Africa Feed Acidifiers Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

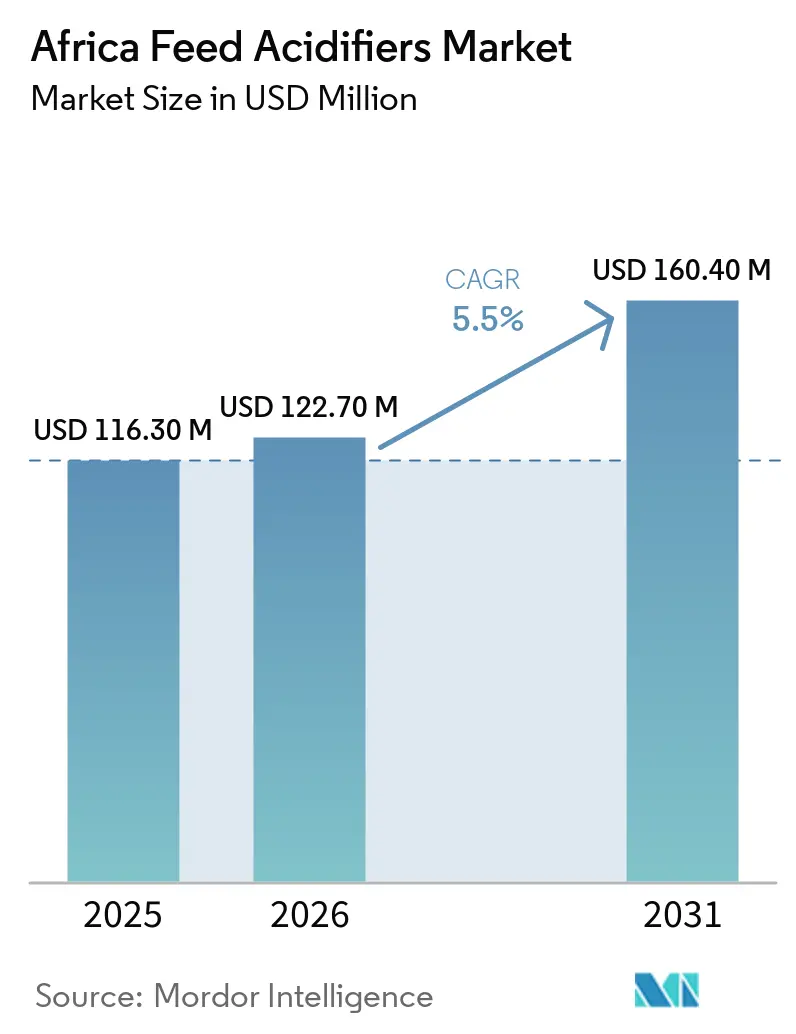

| Base Year Market Size (2025) | USD 116.30 Million |

| Market Size (2026) | USD 122.70 Million |

| Market Size (2031) | USD 160.40 Million |

| Growth Rate (2026 - 2031) | 5.50% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Feed Acidifiers Market Analysis by Mordor Intelligence

The Africa feed acidifiers market size is projected to grow from USD 116.3 million in 2025 to USD 122.7 million in 2026 and is forecasted to reach USD 160.4 million by 2031 at 5.5% CAGR over 2026-2031. The African feed acidifiers market is shaped by hot, humid storage conditions, which increase the risk of mold, bacterial growth, and feed spoilage across many production zones on the continent. Commercial poultry farming is also moving toward a more formal, scaled-up model, underscoring the need for stable feed hygiene, gut health support, and pathogen control inputs as production systems become denser and more standardized. Feed remains the largest cost item in intensive livestock systems, and the Food and Agriculture Organization of the United Nations and the Organization for Economic Co-operation and Development (OECD-FAO) noted that feed accounts for 60% to 80% of total production costs[1]Source: Organization for Economic Co-operation and Development and Food and Agriculture Organization, “OECD-FAO Agricultural Outlook 2023-2032,” OECD Publishing, oecd.org, so even small gains in feed efficiency can carry visible value for producers. The Africa feed acidifiers market is also benefiting from stronger pressure to reduce reliance on antibiotic growth promoters, especially among producers that want to align with export standards and stricter food safety expectations. Competition is broad rather than tightly concentrated, and supplier strategy is moving toward local manufacturing, regional blending, and technical support, while exposure to imported raw materials and disease-led feed demand swings remain the main near-term constraints for the Africa feed acidifiers market.

Key Report Takeaways

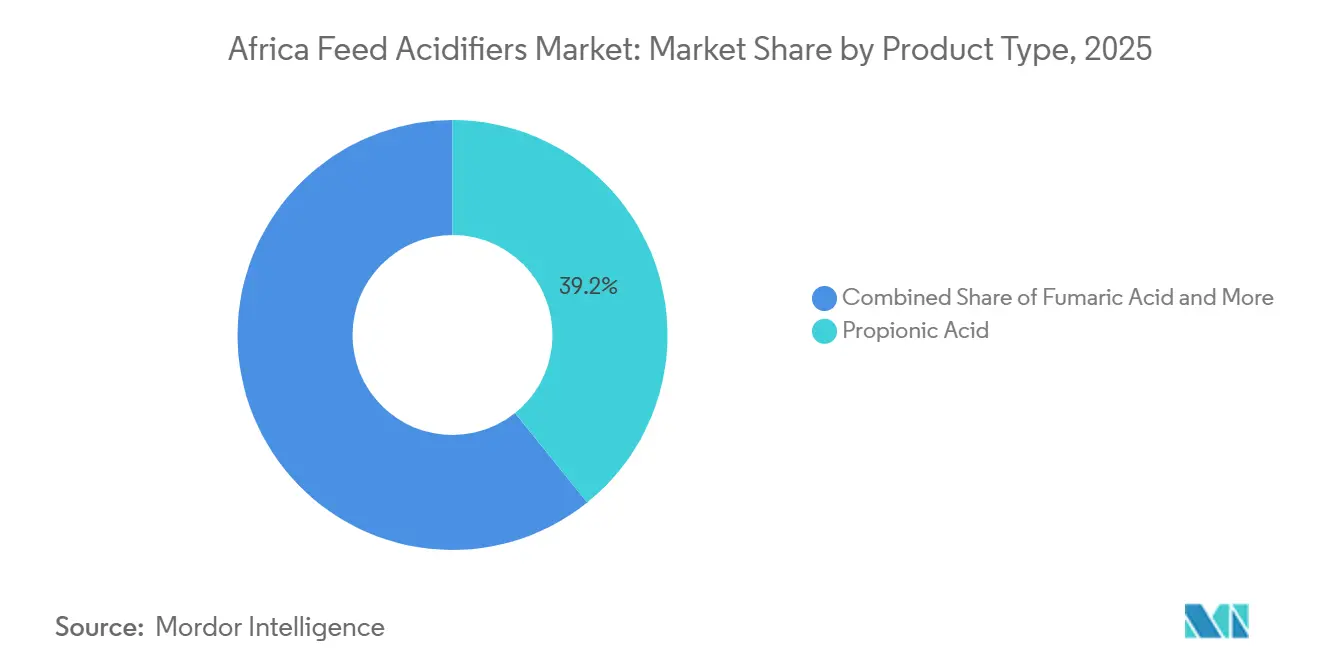

- In the Africa feed acidifiers market, by product type, the largest segment in 2025 was propionic acid with a 39.2% share, while the fastest-growing segment was fumaric acid with a projected 7.8% CAGR during 2026-2031.

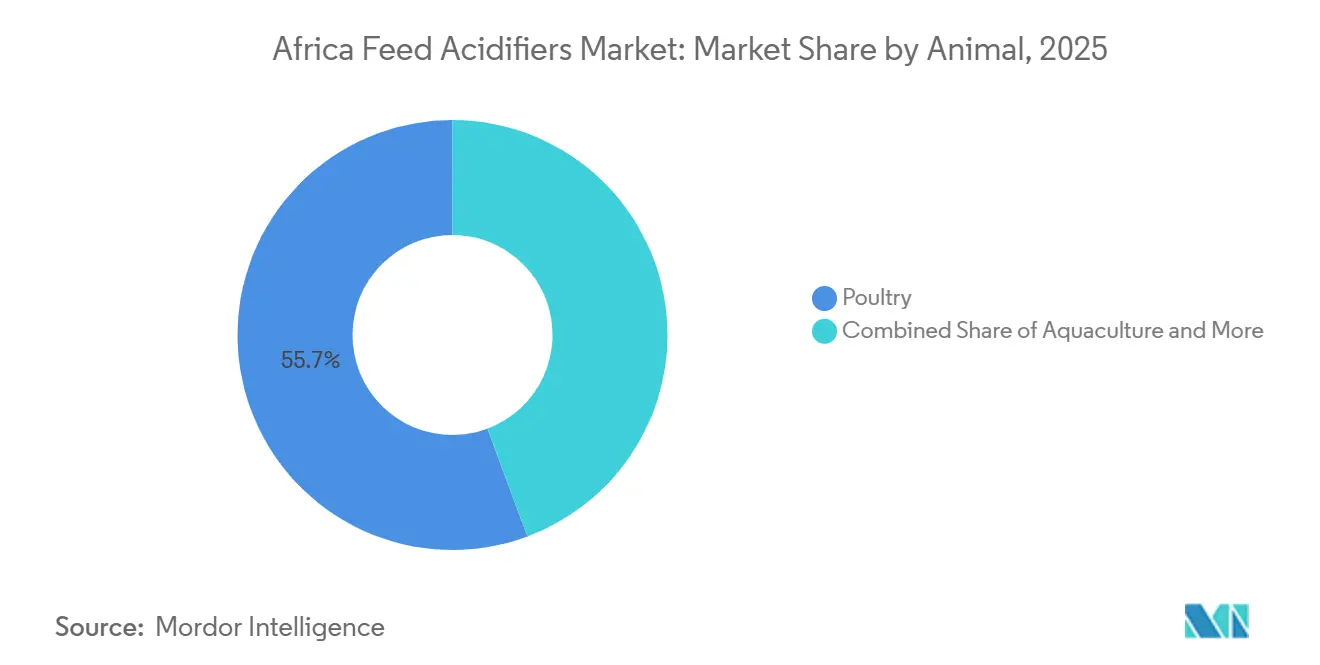

- Africa feed acidifiers market share, by livestock, was led by poultry with a 55.7% share in 2025, while aquaculture was the fastest-growing segment, registering a CAGR of 8.6% during 2026-2031.

- By geography, South Africa accounted for the largest share of the Africa feed acidifiers market size in 2025, with 46.3%, while Nigeria was the fastest-growing segment, registering a CAGR of 7.4% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Africa Feed Acidifiers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Need for Feed Hygiene in Hot and Humid Storage Conditions | +1.4% | Broad relevance across Africa, with stronger intensity in Sub-Saharan Africa, West Africa, and equatorial zones | Short term (≤ 2 years) |

| Expansion of Commercial Poultry Production Across Africa | +1.6% | Nigeria, Egypt, South Africa, Kenya, with spillover into Ghana and Côte d’Ivoire | Medium term (2-4 years) |

| Greater Focus on Feed Conversion Efficiency Under High Feed Cost Pressure | +0.8% | Nigeria, Kenya, and other import-dependent feed systems | Short term (≤ 2 years) |

| Increasing Adoption of Non-Antibiotic Feed Additives in Livestock Nutrition | +0.9% | South Africa, Egypt, and export-oriented producers across Africa | Medium term (2-4 years) |

| Rising Demand for Pathogen Control in Feed and Drinking Water Systems | +0.7% | South Africa, Nigeria, Kenya, and Egypt | Short term (≤ 2 years) |

| Growing Use of Acidifiers to Improve Local Ingredient Digestibility | +0.6% | Nigeria, Kenya, and other markets using lower-quality local inputs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Need for Feed Hygiene in Hot and Humid Storage Conditions

The African feed acidifiers market is closely tied to climate, as much of the continent operates under tropical and subtropical conditions that accelerate microbial growth in stored feed. High ambient temperatures and elevated humidity can quickly reduce feed stability, especially when storage discipline is weak and transport times are long. Scientific work published in 2024 in Agriculture showed that formic acid and propionic acid can reduce Salmonella load in contaminated compound feed, giving acidifiers a dual role in preservation and pathogen management. BASF SE also positions propionic acids, such as Lupro-Cid, for high-temperature and high-moisture conditions, including buffered formats that improve handling safety for feed mills. This combination of climate stress, microbial risk, and product functionality gives the Africa feed acidifiers market a stable demand base that is less dependent on short-term producer sentiment than many other feed additive categories.

Expansion of Commercial Poultry Production Across Africa

Commercial poultry expansion continues to support demand for feed acidifiers across Africa, as larger flocks require consistent feed quality and stronger disease control. The Organization for Economic Co-operation and Development and the Food and Agriculture Organization of the United Nations (OECD-FAO) projected African poultry meat output to rise from 6.7 million metric tons in 2020-2022 to 8.7 million metric tons by 2032, suggesting a larger long-term feed base for additive use. According to the United States Department of Agriculture (USDA), South Africa had already restored weekly poultry processing capacity to 22.6 million birds by July 2024, up from 19 million in 2023, demonstrating how quickly commercial systems can rebuild and resume feed demand. Nigeria also endorsed a livestock reform agenda in 2025 and linked feed and fodder development to broader sector modernization. As commercial density rises, demand becomes increasingly influenced by structured procurement from integrated producers rather than by irregular buying cycles in smallholder channels.

Increasing Adoption of Non-Antibiotic Feed Additives in Livestock Nutrition

The shift toward non-antibiotic production systems in livestock nutrition is creating additional support for feed acidifier adoption across Africa. A 2025 review of antibiotic regulation across 31 African countries found that only 8 had laws banning antibiotics as growth promoters, indicating that regulatory practice remains uneven across the continent. Even so, producers supplying export channels or formal retail buyers are moving ahead of regulation to meet residue, audit, and food safety requirements. Scientific work published in 2025 in Animals found that fumaric acid can improve fermentation efficiency and reduce methane emissions in ruminant systems, supporting the role of organic acids as practical alternatives to older antibiotic-led approaches in some feed programs. As a result, demand is increasingly driven not only by rising feed volumes but also by gradual changes in how larger producers manage performance, compliance, and brand risk.

Rising Demand for Pathogen Control in Feed and Drinking Water Systems

The role of feed acidifiers is expanding beyond basic shelf-life management toward active pathogen control in feed and water systems. Research published in Agriculture during 2024 confirmed that formic acid and propionic acid can reduce Salmonella in contaminated feed, while work published in 2025 in Frontiers in Veterinary Science showed that multi-component organic acid systems support broader gut health and microbial control outcomes. This is particularly important in African poultry operations, where dense flocks can magnify the financial impact of contamination events. In 2025, Kemin Industries developed PROSIDIUM for feed sanitization applications in South Africa, using a peroxypropionic acid and organic acid system designed to control Salmonella and E. coli through multiple action pathways. As integrated producers implement stricter HACCP-aligned feed safety practices, feed acidifiers are increasingly established in routine operations rather than used only for occasional corrective treatment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Price Tolerance Among Small and Mid-Sized Feed Manufacturers | -0.50% | Nigeria, Kenya, and other semi-formal mill networks | Medium term (2-4 years) |

| Uneven Technical Awareness of Inclusion Rates and Product Selection | -0.30% | Landlocked Sub-Saharan markets and semi-commercial farm operators | Long term (≥ 4 years) |

| Fragmented Distribution and Limited Storage Discipline in Some Markets | -0.40% | Several Sub-Saharan African markets with weak warehousing and fragmented channels | Medium term (2-4 years) |

| Volatile Availability and Cost of Imported Raw Materials | -0.40% | Nigeria, Kenya, South Africa, and other import-dependent buyers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Price Tolerance Among Small and Mid-Sized Feed Manufacturers

The Africa feed acidifiers market still faces a clear affordability barrier outside the most developed feed systems. Many mills outside South Africa and Egypt operate on a smaller scale, serve price-sensitive farmer networks, and have little room to pass additional costs through to customers. In Nigeria, layer feed trades at NGN 15,000 to NGN 17,000 per 25 kg bag, equivalent to approximately USD 10 to USD 11, according to The Guardian Nigeria (February 2026), and the Poultry Association of Nigeria is urging millers to lower prices in line with softer grain costs rather than add new cost layers. That kind of pricing pressure makes it harder to adopt acidifiers when buyers still view these products as optional rather than essential. Over time, formal quality rules such as Uganda’s Animal Feeds Act 2024 can help shift the Africa feed acidifiers market from a discretionary purchase model toward a minimum compliance model, but that transition is still uneven across many countries.

Volatile Availability and Cost of Imported Raw Materials

Heavy reliance on imported supply chains for propionic acid and formic acid also constrains the market. These inputs are mainly produced in Europe, China, and North America, so African buyers face both international chemical price swings and local currency pressures simultaneously. BASF SE raised formic acid prices in Europe by EUR 250 per metric ton, or USD 275, in March 2026, underscoring how upstream cost shifts can quickly feed into customer pricing. Nigerian feed producers also highlighted in 2025 that naira weakness raised the landed cost of micro-ingredients well above global benchmarks, which limited reformulation flexibility. This creates a strong case for regional blending, shorter delivery chains, and local stocking models if suppliers want the market to deepen beyond the largest and most resilient feed hubs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Propionic Acid Leads but Specialty Acids Redefine Growth

Propionic acid was the largest product type, accounted for 39.2% of the Africa feed acidifiers market share in 2025. Its leading position reflects strong antifungal and antibacterial performance in grain storage, compound feed preservation, and silage use under warm storage conditions. The Africa feed acidifiers market has long favored this chemistry in South Africa’s commercial poultry systems, where suppliers offer buffered and easier-to-handle formulations for routine mill use. BASF SE supports this position through products such as Luprosil and Lupro-Cid, including combinations of propionic acid and formic acid designed for high-ambient-temperature storage and practical handling. Formic acid remained the next major product group, while lactic acid, acetic acid, sorbic acid, citric acid, and custom multi-acid blends served more specialized roles in gut pH control, drinking water treatment, preservation, and chelation support.

Fumaric acid was the fastest product type, with a projected 7.8% CAGR during 2026-2031 in the Africa feed acidifiers market. That profile is relevant for Kenya’s dairy systems and for South Africa’s feedlot operations, where producers are under pressure to improve performance with better input efficiency. The Africa feed acidifiers market is also seeing a wider shift from single-acid products to multi-acid systems that aim to combine feed hygiene, gut health, and handling safety in one formulation. Perstorp Holding AB highlighted this direction through technical guidance on esterified and heat-stable solutions, which supports the move toward more advanced blends in markets with tougher operating conditions.

By Animal: Poultry Anchors Volume While Aquaculture Posts the Fastest Expansion

Poultry was the largest livestock segment and accounted for 55.7% of the Africa feed acidifiers market in 2025. This reflects poultry’s position as the most commercialized livestock category on the continent and the one most closely linked to formal feed mills with standard additive programs. South Africa’s broiler sector alone consumed close to 4 million metric tons of feed annually, according to the United States Department of Agriculture (USDA), providing the Africa feed acidifiers market with a large and stable volume base within one of its most developed national systems. In poultry, acidifiers support feed hygiene, lower pathogen load, and improve gut conditions, which matters most in high-density broiler and layer operations. Swine and ruminant demand was lower, but acidifier use is still expanding in pig feeding, dairy systems, and feedlot operations, where producers want better nutrient use and more controlled digestive conditions.

The Africa feed acidifiers market size for aquaculture is projected to grow at the fastest pace, with an 8.6% CAGR during 2026-2031. This reflects the wider rise of commercial fish farming, especially in catfish and tilapia systems that need more reliable feed quality and water-linked health management. East Africa’s fish feed infrastructure is expanding quickly, and according to the FAO’s State of World Fisheries and Aquaculture 2024 recorded that local fish feed manufacturing capacity in Tanzania rose from 710 metric tons in 2021 to 3,455 metric tons in 2024, which shows how the regional supply base is maturing. As aquafeed manufacturing becomes more formal, acidifiers move from niche use into standard formulation practice because producers want better gut balance, survival, and feed conversion in pond and cage systems. Other livestock such as equine remain a smaller outlet, but the premium end of the South African commercial market is gradually opening room for specialty acidified feed and drinking water products.

Geography Analysis

South Africa held 46.3% of the Africa feed acidifiers market share in 2025 and remained the largest country market on the continent. Its lead reflects the deepest commercial feed infrastructure, the highest level of poultry integration, and a stronger installed base of modern feed mill operations than most other African countries. The United States Department of Agriculture (USDA) Foreign Agricultural Service projected South African chicken meat output at 1.68 million metric tons in 2026, up from 1.65 million metric tons in 2025[2]Source: USDA Foreign Agricultural Service, “Poultry and Products Annual, South Africa,” USDA Foreign Agricultural Service, apps.fas.usda.gov. Slaughter volumes growing from 19.7 million to 23 million birds per week between 2019 and 2026, and the sector ranking second globally on cost of production after Brazil, according to the Bureau for Food and Agricultural Policy (BFAP)[3]Source: Bureau for Food and Agricultural Policy, “Competitiveness Benchmark Report 2025,” Bureau for Food and Agricultural Policy, bfap.co.za. The United States Department of Agriculture stated that feed accounts for close to 70% of broiler production costs in South Africa, so preservation and efficiency additives retain value even when farm margins are under pressure. Egypt complements this picture by acting as a North African demand and distribution hub, and DSM-Firmenich’s 2024 manufacturing plant in Sadat City strengthened its role as a regional supply point for feed additives moving into Africa and the Middle East.

Nigeria projected to be the fastest country market and is projected to expand at a 7.4% CAGR during 2026-2031 in the Africa feed acidifiers market. The creation of a dedicated Federal Ministry of Livestock Development in 2024 and the April 2025 endorsement of the National Livestock Growth Acceleration Strategy show that feed and fodder development is moving into a higher policy priority position. Nigeria’s November 2024 agreement with JBS for a USD 2.5 billion investment across 6 commercial processing plants, including 3 poultry facilities, points to a larger formal livestock base over time. The country’s import dependence for micro-ingredients means that currency swings can both limit current demand and increase the case for local blending. Kenya remains a key East African market because its aquaculture and feed systems are becoming more formal, which opens more space for specialized acidifier use in fish feed and livestock feed programs.

The Rest of Africa remains an early-stage but important growth frontier for the Africa feed acidifiers market. Markets such as Côte d’Ivoire, Ghana, Uganda, Tanzania, and Zambia are moving from fragmented feed structures toward more formal quality systems, even if adoption remains uneven. Lohmann Breeders, drawing on Organisation for Economic Co-operation and Development and Food and Agriculture Organization of the United Nations projections (OECD-FAO), highlighted that poultry meat output in Sub-Saharan Africa is set for very strong long-term growth, which supports the structural case for feed quality additives. Uganda’s Animal Feeds Act 2024 added formal standards for additive categories, prohibited substances, laboratories, and labeling, which should gradually make entry conditions clearer for international suppliers in the Africa feed acidifiers market.

Competitive Landscape

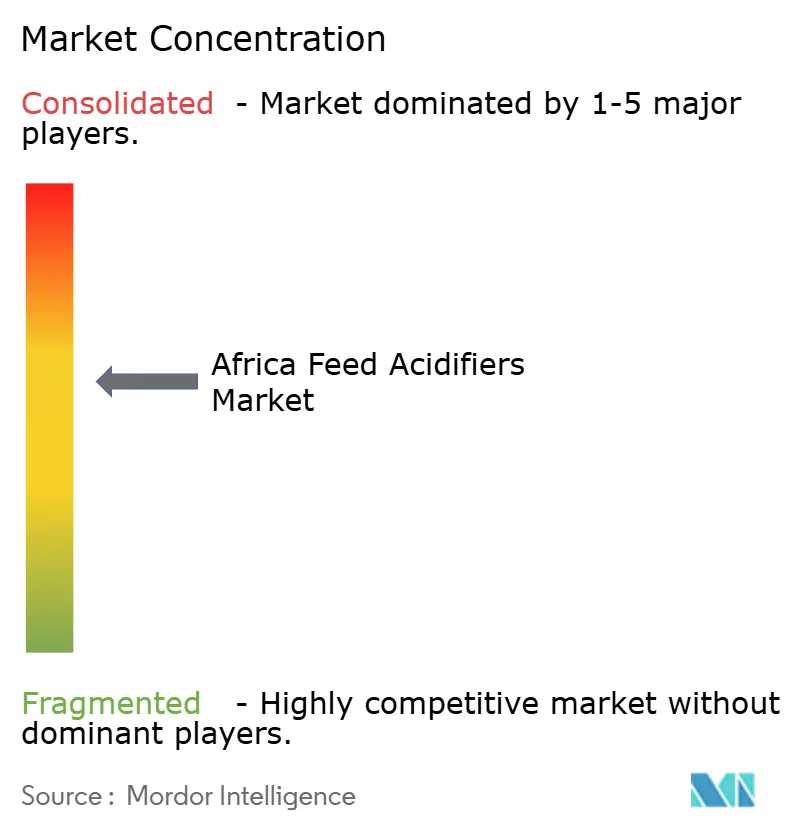

The Africa feed acidifiers market is moderately fragmented, with BASF SE, Cargill, Incorporated, DSM-Firmenich, Kemin Industries, Inc., and Nutreco (SHV Holdings) holding leading positions, while regional distributors and contract formulators still retain a meaningful share. One clear strategy is local manufacturing close to demand centers. Such moves show that competition in the Africa feed acidifiers market is being shaped as much by route-to-market design and technical support as by chemistry alone.

The Africa feed acidifiers market still offers clear white-space opportunities, especially in West and Central Africa where poultry volumes are rising faster than technical field coverage. In these regions, suppliers that invest early in local-language labeling, dosing guidance linked to local grain profiles, and distributor training can secure a stronger first commercial foothold. BASF SE has also supported its competitive position by pairing product supply with digital dosage guidance, which helps customers adjust preservation rates to actual storage and climate conditions. That kind of technical layer matters because many buyers are not only choosing a product, they are also choosing a supplier that can reduce trial-and-error in application. As a result, the Africa feed acidifiers market favors companies that can combine formulation depth, local service, and practical operating support rather than those competing on imported product alone.

Competitive execution is also being shaped by the risk profile of the Africa feed acidifiers market. Imported raw material exposure, foreign exchange volatility, and short-cycle feed demand swings after disease outbreaks all affect pricing, inventory, and customer planning. South Africa’s poultry system, for example, faced Highly Pathogenic Avian Influenza outbreaks in 2025, and such events can disrupt normal feed demand while also raising interest in stronger pathogen control once flocks are rebuilt. Export compliance pressure adds another layer because producers that want access to stricter markets need additive programs that are documented, repeatable, and easier to audit. This means the suppliers best placed in the Africa feed acidifiers market are those with strong regional footprints, registered portfolios, technical teams on the ground, and enough supply flexibility to manage both cost shocks and changing biosecurity needs.

Africa Feed Acidifiers Industry Leaders

BASF SE

Cargill, Incorporated

DSM-Firmenich

Kemin Industries, Inc.

Adisseo Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: BASF SE announced a EUR 250-per-metric-ton price increase for formic acid in Europe. Formic acid is a core input for feed and drinking water acidification to control pathogens and fungi, so this development is directly relevant to African buyers who depend on imported acidifier raw materials and finished solutions.

- March 2025: Kemin Industries, Inc. launched PROSIDIUM, a next-generation feed sanitizer based on peroxypropionic and organic acid chemistry, and regulatory approvals are underway in South Africa. This is highly specific to the Africa feed acidifiers market because it supports direct product entry into the region’s largest country market and strengthens the pathogen control segment.

- September 2024: DSM-Firmenich inaugurated its Animal Nutrition and Health premix and additives plant in Sadat City, Egypt, with an annual capacity of 10,000 metric tons, supplying vitamins, minerals, and organic acid-based feed additives across Africa, the Middle East, and Southern Europe. This is directly relevant to the Africa feed acidifiers market because regional production can reduce lead times and import dependence for acidifier supply in African feed markets.

Africa Feed Acidifiers Market Report Scope

Feed acidifiers are organic acid-based compounds that are added to animal feed to preserve quality, control pathogens, and improve digestibility. The Africa feed acidifiers market report is segmented by product type (propionic acid, formic acid, fumaric acid, and other acidifiers), by animal (poultry, swine, ruminants, aquaculture, and others), and by geography (South Africa, Egypt, Nigeria, Kenya, and the Rest of Africa). The market forecasts are provided in terms of value (USD) and volume (Metric Tons).

| Formic Acid |

| Propionic Acid |

| Lactic Acid |

| Other Organic Acidifiers |

| Aquaculture | Fish |

| Shrimp | |

| Other Aquaculture Species | |

| Poultry | Broiler |

| Layer | |

| Other Poultry Birds | |

| Ruminants | Beef Cattle |

| Dairy Cattle | |

| Other Ruminants | |

| Swine | |

| Other Animals |

| South Africa |

| Egypt |

| Nigeria |

| Kenya |

| Rest of Africa |

| By Product Type | Formic Acid | |

| Propionic Acid | ||

| Lactic Acid | ||

| Other Organic Acidifiers | ||

| By Animal | Aquaculture | Fish |

| Shrimp | ||

| Other Aquaculture Species | ||

| Poultry | Broiler | |

| Layer | ||

| Other Poultry Birds | ||

| Ruminants | Beef Cattle | |

| Dairy Cattle | ||

| Other Ruminants | ||

| Swine | ||

| Other Animals | ||

| By Country | South Africa | |

| Egypt | ||

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current outlook for feed acidifiers in Africa?

The Africa feed acidifiers market was valued at USD 116.3 million in 2025.

Which product category leads current demand?

Propionic acid was the largest product type with 39.2% share in 2025 because it is widely used for mold control, bacterial control, and feed preservation under warm storage conditions.

Which livestock category is expanding fastest?

Aquaculture is the fastest livestock segment, with an 8.6% CAGR during 2026-2031, supported by wider fish feed development and more formal aquafeed production across African markets.

Why is South Africa so important in this space?

South Africa held 46.3% share in 2025 because it has the deepest commercial poultry base, advanced feed mills, and strong investment in large-scale poultry operations.

Page last updated on: