Engine Driven Welders Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.33 Billion |

| Market Size (2031) | USD 1.69 Billion |

| Growth Rate (2026 - 2031) | 4.91% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Engine Driven Welders Market Analysis by Mordor Intelligence

The Engine Driven Welders Market size is projected to be USD 1.27 billion in 2025, USD 1.33 billion in 2026, and reach USD 1.69 billion by 2031, growing at a CAGR of 4.91% from 2026 to 2031.

Operators that work away from reliable grid power are pairing diesel reliability with LPG-assisted or dual-fuel configurations to cut nitrogen oxide emissions by up to 40% while preserving continuous-duty power in the field. Diesel platforms remain the baseline because they combine durability, serviceability, and high auxiliary output that supports tools and air systems on remote sites where downtime is costly. Rental leaders are tightening performance expectations by tying lease pricing to measured fuel burn per arc-on hour, which accelerates OEM investment in telematics and efficiency-focused designs. Integration is also reshaping fleets, as single-chassis systems that combine welding, compressed air, and power generation reduce truck weight and reclaim usable bed space for tools and consumables. Emission limits in enclosed spaces are prompting selective deployment of battery-hybrid units that blend lithium-ion storage with compact engines to meet work rules without sacrificing utility in tight or sensitive locations.

Key Report Takeaways

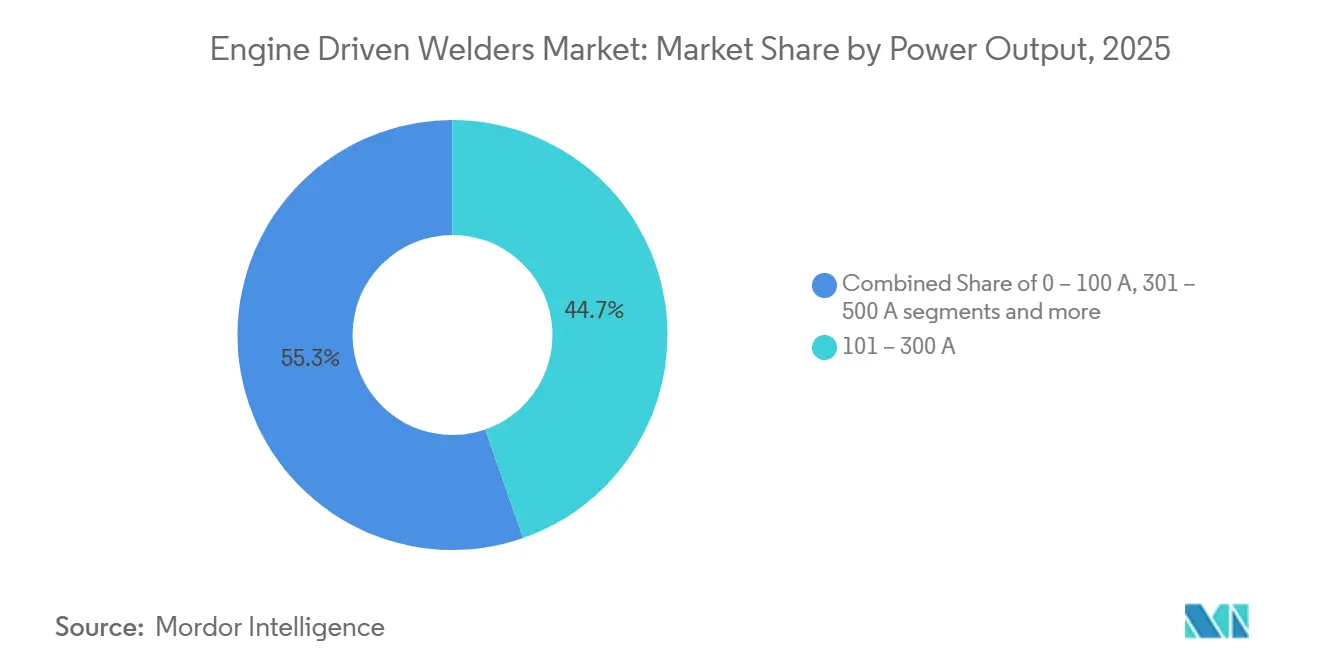

- By power output, the 101–300 ampere band led with 44.67% of the engine-driven welders market share in 2025, while units above 500 amperes are projected to advance at a 5.21% CAGR through 2031.

- By fuel type, diesel accounted for 67.81% of the engine-driven welders market size in 2025, while LPG/CNG alternatives are projected to post the fastest CAGR at 5.78% through 2031.

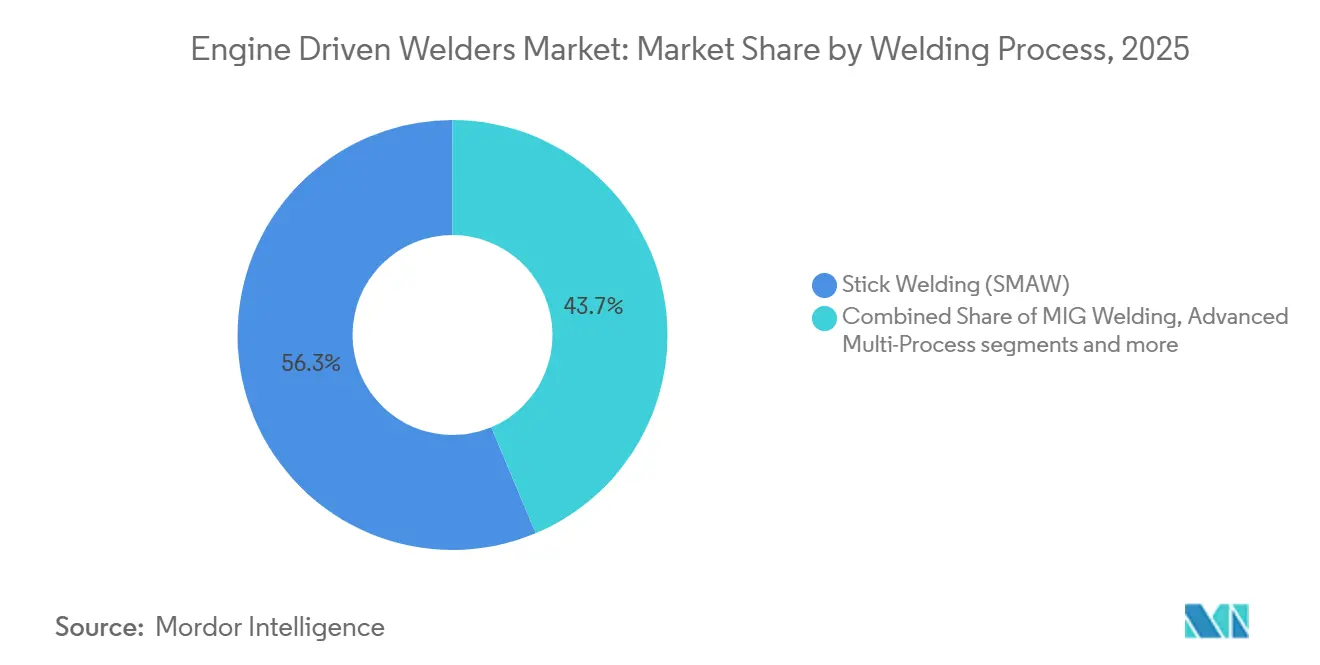

- By welding process, stick welding held 56.32% of the engine-driven welders market share in 2025, while advanced multi-process platforms are projected to grow at a 6.23% CAGR to 2031.

- By end-user industry, construction and infrastructure accounted for 31.23% of the engine-driven welders market size in 2025, while mining and quarrying is projected to expand at 6.47% through 2031.

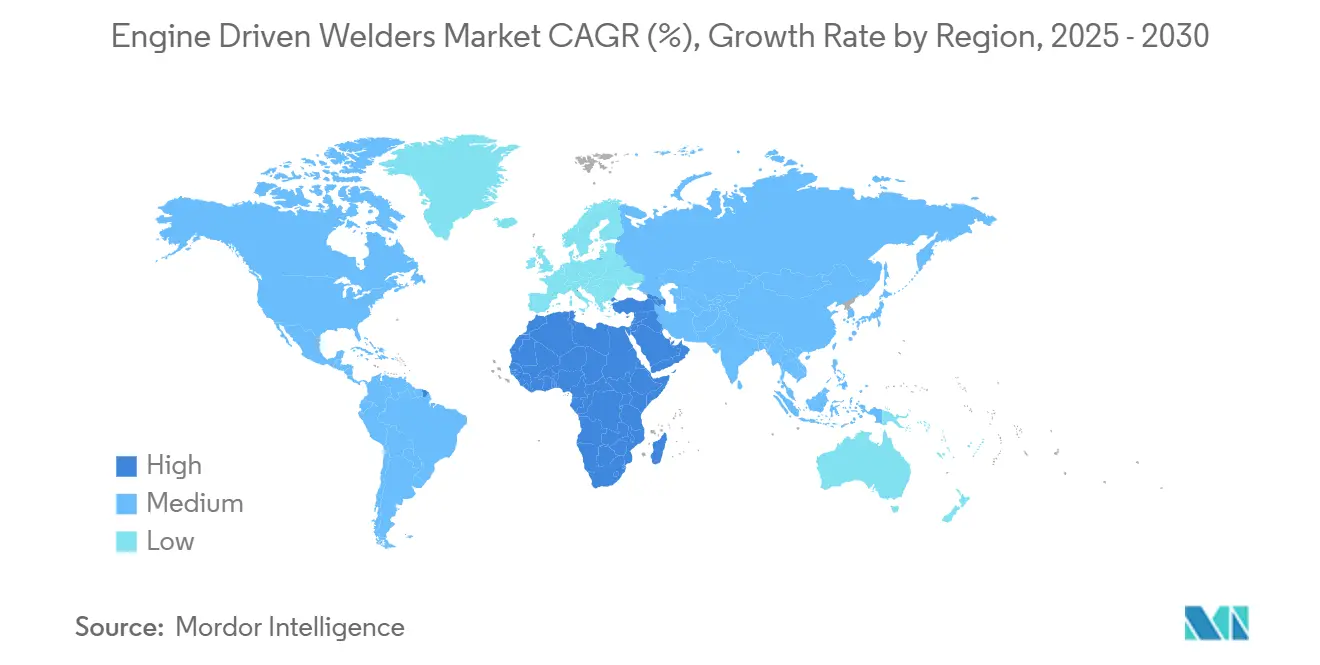

- By geography, Asia-Pacific led with 48.21% of the engine-driven welders market size in 2025, while the Middle East and Africa region is projected to record the fastest CAGR at 7.21% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Engine Driven Welders Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Oil and Gas Pipeline Infrastructure | +1.2% | Global, concentrated in North America, the Middle East, and Central Asia, with early pipeline corridor establishment | Medium term (2–4 years) |

| Growing Construction Activity in Remote and Rural Areas | +0.9% | APAC core, spillover to Sub-Saharan Africa, Latin America | Long term (≥ 4 years) |

| Growth in Mobile Welding and Maintenance Services | +0.8% | Global, strong in North America service-truck fleets, the Middle East industrial maintenance | Medium term (2–4 years) |

| Increasing Military and Defense Field Operations Requirements | +0.7% | North America, Europe, APAC | Short term (≤ 2 years) |

| Rising Demand from Agricultural Equipment Manufacturing and Repair | +0.4% | North America and EU rural zones, Australia, Brazil, Argentina | Medium term (2–4 years) |

| Natural Disaster Recovery and Emergency Infrastructure Repair | +0.3% | National hot spots in hurricane and earthquake zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expansion of Oil and Gas Pipeline Infrastructure

The pipeline buildout cycle remains a durable demand engine for high-amperage, constant-voltage engine-driven platforms that can deliver repeatable arc stability for automated girth welding over multi-year project timelines. The INGAA Foundation’s long-range outlook for North America highlights around 140,000 miles of new gas transmission and gathering capacity additions through 2052, which sustains a baseline of right-of-way work that depends on mobile welding power at every spread. Recent activity tallies track tens of billions of dollars in active and proposed projects, with examples that include greenfield routes designed to move Permian volumes to Gulf Coast egress and Canadian capacity expansions to support regional demand centers. The construction cadence brings recurring needs for welding systems that handle preheats, bevel tolerances, and strict procedure control in variable environmental conditions. Project timing remains sensitive to midstream economics and downstream offtake conditions, which can shift start dates but rarely eliminate the structural need for on-site welding power in the build phase. Equipment planners who standardize on rugged high-output models with automation-ready duty cycles and auxiliary power headroom protect utilization across thick-wall and long-duration joints in this pipeline backlog context[1]Industrial Info Resources, “Trade Group Calls for 140,000 Miles of New Natural Gas Pipelines,” Industrial Info, industrialinfo.com.

Growing Construction Activity in Remote and Rural Areas

Workloads tied to data centre campuses, renewable generation, and corridor infrastructure continue to expand and are shifting more activity into locations where the grid is weak or unavailable during early phases. In the United States, 2026 planning documents point to modest overall start growth, with private office construction dominated by hyperscale data centers that demand high electrical capacity and long construction sequences, which keep welding crews busy across steel frames, racks, and auxiliary structures. Engine-driven welders support this motion because they can power tools, air compressors, and lighting while maintaining stable arcs away from mains power. Contractors balance deployment by emphasizing payload-optimized all-in-one systems on service trucks to cut trips and reduce setup time, which becomes more valuable on large, dispersed sites. Input costs, tariffs, and permitting have extended some timelines, yet the requirement to build out power-hungry facilities in dispersed locations favors mobile platforms for both structural and MRO welding scopes. Contractors that link engine-driven welder performance data to scheduling and labor allocation gain utilization insight and contain fuel overhead on remote work packages.

Growth in Mobile Welding and Maintenance Services

Service-truck platforms are moving toward integrated power solutions that combine welding output, air compression, and auxiliary generation in a single unit, which frees payload and simplifies upfits. Recent launches in hydraulically driven all-in-one categories highlight weight savings up to 400 pounds and footprint reductions of nearly half compared to legacy separate units, which lets fleets carry more consumables or tools per trip. Those integration gains map to service KPIs where fewer trips and faster setup translate into more billable work per day. Rental providers are also standardizing telematics that log fuel burn and arc-on hours to formalize utilization-based pricing and maintenance planning, which in turn pressures OEMs to embed communication modules and data hooks at the controller level. As service organizations consolidate inventory around multiprocess platforms, they increase first-time-fix rates because one system can tackle steel, stainless, and aluminum jobs without cabling changes. That dynamic continues to push demand for versatile engine-driven welders that anchor field productivity in the engine-driven welders market.

Increasing Military and Defense Field Operations Requirements

Defense shipbuilding, depot maintenance, and field repairs require a mobile welding capability that fits within strict safety and quality systems while surviving harsh duty cycles. Current national plans elevate naval force structure goals over multi-decade horizons, which have second-order effects on welding workloads at yards and on auxiliary systems that need repair and retrofit between deployments. Workforce development initiatives that emphasize welding and precision fabrication skills are in place to mitigate shortages across defense supply chains, which supports a shift toward equipment with easier setup, remote control, and digital documentation. Procurement pathways prioritize compliant platforms with proven reliability, clear maintenance regimes, and traceable performance data. Expeditionary units and shipboard teams also benefit from compact, integrated systems that combine welding with compressed air and power generation, which reduces the count of separate devices that must be fueled and maintained. That mix of quality, portability, and integration is strengthening the case for premium fleets in the engine-driven welders market that can deliver repeatable results under defense standards.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Emission Regulations Restricting Usage in Enclosed Spaces | -0.8% | California, EU Stage V regions, regulated underground and confined sites | Short term (≤ 2 years) |

| High Fuel Consumption and Operational Cost | -0.6% | Global, acute where subsidies are removed or carbon pricing applies | Medium term (2–4 years) |

| Frequent Maintenance Requirements and Downtime | -0.4% | APAC and Africa where OEM service networks are sparse | Long term (≥ 4 years) |

| Noise Pollution and Operator Discomfort | -0.3% | Urban construction zones in North America and Western Europe, dense Asia city cores | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Emission Regulations Restricting Usage in Enclosed Spaces

Toxic air contaminant designations for several welding-related metals limit unvented engine operation in enclosed spaces, which has narrowed diesel use in tight indoor environments. In regulated jurisdictions, emission standards drive the adoption of aftertreatment and periodic regeneration cycles on diesel engines, adding maintenance steps and affecting scheduling on long shifts. Owners address these constraints with LPG/CNG alternatives in some settings and with battery-hybrid systems that supply arc power without continuous engine exhaust. Site rules in underground work and confined spaces have also accelerated interest in equipment with lower tailpipe emissions and smaller footprints. Organizations that standardize safe ventilation and fume extraction and match equipment to air-quality requirements maintain compliance while preserving productivity. This pattern is reinforcing a mixed-technology toolbox within the engine-driven welders market[2]California Air Resources Board, “Welding Emissions Activities,” California Air Resources Board, ww2.arb.ca.gov.

High Fuel Consumption and Operational Cost

Fuel costs and engine maintenance outlays remain leading budget items for owners who use engine-driven welders on intermittent duty. Published specifications for diesel units in the mid-output class show steady fuel draw under continuous welding load, which is economical at high utilization but becomes harder to justify for seasonal or low-hour applications. As more regions reduce fuel subsidies or expand carbon pricing, operators are reassessing the balance between diesel, LPG/CNG, and hybrid options based on local refueling access and work mix. Interest in dual-fuel retrofits has increased because they retain diesel torque characteristics while enabling cleaner operation in certain environments, yet these kits add several thousand dollars per machine and require reliable LPG access to realize the benefits. Fleet operators that implement telematics-based idle control and preventive maintenance scheduling can cut unnecessary fuel burn and extend service intervals across their fleets. That combination of technology and maintenance discipline helps contain the total cost of ownership in the engine-driven welders market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power Output: Stratification Mirrors Application Intensity

The 101–300 ampere class captured 44.67% of 2025 revenue and remains the workhorse for pipeline crews and light-to-medium structural fabrication across dispersed job sites. These units balance portability with enough output headroom to run common electrodes and to power auxiliary tools through onboard generators, which keeps small teams productive in the field. Buyers select models with stable arc characteristics, strong duty cycles, and easy cable management to handle out-of-position work on steels with variable surface conditions. Companies that deploy these machines at scale often train on AWS structural and pipeline codes so that equipment capability translates into consistent, code-compliant welds. The appeal of this band is its flexibility, which covers a wide swath of use cases while keeping total truck payload in check for service vehicles in the engine-driven welders market.

Above 500 amperes, units are projected to grow at 5.21% through 2031 as heavy fabrication and shipyards automate thick-plate welding and as megaprojects in concrete and steel require higher deposition rates. The value proposition at the high end is sustained output under demanding duty cycles with a footprint that still allows truck or skid mounting, so teams can bring industrial-grade capability to large field assemblies. Users also value the ability to power air-arc gouging and to run larger wire diameters with stable spray transfer, which reduces pass counts. Several integrated models combine welding, compressed air, and auxiliary power to simplify upfits, reflecting the shift to single-chassis solutions that save payload and bed space. That platform consolidation reduces equipment sprawl and speeds setup for crews tasked with diverse steelwork on a given day in the engine-driven welders market[3]Lincoln Electric, “Ranger 330MPX Engine Drive,” Lincoln Electric, lincolnelectric.com.

By Fuel Type: Diesel Dominance Faces Low-Emission Disruption

Diesel powertrains held 67.81% of global sales in 2025 on the strength of durability, fuel efficiency under load, and the ability to run long hours on remote sites without grid support. Pipeline and heavy construction contractors prefer diesel because of robust torque at low RPM and safe handling characteristics on Tier 1 sites, which lowers hazards during refueling. Serviceability is also a differentiator, with mature parts networks and long engine lifecycles when maintenance is consistent and aligned to duty cycles. As ESG policies and local emission constraints tighten, fleet owners are piloting dual-fuel kits that allow LPG blending on appropriate jobs to achieve cleaner operation without losing continuous-duty power. That hybridized approach, paired with idle management and telematics-driven maintenance, allows owners to control costs while meeting site rules in the engine-driven welders market.

LPG/CNG alternatives are projected to expand at 5.78% per year, lifting their role in regulated indoor and urban applications where air-quality limits are tight. Owners adopt these solutions to reduce nitrogen oxide and particulate output and to gain access to sites that restrict diesel engines in enclosed areas. Gasoline continues to serve entry-level and light-duty use where purchase price and low weight matter more than long-hour efficiency, especially for intermittent repair and farm applications. Hybrid configurations that pair engines with batteries are emerging to bridge the gap between clean operation and long shifts, with compact battery-first models already serving certain confined or power-limited environments. As refueling networks and charging infrastructure mature, hybrid and alternative systems will continue to supplement diesel where rules and duty cycles permit in the engine-driven welders market.

By Welding Process: Stick Dominates, Multi-Process Expands

Stick welding retained 56.32% of 2025 demand because it tolerates surface contaminants, functions in wind or rain with minimal shielding complexity, and suits a wide range of joint positions on structural steel and pipe. Field crews favor a stick for repair and fit-up tasks and for pipeline work where procedures specify particular electrodes and heat inputs. The process also wins on simplicity and portability, which is valued when jobs are dispersed, and schedule pressure is high. Welders switch to gas-shielded processes where deposition rates and appearance requirements justify it, particularly on repetitive production work. That mix keeps sticking as the baseline while other processes expand in targeted applications within the engine-driven welders market.

Advanced multiprocess platforms are projected to grow 6.23% per year as contractors push for single-tool flexibility that can handle stick, MIG, TIG, flux-cored, and air-carbon arc gouging without cable swaps. Integrated platforms with on-board air and auxiliary power address field realities by enabling a technician to cut, prep, and weld without hauling multiple standalone units. That flexibility increases first-time-fix rates and simplifies truck layouts, which supports higher daily productivity. Digital controls with remote voltage or wire feed adjustment at the feeder further reduce walk time and improve parameter accuracy on long cable runs. Together, these features support mixed-material and mixed-process jobs that define maintenance and project scopes for mobile crews in the engine-driven welders market.

By End-User Industry: Construction Leads, Mining Accelerates

Construction and infrastructure accounted for 31.23% of shipments in 2025, reflecting consistent use across commercial buildings, bridges, utility structures, and large campus builds where on-site steelwork dominates. In 2026, non-residential categories such as data centers display strength even as residential remains mixed, which keeps equipment demand steady for structural, MEP support, and commissioning work. Engine-driven welders provide power redundancy and flexibility when grid connections lag construction phases, especially in rural counties and new corridors. Crews value systems that handle variable thickness and out-of-position work on beams, bracing, and platforms, without complex setup or fragile cabling in outdoor conditions. This profile sustains a leading share for construction uses within the engine-driven welders market.

Mining and quarrying is projected to be the fastest-growing application at 6.47% per year, driven by lithium and copper projects linked to electrification supply chains. Mine sites demand rugged, continuous-duty welders with voltage-reduction devices where site safety rules require them and with proven cooling and filtration for dusty and high-heat conditions. Operators often standardize on diesel units for longevity and for strong torque profiles that hold arc stability for heavy section work. Even as equipment electrification rises inside some mines, engine-driven welders remain essential for field repairs on large machines and for remote infrastructure tasks. Service windows on mines are narrow and expensive, so reliability and quick diagnostics drive purchase decisions in the engine-driven welders market.

Geography Analysis

Asia-Pacific held 48.21% of 2025 revenue on the back of strong manufacturing bases and large public works programs that continue to expand corridors, energy assets, and industrial facilities across diverse climates and terrains. Fabrication tied to shipbuilding, automotive, energy, and large-scale infrastructure sustains regular use of mobile welders for both construction and MRO tasks in areas where temporary power is necessary. The region’s project mix favors equipment that can operate in humid, hot, or high-altitude conditions with stable arcs and reliable auxiliary power. As more owners layer in digital monitoring and remote parameter control, multiprocess platforms with telematics are gaining attention across service fleets. Emission constraints vary by city and country, which is prompting selective uptake of LPG and hybrid units for indoor or restricted sites, while diesel remains dominant on open-air projects in the engine-driven welders market.

North America shows stable demand patterns supported by structural steel, energy infrastructure, and expanding data center activity that relies on mobile power at greenfield sites. Contractors respond to labor shortages by investing in integrated welders that compress setup time and allow smaller crews to cover more tasks per shift. Tier 4 Final rules and local toxic air contaminant classifications limit diesel use in enclosed spaces, which lifts interest in LPG and hybrid options for indoor work or night shifts near residences. Field repair and utility work continue to favor robust diesel units for long-hour use in remote or weather-exposed settings. As telematics gain traction across rental and fleet operators, utilization tracking is influencing fleet renewal choices in the engine-driven welders market.

The Middle East and Africa region is projected to grow fastest at 7.21% as countries advance megaprojects, expand energy and petrochemical capacity, and modernize utility networks. Harsh environmental conditions and long distances between depots raise the value of ruggedness, simple maintenance access, and reliable local parts channels. Owners often standardize on global brands that maintain distributor networks with warranty coverage and consumable pipelines to reduce downtime risk. Large fabrication yards and field teams benefit from high-output multiprocess units that share components across fleets, which simplifies stocking and training. The long project horizons and capital intensity of infrastructure and energy investments continue to underpin equipment needs across heavy-duty and service-truck applications in the engine-driven welders market.

Competitive Landscape

The competitive field features global incumbents with broad portfolios and deep service networks alongside regional specialists and rental channel influence on feature roadmaps. Integration is a defining theme, as leading suppliers are expanding single-chassis offerings that combine welding output, compressed air, and auxiliary generation to help fleets save payload and reduce equipment count per truck. Mergers and acquisitions are reshaping capabilities in mobile power and automation, reinforcing the one-stop positioning some brands now pursue for service-truck upfits. Rental firms are using telematics to track utilization and fuel efficiency and are working with OEMs to embed connectivity in controllers so they can align lease terms to measured performance. The result is a feedback loop where real-world duty-cycle data informs hardware updates and software features across next-generation models in the engine-driven welders market.

Strategic moves over the last two years underscore a shift toward mobility, digital control, and clean-operation flexibility. One OEM integrated battery-first portable systems into its lineup to serve confined or power-limited environments where engine exhaust is restricted, while retaining hybrid modes that can supplement wall power when available. Another focused on remote parameter adjustment and cloud-connected workflow tools that reduce walk time on long cable runs and improve consistency across large job sites. These products and software steps raise switching costs by tying outcomes to data and remote control, which mirrors moves in adjacent industrial automation domains. The common aim is to help owners extract more productive hours per day while complying with local emissions and noise requirements in the engine-driven welders market.

Customers are also standardizing training and safety practices to match equipment capabilities, which keeps uptime high and reduces rework that hurts schedules and margins. Aftermarket support and extended service intervals figure prominently in buying decisions because distributed work programs depend on predictable maintenance cycles. Global suppliers that backstop fleets with regional parts availability, service training, and digital diagnostics retain an advantage when owners compare the lifetime cost of ownership. At the same time, emerging entrants are staking positions in fast-growing niches such as battery-first rail welding and compact hybrid units for specialty trades. Competitive intensity will remain high as rental channels steer feature roadmaps through telematics data and as OEMs race to integrate more value into mobile welding platforms in the engine-driven welders market.

Engine Driven Welders Industry Leaders

Lincoln Electric Holdings Inc.

Miller Electric Mfg LLC (ITW)

ESAB Corp.

Denyo Co., Ltd.

Multiquip Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Titan Wind Energy contracted ESAB for welding and handling equipment for its EUR 300 million XXL monopile manufacturing facility in Cuxhaven, Germany, which will produce 14-meter-diameter, 140-meter-long offshore wind foundations weighing 3,500 tonnes, with an annual capacity of 200 XXL monopiles or approximately 350,000 tonnes of steel foundations. The factory will employ over 600 workers and feature high-automation welding systems.

- January 2026: Enbridge's CAD 4 billion Sunrise Expansion Program in British Columbia received a recommendation for approval from the Canadian Energy Regulator, encompassing 11 new natural gas pipeline loops totaling 139 kilometers, two new compressor stations, and infrastructure upgrades. The project is estimated to create over 2,500 jobs during peak construction.

- September 2025: Harland & Wolff shipyard in Belfast completed the Factory Acceptance Test of advanced robotic welding equipment for the UK's Fleet Solid Support programme, with Pemamek's PEMA Vision Robotic Welding Portals forming the core of a new automated panel line. Navantia UK is investing £115 million across four UK yards, securing over 1,000 jobs.

- July 2024: Lincoln Electric acquired Vanair Manufacturing, LLC, a specialist in vehicle-mounted compressors, generators, welders, hydraulics, chargers/boosters, and electrified power equipment with around USD 100 million in annual revenue.

Global Engine Driven Welders Market Report Scope

The Engine Driven Welders Market Report is Segmented by Power Output (0–100 A, 101 – 300 A, and more), by Fuel Type (Gasoline, Diesel, and more), by Welding Process (Stick Welding (SMAW), MIG Welding (GMAW) and more), by End-User Industry (Construction & Infrastructure, and more), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| 0 – 100 A |

| 101 – 300 A |

| 301 – 500 A |

| Above 500 A |

| Gasoline |

| Diesel |

| LPG / CNG |

| Alternative & Hybrid Systems |

| Stick Welding (SMAW) |

| MIG Welding (GMAW) |

| TIG Welding (GTAW) |

| Advanced Multi-Process (Pulse-MIG, Gouging) |

| Construction & Infrastructure |

| Oil & Gas / Pipeline |

| Mining & Quarrying |

| Shipbuilding & Marine |

| Power Generation & Utilities |

| Automotive and General Manufacturing |

| General Maintenance & Repair |

| Others (Agriculture & Farming, Rental & Leasing Companies, etc.) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Peru | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Turkey | |

| Egypt | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Power Output | 0 – 100 A | |

| 101 – 300 A | ||

| 301 – 500 A | ||

| Above 500 A | ||

| By Fuel Type | Gasoline | |

| Diesel | ||

| LPG / CNG | ||

| Alternative & Hybrid Systems | ||

| By Welding Process | Stick Welding (SMAW) | |

| MIG Welding (GMAW) | ||

| TIG Welding (GTAW) | ||

| Advanced Multi-Process (Pulse-MIG, Gouging) | ||

| By End-User Industry | Construction & Infrastructure | |

| Oil & Gas / Pipeline | ||

| Mining & Quarrying | ||

| Shipbuilding & Marine | ||

| Power Generation & Utilities | ||

| Automotive and General Manufacturing | ||

| General Maintenance & Repair | ||

| Others (Agriculture & Farming, Rental & Leasing Companies, etc.) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Peru | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Kuwait | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size and outlook for the engine-driven welders market?

The engine-driven welders market size was USD 1.27 billion in 2025 and is projected to reach USD 1.69 billion by 2031 at a 4.91% CAGR over 2026-2031. This reflects steady demand across construction, energy, and field service applications.

Which fuel type leads demand, and what is changing?

Diesel platforms led with 67.81% of 2025 sales, and owners are piloting LPG/CNG and hybrid configurations to meet stricter emission rules, especially in enclosed or urban sites where air-quality limits apply.

Which output class is most popular and where is growth fastest?

The 101–300 ampere class led with 44.67% share in 2025 across pipeline and structural work, while units above 500 amperes are projected to grow at 5.21% through 2031 on heavy fabrication and shipyard demand.

What are the standout use cases driving purchases in 2026?

Structural steel on data center and infrastructure projects, remote pipeline spreads, and mining maintenance drive purchases, with integrated single-chassis systems gaining traction for service trucks in dispersed work.

How are regulations shaping equipment choices on job sites?

Toxic air contaminant rules and local noise limits restrict diesel in enclosed spaces and dense urban areas, which increases adoption of LPG and hybrid solutions and pushes OEMs to improve sound attenuation and telematics.

Which region leads demand, and which is growing fastest?

Asia-Pacific led with 48.21% of 2025 revenue thanks to broad industrial and infrastructure activity, while the Middle East and Africa are projected to grow fastest at 7.21% through 2031 as megaprojects progress.

Page last updated on: