Welding Consumables Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 16.79 Billion |

| Market Size (2030) | USD 21.79 Billion |

| Growth Rate (2025 - 2030) | 5.35% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

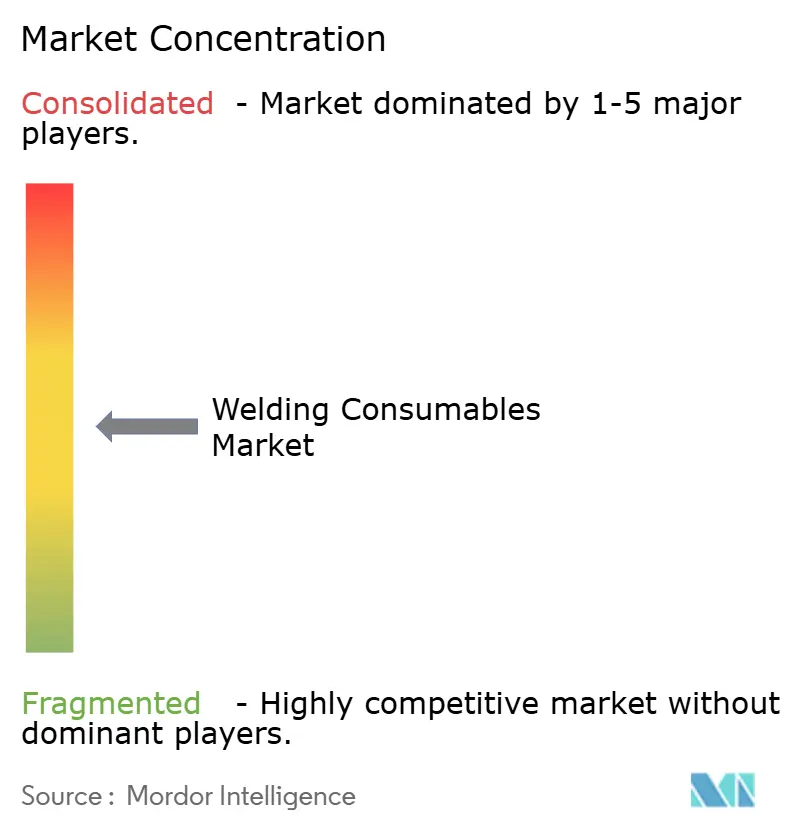

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Welding Consumables Market Analysis by Mordor Intelligence

The Welding Consumables Market size is estimated at USD 16.79 billion in 2025, and is expected to reach USD 21.79 billion by 2030, at a CAGR of 5.35% during the forecast period (2025-2030).

Robust infrastructure programs in Asia-Pacific, rising adoption of automated fabrication lines, and the automotive shift toward lightweight metals are the principal engines of expansion. Producers are channelling investment into premium flux-cored and metal-cored wires that maintain arc stability in robotic cells, while low-hydrogen stick electrodes retain relevance on construction sites that demand portability. Environmental regulation is simultaneously pushing demand toward low-fume formulations, and solid-state joining technologies such as friction stir welding are beginning to recalibrate long-term consumable intensity. Competitive dynamics remain moderate, with global suppliers leveraging R&D depth, automation know-how, and aftermarket service networks to protect their share.

Key Report Takeaways

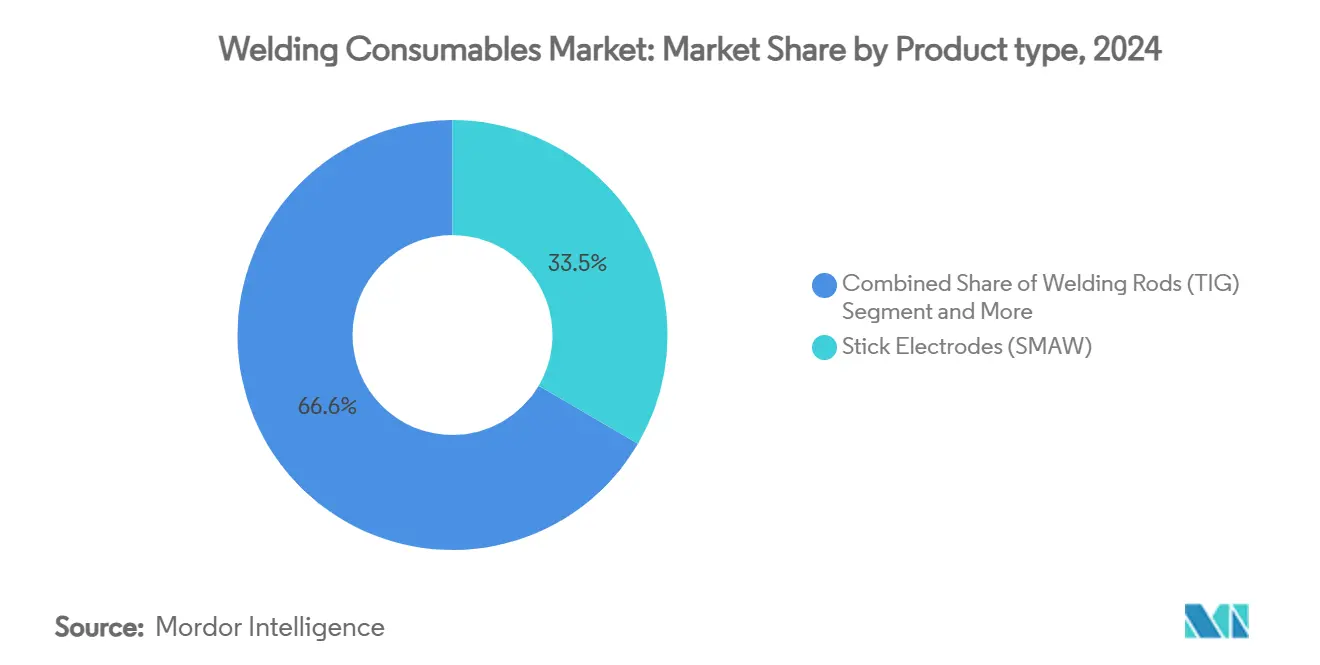

- By product type, stick electrodes held 33.45% of the welding consumables market share in 2024, whereas flux-cored wires are forecast to expand at an 8.8% CAGR to 2030.

- By material, steel consumables dominated the welding consumables market with a 46.2% share of the welding consumables market size in 2024, while aluminum products are set to record a 10.2% CAGR through 2030.

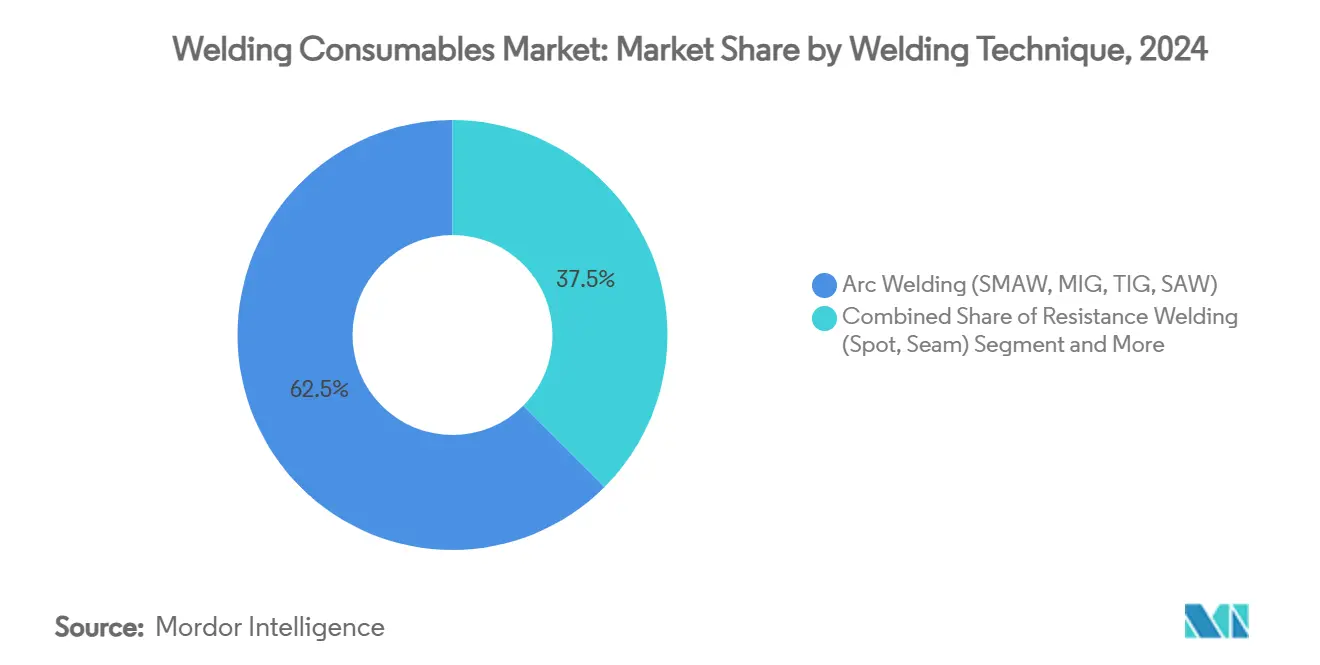

- By welding technique, arc processes captured 62.5% revenue in 2024; laser and electron-beam methods are projected to post an 11.4% CAGR over the forecast window.

- By end-use industry, building and construction led with 28.4% contribution in 2024, whereas shipbuilding and offshore applications are projected to climb at a 12.6% CAGR up to 2030.

- By geography, Asia-Pacific accounted for 43.6% of global demand in 2024, while the Middle East & Africa market is anticipated to grow fastest at an 8.9% CAGR to 2030.

Global Welding Consumables Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid infrastructure build-out in APAC driving steel fabrication demand | 0.6% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Skill-gap led automation uptick raises premium wire & flux demand | 0.5% | Global, concentrated in North America & EU | Short term (≤ 2 years) |

| Light-weight vehicle shift boosting aluminum filler metal use | 0.4% | Global, led by North America, EU, China | Medium term (2-4 years) |

| Surging offshore wind foundations need high-toughness consumables | 0.4% | North America & EU offshore, expanding to APAC | Long term (≥ 4 years) |

| Green-steel mandates spurring low-hydrogen electrode innovation | 0.3% | EU leading, expanding to North America & APAC | Long term (≥ 4 years) |

| High-performance alloys demand in specialized industries like aerospace and oil & gas | 0.3% | Global, concentrated in North America & EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Infrastructure Build-out in APAC Driving Steel Fabrication Demand

Asia-Pacific governments continue to expedite transport corridors, energy pipelines, and urban renewal programs that intensify steel usage. India’s National Infrastructure Pipeline alone envisions finished steel demand climbing from 136 million t in fiscal 2024 to as high as 275 million t by fiscal 2034, concentrating consumable volumes in heavy-plate fabrication. Fabricators are scaling submerged-arc welding lines that pair high-flux deposition rates with low-hydrogen wire chemistries to secure defect-free joints on thick sections. Chinese EPC contractors tendering for Belt and Road projects favor electrodes certified to AWS E7018 classifications for seismic-grade structures, stimulating premium stick electrode sales. The influx of mega-projects is therefore widening the addressable pool for specialty consumables that guarantee mechanical reliability under elevated heat inputs.

Skill-gap Led Automation Uptick Raises Premium Wire & Flux Demand

The welding labor shortfall is deepening as skilled personnel retire faster than replacements enter the trade; the American Welding Society projects 330,000 additional professionals will be required by 2028. Manufacturers are closing the gap by installing robotic cells that consume flux-cored and metal-cored wires engineered for consistent droplet transfer at high travel speeds. Real-time adaptive controls driven by artificial intelligence now monitor arc stability, prompting suppliers to formulate wires with narrow chemical tolerances and copper-free finishes that avoid contact-tip fouling. Early adopters such as automotive frame makers report double-digit productivity gains, reinforcing the pull toward premium consumables that align with automated workflows.

Light-weight Vehicle Shift Boosting Aluminum Filler Metal Use

Automakers are replacing steel body-in-white assemblies with aluminum sub-structures to improve electric-vehicle range and comply with emission norms. Friction stir welding delivers joints achieving 90% of parent-metal strength without filler or shielding gas, yet complex geometries and service repairs continue to rely on ER5356 and ER4043 wire grades. Advancements in micro-alloyed, scandium-modified wires are mitigating porosity and hot-crack susceptibility in multi-pass joints. Demand is also rising for bifunctional consumables that seamlessly join aluminum to galv anized steel, meeting crash-worthiness targets while controlling intermetallic layer thickness below 10 µm. These material innovations are securing new revenue streams across the welding consumables market.

Surging Offshore Wind Foundations Need High-Toughness Consumables

The floating and fixed-bottom offshore wind fleet under construction across the North Sea and Atlantic seaboard requires monopile and transition-piece welds able to absorb 75 J at -40 °C per project specifications. Consumable suppliers are developing submerged-arc flux and wire sets alloyed with nickel and micro-alloyed niobium to retain Charpy toughness after heat inputs surpassing 100 kJ/cm. Manufacturers of thermo-mechanically controlled processed (TMCP) steels insist on traceable batch documentation, pushing vendors toward digital certificates accessible through blockchain portals. As project developers extend into typhoon-prone Asian waters, impact and fatigue requirements are intensifying and cementing a long-horizon growth path for high-toughness consumables.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile raw-material (nickel, molybdenum) prices inflate costs | -0.3% | Global, acute in stainless steel applications | Short term (≤ 2 years) |

| Emergent solid-state joining (FSW, bonding) curbs consumable intensity | -0.3% | Global, led by automotive & aerospace sectors | Long term (≥ 4 years) |

| Stringent fume-emission norms raise compliance spend | -0.2% | North America & EU, expanding globally | Medium term (2-4 years) |

| 3-D printed near-net parts reduce welding steps in aerospace | -0.2% | North America & EU aerospace hubs | Long term (≥ 4 years) |

| Regional environmental regulatory changes | -0.1% | Global, varying by jurisdiction | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Raw-material Prices Inflate Costs

Nickel and m olybdenum price swings are compressing margins on stainless and high-alloy consumables, forcing frequent list-price adjustments. ESAB’s 2024 10-K flags these metals as principal cost drivers and notes hedging limitations under long-term supply contracts. End-users in petrochemical fabrication, therefore, weigh substitution toward duplex or lean-alloy grades, trimming premium consumable offtake when nickel spikes exceed 25 %. Wire makers are experimenting with chromium-rich flux-cored compositions to sustain corrosion resistance while reducing nickel content, but extensive requalification costs temper adoption. The uncertainty adds procurement complexity, constraining forecast visibility for both suppliers and buyers.

Emergent Solid-State Joining Curbs Consumable Intensity

Friction stir welding and other solid-state techniques are trimming the need for filler metals and shielding gases while still delivering joints that retain roughly 90% of the original aluminum’s strength. The method consumes less energy and emits fewer fumes, suiting the auto industry’s move toward lighter electric vehicles and tighter sustainability goals. Its reach is widening from standard aluminum panels to mixed-material joints in cars, aircraft, and marine structures because it keeps distortion low and reduces production costs. Research teams are now validating the process for steel and underwater repairs, signalling even broader applicability. When paired with additive manufacturing, friction stir welding allows near-net-shape parts to be built and joined in a single flow, a shift that could permanently shrink traditional consumable demand in selected applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Flux-Cored Wires Drive Innovation

Flux-cored wires, despite holding only 26.8% of 2024 revenue, are rewriting productivity benchmarks and underpinning the fastest segment CAGR at 8.8% to 2030, outpacing the broader welding consumables market. Stick electrodes remain the largest category in the welding consumables market with a 33.45% share, owing to unrivalled portability for field erection and maintenance tasks. Yet, automated ship-panel and truck-chassis lines increasingly specify dual-shield flux-cored wires that support deposition rates exceeding 12 kg/h, cutting weld cycle time by nearly 35%. The shift is stimulating ancillary demand for compatible robotic torch consumables and calibrated flux recovery systems.

Product portfolios are diversifying with metal-cored variants offering lower silicate residue, thereby trimming post-weld cleaning on automotive production. Submerged-arc flux and wire bundles remain critical for heavy-plate fabrication and claim 14% share of the welding consumables market size, thanks to their ability to deliver uniform penetrations on 30 mm steel for wind-tower sections. TIG rods secure aerospace and precision fabrication orders where porosity thresholds are stringent. The residual market occupies oxy-fuel brazing rods and specialty powders used in wear-overlay applications, which continue to serve niche repair operations despite the advance of higher-speed processes.

By Material Type: Aluminum Surge Reshapes Dynamics

Steel consumables dominated with a 46.2% share in 2024, confirming steel’s primacy across construction, pipelines, and pressure vessels. Nonetheless, the aluminum subset is set to rise at a 10.2% CAGR, led by battery-electric vehicle platforms demanding sub-40 kg body-in-white weight for extended range. This divergence compels suppliers to certify weld wires against OEM-specific crash-pulse tests, sharpening competitive differentiation through metallurgical refinements.

Within the welding consumables market size, nickel-based rods for LNG cryogenic tanks and cobalt-free Haynes substitutes for aerospace hot-section components register mid-single-digit growth, safeguarded by stringent material codes. Copper and t itanium wires clustered under “Others” remain small yet strategic, supporting medical implants and satellite structures. Ongoing R&D investigates rare-earth inoculation to refine grain structures in high-strength steel weld metals, promising toughness gains that could broaden steel’s performance envelope and preserve share against aluminum incursion.

By Welding Technique: Laser Technologies Emerge

Arc welding processes SMAW, GMAW, GTAW, and SAW retained 62.5% revenue leadership in 2024, giving the welding consumables market dependable volume anchors. Conversely, laser and electron-beam methods, though currently representing 6% share, are forecast to compound at 11.4% CAGR owing to exacting tolerances in electronics and e-mobility components. Fibre-laser investments by tier-1 battery-pack suppliers highlight an appetite for spatter-free seams and minimal heat-affected zones that traditional arcs struggle to deliver.

While laser welding consumes far fewer fillers, hybrid laser-arc platforms that overlay a GMAW wire into the keyhole are emerging, preserving consumable demand while leveraging laser speed. Resistance spot welding continues its indispensable role on automotive assembly lines, delivering over 5,000 weld nuggets per body at cycle times under 400 ms. Oxy-fuel gas welding is receding, confined to artisan workshops and on-site repairs where equipment simplicity overrules throughput economics, yet it underscores the diverse process mix sustaining overall consumable volumes.

By End-Use Industry: Shipbuilding Accelerates

Building and construction generated 28.4% of 2024 turnover in the welding consumables market, anchored by skyscraper frames, bridges, and industrial sheds that each consume kilometres of E7018 electrodes and ER70S-6 wires. Rapid urbanisation in Southeast Asia and the Gulf Cooperation Council continues to funnel structural steel orders toward local fabricators, underpinning steady rod replenishment cycles.

Shipbuilding and offshore, however, is the sprinter, forecast to surge at 12.6% CAGR as global offshore wind capacity tops 380 GW by 2030, compared with 75 GW in 2024. Each 15 MW turbine foundation demands up to 400 t of weld metal, primarily via submerged-arc multi-wire systems that boost deposition to 30 kg/h. Oil & gas remains resilient, commissioning clad pipelines and FPSO hulls that rely on nickel-alloy fillers to combat sour service corrosion. Aerospace and defence keep specialty consumable uptake solid with their insistence on defect-free titanium and aluminum joining for next-generation fighter fuselages.

Geography Analysis

Asia-Pacific dominated the welding consumables market with a 43.6% of global demand in 2024 and is forecast to retain leadership through 2030. China’s continued capacity additions in shipyards and heavy equipment, coupled with India’s infrastructure push, funnel large-volume orders toward regional consumable producers that enjoy proximity advantages. Japanese and South Korean vehicle manufacturers add further depth through steady robotic GMAW wire call-offs. The welding consumables market size derived from Asia-Pacific is underpinned by cost-competitive manufacturing clusters that integrate vertically into flux and wire production, ensuring local availability and buffering against freight surcharges.

North America remains technologically influential. U.S. fabricators are expanding robotic installations to offset an ageing workforce, amplifying demand for metal-cored wires and laser hybrid consumables that can deliver high first-pass yield. Federal incentives for offshore wind manufacturing hubs along the Atlantic coast are channelling capital into new flux-cored wire lines tailored for thick-wall monopiles. Canada’s heavy-haul railcar refurbishment and LNG export terminal construction likewise sustain orders for low-temperature stick electrodes and high-nickel fluxes.

Europe mirrors these trends, albeit with stricter environmental rules that propel early adoption of low-fume wires and fume-extractor torches. Germany and the Netherlands spearhead offshore wind fabrication, necessitating consumables certified under EN 10204 3.2 inspection regimes. The Middle East & Africa, while contributing a smaller base, is the fastest-growing geography at 8.9% CAGR. Offshore expansion in Saudi Arabia and deep-water projects off Angola are pushing upmarket demand for corrosion-resistant weld wires. South America, led by Brazil’s automotive and hydroelectric projects, rounds out the regional picture with moderate, investment-led uptake.

Mordor Intelligence provides coverage of the welding consumables market across other key regional markets. Detailed country-level analysis extends to United States incorporating local coverage and market participation, as required.

Competitive Landscape

Lincoln Electric, ESAB Corporation, and Illinois Tool Works anchor a moderate-concentration field where the top five suppliers collectively control nearly 55% of revenue. Lincoln Electric posted USD 4.0 billion net sales in 2024 and continues to channel double-digit R&D outlays into hyper-fill bulk wire drums optimised for robotic tandem arcs. ESAB leverages a multi-brand portfolio and an installed base of digital welding power sources to cross-sell cored wire upgrades, particularly in developing markets where equipment renewal cycles are accelerating.

Strategic moves are converging on automation integration. Lincoln Electric’s 2025 acquisition program targets vision-guided robotic integrators that can pre-configure turnkey cells, bundling wires, torches, software, and service contracts. ESAB’s operating model emphasizes cloud-connected power sources that stream real-time weld data, offering predictive maintenance insights back to plant managers. Illinois Tool Works sustains competitiveness through intellectual-property depth in pulse-waveform control, licensing synergic programs to automotive OEMs, and driving pull-through of premium MIG consumables.

New entrants concentrate on laser consumables and metallurgical tweaks for high-entropy alloys, yet barriers remain steep given qualification requirements and distributor entrenchment. Suppliers are also scrutinizing additive-manufacturing synergies, developing wire chemistries suitable for wire-arc additive manufacturing that keep deposition stable at 10 kg/h deposition without compromising mechanical properties. Environmental legislation could tilt the share toward innovators able to validate low-fume or fume-free consumable technologies, while friction stir and hybrid laser-arc processes represent latent threats to consumable demand in certain joints.

Welding Consumables Industry Leaders

Lincoln Electric Holdings Inc.

ESAB Corporation

Illinois Tool Works Inc. (Miller Welding)

voestalpine Böhler Welding GmbH

Kobe Steel Ltd. (Kobelco Welding)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Lincoln Electric reported Q1 2025 net sales of USD 1.004 billion, up 2.4% year-on-year, citing acquisition synergies and disciplined cost control.

- February 2025: Lincoln Electric disclosed full-year 2024 revenue of USD 4.0 billion, maintaining a 17.6% adjusted operating margin amid softer organic volumes.

- January 2025: Colfax Corporation agreed to acquire Victor Technologies for USD 947.3 million, expanding its ESAB arm into cutting and gas-control niches.

- November 2024: Lincoln Electric launched HyperFill STT and HyperFill RA consumables designed to raise travel speed and deposition efficiency in heavy fabrication.

Global Welding Consumables Market Report Scope

| Stick Electrodes (SMAW) |

| Welding Rods (TIG) |

| Submerged Arc Welding (SAW) Flux & Wire Sets |

| Flux-Cored Wires |

| Welding Wires (GMAW/MIG/ Solid Wires) |

| Others (Oxy-fuel Welding Rods, Welding Powder, Shielding Gases, Tips, etc.) |

| Steel Welding Consumables (carbon, Stainless) |

| Aluminum Welding Consumables |

| Nickel-Based Welding Consumables |

| Others (Copper, Titanium, Cobalt) |

| Arc Welding (SMAW, MIG, TIG, SAW) |

| Resistance Welding (Spot, Seam) |

| Oxy-Fuel Welding |

| Others (Laser Welding, Electron Beam Welding) |

| Building & Construction |

| Automotive & Transportation |

| Shipbuilding & Offshore |

| Oil & Gas, Energy Infrastructure |

| Heavy Machinery & Industrial Equipment |

| Aerospace & Defense |

| Others (Railway, Consumer Goods) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Peru | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Turkey | |

| Egypt | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Product Type | Stick Electrodes (SMAW) | |

| Welding Rods (TIG) | ||

| Submerged Arc Welding (SAW) Flux & Wire Sets | ||

| Flux-Cored Wires | ||

| Welding Wires (GMAW/MIG/ Solid Wires) | ||

| Others (Oxy-fuel Welding Rods, Welding Powder, Shielding Gases, Tips, etc.) | ||

| By Material Type | Steel Welding Consumables (carbon, Stainless) | |

| Aluminum Welding Consumables | ||

| Nickel-Based Welding Consumables | ||

| Others (Copper, Titanium, Cobalt) | ||

| By Welding Technique | Arc Welding (SMAW, MIG, TIG, SAW) | |

| Resistance Welding (Spot, Seam) | ||

| Oxy-Fuel Welding | ||

| Others (Laser Welding, Electron Beam Welding) | ||

| By End-Use Industry | Building & Construction | |

| Automotive & Transportation | ||

| Shipbuilding & Offshore | ||

| Oil & Gas, Energy Infrastructure | ||

| Heavy Machinery & Industrial Equipment | ||

| Aerospace & Defense | ||

| Others (Railway, Consumer Goods) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Peru | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Kuwait | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size and expected growth rate of the welding consumables market?

The welding consumables market was valued at USD 16.79 billion in 2025 and is projected to post a 5.35% CAGR through 2030.

Which region accounts for the largest share of demand?

Asia-Pacific led with 43.6% of global revenue in 2024, driven by expansive infrastructure programs across China, India, and Southeast Asia.

Which product categories dominate and which are growing the fastest?

Stick electrodes held 33.45% of 2024 sales, while flux-cored wires are forecast to grow at an 8.8% CAGR to 2030.

How are environmental regulations shaping consumable development?

New EPA air-quality standards are spurring demand for low-fume rods and wires as fabricators invest in cleaner processes to meet compliance deadlines.

What impact is the welding labor shortage having on the market?

Shortfalls in skilled welders are accelerating adoption of robotic cells that require premium, automation-ready wires with tight chemical tolerances.

Will friction stir welding reduce long-term demand for traditional consumables?

Solid-state processes such as friction stir welding eliminate filler metals in many aluminum and mixed-material joints, posing a gradual but structural drag on consumable volumes.

Page last updated on: