Africa Feed Pigments Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

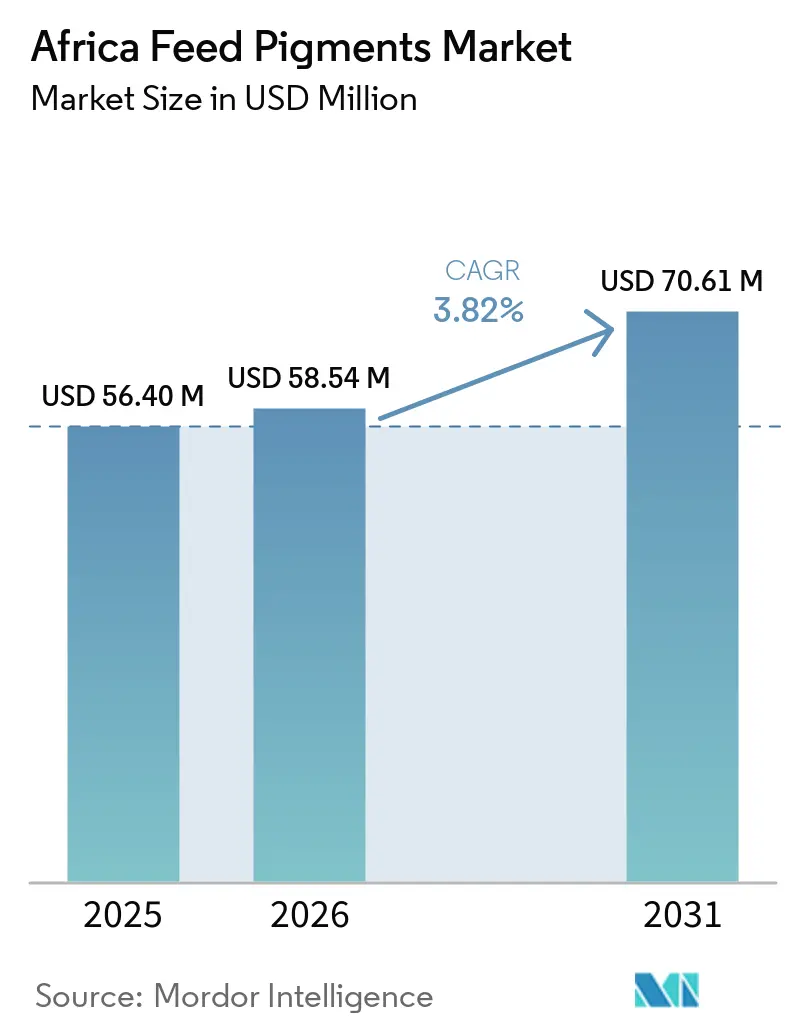

| Base Year Market Size (2025) | USD 56.40 Million |

| Market Size (2026) | USD 58.54 Million |

| Market Size (2031) | USD 70.61 Million |

| Growth Rate (2026 - 2031) | 3.82% CAGR |

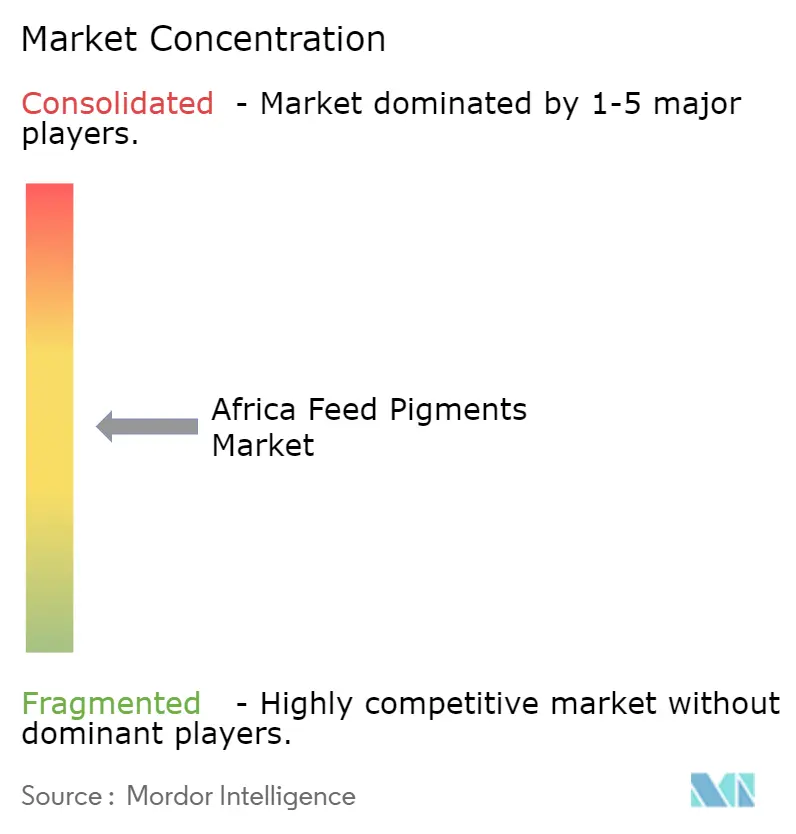

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Feed Pigments Market Analysis by Mordor Intelligence

The Africa feed pigments market was valued at USD 56.40 million in 2025 and is projected to grow from USD 58.54 million in 2026 to USD 70.61 million by 2031, registering a CAGR of 3.82% during the forecast period from 2026 to 2031. The market is experiencing a shift from small-scale feed mixing to commercial compound feed production, particularly in South Africa, Egypt, and the main livestock corridors of East Africa, where formal feed systems enable more consistent use of additives. Poultry remains a key driver of demand, as yolk and skin color are important quality indicators. Additionally, Egypt’s intensive aquaculture sector supports carotenoid use through standardized feed programs. The market is also witnessing a gradual transition toward traceable natural inputs, driven by the growth of branded poultry programs and increased retailer focus on ingredient transparency and product consistency. BASF SE and DSM-Firmenich AG dominate the synthetic carotenoid segment, while the natural pigment supply remains fragmented, providing opportunities for specialist suppliers with strong regional distribution networks. Challenges such as import dependence, foreign exchange constraints, and inadequate storage conditions continue to hinder the pace of adoption. However, these factors are unlikely to significantly impact the market's long-term growth prospects.

Key Report Takeaways

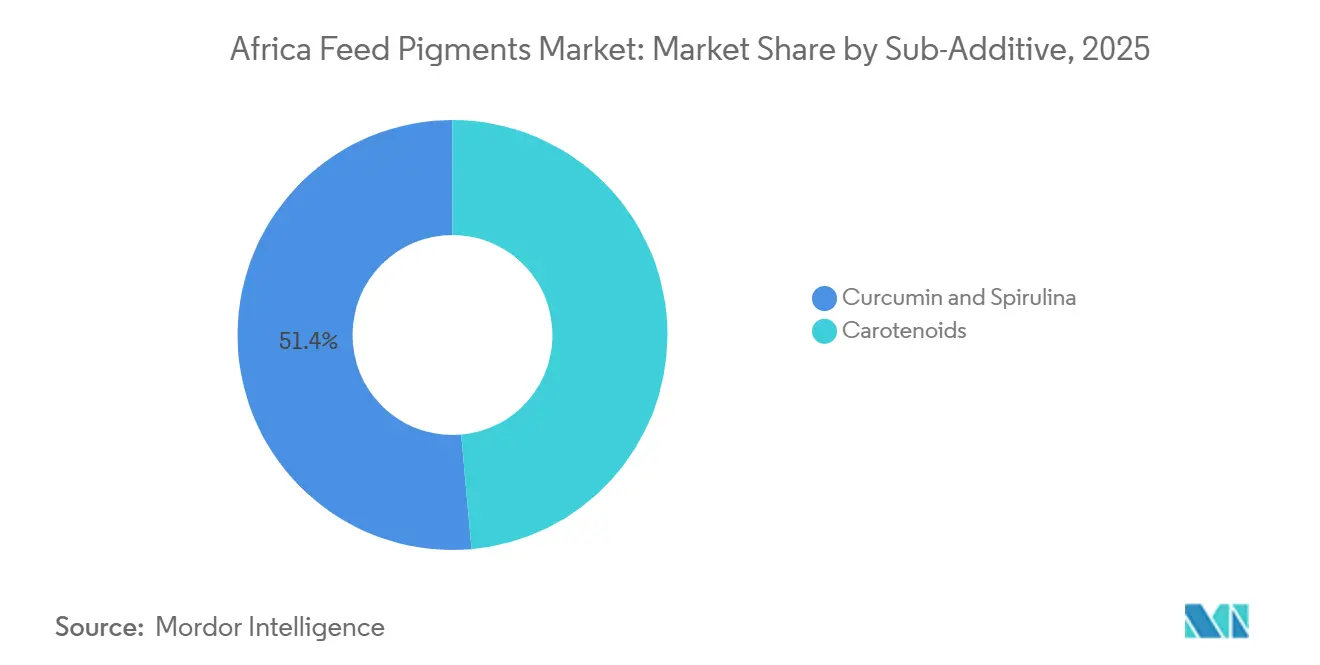

- By sub-additive, the Africa feed pigment market share for curcumin and spirulina was the largest 51.4% in 2025, while the Africa feed pigment market size for carotenoids is forecast to grow at the fastest CAGR of 4.0% from 2026 to 2031.

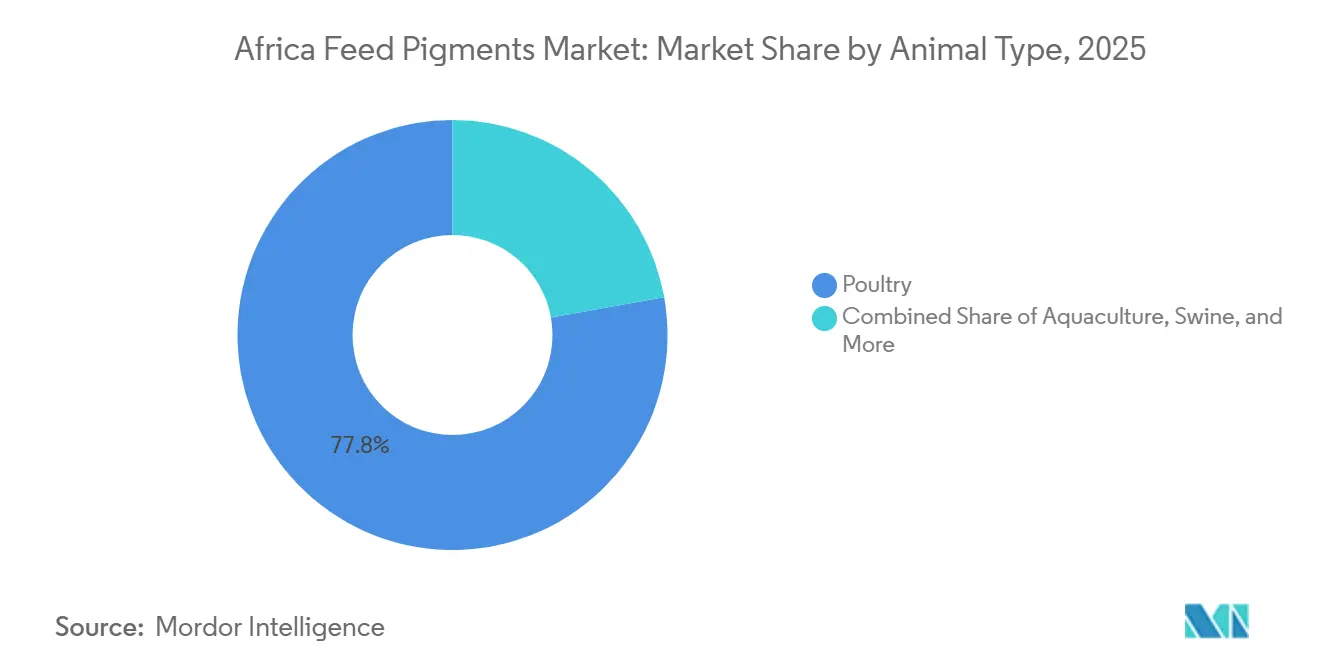

- By animal, poultry accounted for the largest market share of 77.8% in 2025, while poultry is projected to grow the fastest CAGR of 4.1% from 2026 to 2031.

- By geography, South Africa accounted for the largest 48.6% market share in 2025, and it is also projected to grow at the fastest CAGR of 4.6% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Africa Feed Pigments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising poultry feed demand and premium egg color requirements | +1.2% | South Africa, Egypt, and Nigeria | Short term (≤ 2 years) |

| Expansion of commercial feed mills across Africa | +0.8% | Kenya, Nigeria, and South Africa | Medium term (2-4 years) |

| Aquaculture scale-up in Egypt, Nigeria, and East Africa | +0.7% | Egypt, Nigeria, and East Africa | Medium term (2-4 years) |

| Shift toward natural pigments in branded poultry products | +0.9% | South Africa, Egypt, and Kenya | Medium term (2-4 years) |

| Modern retail and foodservice color consistency requirements | +0.5% | South Africa and Egypt | Short term (≤ 2 years) |

| Tax and VAT relief on specialized feed inputs in select markets | +0.4% | Egypt, Kenya, and Rest of Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Poultry Feed Demand and Premium Egg Color Requirements

The Africa feed pigments market is witnessing growing demand driven by the expansion of commercial poultry production, particularly in South Africa. Poultry is the largest contributor to South Africa's agricultural sector and a major consumer of compound feed. According to the United States Department of Agriculture, South Africa's chicken meat production is forecasted to reach 1.68 million tons in 2026, up from an estimated 1.64 million tons in 2025, supported by industry growth and improved feed economics[1]Source: United States Department of Agriculture Foreign Agricultural Service (USDA FAS), “Poultry and Products Annual – Republic of South Africa (SF2025-0026),” fas.usda.gov.. With the increase in poultry production, the demand for specialized feed additives, such as carotenoid pigments, is also rising. Egg producers are increasingly incorporating pigments to ensure consistent yolk coloration that meets retail and branded egg program standards. As yolk color significantly influences consumer purchasing decisions, feed pigments have become a critical component of layer feed formulations, driving their adoption across the poultry feed industry and contributing to market growth in Africa.

Expansion of Commercial Feed Mills Across Africa

The establishment of large-scale commercial feed manufacturing facilities is strengthening the foundation of the Africa feed pigments market. Modern feed mills are equipped to incorporate specialty additives through precise formulation and quality-control systems. For instance, in February 2026, De Heus inaugurated a USD 23.2 million feed manufacturing plant in Athi River, Kenya, with an initial annual production capacity of 240,000 metric tons, catering to poultry, pigs, ruminants, and aquaculture sectors[2]Source: De Heus Animal Nutrition, “De Heus Kenya Opens Landmark Feed Mill in Athi River, Boosting Agricultural Sector and Regional Growth,” deheus.com.. These investments increase the volume of feed produced through industrial processing facilities, enhancing the potential adoption of feed pigments to improve product quality and consistency in livestock and poultry production. As commercial feed production capacity expands across Africa, pigment suppliers benefit from access to a wider customer base adhering to standardized feed manufacturing practices, thereby driving the growth of the Africa feed pigments market.

Aquaculture Scale-Up in Egypt, Nigeria, and East Africa

The rapid expansion of aquaculture production is driving significant opportunities in the Africa feed pigments market. Commercial fish farming depends extensively on formulated feeds that include specialty additives like pigments. The growth of intensive and semi-intensive aquaculture systems has heightened the need for feed formulations that enhance fish quality, appearance, and market acceptance. As fish farming becomes increasingly commercialized and export-focused, producers are prioritizing consistent product characteristics to meet consumer and retail standards. Additionally, rising investments in aquaculture across various African countries are bolstering the demand for feed additives, contributing to the sustained growth of the feed pigments market.

Shift Toward Natural Pigments in Branded Poultry Products

The Africa feed pigments market is experiencing growth due to the increasing preference for natural feed additives in commercial poultry production. Natural pigments are becoming more popular as they offer coloration benefits while also contributing to animal health and product quality. A study published in the Antioxidants journal demonstrated that dietary curcumin supplementation in broilers enhanced growth performance, antioxidant status, intestinal morphology, and meat quality, emphasizing the multifunctional advantages of naturally derived pigment ingredients. As poultry producers and food retailers focus more on clean-label and naturally sourced inputs, feed manufacturers are exploring natural pigment formulations that align with premium product positioning. This trend is anticipated to drive the adoption of natural feed pigments in Africa’s growing poultry industry.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High import dependence for carotenoids and pigment premixes | -0.4% | Sub-Saharan Africa and North Africa | Long term (≥ 4 years) |

| Cost-sensitive poultry economics limit pigment inclusion rates | -0.3% | Kenya, Nigeria, and Rest of Africa | Short term (≤ 2 years) |

| Foreign exchange shortages delay additive procurement | -0.3% | Nigeria, Kenya, and Rest of Africa | Medium term (2-4 years) |

| Heat and storage instability in fragmented logistics networks | -0.2% | Sub-Saharan Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Import Dependence for Carotenoids and Pigment Premixes

The Africa feed pigments market is constrained by its significant dependence on imported specialty feed additives, including carotenoids and pigment premixes. This reliance increases vulnerability to supply chain disruptions and higher procurement costs. A 2025 study published in the journal Ruminants highlighted the high cost and limited availability of feed additives in sub-Saharan Africa as significant obstacles to their adoption in livestock production systems. These issues are particularly critical for feed pigments, which are predominantly sourced through international supply chains and require additional logistics and distribution efforts. Consequently, feed manufacturers may reduce pigment inclusion in feed formulations during periods of cost pressure, limiting market penetration and constraining the growth of the Africa feed pigments market.

Cost-Sensitive Poultry Economics Limit Pigment Inclusion Rates

The Africa feed pigments market faces challenges due to the high cost structure of poultry production, which limits the use of non-essential feed additives among cost-sensitive producers. According to the United States Department of Agriculture (USDA) Grain and Feed Annual 2025 for Kenya, feed constitutes 82% of the total chicken meat production costs. Given the significant share of feed expenses in poultry operations, producers tend to prioritize essential nutritional ingredients over specialty additives to manage input costs. Since feed pigments primarily serve to enhance product appearance and quality rather than improve animal performance, their use is often reduced or delayed during periods of financial pressure. This cost-focused purchasing behavior, particularly among small and medium-scale poultry producers, continues to hinder the wider adoption of feed pigments in the African market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub-Additive: Natural Pigment Demand Shifts Toward Dual-Function Formulations

The Africa feed pigment market share for curcumin and spirulina accounted for the largest 51.4% in 2025. Curcumin and spirulina maintain their leading position due to their combined pigmentation benefits and functional nutritional attributes, which appeal to commercial livestock and aquaculture producers. Their usage aligns with the increasing preference for natural feed ingredients that enhance animal performance while providing color enhancement. This dual-purpose value proposition drives adoption across various species and sustains demand for naturally sourced pigment solutions.

The Africa feed pigment market size for carotenoids is projected to grow at the fastest CAGR of 4.0% from 2026 to 2031. This growth is primarily attributed to their increasing application in aquaculture and poultry feed, where coloration is a critical quality factor for fish flesh, shrimp, egg yolks, and poultry skin. Additionally, carotenoids offer antioxidant benefits that promote animal health and productivity. The expansion of commercial feed production and the rising demand for premium-quality animal protein products are further driving the inclusion of carotenoid-based additives. These factors collectively support strong long-term growth prospects for this segment.

By Animal Type: Poultry Dominates, Aquaculture Emerges as Growth Frontier

Poultry held the largest market share of 77.8% in 2025. Poultry remains the dominant consumer of feed pigments because visual characteristics such as yolk color, skin pigmentation, and meat appearance directly influence purchasing decisions. Commercial layer and broiler operations use pigments to achieve product consistency and meet consumer preferences across retail channels. The sector’s large feed consumption volumes and extensive integration into formal supply chains create sustained demand for pigmentation additives. These advantages keep poultry as the primary end-use segment for feed pigments throughout the region.

Poultry is forecast to grow at the fastest CAGR of 4.1% from 2026 to 2031. Continued expansion of commercial poultry production, increasing protein consumption, and greater adoption of nutritionally balanced feed are supporting this growth trajectory. Producers are placing greater emphasis on feed efficiency, animal performance, and product quality, which encourages the use of specialized additives, including pigments. Retail demand for consistently colored eggs and poultry products further strengthens usage rates. As modern poultry production systems continue to expand, pigment consumption is projected to increase alongside overall feed demand.

Geography Analysis

South Africa accounted for the largest market share of 48.6% in 2025 and is projected to grow at the fastest CAGR of 4.6% from 2026 to 2031. The country benefits from a well-developed commercial feed industry, integrated poultry production systems, and extensive use of feed additives. Large-scale livestock operations emphasize feed quality, nutritional consistency, and product appearance, fostering favorable conditions for pigment adoption. Additionally, strong retail penetration supports demand for visually consistent poultry and livestock products. These structural advantages position South Africa as the leading regional market for feed pigment consumption.

Egypt remains a significant contributor due to its advanced aquaculture industry and increasing reliance on formulated feed. Commercial fish production requires consistent feed quality and nutritional inputs, driving demand for pigmentation additives used in aquafeed formulations. Intensive farming practices have encouraged the adoption of specialized feed ingredients that enhance product appearance and support animal performance. The country's established aquaculture infrastructure differentiates its demand profile from poultry-focused markets in other parts of Africa. Continued investment in commercial fish production is projected to sustain feed additive consumption and reinforce Egypt’s importance within the regional industry.

The rest of Africa represents an emerging opportunity as livestock commercialization and compound feed production continue to expand. According to the United States Department of Agriculture Egyptian Aquaculture Industry 2025 Update, Egypt’s aquaculture sector currently accounts for approximately 80% of the country’s total fish production, highlighting the importance of intensive feed-based production systems that rely on specialized additives and nutritional inputs[3]Source: United States Department of Agriculture (USDA) Foreign Agricultural Service, Egyptian Aquaculture Industry 2025 Update, apps.fas.usda.gov.. Similar modernization trends are gradually emerging in Nigeria, Tanzania, and other African markets, creating additional opportunities for feed pigment adoption.

Competitive Landscape

The market is moderately fragmented, with key players including BASF SE, DSM-Firmenich AG, Kemin Industries, Inc., Nutreco N.V., and Adisseo (China National Bluestar (Group) Co., Ltd.). The competitive landscape features a mix of multinational feed additive suppliers and regional distribution specialists. Global manufacturers maintain strong positions in synthetic carotenoids due to the specialized technology, rigorous quality control, and regulatory expertise required for production. These factors create high barriers to entry and support established supplier relationships with major feed producers. Conversely, natural pigment suppliers focus on differentiation through traceability, sustainability, and plant-based sourcing. This results in a market structure with concentrated supply in synthetic pigments and broader participation in natural pigment categories.

Competition in the market is increasingly shaped by product innovation, technical support, and supply chain reliability. Feed manufacturers prioritize additives that deliver consistent pigmentation performance while promoting animal health and production efficiency. In response, suppliers are expanding their product portfolios to integrate coloring functionality with nutritional benefits. Natural pigment offerings are gaining traction as livestock and aquaculture producers explore alternatives that align with shifting consumer preferences. Additionally, distribution capabilities remain critical, as access to technical expertise and reliable product availability significantly influences purchasing decisions in African feed markets.

Recent investments underscore the commitment of leading suppliers to enhancing regional operations. For instance, in September 2024, DSM-Firmenich AG inaugurated a 10,000-square-meter Animal Nutrition and Health manufacturing facility in Sadat City, Egypt. This facility is designed to produce vitamins, minerals, and feed additives for regional customers, bolstering local manufacturing capabilities and ensuring a more reliable supply of additives to commercial feed producers. Such investments not only strengthen competitive positioning but also improve service responsiveness in the expanding African livestock and aquaculture markets.

Africa Feed Pigments Industry Leaders

BASF SE

DSM-Firmenich AG

Kemin Industries, Inc.

Nutreco N.V.

Adisseo (China National Bluestar (Group) Co., Ltd.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: PAI Partners SAS has agreed to acquire Innovad Group BV, a global provider of specialty animal nutrition and feed additive solutions. This acquisition aims to enhance its innovation capabilities and expand its market presence in feed additives, including pigment-related products, to support the evolving livestock feed industry in Africa.

- September 2024: DSM-Firmenich AG inaugurated a 10,000-square-meter Animal Nutrition and Health manufacturing facility in Sadat City, Egypt, with an annual capacity of 10,000 metric tons for vitamins, minerals, and feed additives, including carotenoids. The investment strengthens regional supply capabilities for feed pigment and animal nutrition markets across Africa.

- July 2024: Nutreco N.V. acquired AECI Animal Health (Pty) Ltd in South Africa, expanding its distribution network for specialty feed additives in the region and improving market access for value-added nutrition solutions, such as pigmentation ingredients used in poultry and aquaculture feed formulations.

Africa Feed Pigments Market Report Scope

Feed pigments are natural or synthetic additives incorporated into animal feed to enhance the coloration of egg yolks, poultry skin, fish flesh, and shrimp. Additionally, they contribute to product appeal and may offer antioxidant and nutritional benefits. The Africa feed pigments market report is segmented by sub-additive (carotenoids and curcumin and spirulina), by animal (aquaculture, poultry, ruminants, swine, and other animals), and by geography (Egypt, Kenya, South Africa, and the Rest of Africa). The market forecasts are provided in terms of value (USD) and volume (metric tons).

| Carotenoids |

| Curcumin and Spirulina |

| Aquaculture | Fish |

| Shrimp | |

| Other Aquaculture Species | |

| Poultry | Broiler |

| Layer | |

| Other Poultry Birds | |

| Ruminants | Beef Cattle |

| Dairy Cattle | |

| Other Ruminants | |

| Swine | |

| Other Animals |

| Egypt |

| Kenya |

| South Africa |

| Rest of Africa |

| By Sub-Additive | Carotenoids | |

| Curcumin and Spirulina | ||

| By Animal Type | Aquaculture | Fish |

| Shrimp | ||

| Other Aquaculture Species | ||

| Poultry | Broiler | |

| Layer | ||

| Other Poultry Birds | ||

| Ruminants | Beef Cattle | |

| Dairy Cattle | ||

| Other Ruminants | ||

| Swine | ||

| Other Animals | ||

| By Geography | Egypt | |

| Kenya | ||

| South Africa | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the Africa feed pigments space in 2026?

Africa feed pigment market is valued at USD 58.5 million USD in 2026.

Which animal category drives the most demand for feed pigments in Africa?

Poultry leads by a wide margin, with the largest 77.9% share in 2025.

What is the biggest pigment type in current use across Africa?

Curcumin and Spirulina is the largest pigment type segment, with 51.4% share in 2025.

Why is South Africa so important for feed pigment suppliers?

South Africa held the largest 48.6% share in 2025 and is forecast to grow at the fastest 4.7% CAGR from 2026 to 2031, supported by large feed volumes, integrated producers, and stronger retail standards.

Page last updated on: