Light-Sport Aircraft Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

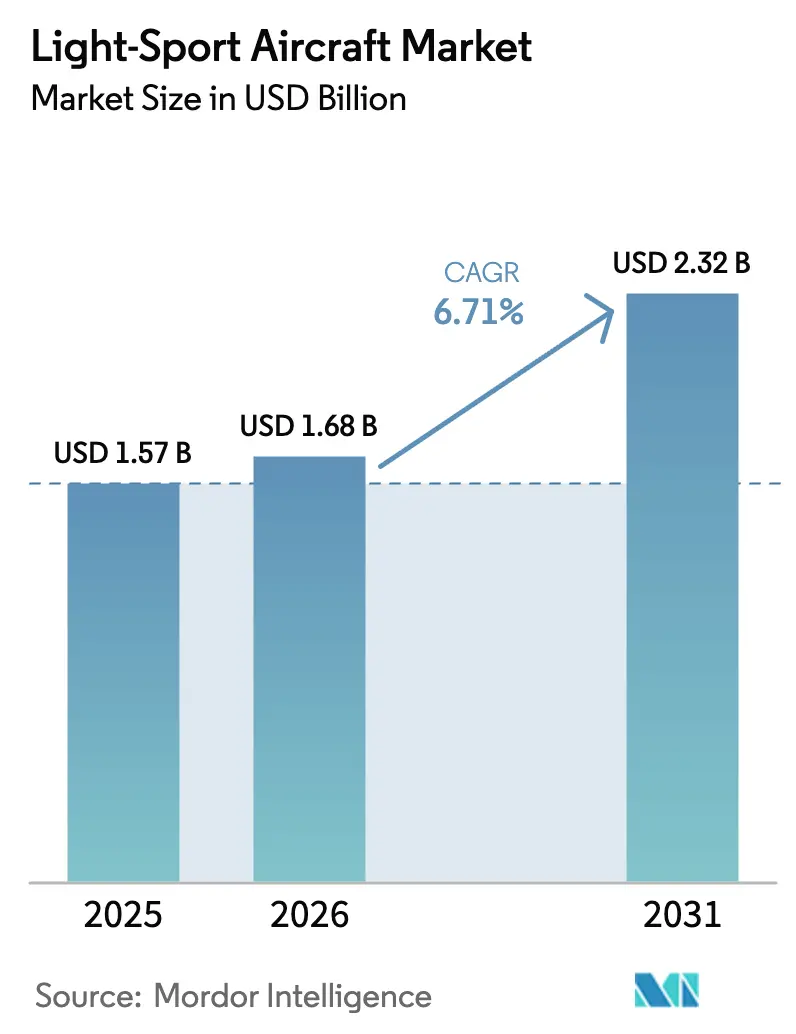

| Market Size (2026) | USD 1.68 Billion |

| Market Size (2031) | USD 2.32 Billion |

| Growth Rate (2026 - 2031) | 6.71% CAGR |

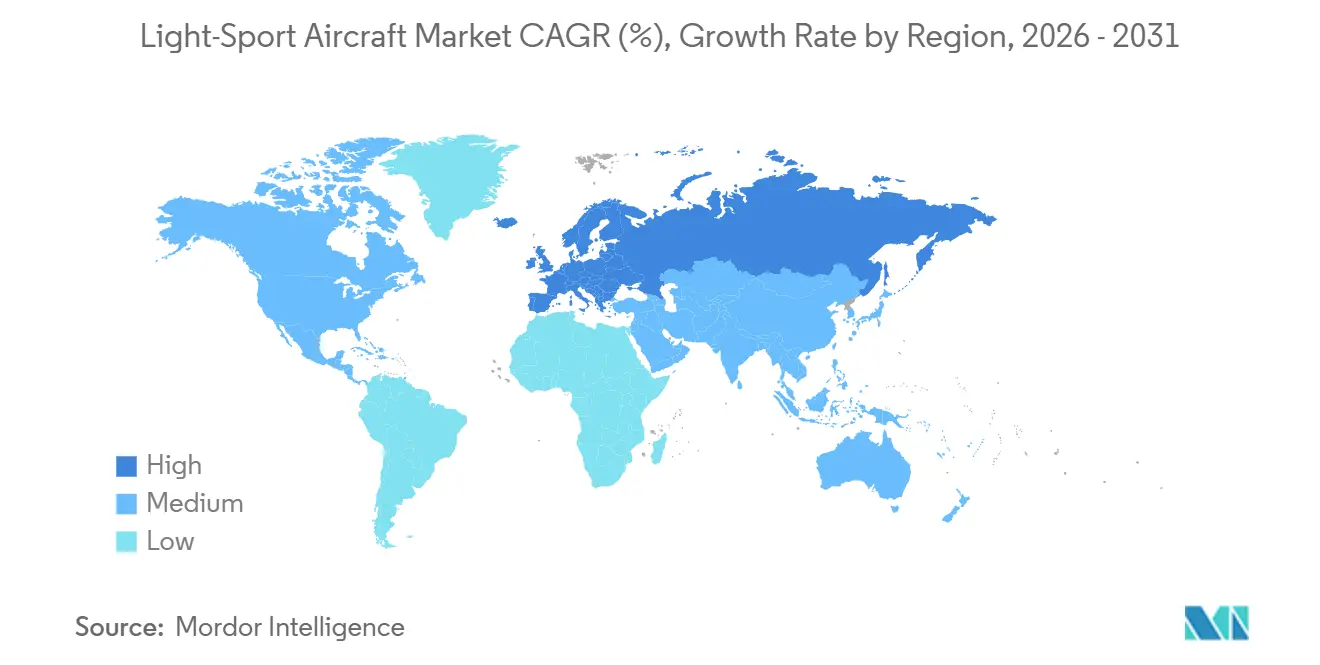

| Fastest Growing Market | Europe |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Light-Sport Aircraft Market Analysis by Mordor Intelligence

The light-sport aircraft market size is expected to grow from USD 1.57 billion in 2025 to USD 1.68 billion in 2026 and is forecasted to reach USD 2.32 billion by 2031 at a 6.71% CAGR over 2026-2031. The change in trajectory is rooted in the FAA's Modernization of Special Airworthiness Certification final rule, which replaces weight ceilings with performance-based stall-speed criteria that expand what qualifies as lightsport, reshaping buyer behavior and training-fleet planning without adding medical burdens for medical pilots holding a driver's license. Momentum is shifting toward amphibious-capable designs and electrified trainers, as seaplanes and electric propulsion outpace the category average. At the same time, internal combustion engines remain prevalent due to range and refueling advantages, especially in high-utilization training operations. Flight training demand continues to anchor near-term unit orders, reflecting large fleet additions by major schools. At the same time, aerial work unlocks incremental use cases as MOSAIC clarifies compensated operations under manufacturer-stated limitations. Europe's faster growth outlook rides on strong OEM presence and tailwinds from propulsion-system certification, while North America retains the largest installed base and the most immediate regulatory lift. Competitive intensity remains moderate, with training-focused OEMs expanding capacity and premium performance brands differentiating through safety features, modern avionics, and factory support networks.

Key Report Takeaways

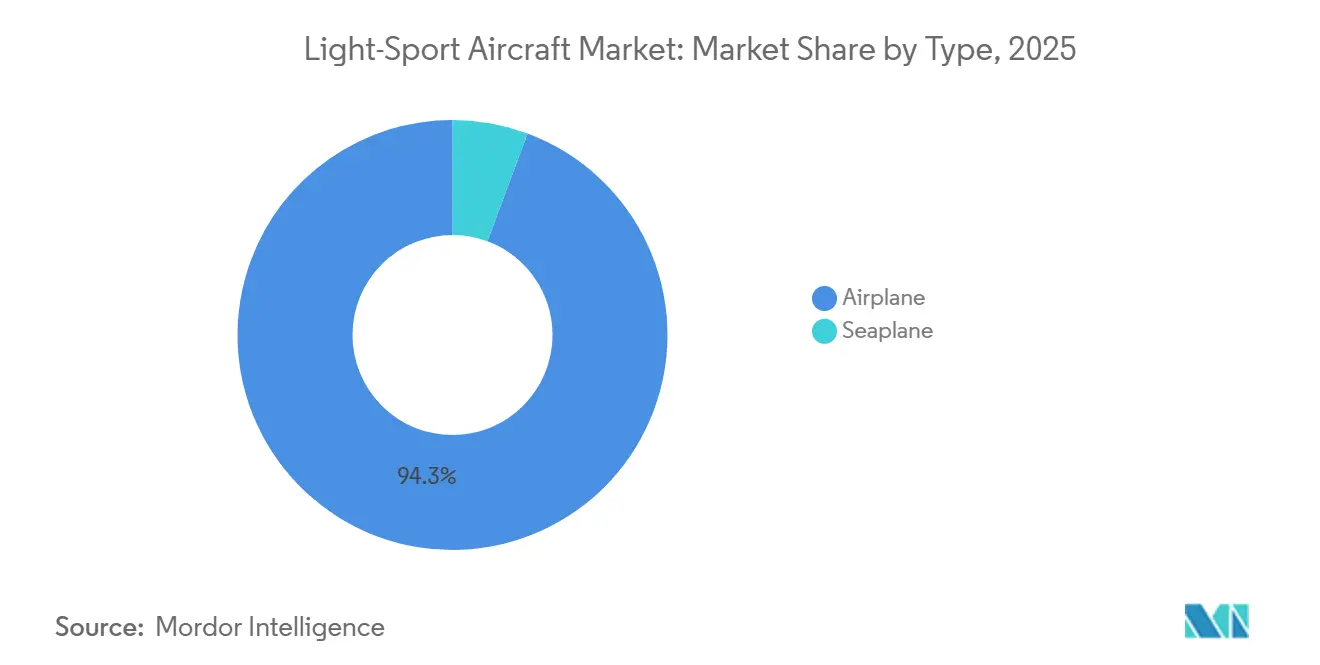

- By type, airplanes led the light-sport aircraft market with a 94.32% share in 2025; seaplanes are projected to grow at a 7.78% CAGR through 2031.

- By propulsion, internal combustion engines held a 90.45% share of the light-sport aircraft market in 2025; electric propulsion is projected to grow at a 14.43% CAGR through 2031.

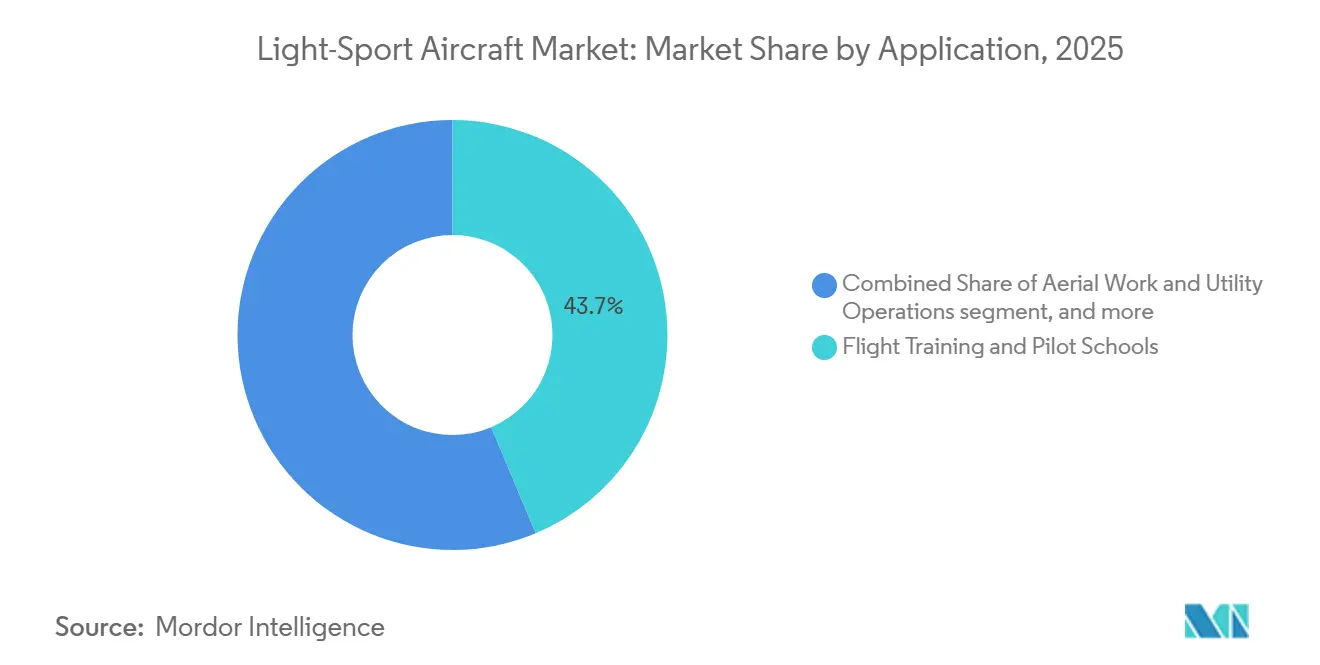

- By application, flight training and pilot schools accounted for a 43.67% share of the light-sport aircraft market in 2025; aerial work and utility operations are projected to grow at an 8.62% CAGR through 2031.

- By geography, North America held a 40.03% share of the light-sport aircraft market in 2025; Europe is projected to grow at a 7.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Light-Sport Aircraft Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| MOSAIC final rule expands LSA capabilities and sport pilot privileges | +2.3% | Global, strongest in North America and Europe; spillover to Asia-Pacific via certification reciprocity | Medium term (2-4 years) |

| Flight training demand and fleet renewal favor cost-effective LSA trainers | +1.8% | North America (primary), Europe and Asia-Pacific (emerging hubs in India, South Korea) | Short term (≤ 2 years) |

| Composite airframes and modern avionics reduce operating cost and improve safety | +1.2% | Global; strongest adoption in training fleets (North America, Europe) and owner-flown segments | Long term (≥ 4 years) |

| BasicMed expansion and sport-pilot pathways broaden the eligible pilot pool | +0.9% | United States (BasicMed), Canada (recognition pathways); limited EASA equivalency | Medium term (2-4 years) |

| Unleaded avgas transition pathways (fleet authorizations) de-risk engine operations | +0.8% | United States (2030 mandate), Alaska (2032); parallel transition in Canada, Europe following FAA lead | Medium term (2-4 years) |

| Limited aerial-work authorizations under MOSAIC create new revenue streams | +0.5% | North America, Australia (agricultural/infrastructure patrol); regulatory clarity pending in EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

MOSAIC Final Rule Expands LSA Capabilities And Sport Pilot Privileges

The FAA’s July 2025 MOSAIC final rule replaces prescriptive weight limits with a 59-knot calibrated airspeed VS1 threshold for sport pilots and a 61-knot VS0 for aircraft certificated after July 2026, enabling broader aircraft eligibility and operational flexibility. The rule authorizes four-seat configurations, retractable landing gear, controllable-pitch propellers, and night operations subject to appropriate endorsements and medical status under the new framework.[1]Federal Aviation Administration, “Modernization of Special Airworthiness Certification,” Federal Register, federalregister.gov The shift immediately widens the pool of sport-pilot-eligible aircraft, with association analysis indicating that a large portion of legacy single-engine piston models now fall within sport-pilot privileges under performance criteria rather than legacy weight caps. Manufacturer statements and product updates show rapid alignment, including amphibious and advanced avionics variants that benefit from the performance-based approach. The staged effective dates, with pilot training and repairman updates in late 2025 and airworthiness certification changes in 2026, create a manageable transition period for schools and OEMs to adjust fleets and production scheduling.

Flight Training Demand And Fleet Renewal Favor Cost-Effective LSA Trainers

High-utilization training schools continue to expand fleets with modern, low-operating-cost platforms, sustaining near-term order books and line utilization for LSA-aligned OEMs. Fleet procurement in 2025 and early 2026 concentrated on glass-cockpit trainers and multi-engine types to support progression from entry certificates to commercial ratings, signaling the value of standardized avionics and maintenance across large operations. OEM announcements point to increased training capacity at schools in North America and Europe, with deliveries of single- and twin-trainers that fit within or parallel to the expanding LSA envelope. Aligning MOSAIC privileges with training profiles, including night operations with endorsements, enhances aircraft utility and scheduling flexibility at busy schools. Electrified trainers add a complementary pathway to sustainability goals at select locations where short sorties and charging infrastructure align with curriculum needs.

BasicMed Expansion And Sport-Pilot Pathways Broaden The Eligible Pilot Pool

Effective November 18, 2024, BasicMed parameters expanded to cover up to seven occupants and a 12,500-pound maximum takeoff weight, while allowing pilot examiners to conduct flight checks under BasicMed, aligning with MOSAIC’s broader aircraft eligibility and smoothing progression from sport to private privileges.[2]Federal Aviation Administration, “FAA Updates BasicMed Program,” Federal Aviation Administration, faa.gov The pathway enables new entrants to start under sport-pilot privileges with a driver’s license, then transition to private-pilot operations while meeting BasicMed’s periodic physician exam and online education requirements. This alignment reduces attrition due to medical hurdles for pilots who meet BasicMed requirements and streamlines training investments across certificates. The combined effect increases the addressable base of recreational and career-oriented pilots who can legally operate a wider range of aircraft within an LSA-relevant performance envelope. Schools and clubs benefit from the continuity of training between sport and private tracks, improving fleet utilization and student retention prospects.

Composite Airframes And Modern Avionics Reduce Operating Cost And Improve Safety

Carbon-fiber and advanced composite structures reduce airframe weight while maintaining strength, delivering fuel savings and higher useful loads that fit within MOSAIC’s performance criteria. Factory production and builder-assist options have matured for popular models, providing standardized glass panels, ADS-B compliance, and autopilot features that align with training and safety requirements. Safety-forward designs include integrated angle-of-attack indication and spin-resistant configurations on select amphibious platforms, which can aid training consistency and risk management in the entry segment. Insurers have indicated that documented safety features and modern avionics can contribute to premium advantages for well-operated fleets, especially when paired with recurrent training and hangared storage. OEM roadmaps that combine composite construction, modern avionics, and compliant performance envelopes are positioned to capture replacement cycles at schools and flying clubs as MOSAIC broadens eligible models.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-chain bottlenecks for engines, avionics, and composites | -1.1% | Global (Rotax engines, Garmin avionics); acute in EU due to Ukraine relocation, Asia-Pacific for imports | Medium term (2-4 years) |

| Insurance availability and premium pressure for GA/LSA operators | -0.6% | North America (litigious jurisdictions), Global (reinsurance-driven hardening) | Short term (≤ 2 years) |

| Electric LSA endurance/charging limits constrain training throughput | -0.3% | Adoption pockets: Europe (Velis Electro fleets), North America (early-adopter schools) | Long term (≥ 4 years) |

| Airspace and VFR/day restrictions cap utility in dense corridors | -0.2% | Europe (Class A/B restrictions), US coastal corridors (New York, Los Angeles); less severe in rural hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Insurance Availability And Premium Pressure For GA/LSA Operators

Aviation insurers have flagged modest firming for 2026, with the best pricing available to operators that maintain clean loss records, structured recurrent training, and documented safety features across fleets. Premium differentiation often reflects pilot total time, time in type, recency of training, and aircraft equipment levels more than the specific medical certification path, which lowers uncertainty for operators adapting to MOSAIC and BasicMed intersections. Rate dispersion remains notable for new operations without claims history or for higher hull values, which can translate to elevated base rates until operators establish stable safety performance over time. Documented mitigations like hangared storage, defined currency standards, and modern avionics often qualify for credits that partially offset broader market pressure. The overall implication for the light-sport aircraft market is that professionally managed fleets can contain insurance inflation. At the same time, casual or newly established operations face a higher bar to achieve best-available pricing.

Supply-Chain Bottlenecks For Engines, Avionics, And Composites

Geopolitical and industrial constraints have extended lead times for critical subsystems and materials in recent cycles, with specific OEM relocations and capacity adjustments illustrating continued fragility in certain value-chain tiers. Production lines that integrate more vertically or add semi-automated capacity for motors or key components can better buffer demand surges that follow regulatory shifts, such as MOSAIC. Airframe manufacturers expanding facilities and forward-booking slots signal demand visibility, but must coordinate with avionics and engine suppliers to prevent kit allocations from delaying completed-aircraft deliveries. For operators and schools, parts scarcity or delayed avionics shipments can lengthen downtime, affecting training throughput and utilization targets. As suppliers ramp up output across Europe and North America through targeted investments, risk reduces over a multi-year period. However, tactical scheduling and diversified sourcing remain prudent in the light-sport aircraft market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Airplanes Dominate, Seaplanes Gain Momentum

Airplanes accounted for 94.32% market share in 2025, the highest share across types in the light-sport aircraft market, while seaplanes are projected to grow at a 7.78% CAGR to 2031 from a smaller installed base. The profile reflects extensive land-based training fleets and high dispatch reliability on paved and grass strips, with embedded infrastructure at schools and clubs across North America and Europe. OEM shipment data show meaningful volumes for conventional configurations, supported by broad familiarity among instructors and maintenance teams. Amphibious platforms add distinct use cases in waterfront regions and recreational corridors, and they benefit from MOSAIC’s performance framing, which favors stall-speed parameters for operational approval rather than legacy weight caps. A flagship amphibious model raised its gross weight in 2024 and emphasizes spin-resistant characteristics, placing it as a premium niche choice for operators who value water access and safety systems.

Growth prospects for seaplanes reflect underpenetrated coastal, lake-country, and island routes where waterborne access can substitute for longer overland segments or limited surface infrastructure. With MOSAIC’s flexibility around performance-based standards, future four-seat configurations and expanded equipment options improve mission versatility where takeoff and landing areas are constrained by geography. For landplanes, the light-sport aircraft market size narrative centers on training-cycle stability, high airframe utilization, and standardized avionics that streamline instruction and maintenance planning at scale. The interplay between these subsegments supports a portfolio approach for schools and owner-operators who split time between paved strips and water sites depending on season, mission, and region. Shipment concentration in 2025 among a handful of brands underscores the importance of after-sales support and the availability of ready parts in sustaining uptime for both land and water operations.

By Propulsion Type: Electric Surges As ICE Holds Share

Internal combustion engines held 90.45% market share in 2025, maintaining their leading position in the light-sport aircraft market, reflecting their refueling speed, range, and established maintenance networks. Electric propulsion is projected to grow at a 14.43% CAGR through 2031, driven by type-certified electric trainers entering new national markets and certified motors reaching production readiness with integrated power electronics. ICE platforms retain strong appeal in training environments that demand rapid turnarounds and consistent sortie lengths, with multi-fuel capability on select modern engines supporting unleaded transitions in parallel with regulatory milestones. Electric trainers deliver compelling noise and emissions profiles for urban or noise-sensitive airfields, and early adopters align them to short-stint syllabi and local-area circuits where infrastructure supports repeat charging within an instructional day.

The light-sport aircraft market-share dynamic between ICE and electric reflects a dual-track adoption, where sustainability targets and community acceptance drive experimentation. At the same time, operational throughput sustains ICE's predominance in high-hour programs. Certified electric motors with strong power-to-weight ratios position OEMs to explore two- to four-seat applications, which could broaden use cases as battery systems improve and hybrid architectures emerge. Fleet managers weigh acquisition cost, infrastructure, and dispatch needs against environmental and reputational goals, shaping a measured acceleration curve in electric adoption over the forecast period. ICE remains the default for cross-country training segments and back-to-back scheduling. At the same time, electric gains are being made in pattern work and community engagement initiatives at facilities with grid capacity and charging solutions.

By Application: Training Anchors, Aerial Work Accelerates

Flight training and pilot schools accounted for 43.67% of 2025 demand in the light-sport aircraft market, as measured by application mix, supported by multi-year fleet programs and nationwide maintenance bases at large providers. Aerial work and utility operations are projected to grow at 8.62% CAGR to 2031 as MOSAIC authorizes specified compensated operations when documented in the Pilot’s Operating Handbook and in the aircraft statement of compliance. For training, standardized glass cockpits and modern safety systems help schools maintain consistency and reduce transition friction between aircraft types, which supports throughput goals across complex nationwide networks. For aerial work, expanded use cases such as infrastructure inspection and agricultural surveillance create incremental flying hours and utilization opportunities in regions where missions align with VFR day conditions.

The light-sport aircraft market narrative for aerial work presents new revenue opportunities for local operators and small providers who can equip aircraft with appropriate sensors and documentation to support compliant missions. Training remains the largest anchor across applications due to predictable student pipelines and well-defined rating progressions, which favor fleet standardization and scale procurement. Recreational ownership and clubs continue to supply the balance of hours, with MOSAIC’s allowances for night operations with proper endorsements increasing potential utilization windows in favorable conditions. Over the forecast horizon, the mix of training stability and expansion of aerial work supports a balanced growth profile as operators adapt fleets to performance-based certification and incremental mission sets.

Geography Analysis

North America held a 40.03% share of the light-sport aircraft market in 2025 and is expected to benefit from MOSAIC’s staged implementation across training and airworthiness. The regulatory modernization expands eligible aircraft and missions, supporting fleet augmentation at schools and rental networks. Schools with national networks have begun taking deliveries aligned to their plans, reinforcing a steady pipeline of glass-cockpit trainers. As BasicMed and MOSAIC converge, pilots may progress more fluidly from sport to private privileges, improving utility and time-on-type continuity for operators. Across the US and Canada, regulatory validation and OEM support underpin the fleet renewal cycle in the light-sport aircraft market.

Europe is projected to grow at a 7.88% CAGR through 2031, supported by a robust OEM ecosystem and momentum in propulsion certification. European training organizations continue to add single and twin models with modern avionics to scale capacity, guided by standardized procedures for airline-oriented training tracks. With a certified 125 kW electric motor approved by EASA and production capacity enabled by semi-automated lines in France and the UK, European OEMs and integrators have a clear path to expand electrified options for training and short-hop missions.[3]Safran Electrical & Power, “Safran Obtains EASA Certification of the First Electric Motor for New Air Mobility,” Safran, safran-group.com Cross-border certification structures help OEMs deploy platforms more broadly, while market readiness varies by airport infrastructure, charging capacity, and training doctrine. Facility expansions and forward order coverage at leading manufacturers indicate a sustained book of business that extends into the forecast window.

Asia-Pacific, South America, and the Middle East and Africa collectively account for the balance, with certifications and partnerships opening new channels for electrified trainers and modern LSAs. The first national safety certificate for a fully electric light trainer in South Korea highlights entry points for low-noise aircraft in urban or noise-sensitive airspaces. Manufacturers and training providers in South Asia have advanced direct-factory representation and launched new academies to accelerate fleet support and spare-parts responsiveness. Regional growth trajectories are likely to track national regulatory alignment, airport readiness, and training demand, with incremental adoption of electric trainers where infrastructure and curricula support charging throughout the day. Over the forecast period, the light-sport aircraft market benefits from cascading adoption as certification reciprocity and OEM support networks deepen in newer geographies.

Competitive Landscape

The light-sport aircraft market remains moderately concentrated, with a few OEMs dominating volumes and several niche participants focusing on kits and region-specific roles. Training-focused OEMs prioritize glass-cockpit standardization, modern composites, and support networks, while premium-performance manufacturers emphasize safety features and mission flexibility. Amphibious platforms continue to cater to a premium niche with spin-resistant characteristics and expanded mission profiles. Strategic developments include capacity building, certification milestones, and distribution expansion. Certified electric motors and semi-automated production lines are enabling electrified trainers and short-range craft. Factory expansions and forward-booked production slots aim to meet demand and stabilize lead times. Flight training organizations maintain multi-year procurement programs to ensure fleet readiness and nationwide coverage. Niche entrants innovate with high-wing designs and avionics upgrades for backcountry and STOL use cases.

Corporate strategies focus on production continuity and geographic resilience. Some OEMs have diversified manufacturing to reduce geopolitical risks and ensure supply consistency. Expansion of direct-factory representation in growth markets enhances operator support and shortens spare-parts cycles. The light-sport aircraft market reflects a dual pathway, with established players defending market share and innovators driving new opportunities in electric trainers, amphibious roles, and backcountry capabilities.

Light-Sport Aircraft Industry Leaders

Flight Design general aviation GmbH

Van's Aircraft, Inc.

PIPISTREL D.O.O.

ICON Aircraft, Inc.

Costruzioni Aeronautiche TECNAM S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: CubCrafters announced that its Carbon Cub UL has officially entered production. The Carbon Cub UL is available as a factory-built LSA and as a factory-builder-assisted Experimental Amateur-Built (EAB) aircraft. It features advanced carbon-fiber construction, modern technology, and notable performance capabilities.

- March 2026: Canavia Aviation Academy, located in the Canary Islands, received a new multiengine P2006T NG. This addition increases Canavia’s Tecnam fleet to nine aircraft, comprising six P2008JCs and three P2006Ts.

- February 2026: Tecnam announced a partnership with Blue Skies Aviation Solutions (Pvt) Ltd to establish a new Approved Training Organization (ATO) in Sri Lanka. To develop a pilot training capability, Blue Skies Aviation has chosen an all-Tecnam fleet, comprising three P-Mentors and one P2006T NG.

Global Light-Sport Aircraft Market Report Scope

A light-sport aircraft (LSA) is defined as an aircraft (other than a helicopter or powered-lift aircraft) with a maximum takeoff weight of under 1,320 pounds (~599 kgs). LSAs usually have one or two seats. The market study does not include gliders, gyroplanes, lighter-than-air aircraft, powered parachutes, or weight-shift-control aircraft.

The light-sport aircraft market is segmented by type, propulsion type, application, and geography. By type, the market is segmented into airplane and seaplane. By propulsion type, the market is classified into conventional ICE, hybrid‑electric, and electric. By application, the market is segmented into flight training and pilot schools, personal/recreational ownership, aerial work and utility operations, and rental/flying clubs. The report also covers the sizes and forecasts for the light-sport aircraft market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Airplane |

| Seaplane |

| Conventional ICE |

| Hybrid‑Electric |

| Electric |

| Flight Training and Pilot Schools |

| Personal/Recreational Ownership |

| Aerial Work and Utility Operations |

| Rental/Flying Clubs |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Type | Airplane | ||

| Seaplane | |||

| By Propulsion Type | Conventional ICE | ||

| Hybrid‑Electric | |||

| Electric | |||

| By Application | Flight Training and Pilot Schools | ||

| Personal/Recreational Ownership | |||

| Aerial Work and Utility Operations | |||

| Rental/Flying Clubs | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the Light-Sport Aircraft Market growth outlook to 2031?

The light-sport aircraft market is projected to grow from USD 1.68 billion in 2026 to USD 2.32 billion by 2031 at a 6.71% CAGR, supported by MOSAIC-driven eligibility expansion, training demand, and selective electrification.

How does MOSAIC change what aircraft qualify for sport-pilot privileges?

MOSAIC replaces weight ceilings with performance-based stall-speed criteria, authorizes more configurations including four seats and certain equipment, and enables night operations with proper endorsements and medical status under the updated framework.

Which segments are expanding the fastest in the Light-Sport Aircraft Market?

Seaplanes and electric propulsion are set to outpace the category average, with projected CAGRs of 7.78% and 14.43% respectively through 2031, while internal combustion engines retain the largest installed base due to training throughput and range.

Why does flight training remain the largest application in this market?

Training fleets benefit from standardized glass cockpits, strong OEM support, and clear rating pathways, while large schools continue to scale fleets and maintenance networks to meet steady student pipelines.

Where is regional growth strongest for the Light-Sport Aircraft Market?

Europe shows the fastest projected regional CAGR to 2031, aided by propulsion certifications and OEM facility expansions, while North America retains the largest base and the most immediate regulatory uplift from MOSAIC.

What are the main operational restraints for operators adopting electric LSAs?

Endurance and charging cycles currently constrain training throughput to shorter sorties and structured schedules at fields with adequate infrastructure, which keeps electric trainers complementary to ICE fleets for high-hour programs.

Page last updated on: