Africa Feed Flavors and Sweeteners Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

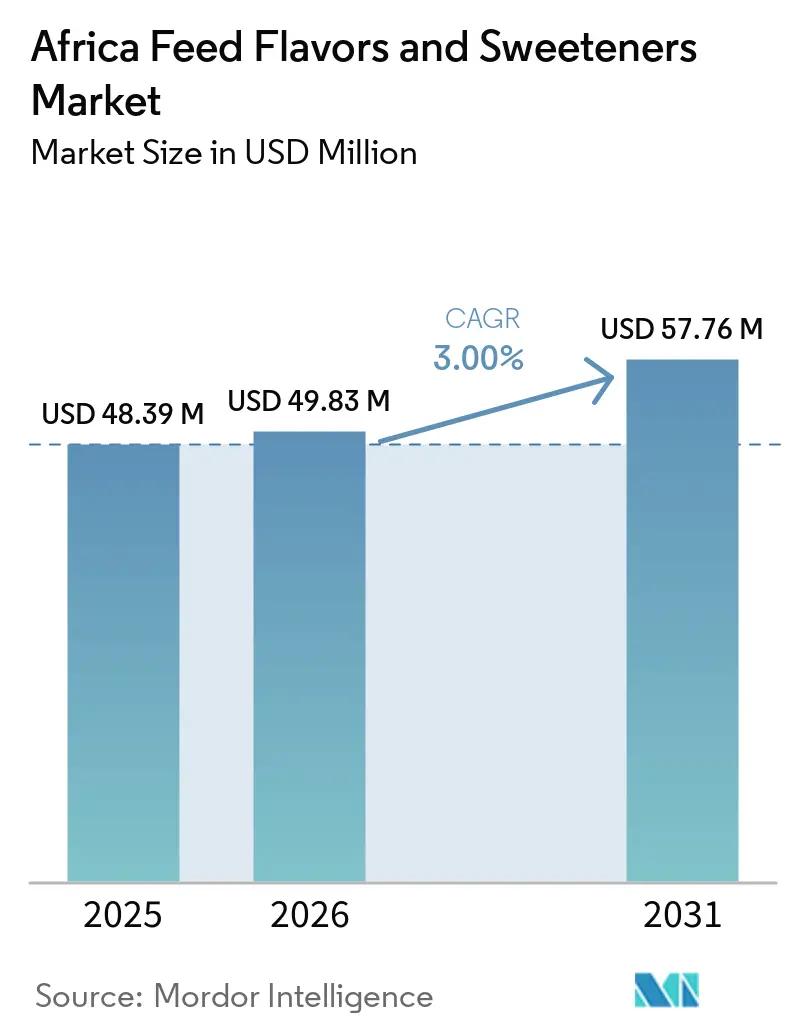

| Base Year Market Size (2025) | USD 48.39 Million |

| Market Size (2026) | USD 49.83 Million |

| Market Size (2031) | USD 57.76 Million |

| Growth Rate (2026 - 2031) | 3.00% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Feed Flavors and Sweeteners Market Analysis by Mordor Intelligence

The Africa feed flavors and sweeteners market was valued at USD 48.39 million in 2025 and is projected to grow from USD 49.83 million in 2026 to USD 57.76 million by 2031 at a CAGR of 3.0% from 2026 to 2031. The adoption of these flavors and sweeteners is most pronounced in regions where formal feed formulation practices are already in place. South Africa, Egypt, and Kenya dominate the commercial landscape, housing integrated feed mills, dairy operations, and poultry systems that demand standardized rations and consistent intake support. Heightened regulatory scrutiny surrounding antimicrobial resistance has amplified the significance of phytogenic palatants. Suppliers now tout these palatants not only as enhancers of feed acceptance but also as integral components of broader non-antibiotic nutrition initiatives. The African Continental Free Trade Area (AfCFTA) is set to reform cross-border trade, potentially easing access to premixes in inland markets. This is crucial for a category that heavily relies on organized distribution and technical backing. Furthermore, in East and Southern Africa, heat stress emerges as a significant concern. During sweltering periods, animals often shy away from feed, prompting formulators to bolster flavor support to counteract intake losses.

Key Report Takeaways

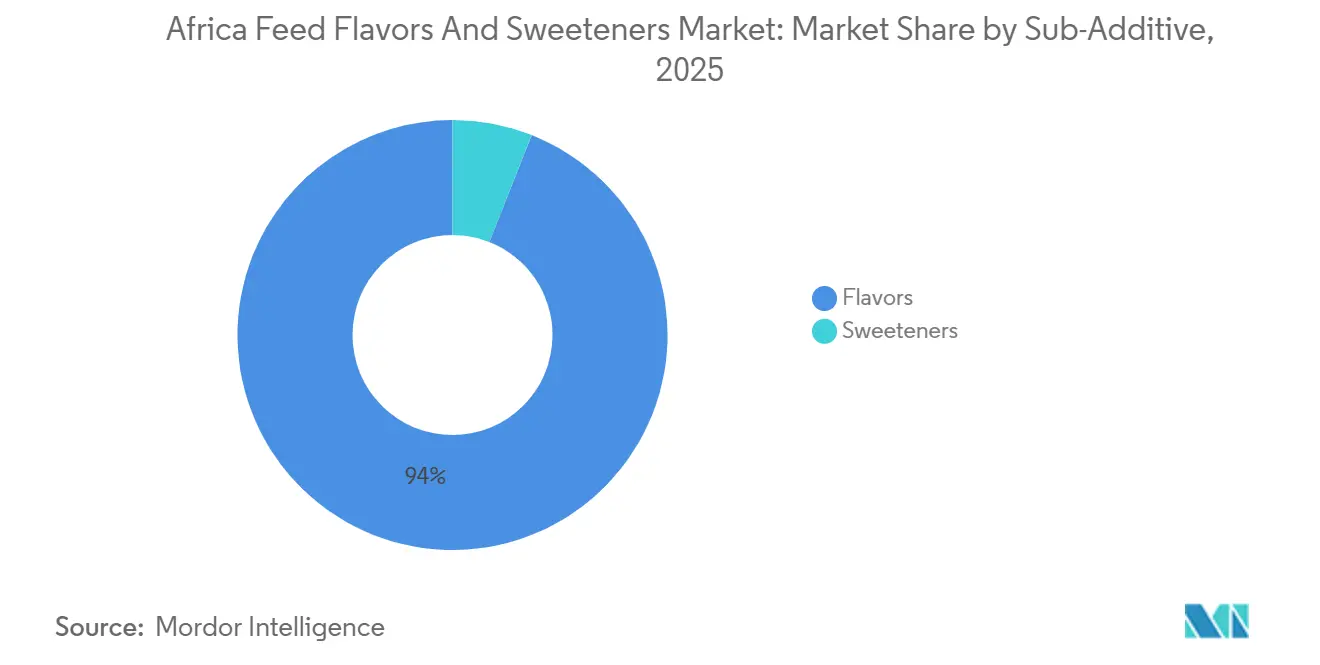

- By sub-additive, the Africa feed flavors and sweeteners market share for flavors was the largest 94.0% in 2025, while the Africa feed flavors and sweeteners market size for sweeteners is forecast to grow at the fastest CAGR of 3.0% from 2026 to 2031.

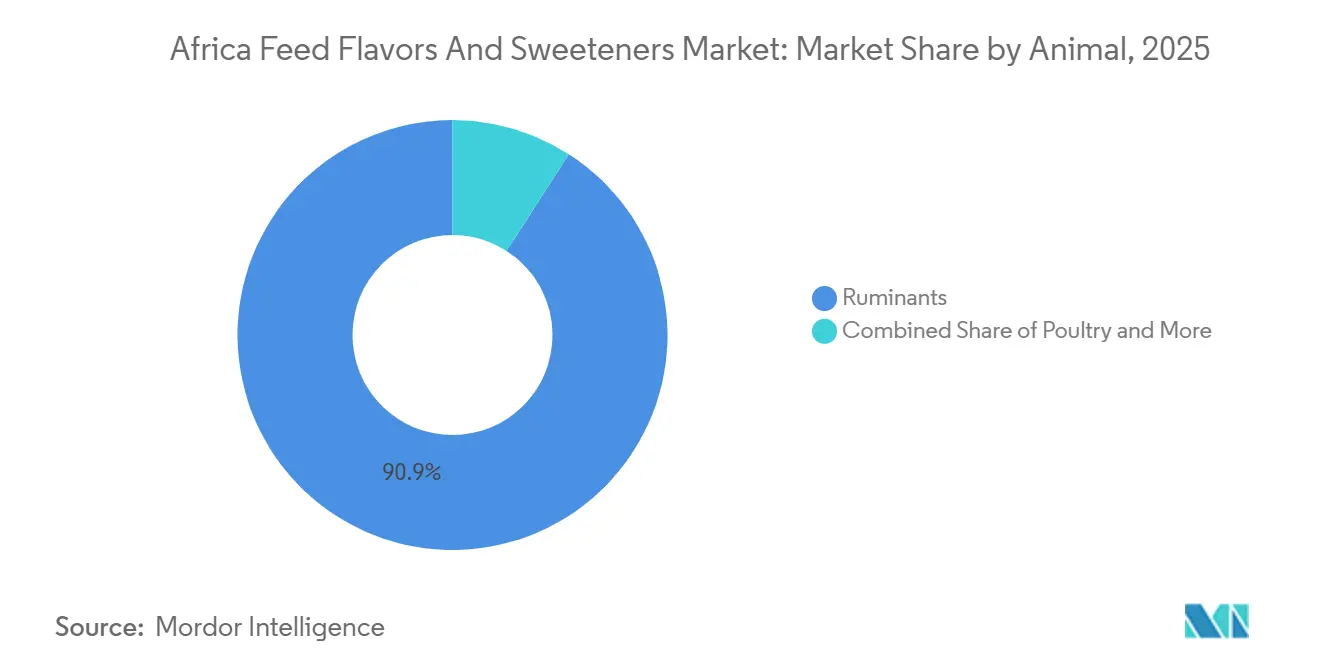

- By animal, ruminants accounted for the largest market share of 90.9% in 2025, while swine is projected to grow the fastest CAGR of 4.3% from 2026 to 2031.

- By geography, South Africa accounted for the largest 48.0% market share in 2025, and it is also projected to grow at the fastest CAGR of 3.4% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Africa Feed Flavors and Sweeteners Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Industrialization of poultry and dairy feed | +0.7% | South Africa, Egypt, Kenya, and Nigeria | Medium term (2-4 years) |

| Feed intake and conversion ratio optimization focus | +0.5% | Africa-wide, with concentration in South Africa and Egypt | Long term (≥ 4 years) |

| Replacement of antibiotic-led performance tools | +0.5% | Kenya, South Africa, Nigeria, and Rest of Africa | Medium term (2-4 years) |

| Natural and phytogenic palatability demand | +0.4% | South Africa, Kenya, and Rest of Africa | Long term (≥ 4 years) |

| Heat-stress intake stabilization needs | +0.3% | East Africa and Southern Africa, with spillover into West Africa | Short term (≤ 2 years) |

| African Continental Free Trade Area (AfCFTA)-led formal feed trade integration | +0.4% | Africa-wide, with early gains in Ethiopia, Zimbabwe, and West Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Industrialization of Poultry and Dairy Feed

As Africa's livestock feed production industrializes, particularly in poultry and dairy, the importance of palatability and feed intake management is rising. According to the United States Department of Agriculture (USDA) Foreign Agricultural Service (FAS) in 2025, poultry feed made up roughly 41% of Kenya's total compound feed output, with dairy feed close behind at 39%[1]Source: United States Department of Agriculture Foreign Agricultural Service, “Poultry and Products Situation – Kenya,” apps.fas.usda.gov.. This underscores the dominance of commercially formulated feed in Kenya's organized feed industry. With feed manufacturers increasingly adopting standardized compound feed for poultry and dairy, there's a growing demand for flavoring and sweetening additives. These additives are crucial for ensuring feed acceptance, promoting consistent intake, and enhancing the efficacy of pelleted and processed rations. This trend towards commercial feed manufacturing is expanding the market for feed flavors and sweeteners throughout Africa.

Feed Intake and Conversion Ratio Optimization Focus

As livestock producers in Africa prioritize feed intake and conversion efficiency to manage production costs, the market for feed flavors and sweeteners is witnessing a surge. The United States Department of Agriculture Foreign Agricultural Service highlights that by 2025, feed costs in Kenya could constitute a staggering 82% of the total expenses in chicken meat production, underscoring the pivotal role of feed performance in determining farm profitability. In light of this, there is a growing trend of integrating feed flavors and sweeteners into commercial formulations. These additives not only boost palatability but also promote steady feed consumption, especially in processed and pelleted diets. With producers on the lookout for solutions that enhance nutrient utilization and bolster production economics, the demand for feed flavors and sweeteners is poised for growth in Africa's commercial livestock sector.

Replacement of Antibiotic-Led Performance Tools

As the livestock industry in Africa pivots towards antibiotic alternatives, the market for feed flavors and sweeteners is reaping the benefits. According to a 2025 systematic review published in npj Antimicrobial Resistance, evidence of transmission of antibiotic-resistant bacteria between humans and livestock was identified across African production systems, reinforcing the need for more responsible antimicrobial use in animal agriculture. In their quest for alternatives to traditional antibiotic performance programs, producers are increasingly turning to feed additives that bolster both animal health and feed intake. By enhancing palatability and promoting regular consumption, feed flavors and sweeteners are playing a pivotal role in this shift towards non-antibiotic livestock production strategies across the continent.

Natural and Phytogenic Palatability Demand

Growing interest in natural and phytogenic feed additives, known to enhance animal performance and feed acceptance, is propelling the Africa feed flavors and sweeteners market. A 2025 review in Ruminants highlighted that natural feed additives in sub-Saharan Africa's ruminant systems boosted growth performance, feed efficiency, immune responses, and nitrogen outcomes. Such findings are motivating livestock producers to turn to plant-based solutions, especially flavors and sweeteners from herbs, spices, and botanical extracts. With commercial feed manufacturers increasingly adopting these natural ingredients in livestock diets, the demand for phytogenic flavoring and sweetening products is set to surge across Africa.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost-sensitive inclusion economics | -0.6% | Africa-wide, most acute in Rest of Africa and Kenya | Short term (≤ 2 years) |

| Substitute additives and flavor masking workarounds | -0.4% | Africa-wide, concentrated in informal and semi-commercial operations | Medium term (2-4 years) |

| FX-driven import cost inflation | -0.5% | Kenya, Nigeria, Ethiopia, and Rest of Africa | Short term (≤ 2 years) |

| Local sweetener and molasses supply unreliability | -0.3% | East Africa and Southern Africa, with spillover into West Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cost-Sensitive Inclusion Economics

The feed flavors and sweeteners market in Africa encounters challenges as livestock producers prioritize essential nutritional components over specialty additives in feed formulations due to cost considerations. According to the United States Department of Agriculture Foreign Agricultural Service (USDA FAS), Egypt's corn consumption reached 15.8 million metric tons in the 2025/26 marketing year, driven by a recovery in the poultry sector. With commercial livestock production requiring substantial feed grain inputs, a significant portion of feed budgets is allocated to core energy ingredients. This focus restricts the financial resources available for non-essential additives, limiting the adoption of feed flavors and sweeteners, particularly among producers aiming to control feed costs and sustain competitive production economics.

Substitute Additives and Flavor Masking Workarounds

In Africa, the feed flavors and sweeteners market grapples with competition from budget-friendly feed alternatives, which diminish the perceived necessity for specialized palatability additives. A 2025 review published in the International Journal of Veterinary Sciences and Animal Husbandry highlighted that livestock nutrition is increasingly turning to agro-industrial by-products, crop residues, insects, algae, and other locally sourced feed resources[2]Source: International Journal of Veterinary Sciences and Animal Husbandry, “Alternative Feed Ingredients in Poultry Diets,” veterinarypaper.com.. These alternatives not only cut down feed costs but also enhance feeding economics. Given their accessibility and cost-effectiveness compared to imported specialty additives, many livestock producers favor these alternatives over commercial flavoring and sweetening products. This trend, especially pronounced among cost-sensitive producers, curtails the adoption of feed flavors and sweeteners, thereby hindering market growth across the continent.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub-Additive: Flavor Dominance Masks a Structural Sweetener Opportunity

The Africa feed flavors and sweeteners market share for flavors accounted for the largest 94.0% in 2025, reflecting the strong preference for palatability enhancement solutions in the region’s livestock sector. The market dynamics are shaped by the prevalence of ruminant production systems, where feed flavors play a pivotal role in ensuring feed acceptance and consistent intake, regardless of forage and ration variations. Commercial feed manufacturers are increasingly infusing flavoring solutions into their compound feeds, aiming to boost product consistency and enhance animal performance. Demand is particularly pronounced in organized feed channels, emphasizing the significance of formulation precision and intake management for livestock productivity.

The Africa feed flavors and sweeteners market size for sweeteners is projected to grow at the fastest CAGR of 3.0% from 2026 to 2031, outpacing the more mature flavor segment as feed producers explore broader palatability strategies. The surge is bolstered by the rising commercialization of livestock production and heightened awareness regarding feed intake optimization, especially during challenging production phases. Sweeteners are carving a niche in young animal nutrition and specialized feed applications, where their role in enhancing feed acceptance can drive production efficiency. While their uptake lags behind flavors—primarily because many African livestock systems still emphasize fundamental nutritional needs—the gradual modernization of feed manufacturing is paving the way for deeper market penetration.

By Animal: Ruminant Dominance Masks Faster-Moving Growth in Swine

The Ruminants held the largest 90.9% of the market share in 2025, highlighting the importance of cattle, sheep, and goats within Africa’s livestock economy. The continent's robust ruminant population drives a significant appetite for feed additives, especially those enhancing feed acceptance and ensuring stable intake. Commercial rations frequently incorporate feed flavors to navigate dietary shifts and address variations in forage quality. This demand is most pronounced in organized dairy and beef sectors, where consistent feed consumption directly ties to productivity. Such a concentrated focus on specific species continues to influence market purchasing behaviors.

The Swine is forecast to grow at the fastest CAGR of 4.3% from 2026 to 2031, supported by the gradual expansion of commercial pork production in several African countries. Contemporary swine farms prioritize feed efficiency and nutritional oversight, paving the way for the integration of palatability-boosting additives. Sweeteners play a crucial role, especially in the early feeding stages, where their influence on feed acceptance can significantly impact growth. As producers lean more towards formulated feed strategies and structured practices, the demand for flavors and sweeteners in swine nutrition is set to surge from its current modest levels, driving the segment's rapid expansion.

Geography Analysis

South Africa accounted for the largest 48.0% market share in 2025 and is projected to grow at the fastest CAGR of 3.4% through 2031, maintaining its position as the region’s leading market. The country benefits from a highly developed commercial feed sector, integrated livestock production systems, and strong technical support from animal nutrition suppliers. Feed manufacturers increasingly focus on improving feed efficiency, intake consistency, and ration quality, creating favorable conditions for flavor and sweetener adoption. Commercial dairy, beef, poultry, and swine operations continue to drive demand for specialized feed additives as producers seek productivity improvements and more consistent animal performance.

Egypt and Kenya represent important growth centers due to their expanding commercial feed industries and increasing adoption of formulated livestock diets. Egypt's livestock sector benefits from large-scale poultry production and a structured feed manufacturing base that supports the use of value-added feed ingredients. Kenya provides a diversified demand profile through its strong dairy and poultry industries, where feed intake and ration consistency remain key management priorities. Both countries continue to witness improvements in feed manufacturing capabilities, creating opportunities for additive suppliers to expand product penetration through commercial feed channels and technical nutrition programs.

Rest of Africa continues to offer significant growth potential as commercial feed production expands beyond the region’s established livestock markets. Increasing investment in feed manufacturing infrastructure is improving access to formulated feed and supporting the modernization of livestock production systems across West and East Africa. In 2024, Nutreco N.V. (a subsidiary of SHV Holdings N.V.) inaugurated a state-of-the-art fish and poultry feed facility in Ibadan, Nigeria, under its brands Skretting and Trouw Nutrition. With an annual production capacity of 125,000 metric tons, this facility underscores the strengthening of organized feed supply chains. Such expansions bolster the adoption of cutting-edge animal nutrition solutions across Africa's emerging markets.

Competitive Landscape

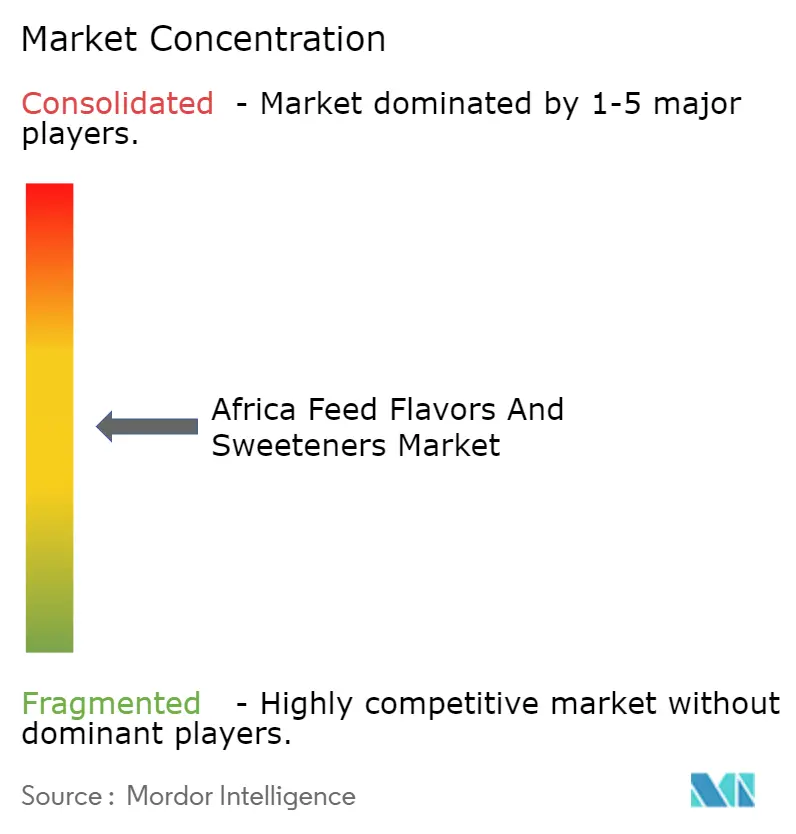

In Africa, the feed flavors and sweeteners market is moderately fragmented, with competition primarily among specialized feed additive manufacturers and animal nutrition firms. Key players such as Adisseo France SAS, Archer Daniels Midland Company, Kemin Industries, Inc., Norel, S.A., and Phytobiotics Futterzusatzstoffe GmbH vie for dominance, emphasizing product quality, formulation expertise, technical support, and robust customer relationships. The market prioritizes enhancing palatability, optimizing feed intake, and offering species-specific nutritional solutions. Suppliers distinguish themselves through their application knowledge and adaptability to the diverse livestock production systems found across African nations.

Technical support and proximity to the supply chain are pivotal, as feed manufacturers seek solutions tailored to local raw materials, climatic nuances, and specific livestock production systems. To bolster their regional presence, suppliers are making strides through manufacturing investments, forging distribution partnerships, and enhancing technical service capabilities. Companies boasting a diverse animal nutrition portfolio can leverage cross-selling opportunities, presenting flavors and sweeteners in tandem with enzymes, probiotics, vitamins, and other specialty feed ingredients. This holistic approach appeals to commercial feed mills, which prefer sourcing comprehensive nutritional solutions from fewer suppliers, thereby fortifying long-term relationships and amplifying market penetration.

Investments in regional manufacturing and animal nutrition infrastructure are reshaping competitive dynamics. In September 2024, dsm-firmenich AG inaugurated a state-of-the-art premix and additives facility for Animal Nutrition and Health in Sadat City, Egypt. With a robust annual production capacity of 10,000 metric tons, this facility bolsters dsm-firmenich's reach across Africa and its neighboring regions[3]Source: dsm-firmenich AG, “dsm-firmenich Opens Animal Nutrition and Health Manufacturing Plant in Egypt,” dsm-firmenich.com.. The strategic investment not only ensures reliable local supply but also amplifies technical support and responsiveness to the ever-evolving needs of customers. As the appetite for specialized feed additives surges, firms equipped with regional production assets, deep application expertise, and expansive distribution networks are poised to lead the market.

Africa Feed Flavors and Sweeteners Industry Leaders

Adisseo France SAS

Archer Daniels Midland Company

Kemin Industries, Inc.

Norel, S.A.

Phytobiotics Futterzusatzstoffe GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Archer Daniels Midland Company and Alltech, Inc. have inked a definitive agreement to form a joint venture focused on animal feed in North America. This collaboration bolsters their capabilities in animal nutrition and augments their expertise in feed formulation, paving the way for innovations in global feed additive markets, such as feed flavors and sweeteners.

- September 2024: DSM-Firmenich AG opened a new Animal Nutrition and Health manufacturing facility in Egypt with an annual capacity of 10,000 metric tons, strengthening regional production of specialty feed additives and enhancing the supply of palatability solutions, including feed flavors and sweeteners, across Africa.

Africa Feed Flavors and Sweeteners Market Report Scope

Feed flavors and sweeteners are specialty feed additives used to enhance the taste, aroma, and overall palatability of animal feed, encouraging consistent feed intake and reducing feed refusal. These additives boost feed acceptance across various livestock species, especially during dietary transitions, stressful conditions, or when incorporating less palatable ingredients into feed formulations. The Africa feed flavors and sweeteners market report is segmented by sub-additive (flavors and sweeteners), by animal (aquaculture, poultry, ruminants, swine, and other animals), and by geography (Egypt, Kenya, South Africa, and Rest of Africa). The market forecasts are provided in terms of value (USD) and volume (metric tons).

| Flavors |

| Sweeteners |

| Aquaculture | Fish |

| Shrimp | |

| Other Aquaculture Species | |

| Poultry | Broiler |

| Layer | |

| Other Poultry Birds | |

| Ruminants | Beef Cattle |

| Dairy Cattle | |

| Other Ruminants | |

| Swine | |

| Other Animals |

| Egypt |

| Kenya |

| South Africa |

| Rest of Africa |

| By Sub-Additive | Flavors | |

| Sweeteners | ||

| By Animal | Aquaculture | Fish |

| Shrimp | ||

| Other Aquaculture Species | ||

| Poultry | Broiler | |

| Layer | ||

| Other Poultry Birds | ||

| Ruminants | Beef Cattle | |

| Dairy Cattle | ||

| Other Ruminants | ||

| Swine | ||

| Other Animals | ||

| By Geography | Egypt | |

| Kenya | ||

| South Africa | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the forecast value of the Africa feed flavors and sweeteners sector by 2031?

The Africa feed flavors and sweeteners market size is forecast to reach at USD 57.76 million by 2031.

Which sub-additive leads demand across Africa?

Flavors lead by a wide margin, held the largest 94.0% market share in 2025.

Which animal group creates the largest demand base?

Ruminants accounted for the largest 90.9% market share in 2025.

Why is South Africa the key country in this space?

South Africa held the largest 48.0% market share in 2025 and is also the fastest-growing country segment at 3.4% CAGR from 2026 to 2031.

Page last updated on: