Plasma Protein Therapeutics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

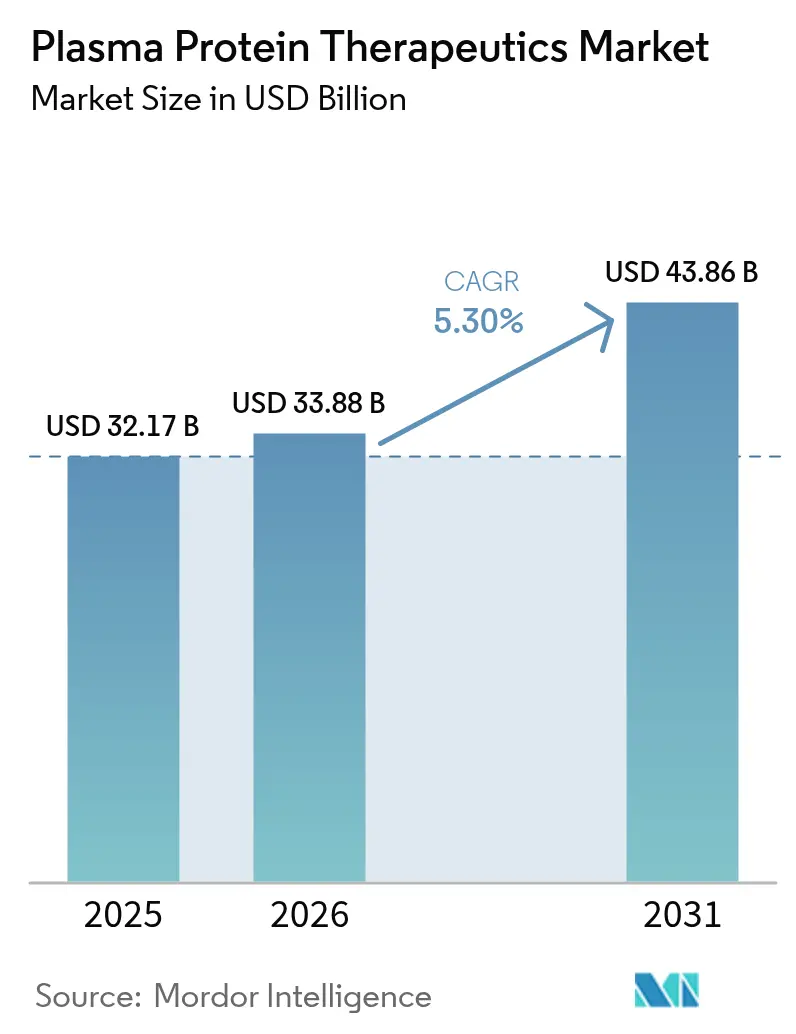

| Market Size (2026) | USD 33.88 Billion |

| Market Size (2031) | USD 43.86 Billion |

| Growth Rate (2026 - 2031) | 5.30% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Plasma Protein Therapeutics Market Analysis by Mordor Intelligence

The Plasma Protein Therapeutics market size is expected to grow from USD 32.17 billion in 2025 to USD 33.88 billion in 2026 and is forecast to reach USD 43.86 billion by 2031 at 5.3% CAGR over 2026-2031.

Immunoglobulins remain the economic backbone of the plasma protein therapeutics market, capturing 42.60% of 2024 revenues, while next-generation collection technologies—such as the FDA-cleared Rika Plasma Donation System—are cutting donation times from 75 to 35 minutes, easing long-standing supply constraints. Asia-Pacific is advancing at a projected 7.87% CAGR on the back of major infrastructure projects, including Indonesia’s 600,000-liter fractionation facility. Competitive momentum is underlined by a 15% profit leap at CSL Behring in 2024 and Grifols’ governance overhaul aimed at quicker execution. Regulatory headwinds persist, yet yield-boosting tools such as Haemonetics’ iNomi algorithm, which lifts plasma volume by 9–12%, are widening margins and bolstering supply plasma.

Key Report Takeaways

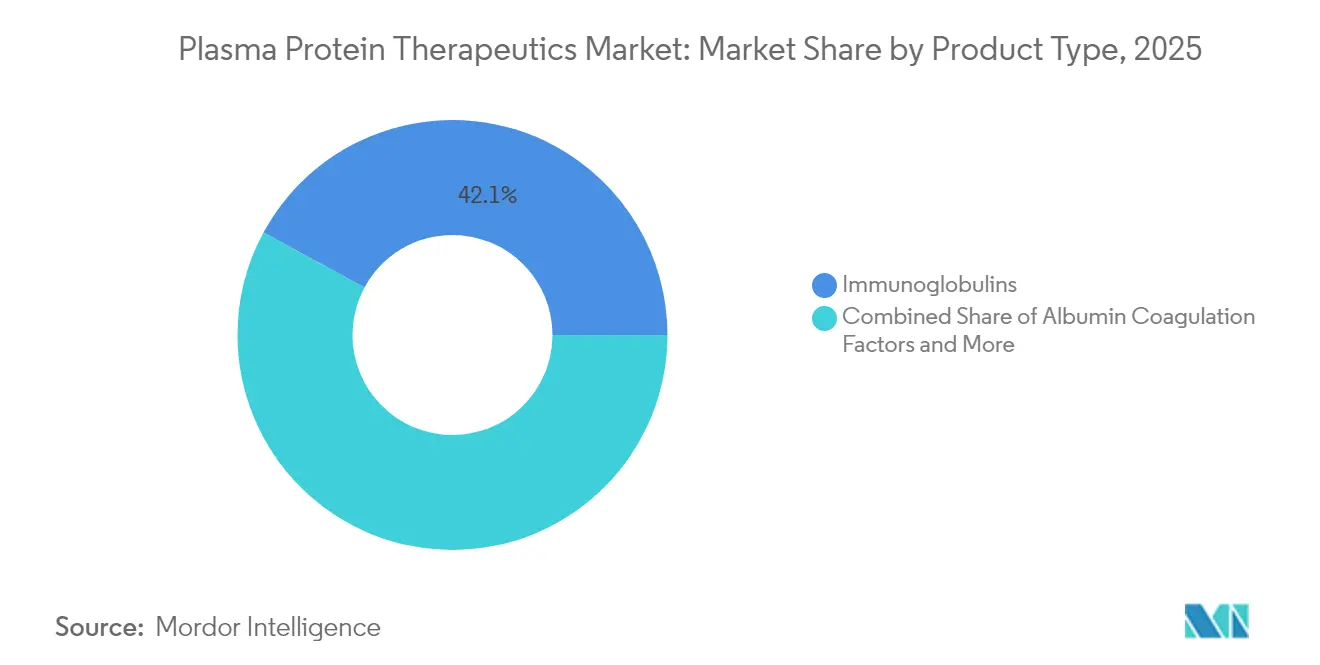

- By product type, immunoglobulins led with 42.10% of plasma protein therapeutics market share in 2025, while alpha-1 antitrypsin is projected to expand at a 5.92% CAGR through 2031.

- By application, immunology & neurology disorders accounted for 47.30% share of the plasma protein therapeutics market size in 2025, whereas respiratory disorders are set to grow at 7.31% CAGR to 2031.

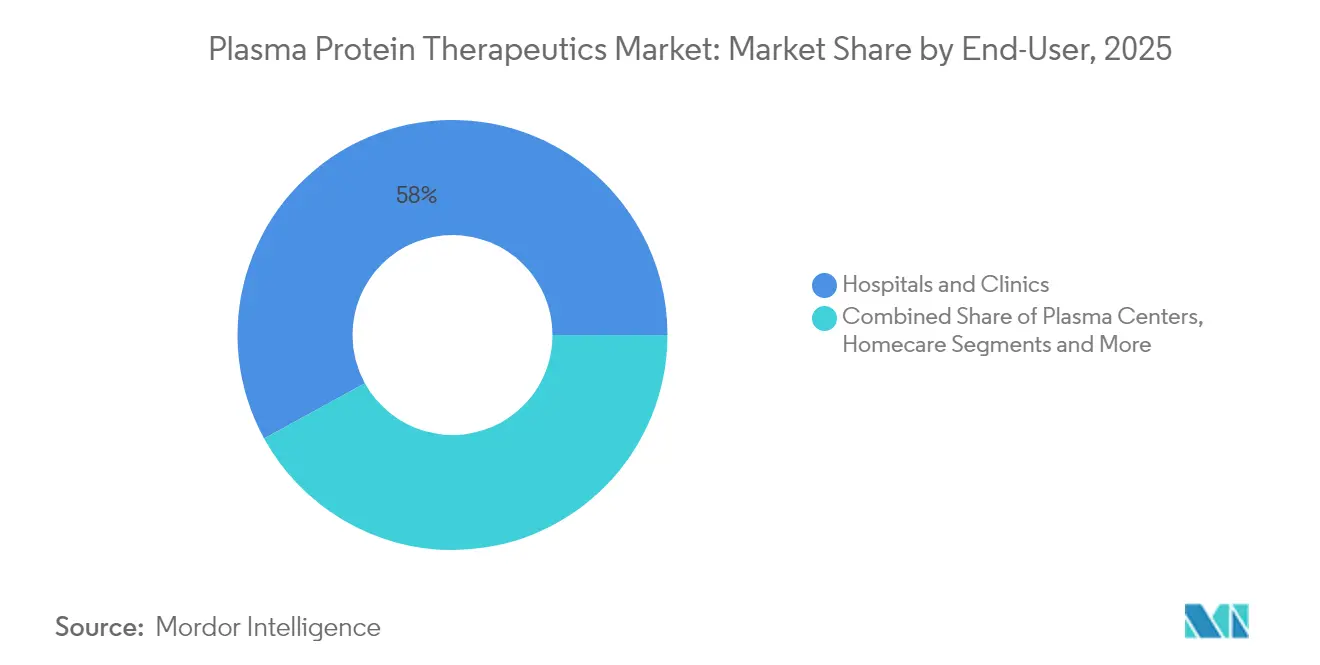

- By end-user, hospitals and clinics held 58.00% of revenues in 2025; plasma centers record the fastest projected CAGR at 6.35% for 2026-2031.

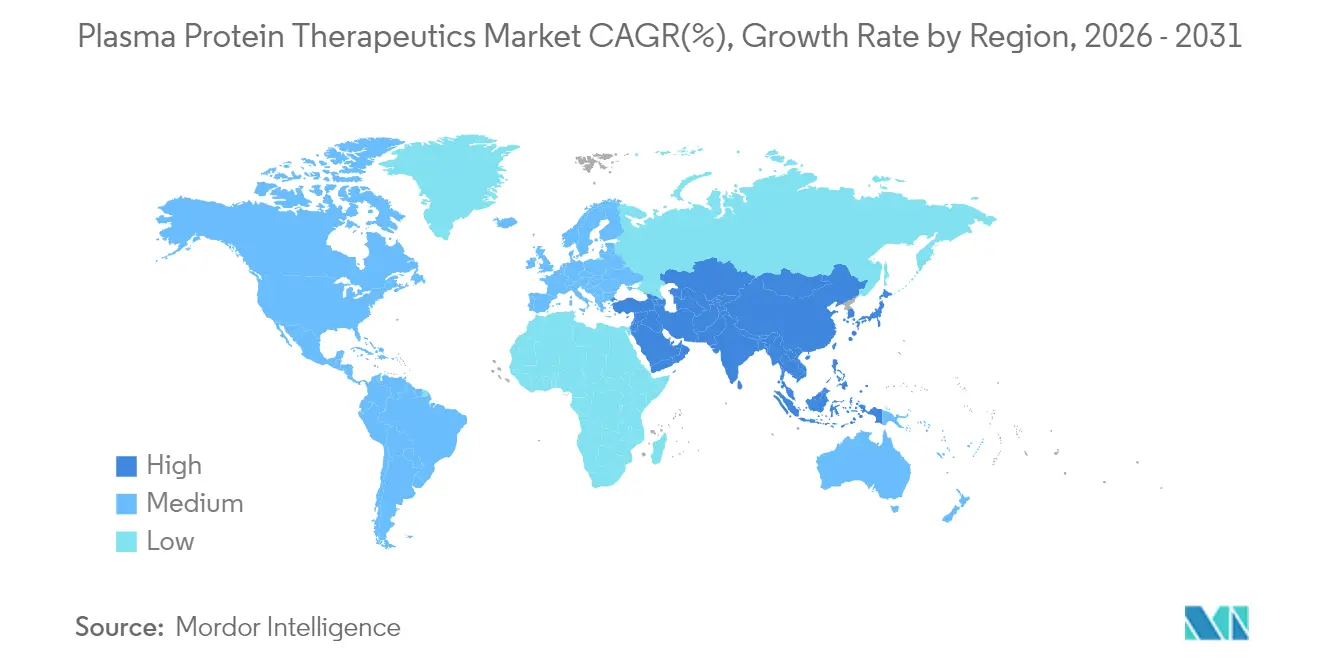

- By region, Asia-Pacific is the fastest-growing geography with a 7.61% CAGR, while North America retained the largest revenue base at 41.10% in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Plasma Protein Therapeutics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Home-based Subcutaneous Immunoglobulin Therapy | +1.20% | North America & Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Expansion of Plasma Collection Centers | +1.50% | Global, concentrated in North America | Short term (≤ 2 years) |

| Rising Incidence of Autoimmune & Neurological Diseases | +0.80% | Global, higher in developed markets | Long term (≥ 4 years) |

| Extended Half-life Coagulation Factors in Japan & South Korea | +0.70% | Asia-Pacific with global spill-over | Medium term (2-4 years) |

| Intensifying R&D Investment | +0.60% | North America & Europe | Long term (≥ 4 years) |

| Hyperimmune Globulins for Novel Viral Threats | +0.30% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Home-Based Sub-Cutaneous Immunoglobulin Therapy

FDA approval of an expanded XEMBIFY label in July 2024[1]Grifols, "Grifols receives expanded XEMBIFY® (immune globulin subcutaneous human-klhw) label in U.S., strengthening its Ig portfolio for patients," grifols.com enables treatment-naïve patients to initiate subcutaneous therapy without prior intravenous dosing, thereby reducing clinic visits and expanding the addressable population. Phase 4 data confirm biweekly dosing maintains total Ig levels, enhancing adherence. Home infusion reduces healthcare resource utilization by 69% compared to IV administration, resulting in payer savings and higher manufacturer margins. Direct-to-patient logistics support new revenue streams, while improved quality of life drives patient preference toward self-administration. Manufacturers are responding with nurse-support apps and wearable pump programs that further reduce treatment burden.

Expansion of Plasma Collection Centers

CSL Plasma’s roll-out of the Rika system across nearly half its U.S. network trims donation sessions to 35 minutes, a 30-50% throughput gain that directly lifts plasma volume. Simultaneously, the FDA is drafting risk-based donor guidelines that replace rigid time-based deferrals with individual assessments, expected to enlarge the eligible donor pool. These moves relieve a chronic supply bottleneck hampering the plasma protein therapeutics market. Advanced centers also deploy comfort-enhancing lounges and digital booking, improving donor retention. Collectively, the infrastructure expansion sets higher capital barriers that smaller firms struggle to match, reinforcing incumbent advantages.

Increasing Incidence of Autoimmune and Neurological Diseases

Improved diagnostics have raised the catalog of recognized primary immunodeficiencies from 250 in 2003 to over 400 variants in 2025. Broader therapeutic indications—covering CIDP, Guillain-Barré syndrome, and myasthenia gravis—are unlocking sustained demand for immunoglobulins. Grifols’ Biotest expects cumulative U.S. sales of approximately USD 1 billion from Yimmugo[2]Grifols, "Grifols’ Biotest to achieve USD 1 billion in US sales of Yimmugo® over next seven years," grifols.com over the coming seven years, underscoring commercial traction. Specialty neurologists increasingly view IVIg as frontline therapy, lengthening treatment duration per patient. Parallel growth in autoimmune dermatology indications, such as pemphigus, adds incremental volume. These epidemiological shifts underpin stable double-digit demand growth for plasma-derived proteins.

Increasing Approval of Extended Half-Life Coagulation Factors in Japan & South Korea

Regulators in Japan and South Korea are fast-tracking extended half-life (EHL) factor IX and VIII products, allowing infusion intervals to stretch from thrice-weekly to once every 7-14 days. The improvement elevates adherence among hemophilia patients and reduces overall factor consumption per quality-adjusted life year, making premium pricing palatable to payers. CSL Behring’s HEMGENIX, a one-time gene therapy for hemophilia B, has gained positive reimbursement decisions in several European states, signaling a global shift toward curative approaches. First-mover firms in EHL and gene therapy capture durable share and can leverage real-world evidence from Asia-Pacific to accelerate approvals elsewhere.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Plasma Supply Constraints Due to Donor Shortages in Europe | -1.20% | Europe, with spillover effects to global fractionation capacity | Medium term (2-4 years) |

| Price Pressures from National Tendering Systems in Brazil, Turkey & Thailand | -0.80% | Brazil, Turkey, Thailand, with potential expansion to other emerging markets | Short term (≤ 2 years) |

| Strict US FDA Fractionation Capacity Validation Delays | -1.10% | United States, affecting global supply chains and product availability | Medium term (2-4 years) |

| High Cost & Limited Reimbursement for Alpha-1 Antitrypsin in Emerging Asia | -0.70% | APAC emerging markets, particularly India, Southeast Asia, with gradual impact on China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Strict Regulations for the Handling of Plasma Protein Products

The FDA mandates donor-specific collection volumes[3]Center for Biologics Evaluation and Research, “Volume Limits for Automated Collection of Source Plasma,” fda.gov, calculated by sex, weight, and hematocrit, which adds workflow complexity and a software validation burden. Emerging economies face additional hurdles, including limited cold-chain infrastructure and slower licensure processes, which can delay product launches. The 2025 FDA guidance agenda[4]AABB, “FDA Releases 2025 Guidance Agenda,” aabb.org lists five fresh documents on blood components, signaling further regulatory churn. Large incumbents leverage in-house regulatory affairs teams to navigate shifting rules, consolidating market power.

High Cost & Limited Reimbursement

Plasma protein therapies require 7-12 months from collection to finished vial, locking up significant working capital. European payers now employ value-based assessments, often challenging premium pricing for novel biologics. A projected regional plasma shortfall of 4-8 million liters by 2025 forces imports and inflates acquisition costs. Policymakers weigh domestic collection incentives, but implementation lags behind market expansion, sustaining the cost-constraint cycle.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dominance of Immunoglobulins and Momentum in Alpha-1 Antitrypsin

Immunoglobulins generated 42.10% of 2025 revenue, demonstrating the single largest plasma protein therapeutics market share in a portfolio spanning primary immunodeficiencies and neurological disorders. The segment’s sustained growth is fueled by subcutaneous formulations that migrate therapy from hospital to home, further enlarging demand. Innovations such as Grifols’ XEMBIFY, which posted 15.8% annual sales growth, exemplify the resilience of this category. Simultaneously, the coagulation factor arena is shifting toward gene-based cures; approval momentum for CSL Behring’s HEMGENIX underlines the gradual substitution of replacement therapy with potentially one-time interventions.

Alpha-1 antitrypsin products represent the fastest-expanding niche, advancing at a forecast 5.92% CAGR through 2031 as early-diagnosis programs uncover latent AATD patients. Gene-editing pipelines led by Prime Medicine promise disease-modifying potential, attracting institutional investors. C1 esterase inhibitors preserve a specialized yet essential role for hereditary angioedema management, with steady uptake driven by improved diagnostic awareness. Hyperimmune globulins, meanwhile, are carving new territory by targeting emerging infectious diseases, offering manufacturers a counter-cyclical revenue hedge.

By Application: Immunology & Neurology at the Forefront with Respiratory on the Rise

Immunology and neurology disorders accounted for 47.30% of the plasma protein therapeutics market size in 2025, mirroring the breadth of indications covered by immunoglobulins. Clinical data affirm IVIg efficacy in CIDP and Guillain-Barré, sustaining multi-year therapy arcs. Hospitals harness protocolized IgG dosing calculators to optimize utilization, ensuring predictable procurement volumes. In parallel, dermatological applications—such as in pemphigus treatment—are gaining recognition, diversifying the clinical footprint.

Respiratory disorders post the steepest trajectory, with a 7.31% projected CAGR, anchored by augmentation therapy for AATD. A 2025 longitudinal study confirmed significant slowing of lung density decline in PiSZ and PiZZ genotypes when therapy commences early. Hematology remains pivotal; extended half-life coagulation factors reduce infusion frequency and improve prophylaxis adherence. Critical care uses of albumin and prothrombin complex concentrates broaden as randomized studies, including a 2025 cardiac surgery trial, demonstrate improved hemostasis over frozen plasma news-medical.net.

By End-User: Hospitals Retain Primacy while Plasma Centers Accelerate

Hospitals and clinics dispensed 58.00% of 2025 volume, reflecting the complexity of intravenous infusions that mandate on-site monitoring. Pharmacy automation and specialized infusion suites streamline throughput, yet payer incentives for home-based care are gradually moderating hospital dominance. The proliferation of subcutaneous products prompts teaching hospitals to launch patient-training programs, smoothing the transition to self-administration.

Plasma centers represent the fastest-growing end-user group, forecast to expand at 6.35% CAGR. CSL’s REACH initiative, operational across almost 350 centers, uses customer-experience analytics to improve donor satisfaction and retention. Advanced machines with iNomi technology optimize collection volume on an individualized basis, enhancing efficiency and yield. Specialty clinics and home-health providers form a small yet rising cohort, capitalizing on telemedicine to supervise remote infusions and integrate adherence monitoring.

Geography Analysis

North America commanded 41.10% of 2025 global revenue, anchored by more than 1,000 FDA-licensed plasma collection facilities and broad insurance coverage. The FDA’s clearance of the Rika device, which halves collection time, directly addresses supply adequacy. Pending risk-based donor regulations could further expand the eligible donor base and cement regional leadership. Manufacturers leverage strong reimbursement ecosystems, although value-based contracts are emerging for high-cost gene therapies, reshaping long-term pricing models.

Asia-Pacific is forecast to grow at 7.61% CAGR, the quickest pace globally. China’s blood products market aided by Terumo’s USD 15 million localization investment earmarked for 2025. Indonesia’s forthcoming 600,000-liter fractionation plant exemplifies public-private collaboration aimed at reducing import dependence. Japan and South Korea grant accelerated approvals for EHL coagulation factors, positioning the sub-region as an innovation testbed.

Europe maintains strategic importance but grapples with a projected 4-8 million-liter plasma gap by 2025, prompting calls for 2 million additional donors. The Proposed SoHO Regulation underscores donor safety and quality but may impose extra compliance costs. Nevertheless, recent positive reimbursement decisions for HEMGENIX illustrate payer readiness to fund transformative therapies. Middle East & Africa and South America, while smaller, are benefitting from gradual diagnostic expansion and donor-education campaigns, setting the stage for steady uptake

Competitive Landscape

The plasma protein therapeutics market is moderately concentrated, with CSL Behring, Takeda, Grifols, Octapharma and Kedrion collectively controlling a dominant revenue share. Grifols’ February 2024 governance shift separated executive management from family ownership, elevating Nacho Abia as CEO to sharpen operational focus. CSL Behring reported USD 2.91 billion net profit in 2024, buoyed by immunoglobulin demand and collection efficiency gains.

Vertical integration remains the prevailing strategy; leading firms own donor centers, fractionation plants and specialty pharmacies, ensuring control over quality and margin. Technology differentiation is intensifying: Haemonetics’ Persona platform adds 9–12% more plasma per donation, offering a compelling ROI for large center operators. Meanwhile, Asahi Kasei’s Planova FG1 virus-removal filter accelerates downstream processing, lowering batch failures and reinforcing supply reliability.

Geographic diversification is another hallmark. CSL divested its Wuhan plasma operations for USD 185 million, reallocating capital to localize higher-value therapies across China. Octapharma invests in Swiss and Swedish capacity expansions, while Kedrion pursues Latin American partnerships to secure fractionation routes. Smaller players focus on niche hyperimmune products, often leveraging contract manufacturing to circumvent scale disadvantages.

Plasma Protein Therapeutics Industry Leaders

-

Octapharma USA Inc.

-

Takeda Pharmaceutical Company Limited

-

Biotest UK

-

Grifols, S.A.

-

CSL Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Prime Medicine unveiled a preclinical Alpha-1 Antitrypsin Deficiency program using Prime Editing, targeting an IND/CTA filing in 2026.

- April 2025: KRRO-110 received orphan-drug designation for AATD treatment.

- February 2025: CSL sold Wuhan plasma assets to Chengdu Rongsheng for USD 185 million.

Global Plasma Protein Therapeutics Market Report Scope

Plasma protein therapy treats distinct medical conditions, restoring missing or inadequate proteins found in plasma to allow their receivers to lead healthier and more productive lives. Patients who rely upon plasma protein therapies generally require regular infusions for their lives.

The Plasma Protein Therapeutics Market is Segmented by Product (Immunoglobulin, Albumin, Plasma Derived Factor Vlll, and Other Products), Application (Hemophilia, Idiopathic Thrombocytopenic Purpura, Primary Immunodeficiencies, and Other Applications), and Geography (North America (United States, Canada, and Mexico), Europe (Germany, United Kingdom, France, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, India, Australia, South Korea, and Rest of Asia-Pacific), Middle East and Africa (GCC, South Africa, and Rest of Middle East and Africa), and South America (Brazil, Argentina, and Rest of South America)). The report offers value (in USD million) for the above segments.

| Immunoglobulins | Intravenous Ig |

| Sub-cutaneous Ig | |

| Hyperimmune Globulins (Anti-D, Hep B, Varicella, RSV, others) | |

| Albumin Coagulation Factors | |

| Coagulation Factors | Factor VIII |

| Factor IX | |

| von Willebrand Factor | |

| Fibrinogen Concentrate | |

| Alpha-1 Antitrypsin | |

| C1 Esterase Inhibitor | |

| Other Plasma-Derived Proteins |

| Immunology & Neurology Disorders | Primary Immunodeficiency (PID) |

| Secondary Immune Deficiency | |

| Chronic Inflammatory Demyelinating Polyneuropathy (CIDP) | |

| Myasthenia Gravis | |

| Hematology & Coagulation Disorders | Hemophilia A |

| Hemophilia B | |

| von Willebrand Disease | |

| Respiratory Disorders | |

| Critical Care & Trauma | |

| Others |

| Hospitals and Clinics |

| Specialty Plasma Centers |

| Homecare |

| Research & Academic Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia- Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Product Type | Immunoglobulins | Intravenous Ig |

| Sub-cutaneous Ig | ||

| Hyperimmune Globulins (Anti-D, Hep B, Varicella, RSV, others) | ||

| Albumin Coagulation Factors | ||

| Coagulation Factors | Factor VIII | |

| Factor IX | ||

| von Willebrand Factor | ||

| Fibrinogen Concentrate | ||

| Alpha-1 Antitrypsin | ||

| C1 Esterase Inhibitor | ||

| Other Plasma-Derived Proteins | ||

| By Application | Immunology & Neurology Disorders | Primary Immunodeficiency (PID) |

| Secondary Immune Deficiency | ||

| Chronic Inflammatory Demyelinating Polyneuropathy (CIDP) | ||

| Myasthenia Gravis | ||

| Hematology & Coagulation Disorders | Hemophilia A | |

| Hemophilia B | ||

| von Willebrand Disease | ||

| Respiratory Disorders | ||

| Critical Care & Trauma | ||

| Others | ||

| By End-User | Hospitals and Clinics | |

| Specialty Plasma Centers | ||

| Homecare | ||

| Research & Academic Institutes | ||

| By Geography (Value) | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia- Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the size of the Plasma Protein Therapeutics Market?

The Plasma Protein Therapeutics Market is USD 33.88 Billion in 2026.

What is driving growth in the plasma protein therapeutics market?

Growth is fueled by faster plasma collection technologies, rising diagnoses of autoimmune and neurological disorders, and regulatory approvals of home-based subcutaneous immunoglobulin therapy.

Which product category holds the largest revenue share?

Immunoglobulins dominate with 42.10% of 2025 revenue, benefiting from expanded indications in neurology and immunology.

How are new technologies improving plasma supply?

Devices like the Rika Plasma Donation System cut collection time to 35 minutes and algorithms such as iNomi lift yield by up to 12%, boosting overall supply.

What challenges limit market expansion?

Strict handling regulations increase compliance costs, and reimbursement pressures constrain premium pricing, shaving an estimated 2% from potential CAGR.

Are gene therapies a threat to traditional plasma products?

Gene therapies like HEMGENIX offer curative potential for select disorders, but the breadth of indications for plasma-derived proteins ensures continued demand in the medium term.

Page last updated on: