United States Welding Consumables Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

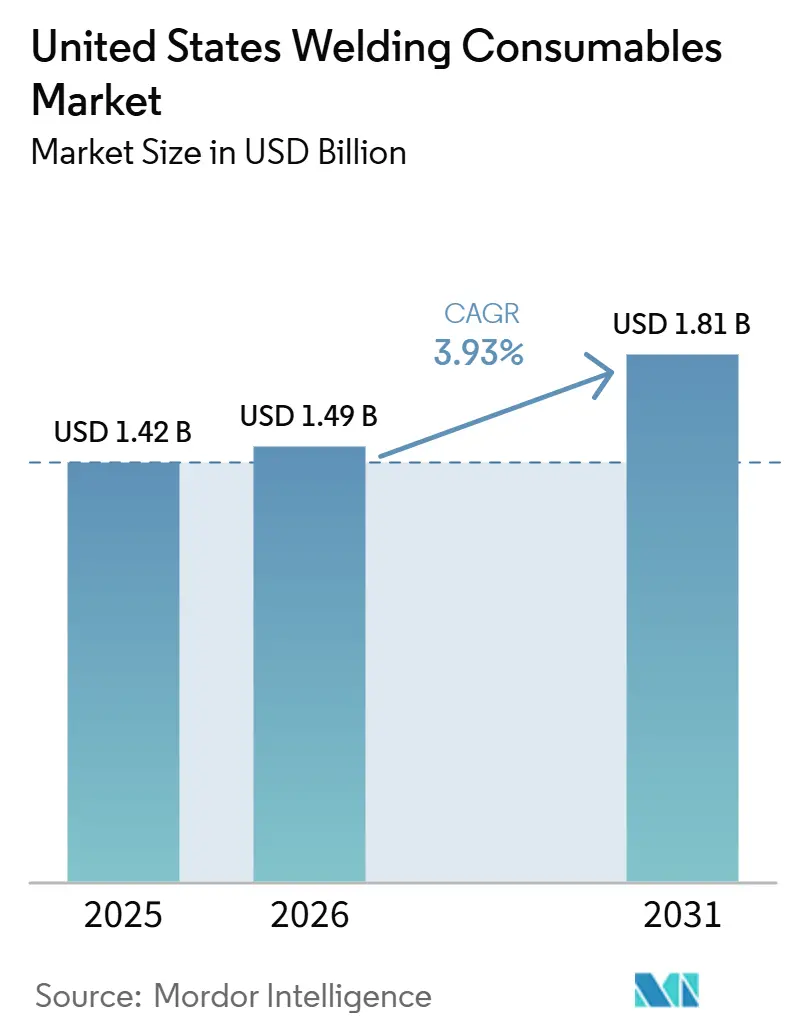

| Base Year Market Size (2025) | USD 1.42 Billion |

| Market Size (2026) | USD 1.49 Billion |

| Market Size (2031) | USD 1.81 Billion |

| Growth Rate (2026 - 2031) | 3.93% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Welding Consumables Market Analysis by Mordor Intelligence

The United States Welding Consumables Market size is expected to grow from USD 1.42 billion in 2025 to USD 1.49 billion in 2026 and is forecast to reach USD 1.81 billion by 2031 at 3.93% CAGR over 2026-2031.

Policy-led infrastructure work, a fresh wave of domestic manufacturing, and large-scale energy infrastructure projects continue to shape demand conditions for electrode, wire, and flux suppliers. The United States welding consumables market is also benefiting from defense procurement tied to shipbuilding and naval maintenance, which supports steady uptake in certified grades that comply with naval and nuclear standards. At the same time, the United States welding consumables market contends with labor shortages among experienced welders, prompting higher adoption of automation and process shifts that improve productivity per operator. Energy-sector buildouts, including new natural-gas pipelines to serve LNG and power demand, are accelerating qualified consumables purchases on compressed timelines. The balance of policy tailwinds and structural headwinds positions the United States welding consumables market for steady growth, where supply reliability, quality assurance, and automation readiness become core differentiators.

Key Report Takeaways

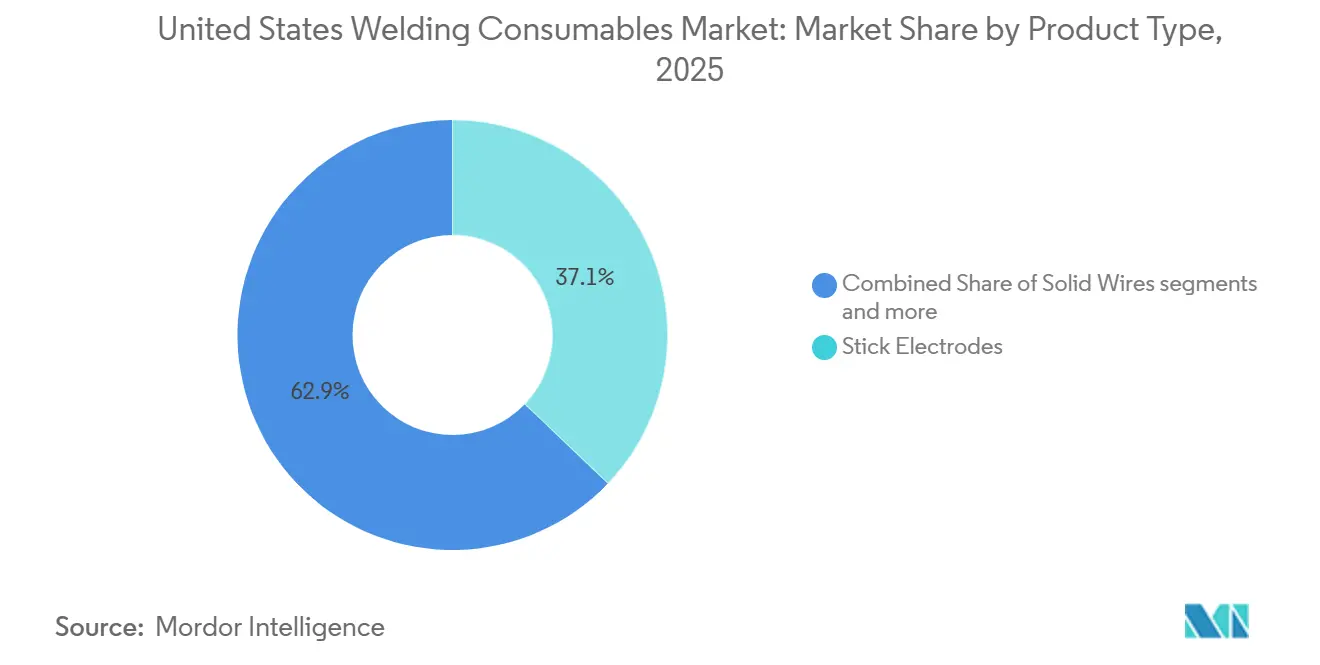

- By product type, stick electrodes led with 37.12% of the United States welding consumables market share in 2025, while flux-cored wires are forecast to expand at a 5.76% CAGR through 2031.

- By welding process, arc processes accounted for a 46.87% share of the United States welding consumables market size in 2025, and laser & hybrid methods are projected to post the fastest 6.34% CAGR through 2031.

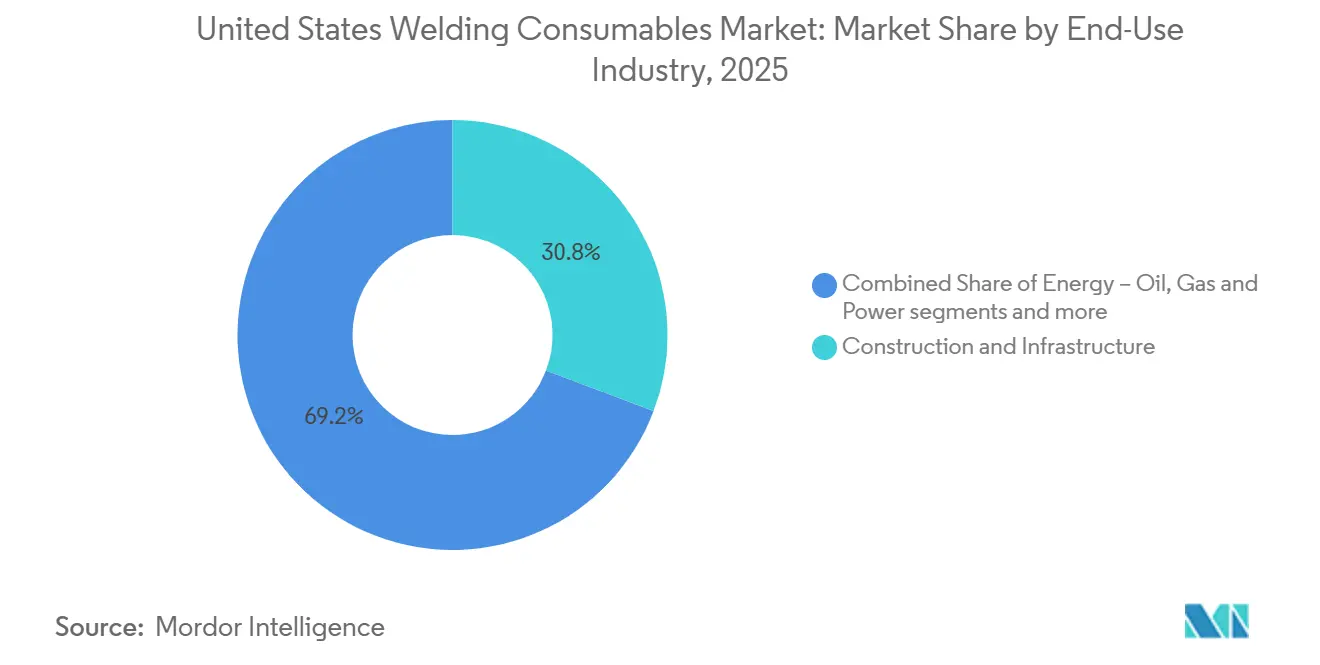

- By end-use industry, construction held 30.76% United States welding consumables market share in 2025, while shipbuilding and offshore operations are set to advance at a 6.78% CAGR to 2031.

- By geography, the Midwest captured 34.12% share in 2025, and the West is expected to grow at a 5.23% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with United states representing one among them. The global report on welding consumables market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

United States Welding Consumables Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure investment implementation | +0.8% | National, with early gains in Texas, Florida, Pennsylvania bridge corridors | Medium term (2-4 years) |

| Onshoring of heavy manufacturing and metal fabrication | +1.2% | South (TX, SC, MS, KY), Midwest (OH, IN), Southwest (AZ) | Long term (≥ 4 years) |

| Natural gas pipeline expansion and replacement | +0.7% | Gulf Coast, Permian Basin, Appalachia, Southeast power hubs | Medium term (2-4 years) |

| Commercial construction boom in Sunbelt states | +0.6% | South (TX, FL, GA, NC), West (AZ), with Texas leading | Medium term (2-4 years) |

| Shipbuilding and naval construction uptick | +0.4% | Gulf Coast shipyards, Great Lakes modular yards, Northeast hubs | Long term (≥ 4 years) |

| Oil and gas MRO activities | +0.3% | Gulf Coast refineries, Permian midstream, Gulf of Mexico platforms | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Infrastructure Investment and Modernization Act Implementation

Federal infrastructure spending has raised the floor for steel-intensive work in bridges and highways, supporting steady demand for structural welding consumables that meet bridge and structural codes. The Infrastructure Investment and Jobs Act continues to funnel multi-year allocations through the Federal Highway Administration, which provides visibility into state-level bridge programs and related steel fabrication needs[1]Federal Highway Administration, “Infrastructure Investment and Jobs Act, Bridge Funding by State,” FHWA, fhwa.dot.gov . While inflation in construction inputs has tempered the immediate physical delivery, the funding horizon remains robust, supporting workloads through 2026. This is particularly pertinent for low-hydrogen stick electrodes, solid wires, and flux-cored wires, all essential for bridges and heavy civil steel projects. The United States welding consumables market benefits when schedule pressure pushes contractors toward automation-ready consumables that support repeatability and consistent bead quality. State transportation plans layered on federal allocations keep backlogs steady for steel girder fabrication and field assembly, which supports consumables offtake throughout the forecast window.

Onshoring of Heavy Manufacturing and Metal Fabrication

Manufacturers are increasing domestic capacity in semiconductors, batteries, and advanced equipment, which reinforces medium-term demand for specialized filler metals across stainless, nickel, and aluminum grades. The United States welding consumables market is seeing more specifications that call for traceability and cleanroom-compatible consumables in fabs and battery facilities as OEMs localize high-value steps. In automotive supply chains, new facilities in the South and Southwest are aligning equipment selection with automation-friendly wires and process controls that reduce rework and help bridge skill gaps on large projects. The United States welding consumables market is also benefiting from broader supplier quality frameworks that encourage dual certification and documented procedure qualification, which deepens the role of premium grades in regulated environments. As more capital projects move from announcement to installation, purchasing cycles for welding consumables become more predictable and favor suppliers with local inventories and technical support.

Natural Gas Pipeline Network Expansion and Replacement

Large new-build natural-gas capacity scheduled for 2026 is driving procurement for pipe steel, SAW consumables, and cellulosic electrodes used in field construction. Industry sources indicate that up to 22 Bcf/d of new pipeline capacity could enter service in 2026, the biggest yearly addition since 2008, which sharpens demand for qualified consumables on accelerated schedules[2]Chris Newman, “U.S. Natural Gas Pipeline Capacity Set for Biggest Buildout Since 2008,” Natural Gas Intelligence, naturalgasintel.com . Project announcements from major midstream operators point to sustained workstreams that connect supply basins to LNG export terminals and gas-fired generation, which is relevant for SAW wire and flux in spiral and longitudinal seam welding. Replacement programs on older lines maintain a parallel channel of demand for sleeve installations, valve replacements, and corrosion repair, which keeps stick electrodes and low-hydrogen wires in use on maintenance jobs. The United States welding consumables market sees reliable offtake when permitting clarity and demand visibility, shortening project lead times, and keeping fabrication shops at high utilization.

Commercial Construction Boom in Sunbelt States

Commercial and manufacturing construction spending climbed to one of the highest levels in recent decades as of early 2025, with Sunbelt states outpacing the national trend. Texas led in total commercial spending, while Arizona ranked first on a per-capita basis at USD 5,980, reflecting large semiconductors, batteries, and related projects that intensify structural steel work. The United States welding consumables market benefits when high-deposition solutions, including flux-cored wires and optimized solid wires, help fabricators meet tight schedules on data centers, logistics hubs, and process plants. Sunbelt population growth and pro-build permitting continue to support multi-year pipelines in offices, multifamily, and mixed-use structures, which support stable consumables requirements for erection and fit-out. This regional tilt keeps distributors in Texas, Florida, Georgia, North Carolina, and Arizona focused on stocking approved grades and aligning service models with fast-cycle job sites.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging welder workforce and limited replacement pipeline | -0.9% | National, acute in Rust Belt and Gulf Coast shipyards | Long term (≥ 4 years) |

| Raw material price volatility for steel wire and flux | -0.5% | National, concentrated in Midwest wire-rod mills | Short term (≤ 2 years) |

| Shift toward alternative joining in automotive | -0.3% | Midwest auto corridor, Southeast EV plants | Medium term (2-4 years) |

| Economic sensitivity to construction and manufacturing | -0.4% | National, with Sunbelt and industrial states more exposed | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging Welder Workforce with Limited Replacement Pipeline

The median age of welders is higher than the broader workforce, which tightens the available labor pool and raises training burdens for employers. Many fabricators respond by adopting automation, robotic cells, and standardized procedures that reduce skill variability, which shifts consumables selection toward products that support consistent arc starts and repeatable bead geometry. The United States welding consumables market is thus seeing stronger interest in wires and fluxes with tight tolerances and documented performance for automated processes. Training pathways are also evolving, with more emphasis on certifications that align with robotic arc welding and resistance welding to broaden operator capabilities in shorter timeframes. Over the forecast period, this demographic pressure encourages process substitution in some applications while supporting premium-grade consumables in others that remain arc-based.

Raw Material Price Volatility for Steel Wire and Flux

Input costs for steel wire rod and certain flux minerals can move quickly when regional supply tightens, or import flows shift, which complicates pricing for multi-year bids. Smaller electrode manufacturers face margin pressure when spot costs rise faster than contracted prices, leading to cautious procurement and leaner inventories. The United States welding consumables market reflects this volatility in shorter quoting windows, expanded use of surcharges, and more frequent adjustments to distributor price lists. Flux components sourced from limited domestic mines or under tariff regimes add another layer of variability that affects product availability and lead times. Suppliers with diversified sourcing, hedging strategies, and local inventories are better positioned to maintain service levels during short spikes in raw material costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Stick Electrodes Drives Market Demand

Stick electrodes held the largest share at 37.12% of 2025 revenue within the United States welding consumables market, while flux-cored wires are projected to grow fastest at a 5.76% CAGR through 2031. Stick remains entrenched in field repairs, structural projects, and maintenance tasks where portability, setup speed, and tolerance to surface conditions outweigh the productivity gains of continuous-wire processes. The United States welding consumables market continues to rely on low-hydrogen and cellulosic stick grades for pipeline tie-ins, remote construction, and repair work across energy and civil sites. In parallel, flux-cored wires are gaining share because they deliver high deposition rates in vertical and overhead positions, suiting bridge erection, high-rise construction, and modular shipbuilding, where labor cost per linear foot matters. Code updates and quality frameworks in structural steel maintain the need for certified consumables in both stick and flux-cored formats, which supports a balanced product mix across shop and field uses.[3]American Welding Society, “AWS D1.1/D1.1M:2025 Introduces a New Grade of Structural Steel for Prequalified Welding,” AWS Welding Digest, aws.org

Flux-cored wires are aligned with automation on large projects and in robotic cells that prioritize repeatability and throughput, which fuels their leading growth profile through 2031. Solid wires remain a steady mid-market option for automotive, heavy equipment, and general fabrication due to their stable arc characteristics and compatibility with standard GMAW systems. SAW flux and wire hold a durable niche in pressure vessels, line pipe mills, and heavy structural sections because consistent mechanical properties and controlled heat input justify capital investment in flux handling and process controls. TIG rods and brazing alloys serve high-purity or thin-wall applications in aerospace, pharmaceutical piping, and food-grade stainless work, which carry premium pricing and strict documentation needs. The United States welding consumables industry is expected to see continued optimization of product selection by job context, which sustains stick volumes in field work and supports above-market growth for flux-cored products in structural and modular builds.

By Welding Process: Arc Welding Anchors Demand Rises with Technology Shifts

Arc welding processes accounted for a 46.87% share of the United States welding consumables market in 2025, while laser and hybrid methods are forecast to post a 6.34% CAGR through 2031. Within arc, GMAW/MIG dominates high-volume manufacturing because it balances productivity with moderate skill requirements, while FCAW is the workhorse in structural steel and shipbuilding due to high deposition and all-position capability. GTAW/TIG remains the standard for critical joints in aerospace and sanitary systems where weld integrity and appearance drive acceptance, and SMAW/stick remains essential in field work where generator power and portability are key. The United States welding consumables market continues to see growth in arc processes by volume as infrastructure and energy work expands, even as some high-volume manufacturing lines adopt alternatives.

Laser and hybrid laser arc systems are advancing in body-in-white and battery enclosures, where speed, precision, and fit-up tolerance reduce takt time and rework. This shift reduces consumables intensity in selected applications, yet many production lines still require arc processes for gap tolerance, multipass geometry, or legacy tooling. Resistance welding keeps its role in automotive and appliances, though its consumables footprint is limited to electrode tips and conductive components rather than filler metals. Over the forecast period, the United States welding consumables market will balance incremental substitution by laser and resistance in automotive with stable or rising arc demand in construction, energy, and defense, which supports steady volumes for solid wires, flux-cored wires, stick electrodes, and SAW consumables.

By End-Use Industry: Construction Leads Volume, Shipbuilding Outpaces Growth

Construction and infrastructure captured 30.76% of 2025 revenue in the United States welding consumables market, while shipbuilding and offshore operations are projected to grow at a 6.78% CAGR to 2031. Federal highway and bridge programs continue to back steel-intensive civil works, and structural codes sustain demand for qualified stick, solid, and flux-cored products used in fabrication and erection. Commercial building and manufacturing construction pipelines are strong in Sunbelt states, which supports shop volumes for beams, columns, mezzanines, and rack systems that depend on high deposition solutions. Energy-related projects add steady maintenance and upgrade work, keeping the United States welding consumables market broadly diversified across new builds and MRO.

Shipbuilding and offshore operations show the fastest trajectory in defense support and modular construction practices that distribute welding tasks across more suppliers. Naval requirements favor consumables with documented performance under MIL and ASME codes, which supports premium price points and recurring requalification in approved vendor lists. Automotive and transportation remain important for wires in robotic arcs, though certain EV body structures and battery applications lean toward alternative joining that can reduce filler metal use. Heavy equipment and machinery maintain regular replacement cycles and upgrades in mining, agriculture, and processing, which support a baseline of consumables orders from OEMs and rebuilders. The United States welding consumables industry continues to pivot product portfolios and service models toward the needs of civil, energy, and defense projects that dominate near-term growth.

Geography Analysis

The Midwest held the largest share at 34.12% in 2025 within the United States welding consumables market, while the West is expected to grow fastest at a 5.23% CAGR through 2031. The Midwest’s base reflects a dense network of automotive manufacturing, heavy equipment, and steel production that sustains continuous demand for solid wires, flux-cored wires, and stick electrodes in both shop and field settings. Suppliers here emphasize reliability, approved procedures, and consistent quality across large OEM and Tier 1 accounts, which helps stabilize volumes in the United States welding consumables market.

The South ranks next by share and benefits from a concentration of energy infrastructure, petrochemicals, and fast-growing commercial and manufacturing construction. Texas and neighboring states continue to drive orders tied to pipelines, LNG support assets, data centers, and logistics hubs, all of which consume structural steel and drive field erection that relies on high deposition consumables. Builders in Florida and Georgia add capacity in warehousing, ports, and mixed-use development, which favors distributors that can deliver approved consumables at short notice. Over the forecast period, the United States welding consumables market in the South remains supported by energy MRO and construction activity that withstands swings in manufacturing output.

The West leads by growth rate and is lifted by semiconductors, batteries, renewable energy, and aerospace programs that keep demand concentrated in higher-specification consumables. Arizona’s per-capita commercial spending underscores the scale of ongoing advanced manufacturing projects, which draw on fabricators familiar with cleanroom and structural code compliance. California and the Pacific Northwest add demand from defense and aerospace fabrication and specialized shipyard activity, where TIG and resistance processes complement arc-based production. The Northeast remains the smallest regional share but maintains niche strength in nuclear maintenance, bridge rehabilitation, and naval work that depends on dual-certified consumables and strict documentation. Across all regions, the United States welding consumables market share profile reflects where energy infrastructure, civil projects, and advanced manufacturing place the greatest draw on certified grades and dependable supply.

Competitive Landscape

The United States welding consumables market is moderately concentrated. Lincoln Electric, ESAB Corporation, Illinois Tool Works’ Hobart Brothers, voestalpine Böhler Welding USA, and Kobelco maintain nationwide reach through integrated equipment and consumables offerings, depth in specialty alloys, and strong distributor networks. Strategic focus is centered on automation enablement, rapid qualification support, and local inventory coverage that can meet tight timelines across defense, energy, and civil projects. The United States welding consumables market increasingly rewards vendors that can bundle application support, code compliance, and supply assurance.

Mergers and acquisitions are aligning product portfolios with high-growth and regulated end markets. ESAB agreed to acquire EWM GmbH in June 2025 for approximately EUR 275 million (USD 298 million), adding heavy industrial equipment and advanced automation capabilities that strengthen its position with large fabricators. In February 2026, ESAB finalized the purchase of Eddyfi Technologies for USD 1.45 billion, expanding into inspection and monitoring solutions that complement welding workflows in aerospace, defense, nuclear, and civil infrastructure. Lincoln Electric’s acquisition of Alloy Steel Australia in August 2025 broadened its presence in wear plate solutions and engineered services that support maintenance-heavy sectors, adding leverage in MRO-oriented consumables demand.

Product strategies emphasize certified grades, narrow tolerances, and automation-ready characteristics that reduce variability and speed qualification. Vendors are adding technical service capacity to help customers meet AWS, ASME, and customer-specific requirements, especially in defense and sanitary applications that demand stringent documentation. In niches like food, beverage, and pharma plants, orbital TIG welding of stainless tubing is aligned with hygienic design standards and drives demand for high-purity rods and documented heat lot traceability. Across segments, the United States welding consumables market favors suppliers that couple materials technology with application engineering, local inventory, and consistent on-time delivery.

United States Welding Consumables Industry Leaders

Lincoln Electric Holdings Inc.

ESAB Corporation

Illinois Tool Works Inc. (Hobart Brothers)

Kobe Steel Ltd. (Kobelco Welding of America)

voestalpine Böhler Welding USA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: ESAB Corporation closed the acquisition of Eddyfi Technologies for USD 1.45 billion, expanding exposure to inspection and monitoring with integrated solutions for aerospace, defense, nuclear, and civil infrastructure.

- January 2026: Kinder Morgan advanced USD 7 billion in natural gas pipeline projects, including Trident and Mississippi Crossing, to serve LNG and power markets amid faster regulatory timelines.

- August 2025: Lincoln Electric completed the acquisition of the remaining interest in Alloy Steel Australia, deepening its portfolio in wear-plate solutions and engineered services for maintenance-driven sectors.

United States Welding Consumables Market Report Scope

The United States Welding Consumables Market Report is Segmented by Product Type (Stick Electrodes, Solid Wires, Flux-Cored Wires, SAW Flux & Wire, TIG Rods & Brazing Alloys), by Welding Process (Arc [SMAW/Stick, GMAW/MIG, GTAW/TIG, FCAW], Resistance Welding, Laser & Hybrid Welding), by End-Use Industry (Construction & Infrastructure, Automotive & Transportation, Energy (Oil, Gas & Power), Shipbuilding & Offshore, Heavy Equipment & Industrial Machinery, Others), and by Geography (Northeast, Midwest, South, West). The Market Forecasts are Provided in Terms of Value (USD Billion).

| Stick Electrodes |

| Solid Wires |

| Flux-Cored Wires |

| SAW Flux & Wire |

| TIG Rods & Brazing Alloys |

| Arc | SMAW (Stick) |

| GMAW / MIG | |

| GTAW / TIG | |

| FCAW | |

| Resistance Welding | |

| Laser & Hybrid Welding |

| Construction & Infrastructure |

| Automotive & Transportation |

| Energy (Oil, Gas & Power) |

| Shipbuilding & Offshore |

| Heavy Equipment & Industrial Machinery |

| Others |

| Northeast |

| Midwest |

| South |

| West |

| By Product Type | Stick Electrodes | |

| Solid Wires | ||

| Flux-Cored Wires | ||

| SAW Flux & Wire | ||

| TIG Rods & Brazing Alloys | ||

| By Welding Process | Arc | SMAW (Stick) |

| GMAW / MIG | ||

| GTAW / TIG | ||

| FCAW | ||

| Resistance Welding | ||

| Laser & Hybrid Welding | ||

| By End-Use Industry | Construction & Infrastructure | |

| Automotive & Transportation | ||

| Energy (Oil, Gas & Power) | ||

| Shipbuilding & Offshore | ||

| Heavy Equipment & Industrial Machinery | ||

| Others | ||

| By Region | Northeast | |

| Midwest | ||

| South | ||

| West | ||

Key Questions Answered in the Report

What is the United States welding consumables market growth outlook for 2031?

The United States welding consumables market is projected to reach USD 1.81 billion by 2031 at a 3.93% CAGR over 2026-2031, supported by infrastructure, energy buildouts, and domestic manufacturing.

Which product type leads to demand in the United States welding consumables market?

Stick electrodes led with 37.12% market share in 2025, while flux-cored wires are the fastest growing on high deposition and automation friendly applications.

Which welding processes will grow fastest in the United States welding consumables market?

Laser & hybrid methods are forecast to grow at a 6.34% CAGR through 2031, while arc processes retain the largest use across construction, fabrication, and maintenance.

Which end use segment drives the most volume for United States welding consumables market?

Construction & infrastructure accounted for 30.76% of 2025 revenue, with shipbuilding & offshore operations showing the fastest growth to 2031.

Which region will grow fastest for United States welding consumables market through 2031?

The West is projected to grow at a 5.23% CAGR, driven by semiconductors, batteries, renewables, and aerospace activity, while the Midwest holds the largest current share.

How are labor constraints affecting the United States welding consumables market?

A tight-weld pipeline is increasing automation adoption and process standardization, which shifts demand toward automation ready wires and certified consumables that support consistent quality.

Page last updated on: