Hemostasis And Tissue Sealing Agents Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 10.68 Billion |

| Market Size (2031) | USD 15.74 Billion |

| Growth Rate (2026 - 2031) | 8.07% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

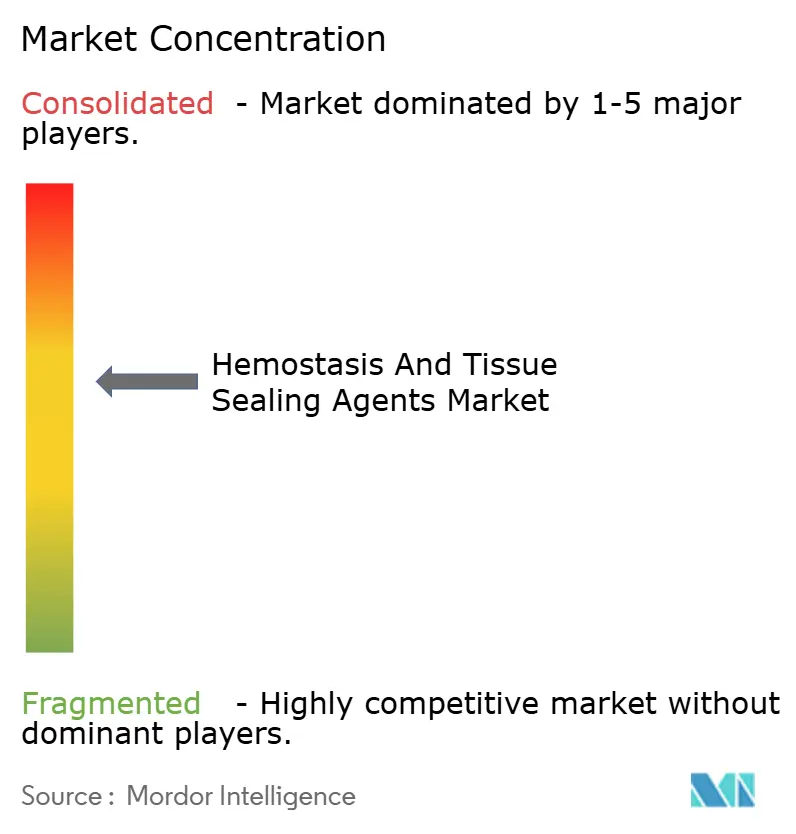

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hemostasis And Tissue Sealing Agents Market Analysis by Mordor Intelligence

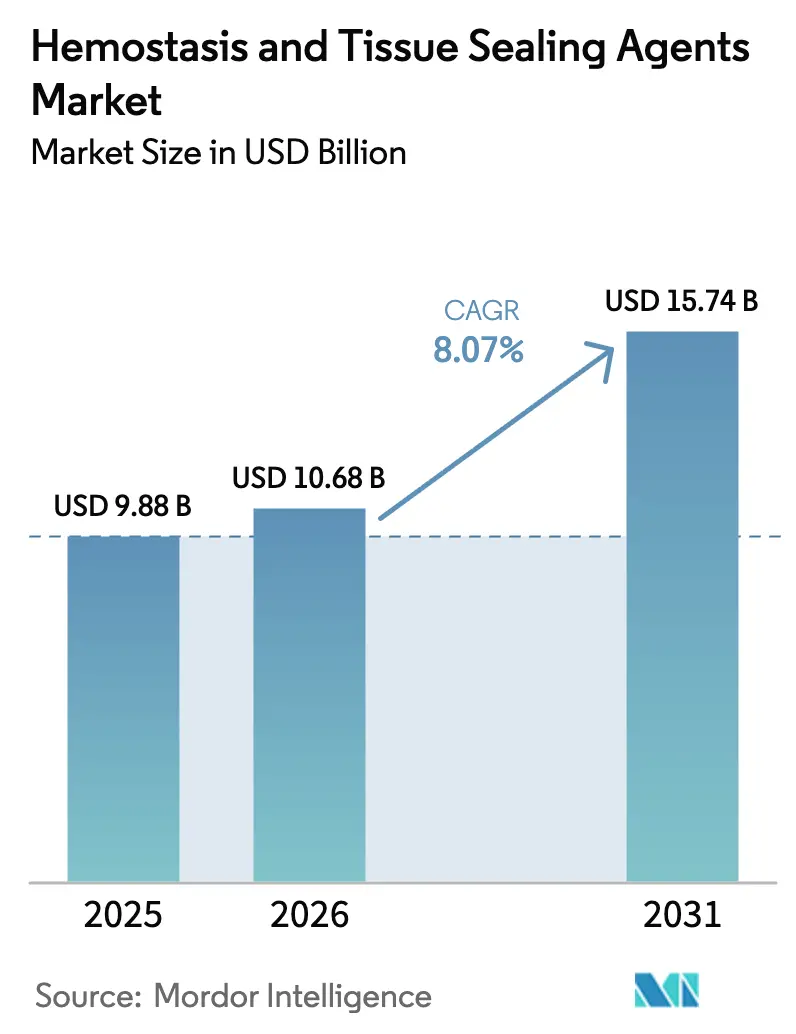

The hemostasis & tissue sealing agents market size is expected to grow from USD 9.88 billion in 2025 to USD 10.68 billion in 2026 and is forecast to reach USD 15.74 billion by 2031 at 8.07% CAGR over 2026-2031. Adoption is accelerating as bleeding control tools evolve from basic topical powders to bio-engineered sealants that integrate with robotic and image-guided surgery platforms. Complex surgical caseloads tied to aging demographics and chronic disease management continue to widen the addressable base of procedures that rely on sophisticated clot-promoting solutions. Minimally invasive and outpatient techniques further lift unit volumes because surgeons need agents packaged for fast, single-use deployment in confined visual fields. Regulatory agencies have also reduced approval friction for moderate-risk devices, allowing innovators to commercialize differentiated formulations more quickly and capture unmet clinical niches. Together, these forces keep the hemostasis & tissue sealing agents market on a clear expansion path despite ongoing cost containment pressures.

Key Report Takeaways

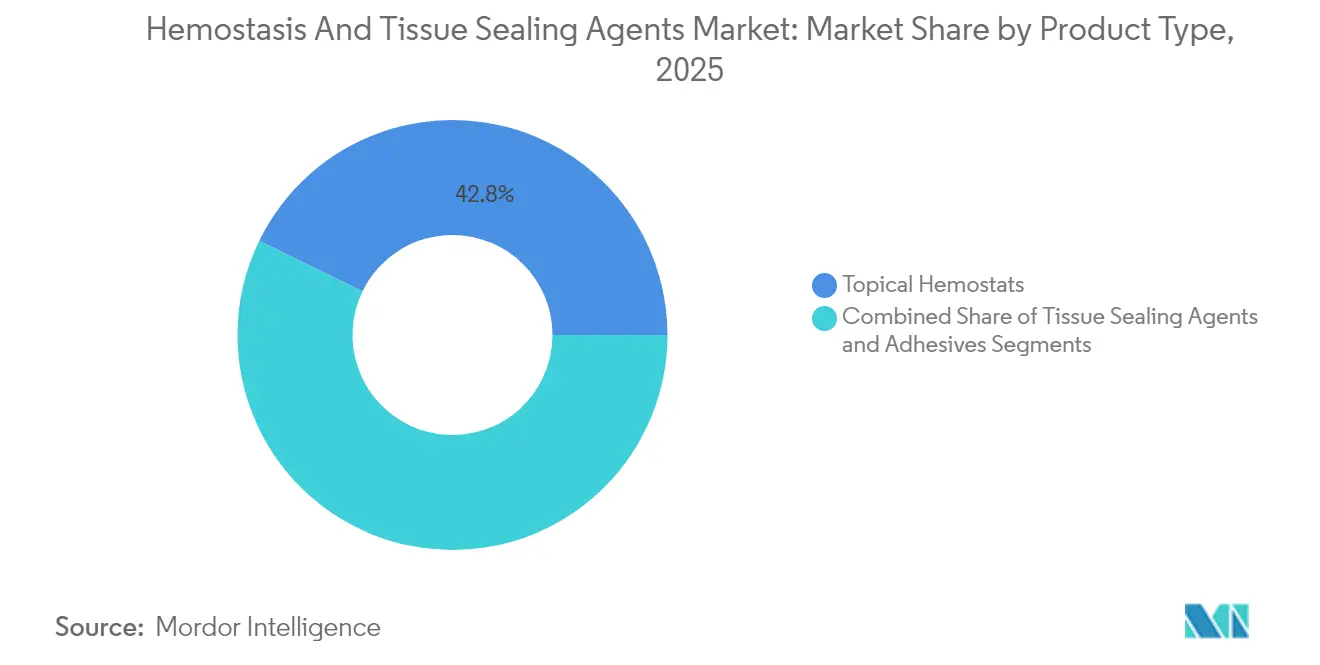

- By product type, Topical Hemostats held 42.78% of the hemostasis & tissue sealing agents market share in 2025, while Tissue Sealing Agents are forecast to post the fastest 9.98% CAGR through 2031.

- By material, collagen-based solutions led with 36.10% revenue share in 2025; polysaccharide formulations are poised to climb at a 12.41% CAGR over 2026-2031.

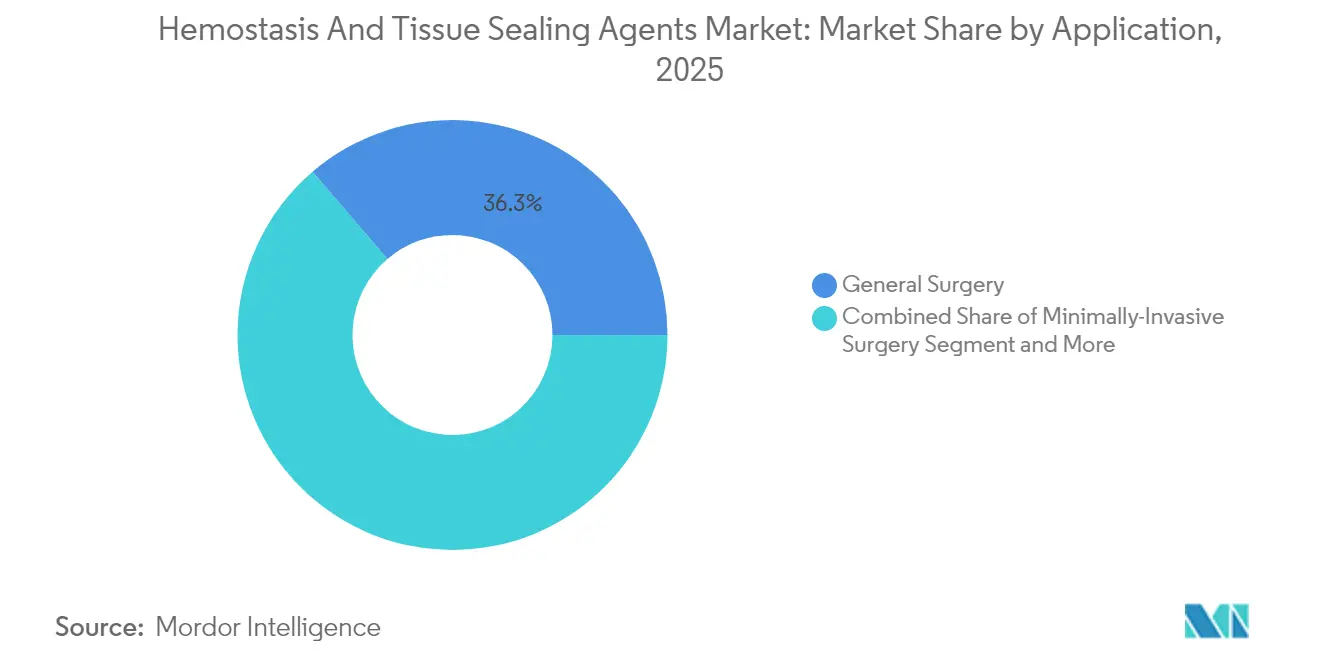

- By application, general surgery dominated with 36.28% share of the hemostasis & tissue sealing agents market size in 2025; minimally invasive surgery is set to expand at a 10.11% CAGR during the same horizon.

- By end-user, hospitals controlled 62.10% of the hemostasis & tissue sealing agents market size in 2025, while ambulatory surgical centers (ASCs) are on track for the highest 10.18% CAGR to 2031.

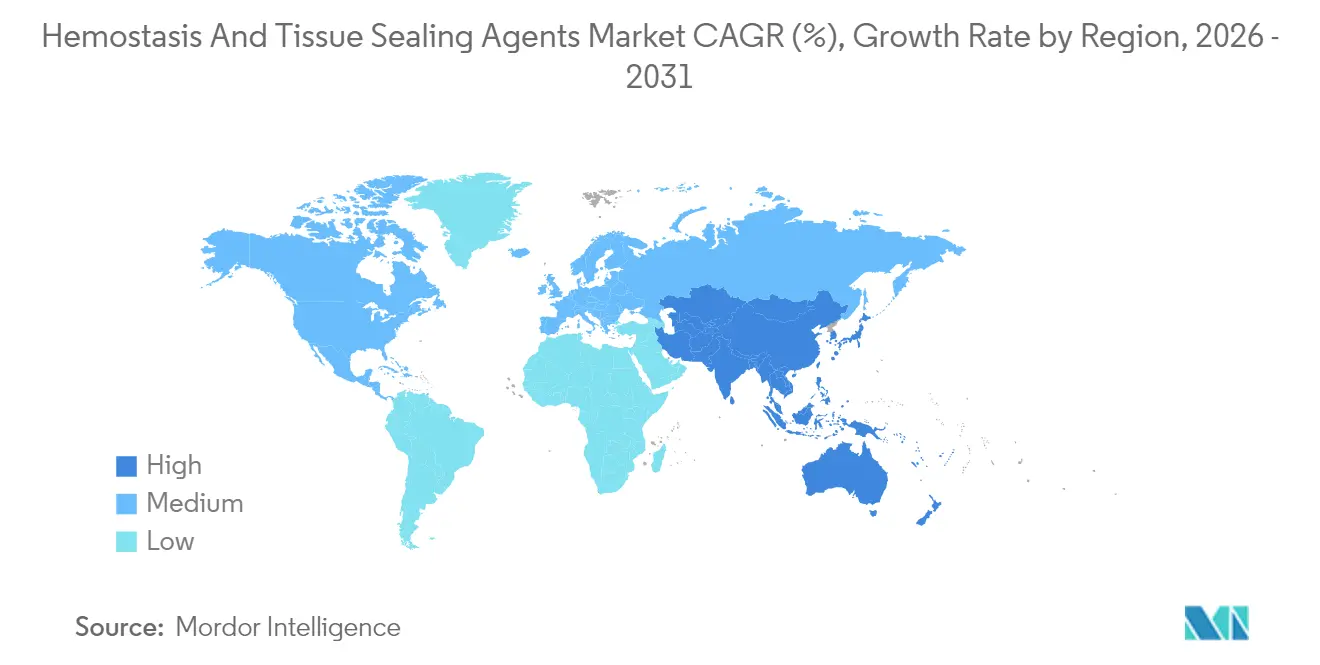

- By geography, North America led with 39.55% revenue share in 2025; Asia-Pacific posts the fastest regional CAGR at 9.38% during the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hemostasis And Tissue Sealing Agents Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Prevalence of Chronic Blood Disorders | +1.2% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Rising Number of Surgical Procedures & Trauma Cases | +1.8% | Global, accelerated in Asia-Pacific and emerging markets | Medium term (2-4 years) |

| Broader Applicability Across Multiple Specialties | +1.5% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Growing Adoption of Minimally Invasive Surgery | +1.4% | Global, led by developed markets | Short term (≤ 2 years) |

| Outpatient ASC Boom Boosting Single-Use Flowables | +0.9% | North America, expanding to Europe | Short term (≤ 2 years) |

| Fast-Track FDA Approvals for Bio-Engineered Plant Agents | +0.7% | North America, with global spillover | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Prevalence of Chronic Blood Disorders

Hemophilia A affects 17.1 per 100,000 males worldwide, and the total diagnosed hemophilia population surpassed 273,000 in 2024, leaving hundreds of thousands more undiagnosed. Annual direct care costs for a single patient can rise beyond USD 869,940, motivating hospitals to adopt advanced sealants that shorten procedures and reduce blood loss. Von Willebrand disease adds further demand diversity, as peri-operative bleeding risks differ across demographic groups[1]Centers for Disease Control and Prevention, “Von Willebrand Disease,” cdc.gov. Gene-therapy protocols now reaching commercialization in hemophilia B often require catheter-based liver infusion, increasing surgical complexity and the need for precision bleeding control. Collectively, these patient pools ensure long-term volume growth for the hemostasis & tissue sealing agents market.

Rising Number of Surgical Procedures & Trauma Cases

Penetrating abdominal trauma represents 24% of trauma admissions, making rapid hemostasis a determinant of survival in both military and civilian settings. Evidence shows that pre-hospital tranexamic acid can cut 24-hour mortality by 19.6% in trauma victims, supporting broader pre-operative use of topical or flowable sealants that augment systemic therapies. Beyond trauma, the global surgical backlog created during the pandemic continues to unwind, lifting elective orthopedic and cardiovascular procedure counts and bolstering steady demand for the hemostasis & tissue sealing agents market.

Broader Applicability Across Multiple Specialties

Modern fibrin sealants now perform across cardiovascular, orthopedic, and general surgery with a 35% reduction in transfusion requirements and 25-minute average time savings per procedure, as demonstrated by VERASEAL clinical data[2]Johnson & Johnson Medical, “VERASEAL Fibrin Sealant,” jnjmedtech.com. Room-temperature patches such as Hemopatch have removed cold-chain constraints, enabling adoption in mid-tier facilities that previously relied on gauze or electrocautery alone. FDA reclassification of viscoelastic coagulation analyzers to Class II status also promotes point-of-care clot monitoring, encouraging surgeons to fine-tune sealant choice by specialty rather than defaulting to a single agent.

Growing Adoption of Minimally Invasive Surgery

Laparoscopic, endoscopic, and robotic platforms dominate many subspecialties, so sealants must deliver rapid control without obscuring the lens or sticking to instruments. Precision spray tips coupled with flexible applicators now allow flowable agents to reach deep cavities while preserving the view for 3-D camera systems. Cardiovascular surgeons executing transcatheter interventions increasingly prefer fibrin or synthetic patches that sustain adhesion under pulsatile flow, helping to extend the hemostasis & tissue sealing agents market into structural heart procedures.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Product Cost | –1.1% | Global, particularly acute in emerging markets | Long term (≥ 4 years) |

| Stringent Regulatory & Approval Pathways | –0.8% | Global, with regional variations | Medium term (2-4 years) |

| Plasma-Derived Fibrinogen Supply Constraints | –0.6% | Global, concentrated in Europe and North America | Short term (≤ 2 years) |

| Eco-Disposal Concerns for Synthetic Adhesives | –0.3% | Europe and North America, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Product Cost

Premium sealants can exceed USD 350 per unit, a burden for facilities where reimbursements trend flat while labor and supply costs climb. Hospitals increasingly request health-economic dossiers that link higher acquisition prices to reductions in transfusions or readmissions. Emerging biosimilars and synthetic alternatives are beginning to narrow price gaps, yet formulary committees in lower-income regions still opt for oxidized cellulose gauze, tempering adoption in part of the hemostasis & tissue sealing agents market.

Stringent Regulatory & Approval Pathways

Mandatory electronic submissions under FDA’s eSTAR De Novo program start in October 2025, adding documentation tasks even as they streamline file architecture[3]Emergo, “FDA Announces De Novo eSTAR Implementation Date,” emergobyul.com. In Europe, MDR demands post-market clinical follow-up and more frequent audits, stretching timelines for small developers. These hurdles elevate development costs, limiting the pipeline of first-in-class agents from academic spin-outs and niche innovators.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Tissue Sealants Drive Innovation Acceleration

Topical Hemostats captured 42.78% of the hemostasis & tissue sealing agents market share in 2025 thanks to decades of surgeon familiarity and broad procedural coverage. They remain staples in orthopedics and general surgery, where quick mechanical tamponade is often sufficient. Yet growth is slower because the segment’s formulations are mature and face commoditization. Tissue Sealing Agents, by contrast, are forecast to advance at a 9.98% CAGR as they introduce dual-function capabilities that both halt bleeding and bond tissue planes, shortening suturing time. Flowable fibrin sealants deliver 92.4% hemostasis within 4 minutes, while synthetic polyethylene glycol glues resist washout in high-flow fields, extending indications to cardiovascular repairs. Room-temperature storage in products such as Hemopatch removes logistical barriers, widening rural and military adoption.

Mechanical sponges still dominate high-volume trauma kits, yet bio-engineered sealants now integrate antibacterial agents to lower infection risk, lifting their value proposition. The hemostasis & tissue sealing agents market benefits as procurement teams bundle these sealants with staplers and energy devices, creating cross-selling momentum. Looking forward, plant-based gels that polymerize on contact with blood are expected to win shelf space in emergency response bags because they combine rapid action with easy disposal. These dynamics underpin the sustained double-digit expansion of tissue sealing agents within the broader hemostasis & tissue sealing agents market.

By Material: Polysaccharide Innovation Accelerates Growth

Collagen formulations commanded 36.10% of 2025 revenue on the strength of long-term safety records and natural resorption profiles. Surgeons appreciate their pliability, which allows patching of irregular surfaces. Gelatin foams provide lower-cost alternatives for routine cases, but they swell several times their volume, limiting use in constrained anatomy. Oxidized regenerated cellulose (ORC) fills niche requirements where acidic pH helps with bacteriostasis.

Polysaccharide-based platforms now record the fastest 12.41% CAGR, a trend driven by breakthroughs such as aldehyde-modified riclin sponges that absorb 59.4 g/g of blood and seal porcine wounds in 30 seconds. Chitosan-derived adhesive films under evaluation for meniscus repair illustrate material versatility across orthopedic sports medicine. Beyond performance, these bio-sourced inputs sidestep plasma-supply volatility and align with hospital sustainability targets. As a result, polysaccharides are steadily expanding their foothold in the hemostasis & tissue sealing agents market, particularly within Asia-Pacific systems that prefer plant-origin consumables for cultural and regulatory reasons.

By Application: Minimally Invasive Surgery Transforms Demand

General surgery generated 36.28% of 2025 sales due to high procedure counts across colorectal, gallbladder, and hernia repairs. Surgeons often keep oxidized cellulose and fibrin glues on standby to manage diffuse oozing. Trauma settings rely on flowables capable of rapid deployment through syringes, whereas hemophilia cases require agents validated in anticoagulated blood.

Minimally invasive surgery represents the fastest-rising niche with a 10.11% CAGR as single-port laparoscopy and robotic systems enter mainstream use. These approaches necessitate sealants that remain visible under high-definition optics, permit precise metered delivery, and avoid instrument fouling. Companies now bundle articulating spray applicators with cartridges to reach retroperitoneal spaces, thus lifting ASPs and contributing meaningfully to the hemostasis & tissue sealing agents market.

By End-User: ASC Growth Reshapes Distribution

Hospitals retained 62.10% share of the hemostasis & tissue sealing agents market size in 2025 since complex vascular and transplant interventions demand top-tier hemostasis supplies. Health systems are centralizing purchasing, leading to portfolio-wide contracts that favor suppliers able to cover mechanical, active, and flowable categories. Economic value analysis drives decisions, and published data indicate FLOSEAL’s use can cut operative time by 9 minutes and save USD 168,000 annually in a mid-size institution.

ASCs post a 10.18% CAGR as payers migrate cataract, ENT, and orthopedic arthroscopy outside hospitals. These centers value single-use kits that minimize turnover time and operate on consignment models to limit cash tied in inventory. Manufacturers respond with small-volume packs and off-the-shelf storage temperatures that align with ASC logistics, reinforcing penetration of the hemostasis & tissue sealing agents market into outpatient care.

Geography Analysis

North America captured 39.55% of 2025 revenue for the hemostasis & tissue sealing agents market. The region benefits from high procedural intensity, robust reimbursement, and a proactive regulatory environment. FDA clearance of the first acellular tissue-engineered vessel for extremity trauma underscores the agency’s support for innovation, giving local developers a home-field advantage. Supply chain resilience remains top of mind after plasma shortages highlighted reliance on imported raw materials, prompting investments in domestic facilities for fibrinogen purification.

Asia-Pacific delivers the highest 9.38% CAGR, driven by expanding hospital infrastructure and medical tourism. India’s hospital market is forecast to reach USD 193 billion by 2032, more than doubling 2024 levels, and this infrastructure build-out directly boosts consumable requirements. In China, procurement reforms are pressuring price points, so vendors emphasize evidence of reduced transfusion rates and shorter stays to justify premium sealants. Japan, South Korea, and Singapore continue to pioneer robotic and hybrid OR installations that naturally rely on advanced bleeding management tools, feeding further growth in the hemostasis & tissue sealing agents market.

Europe sustains a substantial but slower-growing share amid MDR compliance costs and raw-material constraints. The continent’s push for 2 million new plasma donors aims to lower dependence on US supply. Sustainability mandates also spur demand for biodegradable patches, giving European polymer research centers an innovation edge. Meanwhile, reimbursement systems that reward outcomes should eventually favor higher-performance sealants able to document reductions in re-operation rates, supporting a steady contribution to the global hemostasis & tissue sealing agents market.

Competitive Landscape

The hemostasis & tissue sealing agents industry features a moderately fragmented structure: the top five suppliers collectively hold a significant revenue share globally. Baxter, Ethicon, and CSL Behring leverage integrated plasma collection networks and long-tenured brands, affording pricing power and surgeon loyalty. Merit Medical’s USD 120 million buyout of Biolife reinforces a trend toward targeted tuck-ins that add niche formulations such as chitosan-based powders. Teleflex’s planned EUR 760 million purchase of BIOTRONIK’s vascular intervention line reveals appetite for complementary portfolios that span both closure devices and adjunct hemostats.

Innovation pipelines emphasize delivery systems over base chemistry. Examples include dual-chamber syringes that mix fibrin components on demand and robotic-compatible flexible tips designed for single-port surgery. Sustainability themes encourage R&D into recyclable glues and plant-derived scaffolds. New entrants often license university patents on polysaccharide hydrogels with antimicrobial properties, positioning themselves as acquisition targets once clinical data mature. In parallel, established players form partnerships with image-guided device manufacturers to embed sealant applicators into stapling platforms, reinforcing switching costs in the hemostasis & tissue sealing agents market.

Competitive success increasingly hinges on publishing real-world economic evidence. Peer-reviewed studies show VERASEAL reduces transfusions and operating time across multiple specialties, information that procurement teams weigh heavily when selecting formulary products. Manufacturers lacking published data risk relegation to price-driven commodity tiers, underscoring the strategic importance of post-market surveillance and health-outcome registries.

Hemostasis And Tissue Sealing Agents Industry Leaders

Baxter International, Inc.

Becton, Dickinson & Company

Johnson & Johnson

Medtronic Plc.

Pfizer, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Merit Medical Systems acquired Biolife, a specialized hemostatic device maker, for USD 120 million, expanding Merit's acute bleeding control portfolio.

- April 2025: Baxter International launched the room-temperature Hemopatch Sealing Hemostat to simplify operating-room logistics.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global hemostasis and tissue sealing agents market as revenue derived from topical hemostats, biologic or synthetic sealants, and surgical adhesives that are applied inside the operating theater to stem bleeding and unite tissue during general, cardiovascular, orthopedic, neurosurgical, and trauma procedures. According to Mordor Intelligence, the market reached USD 9.88 billion in 2025 and is projected to expand through 2030.

Scope exclusion: consumer first-aid styptics, over-the-counter skin glues, and veterinary products are not evaluated.

Segmentation Overview

- By Product Type

- Topical Hemostats

- Mechanical Hemostats

- Active Hemostats

- Flowable Hemostats

- Tissue Sealing Agents

- Fibrin Sealants

- Synthetic Sealants

- Adhesives

- Cyanoacrylate

- Albumin & Glutaraldehyde

- Topical Hemostats

- By Material

- Gelatin-based

- Collagen-based

- ORC-based

- Polysaccharide-based

- By Application

- General Surgery

- Minimally-Invasive Surgery

- Trauma

- Hemophilia

- Other Applications

- By End-User

- Hospitals

- Ambulatory Surgical Centers

- Other End-Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed surgeons, operating-room nurses, hospital procurement heads, and regulatory specialists across North America, Europe, and key Asia-Pacific hubs. These conversations validated device mix, typical dose sizes, price corridors, and regional adoption curves, while short surveys with distributors filled information gaps on channel margins.

Desk Research

We began by mapping the surgical episode: volumes, procedure mix, and device uptake trends were pulled from open datasets such as FDA 510(k) clearances, WHO Global Health Observatory surgery rates, Eurostat hospital discharge statistics, and the American College of Surgeons NSQIP. Trade codes for fibrin sealants and flowable hemostats were mined from UN Comtrade, followed by import duty filings that reveal average selling prices. Our analysts supplemented these public sources with paywalled intelligence from D&B Hoovers and Dow Jones Factiva to benchmark company revenues and spot inflection points in quarterly calls.

Regulatory guidelines, peer-reviewed journals like Annals of Surgery, and associations such as the International Society on Thrombosis and Haemostasis helped us verify efficacy claims and emerging indications. The sources listed illustrate our evidence base; many additional publications and datasets were reviewed to cross-check figures and clarify assumptions.

Market-Sizing & Forecasting

A top-down reconstruction built on procedure counts and average agent usage per surgery established the demand pool, which was then checked with selective bottom-up supplier roll-ups and channel checks. Core variables, including procedure growth, sealant penetration, average selling price movements, reimbursement shifts, and hospital bed additions, feed a multivariate regression that projects value through 2030. Where bottom-up estimates diverged, we adjusted volumes using midpoint elasticities agreed upon during expert calls before final triangulation.

Data Validation & Update Cycle

Outputs pass anomaly scans and variance checks, after which a senior reviewer challenges assumptions. Reports refresh every year; material events such as new class-wide recalls trigger interim updates. A final analyst sweep ensures clients receive the most current view.

Why Mordor's Hemostasis And Tissue Sealing Agents Baseline Commands Reliability

Published figures often differ because firms pick dissimilar product baskets, price anchors, and revision cadences. We acknowledge these realities upfront and show how scope and variable choice shift totals.

Key gap drivers include narrower hospital-only scopes, unvalidated price erosion rates, and omission of combination agents by some publishers, alongside less frequent refresh cycles that miss recent ASP upticks tied to minimally invasive kits.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 9.88 billion (2025) | Mordor Intelligence | - |

| USD 6.26 billion (2025) | Global Consultancy A | Excludes ambulatory volumes and assumes steep annual ASP decline unsupported by field interviews |

| USD 5.70 billion (2024) | Industry Association B | Segregates hemostats from sealants and omits advanced combination products, compressing market scope |

These comparisons show that when scope is complete, variables are transparent, and updates are timely, Mordor's baseline offers decision-makers a balanced and reproducible reference point.

Key Questions Answered in the Report

What is the current value of the hemostasis & tissue sealing agents market?

The hemostasis & tissue sealing agents market size reached USD 10.68 billion in 2026 and is projected to rise to USD 15.74 billion by 2031.

Which product segment is expanding the fastest?

Tissue Sealing Agents are forecast to grow at a 9.98% CAGR on the back of dual-function sealing and hemostasis capabilities.

Why are polysaccharide materials gaining traction?

Polysaccharide sponges and gels offer ultra-high absorption, rapid biodegradation, and a sustainable supply chain, driving a 12.41% CAGR in this material segment.

How will ambulatory surgical centers influence demand?

ASCs prioritize single-use, quick-prep flowables, pushing their end-user segment to a 10.18% CAGR and reshaping distribution strategies.

What regions present the strongest growth opportunities?

Asia-Pacific leads with a 9.38% CAGR due to hospital build-outs and rising medical tourism, while North America remains the largest revenue contributor.

Page last updated on: