Market Overview

| Study Period | 2021 - 2031 |

|---|---|

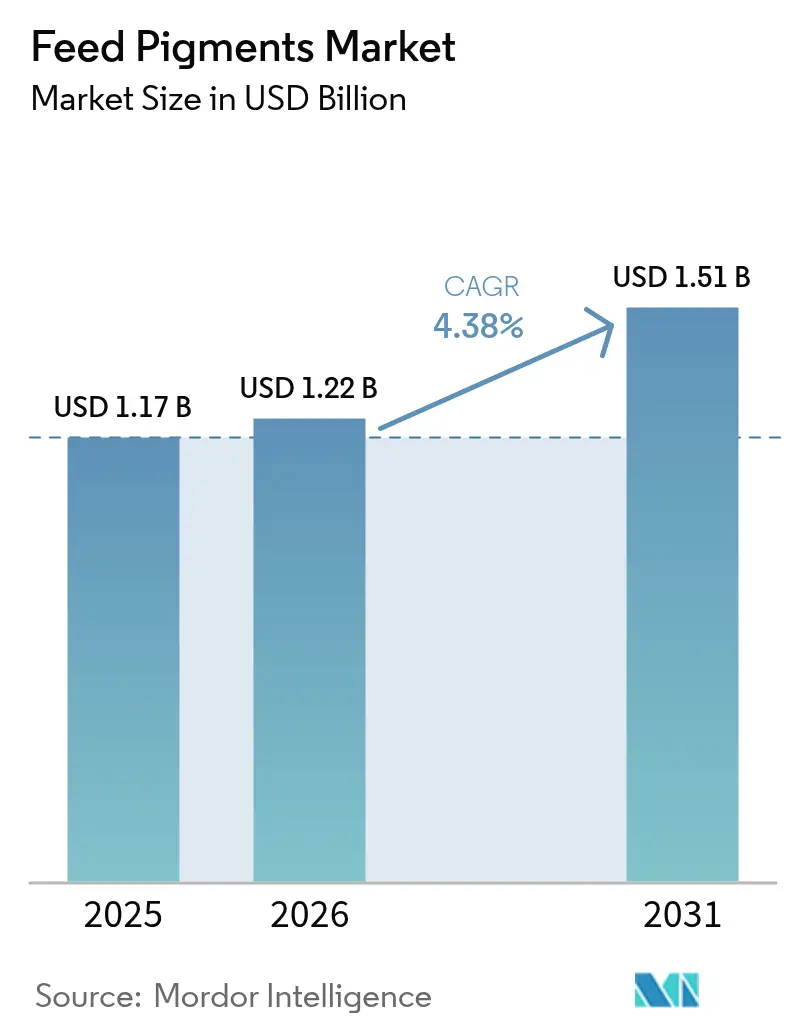

| Market Size (2026) | USD 1.22 Billion |

| Market Size (2031) | USD 1.51 Billion |

| Growth Rate (2026 - 2031) | 4.38% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Feed Pigments Market Analysis by Mordor Intelligence

The feed pigments market size is expected to grow from USD 1.17 billion in 2025 to USD 1.22 billion in 2026 and is forecast to reach USD 1.51 billion by 2031 at 4.38% CAGR over 2026-2031. Robust poultry and aquaculture expansion, coupled with consumer demand for naturally colored animal products, underpins this growth. Functional carotenoids that combine coloration and antioxidant activity are displacing synthetic dyes as regulators tighten antibiotic-growth-promoter bans. Bio-encapsulation technologies that improve pigment stability and uptake are lowering inclusion costs, while circular-economy sourcing options are gaining traction in regions that valorize agro-waste. Producers able to validate traceability and navigate lengthy approval processes remain competitively positioned.[1]Source: U.S. Food and Drug Administration, “Food Additive Petitions for Animal Food,” fda.gov

Key Report Takeaways

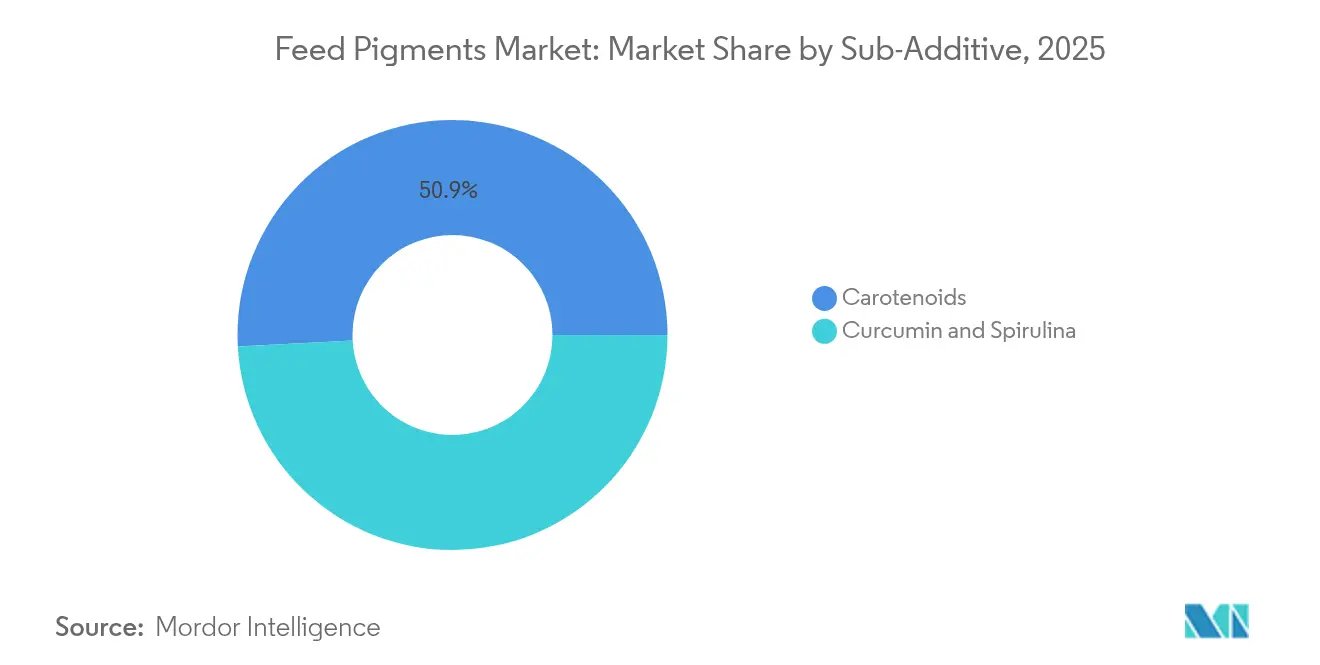

- By sub-additive, carotenoids led with 50.86% of the feed pigments market share in 2025, and are projected to expand at a 4.62% CAGR through 2031.

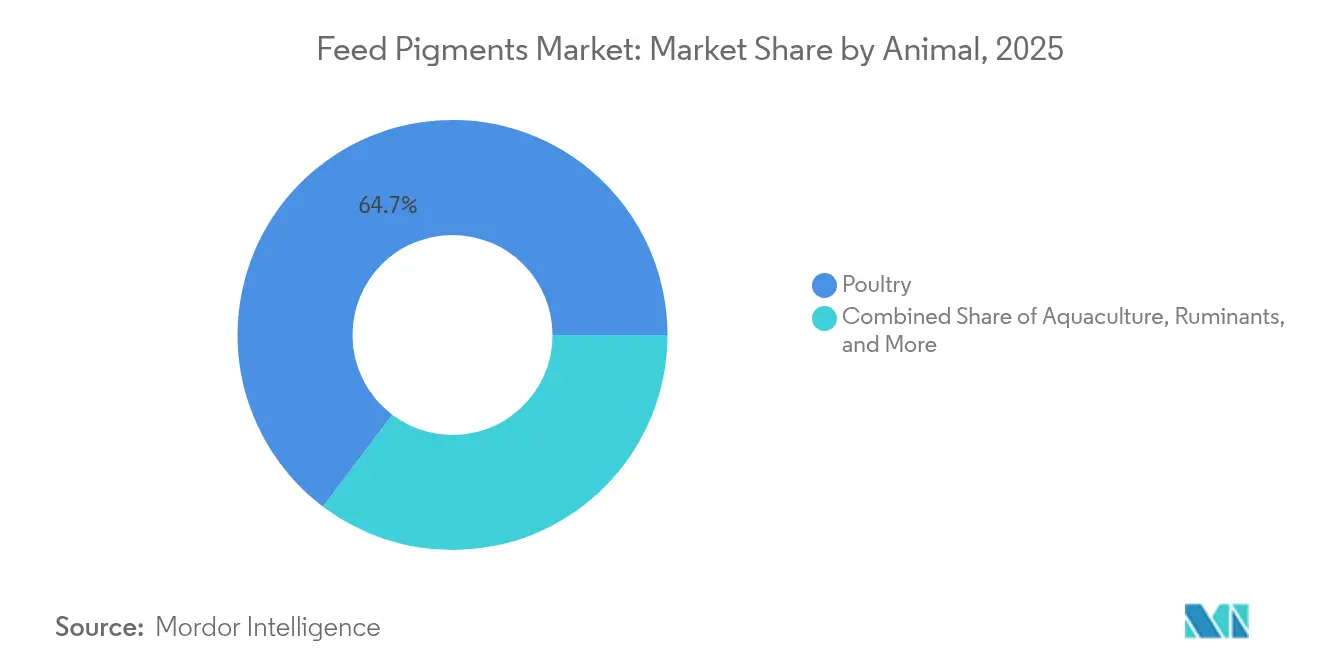

- By animal, poultry accounted for 64.72% of the feed pigments market size in 2025 and is tracking a 4.55% CAGR to 2031.

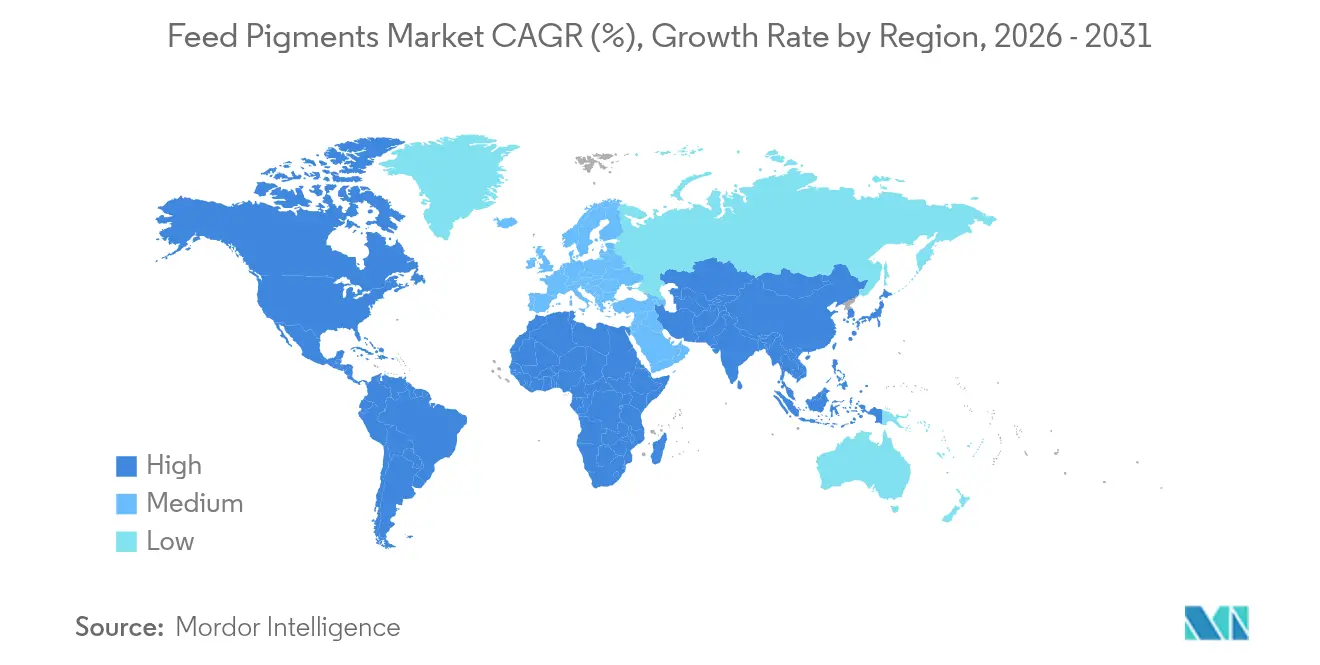

- By geography, Asia-Pacific held a 31.10% share of the feed pigments market in 2025, while North America is forecast to grow at a 5.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Feed Pigments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of global poultry and aquaculture industries | +1.8% | Asia-Pacific and South America | Medium term (2-4 years) |

| Rise in consumer demand for naturally pigmented animal products | +1.2% | North America and European Union | Long term (≥ 4 years) |

| Enforcement of antibiotic-growth-promoter bans that favor functional pigments | +0.9% | European Union and North America | Short term (≤ 2 years) |

| Increasing adoption of carotenoids for oxidative-stress mitigation in high-density farming | +0.6% | Global intensive farms | Medium term (2-4 years) |

| Bio-encapsulation technology lowering feed-conversion costs | +0.4% | North America and European Union | Long term (≥ 4 years) |

| Circular-economy sourcing of pigments from agro-waste streams | +0.3% | India, Brazil, and Southeast Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of global poultry and aquaculture industries

World poultry output hit new highs in 2025, while aquaculture now delivers more than half of global fish protein. Chinese growers alone produce over 60% of farmed seafood, driving strong demand for astaxanthin to achieve export-grade salmonid flesh color. Broiler and layer operations use carotenoids not only for visual appeal but also to reduce oxidative spoilage, extending shelf life under cold-chain constraints. Because ISO 22000 and HACCP audits emphasize ingredient traceability, integrators favor suppliers that certify natural pigment origins. Many Asian producers add dedicated pigment premix lines to ensure uniform dosing across large-scale feed mills, a shift that keeps the feed pigments market on a steady uptrend.

Rise in consumer demand for naturally pigmented animal products

Consumers associate deeper egg-yolk and salmon hues with freshness and nutritional value, enabling premium mark-ups of 15–25% in U.S. retail channels. Similar behavior in Western Europe has spurred cage-free eggs that rely on higher natural carotenoid inclusion. Retailers now print color-fan indices on carton sides, nudging producers toward tighter pigmentation programs. The trend is spreading to upper-income segments in Southeast Asia, where quick-service restaurants specify target skin color scores for roasted chicken menus. These preferences give momentum to the feed pigments market, widening margins for integrators that can guarantee consistent color without synthetic dyes.

Enforcement of antibiotic-growth-promoter bans that favor functional pigments

The European Union's complete ban on antibiotic growth promoters, followed by similar restrictions in the United States and Canada, has prompted feed manufacturers to explore pigment sources with demonstrated immunomodulatory properties.[3]U.S. Food and Drug Administration. "FDA Letter to Industry: Industry Encouraged to Contact FDA Regarding Novel Animal Foods with Drug Claims." Functional pigments such as astaxanthin and phycocyanin help replace antibiotic performance gaps by boosting immunity and reducing gut inflammation. Large broiler complexes in Brazil now layer 40–60 mg/kg of protected astaxanthin to improve livability during hot-season cycles. Because regulators grant Generally Recognized as Safe status to several algal carotenoids, feed formulators view them as dual-purpose tools delivering both color and health support, thus reinforcing the growth trajectory of the feed pigments market.

Increasing adoption of carotenoids for oxidative-stress mitigation in high-density farming

Crowded housing and rapid turnover elevate free-radical loads, hampering growth and meat color retention. Controlled trials show 100 mg/kg astaxanthin reduces broiler malondialdehyde by 22% and improves breast color stability after cold storage. Shrimp ponds running 160 PL/m² observe lower post-harvest yellowness loss when feeds carry 70 mg/kg canthaxanthin. These dual benefits feed cost optimizers’ decision matrices, keeping carotenoids at the center of the feed pigments industry product pipelines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile prices of natural pigment raw materials | −1.1% | Import-dependent regions | Short term (≤ 2 years) |

| Lengthy and fragmented regulatory approval pathways | −0.8% | European Union and North America | Medium term (2-4 years) |

| Cross-pigment competitive absorption limiting dosage efficiency | −0.5% | Global multi-pigment blends | Medium term (2-4 years) |

| Micro-plastic contamination risk in algal biomass supply | −0.3% | Coastal aquaculture zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile prices of natural pigment raw materials

Crop-linked supplies face weather swings and geopolitical risk. Annatto seed quotations in Peru climbed 38% between 2024 and 2025 as El Niño cut yields, pressuring cost-plus contracts in Europe. Saffron-based crocin soared when transport insurance premiums spiked in the Persian Gulf. Because pigments often represent 8–10% of complete-feed cost, such volatility can erode margins and temper procurement enthusiasm, constraining the feed pigments market.

Lengthy and fragmented regulatory approval pathways

Securing EU feed-additive approval averages 3.5 years and USD 0.6 million per dossier, while parallel U.S. processes follow the FDA’s Animal Food Ingredient Consultation route now that the Association of American Feed Control Officials (AAFCO) MOU has lapsed. These disparate regimes force suppliers to duplicate toxicology and stability data, tying up capital and deterring startups. Larger incumbents turn their compliance scale into a competitive moat, but overall market velocity slows, delaying novel formulations that could accelerate the feed pigments market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub-Additive: Carotenoids Command Pigmentation Programs

Carotenoids accounted for 50.86% of the feed pigments market size in 2025 and are projected to log a 4.62% CAGR through 2031. Astaxanthin remains the costliest molecule yet delivers unmatched flesh-color scores for salmonids at 50–100 mg/kg inclusion, keeping it indispensable in high-value species. Beta-carotene supports yolk and skin hues in poultry, while canthaxanthin is gaining ground in shrimp grow-outs owing to its resilient orange tone. Spirulina-derived phycocyanin is penetrating niche broiler labels that market “blue-green” clean-label cues and leverage its immunomodulatory traits. Curcumin, although coloring at a lower intensity, appeals to premium layer houses positioning cage-free eggs with enhanced antioxidant profiles.

Advances in micro-encapsulation continue to raise carotenoid bioavailability, letting integrators trim dose rates and reinvest savings in health additives. Sustainability narratives are also reshaping procurement: growers increasingly favor vertically integrated suppliers that certify algae origin and renewable-energy use. Such attributes reinforce customer loyalty and insulate margins, strengthening long-term leadership of carotenoids within the feed pigments market.

By Animal: Poultry Remains Core Revenue Engine

Poultry held 64.72% of the feed pigments market share in 2025 and is projected to grow at a 4.55% CAGR through 2031, as global consumption of chicken and eggs continues to rise. Modern broiler complexes in the United States utilize multicolored cameras on processing lines to verify skin yellowness and adjust dosing in real-time, thereby minimizing downgrades. Layers increasingly adopt blended carotenoid premixes that ensure uniform yolk color even when raw-material supplies fluctuate. Spirulina and marigold swaps are common in Indian feed mills that seek price arbitrage without compromising fan-chart consistency.

Aquaculture, while smaller in current value, registers the fastest incremental demand. Salmon growers pay premiums for high-purity astaxanthin with low isomeric drift, and shrimp exporters in Vietnam switched to protected canthaxanthin beads to satisfy importers’ shell-color criteria. Swine and ruminant segments remain niche, protected lutein trials in dairy suggest future upside for milk-fat coloration, but commercial uptake remains tentative. Overall, animal-specific innovations amplify downstream differentiation and sustain a steady expansion path for the broader feed pigments market.

Geography Analysis

Asia-Pacific represented 31.10% of the feed pigments market size in 2025, anchored by China’s dominant aquaculture and India’s rapidly scaling poultry sectors. Chinese feed integrators increasingly lock in multi-year astaxanthin contracts to secure color grades demanded by EU retail buyers. India’s broiler companies deploy mobile lab vans that monitor yolk color scores across contract farms, ensuring brand uniformity despite dispersed production. Emerging hubs such as Vietnam and Indonesia are embracing cost-efficient spirulina blends to raise value-added export offerings, thereby diversifying regional pigment demand drivers.

North America exhibits the fastest regional expansion at a 5.12% CAGR to 2031, propelled by regulatory shifts that favor natural pigments over synthetic lakes. U.S. salmon farmers in Maine and Alaska leverage cold-water conditions to market premium color profiles, reinforcing demand for stabilized astaxanthin. Mexican integrators are upgrading premix facilities to include precision dosing modules, improving consistency amid rising quick-service restaurant requirements. Canada’s feed mills integrate blockchain tracking of carotenoid batches to satisfy both domestic and export audits, tightening supply-chain transparency.

Europe maintains stringent approval frameworks that privilege suppliers with extensive dossiers. While region-wide bans on synthetic dyes strengthen natural adoption, economic headwinds temper volume growth, pushing suppliers toward efficiency innovations and sustainability certifications to defend share. Pilot projects harness waste-stream lycopene in Spain, aligning with the European Green Deal’s circular-economy goals and signaling future procurement shifts. Collectively, these geographic dynamics shape multi-speed growth corridors that keep the global feed pigments market competitive yet opportunity-rich.

Competitive Landscape

The feed pigments market is loosely concentrated, with the top five suppliers, DSM-Firmenich, BASF, Bordas S.A., Synthite Industries Pvt. Ltd., and Nutrex, holding a combined 31% revenue share in 2024. This split shows that no single company exerts dominant control, giving mid-tier and regional specialists room to compete on niche formulations and price-service bundles.

DSM-Firmenich leads the group through its integrated algae cultivation and micro-encapsulation platform that supports major aquaculture contracts. BASF differentiates through regulatory agility, becoming the first to win the European Food Safety Authority (EFSA) clearance for an algae-derived beta-carotene poultry premix in December 2024. Synthite Industries uses its Kerala oleoresin complex, commissioned in July 2024, to secure marigold and paprika streams that back lutein and capsanthin lines, upgraded its Spanish annatto plant to ISO 22000, and added waste-heat recovery in September 2024, signaling cost discipline and sustainability focus. Nutrex partnered with Wageningen University to pilot nano-lipid carriers that raise astaxanthin uptake by 25% in shrimp feeds, positioning it as an innovation-driven challenger.

Price volatility in natural raw materials amplifies competition, pushing suppliers to hedge through vertical integration or multi-source procurement strategies. Technical service has become a decisive lever, with the leading five deploying on-farm color-scoring apps and live formulation support to lock in distributor loyalty. Sustainability metrics now appear in purchase tenders, rewarding companies that document carbon footprints and circular-economy pigment sourcing. Regional feed-mill consolidation pressures smaller pigment vendors while giving the top five a platform to negotiate multi-year agreements. At the same time, fast-growing niche producers targeting algae or spice waste streams can still capture share by undercutting price and offering localized logistics.

Feed Pigments Industry Leaders

-

DSM-firmenich

-

BASF

-

Synthite Industries Pvt. Ltd.

-

Nutrex

-

Bordas S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: DSM-Firmenich completed a USD 45 million astaxanthin capacity expansion in Norway, deploying advanced bio-encapsulation lines for higher pigment retention.

- December 2024: BASF won European Food Safety Authority clearance for its algae-based beta-carotene feed additive for poultry.

- November 2024: Kemin Industries bought Brazilian pigment maker Nutron for USD 85 million, establishing localized carotenoid production capacity.

Global Feed Pigments Market Report Scope

Carotenoids, Curcumin & Spirulina are covered as segments by Sub Additive. Aquaculture, Poultry, Ruminants, Swine are covered as segments by Animal. Africa, Asia-Pacific, Europe, Middle East, North America, South America are covered as segments by Region.

By Sub-Additive

| Carotenoids |

| Curcumin and Spirulina |

By Animal

| Aquaculture | Fish |

| Shrimp | |

| Other Aquaculture Species | |

| Poultry | Broiler |

| Layer | |

| Other Poultry Birds | |

| Ruminants | Beef Cattle |

| Dairy Cattle | |

| Other Ruminants | |

| Swine | |

| Other Animals |

By Geography

| Africa | Egypt |

| Kenya | |

| South Africa | |

| Rest of Africa | |

| Asia-Pacific | Australia |

| China | |

| India | |

| Indonesia | |

| Japan | |

| Philippines | |

| South Korea | |

| Thailand | |

| Vietnam | |

| Rest of Asia-Pacific | |

| Europe | France |

| Germany | |

| Italy | |

| Netherlands | |

| Russia | |

| Spain | |

| Turkey | |

| United Kingdom | |

| Rest of Europe | |

| Middle East | Iran |

| Saudi Arabia | |

| Rest of Middle East | |

| North America | Canada |

| Mexico | |

| United States | |

| Rest of North America | |

| South America | Argentina |

| Brazil | |

| Chile | |

| Rest of South America |

| By Sub-Additive | Carotenoids | |

| Curcumin and Spirulina | ||

| By Animal | Aquaculture | Fish |

| Shrimp | ||

| Other Aquaculture Species | ||

| Poultry | Broiler | |

| Layer | ||

| Other Poultry Birds | ||

| Ruminants | Beef Cattle | |

| Dairy Cattle | ||

| Other Ruminants | ||

| Swine | ||

| Other Animals | ||

| By Geography | Africa | Egypt |

| Kenya | ||

| South Africa | ||

| Rest of Africa | ||

| Asia-Pacific | Australia | |

| China | ||

| India | ||

| Indonesia | ||

| Japan | ||

| Philippines | ||

| South Korea | ||

| Thailand | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| Europe | France | |

| Germany | ||

| Italy | ||

| Netherlands | ||

| Russia | ||

| Spain | ||

| Turkey | ||

| United Kingdom | ||

| Rest of Europe | ||

| Middle East | Iran | |

| Saudi Arabia | ||

| Rest of Middle East | ||

| North America | Canada | |

| Mexico | ||

| United States | ||

| Rest of North America | ||

| South America | Argentina | |

| Brazil | ||

| Chile | ||

| Rest of South America | ||

Market Definition

- FUNCTIONS - For the study, feed additives are considered to be commercially manufactured products that are used to enhance characteristics such as weight gain, feed conversion ratio, and feed intake when fed in appropriate proportions.

- RESELLERS - Companies engaged in reselling feed additives without value addition have been excluded from the market scope, to avoid double counting.

- END CONSUMERS - Compound feed manufacturers are considered to be end-consumers in the market studied. The scope excludes farmers buying feed additives to be used directly as supplements or premixes.

- INTERNAL COMPANY CONSUMPTION - Companies engaged in the production of compound feed as well as the manufacturing of feed additives are part of the study. However, while estimating the market sizes, the internal consumption of feed additives by such companies has been excluded.

| Keyword | Definition |

|---|---|

| Feed additives | Feed additives are products used in animal nutrition for purposes of improving the quality of feed and the quality of food from animal origin, or to improve the animals’ performance and health. |

| Probiotics | Probiotics are microorganisms introduced into the body for their beneficial qualities. (It maintains or restores beneficial bacteria to the gut). |

| Antibiotics | Antibiotic is a drug that is specifically used to inhibit the growth of bacteria. |

| Prebiotics | A non-digestible food ingredient that promotes the growth of beneficial microorganisms in the intestines. |

| Antioxidants | Antioxidants are compounds that inhibit oxidation, a chemical reaction that produces free radicals. |

| Phytogenics | Phytogenics are a group of natural and non-antibiotic growth promoters derived from herbs, spices, essential oils, and oleoresins. |

| Vitamins | Vitamins are organic compounds, which are required for normal growth and maintenance of the body. |

| Metabolism | A chemical process that occurs within a living organism in order to maintain life. |

| Amino acids | Amino acids are the building blocks of proteins and play an important role in metabolic pathways. |

| Enzymes | Enzyme is a substance that acts as a catalyst to bring about a specific biochemical reaction. |

| Anti-microbial resistance | The ability of a microorganism to resist the effects of an antimicrobial agent. |

| Anti-microbial | Destroying or inhibiting the growth of microorganisms. |

| Osmotic balance | It is a process of maintaining salt and water balance across membranes within the body's fluids. |

| Bacteriocin | Bacteriocins are the toxins produced by bacteria to inhibit the growth of similar or closely related bacterial strains. |

| Biohydrogenation | It is a process that occurs in the rumen of an animal in which bacteria convert unsaturated fatty acids (USFA) to saturated fatty acids (SFA). |

| Oxidative rancidity | It is a reaction of fatty acids with oxygen, which generally causes unpleasant odors in animals. To prevent these, antioxidants were added. |

| Mycotoxicosis | Any condition or disease caused by fungal toxins, mainly due to contamination of animal feed with mycotoxins. |

| Mycotoxins | Mycotoxins are toxin compounds that are naturally produced by certain types of molds (fungi). |

| Feed Probiotics | Microbial feed supplements positively affect gastrointestinal microbial balance. |

| Probiotic yeast | Feed yeast (single-cell fungi) and other fungi used as probiotics. |

| Feed enzymes | They are used to supplement digestive enzymes in an animal’s stomach to break down food. Enzymes also ensure that meat and egg production is improved. |

| Mycotoxin detoxifiers | They are used to prevent fungal growth and to stop any harmful mold from being absorbed in the gut and blood. |

| Feed antibiotics | They are used both for the prevention and treatment of diseases but also for rapid growth and development. |

| Feed antioxidants | They are used to protect the deterioration of other feed nutrients in the feed such as fats, vitamins, pigments, and flavoring agents, thus providing nutrient security to the animals. |

| Feed phytogenics | Phytogenics are natural substances, added to livestock feed to promote growth, aid in digestion, and act as anti-microbial agents. |

| Feed vitamins | They are used to maintain the normal physiological function and normal growth and development of animals. |

| Feed flavors and sweetners | These flavors and sweeteners help to mask tastes and odors during changes in additives or medications and make them ideal for animal diets undergoing transition. |

| Feed acidifiers | Animal feed acidifiers are organic acids incorporated into the feed for nutritional or preservative purposes. Acidifiers enhance congestion and microbiological balance in the alimentary and digestive tracts of livestock. |

| Feed minerals | Feed minerals play an important role in the regular dietary requirements of animal feed. |

| Feed binders | Feed binders are the binding agents used in the manufacture of safe animal feed products. It enhances the taste of food and prolongs the storage period of the feed. |

| Key Terms | Abbreviation |

| LSDV | Lumpy Skin Disease Virus |

| ASF | African Swine Fever |

| GPA | Growth Promoter Antibiotics |

| NSP | Non-Starch Polysaccharides |

| PUFA | Polyunsaturated Fatty Acid |

| Afs | Aflatoxins |

| AGP | Antibiotic Growth Promoters |

| FAO | The Food And Agriculture Organization of the United Nations |

| USDA | The United States Department of Agriculture |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms