Nickel Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

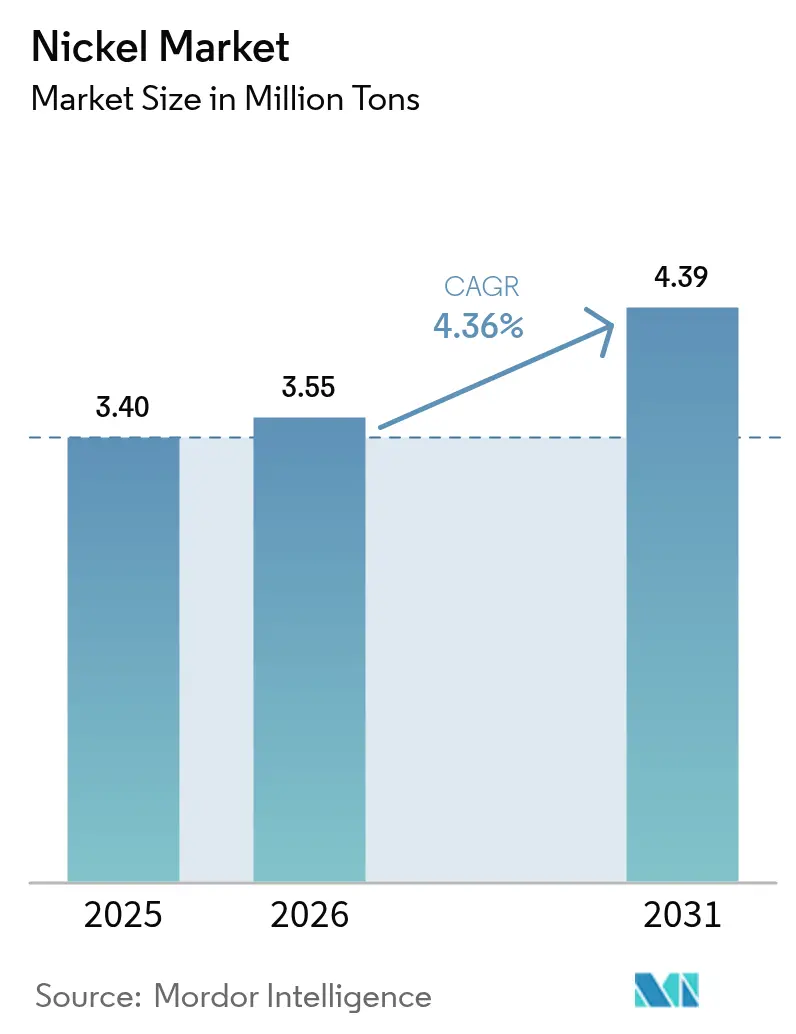

| Market Volume (2026) | 3.55 Million tons |

| Market Volume (2031) | 4.39 Million tons |

| Growth Rate (2026 - 2031) | 4.36% CAGR |

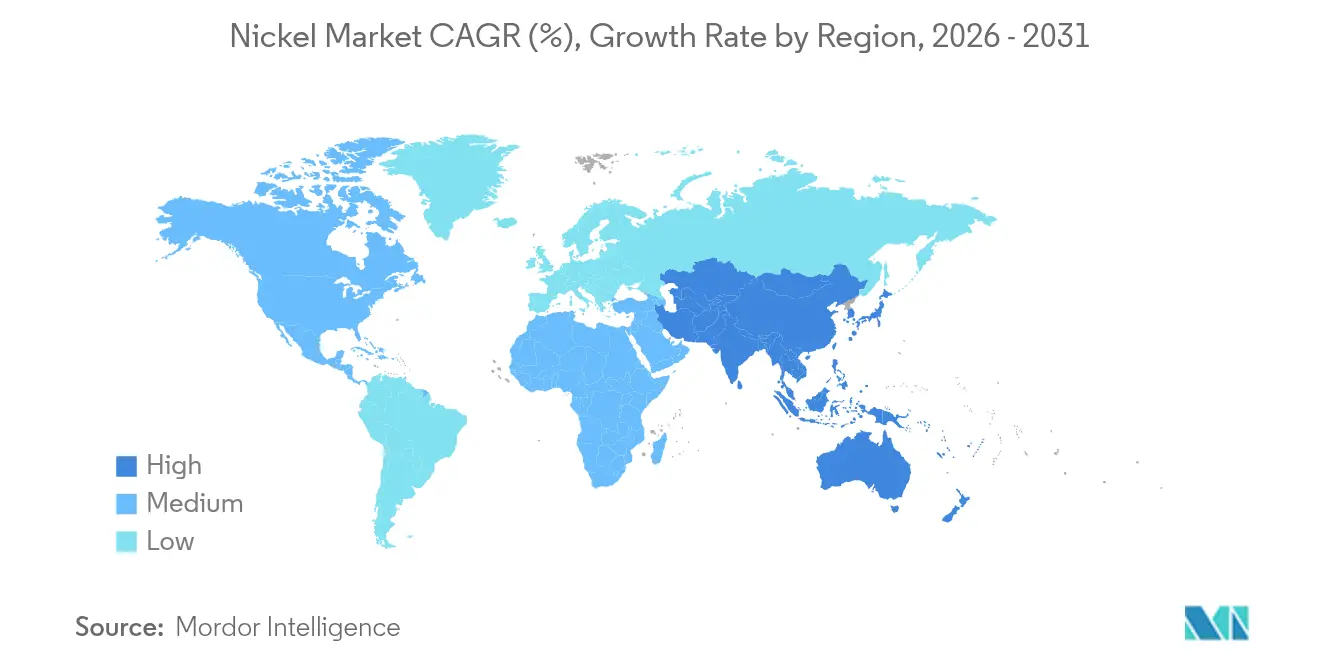

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nickel Market Analysis by Mordor Intelligence

The Nickel Market size was valued at 3.40 million tons in 2025 and estimated to grow from 3.55 million tons in 2026 to reach 4.39 million tons by 2031, at a CAGR of 4.36% during the forecast period (2026-2031). Surging stainless-steel production in China and Indonesia, sustained investment in battery-grade refining, and mounting preference for low-carbon supply chains underpin volume growth, even as persistent Class II oversupply weighs on benchmark prices. Indonesia’s cost-advantaged nickel pig iron and high-pressure acid-leach hubs now account for more than 60% of the supply, reshaping trade flows and accelerating vertical integration into Chinese stainless-steel complexes. Battery-sector demand, though still a minority share, drives strategic capital allocation toward Class I projects capable of supplying electric-vehicle cathodes amid a simultaneous surplus of lower-grade material and deficit of battery-ready feedstock. Policy risk remains elevated as the Philippines considers export restrictions modeled on Indonesia’s 2014 ore ban, while deep-sea nodule projects emerge as a long-term wildcard for the nickel market.

Key Report Takeaways

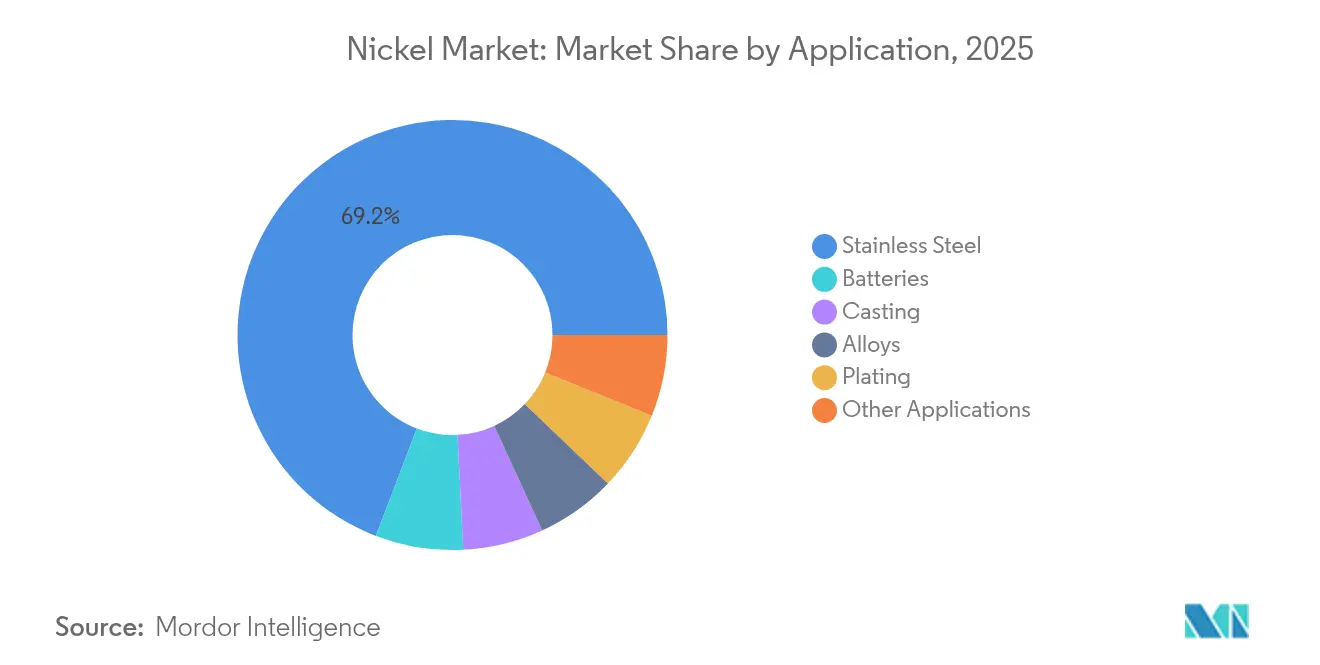

- By application, stainless steel commanded 69.20% of the nickel market share in 2025; batteries are forecast to expand at a 4.96% CAGR through 2031.

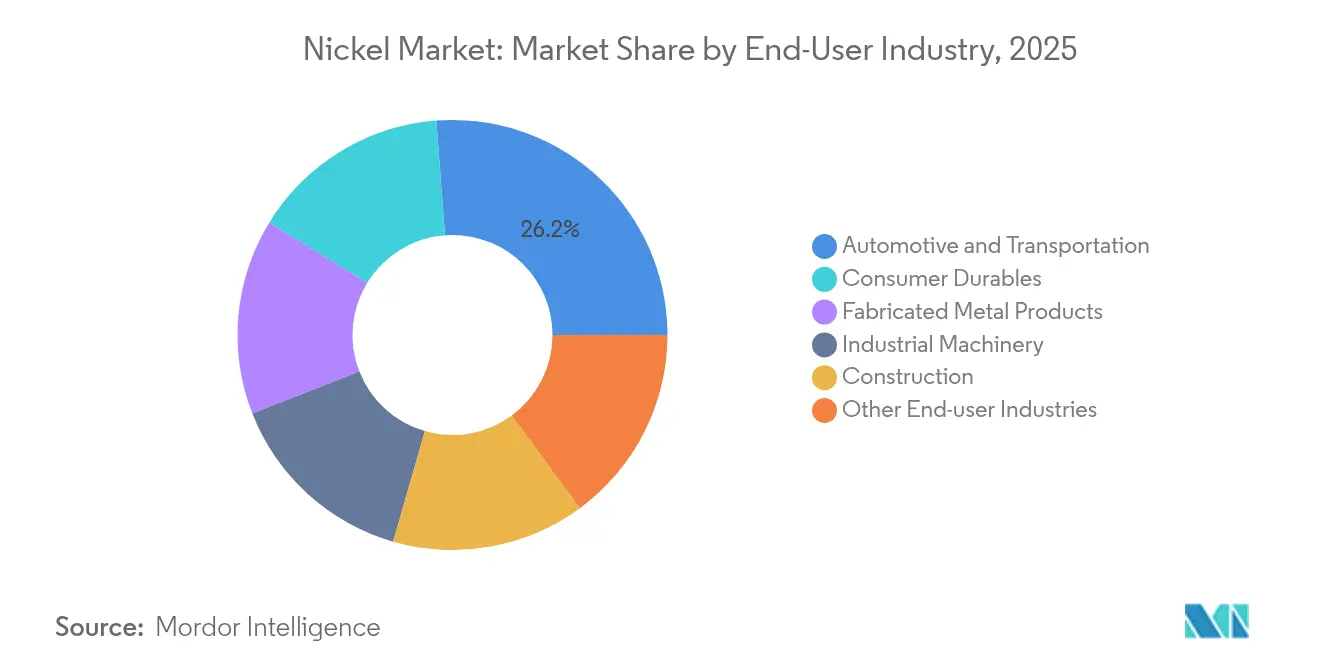

- By end-user industry, automotive and transportation held 26.20% of nickel market in 2025, whereas consumer durables recorded the fastest 4.74% CAGR to 2031.

- By geography, the Asia-Pacific region accounted for 71.10% of the nickel market size in 2025 and is expected to grow at a regional-leading 5.10% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Nickel Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging stainless-steel output in China and Indonesia | +1.5% | Asia-Pacific core, global spillover | Medium term (2-4 years) |

| Rapid build-out of EV battery-grade nickel-sulfate refineries | +0.8% | Global, concentrated in North America and the Asia-Pacific | Long term (≥ 4 years) |

| Green-nickel premiums and OEM supply-chain localization | +0.7% | North America and the EU, expanding to APAC | Medium term (2-4 years) |

| Class I deficit despite overall surplus | +0.6% | Global, acute in battery chains | Short term (≤ 2 years) |

| Multiple emerging deep-sea nodule projects | +0.5% | Global impact from Pacific operations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Stainless-Steel Output in China and Indonesia

Chinese crude stainless-steel production rose 10.6% year-over-year in Q1 2025, reaching 3.58 million tons in March alone. Higher output lifts import demand for nickel-bearing feedstock, while Indonesian nickel pig iron growth creates an integrated corridor that cushions mills against price swings. This symbiosis ensures raw material availability for the nickel market and enables Chinese-Indonesian ventures to operate during downturns that sideline higher-cost Western mines. Yet, the concentration amplifies systemic risk because any disruption—whether policy, weather, or logistics—could quickly tighten global supply.

Rapid Build-Out of EV Battery-Grade Nickel-Sulfate Refineries

Vale finalized the Voisey’s Bay expansion in December 2024, adding 45,000 tons of annual capacity with full ramp-up slated for H2 2026[1]Vale Investor Relations, “Voisey’s Bay Mine Expansion Update,” vale.com. Canada Nickel Company’s Crawford project aims to achieve first output by the end of 2027, projecting 1.6 million tons over a 41-year life. Although BASF-Eramet canceled a USD 2.6 billion Indonesian venture, new refinery announcements in Canada and the United States underscore the nickel market's need for localized, battery-ready feedstock to serve regional gigafactories. Producers aim to blend elevated ESG credentials with carbon-capture technology to unlock potential tax credits and price premiums.

Green-Nickel Premiums and OEM Supply-Chain Localization

Major automakers are now specifying lifecycle-carbon thresholds for battery metals, prompting miners to power their operations with renewables and pilot traceability technology. While the London Metal Exchange dismissed a segregated “clean nickel” contract in 2024, bilateral deals between OEMs and miners such as BHP and Wyloo are surfacing, signaling that sustainability premiums will likely emerge off-exchange. Investor coalitions managing USD 2.7 trillion have demanded deforestation-free nickel supply, accelerating the shift toward localized sourcing in the nickel industry.

Class I Nickel Deficit Despite Overall Surplus

The International Nickel Study Group projects an overall surplus of 198,000 tons for 2025, yet Class I material required for NMC and NCA cathodes remains in short supply[2]. Vale realized only USD 15,800 per ton in Q2 2025, down 15.2% year-over-year, highlighting how Class I producers face margin compression as Indonesian supply sets the floor. Refiners capable of upgrading lower-grade feed now capture higher value, reinforcing investment in hydrometallurgical and conversion routes within the nickel market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Class II oversupply drags benchmark pricing | -0.9% | Global, severe in Asia-Pacific | Short term (≤ 2 years) |

| LFP and sodium-ion battery chemistry adoption | -0.7% | Led by China, expanding globally | Medium term (2-4 years) |

| ESG backlash versus Indonesian HPAL and NPI projects | -0.7% | Indonesia-centric, global chains | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Class II Oversupply Drags Benchmark Pricing

Indonesian nickel pig iron surged from 6% of global supply in 2018 to more than 50% in 2025, depressing prices and forcing higher-cost Western mines into care and maintenance. BHP suspended operations at its Kwinana refinery, Kalgoorlie smelter, Mt Keith, and Leinster mines until 2027, affecting approximately 1,600 workers. Glencore’s 9% decline in 2024 output and Koniambo’s shutdown further highlight pressure on legacy assets as the nickel market adjusts to the new cost leader.

LFP and Sodium-Ion Battery Chemistry Adoption

Lithium-iron-phosphate batteries have increased their share, and Chinese cell makers, such as CATL, are piloting sodium-ion packs that eliminate nickel. Cost-driven OEMs select chemistries with lower material expense for entry-level EVs and stationary storage, capping upside for nickel-rich cathodes. The premium vehicle and aerospace segments still require nickel-based high-energy cells; however, the broader adoption of LFP and sodium-ion batteries dilutes the long-term demand in the nickel market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Steel Leadership Meets Battery Momentum

Stainless-steel production retained 69.20% of the nickel market in 2025, reaffirming the metal’s role in corrosion-resistant alloys across construction, consumer, and industrial spheres. Chinese mills boosted output by 10.6% in early 2025, underpinning bulk demand even as economic growth moderates. Casting and alloy segments serve aerospace and heat-resistant parts with stable but lower volumes, while plating applications extract premium margins for decorative finishes.

The batteries segment, although accounting for a smaller share, is the fastest-growing slice with a 4.96% CAGR through 2031. Demand stems from electric-vehicle packs and grid-scale storage, driving investments such as Vale’s Voisey’s Bay upgrade and Canada Nickel’s carbon-capture-enabled refinery. The nickel market size for batteries is forecast to reach 0.61 million tons by 2031, doubling its 2024 baseline. LFP and sodium-ion adoption constrain the upside, yet high-energy cathodes in premium vehicles continue to favor nickel-rich chemistries that command Class I premiums.

By End-User Industry: Automotive Weight with Consumer Upside

Automotive and transportation captured 26.20% of demand in 2025, spanning stainless-steel exhausts, chassis components, and surging battery requirements. The shift from internal-combustion to electrified drivetrains creates a complex demand curve: stainless-steel content plateaus, but nickel-rich cathodes elevate Class I utilization, shaping future consumption trends in the nickel market.

Consumer durables, including refrigerators, washing machines, and kitchen appliances, are projected to post a 4.74% CAGR through 2031, benefiting from replacement cycles in North America and Europe. Stainless-steel aesthetic preferences and rising disposable income sustain volume growth. Fabricated metal products, construction, and industrial machinery deliver steady demand anchored in infrastructure and energy projects, while aerospace and marine applications rely on specialized high-temperature alloys with limited substitution pathways, reinforcing a stable pull from the nickel market.

Geography Analysis

Asia-Pacific governed 71.10% of global nickel market demand in 2025 and is projected to expand at a 5.10% CAGR through 2031. China’s stainless-steel surge and Indonesia’s vertically integrated supply chain define regional momentum, while possible Philippine ore-export restrictions could further concentrate processing inside ASEAN. Japan and South Korea maintain advanced alloy production, and India’s industrial base steadily lifts consumption.

North America intensifies efforts to localize supply, led by Canada Nickel’s Crawford project and Vale’s Voisey’s Bay expansion. The nickel market size in North America is forecast to grow as gigafactory pipelines in the United States demand Class I feedstock compliant with the Inflation Reduction Act sourcing rules. Mexico’s proximity to U.S. auto plants offers logistical advantages, though tariff volatility injects uncertainty.

Europe balances stringent ESG standards with cost pressures. Automakers seek certified green metal, encouraging investment in low-carbon refining within the bloc and in neighboring Norway. South America, with Brazil holding around 12% of global reserves, attracts capital despite logistics challenges, evidenced by Brazilian Nickel’s Piauí project. The Middle-East and Africa remain emergent but attract Gulf investment funds seeking exposure to future-oriented minerals.

Competitive Landscape

Global supply is moderately fragmented. Product differentiation intensifies around Class I purity and ESG credentials. Producers able to upgrade nickel pig iron or high-pressure leach intermediates into battery-grade sulfate capture premiums that offset depressed benchmark prices. Deep-sea mining entrants like The Metals Company could reshape competitive dynamics if commercial approvals proceed, adding unconventional supply with claimed lower environmental footprints. Strategic partnerships proliferate: OEMs sign long-term offtakes to secure localized supply, and miners explore carbon-capture credits to enhance margins. The competitive field thus bifurcates into cost-driven Class II producers serving stainless-steel flows and premium Class I suppliers aligning with battery chains, each optimizing distinct value propositions within the nickel market.

Nickel Industry Leaders

TSINGSHAN HOLDING GROUP

Vale

Jinchuan Group International Resources Co., Ltd.

Norilsk Nickel

BHP

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: BHP sold its 17% stake in the Kabanga Nickel Project to Lifezone Metals, citing market uncertainty and capital allocation priorities. The Kabanga project, with pre-production capital costs of USD 942 million, is expected to produce 50,000 metric tons of nickel annually upon full operationalization. The exit reflects BHP’s cautious stance on greenfield nickel investments amid oversupply concerns, particularly from Indonesia.

- February 2025: Anglo American announced it to sell its nickel business to MMG Singapore Resources for up to USD 500 million, as part of its strategy to streamline its portfolio. The deal includes two operating ferronickel assets in Brazil—Barro Alto and Codemin—and two greenfield projects, Jacaré and Morro Sem Boné.

Global Nickel Market Report Scope

Nickel is a chemical element and a transition metal, mostly used for high-grade steel manufacturing. The nickel market is segmented by application and geography. By application, the market is segmented into stainless steel, alloys, plating, casting, batteries, and other applications. The report also covers the market size and forecasts for the Nickel market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (kilotons).

| Stainless Steel |

| Casting |

| Alloys |

| Batteries |

| Plating |

| Other Applications |

| Automotive and Transportation |

| Fabricated Metal Products |

| Consumer Durables |

| Construction |

| Industrial Machinery |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Application | Stainless Steel | |

| Casting | ||

| Alloys | ||

| Batteries | ||

| Plating | ||

| Other Applications | ||

| By End-user Industry | Automotive and Transportation | |

| Fabricated Metal Products | ||

| Consumer Durables | ||

| Construction | ||

| Industrial Machinery | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected volume for global nickel industry demand by 2031?

Demand is forecast to reach 4.39 million tons by 2031, up from 3.55 million tons in 2026.

Why does oversupply persist even while battery-grade in nickel industry remains tight?

Class II nickel pig iron floods the market, but Class I material suitable for EV cathodes is in limited supply, creating a simultaneous surplus and deficit.

How significant is Indonesia’s role in supply growth?

Indonesia controls majority of global output through cost-advantaged nickel pig iron and HPAL plants.

Which application in nickel industry segment is growing fastest?

Battery applications are expected to expand at a 4.96% CAGR through 2031, outpacing all other segments.

What ESG trends influence nickel sourcing?

Automakers demand low-carbon, traceable nickel, prompting miners to adopt renewable energy sources and pursue premiums for green nickel.

Are deep-sea nodules a realistic future supply?

Pilot processing has yielded battery-grade sulfate, and commercial approvals are pending, positioning deep-sea nodules as a potential large-scale source after 2030.

Page last updated on: