Pet Food Palatants Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

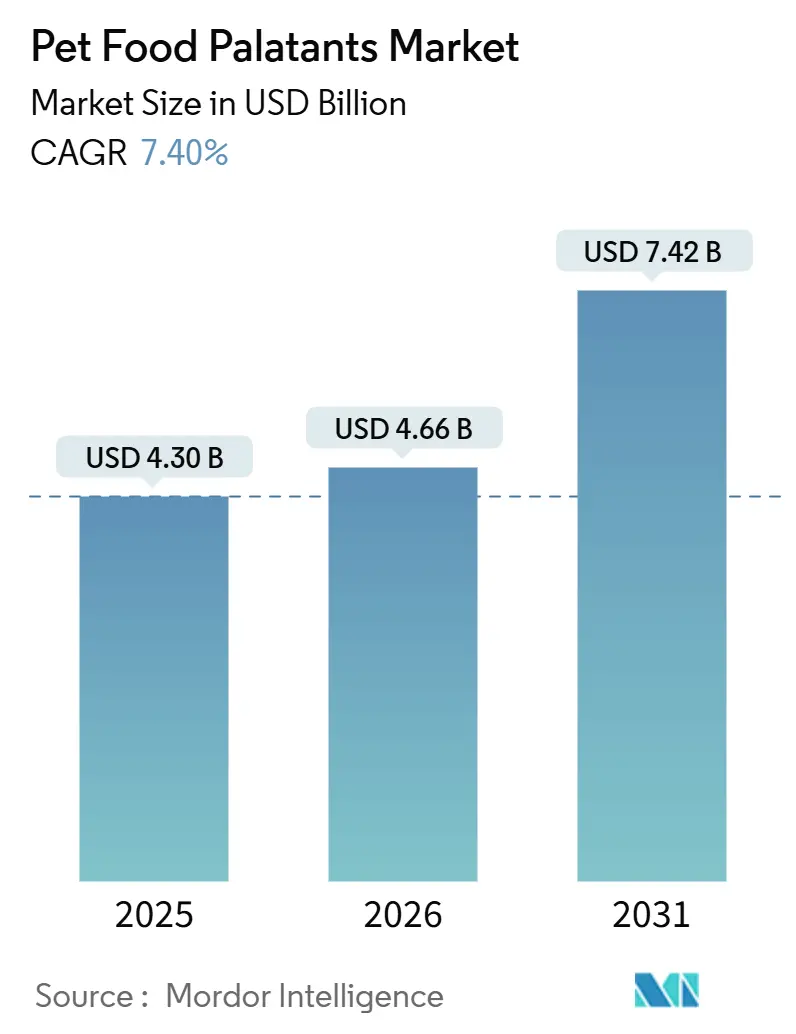

| Market Size (2026) | USD 4.66 Billion |

| Market Size (2031) | USD 7.42 Billion |

| Growth Rate (2026 - 2031) | 7.40% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pet Food Palatants Market Analysis by Mordor Intelligence

The pet food palatants market size is projected to expand from USD 4.30 billion in 2025 and USD 4.66 billion in 2026 to USD 7.42 billion by 2031, registering a 7.4% CAGR between 2026 and 2031. Soaring pet humanization, premium positioning of treats, and rapid innovation in flavor chemistry are reshaping supplier strategies. Dry powder formats still dominate day-to-day kibble production, yet liquid systems are gaining ground as wet and fresh pet foods scale. Sustainability pressures are accelerating the shift toward plant and fermentation-derived profiles, while AI-guided formulation tools cut prototyping time and cost, letting smaller firms compete on novelty. Intensifying clean-label scrutiny in North America and the European Union is prompting investments in traceable, enzymatically produced flavor precursors. Together, these forces are widening the addressable base for the pet food palatants market across both mature and high-growth economies.

Key Report Takeaways

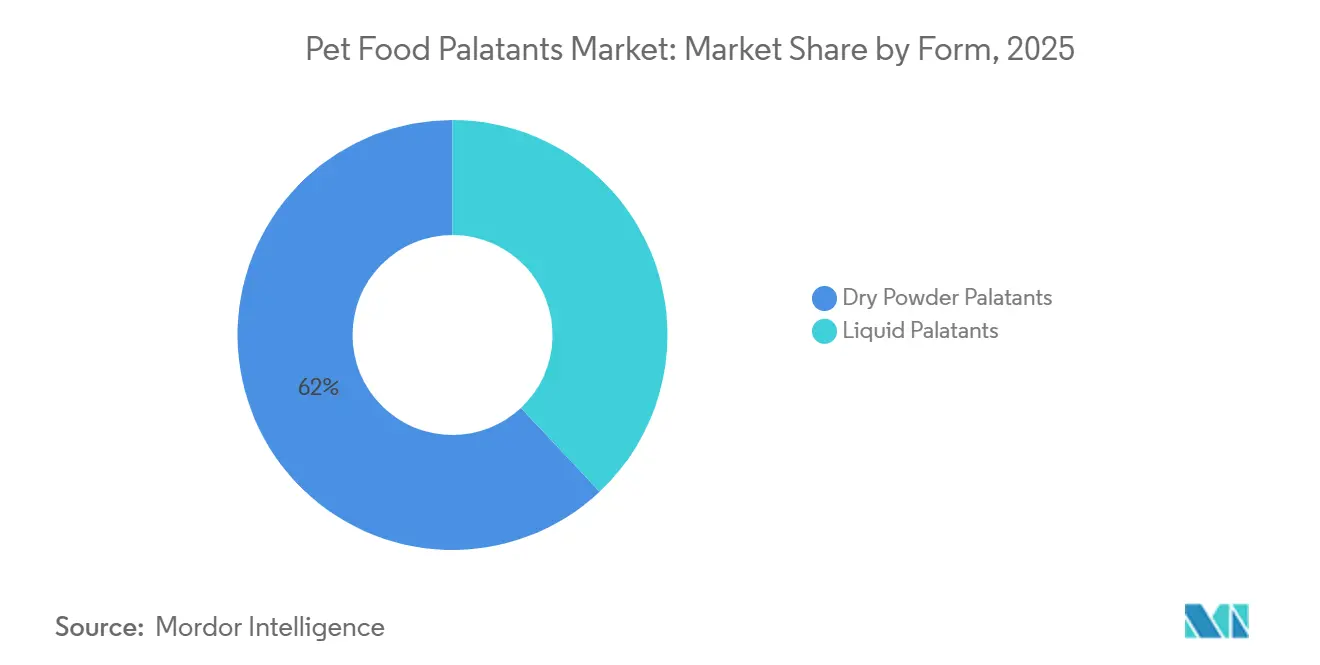

- By form, dry powder palatants held the largest segment, 62% of the pet food palatants market share in 2025, and liquid palatants are the fastest-growing, projected to log a 9.9% CAGR through 2026-2031.

- By source, animal-based palatants are the largest segment, accounting for 58% of the pet food palatants market share in 2025, while plant-based alternatives are the fastest-growing, set to advance at a 10.8% CAGR through 2026-2031.

- By pet type, dogs are the largest segment, 47% of the pet food market size in 2025, and cats are the fastest-growing, forecast to climb at a 9.5% CAGR through 2026-2031.

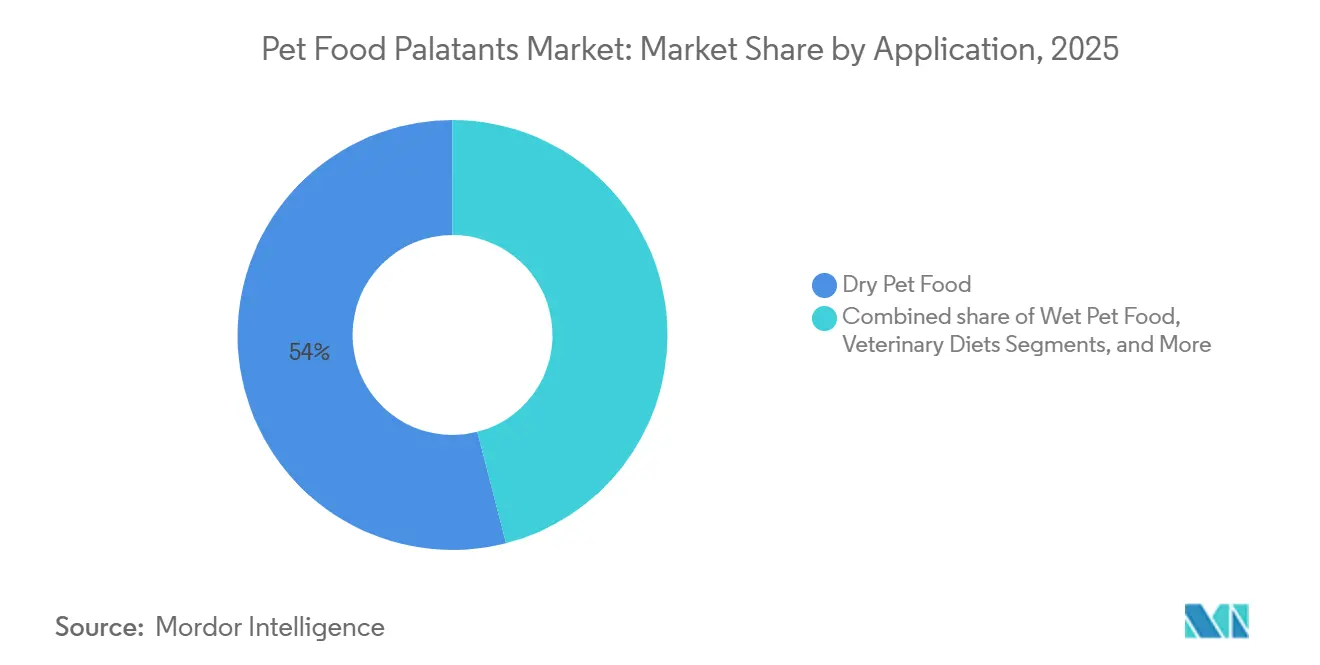

- By application, dry food held the largest segment, 54% of the pet food palatants market size in 2025, and treats and snacks are the fastest-growing, with 10.4% CAGR through 2026-2031.

- By flavor technology, hydrolyzed held the largest segment, accounting for 39% of the pet food palatants market size in 2025, and encapsulated volatile systems are the fastest-growing, posting a 12.3% CAGR through 2026-2031.

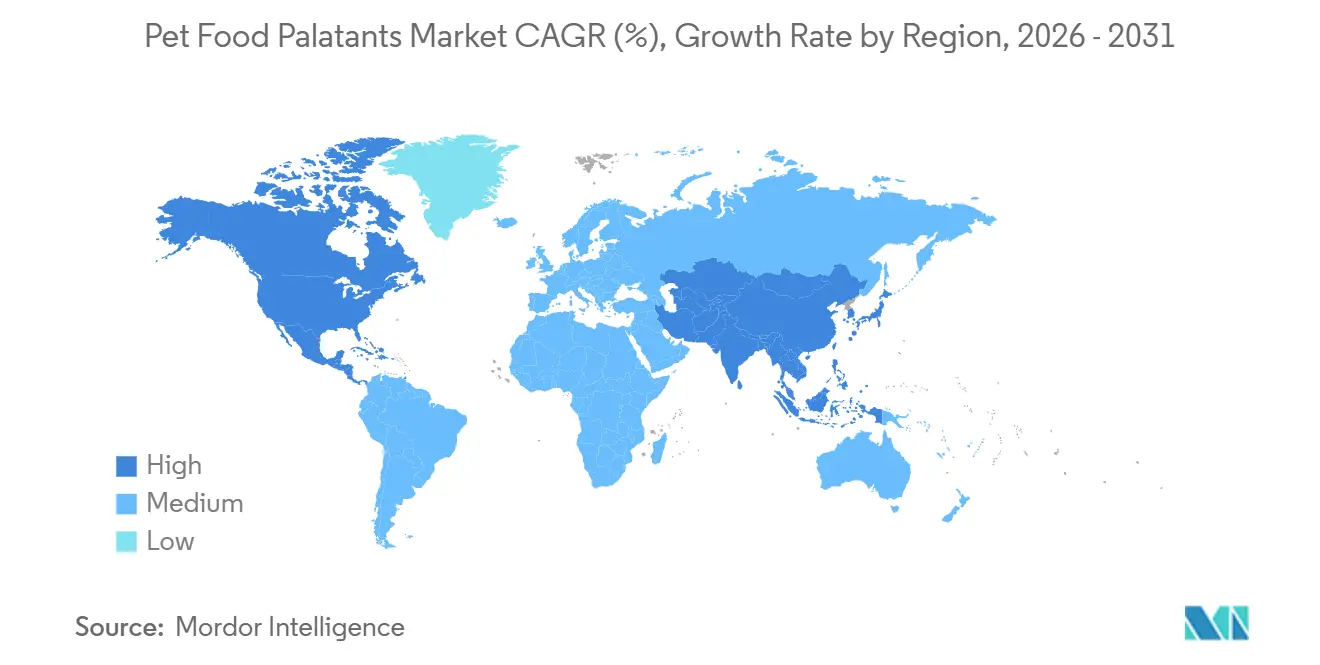

- By geography, North America was the largest region, with 37% of the pet food palate market size in 2025, and Asia-Pacific was the fastest-growing region, with 6.9% CAGR through 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Pet Food Palatants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing focus on premiumization of pet diets | +1.8% | North America and Europe core, and Asia-Pacific accelerating | Medium term (2-4 years) |

| Growing trend of pet humanization fuels market expansion | +1.6% | Global, and strongest in urban centers | Short term (≤ 2 years) |

| Expansion in the wet and fresh pet food market | +1.4% | North America and Asia-Pacific lead | Medium term (2-4 years) |

| Adoption of AI-driven flavor optimization | +0.9% | North America and Europe early adoption | Long term (≥ 4 years) |

| Fermentation-derived umami boosters | +0.7% | Europe and Asia-Pacific core | Long term (≥ 4 years) |

| Postbiotic palatants for gut-health compliance | +0.6% | Global, with regulatory tailwinds | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Focus on Premiumization of Pet Diets

Pet owners now judge value through sensory performance and ingredient narratives, pushing formulators to mask botanical off-notes while amplifying meaty aromas. The United States pet industry is spending a total of USD 158 billion in 2025, a 3.7% increase from 2024, according to APPA data[1]Source: American Feed Industry Association, “Pet Food Launch Trends,” afia.org. This shift has increased the demand for masking undesirable botanical or plant-based off-notes while enhancing savory, meat-like aromas that cater to pets' natural preferences. As premium and specialized diets continue to grow in popularity, palatants are essential for maintaining consistent taste, aroma, and overall feeding experience, especially in formulations that include alternative proteins or functional ingredients.

Growing Trend of Pet Humanization Fuels Market Expansion

The growing trend of pet humanization is reshaping the pet food industry, as pet owners increasingly view their pets as family members and emphasize their health, nutrition, and overall well-being. For instance, according to Canadian statistics, among the 12.2 million households that owned dogs and/or cats, with a total cat and dog population of 17.2 million in 2024, 50.9% owned cats, compared to 49.1% who owned dogs. This change is fueling demand for high-quality, safe, nutritionally balanced pet food products that meet standards similar to those for human food. Consumers are paying closer attention to ingredient labels, sourcing transparency, and product claims, prompting manufacturers to create formulations that align with clean-label, functional, and premium product positioning. Exotic proteins such as venison and kangaroo require bespoke palatants to overcome neophobia.

Expansion in the Wet and Fresh Pet Food Market

The rising demand for wet and fresh pet food is influencing the pet food palatants market, as pet owners prioritize products with higher moisture content, better digestibility, and a more natural feeding experience. Wet and fresh formats are often viewed as closer to human-grade meals, aligning with trends in premiumization and pet humanization. These products depend significantly on palatants to enhance aroma, texture, and taste, ensuring a strong feeding response, particularly among selective eaters such as cats. Consequently, manufacturers are focusing on advanced palatant systems capable of withstanding processing conditions while delivering rich, meat-like sensory profiles, thereby driving increased adoption in this rapidly growing segment.

Adoption of AI-Driven Flavor Optimization

The use of artificial intelligence (AI) in pet food formulation enables more precise, data-driven flavor optimization. By analyzing pet preferences, consumption patterns, and sensory response data, AI tools assist manufacturers in designing targeted palatant systems that enhance acceptance and feeding consistency. This approach facilitates faster product development, improved formulation accuracy, and the customization of flavors for specific pet segments based on factors such as breed, age, or dietary requirements. Additionally, AI-guided optimization supports the incorporation of alternative ingredients by identifying effective methods to mask off-notes and enhance desirable flavors, ultimately improving product performance and competitiveness in the evolving pet food market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in animal-by-product costs | -0.8% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Strict clean-label regulations impact the market | -0.6% | Europe and North America core | Medium term (2-4 years) |

| Limited insect-protein supply chain maturity | -0.4% | Global, and most acute in Western markets | Long term (≥ 4 years) |

| Palatant performance drift in High-Pressure Processing (HPP) lines | -0.3% | North America and Europe are fresh segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strict Clean-Label Regulations Impact the Market

The European Union's Farm-to-Fork policy enforces full traceability, obligating suppliers to record the origin of every amino acid[2]Source: European Commission, “Farm-to-Fork Strategy Ingredient Traceability Requirements,” Ec.europa.eu. Symrise responded with an enzymatically derived line that sidesteps artificial compounds but requires higher inclusion rates, eroding margins. Stringent clean-label regulations, particularly under the European Union’s Farm-to-Fork strategy, are significantly influencing the pet food palatants market by requiring full ingredient traceability and transparency. Suppliers must now document the origin and processing of all components, including individual amino acids, which has increased compliance complexity and operational costs.

Limited Insect-Protein Supply Chain Maturity

The underdeveloped supply chain for insect protein is a constraint on the pet food palatants market, despite increasing interest in alternative and sustainable protein sources. Insect-based ingredients face challenges such as scalability issues, inconsistent supply, and high production costs, which limit their adoption in mainstream pet food formulations. This underdevelopment also impacts the production of insect-derived palatants, as variability in raw material quality affects flavor consistency and product performance. Furthermore, regulatory uncertainties and limited processing infrastructure in key regions further impede market penetration. While insect protein holds long-term potential, current supply chain limitations restrict its contribution to palatant innovation and large-scale commercialization.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Powder Dominates, Liquid Gains in Wet Formats

Dry powder palatants held the largest segment, with 62% of the pet food palatants market share in 2025, and remain the default for kibble because they ship efficiently and disperse evenly during extrusion. This dominance is attributed to their stability during processing, ease of handling, extended shelf life, and cost-effectiveness. Dry powder palatants are particularly well-suited for large-scale dry pet food production, such as extruded kibbles, where consistent taste and aroma are essential. Their extensive use in both standard and premium kibble formulations further solidifies their leading market position.

Liquid palatants are the fastest-growing, projected to log a 9.9% CAGR through 2026-2031, as wet and chilled meals scale globally. This growth is driven by their superior coating efficiency, ability to enhance aroma and taste, and compatibility with wet and fresh pet food formats. Additionally, liquid palatants enable precise flavoring in premium and specialty diets, including those incorporating alternative proteins or functional ingredients, which contributes to their increasing adoption within the pet food industry.

By Source: Animal-Based Leads, Plant-Based Surges

Animal-based palatants are the largest segment, accounting for 58% of the pet food palatants market share in 2025. This dominance is attributed to the strong flavor appeal of meat-based ingredients, which align with pets' natural dietary preferences, particularly dogs' and cats'. Additionally, animal-based palatants offer highly digestible amino acids and proteins, enhancing the nutritional value of pet food. These characteristics make them the preferred choice for mainstream dry and wet pet food formulations, especially in developed markets where pet owners prioritize palatability and product acceptance.

Plant-based alternatives are the fastest-growing, with a 10.8% CAGR through 2026-2031. This growth is driven by increasing demand for sustainable, alternative, and hypoallergenic ingredients, as well as consumer interest in environmentally friendly products. Manufacturers are utilizing plant proteins, yeast extracts, and botanical flavors to mask off-notes while enhancing savory and umami taste profiles. The growth of plant-based palatants is particularly significant in premium, clean-label, and functional pet food segments, where pet owners seek natural ingredient claims without compromising taste. Furthermore, advancements in processing technologies are improving the flavor performance of plant-based palatants, positioning them as a viable alternative to traditional animal-derived products.

By Pet Type: Dogs Lead, Cats Accelerate

Dogs are the largest segment, accounting for 47% of the pet food market size in 2025, a function of higher caloric intake and broader product variety. This dominance is attributed to the substantial global dog population, higher consumption of commercial pet food, and owners' willingness to invest in premium nutrition and palatability enhancements. Dogs generally require larger serving sizes and more diverse diets, which increases the demand for palatants that enhance taste, aroma, and the overall feeding experience. Additionally, dog-specific products lead in both dry kibble and wet food categories, making them a significant contributor to market volume.

Cats are the fastest growing, forecast to climb at a 9.5% CAGR through 2026-2031, driven by heightened understanding of feline olfactory preferences and increasing multi-cat ownership in Asia-Pacific cities. This growth is driven by rising urban cat ownership, increased adoption of indoor pets, and demand for highly palatable, specialized diets. Cats are known for their selective eating habits, making palatants essential for ensuring consistent consumption of both wet and dry food. The premiumization of cat diets, including functional and nutritionally enriched formulations, further drives the need for flavor optimization to maintain acceptance. Additionally, the humanization of pets trend is encouraging cat owners to prioritize high-quality, taste-focused products, thereby increasing the demand for innovative palatants in this segment.

By Application: Dry Food Anchors, Treats Surge

Dry food held the largest segment, holding 54% of the pet food palatants market size in 2025, owing to manufacturing efficiency and price accessibility. Its dominance is supported by widespread adoption among pet owners, convenience, longer shelf life, and lower cost compared to wet food. Dry kibble is often the primary diet for dogs and cats, and palatants play a critical role in enhancing flavor, aroma, and texture to ensure pets consistently consume their meals. Additionally, dry food formulations benefit from high-volume production efficiencies, making this segment a stable and consistent revenue driver for palatant manufacturers.

Treats and snacks are the fastest-growing category, with a 10.4% CAGR through 2026-2031. Growth is fueled by the rising trend of pet humanization, where owners increasingly treat pets as family members and invest in premium, flavorful, and functional snack products. Palatants are critical in this category, as treats and snacks must deliver strong flavor and aroma in smaller portions to encourage repeat consumption. The segment’s growth is also supported by innovations in functional treats, such as dental chews, digestive health snacks, and protein-rich rewards, which require palatants to mask off-notes and maintain palatability.

By Flavor Technology: Hydrolyzed Protein Dominates, Encapsulation Emerges

Hydrolyzed held the largest segment, accounting for 39% of the pet food palatants market size in 2025, leveraging enzymes to unlock small peptides and free amino acids that deliver deep umami character. Hydrolyzed proteins are valued for their ability to enhance flavor intensity, improve digestibility, and provide amino acids that align with pets’ natural taste preferences. These proteins are widely utilized in dry, wet, and specialty pet food formulations, particularly in premium and functional diets, due to their ability to ensure consistent palatability. Furthermore, hydrolyzed proteins effectively mask undesirable flavors in formulations containing plant-based or alternative protein sources, making them a versatile option for manufacturers.

Yeast Extracts are the fastest-growing, posting a 12.3% CAGR through 2026-2031. This growth is attributed to their natural umami-rich flavor profile, which enhances palatability while addressing consumer preferences for clean-label and sustainable ingredients. Yeast extracts are increasingly incorporated into premium wet foods, functional snacks, and treat products, where flavor consistency and intensity are essential.

Geography Analysis

North America was the largest region, with 37% of the market share in the pet food palatants market in 2025. This dominance is attributed to high pet ownership rates, robust consumer spending on premium pet food, and a well-established manufacturing and distribution infrastructure. According to the Veterinary Medical Association, in the United States, 42.6% of dog owners and 32.6% of cat owners were reported in 2025[3]Source: American Veterinary Medical Association, “U.S. Pet Ownership Statistics 2025,” AVMA.org. The region also benefits from advanced formulation technologies and a mature supply chain, enabling consistent delivery of high-quality palatants across dry, wet, and specialty pet food products. Furthermore, pet humanization trends in North America drive investments in premium, functional, and flavor-optimized pet food products, reinforcing the region's market leadership.

Asia-Pacific was the fastest-growing region, with a 6.9% CAGR through 2026-2031. This growth is driven by rising disposable incomes, increasing pet adoption, and greater awareness of pet nutrition and wellness. Rapid urbanization and lifestyle changes in countries such as China, India, and Southeast Asia are boosting demand for premium, clean-label, and functional pet foods, which rely significantly on palatants to enhance taste and aroma. Additionally, the expansion of retail channels and e-commerce platforms in the region is improving access to high-quality pet food products, further accelerating market growth.

Europe will progress amid market maturity, yet traceability rules under the Farm-to-Fork strategy buttress value growth. Germany and the United Kingdom top spending, while Italy and Spain show steady adoption of yeast-based flavor amplifiers in grain-free diets. In Eastern Europe, cost-sensitive consumers still purchase legacy powders, but premium segments in Poland and the Czech Republic are shifting toward encapsulated volatiles for fresh offerings.

Competitive Landscape

The Pet Food Palatants Market is moderately concentrated, with the top five players, including Kemin Industries, Inc., Symrise AG, Archer Daniels Midland Company, Darling Ingredients Inc., and AFB International, Inc., holding a significant market share in 2025. This creates a competitive environment that balances the advantages of scale with opportunities for innovation by smaller specialized companies.

Strategic trends indicate a growing focus on technological differentiation and application-specific solutions, moving away from commodity-based competition. Companies are making substantial investments in AI-driven flavor optimization systems and advanced palatability testing protocols that replicate human food sensory evaluation methods. Market competition is intensifying as established players face challenges from diversified chemical companies and ingredient suppliers pursuing higher-margin palatant opportunities through vertical integration strategies.

Emerging protein sources, such as insect-based and fermentation-derived palatants, offer opportunities to address sustainability concerns while maintaining palatability standards. Smaller companies are disrupting traditional supplier relationships by focusing on niche applications, including veterinary diets and exotic pet foods, where customization capabilities are prioritized over scale advantages in supplier selection.

Pet Food Palatants Industry Leaders

Kemin Industries, Inc.

Symrise AG

Archer Daniels Midland Company

Darling Ingredients Inc.

AFB International, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Kemin Industries published comprehensive research on insect protein meal palatability, demonstrating that black soldier fly larvae can achieve 85-90% palatability scores compared to traditional animal-based formulations.

- May 2024: Kemin Industries introduced a sustainability strategies initiative focusing on alternative protein sourcing and rendered product utilization to reduce the environmental impact of palatant production.

- September 2023: Symrise opened a pet food palatants facility in Chapéco, Brazil. The facility produces palatants for cat and dog food and represents the company's largest pet food operation globally. The inauguration included local officials, business leaders, and project team members. Pet owners prioritize product quality and safety, seeking both palatability and nutritional value.

Global Pet Food Palatants Market Report Scope

Pet food palatants are additives or ingredients designed to improve the flavor, aroma, and overall palatability of pet food products, including dry kibble, wet food, treats, and snacks. The pet food palatants market report is segmented by form (dry powder palatants and liquid palatants), by source (animal-based, plant-based, insect-based, and synthetic), by pet type (dogs, cats, and other pet types), by application (dry pet food, wet pet food, treats and snacks, and veterinary diets), by flavor technology (hydrolyzed protein, yeast extracts, maillard reaction flavors, and other flavor technologies), and by geography (North America, South America, Europe, Asia-Pacific, Middle-East, and Africa). The market forecasts are provided in terms of value (USD).

| Dry Powder Palatants |

| Liquid Palatants |

| Animal-based |

| Plant-based |

| Insect-based |

| Synthetic |

| Dogs |

| Cats |

| Other Pet Types |

| Dry Pet Food |

| Wet Pet Food |

| Treats and Snacks |

| Veterinary Diets |

| Hydrolyzed Protein |

| Yeast Extracts |

| Maillard Reaction Flavors |

| Others |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Mexico | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Form | Dry Powder Palatants | |

| Liquid Palatants | ||

| By Source | Animal-based | |

| Plant-based | ||

| Insect-based | ||

| Synthetic | ||

| By Pet Type | Dogs | |

| Cats | ||

| Other Pet Types | ||

| By Application | Dry Pet Food | |

| Wet Pet Food | ||

| Treats and Snacks | ||

| Veterinary Diets | ||

| By Flavor Technology | Hydrolyzed Protein | |

| Yeast Extracts | ||

| Maillard Reaction Flavors | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Mexico | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will the pet food palatants market be by 2031?

It is projected to reach USD 7.42 billion, up from USD 4.66 billion in 2026, at a 7.4% CAGR through 2026-2031.

Which palatant form is growing fastest?

Liquid palatants are projected to expand at a 9.9% CAGR through 2031 as wet and fresh foods gain share.

What is the main regulatory challenge for suppliers?

Stricter clean-label rules in North America and Europe require full traceability and the removal of synthetic flavor analogs, raising costs and complexity.

How concentrated is supplier power in this space?

The five largest companies control significant of global revenue, indicating moderate concentration but still allowing room for niche and technology-driven entrants.

Page last updated on: