Africa Feed Phytogenics Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

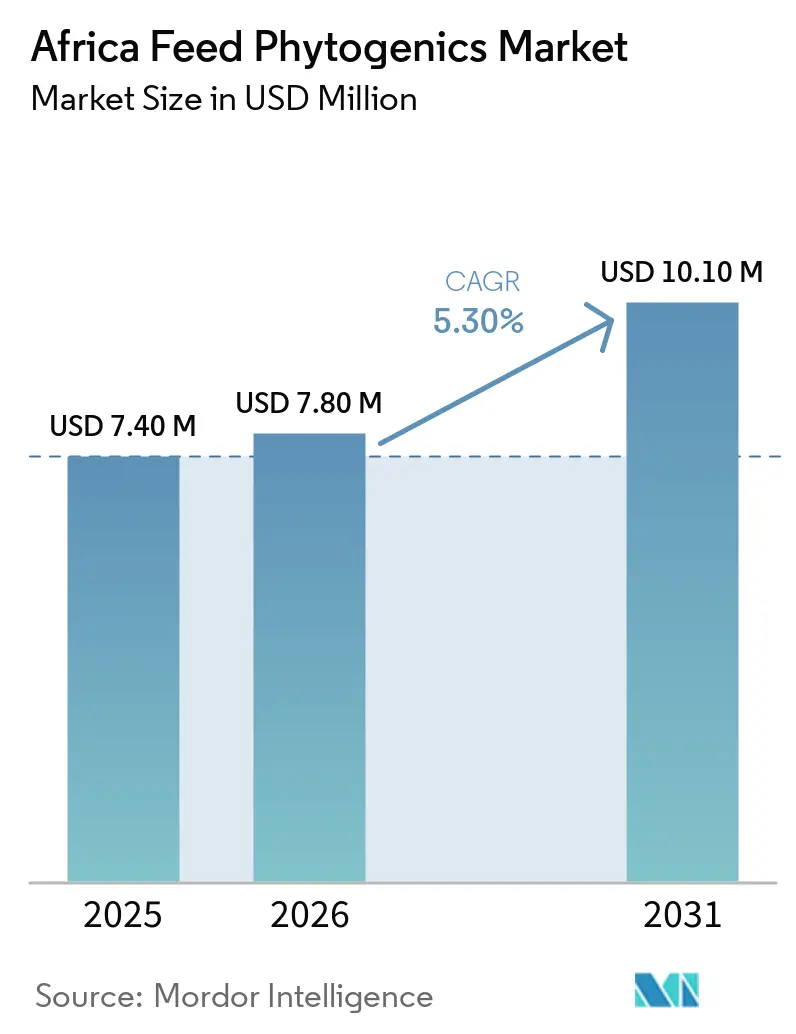

| Base Year Market Size (2025) | USD 7.40 Million |

| Market Size (2026) | USD 7.80 Million |

| Market Size (2031) | USD 10.10 Million |

| Growth Rate (2026 - 2031) | 5.30% CAGR |

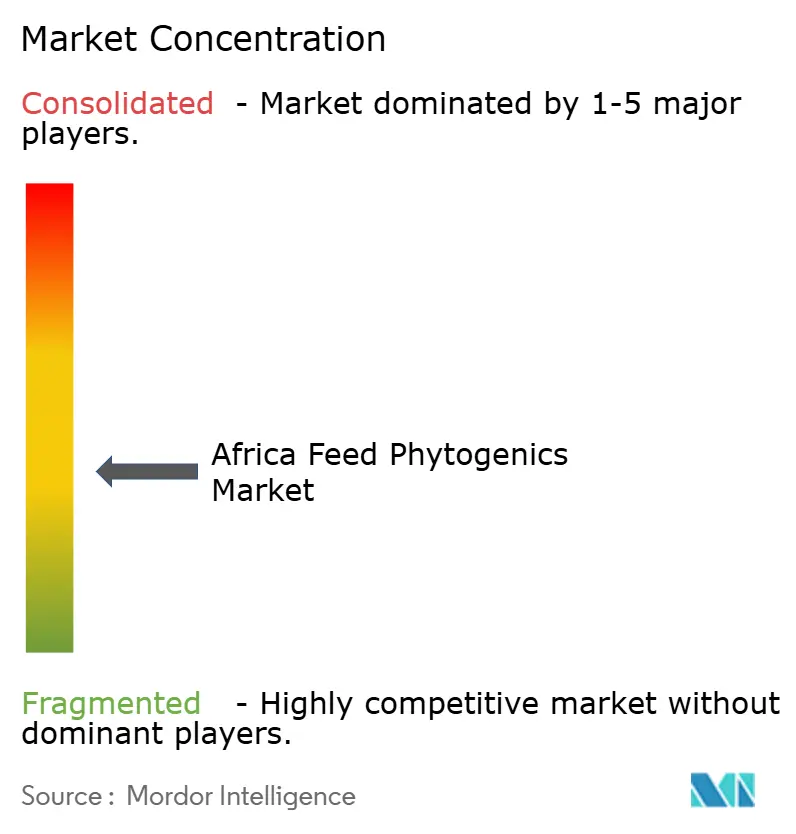

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Feed Phytogenics Market Analysis by Mordor Intelligence

The Africa feed phytogenics market size is projected to grow from USD 7.4 million in 2025 to USD 7.8 million in 2026 and is forecast to reach USD 10.1 million by 2031 at 5.3% CAGR over 2026-2031. The segment is expanding faster than the broader Africa feed additives market, indicating that commercial feed producers are giving greater weight to plant-derived bioactives when evaluating antibiotic-alternative strategies. The 2025 base also places the Africa feed phytogenics market at 1% of global demand, which leaves room for deeper penetration as formal feed formulation practices spread across the continent’s livestock systems. National antimicrobial resistance action plans in Nigeria, Ethiopia, and Zimbabwe are adding policy support for reduced antibiotic dependence in animal production, which improves the operating backdrop for the Africa feed phytogenics market. Heat stress in African livestock systems is also widening demand for antioxidant and stress-management solutions, which gives the Africa feed phytogenics market a second path for growth beyond gut health and performance uses. Suppliers that can pair standardized actives, stable delivery formats, and credible field support are better placed to convert trials into repeat purchases as the Africa feed phytogenics market becomes more structured.

Key Report Takeaways

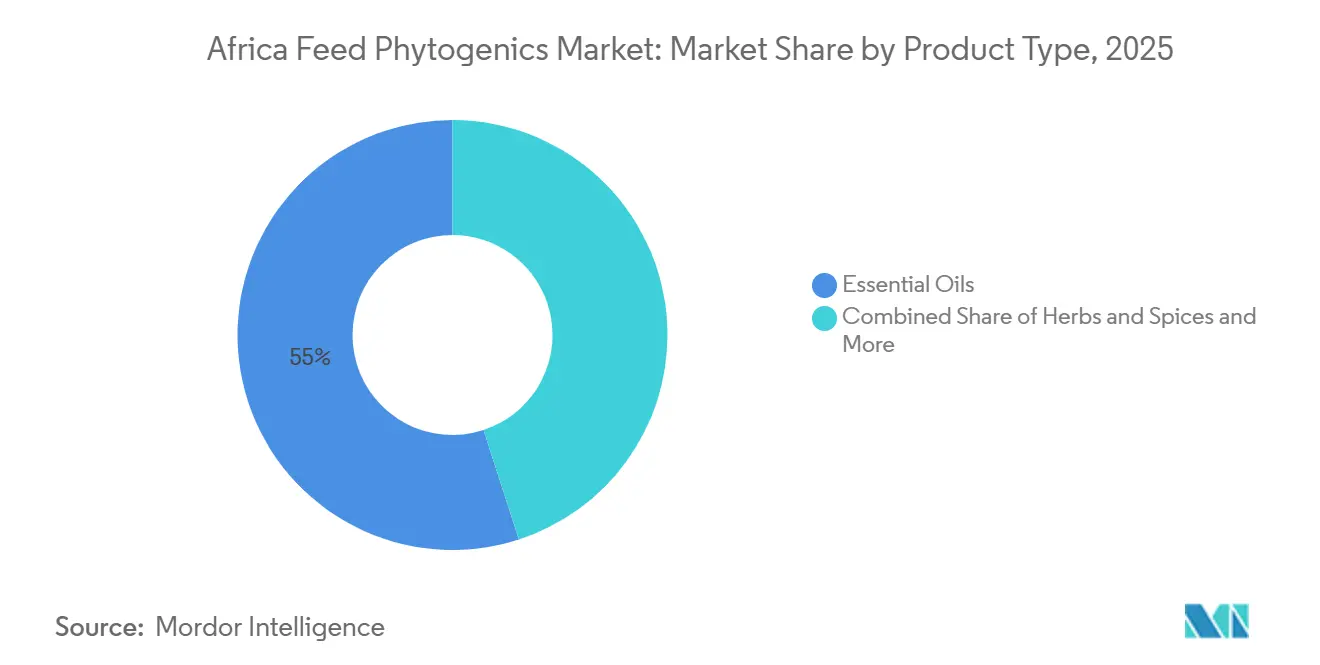

- By product type, the essential oils segment accounted for 55.0% of the Africa feed phytogenics market size in 2025 and is projected to grow at a CAGR of 5.8% during 2026–2031.

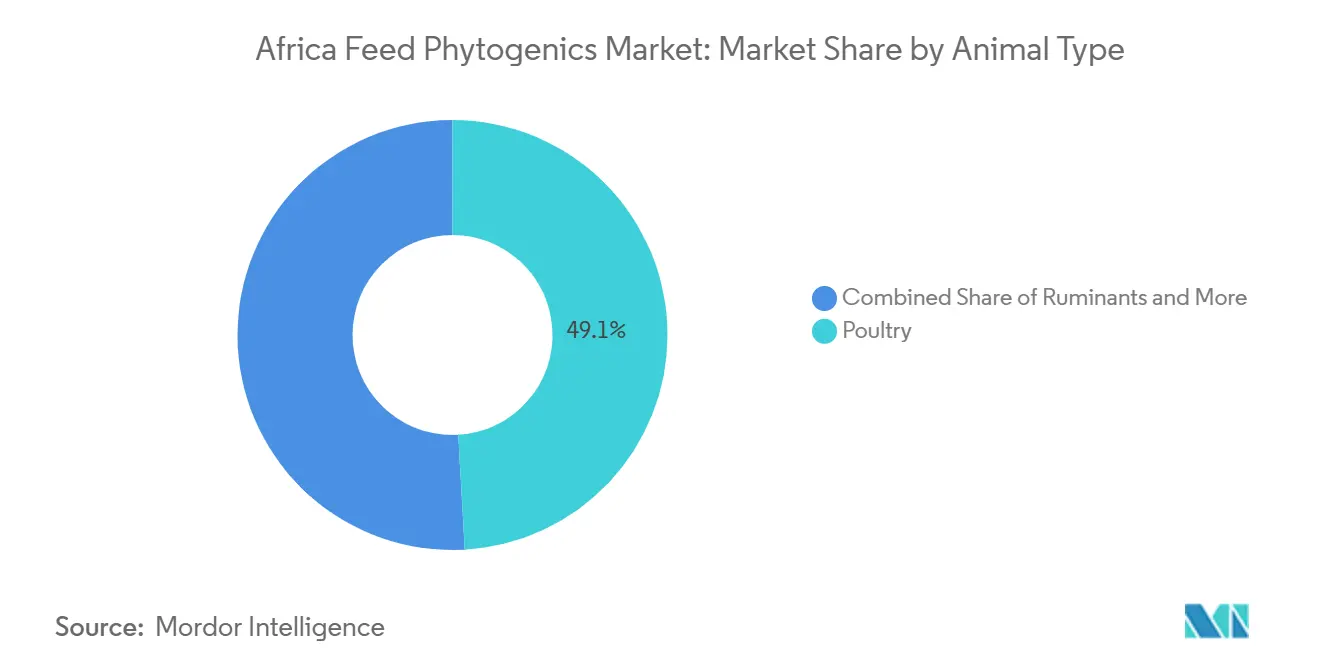

- By animal type, poultry accounted for 49.1% of the Africa feed phytogenics market share in 2025, while aquaculture is forecast to post the fastest 7.4% CAGR during 2026-2031.

- By geography, South Africa held 33.0% share in 2025, while Egypt is anticipated to witness the fastest 6.5% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Africa Feed Phytogenics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Antibiotic-Free Poultry and Aquaculture Programs | +1.2% | Egypt, South Africa, Kenya | Short term (≤ 2 years) |

| Feed Efficiency Improvement Under High Grain-Cost Pressure | +1% | Nigeria, Kenya, South Africa | Short term (≤ 2 years) |

| Demand for Natural Antimicrobial and Gut-Health Solutions in Commercial Feed | +0.9% | South Africa, Egypt, Morocco | Medium term (2-4 years) |

| Encapsulation Improving Phytogenic Stability in Hot and Humid Feed Chains | +0.8% | Nigeria, Kenya, Rest of Africa | Medium term (2-4 years) |

| Heat-stress mitigation needs in tropical livestock systems | +0.7% | Egypt, Nigeria, Kenya, South Africa | Medium term (2-4 years) |

| Standardized Botanical Actives Supporting More Repeatable Field Performance | +0.6% | South Africa, Egypt, Morocco | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Antibiotic-Free Poultry and Aquaculture Programs

Commercial poultry and aquaculture systems in Africa are moving into a stricter phase of antimicrobial resistance control, which directly supports the Africa feed phytogenics market. Nigeria launched its One Health Antimicrobial Resistance National Action Plan 2.0 in October 2024, and Ethiopia launched its fourth national action plan in December 2025, which signals stronger policy pressure on animal production systems to reduce unnecessary antibiotic use. The Food and Agriculture Organization of the United Nations documented in June 2025 that Zimbabwe’s RENOFARM work on broilers reduced antimicrobial overuse through improved husbandry and biosecurity, demonstrating that structured alternatives can work in African production settings. At the product level, poultry research shows that phytogenic blends and essential oil actives can suppress pathogens, improve gut integrity, and support feed efficiency, which fits the compliance and performance goals of modern feed programs.

Feed Efficiency Improvement Under High Grain-Cost Pressure

Feed efficiency remains one of the clearest commercial reasons for phytogenic adoption across Nigeria, Kenya, and South Africa. Producers are under pressure to protect margins when feed input costs rise, so additives that support digestibility and conversion become more relevant to buying decisions. A 2025 study published in Frontiers in Immunology found that thyme oil at 150 mg/kg improved body weight gain, feed conversion ratio, digestive enzyme activity, and economic return in broilers[1]Source: A.M. Saied, A.I. Attia, F.M. Reda, M.S. El-Kholy, M. Alagawany, and A.G. EL Nagar, “Harnessing Natural Feed Additives for Sustainable Production and Economics: The Role of Thymus vulgaris L. Oil as an Antimicrobial Agent and Growth Promoter in Improving Production and Health of Broiler Chickens,” Frontiers in Immunology, frontiersin.org. A separate 2025 study published in Scientific Reports showed that fenugreek oil at 400 mg/kg delivered the most consistent body weight gain and feed conversion improvement among the tested essential oils in broilers. A 2025 systematic review published in Ruminants also confirmed that curcumin-based products and essential oil blends improved average daily gain and feed conversion performance in ruminant systems across sub-Saharan Africa. These results strengthen the case for the Africa feed phytogenics market because even modest performance gains can help offset the added cost of phytogenic inclusion in high-cost feeding environments.

Demand for Natural Antimicrobial and Gut-Health Solutions in Commercial Feed

Commercial feed mills in South Africa, Egypt, and Morocco are paying closer attention to plant-based antimicrobial and gut-health solutions as pressure mounts to reduce routine antibiotic use. This shift is important for the Africa feed phytogenics market because buyers still need to maintain flock performance while lowering reliance on prophylactic medication. A 2025 technical review from EW Nutrition also showed that tannins and saponins can support coccidiosis control by lowering oocyst shedding and lesion scores while preserving beneficial Lactobacillus populations. The Animal Feed Manufacturers Association of South Africa included phytogenic feed additives as a formal discussion topic in its 2025 symposium material, suggesting more structured validation activity in the country’s feed sector. This more organized approach can help the Africa feed phytogenics market move from isolated product trials toward repeat commercial use.

Encapsulation Improving Phytogenic Stability in Hot and Humid Feed Chains

Delivery format matters more in the African feed phytogenics market because many supply chains operate under high heat and humidity and face long transit times. Essential oils and related actives can lose stability when exposed to temperature, oxygen, and light, making reliable delivery a real procurement concern for feed mills. A 2025 Frontiers research paper noted that microencapsulation and standardized extraction improve product consistency, bioavailability, and site-specific release of phytogenic compounds. A 2024 study published in Frontiers in Veterinary Science found that a microencapsulated phyto- and phycogenic blend improved feed conversion ratio and body weight gain in broilers, supporting the role of protected delivery systems under warm, humid feed chain conditions. As a result, encapsulation is becoming an important lever for improving repeatability and expanding the use of Africa feed phytogenics in tropical feed chains.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Batch-to-Batch Variability in Botanical Active Content | -0.80% | Nigeria, Kenya, Rest of Africa | Short term (≤ 2 years) |

| Higher Formulation Cost Versus Conventional Feed Additives | -0.70% | Nigeria, Kenya, Rest of Africa | Medium term (2-4 years) |

| Limited Africa-Specific Field Validation Across Species and Production Systems | -0.60% | Kenya, Nigeria, Morocco, Rest of Africa | Long term (≥ 4 years) |

| Distributor and Technical-Service Gaps Outside Major Livestock Hubs | -0.50% | Rest of Africa, Kenya, Nigeria, Morocco | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Batch-to-Batch Variability in Botanical Active Content

Batch variability in botanical actives remains one of the main constraints to wider adoption of phytogenic products in African feed markets. This issue matters because feed mill buyers need predictable results before they commit to repeat purchasing, especially in markets with limited technical support. A 2025 review published in Frontiers in Veterinary Science identified harvest timing, differences in plant species, growing location, extraction method, and storage conditions as major factors contributing to variation in actives such as thymol, carvacrol, cinnamaldehyde, and apigenin[3]Source: A.I. Oni and O.E. Oke, “Gut Health Modulation through Phytogenics in Poultry: Mechanisms, Benefits, and Applications,” Frontiers in Veterinary Science, frontiersin.org. The challenge is more severe in the rest of Africa markets, where local botanical sourcing may reduce cost but often lacks the quality standardization needed for consistent performance. Suppliers that offer microencapsulation, active-level standardization, and certificate-of-analysis support are better positioned in formal tender processes, but these steps also raise product cost. This creates a clear split between markets that can absorb the premium, such as South Africa, Egypt, and Morocco, and those where price sensitivity still limits adoption.

Higher Formulation Cost Versus Conventional Feed Additives

Higher formulation cost is another clear restraint on the Africa feed phytogenics market, especially outside the most formal livestock systems. Commercial phytogenic products often carry a premium because they include standardized extracts, protected delivery systems, and technical support that basic additives do not require. Research on thyme oil also noted that stability during industrial-scale use is critical, which implies that preserving efficacy often needs better handling and formulation design. Large integrated producers can test return on investment through controlled trials, but smaller operators often cannot justify that same spending with equal certainty. This slows uptake in price-sensitive poultry, ruminant, and mixed farming systems across Nigeria, Kenya, and other secondary markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Essential Oils Lead Formulation Adoption

Essential oils held 55% of the Africa feed phytogenics market share in 2025, making them the largest product type across the regional portfolio and also the fastest growing segment with 5.8% CAGR during the forecast period. A 2024 study in the International Journal of Poultry Science showed that ginger rhizome essential oil at 40-60 µL/kg body weight improved average daily broiler weight gain from 56.09 to 64.83 g/day. This kind of measurable performance outcome helps explain why Essential oils remained the leading product type in the Africa feed phytogenics market in 2025. Key active molecules such as thymol, carvacrol, eugenol, and cinnamaldehyde offer antimicrobial, anti-inflammatory, and digestive-support effects that match the main needs of commercial poultry, ruminant, and aquaculture feed systems in Africa. Their strong availability through international suppliers and their compatibility with pelleted feed and premix systems across South Africa, Egypt, and Nigeria have made them the most established phytogenic format in formal feed mill procurement. Trouw Nutrition's Fytera Perform, a microencapsulated blend of clove, cinnamon, and oregano essential oils validated across 6 independent commercial trials, also shows how the category is moving toward stronger active-level standardization and performance documentation rather than simple botanical labeling. Other phytogenics, including oleoresins, saponins, tannins, and flavonoids, account for the rest of the product mix and are gaining more relevance in niche aquaculture uses and in ruminant feeding programs, especially in Egypt and emerging East African markets.

Herbs and spices reflects the wide local availability of botanicals such as thyme, garlic, rosemary, and lemongrass across East and West Africa. Kenyan research institutions have published peer-reviewed findings on garlic allicin as an antibiotic alternative in broilers, while regional studies on West African pepper and bay leaf have shown positive blood and immune responses in broiler production without reducing meat quality. NOR-FEED, now part of Adisseo, also published evidence in 2025 showing that Nor-Spice AB, a standardized citrus extract containing citroflavonoids and pectic oligosaccharides, improved broiler growth performance, gut health, and carcass quality. This matters because many of the botanical raw materials used in Herbs and spices phytogenics are already cultivated in Kenya, Ethiopia, Tanzania, and Nigeria, which opens the possibility for more region-specific pricing strategies. The growth also reflects how closely this category lines up with antimicrobial resistance policy priorities in countries such as Nigeria and Ethiopia, where herb-derived actives are increasingly seen as credible antibiotic alternatives.

By Animal Type: Aquaculture Emerges as the Fastest-Growing End Segment

Poultry held an estimated 49.1% share of the African feed phytogenics market in 2025, reflecting its dominant role in commercial compounded feed across South Africa, Nigeria, and Egypt. It also remains the main entry point for phytogenic adoption across the continent. Broilers are the leading poultry sub-segment. According to the USDA (United States Department of Agriculture), South Africa's poultry meat output is forecast to reach 1.68 million metric tons in 2026 as the sector continues to recover from the 2023 Highly Pathogenic Avian Influenza (HPAI) cycle, while Nigeria accounts for 24.9% of Africa's commercial poultry volume. The Animal Feed Manufacturers Association's 2025 inclusion of phytogenic feed additives as a symposium topic also points to South Africa's readiness to move from trials to more structured use in broiler systems, especially for essential oil-based products focused on feed conversion and gut health. Layers form the second poultry sub-segment, where commercial integrators in South Africa and Egypt monitor feed conversion on an egg-per-feed-unit basis, creating a separate use case for Herbs and spices-derived products aimed at reproductive efficiency and shell quality. Other poultry birds remain a smaller sub-segment at the current stage of commercial development, while ruminants, including beef cattle, dairy cattle, and other ruminants, remain less penetrated because local evidence is still limited, and pasture-based systems reduce formal additive use compared with poultry.

Aquaculture is the fastest-growing animal type, projected to expand at a 7.4% CAGR from 2026 to 2031. This growth is mainly linked to Egypt's leading role in African aquaculture, where it accounts for 67% of total continental output and supports a sector valued at USD 3.5 billion as per FAO (Food and Agriculture Organization)[2]Source: United States Department of Agriculture Foreign Agricultural Service, “Egyptian Aquaculture Industry, 2025 Update,” United States Department of Agriculture Foreign Agricultural Service, apps.fas.usda.gov. The December 2024 reopening of Egyptian marine fish exports to European Union markets has also added residue-compliance pressure, which supports the use of certified phytogenic aquafeed additives in tilapia, mullet, and marine fish production systems. Shrimp and other aquaculture species are still smaller but are expanding, with saponins and tannins drawing more interest for their antiparasitic and gut-modulating roles in intensive systems across Egypt and selected East African markets. Swine remains concentrated in formal pig integration systems in South Africa, Ghana, and Kenya, where buying decisions still depend heavily on feed conversion economics, while Other animals remains an early-stage category as the formal feed sector gradually broadens beyond core commercial livestock.

Geography Analysis

South Africa accounted for 33% of the African feed phytogenics market in 2025, making it the largest market in the region. That position rests on a formal feed mill network, structured commercial livestock operations, and procurement standards that are stronger than in many other African countries. The United States Department of Agriculture Foreign Agricultural Service reported that South Africa’s poultry sector generated ZAR 65.8 billion, or USD 3.6 billion, in gross agricultural value in 2025. It also forecasts poultry meat production at 1.7 million metric tons in 2026, providing additive suppliers with a large and relatively stable feed demand base. The Animal Feed Manufacturers Association of South Africa adds an institutional layer that helps convert technical product evaluation into structured commercial adoption.

Egypt is the fastest-growing country market in the Africa feed phytogenics market, with a projected 6.5% CAGR during 2026-2031, supported by its large poultry industry and livestock sector valued at approximately EGP 100 billion (USD 2.0 billion) annually, according to Egypt's Ministry of Agriculture and Land Reclamation, alongside increasing adoption of antibiotic-free feeding programs and growing demand for natural feed performance enhancers. Morocco remains a smaller but relevant market because its formal poultry channels are gradually aligning more closely with residue and quality expectations linked to European trade norms.

Kenya is still an early-stage market for phytogenics, but its longer-term importance comes from East Africa’s growing commercial feed base and improving technical capability. Nigeria offers one of the largest upside cases because it has deep poultry demand, but realized adoption remains lower than potential due to price sensitivity, uneven service coverage, and more cautious purchasing behavior outside major feed hubs. The Africa feed phytogenics market in Ethiopia, Tanzania, Ghana, Ivory Coast, and other Rest of Africa countries is also shaped by gradual feed sector formalization rather than by sudden category expansion. Policy action on antimicrobial resistance in countries such as Ethiopia and practical broiler stewardship work in Zimbabwe indicate that more livestock systems are moving toward structured alternatives to indiscriminate antibiotic use. Over time, regional growth will depend on how quickly these secondary markets add the feed infrastructure, distribution reach, and technical support needed for reliable repeat use.

Competitive Landscape

The Africa feed phytogenics market remains moderately fragmented. Cargill, Incorporated, Kemin Industries, Inc., Archer-Daniels-Midland Company, Trouw Nutrition, and Phytobiotics Futterzusatzstoffe GmbH form the leading suppliers in the market. Competition is shaped less by scale alone and more by the ability to offer standardized actives, protected delivery systems, multi-species positioning, and credible local support. This structure means the Africa feed phytogenics market still offers room for share gains through technical differentiation rather than through price competition alone. It also means that supplier quality, validation discipline, and service depth matter as much as portfolio width in formal feed procurement.

Strategic moves over 2024 and 2025 show how suppliers are building those capabilities around the Africa feed phytogenics market. EW Nutrition GmbH acquired a majority stake in Green Innovation in March 2025, strengthening its position in phytogenic gut health solutions and adding formulation expertise relevant to poultry-led markets. Adisseo formally acquired NOR-FEED in October 2024, which expanded its access to standardized botanical solutions for animal feed. DSM-Firmenich opened an Animal Nutrition and Health manufacturing plant in Sadat City, Egypt, in September 2024, which strengthened regional supply infrastructure for specialty feed inputs. These moves matter because supply assurance and product consistency are central buying issues in this category.

The longer competitive question in the Africa feed phytogenics market is which suppliers can connect technology strength with locally relevant proof. Peer-reviewed evidence exists for essential oils, encapsulated blends, and stress-management applications, but buyers still want more local validation across species and production systems. This keeps the field open for suppliers that can back product claims with active-level documentation, species-specific inclusion guidance, and on-the-ground technical service. Aquaculture is one of the clearest white-space areas because Egypt’s feed scale is large, yet supplier differentiation in aquafeed-specific phytogenic programs is still less mature than in poultry. As the market develops, competitive advantage is anticipated to favor companies that can lower adoption friction without weakening product consistency or biological performance.

Africa Feed Phytogenics Industry Leaders

Kemin Industries, Inc.

Trouw Nutrition (Nutreco N.V.)

Phytobiotics Futterzusatzstoffe GmbH

Cargill, Incorporated

Archer-Daniels-Midland Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: EW Nutrition GmbH acquired a majority stake in Green Innovation, an Austrian producer of in-feed phytogenic gut health solutions, including the Activo and Activo Liquid essential oil-based product lines, adding documented phytogenic intellectual property and formulation expertise to its Africa-relevant multi-species gut health portfolio.

- December 2024: Egypt's National Food Safety Authority (NFSA) announced the reopening of Egyptian marine fish exports to EU countries after a three-year suspension, creating a pull for residue-compliant certified phytogenic aquafeed additives across Egypt's tilapia, mullet, and marine fish production systems.

- September 2024: DSM-Firmenich opened a new Animal Nutrition and Health premix and additives manufacturing plant in Sadat City, Egypt, to serve customers in Egypt, the Middle East, Southern Europe, and Africa, strengthening regional supply chain infrastructure for specialty nutritional additives, including phytogenic-adjacent performance and health inputs.

Africa Feed Phytogenics Market Report Scope

Feed Phytogenics market reports provide strategic analysis of plant-derived feed additives (essential oils, herbs, and spices) used to replace antibiotic growth promoters and improve livestock gut health. The Africa feed phytogenics market is segmented by product type (essential oils, herbs & spices, and other phytogenics), by animal type (poultry, ruminants, swine, aquaculture, and other animals), and by geography (South Africa, Egypt, Morocco, Nigeria, Kenya, and Rest of Africa). The market forecasts are provided in terms of value (USD) and volume (metric tons).

| Essential Oils |

| Herbs & Spices |

| Other Phytogenics |

| Aquaculture | Fish |

| Shrimp | |

| Other Aquaculture Species | |

| Poultry | Broiler |

| Layer | |

| Other Poultry Birds | |

| Ruminants | Beef Cattle |

| Dairy Cattle | |

| Other Ruminants | |

| Swine | |

| Other Animals |

| South Africa |

| Egypt |

| Morocco |

| Nigeria |

| Kenya |

| Rest of Africa |

| By Product Type | Essential Oils | |

| Herbs & Spices | ||

| Other Phytogenics | ||

| By Animal Type | Aquaculture | Fish |

| Shrimp | ||

| Other Aquaculture Species | ||

| Poultry | Broiler | |

| Layer | ||

| Other Poultry Birds | ||

| Ruminants | Beef Cattle | |

| Dairy Cattle | ||

| Other Ruminants | ||

| Swine | ||

| Other Animals | ||

| By Geography | South Africa | |

| Egypt | ||

| Morocco | ||

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the Africa feed phytogenics market by 2031?

The Africa feed phytogenics market is forecast to reach USD 10.1 million by 2031 from USD 7.8 million in 2026.

Which animal segment is driving the fastest demand growth in Africa?

Aquaculture is the fastest animal type segment with a projected 7.4% CAGR during 2026-2031, led by Egypt’s large fish feed base.

Which product type leads phytogenic demand in African feed formulations?

Essential oils are the largest product type with 55% share in 2025.

Why is South Africa the largest country market for feed phytogenics in Africa?

South Africa led with 33% share in 2025 because it has a formal feed mill base, strong poultry production, and more structured product evaluation in the feed sector.

Page last updated on: