Europe Welding Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

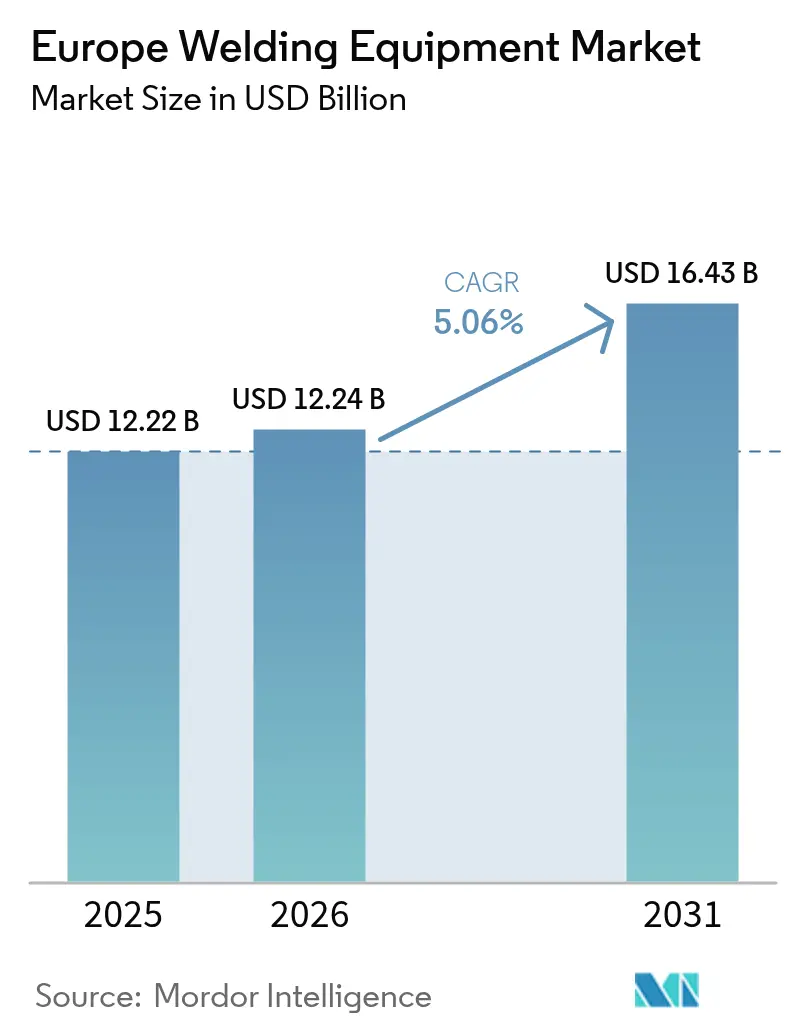

| Base Year Market Size (2025) | USD 12.22 Billion |

| Market Size (2026) | USD 12.24 Billion |

| Market Size (2031) | USD 16.43 Billion |

| Growth Rate (2026 - 2031) | 5.06% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Welding Equipment Market Analysis by Mordor Intelligence

The Europe Welding Equipment Market size is projected to be USD 12.22 billion in 2025, USD 12.24 billion in 2026, and reach USD 16.43 billion by 2031, growing at a CAGR of 5.06% from 2026 to 2031.

The steady expansion of the Europe welding equipment market reflects sustained reshoring of fabrication lines, rapid electric-vehicle gigafactory construction, and public-sector funding for low-carbon infrastructure. These structural forces offset the drag from skilled-labor shortages, high capital costs for lasers and robots, and tighter EU rules on consumable chemistries. Arc welding kept more than half of the Europe welding equipment market in 2025, yet niche laser, soldering, and brazing solutions are scaling in aerospace and battery applications. Across Western Europe, semi-automatic systems remain prevalent among small fabricators, while leading automotive and energy projects are shifting toward fully robotic, data-logged cells.

Key Report Takeaways

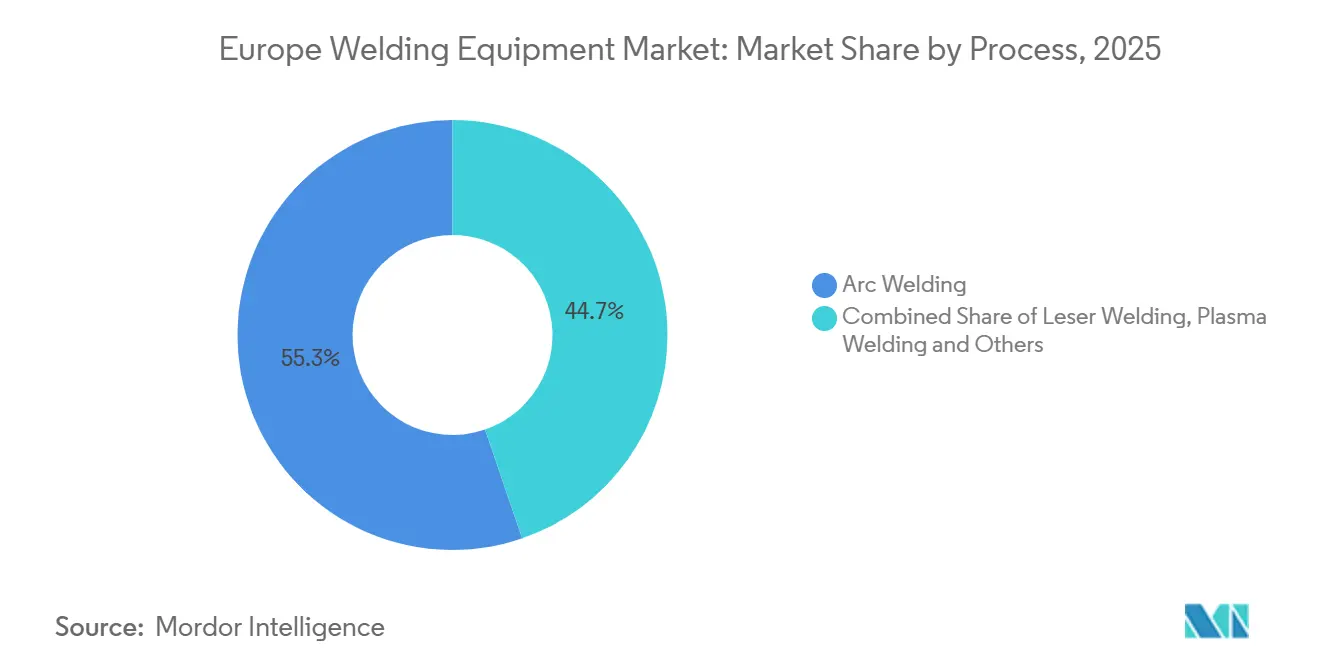

- By process, arc welding led with 55.26% of the Europe welding equipment market share in 2025; specialty soldering and brazing processes are projected to advance at a 7.19% CAGR to 2031.

- By end user, automotive and transportation captured 27.28% of the Europe welding equipment market size in 2025, while the “Others” segment covering aerospace, defense, and maintenance will expand at a 6.95% CAGR through 2031.

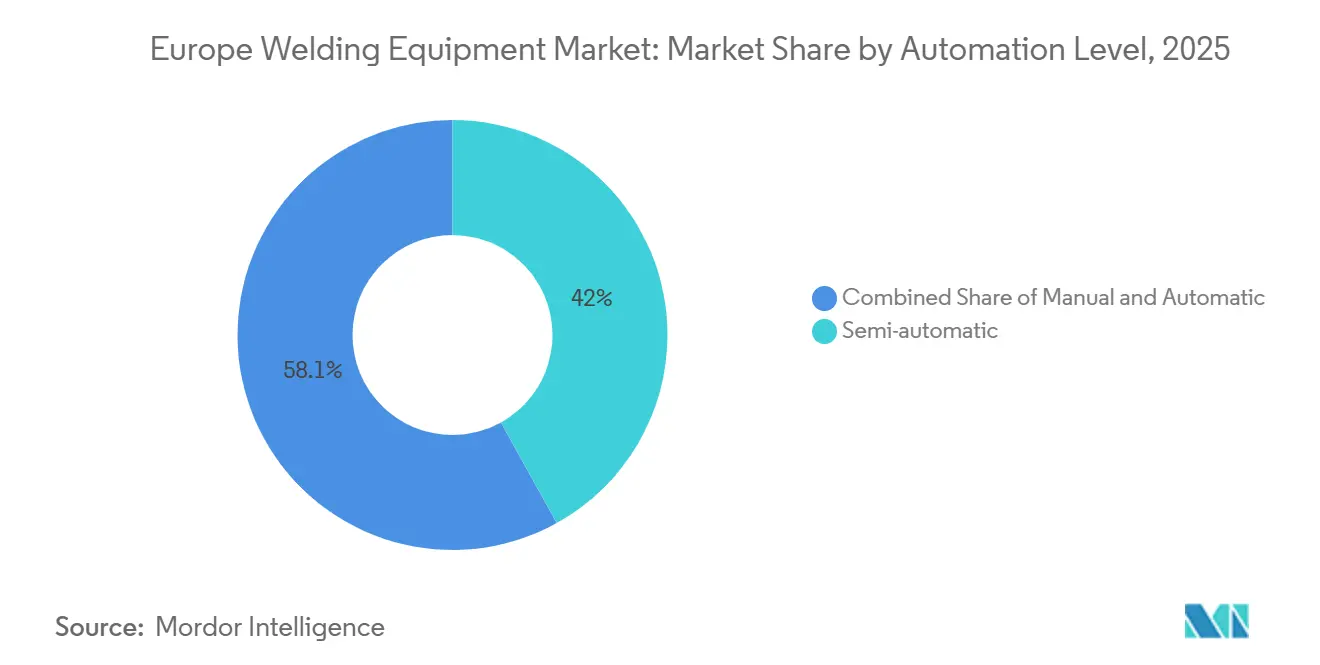

- By automation level, semi-automatic systems held 41.95% revenue in 2025; fully automatic and robotic cells record the fastest growth at a 6.41% CAGR for 2026-2031.

- By geography, Germany accounted for 23.45% of regional sales in 2025, whereas the Rest of Europe bloc is forecast to grow at a 6.10% CAGR, the quickest pace among all sub-regions.

- Lincoln Electric, ESAB, and Fronius together controlled roughly one-third of 2025 revenue; ESAB’s USD 300 million purchase of EWM in June 2025 illustrates ongoing consolidation.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Welding Equipment Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid scale-up of EV gigafactories driving aluminum & battery-pack welding demand | +1.2% | Spain, Germany, France, Hungary, Poland | Short term (≤ 2 years) |

| Automation & robotics penetration across production lines | +1.0% | Germany, Italy, France, Czech Republic | Long term (≥ 4 years) |

| EU Green Deal & REPowerEU-funded hydrogen / grid upgrades | +0.9% | Pan-European | Medium term (2-4 years) |

| Reshoring incentives boosting localized metal-fabrication capacity post-energy crisis | +0.8% | Germany, France, Italy, BENELUX | Medium term (2-4 years) |

| Hand-held fiber-laser welders crossing cost–benefit threshold for SMEs | +0.5% | Germany, Italy, Spain, Poland | Short term (≤ 2 years) |

| Weld-data digital twins enabling Scope-3 emissions audits for OEMs | +0.3% | Germany, France, Sweden, Netherlands | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Scale-Up of EV Gigafactories Driving Aluminum & Battery-Pack Welding Demand

Gigafactory projects inject large, front-loaded orders into the Europe welding equipment market. A USD 4.47 billion cell plant in Spain alone requires more than 120 robotic friction-stir-welding cells worth over USD 100 million. Salzgitter’s battery site added 85 laser stations for copper-to-aluminum joints as of 2025. Peer-reviewed tests confirm servo-controlled machines are essential for additive aluminum tabs, validating premium equipment outlays. Order volumes crest in 2026-2027 and normalize once installed capacity meets vehicle-output plans.

Automation & Robotics Penetration Across European Production Lines

Collaborative robots lifted their share of new welding cells to 18% in 2025, up seven points in three years. EU pilots proved cobots can cut programming time by 60%, letting small batches enter automated flow. Shipbuilding trials with humanoid robots demonstrated 40% faster cycle times in cramped hull sections. Despite clear productivity wins, 54% of shops under 50 staff still weld manually due to capital hurdles, suggesting long-run growth potential as financing solutions mature. The Europe welding equipment market therefore tracks a gradual but durable automation curve.

EU Green Deal & REPowerEU-Funded Hydrogen / Grid Infrastructure Upgrades

REPowerEU channels USD 13.08 billion toward hydrogen pipelines and grid links, stimulating demand for TIG, orbital, and submerged-arc systems. Germany alone targets 10 GW of electrolyzers by 2030, each gigawatt calling for USD 45 million in automated TIG heads. Offshore wind foundations lift orders for high-deposition submerged-arc welders, while regional studies flag certification gaps that funnel extra spending into training and inspection. This program secures a predictable base load for the Europe welding equipment market through 2030.

Reshoring Incentives Boosting Localized Metal-Fabrication Capacity Post-Energy Crisis

European manufacturers accelerated domestic welding investments once 2022-2023 natural-gas prices exposed the hidden costs of Asian supply chains. EU grants of USD 1.31 billion help retrofit brownfield plants with efficient inverters, making the Europe welding equipment market attractive for mid-tier suppliers. EUROFER highlighted a 14% jump in 1H 2025 equipment orders as fabricators retooled for chassis and framework. Subsidy disbursements peak in 2027-2028 before tapering once energy prices stabilize and reshoring pipelines clear. The Europe welding equipment market therefore gains a multi-year tailwind without relying solely on new greenfield complexes.[1]EUROFER, “Economic and Steel Market Outlook 2025-2031,” eurofer.eu

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent shortage of certified welders & trainers despite automation | -0.7% | Germany, UK, France, BENELUX, NORDICS | Long term (≥ 4 years) |

| High capex burden for laser & collaborative robotic systems | -0.6% | Pan-European, acute in Southern and Eastern Europe | Short term (≤ 2 years) |

| Imminent PFAS flux-cored wire restrictions elevating consumable costs | -0.4% | Pan-European, highest impact in Germany, Poland, Czech Republic | Short term (≤ 2 years) |

| Critical raw material (rare-earth laser diode) supply risk under EU CRM Act | -0.3% | Germany, France, Italy (laser-equipment hubs) | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Persistent Shortage of Certified Welders & Trainers Despite Automation

Workforce aging leaves Europe short of 400,000 certified welders by 2030. Annual certifications cover barely 70% of retirements, and Brexit curtails labor inflows into the UK. Vocational schools struggle to replace instructors; two-thirds are already over 55. EU initiatives aim to double female participation but lifted the share only slightly in year one. Each new robot still needs 0.6 skilled staff for set-up and QA, so labor scarcity remains a structural drag on the Europe welding equipment market.[2]European Welding Federation, “Workforce Study 2024,” ewf.be

High Capex Burden for Laser and Collaborative Robotic Systems

Turnkey cobot cells cost USD 196,000-272,000, equivalent to three years of a skilled welder’s wage, stretching SME budgets. One supplier reported a 9.5% revenue drop in 2025 as customers delayed automation buys. Bank lending for machinery shrank 6% in 2024, the first pullback since 2020, while subscription models reached only 15% penetration. Southern and Eastern European shops on sub-6% EBITDA margins feel the pinch most. Until interest rates fall or leasing gains traction, the Europe welding equipment market faces a capex brake.[3]European Central Bank, “Survey on SME Access to Finance 2024,” ecb.europa.eu

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Process: Arc Welding Retains Primacy, Specialized Techniques Accelerate

Arc welding commanded 55.26% of the Europe welding equipment market in 2025, underscoring its versatility in structural steel, shipbuilding, and heavy machinery. Deposition rates of 3-5 kg per hour and deep penetration keep MIG/MAG and TIG firmly in place across thick-section work. Yet specialized soldering and brazing are expanding at a 7.19% CAGR to 2031 as miniaturized electronics and precision turbine repairs demand tight thermal control. Resistance spot welding remains essential for automotive bodies, though new zinc-coated steels push current and force envelopes higher, adding USD 16,000 in servo controls to each gun. Premium laser heads priced at USD 320,000-420,000 are winning battery-tab contracts after trials cut electrical resistance by 12%, but they still represent a minority of total process spend.

Growth patterns split along value lines. Commodity construction sticks with arc and resistance methods that balance cost with adequate quality, locking in bulk orders for inverter power sources. High-value aerospace and EV modules, however, gravitate to laser, soldering, or brazing for narrow heat-affected zones and metallurgical integrity. Plasma welding holds at roughly 3% share for niche titanium and pharma tubing applications, while gas welding recedes to legacy maintenance. The Europe welding equipment market therefore evolves into a two-tier structure: high-volume arc platforms on one end and precision specialty systems on the other.

By End User: Automotive Dominates, Specialty Sectors Gain Traction

Automotive and transportation absorbed 27.28% of 2025 equipment outlays, reflecting Europe’s dense vehicle and tier-supplier network. Electrification projects now specify friction-stir and laser solutions for aluminum battery cases, pushing integrators toward smarter robotic cells. At the same time, the broad “Others” bucket spanning aerospace, defense, and custom fabrication will outgrow all peers at a 6.95% CAGR. NATO members lifting defense spending drive orders for certified TIG stations on fuselage and hull programs, each requiring stringent documentation and weld-data capture. Construction and infrastructure hold a steady 18-20% share thanks to rail and grid upgrades, while oil and gas stay flat at around 9% as LNG and hydrogen retrofits replace new fossil lines.

The contrast highlights shifting margin pools within the Europe welding equipment market. Car makers negotiate tight discounts, pressuring equipment vendors to justify every feature. Conversely, aerospace and defense prime contracts value reliability and documentation, enabling suppliers to price premium systems with 20-25% gross margins. Service and maintenance revenues also rise as aging fleets of robotic cells need upgrades to meet CSRD data mandates, giving OEMs fresh aftermarket streams beyond initial hardware sales.

By Automation Level: Semi-Automatic Holds Scale, Robots Accelerate

Semi-automatic platforms took 41.95% of revenue in 2025, mirroring Europe’s mosaic of job shops that weld short runs with handheld torches and automated wire feed. However, fully automatic and robotic lines are expanding at a 6.41% CAGR as labor costs climb and OEMs enforce 100% seam inspection. Germany, France, and Italy house two-thirds of robotic installs, yet Spain, Hungary, and Poland log the fastest additions linked to battery and body-in-white programs. A single friction-stir cell valued at USD 880,000 handles three-dimensional aluminum shells that manual stations cannot reach, illustrating why high-complexity work migrates first.

Manual stick and oxy-fuel machines now account for below 18% of the Europe welding equipment market and will slip 1-2% a year as battery-powered inverters displace old transformer units. Adoption gaps persist: large plants average five robotic cells each, but only one in five shops under 50 employees owns even a single robot. Cobot prices must fall another 30% or leasing models must spread before SMEs fully embrace automation, keeping semi-automatic gear relevant through 2031.

Geography Analysis

Germany contributed 23.45% of the Europe welding equipment market in 2025, anchored by its automotive supply chain and machine-tool champions. Yet growth momentum is shifting south and east. Spain, Poland, Hungary, and the Czech Republic attract gigafactory and contract-fabrication projects that raise their collective share by two points through 2031. A USD 4.47 billion battery plant in Zaragoza alone translates into USD 160 million of welding orders, much of which flows to local integrators rather than German exporters.

France and Italy each sit near 15% market weight. Toulouse’s aircraft lines demand orbital and TIG solutions that meet NADCAP audits, while Italian shipyards adopt humanoid weld robots to speed cruise-ship hulls. The United Kingdom’s portion slipped below 10% after Brexit logistics and labor hurdles nudged suppliers to mainland Europe, although certification tie-ups help salvage some cross-border work.

BENELUX and the NORDICS combine for roughly 16% thanks to petrochemical piping in Rotterdam and offshore wind towers in Denmark and Sweden. Iberian and Eastern European regions post the fastest CAGRs above 6% as lower wages entice manufacturers to locate new welding-intensive lines there. Equipment brands that invest in regional service centers and multilingual training stand to capture these decentralizing flows within the Europe welding equipment market.

Competitive Landscape

The Europe welding equipment market is moderately fragmented. Lincoln Electric, ESAB, and Fronius hold around one-third of 2025 revenue, leveraging global channels and broad product lines. ESAB’s USD 300 million buyout of EWM added premium German inverters and expanded its mid-market reach, while ESAB’s USD 1.45 billion purchase of Eddyfi Technologies in 2026 brings integrated inspection services that bundle nondestructive testing with welding cells. Such one-stop offerings lock in Tier-1 aerospace and pressure-vessel customers.

Second-tier firms such as TRUMPF, Kemppi, voestalpine Böhler Welding, and EWM (now under ESAB) collectively provide another 20% share. TRUMPF invested USD 43.6 million to enlarge its Austrian laser plant, signaling faith in high-margin fiber systems. Voestalpine’s 2024 buy of ITALFIL secures wire supply and diversifies revenue toward consumables, hedging against hardware cycles. Digital services remain a battleground: less than 20% of Europe’s installed machines stream real-time data, so retrofit IoT modules worth up to USD 1.2 billion represent a lucrative upsell pool.

Asian entrants supply low-price inverters at 40-50% discounts, winning orders in construction and light fabrication where CE marks suffice. Yet ISO 3834 and EN 1090 compliance standards shield advanced applications, preserving pricing power for incumbents. Competitive advantage is moving from standalone equipment to lifecycle partnerships that splice hardware, consumables, software, and field service an integrated approach that shapes future consolidation waves in the Europe welding equipment market.[4]Source: ESAB, “Investor Presentation Q1 2026,” esab.com

Europe Welding Equipment Industry Leaders

Lincoln Electric Holdings Inc.

ESAB Corp.

Fronius International GmbH

Kemppi Oy

voestalpine Böhler Welding

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: TRUMPF and SCHMID Group partnered to co-develop laser-plus-wet-chemistry processes for glass interposers used in advanced semiconductor packages, broadening TRUMPF’s photonics exposure beyond metal welding.

- October 2024: Lincoln Electric finalized its acquisition of Kjellberg Finsterwalde, gaining plasma cutting and laser welding technology that strengthens European automotive and industrial offerings

- October 2024: TRUMPF unveiled the TruLaser Series 1000 Lean Edition at EuroBLECH, targeting SMEs with reduced-feature laser cutters that address labor shortages and price pressure from Asian imports

- July 2024: TRUMPF introduced TruHeat VCSEL drying solutions at Battery Show Europe, underscoring its strategic push into EV battery manufacturing equipment with energy-efficient infrared sources

Europe Welding Equipment Market Report Scope

Welding equipment includes welding machines, power sources and devices used directly to perform the welding process, and devices for quickly assembling the parts to be welded, devices for holding the parts during welding, and the weldment include devices to prevent or reduce warpage of Articles, auxiliary equipment.

A complete background analysis of the European welding equipment market, which includes an assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, and emerging trends in the market segments, market dynamics, production statistics, and geographical coverage are covered in the report.

The market is segmented by Type (Welding Equipment and Welding Consumables), by Process (Arc Welding, Gas Welding, Soldering and Brazing, and Other Processes [Resistance Welding, Forge Welding, etc.]), by End User (Construction and Infrastructure, Oil and Gas, Energy and Power, Automotive and Shipbuilding, Aerospace and Defense, Heavy Engineering, Railways, and Other End Users), and by Country (Germany, UK, France, Italy, Russia, Finland, Netherlands, Belgium, and Rest of Europe). The report offers the market sizes and forecasts for the Europe welding equipment market in value (USD) for all the above segments.

| Arc Welding |

| Resistance Welding |

| Leser Welding |

| Plasma Welding |

| Gas Welding |

| Others - Soldering & Brazing, Forge Welding, etc. |

| Construction & Infrastructure |

| Oil, Gas & Petrochemicals |

| Energy & Power Generation |

| Automotive & Transportation |

| Heavy Engineering & Industrial Equipment |

| Aerospace & Defence |

| Others (Specialized Applications - Small-scale fabrication workshops, maintenance & repair, and custom welding services) |

| Manual |

| Semi-automatic |

| Automatic / Robotic |

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| BENELUX (Belgium, Netherlands, and Luxembourg) |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) |

| Rest of Europe |

| By Process | Arc Welding |

| Resistance Welding | |

| Leser Welding | |

| Plasma Welding | |

| Gas Welding | |

| Others - Soldering & Brazing, Forge Welding, etc. | |

| By End-user | Construction & Infrastructure |

| Oil, Gas & Petrochemicals | |

| Energy & Power Generation | |

| Automotive & Transportation | |

| Heavy Engineering & Industrial Equipment | |

| Aerospace & Defence | |

| Others (Specialized Applications - Small-scale fabrication workshops, maintenance & repair, and custom welding services) | |

| By Automation Level | Manual |

| Semi-automatic | |

| Automatic / Robotic | |

| By Geography | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe |

Key Questions Answered in the Report

What is the projected value of the Europe welding equipment market by 2031?

The market is forecast to reach USD 16.43 billion by 2031.

Which welding process currently contributes the largest revenue share in Europe?

Arc welding, covering MIG/MAG and TIG, held 55.26% of 2025 revenue.

Which segment is expected to grow fastest through 2031?

Specialty soldering and brazing show the quickest pace at a 7.19% CAGR.

Why are EV gigafactories important for equipment suppliers?

Each new battery plant orders hundreds of friction-stir or laser stations, adding more than USD 100 million per project to equipment demand.

How will PFAS restrictions affect consumables?

Reformulation raises flux-cored wire costs 8-12%, pressuring margins and potentially shifting users to solid-wire alternatives.

What is driving adoption of welding digital twins?

EU sustainability rules push OEMs to collect weld-level energy data, spurring retrofits of connected inverters and sensors.

Page last updated on: