Polystyrene Foam Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 44.98 Billion |

| Market Size (2031) | USD 57.22 Billion |

| Growth Rate (2026 - 2031) | 4.92% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polystyrene Foam Market Analysis by Mordor Intelligence

The polystyrene foam market size was valued at USD 42.87 billion in 2025 and estimated to grow from USD 44.98 billion in 2026 to reach USD 57.22 billion by 2031, at a CAGR of 4.92% during the forecast period (2026-2031). Demand resilience stems from the material’s light weight, thermal-insulation performance and cost advantage, qualities that keep it embedded in construction and protective-packaging supply chains even as single-use food-service bans tighten. Expanded polystyrene (EPS) remained the volume leader with 62.15% share in 2024, while extruded polystyrene (XPS) is expanding more quickly at 6.56% CAGR on the back of premium continuous-insulation needs. Asia-Pacific held the largest regional position at 43.65% share in 2024 and is also the fastest-growing territory at 6.91% CAGR, supported by China’s dominance in styrene consumption and subsidy-driven appliance replacements. Regulatory frameworks that reward low-global-warming-potential blowing agents and promote circular-economy recycling are accelerating product reformulations rather than eroding total demand, helping to underpin the polystyrene foam market outlook.

Key Report Takeaways

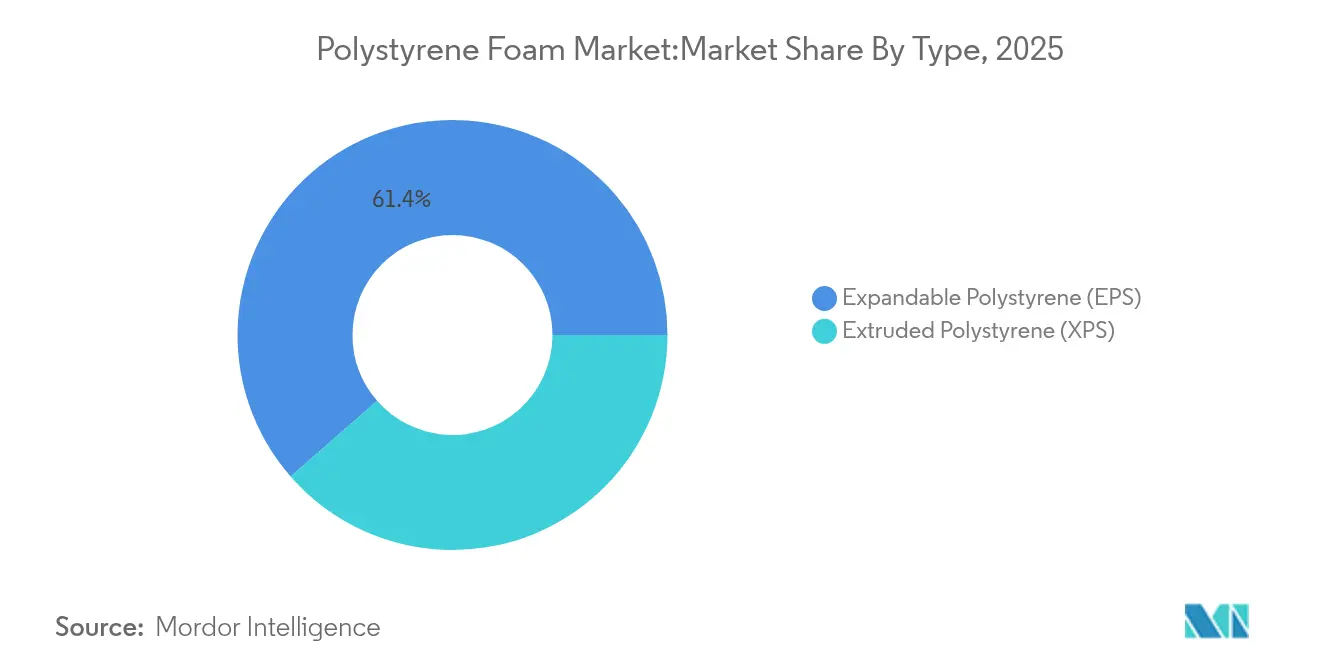

- By type, EPS held 61.43% of the polystyrene foam market share in 2025; XPS is projected to advance at a 6.22% CAGR through 2031.

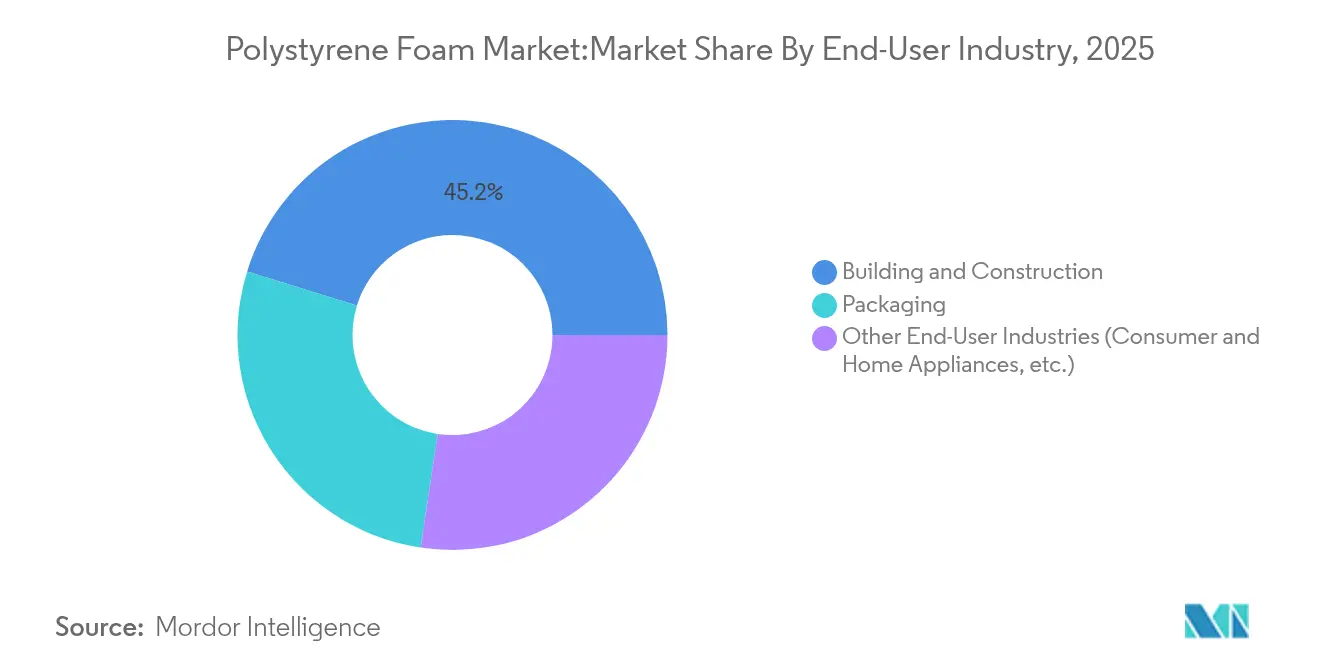

- By end-user industry, building and construction commanded 45.22% of the polystyrene foam market size in 2025, while “other applications” led growth at a 6.88% CAGR to 2031.

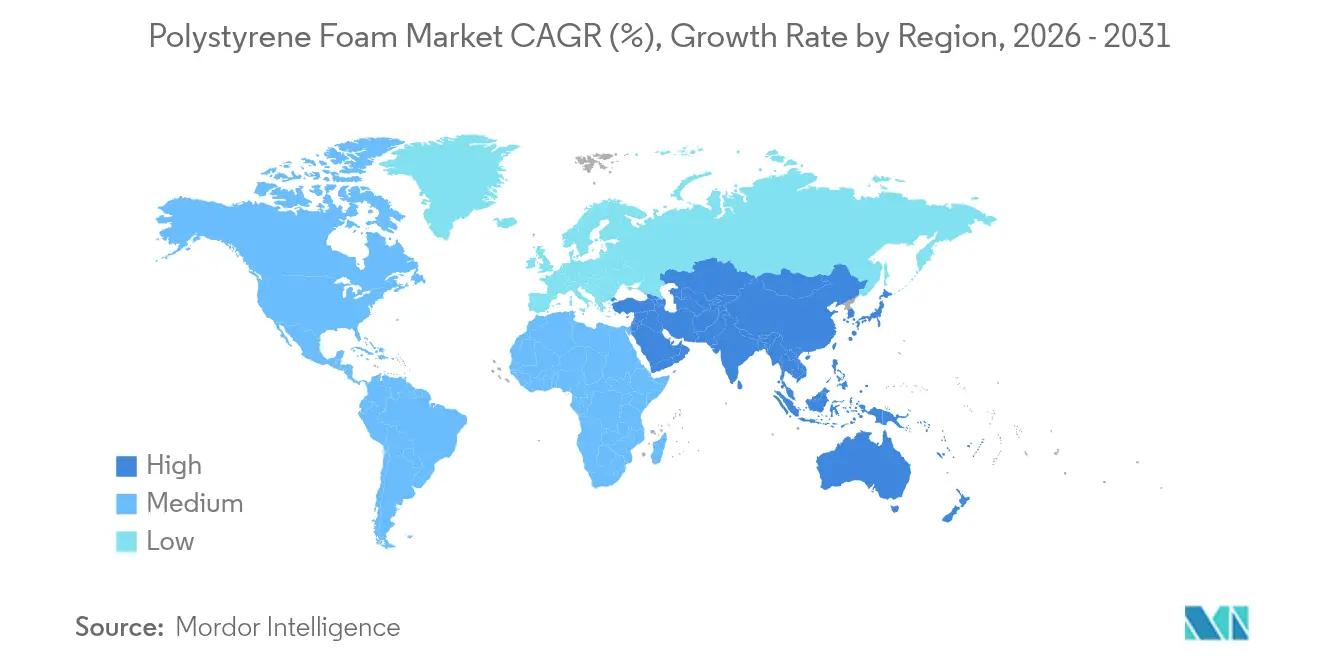

- By geography, Asia-Pacific secured 43.12% revenue share in 2025 and is set to grow at a 6.55% CAGR, sustaining its dual leadership position.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Polystyrene Foam Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Green-building insulation mandates | +1.2% | Global; early gains in North America and EU | Medium term (2-4 years) |

| E-commerce protective-packaging boom | +0.8% | Global; strongest in North America and Asia-Pacific | Short term (≤ 2 years) |

| Cold-chain and pharma-logistics expansion | +0.6% | Global; spill-over to emerging markets | Medium term (2-4 years) |

| Geofoam use in seismic or lightweight embankments | +0.4% | Asia-Pacific core; North America infrastructure projects | Long term (≥ 4 years) |

| Graphite-infused EPS for thin-retrofit insulation | +0.7% | Europe and North America premium markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Green-building Insulation Mandates

Building-energy codes now require continuous insulation, increasing polystyrene-foam uptake in both new construction and retrofits. The International Building Code recognises foam-plastic insulation when fire-safety layers are integrated, enabling LEED credits and up to 30% HVAC-energy savings. DuPont’s low-GWP XPS reformulation cut embodied carbon 94%, illustrating how regulation spurs innovation while safeguarding addressable demand. Nordic policy success with halogen-free flame retardants offers a blueprint for safer EPS adoption worldwide[1]Green Science Policy Institute, “All Flame Retardants Are Not the Same,” greensciencepolicy.org. Such regulatory clarity keeps the polystyrene foam market on a growth path while supporting environmental goals.

E-commerce Protective-Packaging Boom

Parcel volumes continue to climb, driving demand for shock-absorbing, low-density protective shapes. Amazon’s guidelines encourage right-sizing, making EPS moulded parts attractive for fragile items. At the same time, bio-based contenders such as Ecovative’s mycelium packaging are winning sustainability-minded contracts, highlighting a transition rather than a sudden shift. The net effect is incremental growth for the polystyrene foam market as e-tailers balance cost, performance, and environmental targets.

Cold-chain & Pharma-logistics Expansion

Vaccines and biologics rely on consistent 2 °C-8 °C windows during transit. Approved EPS shippers hold that range for up to 23 hours, a critical feature for direct-to-patient delivery models. Thermo Fisher’s recyclable paper cooler shows the direction of travel, yet healthcare suppliers still prioritise proven thermal stability in life-critical lanes, maintaining near-term EPS demand.

Geofoam Adoption for Seismic/Lightweight Embankments

EPS geofoam, roughly 100 times lighter than soil, mitigates settlement and seismic loads in bridge approaches and slide-prone slopes. Italy’s two-decade track record in road restorations and the I-15 rebuild in Utah provide real-world validation, while Germany’s FGSV code standardises specifications, lowering engineering risk and expanding project pipelines[2].Geofoam America, “Lightweight Fill for Embankment Construction,” geofoamamerica.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Styrene-monomer price volatility | -0.9% | Global; most acute in Asia-Pacific hubs | Short term (≤ 2 years) |

| Single-use-plastic bans on EPS food-service | -0.6% | North America and Europe regulatory leaders | Medium term (2-4 years) |

| Mushroom or mycelium packaging substitution | -0.3% | Global; early use in premium niches | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Styrene-monomer Price Volatility

Rising benzene costs transmit directly to styrene and then to polystyrene, pushing producers to announce USD 110 per-ton surcharges in multiple regions in early 2024[3]Trinseo, “Price Increase for Polystyrene Grades in Europe,” trinseo.com. Europe’s shift from net exporter to net importer, with 2023 inflows near 400 kilotons, added supply-chain risk. These swings squeeze converter margins and temper near-term expansion in the polystyrene foam market.

Single-use-Plastic Bans on EPS Food-service

Oregon’s January 2025 prohibition on EPS take-away containers exemplifies tightening curbs. France considered a parallel ban before pausing to align with EU law. Such measures redirect foam demand away from casual dining toward higher-value, longer-life uses, trimming 0.6 percentage points from forecast growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: EPS Dominance Meets XPS Innovation

EPS captured 61.43% of polystyrene foam market share in 2025 on the strength of broad use in building envelopes and molded packaging. The polystyrene foam market size for EPS amounted to USD 26.34 billion in 2025, and the segment is slated to post mid-single-digit gains as recyclability programmes expand. EPS’s low cost and versatility underpin a lasting edge even as regulations favour flame-retardant-free formulations.

XPS generates higher unit margins and is advancing at 6.22% CAGR to 2031. It features thermal conductivity between 0.032-0.037 W/(m·K), outperforming EPS, which ranges 0.035-0.040 W/(m·K). Continuous-insulation codes, space constraints and premium façade designs therefore tilt toward XPS, lifting the polystyrene foam market trajectory in energy-efficient retrofits. DuPont’s AIM-Act-compliant boards and BASF’s sale of its Styrodur line to Karl Bachl sharpen product focus while facilitating capacity adds that sustain competitive intensity.

By End-User Industry: Construction Leadership Amid Diversification

Building and construction applications generated 45.22% of the overall 2025 revenue. Code-mandated continuous insulation and geofoam fills in seismic regions keep the segment at the heart of polystyrene foam market demand. Energy savings of 15-30% in properly insulated buildings provide a clear payback despite higher upfront material spends.

Other applications, covering consumer electronics, appliances and niche modifiers for foamed concrete, lead future growth at 6.88% CAGR. Chinese subsidy programmes that moved 29.64 million consumers into replacement appliances in 2024 lifted styrene demand, indirectly bolstering polystyrene production. Protective shipping forms for smartphones and kitchen appliances reinforce this trend and cushion the polystyrene foam market against softness in food-service packaging.

Geography Analysis

Asia-Pacific’s polystyrene foam market size topped USD 18.49 billion in 2025, equal to 43.12% of global value, and is predicted to post a 6.55% CAGR to 2031. China’s 35% slice of worldwide styrene imports drives resin availability, while appliance-replacement subsidies funnel additional EPS into packaging and insulation lines. India is on track to more than double nameplate capacity by 2028, with Styrenix Performance Materials and Supreme Petrochem riding robust consumer-electronics and automotive plastics demand.

North America retained a solid revenue base close to USD 10.21 billion in 2025. A string of producer price increases in 2024 signalled recovering construction demand, even as AIM-Act rules prompted fast reformulation to ultra-low-GWP blowing-agent systems. Government infrastructure spending and energy-retrofit incentives keep the region an important pillar of the polystyrene foam market.

Europe accounted for roughly USD 7.63 billion and saw imports hit 400 kilotons in 2023 after older styrene units shut. The EU Packaging and Packaging Waste Regulation mandates full recyclability by 2030, spurring investments in depolymerisation and mechanically recycled EPS food-contact grades now under review. These transitions sustain domestic converters but tighten economic margins.

South America and the Middle East & Africa combined delivered slightly under USD 6.54 billion, with demand tied to road building, cold-chain start-ups and disposable-income growth. Lower regulation and expanding grocery e-commerce underpin first-wave EPS penetration, setting the stage for future XPS upgrades as code enforcement strengthens.

Competitive Landscape

The polystyrene foam market is moderately fragmented. Technological advancements are driving differentiation. BASF’s Neopor Plus boards reduce cooling energy by 30% and earn LEED credits, while DuPont’s Styrofoam brand has adopted blowing agents that cut embodied carbon by 94%. Regional players like JSP Corporation focus on bead innovations for automotive applications, and Styrenix Performance Materials is expanding capacity to meet rising domestic demand in India.

Bio-based disruptors, though limited in volume, are influencing branding. Companies like Ecovative Design secure contracts for compostable mycelium packaging, prompting traditional players to invest in circular solutions and emphasize recyclability to maintain market share.

Polystyrene Foam Industry Leaders

Alpek S.A.B. de C.V.

BASF

INEOS Styrolution Group GmbH

Synthos

TotalEnergies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Under Senate Bill 543, Oregon formally prohibited the use of expanded polystyrene foam containers in food service establishments. This legislative action aims to accelerate the transition toward environmentally friendly compostable alternatives.

- June 2024: Abu Dhabi implemented a comprehensive ban on single-use items, including cups, lids, plates, and containers made from expanded polystyrene. This measure is part of a broader initiative to phase out plastics and promote sustainable practices.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the polystyrene foam market as the global sales value of expandable (EPS) and extruded (XPS) polystyrene that exits primary converters in rigid or semi-rigid foam form for use in insulation, protective packaging, consumer goods inserts, and civil engineering lightweight fill. We capture only fresh polymer foam; recycled feedstock is counted once it re-enters the market as a finished foam product, not when collected.

Non-foamed polystyrene grades such as GPPS and HIPS, bead stock sold in bulk before foaming, and downstream fabricated items whose value is dominated by metals, wood, or paper are excluded.

Segmentation Overview

- By Type

- Expandable Polystyrene (EPS)

- Extruded Polystyrene (XPS)

- By End-User Industry

- Building and Construction

- Packaging

- Other End-User Industries (Consumer and Home Appliances, etc.)

- By Geography

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Middle East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed building insulation installers, EPS moulders, XPS board makers, and procurement officers across Asia-Pacific, North America, and Europe. The conversations clarified true converter margins, regional recycling credit pass-through, and realistic construction start rates, letting us fine-tune desk assumptions.

Desk Research

We began with open statistics from agencies such as the United States Geological Survey, Eurostat PRODCOM, and UN Comtrade to benchmark resin flows, followed by insulation and packaging demand indicators from the International Energy Agency, PlasticsEurope, and the World Packaging Organisation. Trade association white papers, patent filings filtered through Questel, and company 10-K filings helped us pin average selling prices and density spreads across regions. Subscription tools, notably D&B Hoovers for converter financials and Dow Jones Factiva for press archives, supplied context where public data thinned out. The sources mentioned are illustrative, and many other publications, databases, and regulatory releases fed our evidence pool.

These references gave us a grounded starting point.

Market-Sizing & Forecasting

We framed a top-down model that starts with national styrene resin production and trade, converts it to foam-grade supply using published yield factors, and then allocates volumes into EPS and XPS pools through documented converter capacity shares. Bottom-up spot checks sampled converter shipments and distributor channel audits validated and occasionally nudged totals. Key variables inside the model include new housing completions, chilled food e-commerce parcel counts, average board thickness shifts, regional building code R-value steps, and styrene price spreads. For outlook, multivariate regression blended with scenario analysis projects demand through 2030; macro drivers like construction spending, e-commerce parcel growth, and insulation retrofit mandates feed the equation. Gaps that appeared in bottom-up samples were bridged by triangulating with primary interview ranges and two-year moving averages.

Data Validation & Update Cycle

Every draft output runs through variance checks against energy intensity ratios, regional GDP multipliers, and prior year import swings before senior analysts sign off. Reports refresh once a year, and we trigger interim updates if styrene prices spike more than fifteen percent or if major policy changes alter foam bans or building code insulation minima.

Why Mordor's Polystyrene Foam Market Baseline Commands Reliability

Published numbers often diverge because firms slice the market at different points in the value chain, anchor to outdated resin prices, or apply one-size growth rates across regions. Mordor's disciplined scope focus and annual refresh cadence reduce those drifts.

Key gap drivers include whether bead stock is booked as revenue, if construction and packaging end uses are both counted, and the currency year used for baseline conversion.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 42.87 B (2025) | Mordor Intelligence | |

| USD 32.2 B (2026) | Global Consultancy A | Excludes packaging foam in Latin America and keeps 2020 price deck unchanged |

| USD 33.56 B (2025) | Research Publisher B | Reports bead stock sales as foam revenue and omits retrofit insulation demand |

The comparison shows that when scope, price base, and demand pools are aligned, Mordor's figure sits logically between conservative resin-only views and aggressive bead stock roll-ups, giving decision makers a balanced, repeatable baseline.

Key Questions Answered in the Report

What is the current Polystyrene Foam Market size?

The polystyrene foam market size reached USD 44.98 billion in 2026 and is forecast to grow steadily at a 4.92% CAGR during 2026-2031.

Which product type leads the polystyrene foam market?

Expanded polystyrene dominates with 61.43% share in 2025, while extruded polystyrene is the faster-growing segment at 6.22% CAGR through 2031.

Why is Asia-Pacific crucial for future growth?

The region holds 43.12% revenue share and posts the highest 6.55% CAGR to 2031, driven by China’s styrene demand and India’s capacity expansions.

How are producers addressing sustainability pressures?

Companies are reformulating blowing agents to ultra-low-GWP levels, commercialising graphite-enhanced EPS, investing in mechanical and chemical recycling, and exploring bio-based alternatives to meet circular-economy mandates.

Page last updated on: