Guidelines on the Use of Therapeutic Apheresis in Clinical Practice—2024 Update,” apheresis.org. Randomized studies published in 2025 demonstrated significant reductions in cytokine levels among COVID-19 patients with neurological complications following exchange sessions. Pediatric data from the Egyptian Pediatric Association Gazette confirmed safety outcomes comparable to adults, encouraging earlier intervention in children. Growing evidence base lowers prescriber hesitancy, accelerates hospital protocol integration, and fuels incremental procedural volume across specialties.

Favorable Reimbursement Policies in Developed Nations

Medicare’s 2025 outpatient fee schedule assigns USD 431.83 per plasma exchange administration, aligning federal coverage with cost-effectiveness studies that place per-session treatment costs at nearly half those of intravenous immunoglobulin. Similar tariff adjustments in Germany and France have created immediate financial incentives for hospitals to favor plasma-based regimens over more expensive biologics. Private insurers are mirroring these revisions, broadening coverage to new autoimmune indications such as sickle cell crises. Improved payment certainty boosts capital purchase justification for advanced systems and accelerates amortization of high-value consumables.

Growing Adoption of Therapeutic Plasma Exchange in Cardiac Surgery

Complex cardiac cases increasingly rely on extracorporeal blood management strategies. NHS England allocated USD 1.5 million to deploy 25 Spectra Optia devices dedicated to sickle-cell patients needing surgical interventions, projecting up to 10,000 additional annual procedures. Spectra’s ability to perform red-cell exchange concurrently with renal replacement reduces transfusion burden and ICU length of stay, compelling leading heart centers in the United States and Japan to adopt similar protocols. Cardiac programs’ high case revenue offsets equipment costs, giving this clinical niche outsized influence on overall procedural demand.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and consumable costs of apheresis systems | –1.2% | Global, pronounced in emerging markets | Long term (≥ 4 years) |

| Limited availability of skilled apheresis personnel | –0.8% | Global, acute in rural & developing regions | Medium term (2-4 years) |

| Vulnerability of plasma supply chain during global crises | –1.0% | Global, most visible in Europe & North America | Short term (≤ 2 years) |

| Regulatory uncertainty regarding pediatric applications | –0.6% | Global, with stricter oversight in EU & U.S. | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital and Consumable Costs of Apheresis Systems

Best-in-class devices exceed USD 100,000 per unit, while single-use kits add USD 1,000-1,200 per procedure, costs that small hospitals in Latin America and Africa struggle to justify. Post-pandemic supply chain shocks elevated resin and membrane prices, inflating column costs by 15% in 2024. Although OEMs offer leasing, pay-per-use, and service bundles, strained health budgets in emerging economies translate into slower replacement cycles and deferred adoption of next-generation platforms.

Limited Availability of Skilled Apheresis Personnel

Each therapeutic plasma exchange session requires nurses and physicians trained in anticoagulation management, real-time hemodynamic monitoring, and emergency complication handling. Surveys by the Southeast Asian Therapeutic Plasma Exchange Consortium found less than one certified operator per million population in Indonesia and Vietnam. Aging workforces in Europe predict a 30% retirement-driven attrition of senior specialists by 2030 unless offset by accelerated training pipelines. Personnel shortages directly cap daily procedure capacity, restraining revenue generation even where equipment is available.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Technology Convergence Reshapes Equipment Landscape

Apheresis machines generated 48.02% of the therapeutic plasma exchange market size in 2025, underscoring their status as the procedural hub across all disease categories. Columns and adsorbers, however, are advancing at a 9.49% CAGR to 2031 as clinicians demand selective pathogen removal with minimal plasma substitution. Integrated devices now combine centrifugal separation with adsorption cartridges, allowing operators to toggle between whole-plasma removal and antibody-specific filtration within the same console. Manufacturers differentiate through sensor-driven anticoagulant titration, closed-system disposables, and cloud-based performance analytics that cut procedure times below 35 minutes.

Recurring consumables revenue remains pivotal: tubing sets, saline, anticoagulants, and replacement fluids contribute nearly 60% of lifetime customer value per installed base. Market incumbents thus bundle hardware leases with long-term consumable contracts, locking in predictable cash flows. Software updates enabling remote troubleshooting and protocol libraries further shift competition from price to platform ecosystem residency, deepening customer dependence and throttling potential displacement by low-cost entrants.

By Indication: Neurological Applications Drive Core Growth

Neurological disorders represented 37.12% of therapeutic plasma exchange market share in 2025 and continue to form the clinical backbone of procedural demand. Rapid antibody clearance markedly reduces ventilator dependence in Guillain–Barré syndrome and cuts ICU stay length in myasthenic crises. Transplant rejection management delivers 9.63% CAGR through 2031, propelled by rising organ donation rates in China, India, and Brazil, and by the integration of plasma exchange into antibody-mediated rejection protocols published by the International Society for Heart and Lung Transplantation. Cardiovascular applications, notably peri-operative red-cell exchange, are reaping spillover benefits from that protocolization, while renal and hematology indications sustain baseline utilization across dialysis centers and hematology wards.

Emerging domains such as long-COVID, pediatric autoimmune encephalitis, and catastrophic antiphospholipid syndrome broaden the therapeutic canvas. As evidence accrues, payers are adding these conditions to reimbursement rosters, ensuring that procedural volume growth is not solely tied to classic autoimmune cohorts. The therapeutic plasma exchange market therefore secures a defensible core in neurology while layering new revenue from rapidly scaling post-transplant and infectious disease niches.

By End-User: Home Care Revolution Transforms Treatment Delivery

Home-based therapy commanded 61.78% share of the therapeutic plasma exchange market in 2025 and is forecast for a 10.29% CAGR to 2031, illustrating a decisive out-of-hospital migration. Portable devices weigh less than 18 kg and plug into standard electrical outlets, allowing certified nurses to conduct sessions in patient living rooms while real-time vitals upload to cloud dashboards. The pandemic catalyzed broad payer acceptance of remote monitoring codes, and many U.S. insurers now reimburse travel-to-home sessions at parity with outpatient departments.

Hospitals remain indispensable for complicated multi-organ cases, yet even tertiary centers acknowledge that reserving in-house resources for acute crises improves capacity utilization. Ambulatory surgery centers fill the intermediate niche, offering same-day procedures for stable patients without full inpatient overheads. Start-up service providers are responding with franchise-style mobile units that bundle equipment, staffing, and consumables under subscription pricing, challenging legacy hospital-only revenue models.

Geography Analysis

North America dominated with 40.66% of therapeutic plasma exchange market share in 2025, buoyed by robust Medicare and private-payer reimbursement that offsets high consumable costs. FDA clearance of the Aurora Xi plasmapheresis system in 2025 added competition and fostered price moderation among incumbent consoles. Canada’s provinces recently harmonized fee schedules with U.S. rates, reducing cross-border procedure leakage and stabilizing domestic demand.

Asia-Pacific is the fastest-growing region at an 8.31% CAGR, propelled by China’s Healthy China 2030 plan that funds apheresis infrastructure in 300 county hospitals. Terumo’s USD 15 million Hangzhou facility expansion secures local supply of Spectra Optia kits, lowering import tariffs and slashing delivery times by 40%. Japan and South Korea maintain mature installed bases, yet upside remains from demographic aging and transplant program expansions. India’s medical tourism growth funnels international patients into private hospitals offering competitive plasma exchange packages.

Europe shows steady but slower expansion. Although universal insurance coverage facilitates access, plasma supply shortages in 2024 forced many EU countries to import 40% of their raw plasma from the United States, prompting the European Blood Alliance to seek two million additional donors. Middle East and Africa markets are nascent but supported by Gulf Cooperation Council investments in tertiary care hubs, while Brazil and Argentina spearhead South American adoption through public-private hospital networks.

Competitive Landscape

The therapeutic plasma exchange market exhibits moderate consolidation, with Terumo, Fresenius Kabi, and Baxter controlling an estimated 70% of global installed consoles. Terumo’s Rika system reached 98 U.S. center installations by late 2024 and targets 25% market penetration by 2027 through faster collection times and donor-tailored volumes. Fresenius Kabi gained FDA clearance for its Adaptive Nomogram software, which dynamically adjusts flow rates to optimize collection volumes, reinforcing its disposable-driven revenue flywheel.

Baxter divested its USD 3.8 billion Kidney Care arm to concentrate on high-growth infusion and apheresis segments, signaling strategic commitment to advanced blood purification platforms. Competitive threat from FcRn inhibitors continues to mount as Argenx reported USD 1.2 billion in 2024 efgartigimod sales, validating non-procedural therapeutic alternatives.

In response, device makers emphasize hybrid systems that couple plasma removal with adsorption cartridges, seeking to preserve procedural relevance by delivering quicker antibody reduction than biologics alone. Midsize entrants focus on low-cost portable consoles for emerging markets, but stringent regulatory requirements and entrenched hospital service contracts keep entry barriers high.

Therapeutic Plasma Exchange Industry Leaders

Asahi Kasei Corporation

Baxter International Inc

Terumo Corporation

B. Braun Melsungen AG

Fresenius Kabi AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Terumo Blood and Cell Technologies partnered with Join Parachute to scale deployment of the Rika Plasma Donation System, tailoring donation volumes to individual donor physiology.

- April 2025: Asahi Kasei Life Science began operations with expanded Planova virus removal filter capacity in Shizuoka and Illinois, supporting biotherapeutic purification pipelines.

- February 2025: Sanquin Blood Supply Foundation signed a 10-year agreement to implement Reveos automated processing, streamlining 400,000 annual whole-blood donations.

- February 2025: NHS England invested USD 1.5 million in 25 Spectra Optia systems to elevate sickle-cell disease care capacity.

- December 2024: Terumo announced a USD 15 million localization investment to manufacture Spectra Optia and Trima Accel at its Hangzhou site.

Global Therapeutic Plasma Exchange Market Report Scope

Therapeutic plasma exchange (TPE), also known as plasmapheresis is an extracorporeal blood purification technique that removes pathogenic substances such as pathogenic autoantibodies, immune complexes, cryoglobulins and cholesterol-containing lipoproteins from the plasma of patients and replaces with substitution fluid such as albumin solution, or often fresh frozen plasma. TPE is used in the treatment of various autoimmune diseases, renal disorders, hematology disorders, etc, which is likely to drive the growth of the market.

| Apheresis Machines |

| Filters |

| Columns & Adsorbers |

| Disposables (Tubing, Kits) |

| Software & Services |

| Neurological Disorders |

| Cardiovascular Disorders |

| Hematology Disorders |

| Renal Disorders |

| Transplant Rejection |

| Other Indications |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics |

| Home Care Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Apheresis Machines | |

| Filters | ||

| Columns & Adsorbers | ||

| Disposables (Tubing, Kits) | ||

| Software & Services | ||

| By Indication | Neurological Disorders | |

| Cardiovascular Disorders | ||

| Hematology Disorders | ||

| Renal Disorders | ||

| Transplant Rejection | ||

| Other Indications | ||

| By End-User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics | ||

| Home Care Settings | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the therapeutic plasma exchange market in 2031?

The market is forecast to reach USD 1.91 billion by 2031.

Which product segment is growing fastest?

Columns and adsorbers, thanks to their 9.49% CAGR tied to antibody-selective removal capabilities.

Why are home-based therapeutic plasma exchange procedures increasing?

Portable consoles, payer parity for remote sessions, and patient preference for reduced hospital exposure are driving a 10.29% CAGR in the home-care segment.

Which region will record the strongest growth through 2031?

Asia-Pacific, supported by public health investments and local manufacturing, is set to post an 8.31% CAGR.

How are alternative therapies affecting equipment manufacturers?

Rising sales of FcRn inhibitors push device makers to add selective adsorption and service bundling to preserve their value proposition.

Page last updated on: