Africa Feed Yeast Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

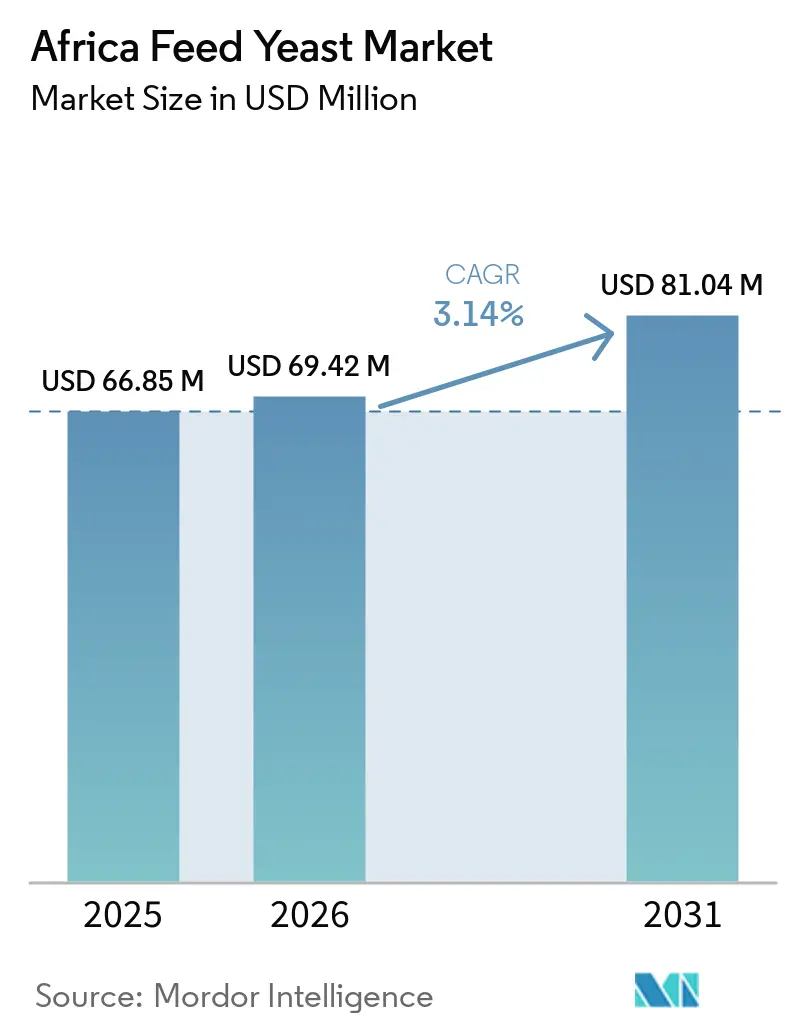

| Base Year Market Size (2025) | USD 66.85 Million |

| Market Size (2026) | USD 69.42 Million |

| Market Size (2031) | USD 81.04 Million |

| Growth Rate (2026 - 2031) | 3.14% CAGR |

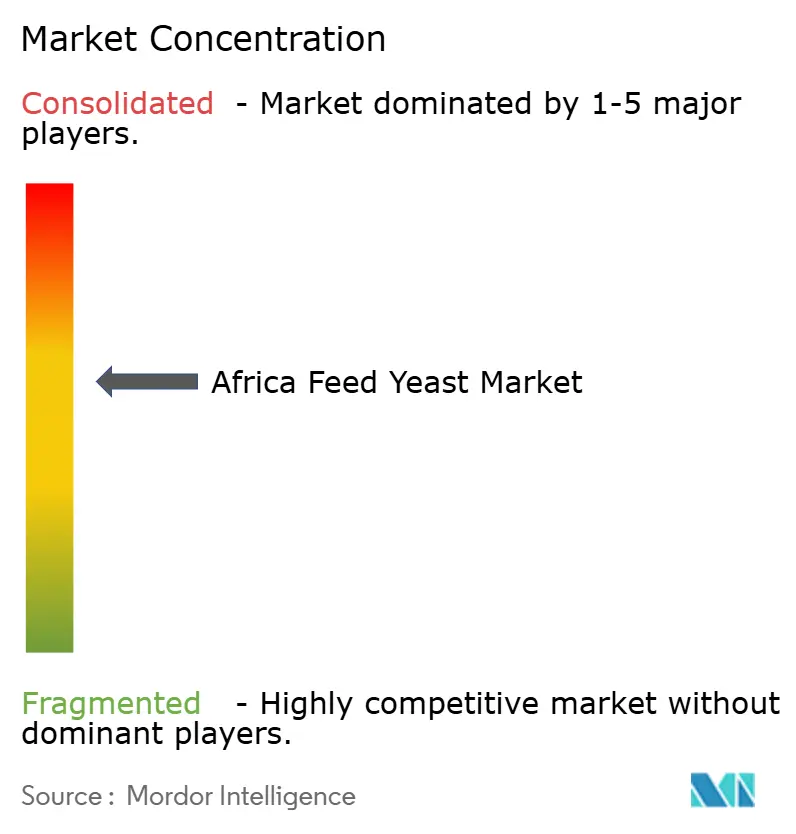

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Feed Yeast Market Analysis by Mordor Intelligence

The Africa feed yeast market size is anticipated to grow from USD 66.85 million in 2025 to USD 69.42 million in 2026 and is forecast to reach USD 8.04 million by 2031 at 3.14% CAGR over 2026-2031. The Africa feed yeast market is moving from opportunistic use toward routine inclusion as commercial feed production becomes more organized in key livestock and aquaculture corridors. Value growth is staying slightly firmer than volume growth because buyers are gradually shifting from low-cost by-product yeast toward live yeast, selenium yeast, and yeast derivatives that offer clearer performance benefits in feed efficiency, gut health, and resilience. The Africa feed yeast market is also being shaped by tighter attention to feed safety, especially where mycotoxin exposure has become a recurring issue in poultry and dairy systems, which supports demand for yeast cell wall fractions and related functional products. In parallel, scientific work on strain-specific yeast performance is making purchase decisions more evidence based, particularly in ruminant and broiler nutrition programs that need measurable returns rather than generic additive claims. Currency pressure remains the main near-term brake on the Africa feed yeast market because many fermentation inputs and specialty products still carry imported cost exposure.

Key Report Takeaways

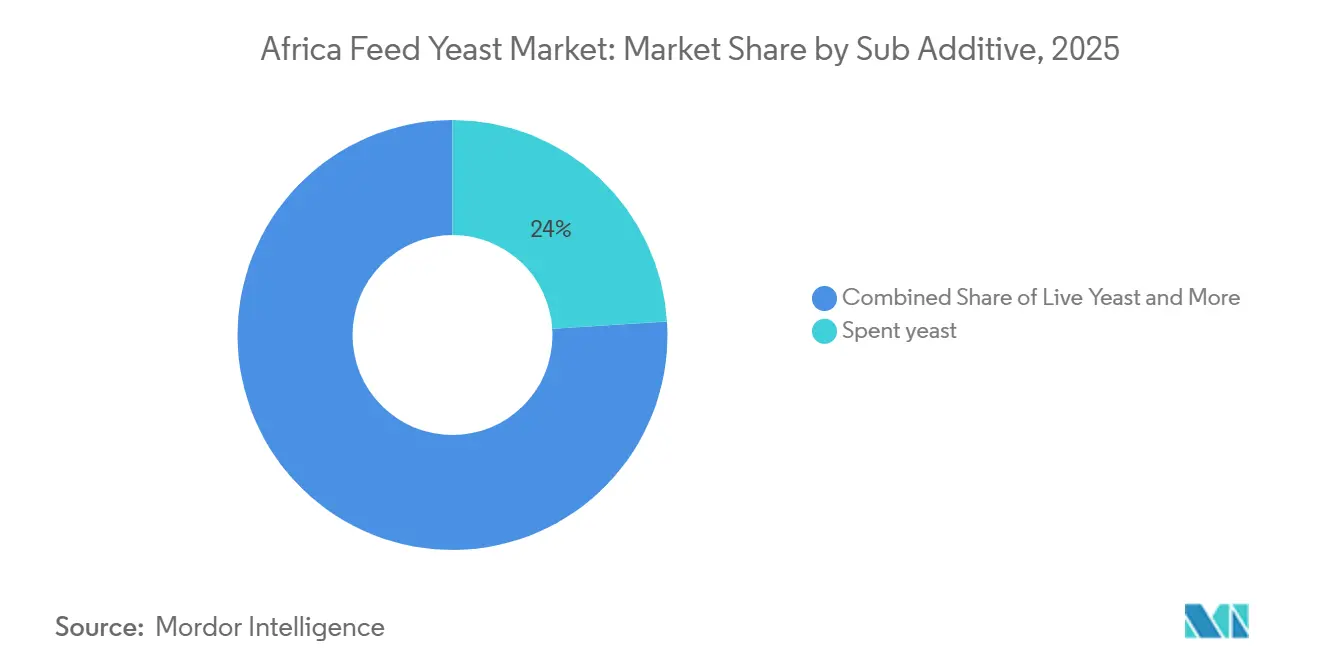

- By sub additive, spent yeast was the largest segment with 24% of the Africa feed yeast market share in 2025, while live yeast is the fastest segment with a 3.5% CAGR through 2031.

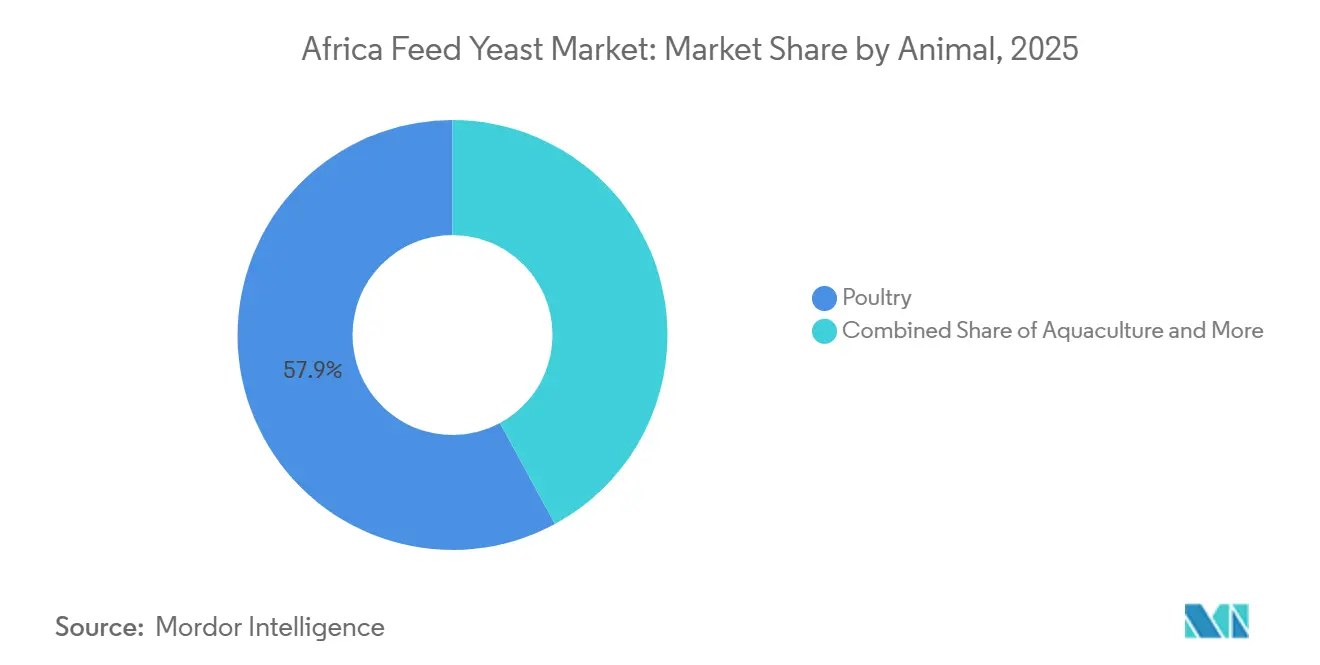

- By animal, poultry was the largest segment with 57.9% of the Africa feed yeast market size in 2025, while swine was the fastest segment with a 3.7% CAGR through 2031.

- By geography, South Africa was the largest segment with 48.4% share in 2025 and was also the fastest segment with a 3.7% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Africa Feed Yeast Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Poultry feed industrialization | +0.8% | Pan-Africa, concentrated in Nigeria, Egypt, South Africa, and Ethiopia | Short term (≤ 2 years) |

| Aquaculture feed expansion | +0.7% | Egypt, Nigeria, Kenya, and Uganda | Medium term (2-4 years) |

| Commercial feed penetration gains | +0.6% | West Africa and East Africa | Medium term (2-4 years) |

| Feed-efficiency optimization under high feed-cost pressure | +0.5% | Global, with strongest impact in South Africa and Kenya | Short term (≤ 2 years) |

| Faster feed registration and licensing in Egypt | +0.4% | Egypt, with spillover into North Africa and the Middle East and Africa region | Medium term (2-4 years) |

| Aflatoxin-risk mitigation through yeast-based resilience solutions | +0.5% | Sub-Saharan Africa, with early gains in Ethiopia, Rwanda, and Kenya | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Poultry Feed Industrialization

Poultry production is making the Africa feed yeast market more structured because larger farms and integrated feed systems depend on consistent formulations rather than variable on-farm mixing. That shift matters because yeast performs best when inclusion rates are stable and tied to measurable production targets such as gut integrity, feed conversion, flock resilience, and output uniformity. In this setting, spent yeast has remained relevant because it delivers protein, nucleotides, and beta-glucans at a price point that works for buyers managing narrow feed margins. The Africa feed yeast market also benefits from the fact that poultry is the first animal segment to formalize when commercial feed capacity expands, which makes it the earliest route for repeat additive adoption. As compound feed systems deepen across South Africa, Egypt, Nigeria, and Ethiopia, the Africa feed yeast market gains from better procurement discipline, stronger technical support, and clearer product differentiation between value-grade and performance-grade yeast solutions.

Aflatoxin-Risk Mitigation Through Yeast-Based Resilience Solutions

Aflatoxin exposure is becoming a stronger purchase driver in the Africa feed yeast market because contamination is no longer treated as an occasional quality issue in many livestock systems. A 2024 study in Tropical Animal Health and Production found that Pichia manshurica supplementation improved rumen fermentation and nutrient degradability in aflatoxin B1-contaminated diets, which supports the case for functional yeast use beyond basic nutrition. A 2025 study in World Journal of Microbiology and Biotechnology also showed that Pichia kudriavzevii supplementation in broiler feed reduced the adverse effects linked with aflatoxin stress, which strengthens the commercial case for strain-specific yeast products. In Ethiopia, a 2025 study reported aflatoxin B1 contamination in 85.4% of sampled dairy concentrates, which underlines how feed safety concerns can shift yeast cell wall and binder products from optional use toward standard use. The Africa feed yeast market therefore gains from a broader value proposition where yeast supports compliance, feed safety, and production stability at the same time.

Aquaculture Feed Expansion

Aquaculture is opening a newer demand channel for the Africa feed yeast market because fish feed buyers are actively looking for protein sources that are more stable than fishmeal and easier to standardize. WorldFish has been advancing sustainable feed work in Nigeria, Kenya, and Zambia through the Feed and Additive for Sustainable Aquatic Food Systems in Sub-Saharan Africa project, and that work has kept single-cell protein and other alternative ingredients in active commercial discussion[1]Source: WorldFish, “Development and Scaling of Sustainable Feeds for Resilient Aquatic Food Systems in Sub-Saharan Africa, Market Assessment of Fish Production and Feed in Nigeria,” WorldFish Program Report 2024-50, worldfishcenter.org. Torula dried yeast and related derivatives fit this need because they offer a useful amino acid profile, dependable supply, and functional benefits that go beyond straight protein replacement. The Africa feed yeast market is likely to benefit most where aquaculture is shifting from fragmented feed use toward dedicated commercial feed production, since that is where ingredient testing and formula upgrading usually accelerate. This demand is still smaller than poultry demand today, but it gives the Africa feed yeast market an additional route for premiumization that is less tied to traditional livestock cycles.

Feed-Efficiency Optimization Under High Feed-Cost Pressure

Feed economics remain a practical driver for the Africa feed yeast market because buyers rarely adopt functional additives unless the performance case is clear at the farm level. A 2025 study available through PubMed Central showed that feed can account for 55% to 75% of poultry production costs, which explains why additives that improve digestibility and feed conversion receive attention even when budgets are tight[2]Source: National Center for Biotechnology Information, “Nutritional Evaluation and Potential of Locally Available Feed Ingredients in Ethiopia,” PubMed Central, pmc.ncbi.nlm.nih.gov. Live yeast, whey yeast, and yeast derivatives attract interest in this environment because they can support nutrient utilization rather than only add another cost line to the formula. The Africa feed yeast market also benefits when millers shift their evaluation from ingredient price per kilogram toward return on inclusion through lower waste, better gut stability, and stronger production consistency. That change in buying logic tends to favor suppliers that can support product claims with local trials, technical service, and repeatable outcomes rather than price competition alone.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Currency volatility and imported-input inflation | -0.6% | Pan-Africa, most acute in Nigeria, Kenya, and Egypt | Short term (≤ 2 years) |

| Low compound-feed penetration in informal channels | -0.5% | West Africa and East Africa smallholder sectors | Medium term (2-4 years) |

| Soybean and protein-meal deficits in East Africa | -0.4% | Kenya, Tanzania, Uganda, and Ethiopia | Medium term (2-4 years) |

| Uneven storage hygiene and additive quality assurance | -0.3% | Sub-Saharan Africa rural and peri-urban zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Currency Volatility and Imported-Input Inflation

Currency instability still limits the Africa feed yeast market because many specialty inputs, fermentation materials, and imported finished additives are priced against hard currencies. When local currencies weaken, distributors face margin pressure and feed mills often postpone upgrades to higher-value yeast formats even if the technical case remains intact. The impact is strongest on smaller commercial mills because they usually lack hedging capacity, deep inventories, or the balance sheet needed to absorb short-term cost shocks. This keeps part of the Africa feed yeast market tied to low-cost product choices and slows the move into live yeast, selenium yeast, and advanced derivatives. The pressure should ease gradually where more in-region manufacturing comes online, but near-term pricing sensitivity remains a defining restraint in the Africa feed yeast market.

Soybean and Protein-Meal Deficits in East Africa

Protein shortages in East Africa also restrain the Africa feed yeast market because weak access to core feed ingredients can delay the broader move into high-specification compound feed. When soybean meal availability is tight, mills often simplify formulas, protect base nutrition first, and delay functional additives that are easier to cut in the short run. That pattern does not remove the long-term case for yeast, but it can slow adoption in exactly the markets where formal feed penetration is still developing. The Africa feed yeast market therefore grows unevenly across East Africa, with demand potential often stronger than near-term purchasing ability. Over time, any regional improvement in oilseed supply, feed milling infrastructure, and ingredient logistics should release deferred demand for yeast products that support performance, safety, and feed efficiency.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub Additive: Spent Yeast Leads Current Demand While Live Yeast Lifts the Future Mix

Spent yeast held the largest Africa feed yeast market share at 24% in 2025, which reflects its strong fit with cost-conscious commercial feed buyers. It remains widely used because it adds protein, nucleotides, and beta-glucans without the price premium attached to more specialized yeast formats. In the Africa feed yeast market, this makes spent yeast the practical choice where poultry and ruminant formulas need functional support, but budget discipline remains strict. Selenium yeast is gaining ground in more formal dairy and layer systems because organic selenium positioning is increasingly tied to animal health, product quality, and premium feeding programs. Torula dried yeast, whey yeast, and yeast derivatives remain smaller today, but each plays a defined role in palatability support, rumen stability, gut health, and feed safety applications.

In Africa feed yeast market size terms, live yeast is set to expand at the fastest 3.5% CAGR through 2031, reflecting a stronger shift toward performance-led buying. The segment benefits from tighter scrutiny of antibiotic reduction, broader use in rumen modulation, and stronger interest in gut integrity solutions for broilers and dairy cattle. In 2025, Research published in Frontiers in Veterinary Science also supported the premium positioning of organic selenium sources by showing greater selenium bioavailability than inorganic forms, which helps explain the longer-term upside for selenium yeast in structured operations. The Africa feed yeast market is therefore moving toward a more layered product mix, where spent yeast keeps scale, but live yeast and derivatives take a larger part of the value. That pattern points to gradual premiumization rather than rapid replacement, which is why lower-cost and higher-function products are likely to coexist through the forecast period.

By Animal: Poultry Holds the Largest Base While Swine Offers the Fastest Expansion

Poultry held the largest market share at 57.9% in 2025, which confirms that the Africa feed yeast market remains anchored in the region’s most commercialized feed chain. Poultry maintains this lead because broiler and layer systems adopt standardized feed faster than most other animal categories, making yeast use easier to scale. In the Africa feed yeast market, broiler formulas usually favor spent yeast and yeast derivatives for gut health and resilience, while premium layer diets show a stronger interest in selenium yeast and live yeast. Other poultry birds add a smaller but visible demand layer, as commercial specialty meat and egg production becomes more organized. This concentration in poultry also means that feed mill practices, disease pressure, and ingredient pricing in the poultry sector have an outsized influence on overall demand direction.

In Africa feed yeast market size terms, swine is projected to expand at the fastest 3.7% CAGR through 2031, supported by the gradual formalization of pig production in selected African markets. The segment is starting from a smaller base than poultry, but it benefits from rising commercial herd management, better attention to feed efficiency, and growing use of specialized nutrition in urban supply chains. The United States Department of Agriculture reported that Nigeria’s livestock reform agenda and new animal health trade protocols are intended to support commercial livestock development, which strengthens the long-term case for higher-value nutrition inputs in swine systems. Ruminants remain important in value terms because live yeast and whey yeast fit well with rumen health applications, while aquaculture is the newer structural opportunity within the Africa feed yeast market. Together, these patterns show a market where poultry still dominates current scale, but future growth is broadening into animal systems that need more technical feeding support.

Geography Analysis

South Africa held 48.4% of Africa feed yeast market share in 2025 and also represented the fastest geographic segment with a 3.7% CAGR through 2031. That combination reflects depth rather than saturation because the country already has the continent’s most established commercial feed ecosystem and still has room to widen use of higher-value yeast formats. The Africa feed yeast market is stronger in South Africa because feed mills, integrators, and commercial livestock operations are more accustomed to performance-based additive decisions and formal supplier support. This gives live yeast, selenium yeast, and derivatives a better chance to defend pricing than in less formal markets where spending remains reactive. South Africa, therefore, continues to set the benchmark for how the Africa feed yeast market evolves as feed quality, technical service, and compliance discipline are further developed.

Egypt remains one of the most important growth engines in the Africa feed yeast market because feed regulation, poultry activity, and aquaculture demand are moving in the same direction. The country’s licensing and registration environment has become more active, helping shorten commercialization timelines for functional feed inputs and improving visibility for suppliers entering the market. Egypt also matters because it connects large-scale poultry production with a meaningful aquaculture base, which gives both traditional yeast products and specialty formats a wider range of applications. In regional terms, Egypt is strengthening the Africa feed yeast market by serving as a North African demand center, where product approvals, industrial feed use, and downstream distribution are becoming more structured.

Nigeria and other parts of West Africa offer significant growth opportunities outside South Africa and Egypt, driven by rising protein demand despite incomplete compound feed penetration. The Africa feed yeast market has substantial potential for expansion, as commercial poultry and swine systems become more structured and advisory-led feed sales gain momentum. In East Africa, growth is less consistent due to improvements in aquaculture and livestock feed production being offset by ingredient shortages and infrastructure challenges, which hinder the adoption of premium additives. Organizations such as WorldFish and the Food and Agriculture Organization of the United Nations have been actively promoting resilient aquatic feed systems and structured formulation practices in sub-Saharan Africa. These efforts are projected to gradually enhance ingredient sophistication across the region. Overall, the Africa feed yeast market develops on varied foundations, with South Africa leading in market maturity, Egypt advancing through regulatory developments, and the broader continent offering long-term conversion potential.

Competitive Landscape

The Africa feed yeast market is projected to remain moderately concentrated at the supplier level in 2025. Key players in the market, including Lesaffre et Compagnie, Archer Daniels Midland Company, Lallemand Inc., DSM-Firmenich AG, and Cargill, Incorporated, compete across overlapping but distinct use cases. The market favors suppliers that can deliver consistent product quality alongside technical service, application support, and effective channel reach into both formal feed mills and more challenging regional markets. This structure ensures that global fermentation specialists maintain visibility at the top of the market, while niche specialists and distributors find opportunities in value-driven product categories. Consequently, market leadership is more pronounced in formal commercial channels than in overall regional consumption.

Strategic moves in the Africa feed yeast market are increasingly centered on localization, portfolio bundling, and faster route-to-market execution. DSM-Firmenich AG strengthened its regional position by opening its Animal Nutrition and Health manufacturing plant in Sadat City, Egypt, in September 2024, thereby reducing lead times and improving supply proximity for customers across Africa and neighboring regions[3]Source: DSM-Firmenich AG, “DSM-Firmenich Opens Animal Nutrition and Health Manufacturing Plant in Egypt,” Press Release, dsm-firmenich.com. In May 2025, Lesaffre et Compagnie also continued expanding its manufacturing depth through its investment agreement with Citra Bonang, which supports longer-term global supply flexibility for yeast products serving African demand corridors. These actions show that leading suppliers are not relying solely on product claims but are also reshaping their footprints, ownership, and logistics.

A key competitive factor in the Africa feed yeast market is the distinction between premium technical positioning and price-driven commodity competition. Multinational suppliers continue to promote live yeast and derivative products, emphasizing traceable efficacy valued by customers. Meanwhile, lower-cost spent yeast products remain prevalent, driven by regional traders and manufacturers utilizing simpler distribution models. This move reflects a broader commitment to developing local distribution channels that could support related biosolutions in the future. As a result, the Africa feed yeast market is anticipated to remain strategically competitive, with premium growth driven by service-oriented differentiation and commodity growth reliant on price competitiveness.

Africa Feed Yeast Industry Leaders

Archer Daniels Midland Company

Cargill, Incorporated

Lallemand Inc.

Lesaffre et Compagnie

DSM-Firmenich AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: De Heus inaugurated a USD 23.2 million (KES 3 billion) animal feed plant in Athi River, Kenya. The facility has an initial production capacity of 240,000 metric tons per year, which is expandable to 260,000 metric tons. It caters to poultry, pigs, ruminants, and aquaculture. This represents the largest private-sector feed mill investment in Kenya in recent years and generates direct demand for functional yeast inclusions at a commercial scale across East Africa.

- May 2026: Angel Yeast Co., Ltd. introduced its North African expansion projects, including a RMB 21 million (USD 3.10 million) investment to expand its Egypt food ingredient production line and build a packaging facility and food ingredient line in Algeria. This follows a joint venture by its Egyptian subsidiary to enhance local supply and customization in North Africa.

- February 2026: The Kenyan government has initiated measures to address low-quality feed formulations, including feed quality reforms and a national feed quality index. These efforts are projected to promote the use of higher-value additives, such as yeast cultures and yeast extracts.

Africa Feed Yeast Market Report Scope

Feed yeast is a protein-rich nutritional supplement derived from cultured yeast (typically Saccharomyces cerevisiae) used in animal and livestock diets. It is added to feed to improve digestion, boost immunity, and enhance the overall growth and health of poultry, cattle, and aquaculture.

The Africa feed yeast market report is segmented by sub-additive (live yeast, selenium yeast, spent yeast, and more), by animal (aquaculture, poultry, and more), and by geography (South Africa, Kenya, Egypt, and the Rest of Africa). The market forecasts are provided in terms of value (USD) and volume (metric tons).

| Live Yeast |

| Selenium Yeast |

| Spent Yeast |

| Torula Dried Yeast |

| Whey Yeast |

| Yeast Derivatives |

| Aquaculture | Fish |

| Shrimp | |

| Other Aquaculture Species | |

| Poultry | Broiler |

| Layer | |

| Other Poultry Birds | |

| Ruminants | Beef Cattle |

| Dairy Cattle | |

| Other Ruminants | |

| Swine | |

| Other Animals |

| South Africa |

| Kenya |

| Egypt |

| Rest of Africa |

| By Sub Additive | Live Yeast | |

| Selenium Yeast | ||

| Spent Yeast | ||

| Torula Dried Yeast | ||

| Whey Yeast | ||

| Yeast Derivatives | ||

| Animal | Aquaculture | Fish |

| Shrimp | ||

| Other Aquaculture Species | ||

| Poultry | Broiler | |

| Layer | ||

| Other Poultry Birds | ||

| Ruminants | Beef Cattle | |

| Dairy Cattle | ||

| Other Ruminants | ||

| Swine | ||

| Other Animals | ||

| Country | South Africa | |

| Kenya | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current outlook for Africa feed yeast demand?

The Africa feed yeast market is projected to rise from USD 69.42 million in 2026 to USD 81.04 million by 2031 at a 3.14% CAGR, supported by more formal feed production and gradual product premiumization.

Which sub additive leads current demand in Africa feed yeast applications?

Spent yeast was the largest sub additive in 2025 with 24.0% share because it balances functional value with lower cost for poultry and ruminant feed buyers.

Which animal segment creates the strongest base for yeast use in feed?

Poultry remains the largest demand center with 57.9% share in 2025 because commercial broiler and layer systems adopt standardized feed and functional additives earlier than most other animal categories.

Where is the strongest geographic position in Africa today?

South Africa was the largest country market with 48.4% share in 2025 and also the fastest-growing geography at a 3.7% CAGR through 2031 due to a more mature commercial feed ecosystem.

Why are functional yeast products gaining attention beyond basic nutrition?

Buyers are using yeast more often for feed efficiency, gut health, and mycotoxin resilience, especially after recent scientific studies linked specific yeast strains with better fermentation performance and reduced aflatoxin stress.

Which companies are shaping competitive activity in Africa feed yeast?

Key participants include Lesaffre et Compagnie, ANGEL YEAST CO., LTD., Lallemand Inc., Novonesis A/S, DSM-Firmenich AG, Alltech, Inc., Evonik Industries AG, Adisseo France S.A.S., and Leiber GmbH, with competition centered on technical service, portfolio breadth, and channel depth.

Page last updated on: