Market Overview

| Study Period | 2020 - 2031 |

|---|---|

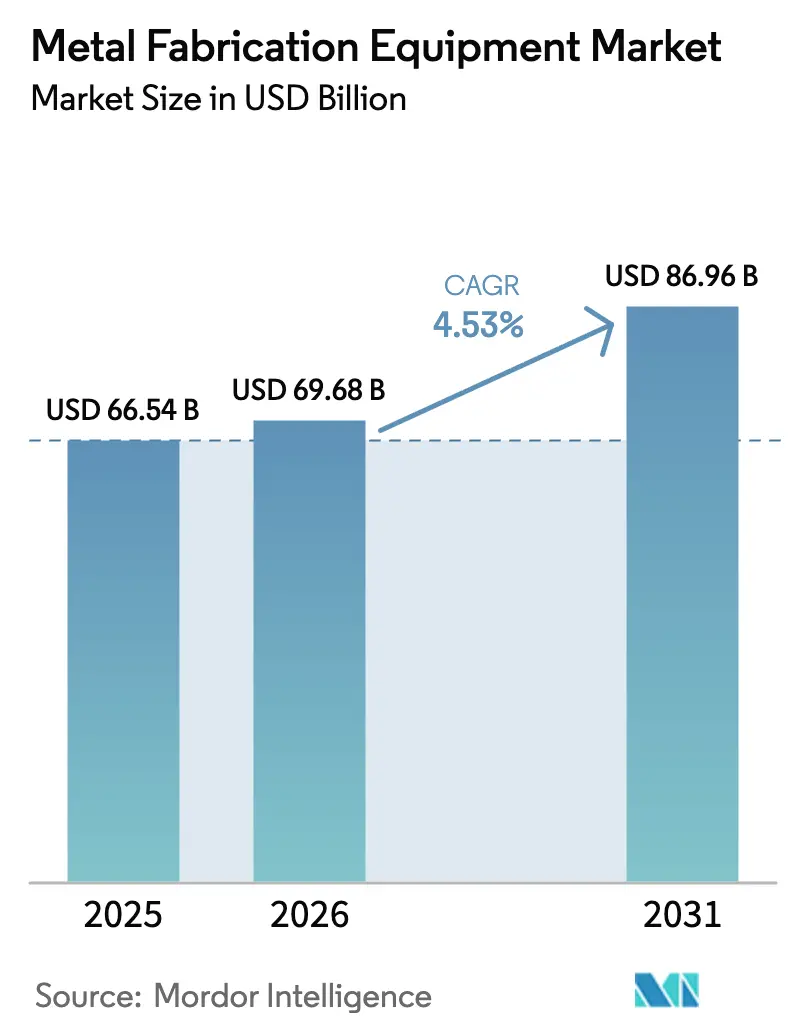

| Market Size (2026) | USD 69.68 Billion |

| Market Size (2031) | USD 86.96 Billion |

| Growth Rate (2026 - 2031) | 4.53% CAGR |

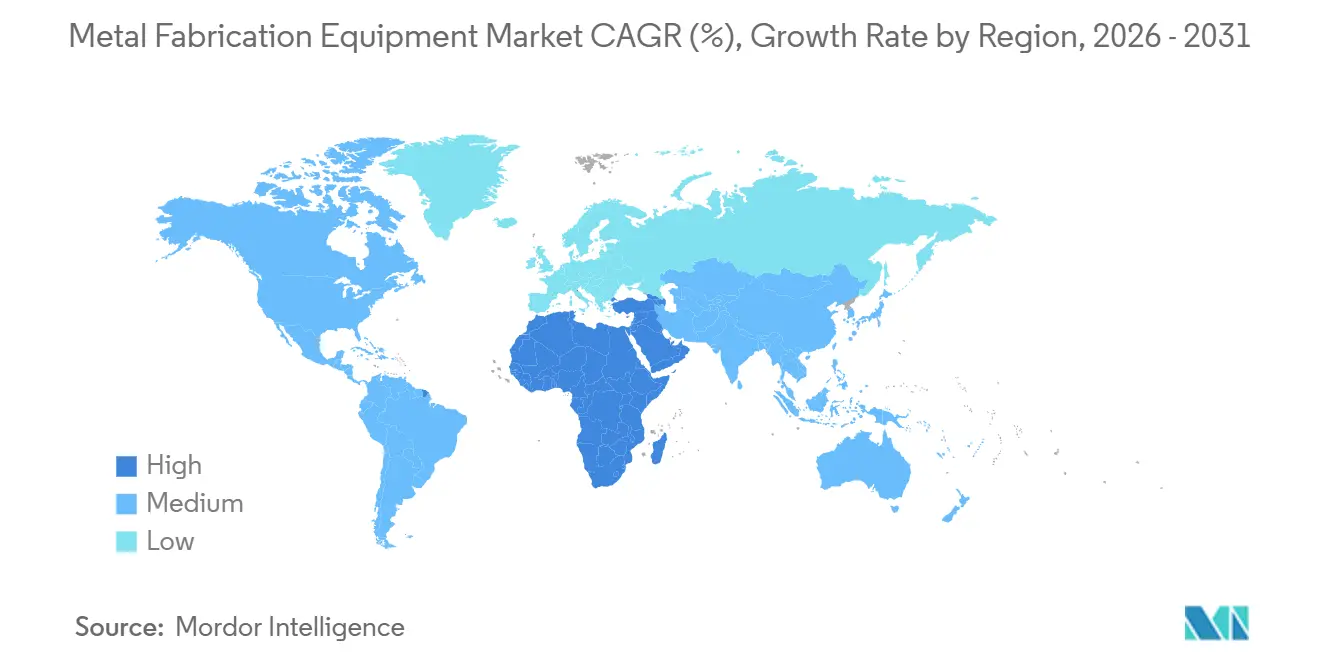

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

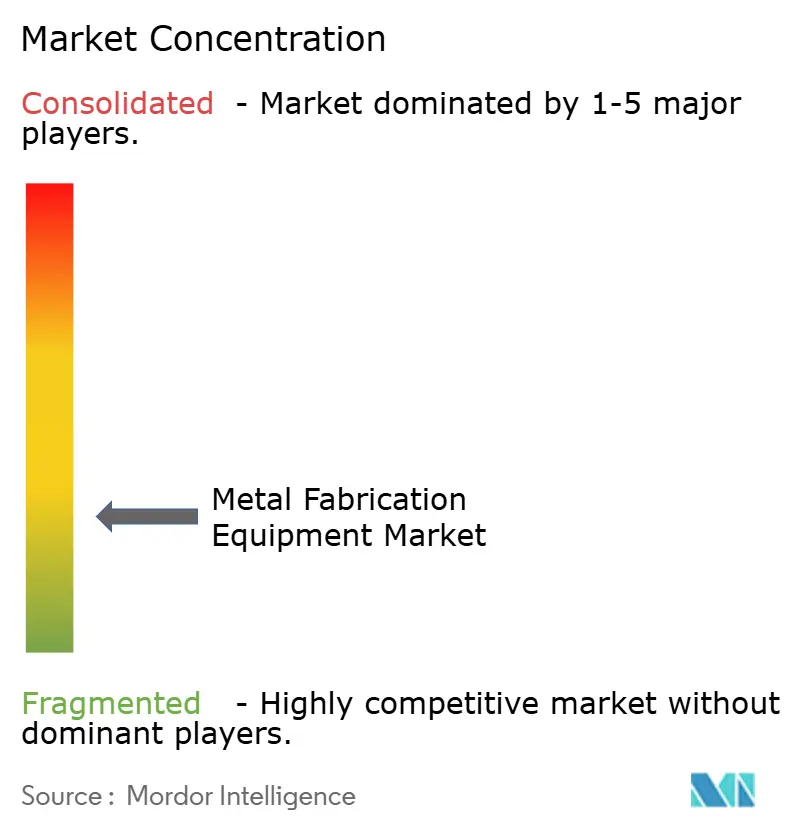

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Metal Fabrication Equipment Market Analysis by Mordor Intelligence

The Metal Fabrication Equipment Market size was valued at USD 66.54 billion in 2025 and is estimated to grow from USD 69.68 billion in 2026 to reach USD 86.96 billion by 2031, at a CAGR of 4.53% during the forecast period (2026-2031).

Robust capital spending in renewable-energy projects, vehicle electrification, and large-scale infrastructure upgrades underpins this steady expansion. Vendors supplying high-power fiber-laser cutters, servo-press brakes, and integrated robotic welding cells are benefiting from shorter product-refresh cycles in automotive plants, the boom in offshore wind towers, and the need to machine recycled alloys with unpredictable carbon content. Equipment purchases are also moving closer to end-markets as manufacturers reshore heavy fabrication to reduce logistics risk and comply with domestic-content rules. Meanwhile, rising cybersecurity threats and raw-material price swings continue to influence procurement timing, pushing buyers to favor machines that include predictive-maintenance software and remote-patch capabilities.

Key Report Takeaways

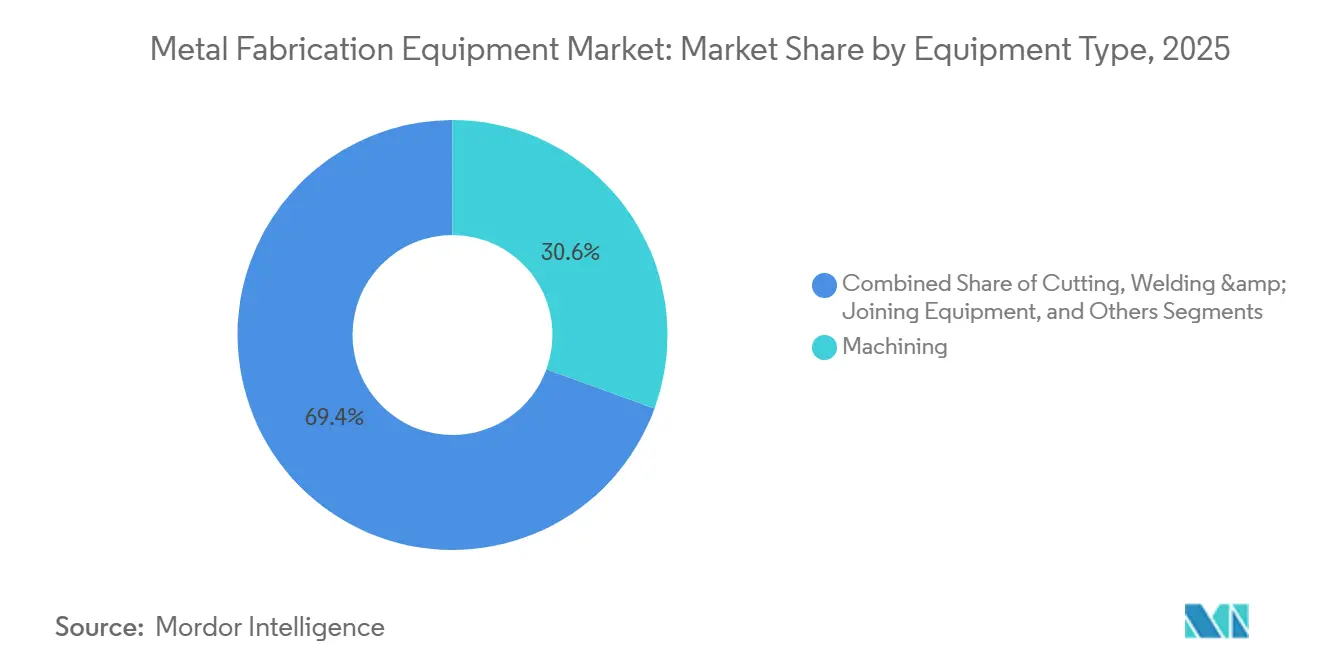

By equipment type, machining captured 30.56% of 2025 revenue; cutting systems are projected to post the fastest 6.78% CAGR to 2031.

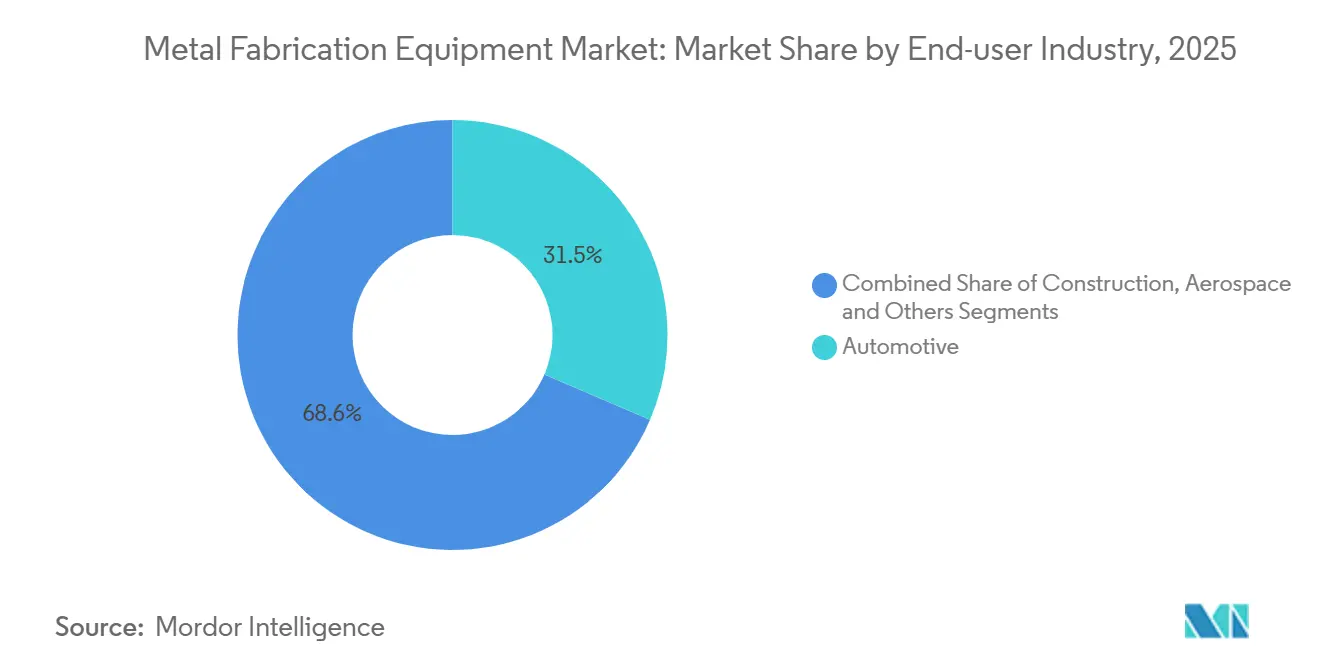

By end-user industry, automotive held 31.45% of 2025 demand, while energy and oil-and-gas applications are set to expand at a 7.56% CAGR through 2031.

By geography, Asia-Pacific commanded 46.76% of 2025 revenue; the Middle East and Africa region is forecast to grow at a 6.23% CAGR to 2031.

Trumpf, Amada, DMG MORI, and Yamazaki Mazak together accounted for 42% of global 2025 sales.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Metal Fabrication Equipment Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing automotive production & model refresh cycles | +1.2% | China, India, ASEAN, North America EV hubs | Medium term (2-4 years) |

| Expanding construction & infrastructure investments | +1.0% | Middle East, India, ASEAN, select North America corridors | Long term (≥ 4 years) |

| Rising demand from aerospace manufacturing | +0.8% | North America, France, UK, Germany, ASEAN final-assembly sites | Medium term (2-4 years) |

| Near-shoring of heavy-fabrication supply chains | +0.7% | United States, Mexico, Poland, Czech Republic, Turkey | Short term (≤ 2 years) |

| Offshore wind-turbine tower build-outs | +0.5% | North Sea basin, Taiwan, Japan, South Korea, U.S. Atlantic | Long term (≥ 4 years) |

| Hybrid additive-subtractive fabrication cells | +0.3% | U.S. aerospace clusters, European precision-engineering zones, select China R&D hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Automotive Production & Model Refresh Cycles

Automakers are compressing model-refresh intervals from seven to under four years, driving frequent retooling of press lines, laser cutters, and robotic welding cells. North American battery-electric vehicle plants now specify up to twelve servo presses and multiple fiber-laser blanking systems for each new platform. Tier-1 suppliers report that every one million incremental battery-electric cars requires about 240 CNC machining centers and 320 robotic welding stations. Incentive programs in India and ASEAN further accelerate orders for high-precision gear-cutting machines. As designs shift toward structural battery packs, demand rises for equipment capable of forming thin-gauge aluminum with repeatability below ±0.05 millimeters.

Expanding Construction & Infrastructure Investments

Megaprojects across Saudi Arabia, India, and Indonesia necessitate heavy-duty press brakes, waterjet cutters, and automated submerged-arc welders to meet compressed commissioning schedules. NEOM alone will consume more than 26 million metric tons of fabricated steel by 2030, requiring on-site plate-forming and laser-cutting capacity[1]Vision 2030, “NEOM Project Overview,” vision2030.gov.sa. Climate-resilient public works programs in the United States and Europe add stainless-steel demand for flood barriers and elevated rail corridors. The rise of prefabricated, modular buildings also boosts orders for CNC plasma cutters that can process 150-millimeter plate without secondary beveling. Suppliers offering turnkey cells that blend forming, joining, and inspection enjoy the largest order backlogs.

Rising Demand from Aerospace Manufacturing

Firm backlogs at Airbus and Boeing secure nine years of production, compelling their supply chains to lock in capacity for titanium bulkheads and Inconel engine mounts [2]Boeing Investor Relations, “Commercial Aircraft Backlog,” boeing.com. Five-axis machining centers with envelope sizes above one meter are now standard in turbine-blade shops, while laser-weld cells deliver porosity below 0.5% in fuel-tank structures. U.S. and French engine programs require additional directed-energy deposition systems for on-site blade repair, cutting material waste by more than 60%. European gear-hobbing specialists report double-digit order growth linked to narrow-body aircraft landing-gear programs. The sector’s rigorous compliance environment rewards vendors that integrate digital-twin simulation and component genealogy tracking into their machine controls.

Near-Shoring of Heavy-Fabrication Supply Chains

U.S. reshoring announcements surged 78% year-on-year in 2024, and each USD 1 billion of relocated fabrication creates equipment demand worth nearly USD 180 million. Automotive, appliance, and defense OEMs prioritize suppliers within 500 miles to minimize freight risk and comply with domestic-content requirements. Mexican press-brake distributors enjoy record backlogs as U.S. buyers diversify away from Asian imports. In Eastern Europe, Czech and Polish job shops install high-power fiber lasers to serve German machinery builders facing skilled-labor gaps. Fast-track delivery expectations favor machine suppliers with regional warehouses and field-service teams.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile raw-steel & non-ferrous prices | -0.9% | Europe, Japan, ASEAN, global import-reliant markets | Short term (≤ 2 years) |

| High cap-ex requirement for next-gen CNC systems | -0.7% | Small and mid-size fabricators worldwide | Medium term (2-4 years) |

| Shortage of skilled welders & machinists | -0.6% | North America, Europe, Australia, India, Vietnam | Long term (≥ 4 years) |

| Cyber-security risk in connected machine tools | -0.4% | Germany, United States, Japan, South Korea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Raw-Steel & Non-Ferrous Prices

Hot-rolled coil steel fluctuated between USD 650 and USD 950 per metric ton in 2024, causing fabricators to renegotiate contracts quarterly and delay machine purchases by more than four months [3]S&P Commodity Insights, “Hot-Rolled Coil Steel Prices,” spglobal.com. Aluminum tracked a 31% price swing, squeezing margins in aerospace and EV battery-enclosure work. Copper peaked above USD 10,000 per metric ton in March 2025 before easing, complicating material forecasts for electrical-equipment shops. Many European service centers cut inventories by 18%, stretching lead times for downstream cutters and brake operators. Such volatility forces buyers to favor equipment suppliers offering leasing or pay-per-use models that preserve cash.

High Cap-Ex Requirement for Next-Gen CNC Systems

Five-axis machining centers with adaptive control and digital-twin interfaces list above USD 500,000, exceeding the capital ceiling of 62% of North American job shops. Advanced fiber-laser systems above 8 kW cost up to USD 1.8 million with automated load-unload modules. Leasing rates climbed 14% in 2024 as interest costs rose, locking out smaller enterprises that lack collateral. Financing hurdles lengthen the payback period to more than five years in cyclical construction and energy end-markets. Vendors responding with subscription software, modular automation kits, and residual-value guarantees gain traction among capital-constrained buyers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Cutting Systems Lead Growth Momentum

Machining retained the largest 30.56% metal fabrication equipment market share in 2025, underscoring its central role in shaping complex engine blocks, turbine disks, and industrial gearboxes. Demand concentrates in five-axis and high-torque horizontal centers capable of maintaining positional accuracy below ±4 microns across extended shifts. Meanwhile, cutting systems are forecast to expand at a 6.78% CAGR to 2031, marking the highest pace within the metal fabrication equipment market. Fiber-laser platforms above 8 kW deliver cut speeds surpassing 100 meters per minute on 3-millimeter mild steel, offering a 40% throughput edge over plasma while producing heat-affected zones under 20 microns. Suppliers bundling nesting software with automatic nozzle changers provide quantifiable material savings that justify the USD 1.5 million investment.

Welding and joining lines transition toward fiber-laser and friction-stir processes to meet porosity limits in battery housings and LNG cryogenic tanks. Across all categories, automation modules such as robotic load/unload, in-process metrology, and vision-guided seam tracking differentiate offerings and position vendors for the next cycle of capacity additions.

By End-User Industry: Energy Projects Outpace Traditional Automotive Demand

Automotive accounted for a commanding 31.45% of 2025 demand within the metal fabrication equipment market, anchored by continuous investment in battery-electric vehicle platforms and lightweight body-in-white architectures. Plants retooling for structural packs install multi-servo press lines and laser blanking centers that shorten die-changeovers to under three minutes. Yet the fastest-growing customer group is energy and oil-and-gas, projected at a 7.56% CAGR through 2031. Floating LNG modules, subsea manifolds, and offshore wind towers require heavy-plate rolling, high-current submerged-arc welding, and robotic cladding of corrosion-resistant alloys.

Rail, shipbuilding, and agricultural machinery add steady base-load demand, often sourcing mid-range plasma cutters and forging presses that balance cost and performance. Vendors tailoring service packages - spare-parts availability, remote diagnostics, and operator training - anchor their competitive edge across these varied end-user ecosystems.

Geography Analysis

Asia-Pacific captured 46.76% of global 2025 revenue, affirming its status as the volume leader in the metal fabrication equipment market. China’s dual-circulation policy targets 70% domestic self-sufficiency in CNC systems by 2027, spurring large government-backed orders for local builders. India’s incentive schemes converted INR 259 billion (USD 3.1 billion) into subsidies for fiber-laser cutters and servo presses, producing a 34% jump in equipment imports from Japan and Germany. ASEAN countries benefit from electronics and automotive FDI, with Vietnam alone attracting USD 8.2 billion in 2024 for metal-intensive assembly lines.

The Middle East and Africa region will log the fastest 6.23% CAGR through 2031. Saudi Arabia’s Public Investment Fund channels USD 500 billion into NEOM, procuring on-site laser and plate-rolling assets for its steel-heavy infrastructure. The UAE expands modular construction techniques for post-Expo 2030 projects, favoring turnkey robotic welding cells that minimize skilled-labor requirements. South Africa accelerates renewable-energy fabrication to localize solar-tracker frames and wind towers.

North America’s second reshoring wave produces a 78% surge in announced relocations during 2024, concentrating demand in the U.S. Midwest and Mexican automotive corridor. Buyers prioritize machines with remote monitoring compliant with IEC 62443 to mitigate ransomware risk. Canada’s aerospace clusters maintain demand for five-axis machining centers with spindle speeds above 30,000 rpm. Europe transitions to low-carbon steel, pushing fabricators to adopt adaptive machining centers capable of compensating for recycled alloy variability. Germany remains the regional anchor despite a 3.1% contraction in 2024 output, while Italy, Spain, and Poland grow through export-oriented equipment production. South America remains modest in scale, yet Brazil’s automotive sector sustains regular purchase cycles for press brakes and welding robots.

Competitive Landscape

Incumbent leaders Trumpf, Amada, DMG MORI, and Yamazaki Mazak jointly held 42% of 2025 global revenue, but regional suppliers continue to fragment the mid-range segment of the metal fabrication equipment market. Trumpf’s TruConnect suite links lasers, press brakes, and storage towers into one dashboard, reducing programming time by 30% and strengthening customer lock-in. DMG MORI’s CELOS X platform packages predictive maintenance and tool-life analytics on a subscription, shifting value from hardware margin to recurring software revenue.

Chinese entrants such as Shenyang Machine Tool and Han’s Laser narrow the technology gap in 3- to 5-axis machines, leveraging domestic scale to compete aggressively on price. European specialists like Prima Industrie and Salvagnini focus on flexible manufacturing systems that fit into space-constrained job shops. Hybrid additive-subtractive cells emerge as a battleground: Mazak’s HYBRID Multi-Tasking line sold 340 units in 2024, while Desktop Metal and EOS push directed-energy deposition paired with in-situ milling for aerospace repairs.

Strategic M&A consolidates automation expertise. Lincoln Electric’s USD 230 million purchase of Baker Industries adds turnkey integration to its welding portfolio, while Bystronic’s buyout of Swiss automation firm Antil introduces robotic palletizing to its high-power laser cutters. Compliance with IEC 62443 standards becomes a market gatekeeper; Siemens and Rockwell embed zero-trust architectures into CNC controllers to assuage OEM cyber-security audits. Vendors able to pair edge-AI optimization with secure connectivity position themselves to capture growth across reshoring and renewable-energy expansions.

Metal Fabrication Equipment Industry Leaders

Trumpf

Shenyang Machine Tool

Okuma

DMG Mori

Colfaxcorp

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Additive Industries launched the MetalFab 420K modular metal AM system targeting aerospace and automotive parts production, demonstrating the continuing convergence of additive and subtractive workflows.

- January 2025: DMG MORI launched the LASERTEC 125 3D hybrid platform, combining 6-kW directed-energy deposition with five-axis milling in a 1,250-mm envelope. Safran and Rolls-Royce placed 23 initial orders.

Global Metal Fabrication Equipment Market Report Scope

Metal fabrication is a process that involves bending, cutting, and assembling metal to create structures. The process of creating metal includes creating machinery and various structures out of various basic materials. The process of fabricating metal also entails building components, machinery, and buildings out of diverse raw materials. The demand for metal fabrication tools is increasing due to a variety of uses, including automotive, job shops, and secondary businesses.

A complete background analysis of the metal fabrication equipment market, which includes an assessment of the emerging trends by segments and regional markets, and significant changes in market dynamics and market overview.

The Metal Fabrication Equipment market is segmented by Geography (North America, Latin America, Asia-Pacific (APAC), Europe, and Middle East and Africa (MEA)), Service Type (Machining and Cutting, Welding, Forming, and Other Service Types), and End-user Industry (Automotive, Aerospace, Construction, Electrical and Electronics, and Other End-user Industries). The report offers market size and forecasts for metal fabrication equipment market in value (USD billion) for all the above segments.

By Equipment Type / Process

| Machining | Machining Centres |

| Lathe Machines | |

| Drilling, Grinding, Honing & Lapping | |

| Gear-Cutting Machines | |

| Other Handling & Cutting Equipment | |

| Cutting | Laser Cutting |

| Plasma Cutting | |

| Waterjet | |

| Others (Sawing & Cut-off Machines, etc) | |

| Welding & Joining Equipment | Arc Welding |

| Oxy-fuel Welding | |

| Laser-Beam Welding | |

| Other Welding Types | |

| Forming | Sheet metal forming (press brakes/bending, punching/notching, shearing, stamping, roll forming) |

| Bulk forming (forging) | |

| Other Presses & Metal-Forming Machines | |

| Other Equipment Types (Material Handling, Workholding & Automation, etc.) |

By End-user Industry

| Automotive |

| Construction |

| Aerospace |

| Electrical & Electronics |

| Industrial Machinery / Heavy Eequipment |

| Shipbuilding & Marine |

| Rail |

| Energy / Oil & Gas |

| Other Industries (HVAC & appliances, metal furniture, etc) |

By Geography

| North America | United States |

| Canada | |

| Rest of North Amercia | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Equipment Type / Process | Machining | Machining Centres |

| Lathe Machines | ||

| Drilling, Grinding, Honing & Lapping | ||

| Gear-Cutting Machines | ||

| Other Handling & Cutting Equipment | ||

| Cutting | Laser Cutting | |

| Plasma Cutting | ||

| Waterjet | ||

| Others (Sawing & Cut-off Machines, etc) | ||

| Welding & Joining Equipment | Arc Welding | |

| Oxy-fuel Welding | ||

| Laser-Beam Welding | ||

| Other Welding Types | ||

| Forming | Sheet metal forming (press brakes/bending, punching/notching, shearing, stamping, roll forming) | |

| Bulk forming (forging) | ||

| Other Presses & Metal-Forming Machines | ||

| Other Equipment Types (Material Handling, Workholding & Automation, etc.) | ||

| By End-user Industry | Automotive | |

| Construction | ||

| Aerospace | ||

| Electrical & Electronics | ||

| Industrial Machinery / Heavy Eequipment | ||

| Shipbuilding & Marine | ||

| Rail | ||

| Energy / Oil & Gas | ||

| Other Industries (HVAC & appliances, metal furniture, etc) | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North Amercia | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of global metal-fabrication equipment sales and how fast will it expand through 2031?

Sales reached USD 69.68 billion in 2026 and are projected to rise to USD 86.96 billion by 2031, reflecting a 4.53% CAGR.

Which equipment category is posting the quickest growth and what drives that momentum?

Cutting systems, led by high-power fiber-laser platforms, are on track for a 6.78% CAGR thanks to faster throughput, narrower kerf widths, and rising demand for thin-gauge components in electric vehicles and aerospace assemblies.

Which customer segment is expected to generate the largest incremental demand over the next five years?

Energy and oil-and-gas projects show the fastest expansion at a 7.56% CAGR as floating LNG terminals, subsea manifolds, and offshore wind towers require heavy-plate rolling and high-current welding solutions.

Why are Asia-Pacific manufacturers ramping up purchases of fiber-laser cutters and servo-press brakes?

China’s push for 70% CNC self-sufficiency and India’s subsidy programs are spurring upgrades to meet tighter tolerances and higher production volumes while reducing reliance on imported machine tools.

Page last updated on: