Africa Feed Minerals Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 0.98 Million |

| Market Size (2026) | USD 1.04 Million |

| Market Size (2031) | USD 1.40 Million |

| Growth Rate (2026 - 2031) | 6.10% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Feed Minerals Market Analysis by Mordor Intelligence

The Africa feed minerals market size is projected to increase from USD 0.98 billion in 2025 to USD 1.04 billion in 2026 and reach USD 1.40 billion by 2031, growing at a CAGR of 6.1% over 2026-2031. According to the "Agri-Food Outlook” report published on April 21, 2026, by Alltech [1]Source: Alltech, “2026 Alltech Agri-Food Outlook Shares Global Feed Production Survey Data,” Alltech, alltech.com, Africa's commercial feed production expanded by 11.5% in 2025, making it the fastest-growing region globally and reflecting the ongoing shift from subsistence feeding practices toward commercial feed systems across poultry, ruminants, and aquaculture. The Food and Agriculture Organization (FAO) and the Organization for Economic Co-operation and Development (OECD) Agricultural Outlook 2025-2034 projected a 33% rise in Africa's meat consumption over the next decade as the continent's population increases from 1.5 billion to 1.8 billion[2]Source: Organisation for Economic Co-operation and Development and Food and Agriculture Organization of the United Nations, “OECD-FAO Agricultural Outlook 2025-2034: Meat,” OECD, oecd.org, supporting long-term demand for mineral supplementation in compound feed. The Africa feed minerals market is also supported by rising feed cost pressures, as producers increasingly prioritize feed efficiency and consistent animal performance, as feed can account for up to 80% of production costs in intensive poultry systems. In early 2026, Nigeria announced a USD 1 billion National Integrated Poultry Project involving 60,000 hectares of feed crop cultivation, expanding commercial feed procurement, and widening the addressable customer base for mineral makrte in West Africa. The Africa feed minerals market remains fragmented, keeping pricing pressure high in standard mineral formats, but leaving opportunities for suppliers offering certified quality, improved bioavailability, and technical support in increasingly formalized feed channels.

Key Report Takeaways

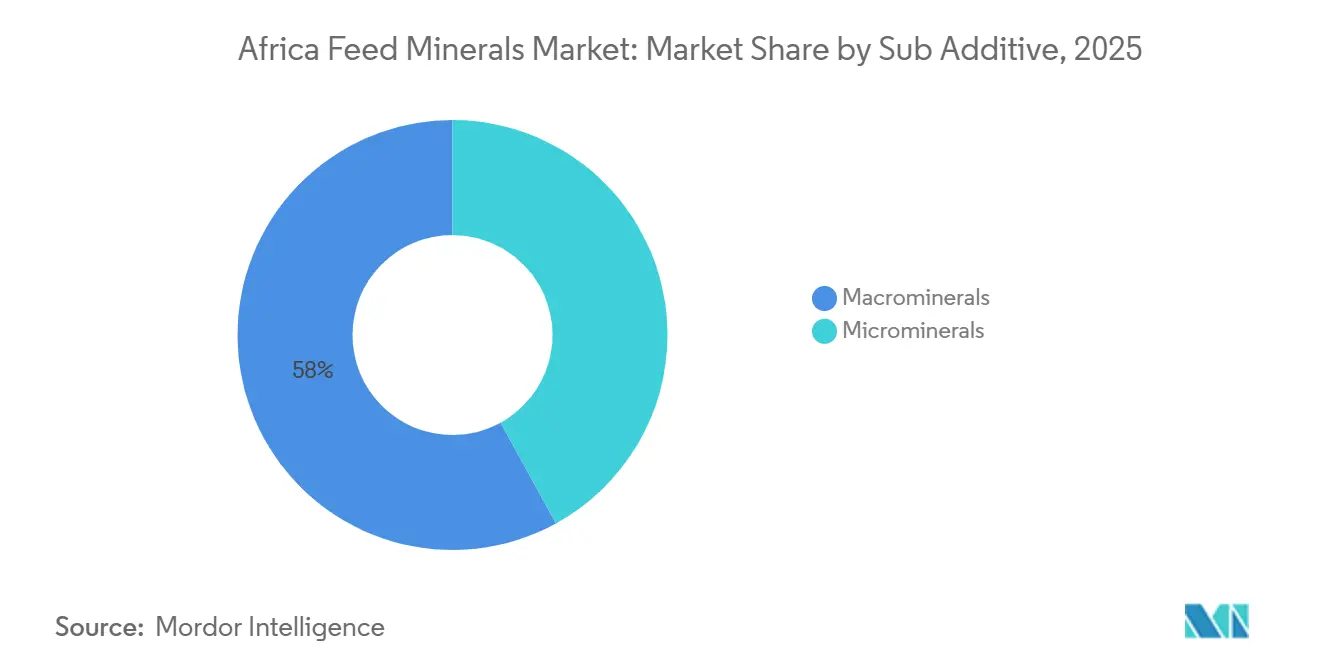

- By sub additive, macrominerals held 58% of the Africa feed minerals market size in 2025, while microminerals are forecast to record the fastest 6.8% CAGR through 2031.

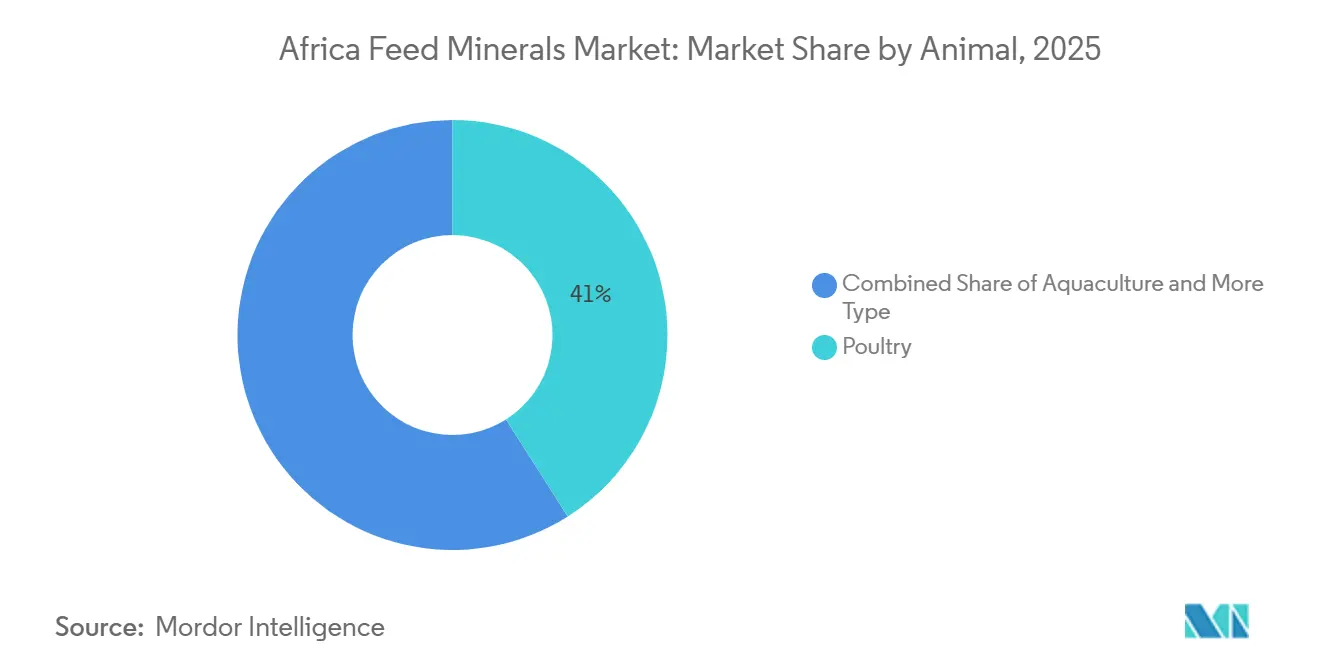

- By animal, poultry held 41% of the Africa feed minerals market share in 2025, while aquaculture is projected to post the fastest 7.3% CAGR through 2031.

- By geography, South Africa led with 27% of the market size in 2025, while Nigeria is projected to advance at the fastest 7.4% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Africa Feed Minerals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Commercial Poultry and Ruminant Feed Demand Across Africa | +1.4% | Africa-wide, with highest intensity in Nigeria, South Africa, and Egypt | Medium term (2-4 years) |

| Rapid expansion of commercial feed mill infrastructure across Africa | +1.0% | South Africa, Nigeria, Kenya, and Egypt, with spill-over to Ivory Coast and Uganda | Medium term (2-4 years) |

| Expansion of Precision Mineral Nutrition in High-Performing Farms | +0.7% | South Africa, Kenya, and Egypt | Long term (≥ 4 years) |

| Wider Shift from Bulk Raw Materials to Formulated Feed Inputs | +0.8% | Nigeria, Kenya, and Rest of Africa | Medium term (2-4 years) |

| Rising Demand for Chelated and Organic Trace Minerals in Hot Climate Production Systems | +0.8% | Africa-wide, with early gains in South Africa, Egypt, and Kenya | Long term (≥ 4 years) |

| Increasing Need for Feed Efficiency Under Volatile Ingredient Costs | +0.7% | Africa-wide, with highest intensity in Nigeria and Kenya | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Commercial Poultry and Ruminant Feed Demand Across Africa

According to the Alltech Agri-Food Outlook 2025[3]Source: Alltech, “Agri-Food Outlook 2025,” Alltech and British Society of Animal Science, bisas.org.uk, Africa added 40 new feed mills in 2024, bringing the total number of facilities to 2,228 and expanding the recurring procurement base for mineral in the Africa feed minerals market. The same report showed that cattle feed production in Africa increased by 32.2% in 2024, while dairy feed volumes grew by 25.7%, indicating stronger adoption of commercial feed practices within ruminant production systems. The OECD-FAO Agricultural Outlook 2025-2034 also projects continued gains in livestock productivity and output over the coming decade, increasing the importance of balanced mineral nutrition for commercial producers seeking higher efficiency and animal performance. As a result, the Africa feed minerals market is gaining support from both poultry and ruminant sectors rather than depending solely on poultry demand. This broadens the customer base for mineral suppliers and reduces the risk of growth being concentrated in a single livestock category.

Expansion of Precision Mineral Nutrition in High-Performing Farms

Commercial broiler and dairy operations across parts of Africa are increasingly emphasizing nutrition programs that support breed performance targets, creating opportunities for bioavailability-assured mineral products in the Africa feed minerals market. A 2025 meta-analysis published in Animals found that replacing inorganic trace minerals with proteinate trace minerals at 50% to 80% substitution reduced feed intake by 7 g per bird, improved average daily gain by 1.67 g, reduced feed conversion ratio by 4.5%, and lowered copper, iron, manganese, and zinc excretion by 14% to 21%. These performance improvements are particularly relevant in commercial production systems, where better feed efficiency can help offset the higher cost of chelated and proteinate mineral forms when feed grain prices are elevated. As more integrated producers focus on productivity, consistency, and nutrient utilization, the Africa feed minerals market is becoming increasingly receptive to premium trace mineral formats, suggesting a value opportunity beyond simple volume growth.

Wider Shift from Bulk Raw Materials to Formulated Feed Inputs

The Africa feed minerals market is benefiting from the gradual transition of livestock producers from bulk raw-material feeding to finished and semi-finished feeds supplied by commercial mills. According to the Alltech Agri-Food Outlook 2026, recent gains in feed production in Africa have been supported by the increasing commercialization of poultry and ruminant production systems, which promote the use of standardized feed formulations. In addition, Nigeria's National Livestock Growth Acceleration Strategy (2025-2035) and Kenya's 2025 feed quality reform initiatives are encouraging a more regulated and quality-focused feed industry. As commercial feed adoption expands, the Africa feed minerals market is projected to experience stronger demand driven by complete ration systems, in which mineral inclusion is determined through formulated nutrition programs rather than informal supplementation practices. This transition is likely to improve repeat purchasing and strengthen the market position of suppliers offering certified, technically supported mineral products.

Rising Demand for Chelated and Organic Trace Minerals in Hot Climate Production Systems

The Africa feed minerals market is also seeing stronger interest in chelated and organic trace minerals because hot-climate production conditions can raise mineral depletion and make standard inorganic formulations less effective. Research conducted at the University of Alexandria and published through Zinpro’s research network found that replacing inorganic trace minerals with metal-amino acid complexes in Nile tilapia diets improved growth and health outcomes, with the strongest economic replacement level at 50% to 55% for growth and 60% to 65% for health measures. This matters in the Africa feed minerals market because heat stress, nutritional stress, and pathogen load often overlap in African production systems. Suppliers that can show local on-farm evidence are in a stronger position to convert standard inorganic demand into higher-value mineral contracts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Penetration of Commercial Feed Milling in Smallholder-Dominated Markets | -1.00% | Sub-Saharan Africa, with highest intensity in inland Nigeria, Kenya, Ethiopia, and Tanzania | Medium term (2-4 years) |

| High Cost Premium of Chelated and Specialty Mineral Products | -0.70% | Africa-wide, with sharpest impact in low-income markets of West and Central Africa | Short term (≤ 2 years) |

| Inconsistent Quality Control and Counterfeit Product Risk in Fragmented Trade Channels | -0.50% | Nigeria, Kenya, and inland Rest of Africa markets | Medium term (2-4 years) |

| Weak Cold Chain and Distribution Infrastructure in Several Inland Markets | -0.50% | Inland sub-Saharan Africa, specifically East and Central Africa landlocked markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Penetration of Commercial Feed Milling in Smallholder-Dominated Markets

A large share of Africa's livestock population still operates outside the commercial feed system, limiting direct access to minerals-based nutrition and constraining volume growth in the Africa feed minerals market. According to the Malabo Montpellier Panel's 2025 report on aquaculture and livestock, as cited by Hatchery FM, poor feed quality and limited physical access to commercial inputs remain major constraints on smallholder productivity. Kenya's 2025 feed sector reform announcement, reported by Science Africa, also noted that feed accounts for 60% to 70% of livestock production costs, while producers outside major commercial zones continue to face inconsistent product quality and fragmented supply channels. Smaller farms often lack the scale and purchasing power needed to justify regular use of premium mineral, resulting in stronger demand from larger commercial production systems. Until aggregation mechanisms, cooperative feed models, and policy support expand commercial feed access to wider rural markets, growth in the Africa feed minerals market is likely to remain uneven across countries and livestock sectors.

High Cost Premium of Chelated and Specialty Mineral Products

Chelated and specialty trace mineral products command a significant price premium over conventional inorganic salts, making their adoption challenging for smaller feed mills and farms with short purchasing cycles. According to a 2025 study published in Animal Bioscience, chelated trace minerals improved dairy calf growth and health outcomes, but their higher acquisition cost remains a practical barrier in price-sensitive markets. Currency depreciation in countries such as Nigeria and Kenya further increases the landed cost of imported specialty minerals that are typically priced in USD. In response to cost pressures, some producers may reduce inclusion rates or continue relying on conventional mineral sources, which can limit performance gains and slow confidence in premium products. As a result, the cost differential continues to restrain the pace of transition in the Africa feed minerals market from high-volume inorganic minerals to higher-value specialty mineral products.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub Additive: Macrominerals Anchor Volume, Microminerals Accelerate Format Upgrading

Macrominerals held 58% of the Africa feed minerals market share in 2025, making them the largest sub-additive category across poultry, ruminant, and aquaculture feed. Calcium, phosphorus, and magnesium remain essential nutritional inputs in commercial formulations, and demand for these products is closely linked to overall feed production rather than optional performance enhancements. South Africa's feed regulatory framework requires commercial feed products to comply with labeling and composition requirements, supporting demand for certified macromineral inputs with verifiable quality. In addition, Solevo Group's 2024 partnership with Phosphea to distribute monocalcium phosphate, monodicalcium phosphate, and dicalcium phosphate across Africa highlights ongoing efforts to strengthen commercial supply channels within the Africa feed minerals industry. As a result, macrominerals remain central to volume growth because they constitute a fundamental component of most commercial feed formulations.

Microminerals are projected to register the fastest CAGR of 6.8% during 2026-2031 in the Africa feed minerals market, reflecting the gradual shift toward performance-oriented nutrition in formal feed channels. According to a 2025 meta-analysis published in Animals, partial substitution of inorganic trace minerals with proteinate trace minerals reduced the excretion of copper, iron, manganese, and zinc by 14% to 21% while improving bird performance, supporting the value proposition of advanced trace mineral products. Zinc, copper, manganese, and selenium remain the principal commercial trace mineral categories, with selenium being particularly important in regions where soil mineral deficiencies affect livestock health. As aquaculture production expands and commercial feed formulations become increasingly standardized across Africa, demand for consistent trace mineral profiles is proejcted to increase. This should enable microminerals to remain the fastest-growing segment of the Africa feed minerals market, even as conventional inorganic salts continue to dominate lower-cost feed systems.

By Animal: Poultry Anchors Market Share as Aquaculture Redefines Growth Dynamics

Poultry accounted for 41% of the Africa feed minerals market size in 2025, making it the largest animal segment in terms of mineral demand across the region. Commercial broiler and layer operations remain the primary users of mineral because they depend on planned feeding programs and measurable performance targets. According to the Alltech Agri-Food Outlook 2025, published by the British Society of Animal Science (BSAS), Africa's broiler feed production recovered to 17.6 million metric tons in 2024, while layer feed volumes increased by 1.7% to 8.47 million metric tons, indicating a return to more stable poultry production after earlier disease-related disruptions. Different nutritional requirements between broilers and layers also support repeat demand for tailored mineral formulations, helping poultry maintain its position as the largest contributor to the Africa feed minerals market.

Aquaculture is projected to register the fastest CAGR of 7.3% in the Africa feed minerals market during 2026-2031, supported by the transition from small-scale fish farming to integrated commercial supply chains. According to Feed Business Middle East and Africa, De Heus commissioned a USD 25 million aquafeed plant in Njeru, Uganda, in August 2025 with an annual production capacity of 100,000 metric tons, making it the largest aquafeed facility in East and Central Africa. Feed Business Middle East and Africa also reported that Aqua-Spark closed the first tranche of its sub-Saharan Africa fund at USD 48 million in March 2026, targeting investments across farming, feed, genetics, and distribution. According to the Food and Agriculture Organization (FAO) State of World Fisheries and Aquaculture (SOFIA) 2024 report, Nile tilapia and Africa catfish remain the dominant aquaculture species in Sub-Saharan Africa. As commercial aquaculture expands and complete extruded feeds become more widely adopted, demand for standardized and species-specific mineral formulations is projected to increase, supporting aquaculture as the fastest-growing animal segment in the Africa feed minerals market.

Geography Analysis

South Africa held 27% of the Africa feed minerals market share in 2025, making it the largest country market in the region. According to the Animal Feed Manufacturers Association of South Africa (AFMA) and industry estimates in 2025, the country has approximately 200 to 250 commercial feed mills. AFMA also reported monthly feed production of 603,190 metric tons in December 2025, highlighting the scale and consistency of formal feed demand. South Africa's vertically integrated poultry sector has also contributed to the adoption of more structured procurement practices for mineral, particularly where composition assurance and technical documentation are required. Archer Daniels Midland Company expanded its Johannesburg animal nutrition operations in April 2025, while De Heus broke ground on a new feed mill in Middelburg in March 2025, with commercial production to begin in August 2026. These developments support South Africa's position as a key market for premium, technically differentiated products in the Africa feed minerals market.

Nigeria is projected to register the fastest CAGR of 7.4% in the Africa feed minerals market during 2026-2031, supported by rising protein demand and policy initiatives aimed at expanding livestock production. According to the Africa Union Inter-Africa Bureau for Animal Resources (AU-IBAR) in 2025, Nigeria's feed and fodder resources represent an untapped opportunity worth more than USD 1 billion annually, while the country still faces a feed deficit of approximately 10% relative to demand. Nigeria's National Integrated Poultry Project and National Livestock Growth Acceleration Strategy 2025-2035 are also encouraging greater formalization of feed procurement and improved industry standards. In 2024, SHV Holdings N.V., through Nutreco, strengthened its regional animal nutrition footprint through the acquisition of AECI Animal Health in late 2024 and the earlier opening of a fish and poultry feed facility in Ibadan, Nigeria, during 2024.

Kenya and the Rest of Africa remain at an earlier stage of feed market commercialization but offer significant expansion opportunities for the Africa feed minerals market. In 2024, De Heus invested KES 3 billion (USD 26 million) in a feed factory in Athi River, Kenya, and established a network of more than 25 dedicated concentrate shops ahead of commercial operations. Tunga Nutrition Kenya Limited expanded aquafeed production capacity to 45,000 metric tons per year in February 2026. Meanwhile, multinational feed companies continue to expand across emerging markets, with FBMEA reporting plans for De Heus to establish a facility in Korhogo, Ivory Coast, reflecting growing confidence in the long-term development of commercial feed systems across the region.

Competitive Landscape

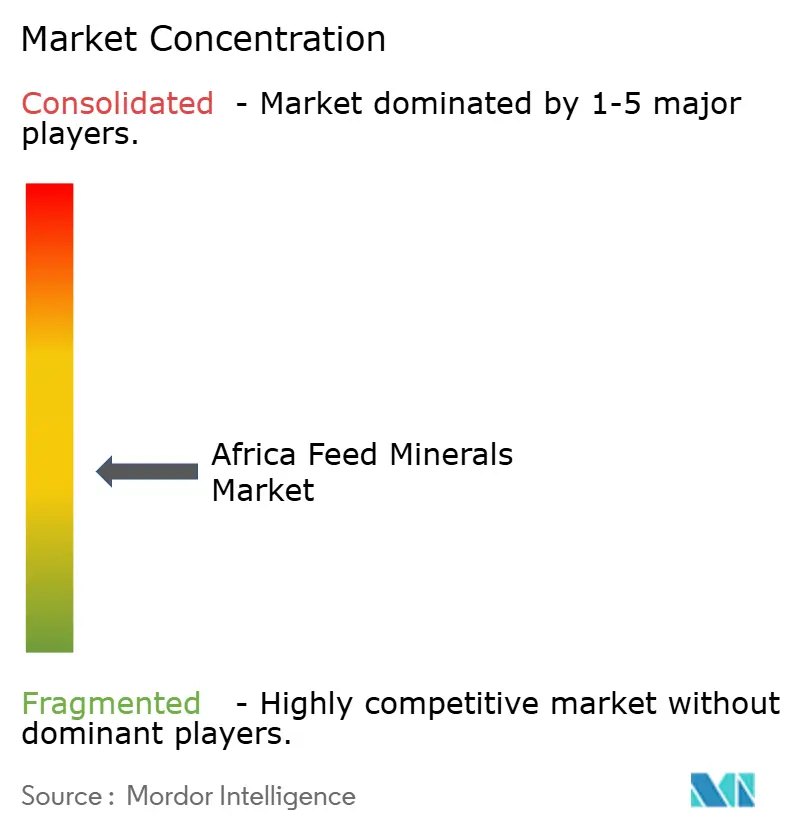

The Africa feed minerals market remains moderately fragmented in 2025, with Archer Daniels Midland Company (ADM), SHV Holdings N.V., Cargill, Incorporated, Alltech, Inc., and Kemin Industries, Inc. as the leading group, with no single company holding a dominant position. Competition in the market increasingly revolves around technical support, product consistency, and regional presence, reflecting the growing preference among commercial feed manufacturers for specification compliance and formulation support. SHV Holdings N.V. strengthened its position in late 2024 through Nutreco's acquisition of AECI Animal Health in South Africa, expanding its feed additive and mineral distribution capabilities in a key regional market. Phibro Animal Health Corporation completed the acquisition of Zoetis Inc.'s medicated feed additive portfolio in November 2024 for USD 400 million, illustrating how suppliers are broadening their animal nutrition and health offerings. In March 2025, Kemin Industries, Inc. introduced PROSIDIUM, a feed pathogen control product, extending its value proposition beyond nutrient delivery into feed safety solutions.

The Africa feed minerals market is also witnessing increased competition around bioavailability and specialty trace mineral technologies. According to Novus International, Inc., the company partnered with Ginkgo Bioworks in September 2024 to develop advanced feed additives that complement its MINTREX bis-chelated trace mineral portfolio and aim to improve mineral bioavailability at lower inclusion rates. Companies such as Alltech, Inc. and Novus International, Inc. have increasingly focused on performance-based mineral solutions targeted at integrated feed mills and commercial livestock operations. Distribution capabilities are also becoming an important competitive differentiator. In 2024, De Heus established a network of concentrate shops in Kenya before commissioning its feed plant, demonstrating a channel-development approach designed to expand market access ahead of volume growth.

Regional and local suppliers such as Agri-Vet, Kimleigh Chemicals South Africa (Kimleigh Chemicals SA), Bluestone Metals and Chemicals, and U-MIX continue to play an important role through strong local distribution networks and customer relationships. As a result, the Africa feed minerals market remains accessible to multiple participants, particularly in standard mineral salts and mid-tier feed channels. Opportunities remain in affordable chelated mineral products, inland distribution networks, and aquaculture-specific mineral programs tailored to species such as tilapia, catfish, and shrimp. Companies that successfully combine technical capabilities with broad market access are likely to strengthen their competitive positions as feed markets across Africa become increasingly formalized.

Africa Feed Minerals Industry Leaders

Archer-Daniels-Midland Company

Nutreco (SHV Holdings N.V.)

Cargill, Incorporated

Alltech, Inc.

Kemin Industries, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Biochem Zusatzstoffe Handels- und Produktionsgesellschaft mbH announced the acquisition of BASF SE’s global glycinate business, adding chelated trace minerals such as copper, iron, manganese, and zinc glycinates to its organic trace mineral portfolio. The deal strengthens supplier consolidation in chelated feed minerals and will affect sourcing options for African feed manufacturers.

- September 2025: Kemin Industries, Inc. completed the acquisition of CJ Youtell Biotech, the enzymes and fermentation subsidiary of CJ Bio, gaining fermentation manufacturing platforms in Shandong and Hunan, China. The acquisition strengthens Kemin Industries, Inc.'s capacity to develop integrated enzyme-mineral formulations to improve the bioavailability of trace minerals in poultry and aquafeed diets and its position across the company caters to, including Africa

- April 2024: Solevo activated its distribution agreement with Phosphea for feed-grade macrominerals, including monocalcium phosphate, monodicalcium phosphate, and dicalcium phosphate, across 12 African markets. The agreement expands access to certified feed phosphate minerals in West and Central Africa and supports more formal mineral sourcing.

Africa Feed Minerals Market Report Scope

Feed minerals are essential inorganic nutrients added to animal feed to support growth, metabolism, reproduction, and overall health.

The Africa Feed Minerals Market Report is Segmented by Sub Additive (Macrominerals and Microminerals), by Animal (Aquaculture, Poultry, Ruminants, Swine, and Other Animals), and by Geography (South Africa, Egypt, Nigeria, Kenya, and the Rest of Africa). The Market Forecasts are Provided in Terms of Value (USD) and Volume in (Metric Tons).

| Macrominerals |

| Microminerals |

| Aquaculture | Fish |

| Shrimp | |

| Other Aquaculture Species | |

| Poultry | Broiler |

| Layer | |

| Other Poultry Birds | |

| Ruminants | Beef Cattle |

| Dairy Cattle | |

| Other Ruminants | |

| Swine | |

| Other Animals |

| South Africa |

| Egypt |

| Nigeria |

| Kenya |

| Rest of Africa |

| By Sub Additive | Macrominerals | |

| Microminerals | ||

| By Animal | Aquaculture | Fish |

| Shrimp | ||

| Other Aquaculture Species | ||

| Poultry | Broiler | |

| Layer | ||

| Other Poultry Birds | ||

| Ruminants | Beef Cattle | |

| Dairy Cattle | ||

| Other Ruminants | ||

| Swine | ||

| Other Animals | ||

| By Country | South Africa | |

| Egypt | ||

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the 2031 outlook for the Africa feed minerals space?

The Africa feed minerals market is forecast to reach USD 1.40 billion by 2031 from USD 1.04 billion in 2026, with growth running at 6.1% CAGR over 2026-2031.

Which sub-additive category leads revenue in Africa feed minerals?

Macrominerals are the largest category, with 58% share in 2025, because calcium, phosphorus, and magnesium remain basic inputs in poultry, ruminant, and aquaculture feed.

Which animal segment is growing fastest in Africa feed minerals demand?

Aquaculture is the fastest animal segment, with a projected 7.3% CAGR over 2026-2031, as fish farming shifts toward commercial feed systems with verified mineral profiles.

Which country leads the regional landscape?

South Africa held the largest country share at 27% in 2025, supported by a dense commercial feed mill base and more formal procurement standards.

Page last updated on: