Pegylated Proteins Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.32 Billion |

| Market Size (2031) | USD 3.89 Billion |

| Growth Rate (2026 - 2031) | 10.93% CAGR |

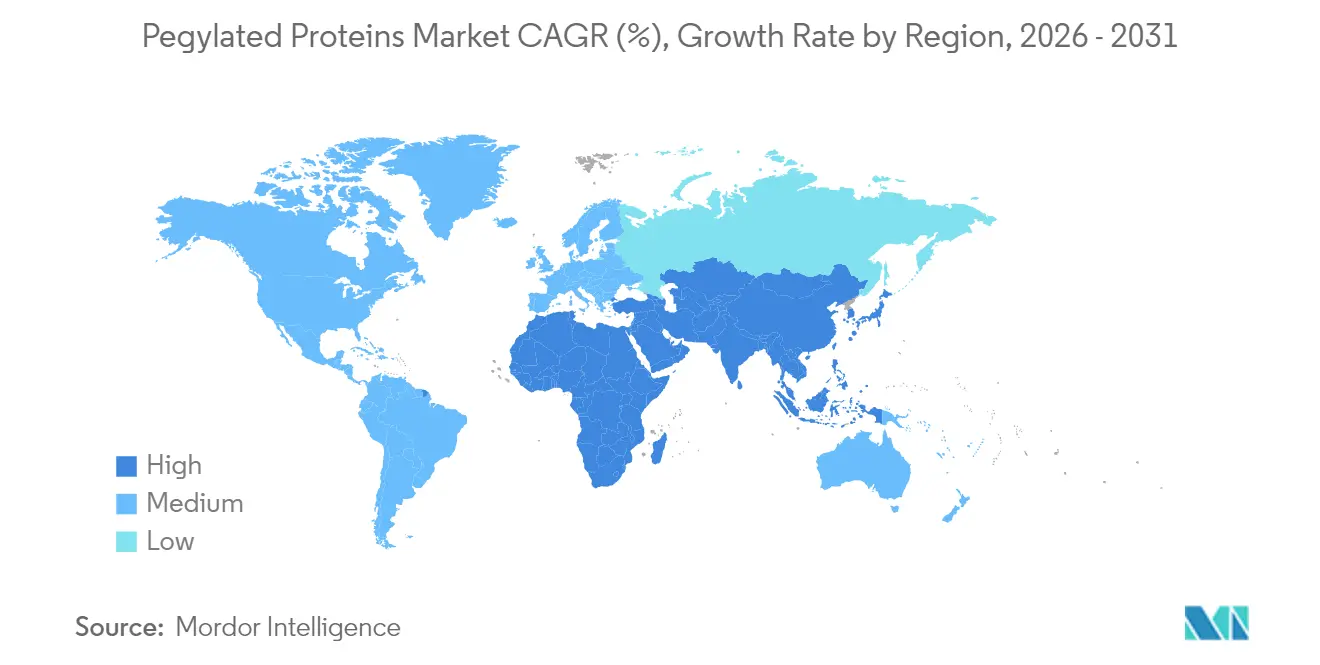

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pegylated Proteins Market Analysis by Mordor Intelligence

The pegylated proteins market size was valued at USD 2.09 billion in 2025 and estimated to grow from USD 2.32 billion in 2026 to reach USD 3.89 billion by 2031, at a CAGR of 10.93% during the forecast period (2026-2031). Growth reflects the technology’s expanding role in extending half-life, reducing immunogenicity and improving stability of biologics across oncology, autoimmune disease and rare-disease pipelines. Vertical integration initiatives, a robust supply of high-purity reagents, and AI-enabled protein-engineering platforms are reinforcing industry momentum. Pharmaceutical developers are accelerating antibody–drug conjugate programs that depend on site-specific PEG linkers to balance potency and safety, while outsourcing of complex chemistries is broadening access to advanced conjugation expertise. Meanwhile, regulatory attention to environmental stewardship is prompting greener production methods, further shaping procurement strategies.

Key Report Takeaways

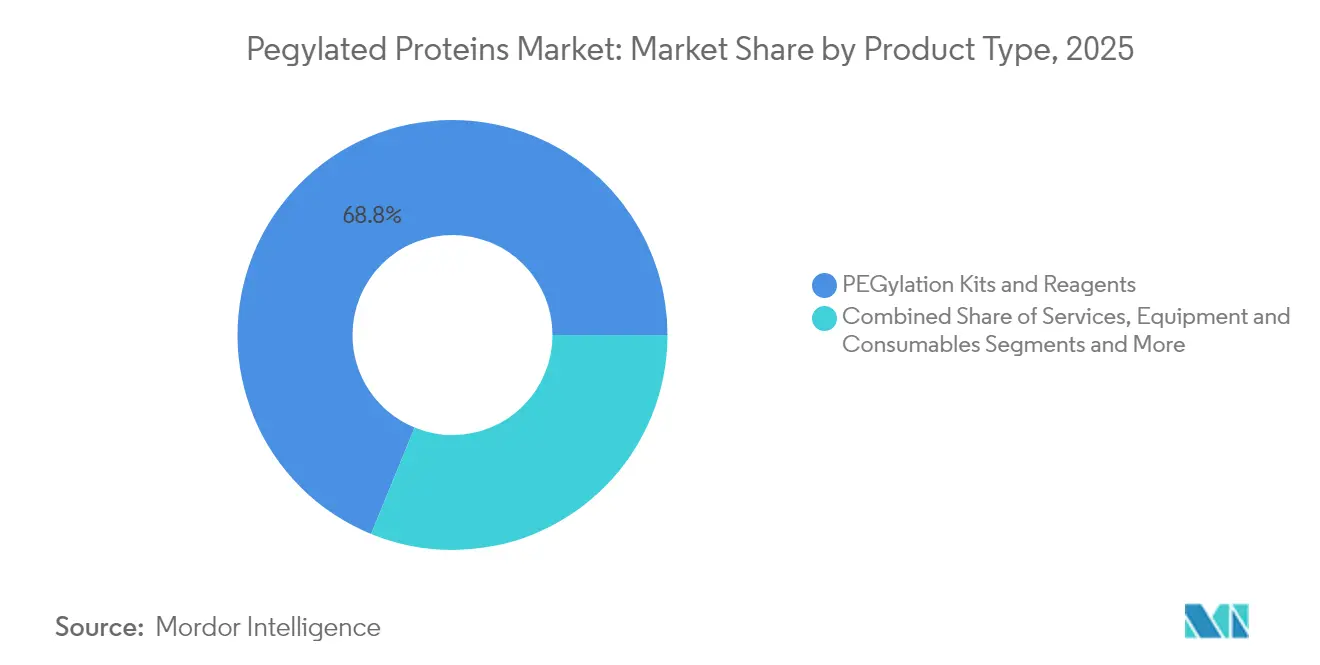

- By product type, PEGylation kits & reagents led with 68.82% revenue share in 2025, whereas services are projected to register a 9.55% CAGR through 2031.

- By protein type, colony-stimulating factors held 62.94% of pegylated proteins market share in 2025, while monoclonal antibodies & ADC linkers are forecast to advance at a 9.86% CAGR.

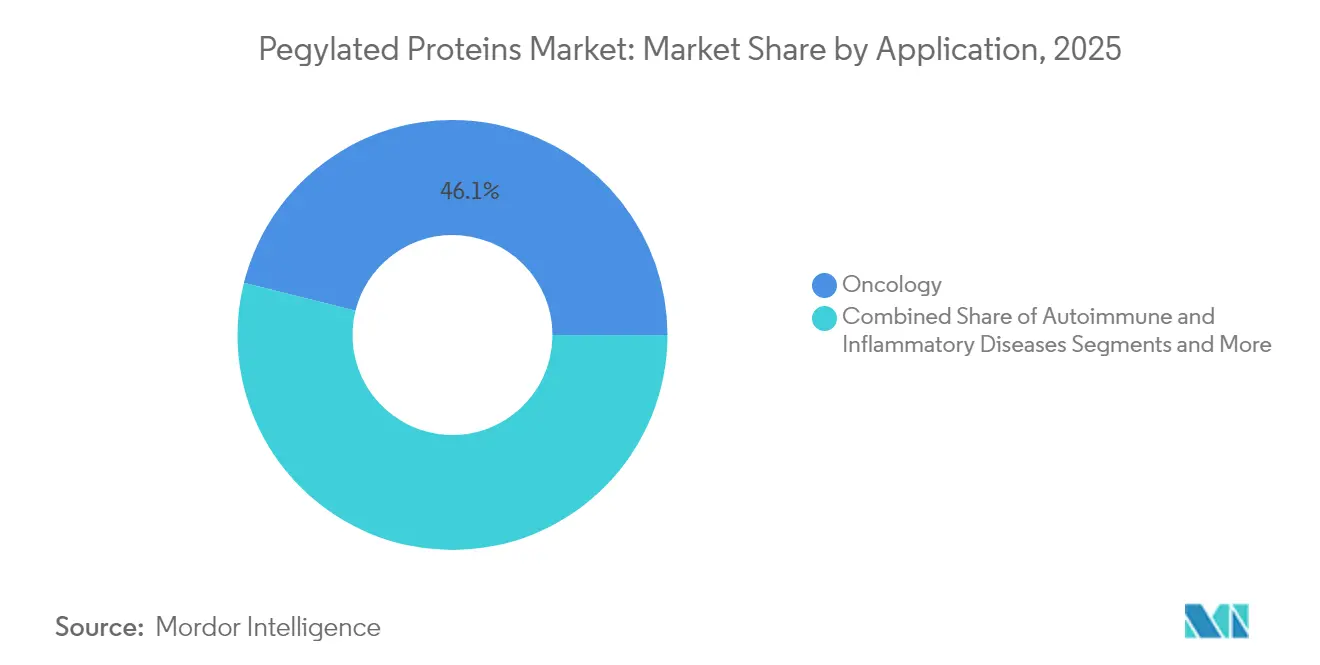

- By application, oncology commanded 46.10% share of the pegylated proteins market size in 2025; autoimmune & inflammatory diseases are projected to expand at 11.02% CAGR to 2031.

- By end user, pharmaceutical & biotechnology companies accounted for 58.97% share in 2025, whereas CROs & CMOs are expected to grow at a 10.62% CAGR.

- By geography, North America contributed 44.05% of 2025 revenue, while Asia-Pacific is forecast to post a 9.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pegylated Proteins Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Prevalence of Chronic Diseases | + 2.1% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

| Increasing Adoption of Long-Acting Biologics | + 1.8% | Global, led by North America, expanding to APAC | Medium term (2-4 years) |

| Expansion of Oncology Pipeline for PEG-Conjugated ADCs | + 2.3% | North America & Europe, with emerging APAC activity | Medium term (2-4 years) |

| R&D Funding Toward Site-Specific Pegylation Chemistries | + 1.4% | North America & Europe core, spill-over to APAC | Long term (≥ 4 years) |

| AI-Enabled Protein Engineering Shortening Optimization Cycles | +1.6% | Global, with early adoption in North America & Europe | Short term (≤ 2 years) |

| Strategic Partnerships for PEG Reagent Supply Security | +1.0% | Global, with focus on US-Europe-Asia supply chains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Prevalence of Chronic Diseases

Demand for long-acting biologics is climbing in aging regions, and PEGylation is integral to lowering dosing frequency for chronic indications. FDA approval of Palopegteriparatide in September 2024 for chronic hypoparathyroidism broadened the technology’s reach beyond oncology by showing that 78.7% of patients maintained normocalcemia without supplemental therapy. The prodrug’s methoxy-PEG carrier improves pharmacokinetics while easing adherence pressures, underscoring how the pegylated proteins market benefits from wider chronic-disease applications.

Increasing Adoption of Long-Acting Biologics

Ropeginterferon alfa-2b achieved a 71.4% complete hematologic response in polycythemia vera at week 52 and cut JAK2 V617F allele burden nearly in half, confirming the value of mono-PEGylated formats.[1]Shan Shan Suo, “Effective Management of Polycythemia Vera With Ropeginterferon Alfa-2b Treatment,” Journal of Hematology, thejh.org An ongoing phase III trial in essential thrombocythemia further validates PEGylation’s flexibility, encouraging drug makers to expand development budgets and fueling pegylated proteins market growth.

Expansion of Oncology Pipeline for PEG-Conjugated ADCs

PEG linkers enhance stability and drug-antibody ratios in new antibody–drug conjugates that collectively topped USD 10 billion in 2023 sales. Datopotamab deruxtecan, patritumab deruxtecan and telisotuzumab vedotin are slated for near-term FDA review, spotlighting the segment’s reliance on precision PEG chemistries. CDMOs have responded by expanding bioconjugation suites, a development that supports ongoing pegylated proteins market expansion.

R&D Funding Toward Site-Specific Pegylation Chemistries

Advances in exactly defined molecular-weight PEGs facilitate pinpoint conjugation control, reducing heterogeneity and immunogenicity.[2]M. J. Burggraef, “Exactly Defined Molecular Weight Poly(ethylene Glycol) Enables Site Identification,” Nature Communications, nature.com Capital is therefore shifting toward site-specific platforms suited for premium-priced therapeutics, positioning innovators to capture high-margin niches within the pegylated proteins market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Drug Failures & Recalls | -1.2% | Global, with higher impact in regulated markets | Short term (≤ 2 years) |

| Anti-PEG Antibody–Mediated Accelerated Blood Clearance | -1.5% | Global, with research focus in North America & Europe | Medium term (2-4 years) |

| Imminent Patent Expiries of First-Generation Pegylated Blockbusters | -0.8% | North America & Europe primarily | Short term (≤ 2 years) |

| Environmental and Regulatory Scrutiny of PEG Waste Streams | -0.7% | Europe leading, expanding to North America & APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Anti-PEG Antibody–Mediated Accelerated Blood Clearance

Researchers at Cornell University demonstrated that poly(carboxybetaine) lipid nanoparticles can bypass anti-PEG antibodies, thereby improving mRNA vaccine performance. Alternative polymers such as branched random-PEG and ganglioside lipid nanoparticles are emerging, yet long-term safety data remain limited.[3] Victoria Atkinson, “Modified Polymer Could Help Drugs Evade Immune System,” Chemical & Engineering News, cen.acs.org Persistent immunogenicity concerns may temper short-term uptake of PEGylated formats.

Environmental and Regulatory Scrutiny of PEG Waste Streams

Europe has begun to weigh lifecycle solvent burdens, noting that peptide APIs can require up to 14 tons of solvent per kilogram produced. Regulatory scrutiny is driving adoption of greener methods and biodegradable packaging, raising compliance costs that could constrain the pegylated proteins market, especially for smaller producers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Services Emerge as Growth Engine

PEGylation kits & reagents accounted for 68.82% of pegylated proteins market share in 2025, reflecting entrenched preferences among drug makers for in-house control of routine conjugations. These off-the-shelf products benefit from streamlined regulatory dossiers and repeat-purchase dynamics that stabilize demand. Services, however, are expanding at a 9.55% CAGR through 2031 as site-specific conjugation, homogenous linker design and analytical validation exceed the skill sets of many internal teams.

The services boom is enlarging the pegylated proteins market size as clients tap CDMOs for custom PEG synthesis, process scale-up and GMP batch release. Mature players are broadening menus to include advanced analytics and regulatory documentation, while niche specialists carve out space in high-purity linker production. This dual-track ecosystem—standard reagents for legacy workflows and bespoke services for frontier science—positions contract providers to capture incremental value as pipeline complexity rises.

By Protein Type: ADC Linkers Drive Innovation

Colony-stimulating factors retained 62.94% of pegylated proteins market share in 2025 thanks to pegfilgrastim’s proven ability to mobilize peripheral stem cells in a single dose. Interferons remain essential in multiple-sclerosis care, keeping that cornerstone segment resilient.

Monoclonal antibodies & ADC linkers are set to post a 9.86% CAGR, the fastest within the category, as oncology developers demand precisely weighted PEG spacers to balance potency and tolerability. These requirements are pushing innovators to adopt exactly defined molecular-weight PEGs that minimize heterogeneity and immunogenicity. The trend is widening pegylated proteins market size for linker chemistries and reinforcing CDMO investment in dedicated bioconjugation suites.

By Application: Autoimmune Diseases Show Promise

Oncology commanded 46.10% of 2025 revenue, propelled by antibody–drug conjugates that use PEG linkers to fine-tune systemic exposure and expand therapeutic windows. Blockbusters such as Enhertu and Kadcyla continue to anchor the pegylated proteins market, and multiple late-stage assets promise to deepen this revenue stream.

Autoimmune & inflammatory diseases represent the fastest-moving application, expected to grow at 11.02% CAGR through 2031. Exosome-modified AAV gene therapy for autoimmune hepatitis recently boosted hepatic T-reg levels while lowering ALT, illustrating PEGylation’s versatility beyond cytotoxic payloads. As immune-mediated indications proliferate, demand for long-acting, tolerable biologics is poised to expand pegylated proteins market size in non-oncology franchises.

By End User: CROs Gain Momentum

Pharmaceutical & biotechnology companies held 58.97% of spending in 2025, leveraging in-house capabilities for late-stage and commercial products. Their dominance secures baseline demand for reagents, equipment and validated workflows that underpin pegylated proteins market stability.

CROs & CMOs are projected to advance at a 10.62% CAGR because sponsors increasingly outsource complex site-specific conjugations. Samsung Biologics’ USD 1.4 billion manufacturing deal in early 2025 exemplifies this shift toward external capacity that can scale multiproduct, multi-modality programs. Expanded outsourcing pipelines thus inject fresh momentum into overall pegylated proteins market growth.

Geography Analysis

North America contributed 44.05% of 2025 revenue, supported by a steady cadence of FDA approvals and extensive manufacturing infrastructure. Thermo Fisher’s USD 2 billion multiyear investment plan and Merck’s USD 1 billion biologics center in Delaware demonstrate continued capital inflows that reinforce pegylated proteins market size in the region. Regulatory clarity and strong IP protections further encourage innovators to base high-value conjugation work domestically.

Europe maintains steady expansion underpinned by mature biopharmaceutical clusters and stringent environmental policies that are prompting early adoption of greener PEGylation practices. The region’s focus on solvent reduction and waste-stream monitoring is influencing global supply contracts, nudging manufacturers toward sustainable chemistries that can meet future compliance thresholds. Established reimbursement frameworks also ensure predictable uptake of approved PEGylated therapies, sustaining pegylated proteins market share across major EU economies.

Asia-Pacific is the fastest-growing territory at a 9.55% CAGR, reflecting rising biomanufacturing capacity and regulatory harmonization that lowers market-entry barriers. Samsung Biologics is adding a new plant to expand linker output, China and India are scaling GMP suites, and regional governments are funding biotech parks to attract multinational projects. These initiatives are enlarging pegylated proteins market size across APAC, while local demand for affordable biologics accelerates technology transfer and workforce training. Collectively, these dynamics are redistributing future growth toward the East without eroding North America’s innovation leadership.

Competitive Landscape

The pegylated proteins market remains moderately fragmented: no single company exceeds one-quarter of global revenue, and about a dozen firms collectively control roughly 70%. Intellectual-property portfolios, GMP reagent output and regulatory track records frame competitive barriers. Nektar’s November 2024 divestiture of its Alabama plant to Ampersand Capital Partners exemplifies how firms recalibrate toward core R&D while securing reagent continuity for clients. Vertical integration lets larger players capture more value, yet niche innovators that specialize in site-specific linkers or AI-driven design continue to win contracts.

Partnerships are intensifying under the proposed U.S. BIOSECURE Act, which will screen foreign supply chains. This scrutiny favors vendors with multi-regional footprints. Furthermore, efforts to replace PEG with PCB or ganglioside polymers are spawning start-ups focused on stealth alternatives, hinting at future disruption. Standardization under FDA 21 CFR 172.820 bolsters incumbents who already meet specification thresholds.

Pegylated Proteins Industry Leaders

Merck KGaA

Thermo Fisher Scientific, Inc

Creative PEGworks

NOF Corporation

JenKem Technology

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Nuclera signed a collaboration with Cytiva to combine its eProtein Discovery System and Cytiva’s Biacore SPR platform for streamlined protein optimization.

- December 2024: Ampersand Capital Partners finalized its acquisition of Nektar Therapeutics’ PEGylation reagent manufacturing business.

Global Pegylated Proteins Market Report Scope

As per the scope of the report, Pegylation is the process of binding or alteration of biological molecules by conjugation with polyethylene glycol is known as PEGylation. PEGylation enhances the stability and solubility of the drug and declines immunogenicity by changing the molecule's electrostatic binding, confirmation, and hydrophobicity. The PEGylated Proteins Market is Segmented by Product Type (PEGylation Kits and Reagents (Monofunctional Linear PEGs, Bifunctional PEGs), Services, and Other Product Types), Protein Type (Colony-stimulating Factor, Interferon, Erythropoietin, and Other Protein Types), End User (Pharmaceutical and Biotechnology Companies, Contract Research Organizations, and Academic Research Institutes), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated sizes and trends for 17 countries across major regions globally. The report offers the value (USD) for the above segments.

| PEGylation Kits & Reagents | Monofunctional Linear PEGs |

| Bifunctional & Multi-arm PEGs | |

| Branched/Y-shape PEGs | |

| Services | Custom PEG Synthesis |

| Analytical & Characterization Services | |

| Contract PEGylation Manufacturing | |

| PEGylated Therapeutic Active Ingredients | |

| Equipment & Consumables |

| Colony-Stimulating Factors (CSFs) |

| Interferons |

| Erythropoietin |

| Recombinant Factor VIII |

| Enzymes (e.g., L-asparaginase) |

| Monoclonal Antibodies & ADC Linkers |

| Other Protein Types |

| Oncology |

| Autoimmune & Inflammatory Diseases |

| Hepatitis & Viral Infections |

| Hematology (Hemophilia, Anemia) |

| Endocrine & Metabolic Disorders |

| Others |

| Pharmaceutical & Biotechnology Companies |

| CROs & CMOs |

| Academic & Research Institutes |

| Hospital Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | PEGylation Kits & Reagents | Monofunctional Linear PEGs |

| Bifunctional & Multi-arm PEGs | ||

| Branched/Y-shape PEGs | ||

| Services | Custom PEG Synthesis | |

| Analytical & Characterization Services | ||

| Contract PEGylation Manufacturing | ||

| PEGylated Therapeutic Active Ingredients | ||

| Equipment & Consumables | ||

| By Protein Type | Colony-Stimulating Factors (CSFs) | |

| Interferons | ||

| Erythropoietin | ||

| Recombinant Factor VIII | ||

| Enzymes (e.g., L-asparaginase) | ||

| Monoclonal Antibodies & ADC Linkers | ||

| Other Protein Types | ||

| By Application | Oncology | |

| Autoimmune & Inflammatory Diseases | ||

| Hepatitis & Viral Infections | ||

| Hematology (Hemophilia, Anemia) | ||

| Endocrine & Metabolic Disorders | ||

| Others | ||

| By End User | Pharmaceutical & Biotechnology Companies | |

| CROs & CMOs | ||

| Academic & Research Institutes | ||

| Hospital Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving the strong growth of the pegylated proteins market?

Elevated demand for long-acting biologics, expanding oncology ADC pipelines, and AI-enabled protein-engineering platforms are collectively propelling the market at an 10.93% CAGR.

Which product category currently leads the pegylated proteins market?

PEGylation kits & reagents hold 68.82% revenue share, reflecting widespread in-house use by pharmaceutical developers.

Why are CROs and CMOs gaining share in pegylated services?

Drug sponsors are outsourcing complex site-specific conjugation to specialized providers, giving CROs & CMOs a forecast 10.62% CAGR through 2031.

Which region is growing fastest in PEGylation adoption?

Asia-Pacific is projected to expand at 9.55% CAGR, supported by government incentives and large-scale CDMO investments.

How are anti-PEG antibodies influencing product design?

The rise of anti-PEG antibody concerns is prompting research into alternative stealth polymers like PCB and ganglioside LNPs, influencing next-generation conjugate strategies.

What impact will environmental regulations have on PEGylation manufacturing?

Tightening solvent and waste guidelines in Europe and beyond are encouraging greener production techniques, potentially raising compliance costs but stimulating innovation in sustainable chemistries.

Page last updated on: