Recombinant Protein Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

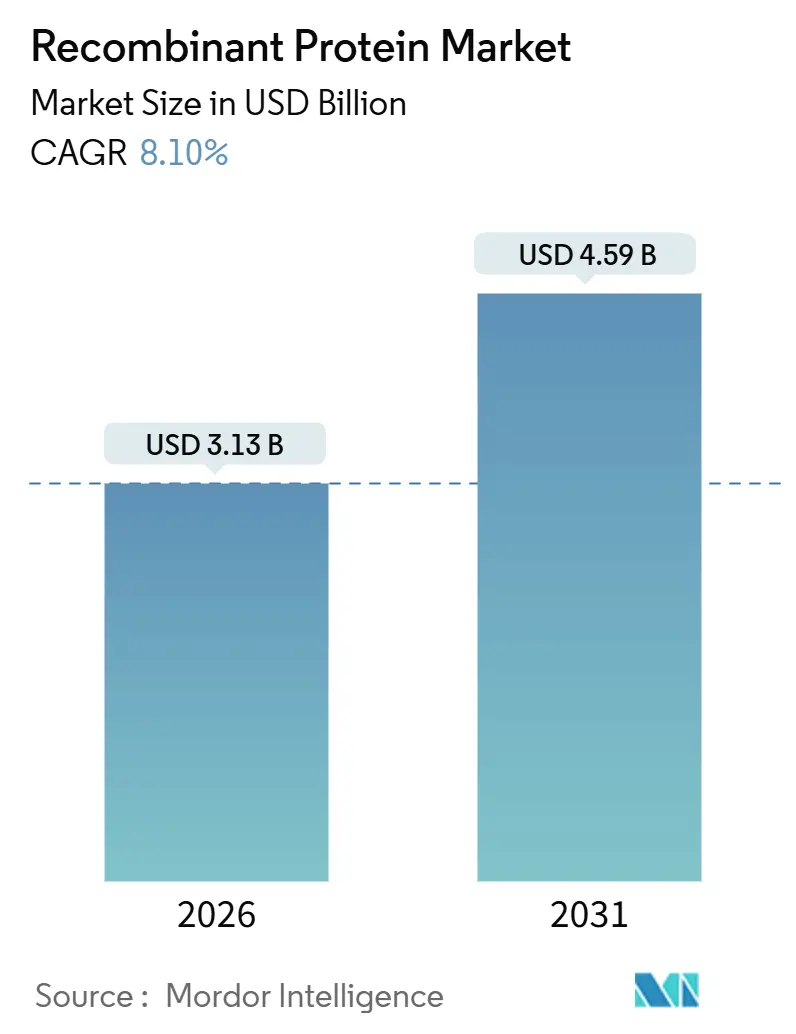

| Market Size (2026) | USD 3.13 Billion |

| Market Size (2031) | USD 4.59 Billion |

| Growth Rate (2026 - 2031) | 8.10% CAGR |

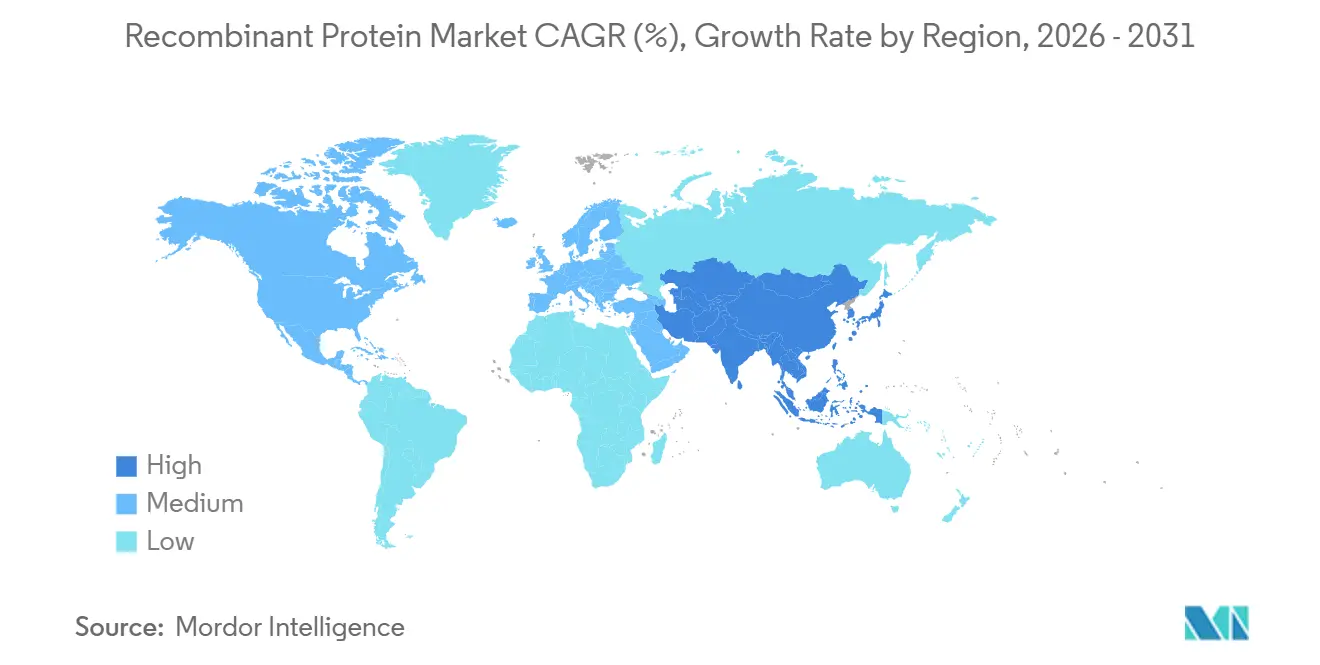

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

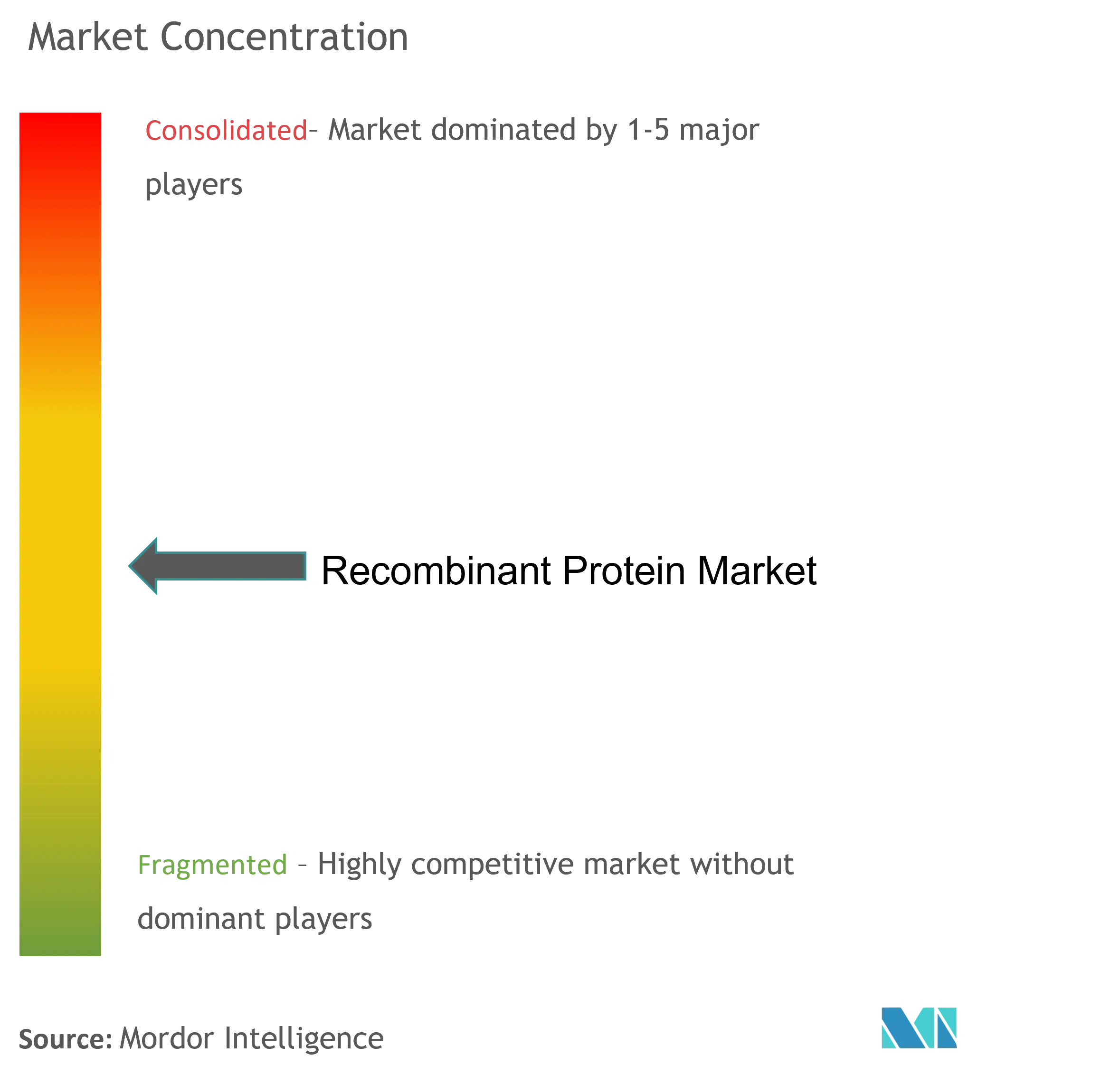

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Recombinant Protein Market Analysis by Mordor Intelligence

The Recombinant Protein Market size is estimated at USD 3.13 billion in 2026, and is expected to reach USD 4.59 billion by 2031, at a CAGR of 8.10% during the forecast period (2026-2031).

Expansion reflects a strategic pivot away from single-target monoclonal antibodies toward precision biologics such as fusion constructs, bispecific formats, and AI-designed scaffolds that address complex oncology, metabolic, and rare-disease indications. Mammalian expression platforms remain the workhorse, yet cell-free and synthetic systems are gaining momentum on the back of faster cycle times and lower capital intensity. Contract development and manufacturing organizations (CDMOs) continue to scale across Asia-Pacific, leveraging cost advantages to win global programs, while FDA fast-track designations and robust National Institutes of Health grants sustain North American leadership. Competitive pressure is mounting as biosimilar entrants, single-use bioreactors, and AI-enabled design shorten timelines and compress margins, creating both risk and opportunity for incumbents.

Key Report Takeaways

- By product, cytokines and growth factors led with 25.2% revenue share in 2025; fusion proteins posted the fastest 8.82% CAGR through 2031.

- By expression system, mammalian platforms captured 46.1% of the recombinant protein market share in 2025, while cell-free systems expanded at an 8.54% CAGR to 2031.

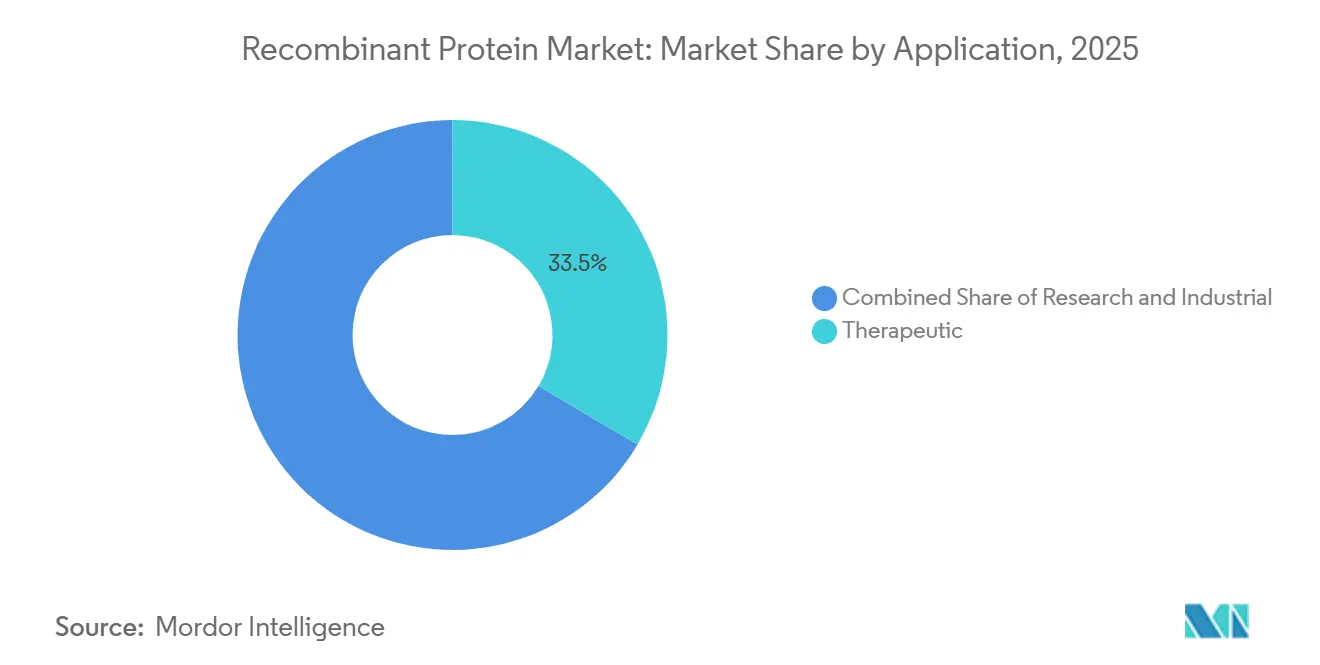

- By application, therapeutic use commanded 33.5% of the recombinant protein market size in 2025 and research is projected to grow at an 8.44% CAGR.

- By end user, pharmaceutical and biotechnology companies held 39.7% revenue share in 2025; CROs and CDMOs registered the highest 8.63% CAGR through 2031.

- By geography, North America accounted for 42.1% revenue in 2025; Asia-Pacific is the fastest-growing region at an 8.81% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Recombinant Protein Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic-Disease Burden Elevates Demand For Biologics | +1.8% | Global, with concentration in North America, Europe, and urban Asia-Pacific | Long term (≥ 4 years) |

| Breakthroughs In High-Yield Expression & Purification Platforms | +1.5% | Global, led by North America and Europe bioclusters | Medium term (2-4 years) |

| Expansion Of Bioclusters & CDMO Capacity Worldwide | +1.4% | Asia-Pacific core, spill-over to North America and Europe | Medium term (2-4 years) |

| Favorable Biologics Reimbursement & Fast-Track Approvals | +1.2% | North America and Europe, emerging in select Asia-Pacific markets | Short term (≤ 2 years) |

| AI-Driven De Novo Protein Design Unlocks Novel Pipelines | +0.9% | North America and Europe, early adoption in China | Long term (≥ 4 years) |

| Single-Use, Low-Capex Bioreactors Democratize Manufacturing | +0.7% | Global, with rapid uptake in Asia-Pacific and emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Chronic Disease Burden Elevates Demand for Biologics

Rising prevalence of diabetes, cancer, and autoimmune disorders is expanding the addressable patient pool for recombinant therapeutics. The World Health Organization added semaglutide to its Model List of Essential Medicines in 2024, recognizing glucagon-like peptide-1 receptor agonists as a cornerstone of obesity and type 2 diabetes management [1]World Health Organization, “Essential Medicines List Update,” who.int. Novo Nordisk's Wegovy and Eli Lilly's Zepbound collectively generated multi-billion-dollar revenues in 2025, underscoring payer willingness to reimburse high-cost biologics when clinical outcomes justify expenditure. Oncology pipelines are shifting toward interleukin-based immunotherapies and bispecific antibodies that engage T cells, with FDA approvals for teclistamab and talquetamab in multiple myeloma validating the dual-targeting paradigm. This trend extends beyond wealthy markets; India and China are scaling biosimilar insulin and erythropoietin production to serve domestic populations, creating a parallel demand stream that favors cost-efficient expression systems and local fill-finish capacity.

Breakthroughs In High-Yield Expression & Purification Platforms

Mammalian cell lines now routinely achieve titers of 10 grams per liter to 15 grams per liter in perfusion culture, halving bioreactor footprint and accelerating clinical supply timelines. Chinese hamster ovary (CHO) cell engineering incorporating CRISPR-mediated knockout of apoptosis pathways and overexpression of chaperones has become standard practice among top-tier CDMOs, enabling clients to compress process development from 18 months to 12 months. Continuous chromatography systems, which integrate bind-elute and flow-through modes, reduce resin consumption by 30% and cut purification cycle time significantly, translating into lower cost-of-goods for high-volume products. Bacterial platforms are benefiting from codon optimization and periplasmic secretion strategies that improve solubility and reduce endotoxin burden, making Escherichia coli viable for simpler cytokines and growth factors. These advances compress the cost-quality frontier, allowing smaller biotechs to compete on manufacturing efficiency rather than relying solely on intellectual property moats.

Expansion Of Bioclusters & CDMO Capacity Worldwide

Asia-Pacific CDMO capacity additions are reshaping global supply chains. Samsung Biologics' Plant 5 in Incheon added 180 kiloliters of single-use capacity in 2024, bringing the site's total to 784 kiloliters and positioning the company as the world's largest contract biomanufacturer by volume. Lotte Biologics committed USD 3.3 billion to a 360-kiloliter greenfield facility in South Korea, targeting both innovator and biosimilar clients. In China, WuXi Biologics operates multiple sites with aggregate capacity exceeding 400 kiloliters, serving domestic and international pipelines with cost structures 20% to 30% below Western peers. North America and Europe are responding with targeted expansions: Lonza's Vacaville acquisition added 330 kiloliters of mammalian capacity, while Fujifilm's Denmark and North Carolina investments total USD 2.8 billion and focus on high-complexity glycoproteins requiring advanced analytics and regulatory pedigree. This geographic diversification reduces concentration risk but also fragments quality standards, prompting regulators to harmonize good manufacturing practice (GMP) inspections under International Council for Harmonisation (ICH) Q7 and Q11 guidelines [2]International Council for Harmonisation, “ICH Q7/Q11 Guidelines,” ich.org.

Favorable Biologics Reimbursement & Fast-Track Approvals

Regulatory agencies are accelerating biologics pathways to address unmet needs. The Center for Drug Evaluation and Research has approved a total of 63 biosimilars for 17 different reference products since 2015. The European Medicines Agency's PRIME scheme provided early scientific advice to 42 biologics developers in 2025, aligning clinical endpoints with regulatory expectations and reducing late-stage attrition. Payer policies are evolving in parallel; the United States Food and Drug Administration finalized interchangeability standards for biosimilars in 2024, allowing pharmacists to substitute without prescriber intervention. Japan's Ministry of Health, Labour and Welfare expanded reimbursement for regenerative medicine products, including recombinant growth factors used in cell therapy manufacturing, signaling a shift toward value-based pricing that rewards clinical differentiation over cost minimization.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent High COGS For Complex Glycoproteins | -1.1% | Global, most acute in high-complexity therapeutic segments | Long term (≥ 4 years) |

| Intensifying Biosimilar-Driven Price Erosion | -0.9% | North America and Europe, spreading to Asia-Pacific | Medium term (2-4 years) |

| Cold-Chain & Fill-Finish Bottlenecks in Emerging Markets | -0.6% | Asia-Pacific, Middle East & Africa, South America | Medium term (2-4 years) |

| Regulatory Ambiguity for Cell-Free Synthesis Platforms | -0.4% | Global, with regulatory focus in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent High COGS for Complex Glycoproteins

Downstream processing for heavily glycosylated proteins still represents 60%–70% of manufacturing outlay, despite resin and process advances. Affinity resins priced at USD 10,000–15,000 per liter require frequent replacement, and extended culture durations inflate overhead costs. Glyco-engineered yeast strains offer promise, but sparse regulatory precedent adds 12–18 months of comparability work, restraining near-term adoption. High cost structures disadvantage biosimilars once reference prices fall, concentrating production among the few players that maintain scale efficiencies. Without step-change gains in glycan control or purification economy, margin pressure will persist and temper recombinant protein market acceleration.

Intensifying Biosimilar-Driven Price Erosion

Humira biosimilars captured significant market share in the United States by volume by 2025, slashing AbbVie’s revenue by USD 6 billion year-over-year. European experience shows reference-product prices falling due to growing adoption of infliximab and rituximab biosimilars. Medicare Part D discounts averaged 65%, signaling payers resolve to widen competition and extend savings. Originators respond with formulation tweaks, subcutaneous options, or strategic exits, yet the repricing cycle extends across tumor necrosis factor inhibitors and anti-VEGF lines. Sustained price erosion dampens revenue growth and forces companies to squeeze costs or chase novel modalities, slightly constraining recombinant protein market performance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Cytokines Anchor Revenue, Fusion Proteins Propel Growth

Cytokines and growth factors accounted for 25.2% of the recombinant protein market share in 2025, sustained by widespread use of interleukins, colony-stimulating factors, and interferons across oncology and immunology. Interleukin-15 programs in particular are expanding T-cell therapies, while next-generation interleukin-2 variants deliver stronger tumor infiltration with lower toxicity. Fusion proteins, though only emerging, are projected to grow at an 8.82% CAGR through 2031, benefiting from half-life extension and dual-targeting mechanisms exemplified by Amgen’s Uplizna [3]Amgen, “Uplizna Product Information,” amgen.com. Demand for hormones such as insulin, erythropoietin, and human growth hormone remains steady, yet biosimilar launches like Semglee and Rezvoglar exert downward price pressure. Monoclonal antibodies and fragments continue to dominate autoimmune and oncology care, while industrial enzymes provide reliable cash flow as sustainability mandates drive the switch from petrochemical catalysts. AI-designed scaffolds and synthetic biology outputs populate early pipelines, suggesting longer-term upside once regulatory clarity and manufacturing readiness mature.

By Expression System: Mammalian Dominance, Cell-Free Momentum

Mammalian hosts held 46.1% of the market share in 2025, reflecting an unrivaled ability to deliver human-like glycosylation essential for immunoglobulins and Fc-fusion constructs. Recombinant protein market size tied to mammalian systems continues to expand as perfusion and fed-batch processes yield titers above 10 g/L, lowering per-gram costs. Cell-free platforms, however, grow fastest at an 8.54% CAGR, offering 48-hour production cycles and site-specific conjugation versatility showcased by Sutro Biopharma’s XpressCF.

Bacterial expression remains a workhorse for non-glycosylated molecules, aided by codon optimization that halves refolding expense. Yeast systems deliver a balance of eukaryotic folding and bacterial scalability, with Pichia pastoris enabling dense fermentations suited for industrial enzymes. Insect cells occupy niche vaccine and viral-like-particle uses, but limited scale constrains their broader stake in the recombinant protein market.

By Application: Therapeutics Lead, Research Use Accelerates

Therapeutic products captured 33.5% of revenue in 2025 as GLP-1 agonists and bispecific antibodies demonstrated strong payer acceptance and clinical gains. The recombinant protein market size for therapeutics is projected to grow with a significant CAGR as additional orphan-disease biologics reach the market. Research applications expand in parallel, propelled by proteomics, CRISPR screens, and synthetic-biology workflows that depend on high-purity reagents.

Academic laboratories are upgrading core facilities with automated purification suites funded by a USD 500 million NIH allocation, improving internal throughput while increasing demand for standardized reference proteins. Industrial uses involving food processing and detergents rely on recombinant enzymes for energy savings and greener profiles; Novozymes’ cold-wash proteases illustrate the commercial potential in sustainability-oriented niches.

By End User: Pharma Dominance, CDMOs Capture Outsourcing Wave

Pharmaceutical and biotech companies commanded 39.7% of spending in 2025, preserving process know-how for blockbuster assets with patent life beyond 2030. Still, CROs and CDMOs register the highest 8.63% CAGR as virtual biotechs outsource development to conserve capital. Lonza’s backlog topped USD 15 billion in 2025 across 150 programs, while Samsung Biologics signed 30 new multi-product agreements in 2024.

Academic and government institutes grow at a more measured pace, tied to grant cycles and internal budget approvals. These institutions demand ISO-certified suppliers and traceable quality, positioning specialized reagent firms such as Sino Biological and Bio-Techne to gain share. As outsourcing proliferates, recombinant protein market dynamics shift toward flexible capacity and compliance credentials.

Geography Analysis

North America held 42.1% of global revenue in 2025, buoyed by concentrated venture funding, FDA regulatory leadership, and entrenched bioclusters in Boston and the San Francisco Bay Area. The FDA issued 68 breakthrough therapy designations across 2024-2025, shaving up to a year off commercialization timelines. Canada’s CAD 950 million Pan-Canadian Biologics and Biosimilars Initiative is set to boost domestic output, reducing import reliance and enlarging the regional recombinant protein market size.

Europe leverages established capacity in Ireland, Switzerland, and Denmark. Lonza’s Visp and Portsmouth sites contribute 200 kL of mammalian volume, while Fujifilm’s new 120 kL Danish plant targets complex glycoproteins. EMA’s PRIME program continues to streamline development, and biosimilar penetration across infliximab and rituximab surpasses 80%, reinforcing Europe’s reputation for value-based procurement.

Asia-Pacific is on an 8.81% CAGR trajectory as China and India escalate CDMO footprints. WuXi Biologics exceeds 400 kL capacity with cost structures undercutting Western peers by up to 30%. Samsung Biologics’ 784 kL site in Incheon further cements regional prominence. Domestic demand for biosimilar insulin and erythropoietin in India also adds volume, broadening recombinant protein market penetration across emerging economies.

Middle East & Africa and South America remain nascent but strategic. Saudi Vision 2030 earmarks USD 2 billion for biomanufacturing to lower import dependency. Brazil recorded significant biosimilar market growth in 2025, although regulatory harmonization lags U.S. and EU benchmarks. South Africa’s Biovac Institute expanded fill-finish output, offering a springboard for regional recombinant protein contracts once WHO prequalification is secured.

Regulatory Landscape

Regulatory oversight for recombinant proteins continues to center on global quality and comparability expectations, with ICH guidance anchoring development and lifecycle change management (notably Q5B for expression constructs and cell lines, Q5E for comparability after manufacturing changes, and Q11 for drug-substance development and manufacture). In the United States and Europe, biosimilar policy and quality guidelines remain key reference points for biotechnology-derived proteins, shaping analytical similarity, process validation, and post-approval change controls across mammalian and microbial expression platforms.

Policy actions in 2024-2026 emphasize faster pathways and clearer expectations for innovators and follow-ons. The FDA finalized interchangeability standards for biosimilars in 2024, while the European Medicines Agency continued to use programs such as PRIME in 2025 to provide earlier scientific advice and alignment on endpoints for biologics developers. In June 2025, FDA Center for Veterinary Medicine issued GFI #288 on Chemistry, Manufacturing, and Controls to support recombinant protein products for veterinary use, and in September 2025 the UK Government Life Sciences Sector Plan reiterated a 150-day approval target with NICE by March 2026, reinforcing the broader push to streamline review while maintaining GMP and validation rigor.

Value Chain Analysis

The recombinant protein value chain starts with upstream inputs and enabling technologies, including expression vectors and engineered host cell lines (CHO, HEK293, E. coli, Pichia, insect, and cell-free systems), followed by critical consumables such as chemically defined media, supplements, WFI-grade utilities, process gases, and chromatography resins and columns. Development then progresses through clone selection and cell line development, upstream manufacturing (fed-batch and perfusion for mammalian systems, and fermentation for microbial systems), and downstream purification where bind-elute chromatography, polishing steps, viral clearance (as applicable), and ultrafiltration/diafiltration drive final purity and yield.

Midstream and downstream work is often handled through a combination of in-house biomanufacturing and outsourced partners. CROs and CDMOs provide process development, scale-up, analytical characterization, and GMP production for clinical and commercial supply. Downstream processing remains a major cost and capacity choke point for complex glycoproteins (with DSP often accounting for 60%-70% of manufacturing outlay in high-complexity products), and resin economics and skilled labor availability limit rapid scale-up. The final stages include formulation and fill-finish, cold-chain logistics for many therapeutic proteins, and distribution to pharmaceutical and biotechnology companies, research institutions, and industrial users, with regional fill-finish and cold-chain gaps affecting time-to-market in emerging geographies.

Competitive Landscape

Global revenue concentration sits majorly among the top 10 suppliers, indicating a moderately fragmented structure that still allows specialized entrants to gain share. Large innovators such as Amgen, Roche, and Novo Nordisk retain in-house capacity to protect intellectual property and margins. CDMOs including Lonza, Samsung Biologics, and WuXi Biologics scale aggressively, exploiting single-use technology and Asian cost advantages to court virtual biotechs and mid-caps.

Competitive differentiation increasingly revolves around AI-driven discovery, continuous manufacturing, and cell-free synthesis. Generate Biomedicines’ USD 273 million Series B in 2024 highlights investor confidence in generative models that compress discovery cycles.

Biosimilar entrants erode margins in mature categories; Amgen’s Amjevita and Boehringer Ingelheim’s Cyltezo together controlled half of Humira’s U.S. volume by 2025, propelling AbbVie to diversify toward new immunology assets.

Recombinant Protein Industry Leaders

Eli Lilly and Company

Thermo Fisher Scientific Inc.

Novartis AG

GlaxoSmithKline PLC

Pfizer Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Capacity build-outs and process-intensification initiatives are creating whitespace for suppliers that can support faster development-to-GMP transitions, particularly for cytokines, enzymes, fragments, and other recombinant proteins suited to microbial and flexible single-use production. April 2026 progress at WuXi Biologics on its Chengdu microbial commercial manufacturing site, including a 15,000 L fermenter and a dual-chamber lyophilization line, reflects increased investment in fermentation plus integrated finishing for non-mAb biologics, where speed and cost determine sourcing decisions. CDMOs and regional manufacturers also have openings to support virtual biotech demand and reduce tech-transfer risk through platform processes and standardized analytics, aligning with the report trend toward scaled outsourcing and shorter cycle times.

Regulatory and policy signals also shape near-term opportunity for compliance-forward manufacturers and tool providers that strengthen validation, documentation, and comparability packages. The EMA concept paper published in January 2026 on revising GMP guidance (Annex 15) points to tighter expectations around qualification and validation practices, which increases the value of robust quality systems, continuous improvement programs, and digital traceability across upstream and downstream operations. In parallel, government programs focused on biomanufacturing ecosystems, including India initiatives linked to BioE3 and the announced rollout of the Biopharma Shakti scheme in 2026, support new hubs where recombinant protein developers can pair discovery, process development, and scalable manufacturing within a framework aimed at regulatory-approval acceleration.

Recent Industry Developments

- July 2026: GSK completed its acquisition of Nuvalent, Inc., following the definitive agreement announced in June 2026. The deal strengthens GSKs oncology pipeline with assets that can increase demand for high-quality recombinant proteins used in discovery, screening, and biologics-enabling workflows. Consolidation at this scale also influences partnering and procurement dynamics across reagent suppliers and CDMOs.

- January 2026: Pfizer entered a non-exclusive license agreement with Novavax to use Matrix-M adjuvant technology in up to two disease areas. The agreement supports vaccine and immunology program expansion where recombinant antigens and protein-based components are central to development and manufacturing. It also broadens cross-company access to a platform that can change formulation and scale-up choices for protein-based candidates.

- December 2025: Thermo Fisher Scientific launched Gibco Bacto CD Supreme FPM Plus and Gibco Bacto CD Supreme Feed (2X) to improve recombinant protein production in E. coli. The launch addresses upstream consistency and productivity, helping researchers and developers reduce variability associated with complex media while simplifying documentation for regulated workflows. Media and feed upgrades at scale can shorten development cycles and improve yields for microbial-expressed cytokines, enzymes, and other non-glycosylated proteins.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues generated from purified recombinant proteins produced using recombinant-DNA expression systems and sold for therapeutic use, pre-clinical or clinical research, and closely related bioprocess reagent use. Revenue values are captured at the selling price for the finished recombinant protein product.

Scope exclusions: contract manufacturing service fees, diagnostic antibodies, and bulk food enzyme applications are excluded from the market totals.

Segmentation Overview

- By Product

- Hormones (Insulin, EPO, hGH, FSH)

- Cytokines & Growth Factors (ILs, CSFs, IFNs)

- Monoclonal Antibodies & Fragments

- Enzymes

- Fusion Proteins & Others

- By Expression System

- Mammalian (CHO, HEK293)

- Bacterial (E. coli)

- Yeast (Pichia, Saccharomyces)

- Insect (Sf9, Sf21)

- Cell-Free / Synthetic

- By Application

- Therapeutic

- Research

- Industrial (Agro-biotech, Food, Detergents)

- By End User

- Pharmaceutical & Biotechnology Companies

- Academic & Research Institutes

- CROs & CDMOs

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of APAC

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by mapping where recombinant proteins show up in real demand, then translating that into volumes, pricing, and use patterns by region. For source checks, we rely on public and official materials such as the US FDA databases (approvals and labels), the National Institutes of Health (NIH) and NCBI resources, the World Health Organization (WHO) and national health agencies for disease and treatment signals, and OECD and World Bank macro and health spend indicators.

To keep the model grounded, we also review company filings and investor presentations, peer reviewed articles that discuss expression systems and yield, and trade and customs statistics where protein and biologics related flows are visible. Paid subscriptions are used selectively for company financials and intelligence, patent databases, and shipment level import and export cuts when the public record is thin. These examples are not exhaustive, and other public sources were also reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure test the demand pool and pricing logic, especially where list prices do not match realized prices or where end use splits are unclear. We speak with a mix of recombinant protein suppliers, distributors, biopharma and research buyers, and domain specialists across APAC, EMEA, and the Americas, so gaps from desk inputs can be filled and assumptions can be rechecked before finalization.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 14% | APAC: 43% |

| Mid tier: 47% | Functional/Unit leaders: 42% | EMEA: 32% |

| Smaller Players: 19% | Managers: 44% | Americas: 25% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where therapy and research demand signals are translated into a recombinant protein spend pool by region, then reconciled to how suppliers typically recognize revenue for purified recombinant proteins. Once the demand pool is created, the main rule is that only revenue tied to recombinant protein products within the defined scope is counted.

Key inputs in the model include biologics and protein drug approval and label activity, therapeutic area level patient and treated population trends, shifts in expression system mix (mammalian, bacterial, yeast, insect, and cell-free), typical ordering patterns from research and bioprocess users, and observed pricing and discount behavior by channel. We corroborate totals with selective bottom-up approximations, such as sampled price per unit multiplied by estimated consumption volumes, plus supplier and channel checks where data is available. After that, we adjust for gaps using conservative assumptions that are validated in interviews.

Forecasting uses scenario analysis supported by a simple multivariate regression layer for variables with stable time series, such as approval cadence, health spending, and research funding trends. Assumptions on price progression and mix are refreshed with expert consensus to avoid overstating growth when demand changes are mainly mix-driven.

Data Validation & Update Cycle

Validation is done through checks that compare model outputs against independent signals, and we also review for sudden jumps that do not match known demand drivers. We run variance checks across regions and end-use splits, and any outlier is traced back to an input like pricing, adoption, or scope treatment before sign-off.

Reports are refreshed annually, with interim updates when material events could change demand or pricing assumptions. If a large variance is detected in a key indicator, we re-contact selected primary respondents to confirm whether the shift is real or timing-driven. Before delivery, a final analyst pass is completed so clients receive the most current view aligned to the stated market definition.

Mordor Intelligence's Recombinant Protein Market Size Measured Against Other Published Estimates

Published figures for recombinant proteins can be far apart, even when the topic appears similar, because each publisher draws the market boundary differently and selects different years for the stated size. Differences can also come from whether pricing is captured at the finished product level, how research versus therapeutic use is split, and how much adjacent biologics revenue is included in the total.

FDA approval and label activity, along with expression system adoption and end-use purchase patterns validated in interviews, are used to keep Mordor Intelligence's estimate tied to purified recombinant protein product revenue rather than broader biologics, vaccine, or service revenues.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.13 B (2026) | |

| Industry Publisher A | USD 3.46 B (2024) | Uses an earlier base year and a broader segmentation frame that does not clearly separate finished recombinant protein product revenue from adjacent life science revenues, which can lift the stated size versus a stricter scope. |

| Research Provider B | USD 2.50 B (2023) | Anchors the market in a different historical year and can apply narrower inclusion rules by type or end-use, which reduces the captured demand pool and can undercount categories treated as core recombinant proteins in other models. |

The spread across the three figures is mostly explained by year selection and what gets counted as recombinant protein revenue in practice. When the scope stays limited to purified recombinant protein products and the assumptions are checked against approvals, adoption, and purchasing behavior, the final number becomes easier to trace and repeat across updates.

Key Questions Answered in the Report

How big is the Recombinant Protein Market?

The recombinant protein market size is expected to reach USD 3.13 billion in 2026 and is projected to reach USD 4.59 billion by 2031.

Which product category currently leads global revenue?

Cytokines and growth factors lead with a 25.2% share, supported by wide oncology and immunology use.

Which expression system is expanding fastest?

Cell-free and synthetic platforms are advancing at an 8.54% CAGR thanks to rapid 48-hour production cycles.

Which region shows the highest growth rate through 2031?

Asia-Pacific posts the fastest regional CAGR at 8.81% as China and India have ramped up CDMO capacity and biosimilar demand.

Why are CDMOs gaining share among end users?

Mid-tier biotechs prefer outsourcing to CDMOs, driving an 8.63% CAGR for the segment as they conserve capital and shorten timelines.

Page last updated on: