Metal Forming Tools Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 37.96 Billion |

| Market Size (2030) | USD 50.27 Billion |

| Growth Rate (2025 - 2030) | 5.78% CAGR |

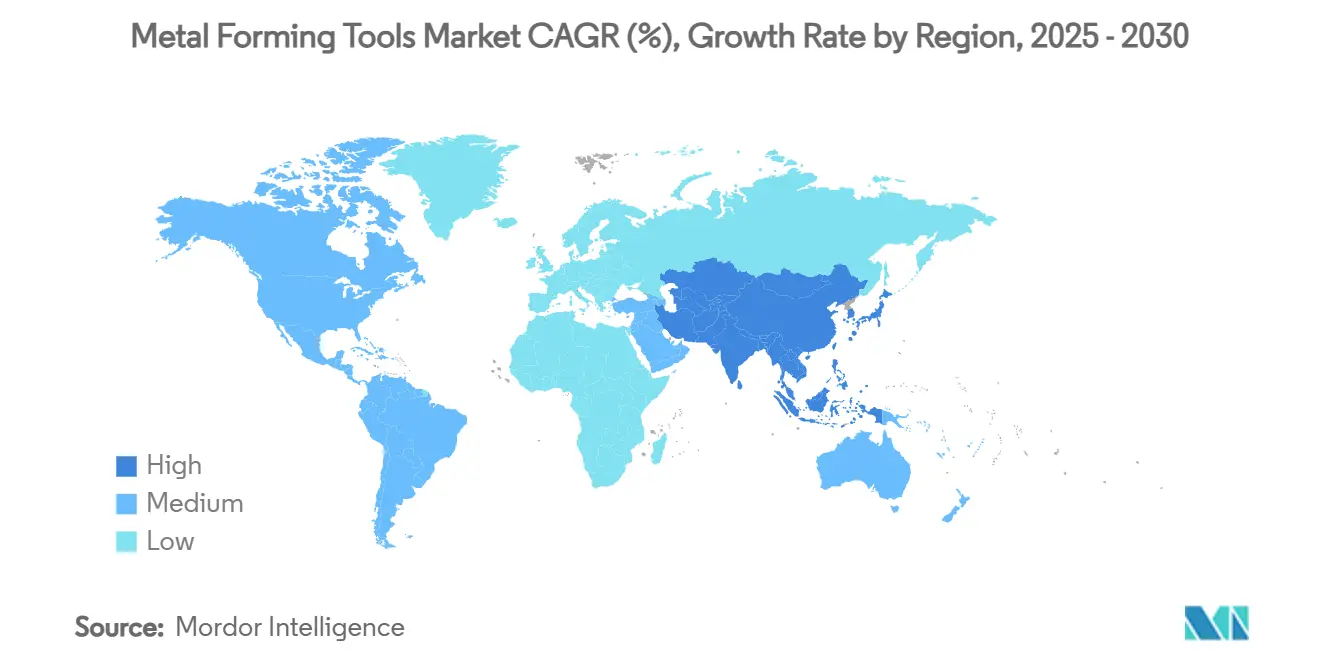

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Metal Forming Tools Market Analysis by Mordor Intelligence

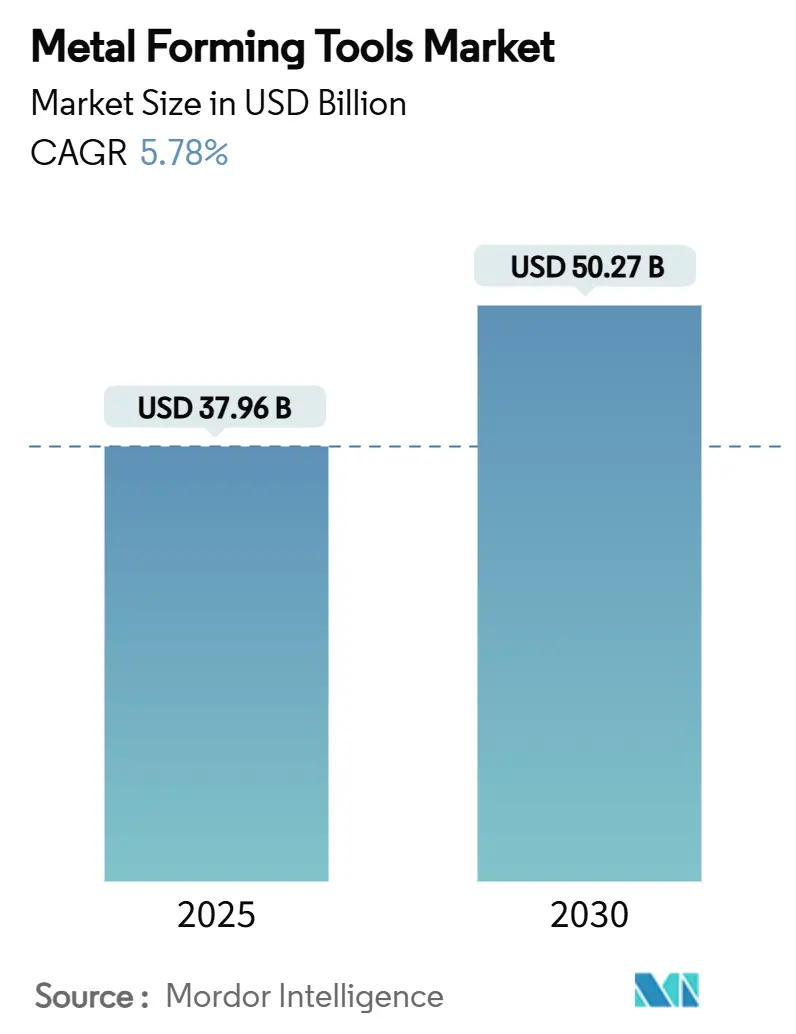

The Metal Forming Tools Market size stands at USD 37.96 billion in 2025 and is projected to reach USD 50.27 billion by 2030, advancing at a 5.78% CAGR. Increasing electric-vehicle (EV) volumes, the widening of reshoring programs in North America and Europe, and a decisive shift from hydraulic to servo-electric presses are the most visible forces driving this trajectory. Automakers now require presses that can shape ultra-high-tensile steels and aluminum gigacast structures, while aerospace and medical-implant producers demand micron-level repeatability. Manufacturers also face an urgent need to offset skilled-labor shortages, leading to broader adoption of automation, real-time process monitoring, and lights-out manufacturing practices. Rapid tooling cycles in aerospace additive manufacturing, government-funded infrastructure programs, and vertical-integration strategies pursued by leading suppliers round out the main growth enablers for the metal forming tools market.

Key Report Takeaways

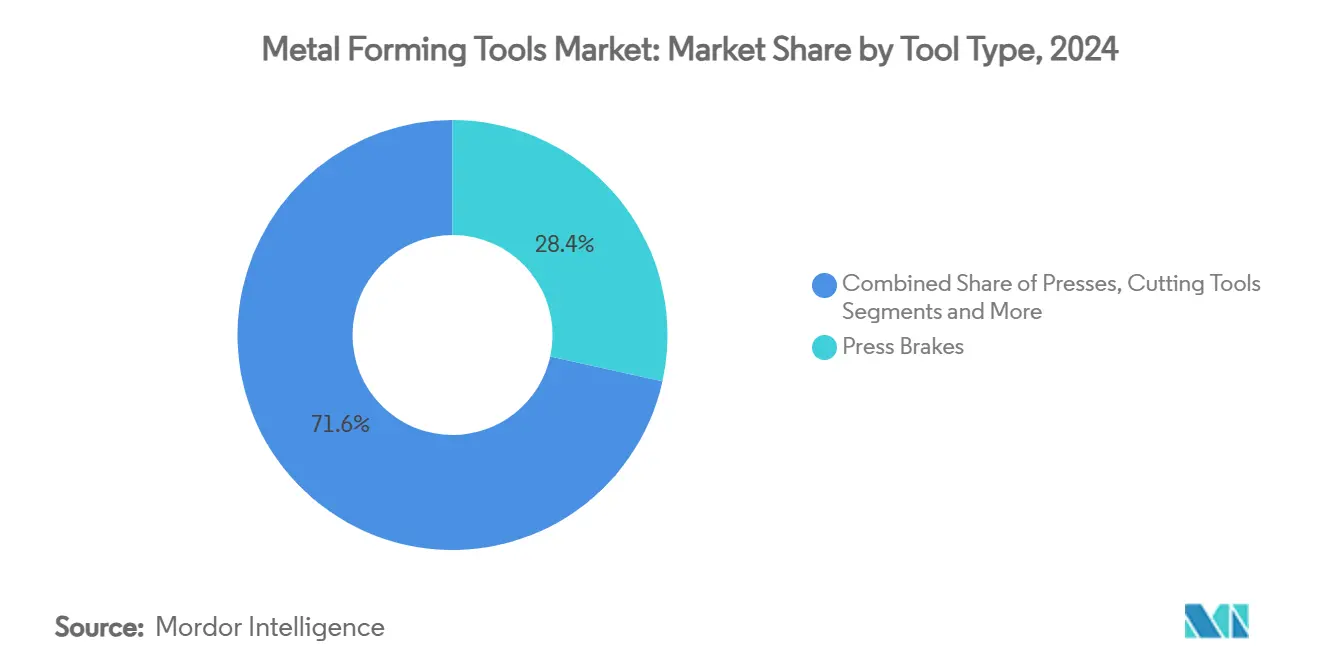

- By Tool Type, Press brakes held 28.45% of the 2024 metal forming tools market share; servo presses are forecast to expand at a 9.80% CAGR to 2030.

- By Forming Process, Stamping dominated with 32.33% share of the 2024 metal forming tools market size; bending equipment records the fastest growth at 6.70% CAGR through 2030.

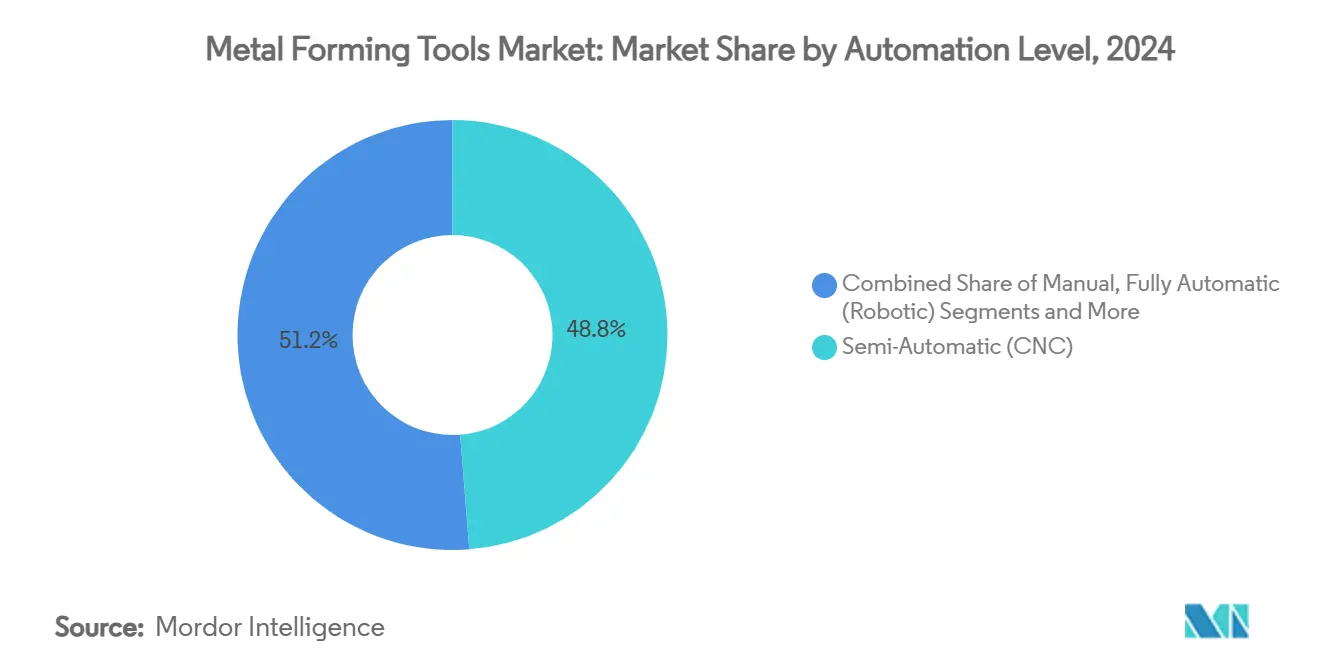

- By Automation Level, Semi-automatic systems accounted for 48.76% of the 2024 metal forming tools market share, while fully automatic solutions are advancing at an 8.90% CAGR over the forecast horizon.

- By End-use Industry, the automotive sector led with 35.46% contribution to the 2024 metal forming tools market size, whereas EV component manufacturing accelerates at 11.20% CAGR to 2030.

- By Geography, Asia-Pacific commanded 41.22% of the 2024 metal forming tools market share, with the region also recording the peak 8.90% CAGR through 2030.

Global Metal Forming Tools Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in EV & lightweight vehicle production | +1.2% | Global – especially China, North America, Europe | Medium term (2-4 years) |

| Demand for precision-engineered medical implants | +0.8% | North America & EU; rising in Asia-Pacific | Long term (≥ 4 years) |

| Re-shoring of manufacturing in North America & EU | +0.6% | North America & EU core, Mexico spill-over | Medium term (2-4 years) |

| Rapid tooling needs for aerospace 3-D printed parts | +0.4% | North America, Europe, selective Asia-Pacific markets | Long term (≥ 4 years) |

| Cold-forming adoption in green-hydrogen equipment | +0.3% | Global; early in EU and Japan | Long term (≥ 4 years) |

| OEM shift to servomechanical presses | +0.2% | Global; led by developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in EV & Lightweight Vehicle Production

EV manufacturing reshapes forming requirements, as plants move from multi-part body-in-white assemblies to single-piece gigacastings. Tesla’s gigacasting condensed more than 70 Model 3 stampings into two Model Y cast sections, prompting rivals from Volvo to Hyundai to pursue similar strategies. This shift elevates demand for servo-electric presses that deliver programmable motion profiles and high forming energies without hydraulic losses. Traditional press builders, such as AIDA Engineering, reported a USD 548 million order backlog driven largely by EV tooling orders, highlighting the commercial pull of the trend. While the upside is clear, raw-material price swings and high-strength-steel springback complications force suppliers to invest in stronger dies and advanced lubrication systems, adding cost and engineering complexity[1]Government of India, "Specialty Steel Production to Rise from 18 Million to 42 Million Tonnes by 2026-27," Press Information Bureau, pib.gov.in.

Demand for Precision-Engineered Medical Implants

Orthopedic plates, screws, and custom joint components require tolerances in the low-micron range and surfaces free of inclusions. Updated U.S. FDA guidance obliges producers to verify tensile strength, fatigue resistance, and corrosion behavior at every design change. These rules raise the bar for servo-electric presses fitted with high-resolution load cells and closed-loop axis control. Titanium and cobalt-chromium alloys, common in implants, harden rapidly during deformation, accelerating tool wear and necessitating premium coatings. Aging populations in Europe, North America, and Japan support stable volume growth, while the sector’s high margins offset the capital costs of specialized forming cells.

Re-shoring of Manufacturing in North America & EU

A reported 287,000 U.S. jobs were linked to reshoring or foreign direct investment in 1H 2023, reflecting a shift from cost-optimization to resilience strategies. Federal programs, including the USD 1.2 trillion Infrastructure Investment and Jobs Act, significantly escalate domestic demand for formed steel shapes, rebar, and cast parts. Servo-electric presses with lower electricity draw and shorter setup times help offset higher labor costs typical in developed economies. Yet the success of reshoring depends on workforce availability; hence, suppliers bundle turnkey automation, training, and preventive-maintenance packages to fast-track plant ramp-ups.

Rapid Tooling Needs for Aerospace 3-D Printed Parts

Serial additive manufacturing in aerospace now requires post-printing forming, straightening, or surface-enhancement operations to meet stringent qualification protocols such as IQ, OQ, and PQ. Hybrid cells that blend 3-D printing with precision forming enable OEMs to hit tolerance windows while scaling batch sizes. Nickel-based superalloys and Ti-6Al-4V powders impose high tool stresses, driving interest in water-cooled dies and sensor-embedded press lines for in-process monitoring. Growth is robust, but the regulatory pathway is complex, prolonging customer validation cycles and limiting the pace of capex releases.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital intensity & long ROI | -0.6% | Global, particularly impacting smaller manufacturers | Medium term (2-4 years) |

| Volatility in steel & carbide prices | -0.5% | Global, with higher impact in price-sensitive markets | Short term (≤ 2 years) |

| Shortage of skilled tool & die makers | -0.4% | North America & EU primarily, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Cyber-security risk in networked press lines | -0.3% | Global, concentrated in developed markets with high automation | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Intensity & Long ROI

Advanced servo presses cost 30–50% more than legacy hydraulic models, even before tooling, robotics, and software are added. Smaller firms find it difficult to clear internal hurdle rates when ROI stretches beyond five years. A Massachusetts apprenticeship program illustrates the parallel human-capital burden, demanding 8,000 work hours and 150 hours of annual classroom instruction for a journeyman tool-and-die credential. Economic uncertainty further suppresses spending, especially where order visibility is limited. Suppliers respond with modular press frames, subscription software, and buy-back guarantees to soften balance-sheet impact, yet adoption remains gated by borrower creditworthiness and macro sentiment.

Volatility in Steel & Carbide Prices

Steel and carbide price swings place direct pressure on production budgets for metal forming tool suppliers. When Beijing imposed export curbs on gallium and germanium, the spot price of gallium jumped almost 20% to USD 332.50 per kilogram by July 2023, showing how geopolitical moves can change input costs overnight. Shifting steel prices influence both the factory floor and customers’ purchasing plans because many buyers postpone new-equipment orders when material costs feel unstable. Carbide tools, which rely on tungsten powders, face similar tension as tight ore supplies and higher refining fees feed into finished-tool prices. The unpredictable cost curve also complicates inventory planning: too much stock ties up cash, yet too little increases the risk of production stoppages. Small and midsize firms feel the strain most because they lack the leverage to lock in long-term contracts or to cushion short-lived price spikes without eroding margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Tool Type: Press Brakes Lead While Servo Technology Accelerates

In 2024, press brakes seized a 28.45% share of the metal forming tools market, showcasing their adaptability in sectors ranging from construction panels to aerospace stringers. The established ecosystems of dies, back-gauges, and offline programming software play a pivotal role in maintaining competitive ownership costs. The fastest-growing category, servo presses, is projected to clock a 9.80% CAGR through 2030, underpinned by energy savings and precise stroke control critical for high-strength steel and aluminum gigacast components. The metal forming tools market size for press brakes is therefore poised to expand steadily, while the servo press slice broadens even faster as OEMs target programmable motion and lower noise. TRUMPF’s Flex Cell mobile bending release in 2024 exemplifies how traditional press-brake leaders are embedding automation to bridge labor shortages and secure incremental revenue.

Growing EV and aerospace backlogs stimulate demand for heavy-tonnage servo presses, notably in Asia-Pacific, where green-field factories skip hydraulic lines entirely. Meanwhile, mechanical presses retain relevance in canned-food lids and standard body panels because their hit rates outpace servo systems on small stroke heights. Dies and punch tooling remain evergreen revenue streams tied to press-fleet size, prompting suppliers to offer subscription-based tool-management portals that alert users to wear patterns. Rolling, cutting, and hydroforming tools form niche sub-markets whose growth tracks specific material trends, such as aluminum extrusions for battery enclosures or hydroformed stainless tubes in fuel-cell stacks.

By Forming Process: Stamping Dominance Faces Bending Innovation

Stamping operations held 32.33% of the metal forming tools market share in 2024, benefiting from entrenched lines in automotive and appliance factories that run around the clock. However, bending machines, aided by collaborative robots and offline programming, are rising at a 6.70% CAGR. The metal forming tools market size tied to bending will therefore gain steadily as mass customization and shorter product life cycles push users toward flexible systems. Cincinnati Incorporated’s EZ Bend cobotic cell shows how vendors slash setup times, letting low-volume, high-mix shops meet fabricator lead-time targets.

Forging continues to anchor aerospace landing-gear blanks and auto crankshafts where directional strength matters, but its share is largely static. Extrusion benefits from lightweighting imperatives in transport and building facades. Laser-assisted cutting marries well with forming processes in integrated cells, yielding part-to-part traceability and reduced work-in-progress. Manufacturers increasingly choose hybrid lines that stamp, bend, and cut in one pass, paying a premium for software-driven flexibility. Suppliers that bundle PLCs, machine vision, and predictive-maintenance analytics thus capture higher wallet share.

By Automation Level: Semi-Automatic Systems Transition to Full Automation

In 2024, semi-automatic machines accounted for 48.76% of the metal forming tools market share, reflecting a midpoint where CNC control coexists with operator oversight. Fully automatic systems, boosted by a robust 8.90% CAGR forecast, attract factories wrestling with labor shortages and tighter tolerance windows. The metal forming tools market size linked to fully autonomous lines is swelling fastest inside giga-factories producing battery trays and motor housings for EVs.

ABB’s OmniVance collaborative tending cell demonstrates productivity gains of up to 60%, freeing scarce technicians for higher-value tasks. Lights-out operations remain nascent but draw attention as energy-cost spikes encourage off-peak scheduling. Sensors and 5G connectivity, such as SMS Group’s smart-factory deployment at Lech-Stahlwerke, illustrate how real-time condition monitoring underpins predictive maintenance. Manual setups persist in aerospace job shops making exotic-metal parts, where volumes are too low for economic automation; however, even here, quick-change tooling and offline simulation shave downtime.

By End-Use Industry: Automotive Leadership Challenged by EV Transformation

Automotive represented 35.46% of the metal forming tools market size in 2024, but must adapt quickly to 11.20% CAGR growth in dedicated EV component lines. Investments like Honda’s USD 15 billion Canadian EV plant and BMW’s Mexico battery-platform expansion underline how new drive-train architectures translate into tooling refresh cycles. Gigacastings require presses exceeding 6,000 tons plus precision die-temperature control, stretching supplier engineering capabilities[2]Invest in Türkiye, "Turkish Machinery Sector Generated USD 47 Billion Revenue Employing 300,000 People," Investment Office, invest.gov.tr.

Aerospace and defense remain premium segments paying for traceability and certification, while industrial machinery delivers steady base-load demand for standard presses. Building and construction recycling policies support structural-steel rolling, especially in fast-urbanizing APAC cities. Electrical and electronics producers push nano-scale tolerances for connectors, spurring high-speed stamping press upgrades. Medical devices, though a smaller volume play, offer high margins because each implant line needs class-cleanroom integration and rigorous validation.

Geography Analysis

Asia-Pacific controlled 41.22% of the 2024 metal forming tools market share and is set to grow at an unrivaled 8.90% CAGR. China’s cluster economies in the Yangtze River Delta and Guangdong deliver vast press orders for EV body shops and consumer electronics casings, while Japan supplies high-precision servo drives and advanced die steels, as shown by Yamaichi Hagane’s distribution accord with Tiangong. India’s Production Linked Incentive (PLI) schemes draw global auto and electronics OEMs, fuelling demand for mid-tonnage CNC brakes and coil-feed lines. Supply-chain diversification into Vietnam, Thailand, and Indonesia accelerates regional installations as firms hedge geopolitical risk[3]National Bureau of Statistics of China, "Manufacturing Value Added Increased 6.0% in May 2024 with Metal Products Growth at 6.6%," National Bureau of Statistics, stats.gov.cn.

North America benefits from reshoring and infrastructure spending. Stimulus programs channel fresh orders into domestic foundries and sheet-metal fabricators. Mexico emerges as a near-shore hub, with automotive and white-goods makers relocating from Asia to cut logistics lead times. U.S. aerospace primes continue to buy precision presses for aluminum-lithium skins and titanium spars, sustaining a technology-rich equipment mix that favors servo-electric and hydraulic-hybrid designs.

Europe battles soft macro conditions yet leans on engineering prowess and sustainability mandates. German mills like ThyssenKrupp Materials Processing added a new slitting line, boosting capacity to 350,000 tons annually, indicating confidence in regional industrial recovery. The EU Green Deal raises demand for energy-efficient machines, while high power prices push operators toward servo presses with regenerative drives. Eastern Europe attracts green-field investments for cost-competitive stamping, but persistent skilled-labor gaps could limit ramp-ups.

Competitive Landscape

Competition is moderately concentrated, with the top 10 players controlling a moderate percentage of global revenue. TRUMPF, Amada, and Schuler (recently rebranded ANDRITZ Schuler) maintain technology leadership by offering integrated press-line, laser, and bending portfolios. Chinese entrants leverage volume cost advantages, forcing incumbents to differentiate through automation suites and global service footprints. TRUMPF’s USD 5.62 billion (EUR 5.2 billion) 2023/24 revenue fell 3.6% amid softer global capex and aggressive Chinese pricing, spotlighting margin pressure on premium products.

Strategic acquisitions mark an ongoing consolidation trend. Wilson Tool International’s January 2025 purchase of PASS Stanztechnik deepens its European footprint and broadens die-set offerings, while United Grinding’s agreement to buy GF Machining Solutions positions the group for ultra-precision tool-grinding synergies. Suppliers also invest in regional service hubs; Komatsu reorganized its U.S. arm in February 2025 to streamline governance and improve customer proximity. Such moves underscore a pivot from pure equipment sales toward lifecycle value propositions encompassing spares, training, and predictive-maintenance analytics.

Technology roadmaps now center on digitalization, energy efficiency, and cybersecurity. Prima Power displayed robotic press-brake cells at EuroBLECH 2024 aimed at unattended operation, while Schuler North America pumped funds into tubular hydroforming to address vehicle lightweighting. Vendors embed OPC-UA or proprietary protocols for data logging, yet face mounting threats from ransomware aimed at networked press lines. Partnerships with cybersecurity specialists, therefore, become a new differentiator for OEM bids in high-security sectors such as defense and medical devices.

Metal Forming Tools Industry Leaders

-

TRUMPF Group

-

Amada Co., Ltd.

-

Schuler AG

-

JIER Machine-Tool Group

-

DMG Mori

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: ANDRITZ AG rebranded Schuler as ANDRITZ Schuler to deepen integrated forming and handling solutions.

- February 2025: Komatsu Ltd. reorganized its U.S. subsidiaries to improve customer convenience and governance.

- January 2025: Wilson Tool International acquired PASS Stanztechnik AG, expanding European punch-press tooling reach.

- November 2024: United Grinding announced an agreement to purchase GF Machining Solutions, closing expected in Q1/Q2 2025.

Global Metal Forming Tools Market Report Scope

| Presses | Mechanical Press |

| Hydraulic Press | |

| Servo-Electric Press | |

| Screw / Knuckle Press | |

| Press Brakes | |

| Rolling Tools (Rolling Mills, Thread Rollers, etc.) | |

| Cutting Tools | |

| Hydroforming Equipment | |

| Dies & Punch Tooling | Stamping Dies |

| Forging Dies | |

| Extrusion Dies | |

| Roll-Forming Tooling |

| Stamping (Cold & Hot) |

| Forging (Hot / Warm / Cold) |

| Rolling (Flat / Section) |

| Extrusion (Direct / Indirect / Hydrostatic) |

| Cutting |

| Bending |

| Others (Extrusion, etc.) |

| Manual |

| Semi-Automatic (CNC) |

| Fully Automatic (Robotic) |

| Lights-Out / Smart Factory |

| Automotive & Transportation |

| Aerospace & Defense |

| Industrial Machinery & Capital Goods |

| Building & Construction |

| Electrical & Electronics |

| Energy (Renewables / Oil & Gas) |

| Medical Devices |

| Others (Consumer Appliances, etc) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Peru | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Turkey | |

| Egypt | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Tool Type | Presses | Mechanical Press |

| Hydraulic Press | ||

| Servo-Electric Press | ||

| Screw / Knuckle Press | ||

| Press Brakes | ||

| Rolling Tools (Rolling Mills, Thread Rollers, etc.) | ||

| Cutting Tools | ||

| Hydroforming Equipment | ||

| Dies & Punch Tooling | Stamping Dies | |

| Forging Dies | ||

| Extrusion Dies | ||

| Roll-Forming Tooling | ||

| By Forming Process | Stamping (Cold & Hot) | |

| Forging (Hot / Warm / Cold) | ||

| Rolling (Flat / Section) | ||

| Extrusion (Direct / Indirect / Hydrostatic) | ||

| Cutting | ||

| Bending | ||

| Others (Extrusion, etc.) | ||

| By Automation Level | Manual | |

| Semi-Automatic (CNC) | ||

| Fully Automatic (Robotic) | ||

| Lights-Out / Smart Factory | ||

| By End-use Industry | Automotive & Transportation | |

| Aerospace & Defense | ||

| Industrial Machinery & Capital Goods | ||

| Building & Construction | ||

| Electrical & Electronics | ||

| Energy (Renewables / Oil & Gas) | ||

| Medical Devices | ||

| Others (Consumer Appliances, etc) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Peru | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Kuwait | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the metal forming tools market by 2030?

The market is expected to reach USD 50.27 billion by 2030 on a 5.78% CAGR trajectory.

Which tool type currently holds the largest share?

Press brakes led in 2024 with a 28.45% share, thanks to their versatility across multiple industries.

Why are servo-electric presses gaining popularity?

They offer higher energy efficiency, programmable motion profiles, and lower maintenance than hydraulic presses, supporting complex EV and aerospace parts.

Which region will grow the fastest through 2030?

Asia-Pacific is forecast to post an 8.90% CAGR, driven by China’s volume demand and Japan’s precision tooling expertise.

How are labor shortages influencing equipment purchases?

Manufacturers adopt fully automatic and collaborative-robot solutions to reduce reliance on scarce, skilled tool-and-die makers.

Page last updated on: