Africa Pet Veterinary Diet Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

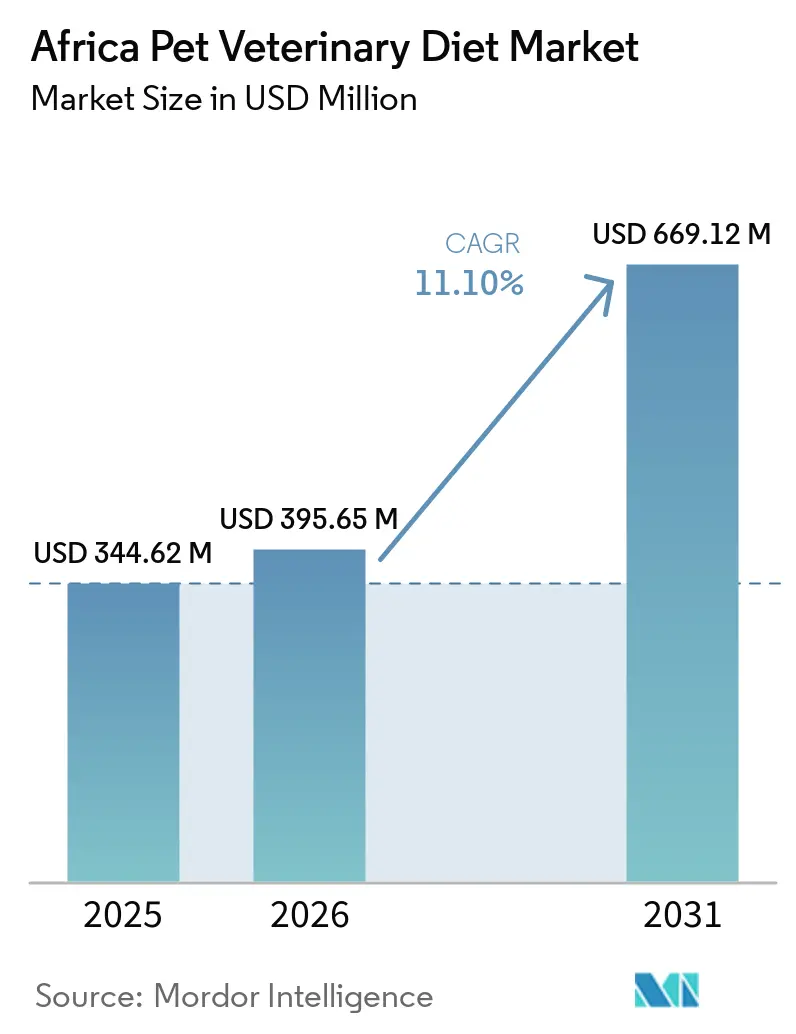

| Base Year Market Size (2025) | USD 344.62 Million |

| Market Size (2026) | USD 395.65 Million |

| Market Size (2031) | USD 669.12 Million |

| Growth Rate (2026 - 2031) | 11.10% CAGR |

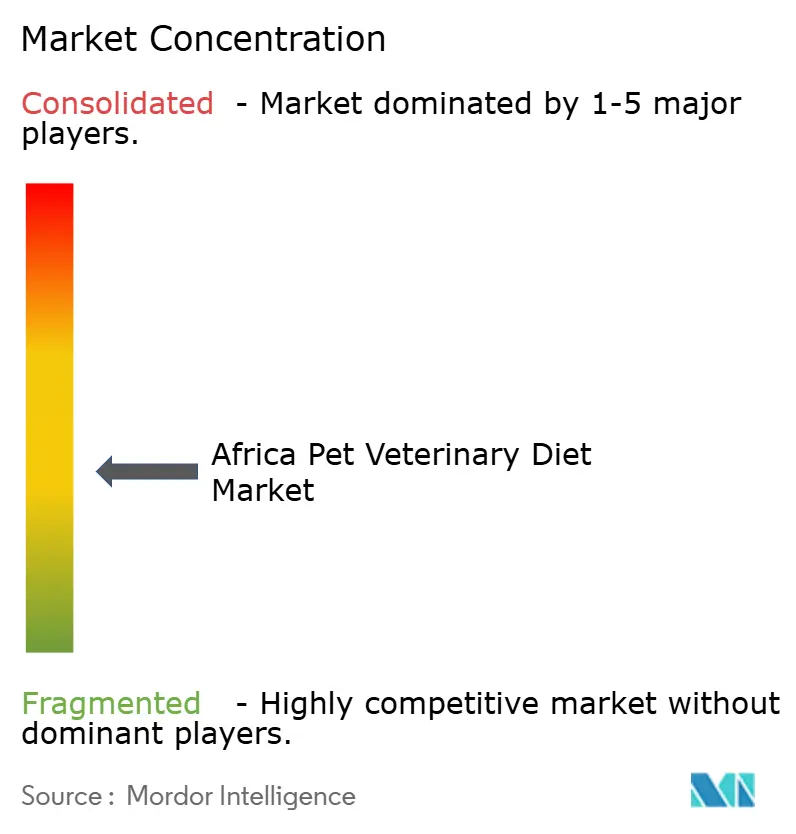

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Pet Veterinary Diet Market Analysis by Mordor Intelligence

The Africa pet veterinary diet market size is projected to grow from USD 344.6 million in 2025 to USD 395.7 million in 2026 and is forecast to reach USD 669.1 million by 2031 at 11.1% CAGR over 2026-2031. Pet humanization and shifts in urban spending are driving this rise, and strengthening demand for premium nutrition and wellness products[1]Source: Trade Intelligence, “South Africa's Pet Care Market Grows to R10.4 Billion as Owners Prioritise Their Furry Family Members,” EWN, ewn.co.za. Statistics South Africa published the country’s first official pet census in May 2026, recording 9.3 million dogs and 5.2 million cats, providing the African pet veterinary diet market with a firmer baseline for clinical nutrition planning[2]Source: Statistics South Africa, “Stats SA Pet Census Reveals $5 Billion Market Opportunity,” SouthAfricanNews24, southafricanews24.com. Broader economic improvement across the continent is widening discretionary spending among urban households, helping more owners move from general pet food to condition-specific diets. The Africa pet veterinary diet market is moderately fragmented, so companies that build stronger ties with clinics and specialist channels can carve out space in niche categories without facing a single dominant rival at every outlet. Tele-veterinary services in Nigeria and other emerging hubs are beginning to expand prescription access beyond major cities, offering the African pet veterinary diet market a practical path into tier-2 and tier-3 demand centers if data access and owner awareness continue to improve.

Key Report Takeaways

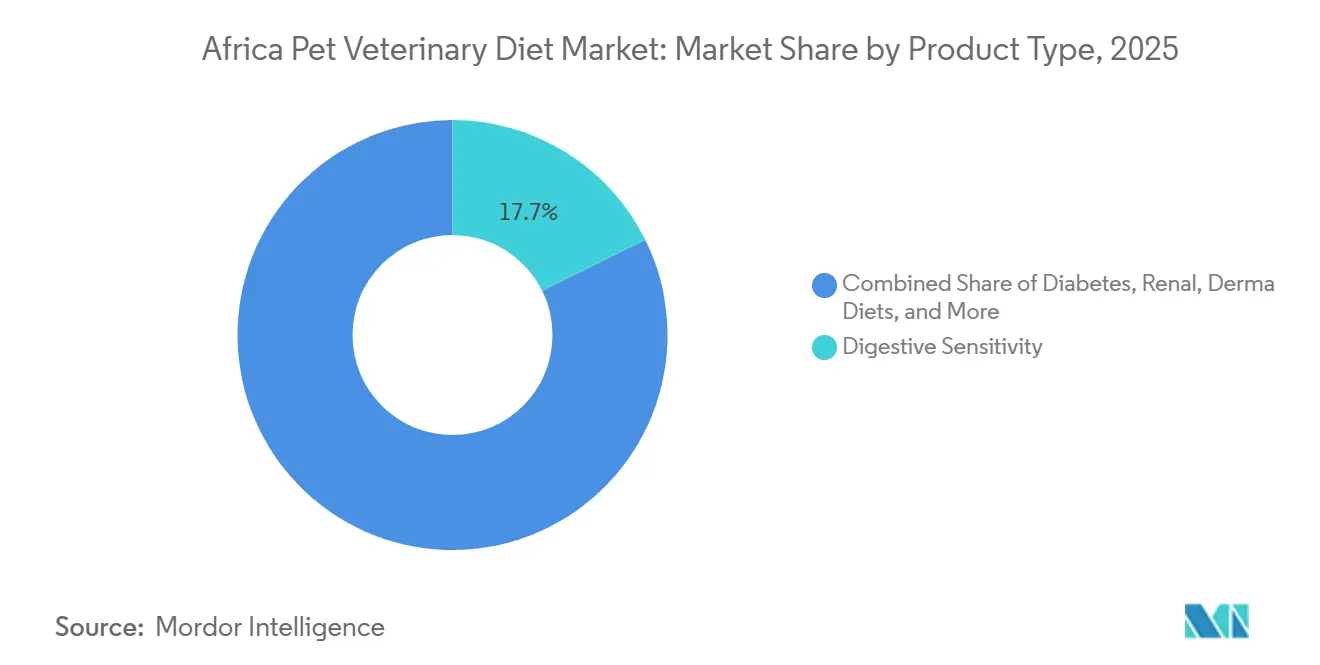

- By product type, digestive sensitivity accounted for the largest Africa pet veterinary diet market share, 17.7%, in 2025, while the oral care diets market size is projected to grow at the fastest CAGR of 9.0% from 2026 to 2031.

- By pets, dogs held the largest Africa pet veterinary diet market share, 53.2%, in 2025, whereas the cats market size is projected to grow at the fastest CAGR of 8.8% from 2026 to 2031.

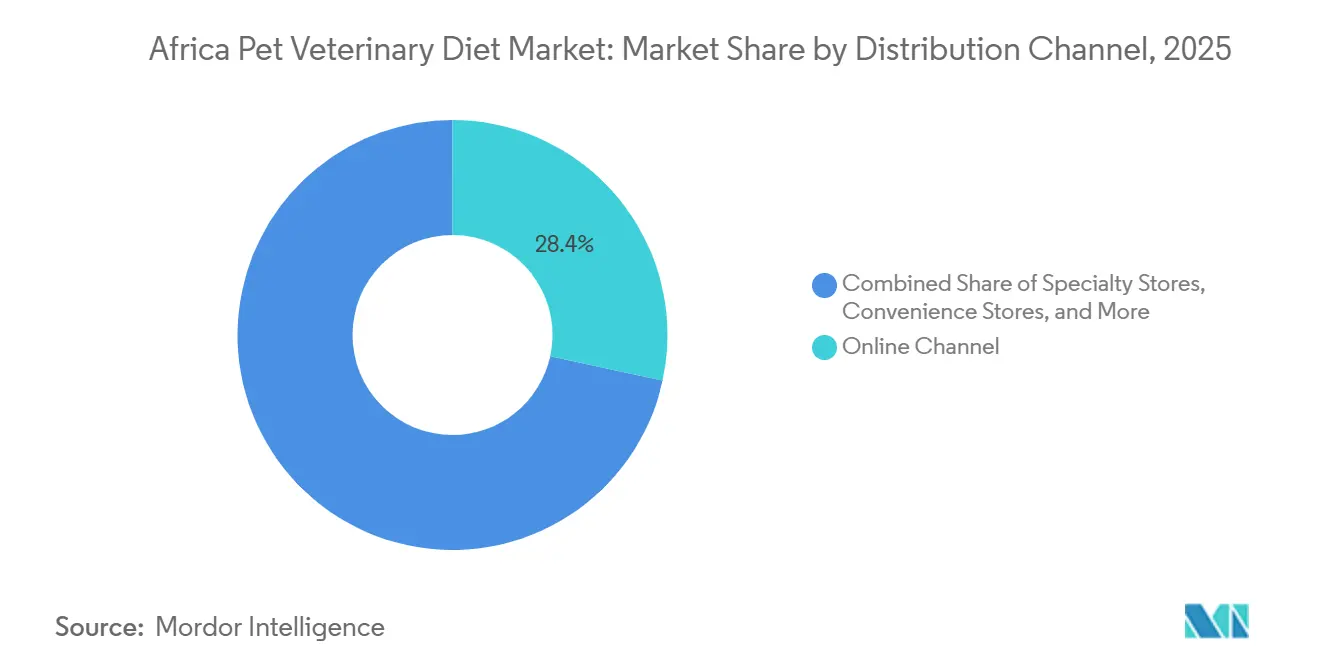

- By distribution channel, the online channel accounted for the largest Africa pet veterinary diet market share, 28.4%, in 2025 and is also projected to record the fastest CAGR of 10.6% from 2026 to 2031.

- By geography, South Africa held the largest Africa pet veterinary diet market size at 15.4% in 2025 and is projected to remain the fastest-growing market, registering a CAGR of 11.4% during 2026–2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Africa Pet Veterinary Diet Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising diagnosis of chronic companion-animal conditions | +2.3% | Africa wide, with highest intensity in South Africa, Nigeria and peri-urban Rest of Africa | Short term (≤ 2 years) |

| Expansion of veterinary prescription nutrition protocols | +2.0% | South Africa, Nigeria, Kenya and urban centers in Rest of Africa | Medium term (2-4 years) |

| Growth of premium and preventive pet care spending | +1.7% | South Africa, with emerging gains in Nigeria and Kenya | Medium term (2-4 years) |

| Tele-veterinary access and digital prescription workflows | +1.4% | Urban South Africa and Rest of Africa | Short term (≤ 2 years) |

| Import Liberalization and Faster Product Registration in Key Markets | +1.1% | South Africa, with spillover to West and East Africa under the African Continental Free Trade Area (AfCFTA) | Medium term (2-4 years) |

| Microbiome-targeted and functional diet innovation | +0.9% | Africa wide, with early adoption in South Africa specialty channels | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Diagnosis of Chronic Companion-Animal Conditions

Companion animals across Africa are being diagnosed more often with renal disease, urinary problems, digestive sensitivity, skin conditions, and metabolic disorders as formal veterinary access improves. This matters because therapeutic diets typically drive repeat purchases once a condition is identified, making demand steadier than in standard pet food categories. The first official South African pet census, published in May 2026, counted 14.5 million cats and dogs, providing the Africa pet veterinary diet market with a larger, more reliable clinical base than earlier estimates. That pet population is already large enough to support meaningful caseloads in organized practice for renal, urinary, digestive, and weight management. As pet lifespan improves with better general nutrition and care, age-linked conditions such as renal insufficiency and obesity are likely to remain a lasting source of demand for prescription diets.

Expansion of Veterinary Prescription Nutrition Protocols

Veterinary clinics are increasingly treating diet as part of therapy rather than as an optional add-on, which is giving the African pet veterinary diet market a stronger clinical foundation. Royal Canin and the University of Pretoria opened Gauteng’s first internationally accredited Cat-Friendly Clinic in July 2025 at the Onderstepoort Veterinary Academic Hospital, raising confidence in feline diagnosis and nutritional management. Clinics trained in accredited settings are more likely to recommend prescription diets earlier in disease management, rather than waiting until the condition is advanced. That gives suppliers with stronger vet education programs a durable advantage that is harder to displace with price cuts alone.

Growth of Premium and Preventive Pet Care Spending

South Africa’s pet care market has expanded steadily, with rising consumer preference shifting toward higher-value and premium nutrition categories. Within this evolving spending pattern, veterinary and condition-specific diets are gaining traction as pet owners increasingly prioritize preventive health, digestive support, weight management, and long-term wellbeing outcomes. This shift is raising average product value and strengthening demand for clinically positioned nutrition solutions. Across urban African markets, younger and more informed pet owners are further accelerating this transition by favoring scientifically formulated diets over general-purpose pet food. As a result, the Africa pet veterinary diet market is increasingly driven by brands that emphasize clinical efficacy, functional health benefits, and veterinary endorsement rather than broad lifestyle positioning.

Tele-Veterinary Access and Digital Prescription Workflows

Enhanced digital connectivity and remote veterinary access are progressively addressing structural barriers in the Africa pet veterinary diet market, particularly the reliance on physical proximity to clinics for specialized nutrition advice. Tele-veterinary platforms and digital consultation tools facilitate quicker interactions between pet owners and veterinarians, enabling earlier diagnoses and timely dietary interventions. This is especially critical for veterinary diets, which often require professional recommendations and continuous monitoring. As these services extend beyond major urban centers into secondary cities and peri-urban areas, more pet owners can access prescription-based nutrition pathways. Overall, digital veterinary ecosystems are improving market penetration for condition-specific diets by enhancing accessibility, consultation efficiency, and adherence to veterinary-led feeding guidelines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium pricing limits mass-market adoption | -2.1% | Africa wide, with the strongest pressure in Nigeria, Kenya and Rest of Africa | Short term (≤ 2 years) |

| Low veterinarian density outside major cities | -1.8% | Primarily Nigeria, Kenya and Rest of Africa, with a secondary effect in rural South Africa | Medium term (2-4 years) |

| Fragmented specialty distribution | -1.4% | Nigeria, Kenya Rest of Africa, with spillover into rural South Africa | Medium term (2-4 years) |

| Limited owner awareness of prescription diet benefits | -1.7% | Africa wide, with higher intensity in Nigeria, Kenya and Rest of Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Premium Pricing Limits Mass-Market Adoption

Therapeutic diets still cost 2 to 4 times as much as standard pet food in many African settings, which keeps adoption concentrated among upper-income urban households. South Africa’s per-capita pet food expenditure reached USD 9.21 in 2025, but even there, the price gap remains wide for many owners[3]Source: The Star, “More Africans Get Cats, Dogs as Disposable Income Grows,” The Star, the-star.co.ke. The problem is not only the headline price, but also the lack of a broad middle tier between premium prescription brands and mass-market feed. That leaves many households treating therapeutic nutrition as a discretionary purchase rather than as part of treatment. The Africa pet veterinary diet market could widen faster if suppliers introduce smaller pack sizes, clinic-linked programs, and more flexible price ladders that reduce trial resistance.

Low Veterinarian Density Outside Major Cities

The Africa pet veterinary diet market still depends heavily on an uneven veterinary map, with most specialist services clustered in major cities. Limited clinical access reduces diagnosis rates first, and that then reduces prescription diet demand in peri-urban and rural areas where many pets still live. South Africa’s strongest veterinary training base remains centered on the University of Pretoria at Onderstepoort, which supports clinical standards but also reflects the concentration of specialist knowledge in formal urban practice. Tele-veterinary tools can offset some of that pressure, but they still depend on stable smartphone access, affordable data, and owner confidence in digital channels[4]Source: Disrupt Africa, “How Nigeria's Vet Konect Uses Mobile, AI Technology to Connect Users to Veterinary Services,” Disrupt Africa, disruptafrica.com. Until the workforce and digital infrastructure improve together, adoption will remain much stronger in urban clusters than in the wider pet population.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Digestive Sensitivity Anchors Volume and Oral Care Commands Fastest Growth

Digestive sensitivity captured 17.7% of the product type segment in 2025, making it the largest category in the Africa pet veterinary diet market. This lead reflects how often gastrointestinal issues appear when pets move from informal feeding or home-prepared food to more structured commercial diets. Digestive care also serves as an early entry point into therapeutic nutrition, as owners and veterinarians can often see response patterns more quickly than with some longer-cycle conditions. Renal and urinary tract disease diets held the next most meaningful combined position, supported by stronger recognition that chronic kidney disease and urolithiasis respond well to dietary management. Derma diets and obesity diets remained smaller, but both categories are gaining ground as the Africa pet veterinary diet industry places more weight on non-drug interventions that can support long-term condition control.

Oral care diets are projected to expand at a 9.0% CAGR through 2026 to 2031, making them the fastest-growing product type in the Africa pet veterinary diet market. Diabetes and other veterinary diets are also advancing as feline endocrine and metabolic conditions receive greater attention in practice. A 2026 study, "Beneficial Effects of a Prebiotic-Postbiotic Supplement on Digestive Health and Fecal Microbiota in Dogs and Cats," reported improvements in digestive health and gut microbiota balance among dogs and cats with mild gastrointestinal disturbances, providing stronger clinical validation for microbiome-focused nutritional formulations within the Africa pet veterinary diet industry.

By Pets: Dogs Dominate and Cats Gain Prescribing Momentum

Dogs accounted for 53.2% of the Africa pet veterinary diet market share in 2025, making them the largest pet type by a significant margin. This dominance is attributed to their widespread presence across urban, peri-urban, and rural households, providing canine therapeutic diets with a broader, more established addressable base than other pet categories. The expansion of organized retail channels and the growing availability of premium veterinary nutrition products are enhancing accessibility and driving the adoption of condition-specific diets for dogs, often under veterinary prescription.

Cats are anticipated to be the fastest-growing segment in the Africa pet veterinary diet market, with a projected CAGR of 8.8% through 2031. This growth is driven by increasing awareness of feline-specific health conditions and a gradual shift toward specialized preventive and therapeutic nutrition for cats. As veterinary diagnostics and pet health awareness improve, the demand for targeted feline diets is projected to rise steadily, driving faster growth than in other pet segments.

By Distribution Channel: Online Leadership Changes Access Patterns

Online channel accounted for 28.4% of the Africa pet veterinary diet market size in 2025, making it the leading distribution format. That position is notable because prescription diets in many other regions still move mainly through veterinary clinics. In Africa, the stronger online role reflects a hybrid model where e-commerce platforms support vet-authorized ordering and repeat purchases once a diet has already been recommended. The model also carries some risk because therapeutic products can be treated like routine pet food if channel controls are weak. South Africa’s ePETstore has introduced exclusive online prescription-diet partnerships that ensure veterinary oversight while improving consumer convenience. This approach offers the Africa pet veterinary diet market a scalable model for integrating clinical control with digital accessibility.

The Online channel is projected to expand at a 10.6% CAGR through 2031, making it the fastest-growing route to market in the Africa pet veterinary diet market. Specialty stores and supermarkets are important supporting channels in South Africa’s larger cities, where premium pet nutrition is becoming easier to find in organized retail. Convenience stores remain small, but they still matter as last-mile outlets in markets where specialist retail infrastructure is limited. ADM’s 2026 clinical publication on PRIOME Metabolic Health postbiotic added evidence for science-backed metabolic formulations, which supports the online sale of specialized products to owners who actively search for validated options.

Geography Analysis

South Africa serves as the commercial anchor of the Africa pet veterinary diet market, holding the largest market share at 15.4% in 2025. The market in South Africa is projected to grow at a compound annual growth rate (CAGR) of 10.8% from 2026 to 2031. The country benefits from a relatively mature pet care ecosystem, supported by established veterinary governance, structured clinical training, and well-developed distribution networks. Strong integration between veterinary clinics, premium retail channels, and pet service providers in regions such as Gauteng and Western Cape enhances demand visibility. This integration facilitates consistent adoption of prescription-led and condition-specific nutrition, positioning South Africa as the largest and most structured demand center in the region.

Nigeria is emerging as a key growth market within the Africa pet veterinary diet landscape. This growth is driven by rapid urbanization, increasing middle-class pet ownership, and improved awareness of preventive pet healthcare. The expansion of veterinary clinics and the gradual strengthening of organized pet retail channels are improving access to therapeutic and condition-specific diets, although adoption remains uneven outside major urban centers. Increasing digital engagement and a growing willingness to invest in premium pet nutrition are projected to support steady market development, positioning Nigeria as a high-potential demand hub for veterinary diets in West Africa.

Kenya is experiencing steady development in its companion animal healthcare ecosystem, supported by increasing clinic density, growing professional veterinary engagement, and the expansion of premium pet care services in urban centers. Rising awareness of preventive nutrition and gradual improvements in pet food distribution networks are driving greater adoption of veterinary diets, particularly in major cities. Alongside Kenya, other African markets, including Morocco, Senegal, Ivory Coast, and Cameroon, are gradually building structured pet care ecosystems. These developments are supported by improving import channels, evolving regulatory frameworks, and increasing awareness of therapeutic pet nutrition. Collectively, these markets contribute to the broader diversification and long-term growth of the Africa pet veterinary diet market beyond the core Southern and West African hubs.

Competitive Landscape

In 2025, the Africa pet veterinary diet market was moderately fragmented, with the top five companies accounting for a significant share of revenue. The competitive landscape was dominated by global players such as Mars, Incorporated and Nestlé S.A., which maintained strong positions through established veterinary nutrition portfolios and long-standing relationships with clinics. Colgate-Palmolive Company also held a significant presence in the premium therapeutic nutrition segment through its veterinary-focused product offerings. Overall, competition in this market was heavily influenced by clinic engagement, as prescription-based products generated more stable, recurring demand than general retail pet food.

Regional and mid-tier players contributed to the competitive structure by leveraging localized pricing strategies, efficient distribution networks, and stronger alignment with regional retailers. Companies such as Ultra Pet Company and VetsBrands effectively competed in value and mid-segment veterinary nutrition categories by responding swiftly to local demand dynamics. This created a dual-layer market structure, where global leaders dominated the premium veterinary diet segment, while regional firms enhanced their presence in price-sensitive and semi-urban segments across the continent.

Competitive intensity was further shaped by the growing convergence of veterinary nutrition and pharmaceutical-led dietary solutions. This trend pushed companies to focus on product specialization and clinical relevance. Consequently, the Africa pet veterinary diet market increasingly favored players that integrated scientific formulation, veterinary collaboration, and consistent clinic availability into their commercial strategies. This combination of clinical credibility and distribution strength emerged as a key differentiator beyond pricing, enabling both global specialists and focused regional brands to coexist within a structurally expanding market.

Africa Pet Veterinary Diet Industry Leaders

Mars, Incorporated

Nestlé S.A. (Nestlé Purina PetCare Company)

Colgate-Palmolive Company (Hill’s Pet Nutrition, Inc.)

General Mills, Inc. (Blue Buffalo Pet Products, Inc.)

Schell & Kampeter, Inc. (Diamond Pet Foods)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Colgate-Palmolive Company (Hill’s Pet Nutrition, Inc.) launched new therapeutic diets for dogs and cats targeting chronic kidney disease alongside food and digestive sensitivities. The multi-condition formulations reflect a shift toward integrated veterinary nutrition solutions, supporting broader adoption of advanced prescription diets across global markets, including Africa.

- October 2025: Dechra introduced the SPECIFIC Heart & Kidney Support Hydrolysed diets for dogs and cats, enhancing its range of therapeutic nutrition products for companion animals with chronic kidney disease. This launch highlights the industry's emphasis on condition-specific veterinary diets and aligns with the rising use of clinically formulated nutrition solutions for managing long-term diseases in pets.

- November 2025: ParaVet launched an AI-powered veterinary care platform in Nigeria through McGregorys Limited, enabling real-time tele-consultations and digital access to licensed veterinarians, improving veterinary service accessibility and strengthening digital-driven adoption of pet and livestock healthcare solutions.

Africa Pet Veterinary Diet Market Report Scope

A pet veterinary diet, also known as a therapeutic or prescription diet, is a specialized pet food scientifically formulated to help manage, treat, or prevent specific medical conditions, including kidney disease, allergies, and obesity.

The Africa Pet Veterinary Diet Market Report is Segmented by Product Type (Diabetes, Digestive Sensitivity, Oral Care Diets, Renal, Urinary Tract Disease, Derma Diets, Obesity Diets, and Other Veterinary Diets), by Pets (Cats, Dogs, and Other Pets), by Distribution Channel (Convenience Stores, Online Channel, Specialty Stores, Supermarkets/Hypermarkets, and Other Channels), and by Geography (South Africa, Nigeria, Kenya and Rest of Africa). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons)

| Diabetes |

| Digestive Sensitivity |

| Oral Care Diets |

| Renal |

| Urinary Tract Disease |

| Derma Diets |

| Obesity Diets |

| Other Veterinary Diets |

| Dogs |

| Cats |

| Other Pets |

| Convenience Stores |

| Online Channel |

| Specialty Stores |

| Supermarkets and Hypermarkets |

| Other Channels |

| South Africa |

| Nigeria |

| Kenya |

| Rest of Africa |

| By Product Type | Diabetes |

| Digestive Sensitivity | |

| Oral Care Diets | |

| Renal | |

| Urinary Tract Disease | |

| Derma Diets | |

| Obesity Diets | |

| Other Veterinary Diets | |

| By Pets | Dogs |

| Cats | |

| Other Pets | |

| By Distribution Channel | Convenience Stores |

| Online Channel | |

| Specialty Stores | |

| Supermarkets and Hypermarkets | |

| Other Channels | |

| By Geography | South Africa |

| Nigeria | |

| Kenya | |

| Rest of Africa |

Key Questions Answered in the Report

What is driving demand for veterinary diets in Africa?

The strongest demand drivers are rising diagnosis of chronic conditions, wider use of prescription nutrition in clinics, premium pet care spending, and improving tele-veterinary access. These factors support growth from USD 395.7 million in 2026 to USD 669.1 million by 2031.

Which pet type generates the highest revenue in Africa?

Dogs led with 53.2% share in 2025 because canine ownership is broader across urban, peri-urban, and rural households, giving canine therapeutic products the largest base.

Which product type area is growing the fastest?

Oral care diets are projected to grow fastest at a 9% CAGR through 2031.

Why is online sales so important in this category?

Online channel held 28.4% share in 2025 and is projected to grow at 10.6% CAGR. Digital ordering helps repeat purchases and improves access in markets where specialty retail and clinics are unevenly distributed.

Page last updated on: