Market Overview

| Study Period | 2020 - 2031 |

|---|---|

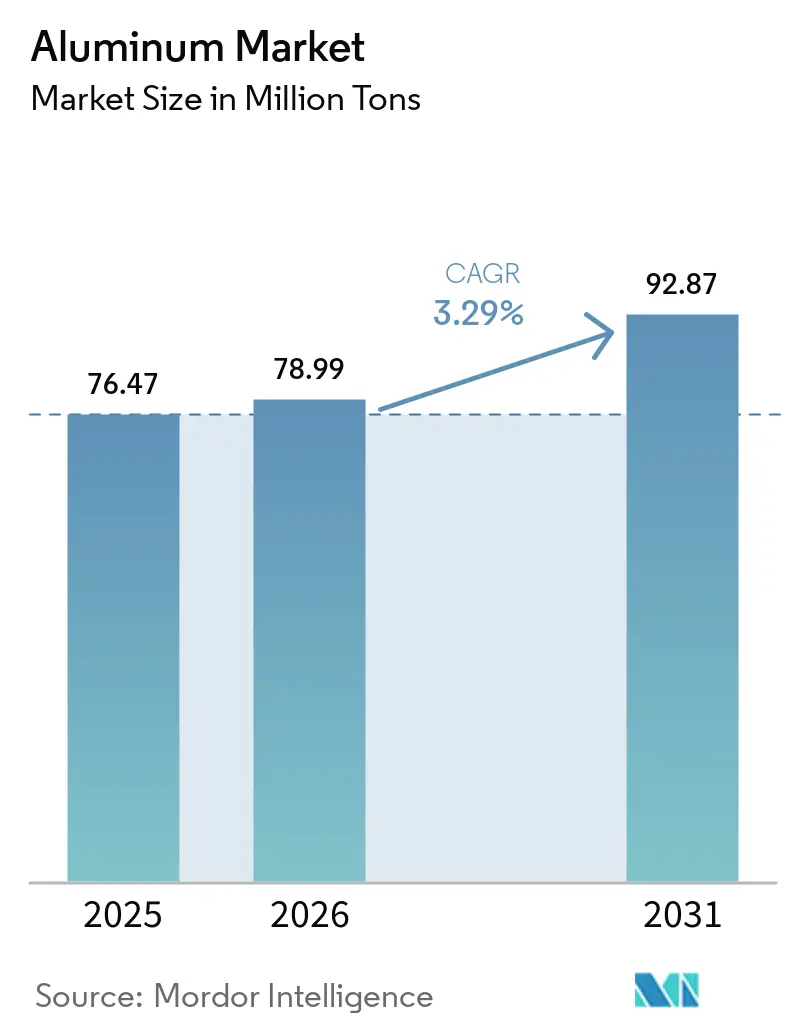

| Market Volume (2026) | 78.99 Million tons |

| Market Volume (2031) | 92.87 Million tons |

| Growth Rate (2026 - 2031) | 3.29% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aluminum Market Analysis by Mordor Intelligence

The Aluminum market size is expected to grow from 76.47 million tons in 2025 to 78.99 million tons in 2026 and is forecast to reach 92.87 million tons by 2031 at 3.29% CAGR over 2026-2031. Robust growth follows aluminum’s position as the second most used metal, its unbeatable strength-to-weight ratio, and a closed-loop recyclability profile that keeps 75% of all metal ever produced in circulation[1]International Aluminium Institute, “Report Reveals Global Aluminium Demand to Reach New Highs After Covid,” international-aluminium.org . Rapid electrification, renewable-energy build-outs, and sustainable packaging mandates are converging to lift demand even as producers confront decarbonization targets, volatile power prices, and trade policy shifts. Top players are channeling capital toward green smelting and scrap recovery, while downstream customers lock in long-run supply to shield themselves from raw material shocks. Asia-Pacific dominates current volumes and retains the fastest trajectory, yet regional capacity ceilings, geopolitical risks, and carbon-border fees are driving fresh investments in North America and the Gulf. Integrated operators with low-carbon billet, recycling depth, and multi-process flexibility stand to capture a growing share of the aluminum industry.

Key Report Takeaways

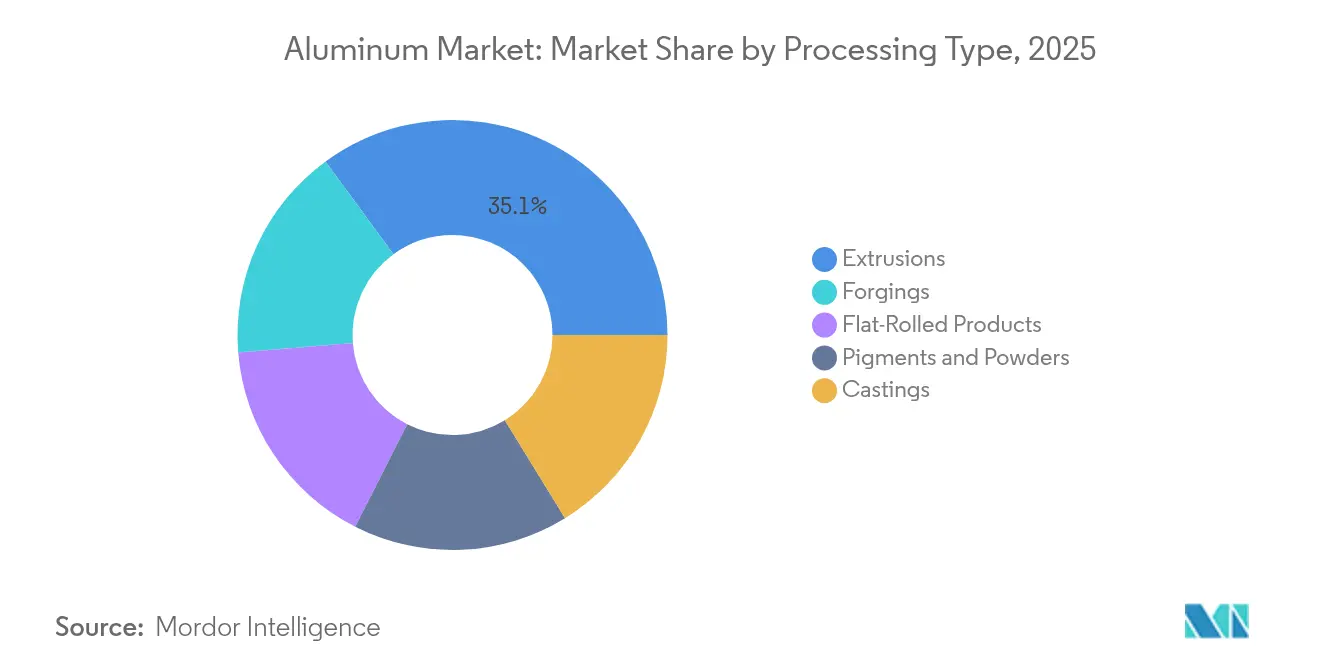

- By processing type, extrusions captured 35.05% of the Aluminum market share in 2025, while castings are projected to advance at a 3.5% CAGR through 2031.

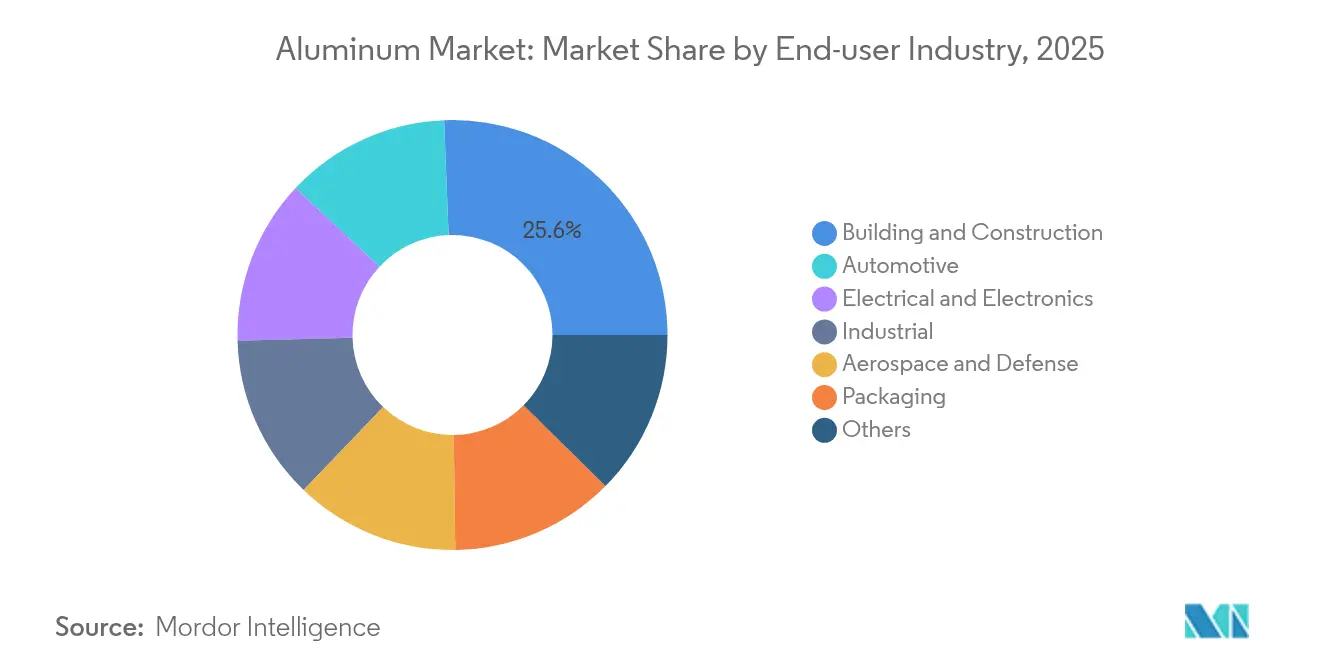

- By end-user industry, building and construction accounted for 25.62% of the Aluminum market size in 2025 and is growing at a 4.39% CAGR toward 2031.

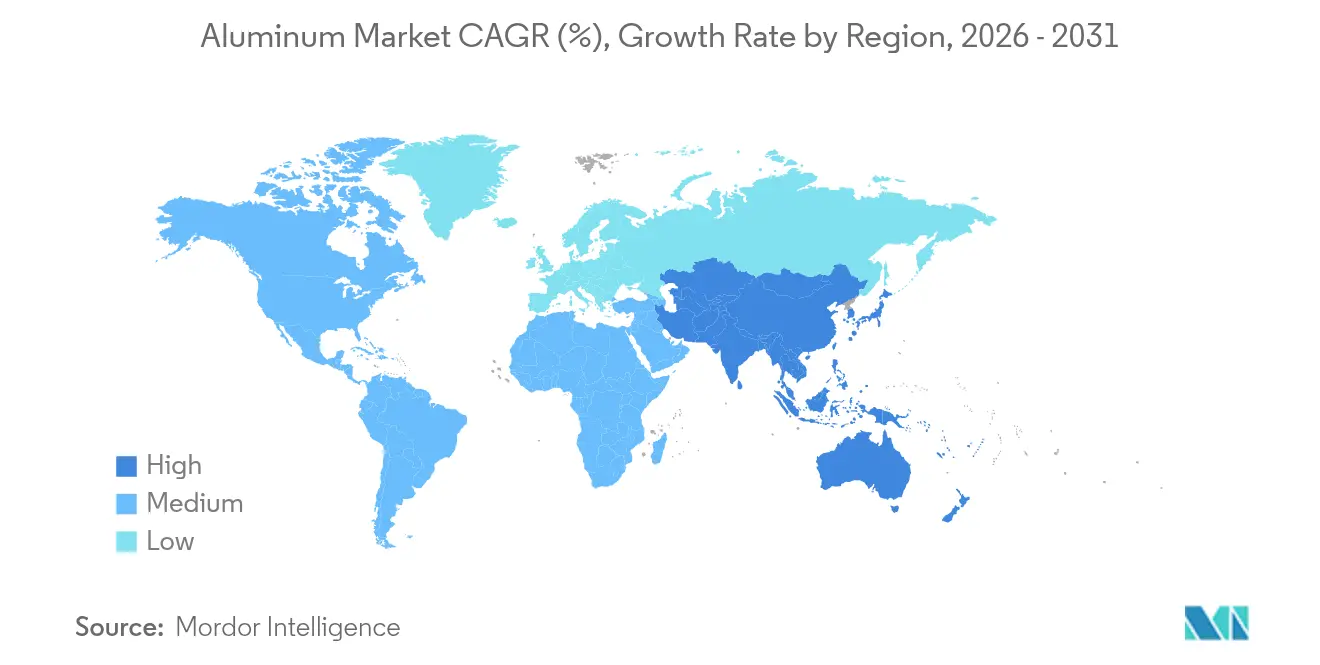

- By geography, Asia-Pacific held 69.58% share of the Aluminum market share in 2025, and is advancing at a CAGR of 3.51%.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Aluminum Market*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging EV-led lightweighting demand | +0.8% | Global, led by China, North America, Europe | Medium term (2-4 years) |

| APAC infrastructure boom | +0.6% | APAC core, global supply chains spill-over | Long term (≥ 4 years) |

| Renewable-energy aluminum demand | +0.5% | Global with early gains in Europe, North America, China | Long term (≥ 4 years) |

| Sustainable packaging shift | +0.4% | Global, led by Europe and North America | Medium term (2-4 years) |

| Hydrogen-ready green smelting capacity | +0.3% | North America, Europe, GCC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging EV-led Lightweighting Demand

Battery electric vehicles house triple the aluminum content of internal-combustion models, hitting 885 lb per car in North America during 2024. Every 10% mass cut extends driving range by roughly 7%, so automakers now specify aluminum for body-in-white, battery trays, crash structures, and thermal systems. EV penetration may plateau in mature markets after 2028, yet model-mix evolution keeps per-unit metal intensity rising, preserving a growth channel for the Aluminum market even as total auto sales fluctuate.

APAC Infrastructure Boom

Asia-Pacific’s megaproject pipeline underpins long-cycle demand visibility. Chinese consumption expanded nearly 16% per year since 2000, dwarfing 1% rates elsewhere. Smart-city grids, high-speed rail, and cross-border power links rely on aluminum’s conductivity and corrosion resistance, ensuring the region’s pull on both primary ingot and fabricated products. Structural slowdowns pose cyclical risk, but stimulus outlays historically cushion downturns, keeping the Aluminum market on an elevated base in the long horizon.

Sustainable Packaging Shift

Aluminum retains 81% recycling rates versus 52% for plastic, making it a favored material in beverage, food, and personal-care formats. Brand-owner net-zero promises and impending EU recyclability rules accelerate the substitution curve, with premium water and cosmetics already shifting to full-body aluminum vessels in the aluminium industry. Cost premiums stay a hurdle in price-sensitive niches, though circularity credentials offset higher material spend for many consumer-facing firms, reinforcing baseline growth for the Aluminum market.

Hydrogen-Ready Green Smelting Capacity

Pilots in Norway and Canada prove hydrogen can displace natural gas in anode preheating, cutting CO₂ footprints by up to 80% while stabilizing long-run electricity costs. New U.S. and Gulf smelter announcements include renewable-power and green-hydrogen provisions from day one, promising cost parity once scale improves. Early movers in the aluminium industry will enjoy tariff relief under carbon-border regimes, positioning low-carbon metal as a premium grade in packaging and mobility supply chains.

Restraints Impact Analysis of Aluminum Market*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy-price volatility | -0.7% | Global, with acute impact in Europe and energy-intensive regions | Short term (≤ 2 years) |

| Carbon-border tariffs and ESG scrutiny | -0.5% | EU imports, with spillover effects to global trade flows | Medium term (2-4 years) |

| Graphene-coated steel threat in cans | -0.2% | Global packaging markets, concentrated in food and beverage sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Energy-Price Volatility

Electricity accounts for nearly 40% of smelting cash costs. European spot power spikes in 2024 forced multiple curtailments that erased over 1 million tons of annualized supply. Smelters cannot ramp down cheaply because frozen pots risk permanent damage, amplifying exposure to intraday price swings. Renewables add long-term stability, but transition financing and grid bottlenecks clamp near-term margins, trimming expansion appetite in high-tariff regions across the aluminium industry.

Carbon-Border Tariffs and ESG Scrutiny

The EU’s Carbon Border Adjustment Mechanism could lift imported primary aluminum costs by 70% once phased in by 2030. Roughly one-third of Chinese exports fall under the levy, forcing producers to install emissions tracking, buy offsets, or pivot to lower-tariff destinations. Compliance investments, data-audit fees, and potential penalties increase trading friction and encourage near-shoring, tempering tonnage flows into Europe and adding complexity to global Aluminum market logistics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Aluminum Market Segment Analysis

By Processing Type:

Extrusions Lead Through VersatilityExtrusions represented 35.05% of Aluminum market share in 2025 on the back of architectural profiles, heat sinks, and vehicle crash-management parts. Extruders able to deliver low-carbon billet at scale are capturing long-term supply contracts with premium pricing clauses. Castings follow as the fastest riser at 3.5% through 2031, buoyed by giga-casting adoption in automotive body structures. Equipment builders report booked-out die-casting lines until 2027, highlighting a capacity sprint that keeps the Aluminum industry size expanding within powertrain and chassis applications.

Flat-rolled products hold a solid slot across beverage can stock and auto panel sheet. Forward-looking mills integrate closed-loop scrap systems, shrinking carbon footprints and locking in feedstock surety. Forgings serve landing-gear and military vehicles, sustaining a high-margin niche underpinned by stringent quality standards. Pigments and powders cater to electronics and additive manufacturing; their trajectory depends on printer penetration rates in aerospace and medical device sectors. The multi-process spectrum underscores aluminum’s adaptability and explains why integrated producers maintain strategic investments across extrusion presses, rolling mills, and die-casting cells to secure wallet share within the broader Aluminum market.

By End-user Industry:

Construction Dominates GrowthBuilding and construction led with 25.62% share of the Aluminum market size in 2025, advancing at a 4.39% CAGR toward 2031 as governments channel fiscal programs into resilient infrastructure. Curtain walls, window frames, and photovoltaic façades benefit from aluminum’s corrosion resistance and recyclability, aligning with green building codes such as LEED and BREEAM. Non-residential projects soak up two-thirds of regional consumption in North America, while APAC megacities sustain volume growth despite macro headwinds. Automotive ranks second yet posts outsized incremental demand as battery enclosures and mega-castings displace steel stampings. Per-vehicle metal loads are trending upward even as overall vehicle output plateaus, providing a stabilizing anchor for the Aluminum industry.

Aerospace and defense order books support steady, high-grade billet demand, though supply chains remain sensitive to certification cycle delays. Packaging extends beyond beverage cans into refillable personal-care lines and premium water bottles, leveraging brand messaging around infinite recyclability. Electrical and electronics segments draw rod, bar, and conductor products for grid hardening and 5G roll-outs. Industrial machinery completes the mosaic, consuming plate and forged products across material-handling gear and robotics. This diversified demand mix gives the Aluminum market resilience against downturns in any single vertical.

Geography Analysis

APAC Aluminum Market

Asia-Pacific retained 69.58% of global volume in 2025 and is tracking a 3.51% CAGR through 2031. While Beijing’s 45 million-ton ceiling slows greenfield smelters, downstream fabrication keeps expanding, propelling internal billet import needs and stimulating investment in secondary aluminum hubs across Malaysia and Indonesia. India scales new cast-house projects to meet smart-city housing and railway electrification, reinforcing the region’s gravitational pull on the Aluminum market.

North America and Europe Aluminum Market

North America produced 3.4% more aluminum products in 2024, yet still logged a 4 million-ton supply deficit. Federal incentives now underpin EGA’s USD 4 billion, 600,000-ton Oklahoma smelter and Century Aluminum’s USD 500 million green-anode plant, marking the first primary capacity additions stateside since 1980. Europe’s share is influenced by energy shocks, shuttered smelters, driving up billet premiums, and elevating import reliance. Yet CBAM incentives and subsidized renewable electricity are luring retrofit projects, such as Rio Tinto’s ELYSIS cell roll-out in Iceland, that promise carbon-free metal by late-decade across the aluminium industry.

MEA and South America Aluminum Market

The GCC leverages low-cost power to export value-added extrusion logs, while Africa’s bauxite pipelines flow toward refining ventures that seek to capture more of the Aluminum industry value chain locally. South American volumes remain steady around alumina-rich Brazil but are constrained by logistics hurdles and capital scarcity.

Competitive Landscape

The Aluminum market exhibits moderate fragmentation. Chinese players dominate spot exports yet grapple with power caps and rising ESG scrutiny. Western majors prioritize low-carbon billets and license-ready zero-emission cells such as ELYSIS, targeting premium margins in packaging and mobility applications. GCC producers exploit captive gas and renewables to ship slab into Europe ahead of the 2030 CBAM inflection. Capital intensity and certification hurdles keep the entry bar high, but state-backed programs in India, Indonesia, and the U.S. are spawning regional champions that will alter trade lanes over the next decade. Overall rivalry thus blends scale players defending core volumes with nimble green-metal innovators grabbing early-stage share, as highlighted in recent aluminum market report.

Aluminum Industry Leaders

Aluminum Corp of China (Chalco)

China Hongqiao Group Limited

Norsk Hydro ASA

Rio Tinto

RUSAL

- *Disclaimer: Major Players sorted in no particular order

Aluminum Market Companies Covered in this Report

- Alcoa Corporation

- AluminIum BahraIn B.S.C. (Alba)

- Aluminum Corp of China (Chalco)

- China Hongqiao Group Limited

- East Hope Group

- Emirates Global Aluminium PJSC

- Novelis Inc.

- Norsk Hydro ASA

- Rio Tinto

- RUSAL

- Xinfa Group

- Vedanta Aluminium

- Century Aluminum Company.

Recent Industry Developments in Aluminum Market

- May 2025: Emirates Global Aluminium confirmed a USD 4 billion Oklahoma smelter with 600,000 t annual capacity that will create 1,000 direct jobs.

- April 2025: Novelis confirmed that its USD 4.1 billion recycling and rolling complex in Bay Minette is set for commissioning in the second half of 2026. The facility aims to enhance the company's recycling capabilities and support its sustainability goals.

Global Aluminum Market Report Scope

Aluminum (Al) is a lightweight silvery-white metal, the most abundant metallic element in Earth's crust, and the most widely used nonferrous metal. The applications include roofing, foil insulation, windows, cladding, doors, shopfronts, balustrading, and architectural hardware. Aluminum is also commonly used in the form of treadplates and industrial flooring. The aluminum market is segmented by processing type, end-user industry, and geography. By processing type, the market is segmented into castings, extrusions, forgings, flat-rolled products, and pigments and powders. The end-user industry segments the market into automotive, aerospace and defense, building and construction, electrical and electronics, packaging, industrial, and other industries. The report also covers market sizes and forecasts in 15 countries across major regions. The market sizing and forecasts are based on volume (million tons) for each segment.

Segmentation Overview

By Processing Type

| Castings |

| Extrusions |

| Forgings |

| Flat-Rolled Products |

| Pigments and Powders |

By End-user Industry

| Automotive |

| Aerospace and Defense |

| Building and Construction |

| Electrical and Electronics |

| Packaging |

| Industrial |

| Others |

By Geography

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Processing Type | Castings | |

| Extrusions | ||

| Forgings | ||

| Flat-Rolled Products | ||

| Pigments and Powders | ||

| By End-user Industry | Automotive | |

| Aerospace and Defense | ||

| Building and Construction | ||

| Electrical and Electronics | ||

| Packaging | ||

| Industrial | ||

| Others | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current global volume for aluminum and how fast is it growing?

The Aluminum market stands at 78.99 million tons in 2026 and is forecast to reach 92.87 million tons by 2031, reflecting a 3.29% CAGR.

Which region accounts for the largest aluminum Industry share?

Asia-Pacific holds 69.58% of worldwide consumption, driven by China's vast smelting base and regional infrastructure spending.

Which end-use consumes the most aluminum industry today?

Building and construction leads with 25.62% of demand thanks to energy-efficient façades, window frames, and large infrastructure projects.

How are carbon-border tariffs likely to influence trade flows?

Europe's CBAM could raise imported primary aluminum costs by up to 70% by 2030, encouraging local low-carbon output and redirecting high-carbon metal to other regions.

What technological breakthrough promises the biggest emission cuts?

The ELYSIS inert-anode smelting cell eliminates direct CO₂ and delivers up to 15% cost savings once scaled, positioning zero-emission aluminum for premium markets.

Page last updated on: