South Africa Pet Nutraceuticals Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

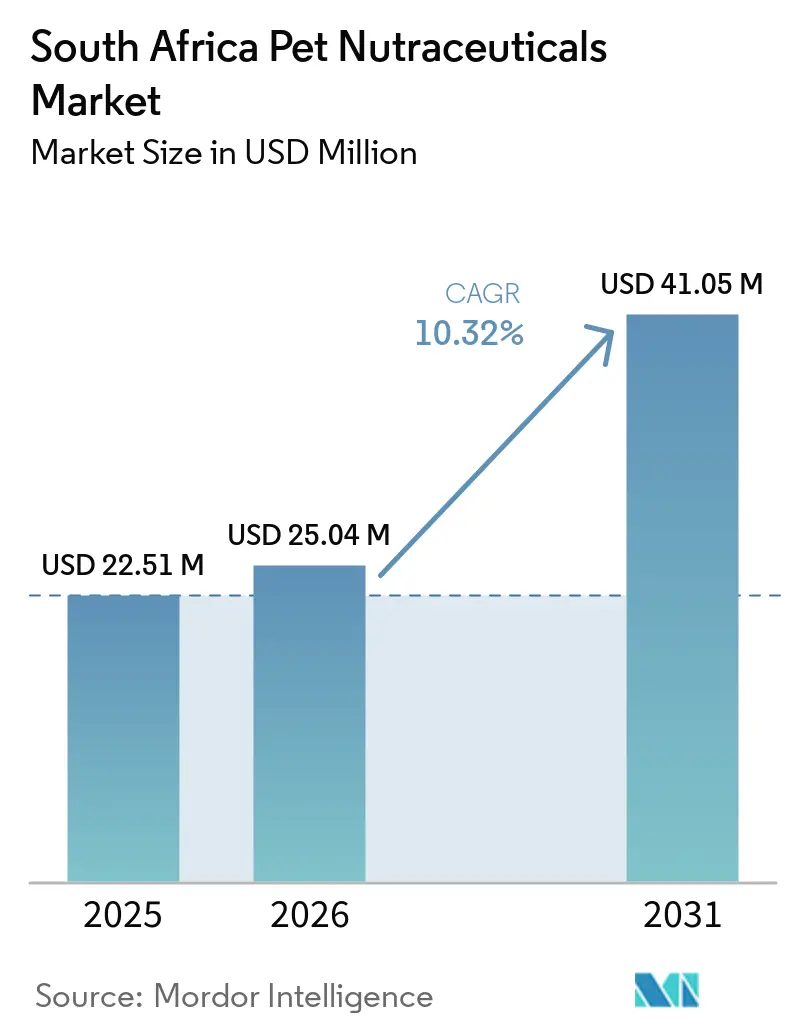

| Base Year Market Size (2025) | USD 22.51 Million |

| Market Size (2026) | USD 25.04 Million |

| Market Size (2031) | USD 41.05 Million |

| Growth Rate (2026 - 2031) | 10.32% CAGR |

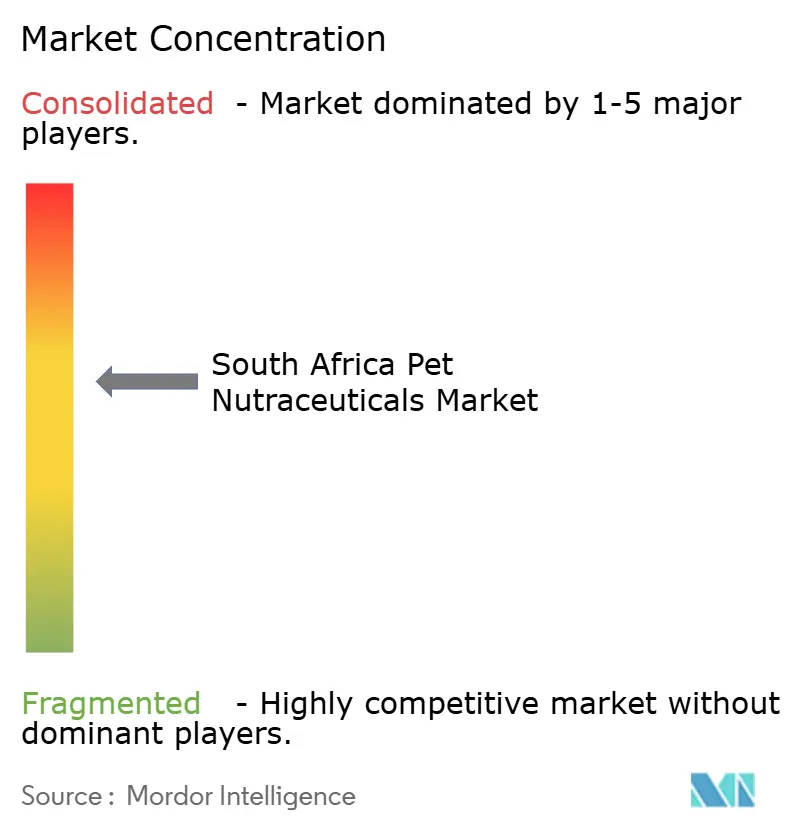

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Pet Nutraceuticals Market Analysis by Mordor Intelligence

The South Africa pet nutraceuticals market was valued at USD 22.51 million in 2025 and is projected to grow from USD 25.04 million in 2026 to USD 41.05 million by 2031, registering a CAGR of 10.32% during the forecast period from 2026 to 2031. The market is being driven by a shift toward preventive pet health, with pet owners increasingly focusing on daily wellness support rather than addressing health issues only after they arise. The emphasis on veterinary-endorsed nutrition is enhancing product quality, as consumers prioritize credibility, ingredient efficacy, and measurable health benefits. Increased product visibility in specialist retail outlets and digital platforms is facilitating access to condition-specific and premium formulations, further supporting market growth. Local production capabilities provide a supply chain advantage, while acquisitions and portfolio expansions are intensifying competition among branded pet wellness products. However, income disparities and regulatory requirements necessitate a dual-market strategy, offering premium products for affluent urban consumers and cost-effective options for price-sensitive households.

Key Report Takeaways

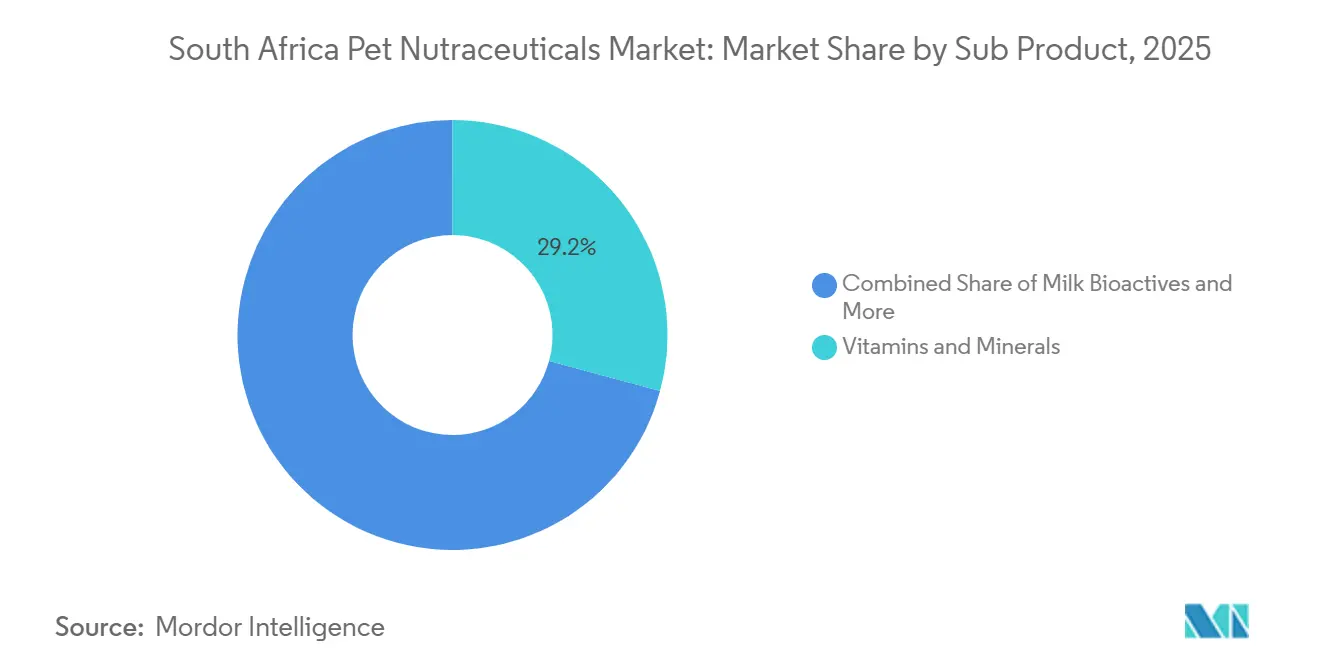

- By sub product, the South Africa pet nutraceuticals market share for vitamins and minerals accounted for the largest 29.2% in 2025, and vitamins and minerals are projected to expand at the fastest 10.7% CAGR from 2026 to 2031.

- By pets, dogs held the largest 82.3% share in 2025, while the South Africa pet nutraceuticals market size for cats is forecast to grow at the fastest CAGR of 13.6% from 2026 to 2031.

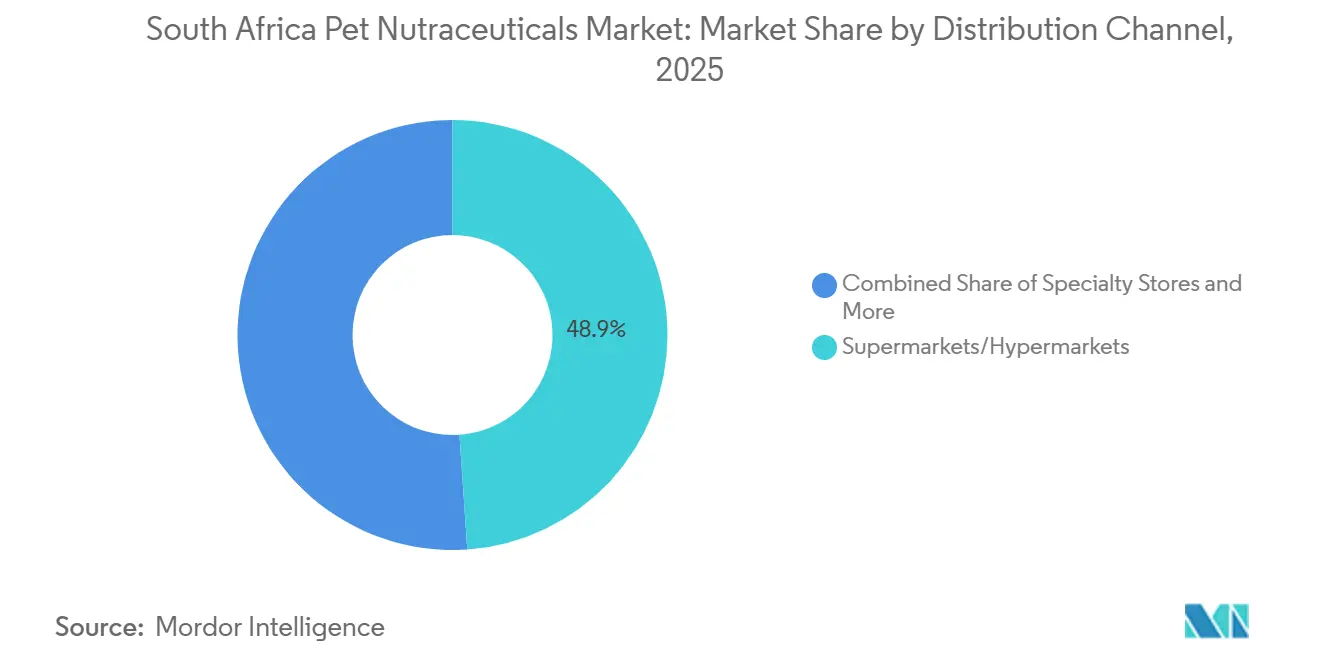

- By distribution channel, supermarkets and hypermarkets captured the largest 48.9% share in 2025, while specialty stores are projected to grow at the fastest CAGR of 11.3% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Africa Pet Nutraceuticals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising pet humanization and preventive wellness spending | +2.5% | National, with early gains in Gauteng and Western Cape | Short term (≤ 2 years) |

| Veterinary-backed condition-specific nutrition adoption | +1.8% | National, with heavier urban concentration | Medium term (2-4 years) |

| Expansion of specialist pet retail and e-commerce availability | +1.6% | Gauteng, Western Cape, and eThekwini metro | Short term (≤ 2 years) |

| Premiumization through joint, digestive, and immune health claims | +1.4% | National, strongest in middle-income and upper-income households | Medium term (2-4 years) |

| Local manufacturing scale-up for branded, quality-controlled supplements | +1.2% | Eastern Cape, North West, and Gauteng | Long term (≥ 4 years) |

| Rising demand for natural, probiotic, and functional ingredient formulations | +1.3% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Pet Humanization and Preventive Wellness Spending

Pet wellness spending in South Africa is increasingly focused on preventive care, driving growth in the pet nutraceuticals market. Consumers are demonstrating a growing preference for products that address multiple health concerns and enhance the long-term quality of life for companion animals. In April 2026, Hill's Pet Nutrition launched Prescription Diet Metabolic + j/d for cats in the global market, including African countries such as South Africa[1]Source: Hill's Pet Nutrition, “Hill’s Pet Nutrition Introduces Innovation to Support Feline Mobility and Weight Management,” hillspet.com. This product combines weight management and mobility support in a single formulation. The launch underscores the rising demand for comprehensive wellness solutions over single-condition products, encouraging repeat purchases and the adoption of premium supplements among pet owners.

Veterinary-Backed Condition-Specific Nutrition Adoption

Veterinary guidance is playing a significant role in influencing pet supplement purchasing decisions, driving growth in the South Africa pet nutraceuticals market. Pet owners are increasingly trusting products developed with clinical input and tailored to address specific health concerns rather than focusing solely on general wellness. In line with this trend, in February 2025, Elanco Animal Health Incorporated introduced Pet Protect in the global market, including African countries such as South Africa, a range of veterinarian-formulated supplements for dogs and cats. These supplements target areas such as joint health, digestive function, immune support, omega-3 supplementation, and multivitamin requirements[2]Source: Elanco Animal Health Incorporated, “Elanco Launches Pet Protect from the Makers of Advantage: Veterinarian-Formulated Supplements for Complete Pet Wellness,” investor.elanco.com. This launch underscores the rising demand for science-based, condition-specific nutrition and highlights the importance of professional credibility in the adoption of pet supplements.

Expansion of Specialist Pet Retail and E-Commerce Availability

Improved retail access is driving growth in the South Africa pet nutraceuticals market by increasing the visibility and availability of specialized pet health products to consumers. Expanded distribution channels allow pet owners to discover and repurchase supplements through both physical stores and online platforms, enhancing market penetration. For instance, in June 2025, Amazon South Africa broadened its local offerings to include pet food, pet supplies, and health supplements, recognizing these as some of the most requested product categories by customers[3]Source: Amazon South Africa, “Amazon South Africa Expands Selection with Grocery, Pet Food, and Vitamins and Supplements Categories,” amazon.co.za. Increased availability through major retail platforms boosts exposure to wellness-oriented pet products and encourages adoption beyond traditional specialist pet stores.

Premiumization Through Joint, Digestive, and Immune Health Claims

Premiumization in the South Africa pet nutraceuticals market is increasingly associated with products and services that offer measurable health benefits and support proactive wellness management. Pet owners are demonstrating a growing willingness to invest in advanced solutions that monitor health conditions and enhance long-term outcomes. Aligning with this trend, on May 6, 2025, Mars, Incorporated introduced a portfolio of artificial intelligence-powered pet health tools as part of its USD 1 billion investment in Pet Nutrition digital innovation in the global market, including African countries such as South Africa. This initiative enhances consumer engagement with preventive care and drives demand for premium health-focused products addressing specific wellness needs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High price sensitivity in mass-market pet nutrition purchases | -1.8% | National, peri-urban and rural markets | Short term (≤ 2 years) |

| Quality and regulatory compliance friction for novel ingredient products | -1.2% | National | Medium term (2-4 years) |

| Import dependence for select active ingredients and finished products | -0.9% | National | Long term (≥ 4 years) |

| Consumer skepticism around efficacy claims in low-trust supplement categories | -0.8% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Price Sensitivity in Mass-Market Pet Nutrition Purchases

Price sensitivity is a notable challenge in the South Africa pet nutraceuticals market, as premium supplements often compete with essential household expenses. Many consumers prioritize basic pet food purchases over specialized wellness products, particularly during periods of financial strain. According to Statistics South Africa, annual consumer price inflation stood at 2.8% in May 2025, highlighting ongoing cost-of-living pressures on households. In this context, higher-priced nutraceutical products may experience slower adoption among mainstream consumers, limiting market penetration beyond premium buyer segments. This affordability gap could constrain volume growth, even as demand for preventive pet health solutions continues to rise.

Quality and Regulatory Compliance Friction for Novel Ingredient Products

Regulatory and labeling requirements pose significant challenges for companies in the South Africa pet nutraceuticals market, particularly for those introducing novel ingredients or advanced functional claims. Compliance with regulations on ingredient disclosure, nutritional statements, and product communication often extends development timelines and increases administrative costs. In response to these challenges, the Pet Food Industry Association of South Africa (PFISA) released its “How to Read Pet Food Labels” guidance in January 2025. This guidance highlights the importance of accurate ingredient presentation, guaranteed analysis, and labeling transparency. These requirements are particularly burdensome for smaller suppliers, delaying product commercialization and hindering innovation within the market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub Product: Vitamins and Minerals Anchors Multifunctional Demand

The South Africa pet nutraceuticals market share for vitamins and minerals was the largest 29.2% in 2025. These products maintain their leading position due to their widespread consumer recognition and availability across mainstream retail channels. Their benefits in supporting immunity, bone health, skin condition, and overall wellness make them a common choice for pet owners. Additionally, their compatibility with various pet life stages enables manufacturers to offer tailored products for puppies, adult pets, and senior animals, ensuring consistent demand across diverse consumer segments.

Vitamins and minerals are forecast to grow at the fastest CAGR of 10.7% from 2026 to 2031. This growth is fueled by rising demand for multifunctional formulations that combine vitamins, minerals, digestive support, and immune health benefits in a single product. Increasing consumer awareness of preventive pet healthcare is driving the adoption of supplements aimed at long-term wellness management. While probiotics, omega-3 fatty acids, proteins, peptides, and milk bioactives are gaining traction as complementary categories, vitamins and minerals remain the primary choice due to their established reputation and clear health benefits.

By Pets: Dogs Lead by Volume, Cats Health Accelerating

Dogs accounted for the largest 82.3% share in 2025. This dominance is attributed to widespread dog ownership across both urban and rural households. Nutraceutical products addressing joint support, mobility, digestive health, and healthy aging are particularly aligned with the health needs of medium and large dog breeds. Additionally, recurring supplementation practices among dog owners drive higher product adoption. Manufacturers continue to focus on canine-specific product development, offering formulations tailored to breed size, activity level, and life stage, further solidifying the category's leading position in the pet nutraceutical market.

Cats are projected to grow at the fastest CAGR of 13.6% from 2026 to 2031. This growth is driven by increasing interest in companion animals that are well-suited to smaller living spaces and urban lifestyles. Cat owners often seek specialized nutritional solutions, creating demand for supplements targeting digestive health, taurine support, urinary wellness, and overall vitality. The category also benefits from strong online research and purchasing trends, as consumers frequently assess ingredient quality and functional claims before making purchases. This behavior supports the growth of premium and species-specific nutraceutical products for cats.

By Distribution Channel: Supermarkets Dominate, Specialist Retail Gains Ground

Supermarkets and hypermarkets held the largest 48.9% share in 2025. These outlets remain the primary purchase locations due to their convenience, allowing consumers to buy wellness supplements during routine grocery shopping. Entry-level products, such as vitamins and mineral formulations, benefit from prominent shelf placement and competitive pricing in these stores. Their widespread geographic presence enables brands to reach a diverse customer base across various income groups. Consequently, supermarkets and hypermarkets continue to play a key role in driving category awareness and volume-based sales.

Specialty stores are forecast to grow at the fastest CAGR of 11.3% from 2026 to 2031. This growth is attributed to increasing consumer demand for expert advice, a broader product range, and access to premium formulations. Specialty retailers are well-equipped to provide detailed information on products such as probiotics, omega-3 supplements, and condition-specific nutraceuticals. Their merchandising strategies facilitate comparison shopping and informed purchasing decisions. Additionally, online retail is contributing to the expansion of this channel through subscription-based models and repeat purchases, while veterinary clinics and other outlets continue to cater to niche customer needs.

Geography Analysis

Gauteng remains the leading provincial market due to its combination of strong consumer purchasing power, extensive veterinary infrastructure, and broad access to specialty pet retail channels. These factors drive higher adoption rates of preventive pet healthcare products and premium nutraceutical formulations. Urban centers within Gauteng provide a concentrated customer base actively seeking products for digestive health, mobility support, and age-related wellness. Additionally, the presence of established retail networks and veterinary professionals enhances awareness of scientifically formulated supplements, fostering favorable conditions for product launches and category growth.

The Western Cape continues to be a significant growth area, driven by strong consumer interest in health-focused pet care and premium nutrition. Consumers in this province often adopt wellness trends emphasizing functional ingredients and long-term preventive health support. Similarly, KwaZulu-Natal is gaining importance as pet ownership increases in urban areas, with households moving beyond basic pet food purchases. Growth in these provinces is supported by expanding retail accessibility and increased awareness of specialized nutritional products aimed at improving pet quality of life and overall well-being.

Secondary provinces present long-term expansion opportunities as awareness of nutraceuticals gradually extends beyond major metropolitan regions. Adoption rates remain lower in these areas due to less developed specialist retail coverage and limited veterinary access compared to Gauteng and the Western Cape. However, national pet ownership trends indicate potential for future market penetration. Recent statistics show in 2026 highlights that South African households own 7.4 million dogs and 2 million cats, highlighting a substantial companion animal base that could support broader supplement adoption as distribution networks improve.

Competitive Landscape

The competitive landscape is moderately consolidated, featuring a combination of multinational pet nutrition companies and established domestic manufacturers competing in both premium and value-oriented segments. Key players include Montego Pet Nutrition (Pty) Ltd (Monic Group), Mars, Incorporated, Nestlé S.A., Hill's Pet Nutrition, Inc. (Colgate-Palmolive Company), and Wellness Pet Company Inc. (Clearlake Capital Group, L.P.). International brands maintain strong positions in clinically focused and veterinarian-recommended products, while local companies leverage pricing strategies, regional distribution networks, and familiarity with domestic consumer preferences. Market participants are increasingly differentiating themselves through science-backed formulations, functional ingredients, and condition-specific nutritional solutions. Factors such as product credibility, ingredient transparency, and retail accessibility remain critical in influencing brand selection, as pet owners prioritize preventive wellness and long-term health management.

Competition is intensifying through portfolio diversification and innovation. Companies are expanding their offerings beyond basic nutritional supplements to include products targeting digestive health, mobility support, immune function, and healthy aging. Premiumization trends are driving investments in advanced formulations that incorporate probiotics, omega-3 fatty acids, peptides, and specialized bioactive ingredients. Retail strategies are also evolving, with brands strengthening their presence across specialty pet stores, veterinary clinics, e-commerce platforms, and mainstream grocery channels. This multi-channel approach enables manufacturers to cater to both value-conscious consumers and premium wellness-focused pet owners.

Strategic product innovation is further heightening competition as manufacturers expand premium wellness offerings tailored to specific pet health needs. For instance, in March 2025, Wellness Pet Company Inc. (Clearlake Capital Group, L.P.) launched new Wellness CORE+ Sensitive Skin and Stomach and Wellness Complete Health Sensitive Skin and Stomach recipes at Global Pet Expo 2025, which target the global market, including African countries such as South Africa. These products feature prebiotics, probiotics, postbiotics, and omega fatty acids to support digestive health and skin wellness. This launch underscores the industry's increasing focus on targeted nutritional solutions and highlights the competitive emphasis on scientifically formulated products designed to address specific health concerns while strengthening premium brand positioning.

South Africa Pet Nutraceuticals Industry Leaders

Montego Pet Nutrition (Pty) Ltd (Monic Group)

Mars, Incorporated

Nestlé S.A.

Hill's Pet Nutrition, Inc. (Colgate-Palmolive Company)

Wellness Pet Company Inc. (Clearlake Capital Group, L.P.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Hill's Pet Nutrition, Inc. (Colgate-Palmolive Company) launched Prescription Diet Metabolic + j/d Feline, enhancing its condition-specific nutrition portfolio with a product designed for weight management and mobility support in cats. This development highlights the increasing emphasis on science-based pet nutraceutical and wellness solutions within veterinary channels in South Africa.

- March 2026: RCL Foods Limited entered into a binding agreement to acquire Martin & Martin (Pty) Ltd for R695 million (USD 38 million). This acquisition aims to expand its pet care portfolio and enhance its position in South Africa's companion animal market, particularly in areas related to pet nutrition and wellness.

- March 2025: Wellness Pet Company Inc., a portfolio company of Clearlake Capital Group, L.P., introduced new Wellness CORE+ Sensitive Skin and Stomach recipes. These formulations include prebiotics, probiotics, postbiotics, and omega fatty acids, highlighting the growing focus on science-based digestive and skin health nutraceuticals shaping premium companion animal wellness products in South Africa.

South Africa Pet Nutraceuticals Market Report Scope

Pet nutraceuticals are functional nutritional products designed to enhance pet health beyond basic dietary needs. These include vitamins, probiotics, omega-3 fatty acids, and bioactive compounds that support immunity, digestion, joint health, skin condition, and overall well-being. The South Africa Pet Nutraceuticals Market Report is Segmented by Sub-Product (Milk Bioactives, Omega-3 Fatty Acids, Probiotics, Proteins and Peptides, Vitamins and Minerals, and More), by Pets (Cats, Dogs, and Other Pets), and by Distribution Channel (Convenience Stores, Online Channel, Specialty Stores, Supermarkets and Hypermarkets, and Other Channels). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

| Milk Bioactives |

| Omega-3 Fatty Acids |

| Probiotics |

| Proteins and Peptides |

| Vitamins and Minerals |

| Other Nutraceuticals |

| Cats |

| Dogs |

| Other Pets |

| Convenience Stores |

| Online Channel |

| Specialty Stores |

| Supermarkets/Hypermarkets |

| Other Channels |

| By Sub Product | Milk Bioactives |

| Omega-3 Fatty Acids | |

| Probiotics | |

| Proteins and Peptides | |

| Vitamins and Minerals | |

| Other Nutraceuticals | |

| By Pets | Cats |

| Dogs | |

| Other Pets | |

| By Distribution Channel | Convenience Stores |

| Online Channel | |

| Specialty Stores | |

| Supermarkets/Hypermarkets | |

| Other Channels |

Key Questions Answered in the Report

What is the outlook for pet nutraceutical sales in South Africa through 2031?

The South Africa pet nutraceuticals market is projected to reach USD 41.05 million by 2031.

Which sub product category leads demand in South Africa?

Vitamins and Minerals led with the largest 29.2% market share in 2025.

Why are cat-focused supplements growing faster than dog-focused products in South Africa?

Cats are forecast to grow at the fastest 13.6% CAGR from 2026 to 2031 because urban buyers are adopting species-specific and premium wellness formats more readily.

Which sales channels matter most for supplement brands in South Africa?

Supermarkets and Hypermarkets remain the largest channel with 48.9% market share in 2025.

Page last updated on: