Welding Electrodes Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

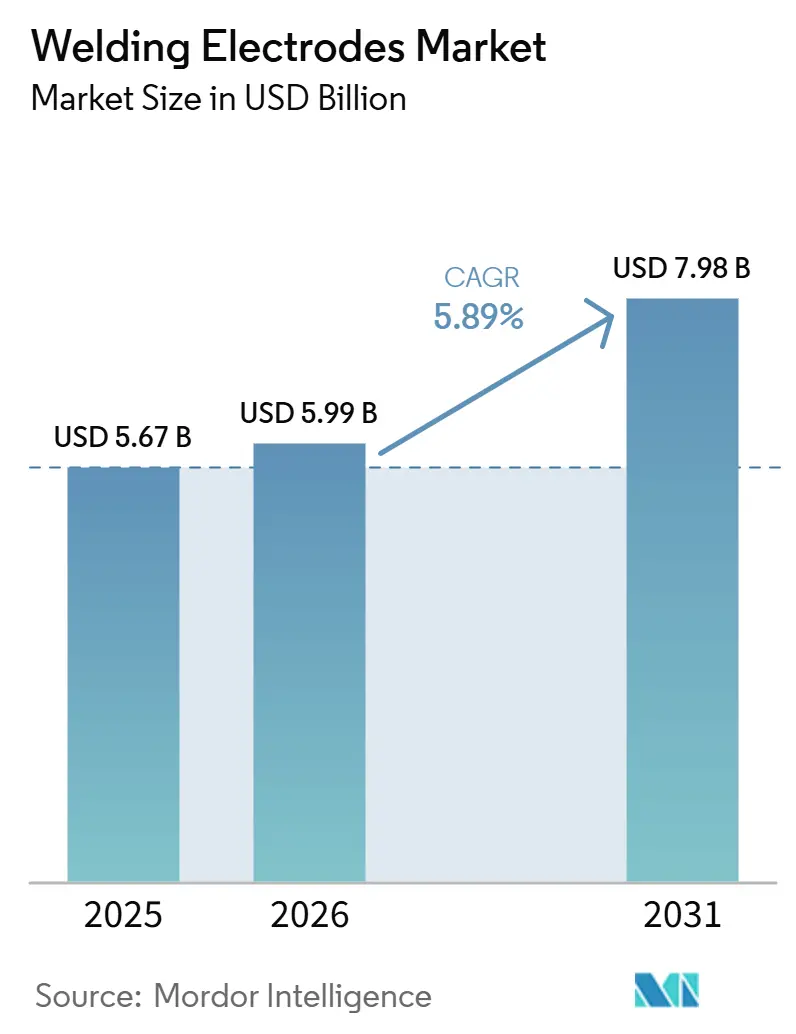

| Market Size (2026) | USD 5.99 Billion |

| Market Size (2031) | USD 7.98 Billion |

| Growth Rate (2026 - 2031) | 5.89% CAGR |

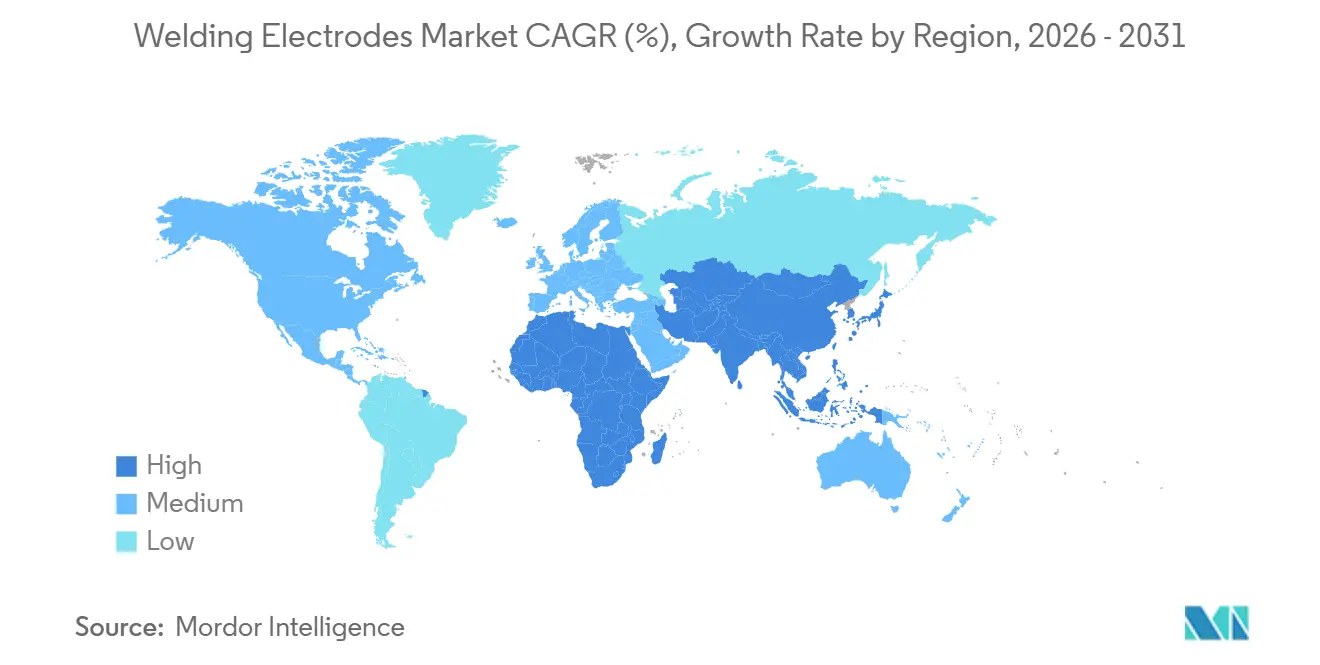

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Welding Electrodes Market Analysis by Mordor Intelligence

The Welding Electrodes Market size is projected to be USD 5.67 billion in 2025, USD 5.99 billion in 2026, and reach USD 7.98 billion by 2031, growing at a CAGR of 5.89% from 2026 to 2031.

Specialty demand linked to low-hydrogen stick formulations for pressure vessels, nickel-alloy electrodes for 9% Ni LNG tanks, and moisture-resistant coatings for marine work supports steady consumption even as automation displaces manual processes in repetitive fabrication. Activity in shipbuilding, cross-country pipelines, and high-rise steel construction continues to anchor volume, while defense manufacturing adds a resilient layer of demand insulated from general construction cycles. Asia-Pacific leads due to China’s shipbuilding scale and South Korea’s LNG carrier specialization, while the fastest growth is shifting to the Middle East and Africa on the back of pipeline programs tied to LNG supply diversification. Competitive strategies are tilting toward integrated ecosystems that bundle equipment and consumables, which reduces price-only competition and supports premium electrode categories. Regulatory and certification intensity also favors suppliers with the metallurgical depth to qualify products for critical applications where failure risks are non-negotiable.

Key Report Takeaways

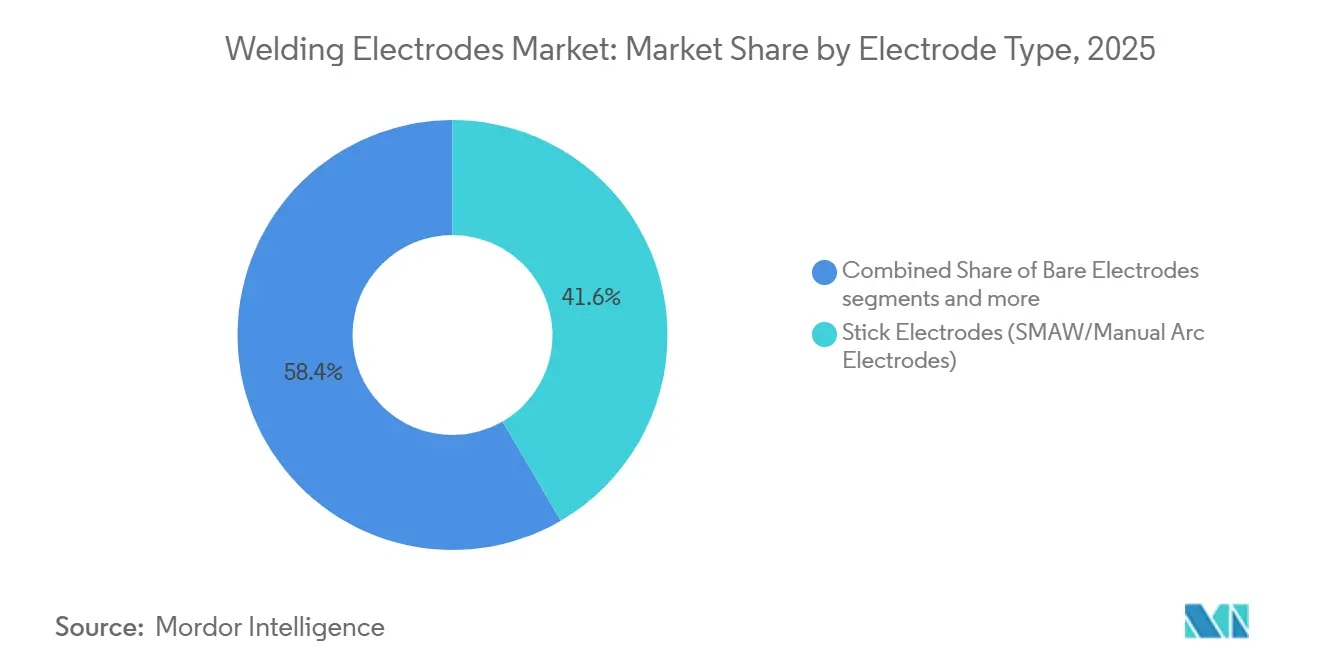

- By electrode type, stick electrodes led with 41.61% market share of the welding electrodes market size in 2025; basic or low-hydrogen stick formulations are projected to grow at a 6.23% CAGR through 2031.

- By coating type, rutile coatings accounted for 43.62% of the share in 2025; basic or low-hydrogen coatings are forecast to expand at a 6.50% CAGR through 2031.

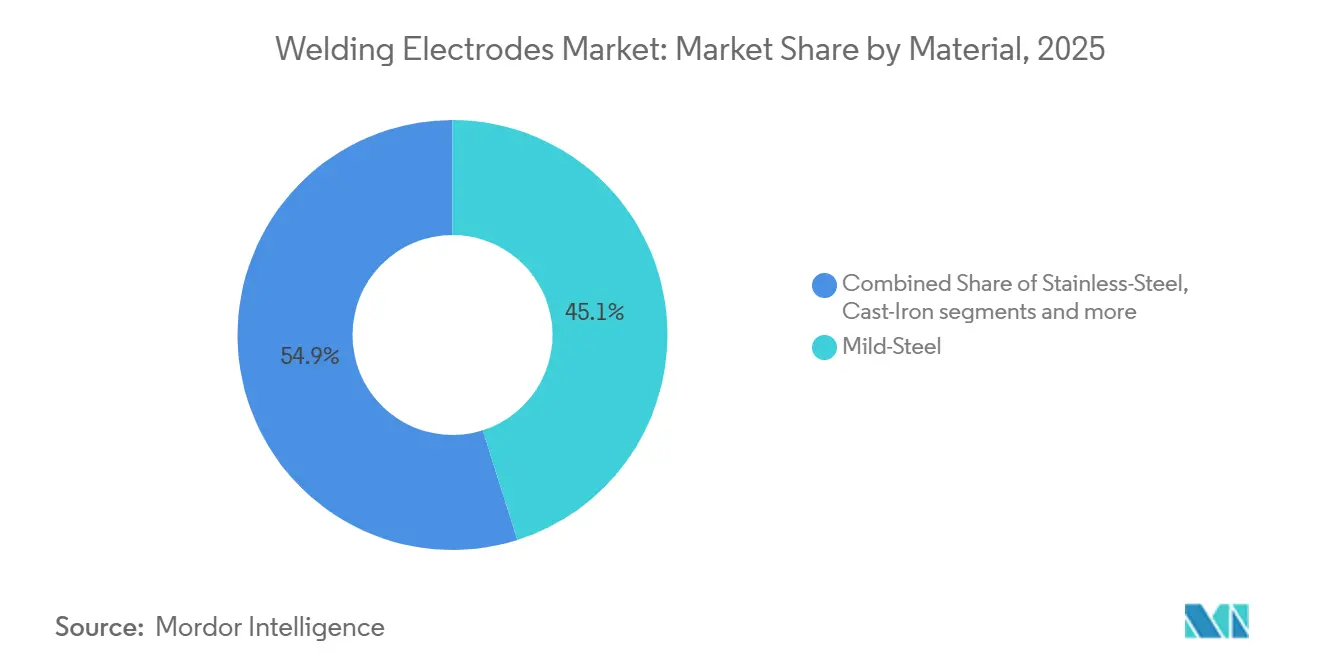

- By material, mild-steel electrodes captured 45.12% of the welding electrodes market share in 2025; nickel and specialty alloy electrodes are expected to advance at a 7.10% CAGR through 2031.

- By end-user industry, construction held 29.32% of the share in 2025; aerospace and defense is projected to grow at a 7.60% CAGR to 2031.

- By geography, Asia-Pacific commanded 45.14% market share in 2025; the Middle East and Africa are expected to post the fastest growth at a 7.90% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Welding Electrodes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Large-Scale Shipbuilding Activity in China and South Korea | +1.2% | Asia-Pacific core (China, South Korea), spillover to Southeast Asia | Medium term (≤ 4 years) |

| Cross-Country Oil and Gas Pipeline Projects | +0.9% | Global, with concentration in Middle East, North America, South America | Medium term (≤ 4 years) |

| Steel Structure Fabrication for High-Rise Construction | +0.8% | Global, particularly Asia-Pacific (China, India), Middle East (UAE, Saudi Arabia, Qatar) | Long term (≥ 4 years) |

| Railway Infrastructure and Rolling Stock Manufacturing | +0.7% | North America, Europe (Italy, Germany), Asia-Pacific | Medium term (≤ 4 years) |

| Wind Turbine Tower Manufacturing and Installation | +0.6% | Europe (Poland, Germany), Asia-Pacific, North America | Long term (≥ 4 years) |

| Defense Vehicle and Equipment Production | +0.5% | North America (US), Asia-Pacific (South Korea, China), Europe | Medium term (≤ 4 years) |

| Source: Mordor Intelligence | |||

Large-Scale Shipbuilding Activity in China and South Korea

China secured about 62% of global shipbuilding orders in 2025, exceeding 1,500 vessels, while South Korea’s HD Hyundai, Hanwha Ocean, and Samsung Heavy Industries booked new orders focused on LNG carriers, VLCCs, and FPSO units. This mix requires low-hydrogen stick electrodes for thick hull plate, nickel-alloy filler metals for cryogenic LNG systems, and flux-cored wires that support high-productivity, multi-pass welds in double-hull spaces. Defense-focused programs such as HD Hyundai’s naval and offshore special ships add specifications that drive adoption of H4R-class electrodes stored in temperature-controlled ovens. Hanwha Ocean’s 2025 order book and aging VLCC fleet dynamics point to a replacement cycle that sustains electrode demand across several years. The scale, technical requirements, and defense orders create a stable base for the welding electrodes market in Asia’s yards.[1]Staff Report, “China Continued Shipbuilding Dominance in 2025, Raking In Most Orders,” The Maritime Executive, maritime-executive.com

Cross-Country Oil and Gas Pipeline Projects

Over 100 offshore pipelines slated to come online in 2026 require positional welding in subsea conditions, where moisture control and hydrogen infusibility are central to avoiding delayed cracking. Flagship projects include Argentina’s Vaca Muerta Sur and Qatar’s North Field East, which rely on cellulosic electrodes for root passes and low-hydrogen electrodes for fill and cap sequences under ASME code regimes. North American projects like Enbridge’s Sunrise Expansion and Energy Transfer’s Texas pipeline program reinforce multi-year demand for qualified consumables and certified procedures. Post-2022 energy security priorities continue to drive cross-border investments that diversify gas supply, supporting specialty electrode usage even as upstream spending cycles shift. This infrastructure build-out is a direct tailwind for the welding electrodes market aligned to pipeline construction standards and workflows.[2]Editorial Team, “The Ten Biggest Offshore Oil and Gas Pipelines in 2026,” Offshore Technology, offshore-technology.com

Steel Structure Fabrication for High-Rise Construction

High-rise projects in Asia-Pacific and the Middle East are adopting steel frame systems at scale because modular prefabrication cuts on-site assembly time for structural cores and columns. Structural grades such as Q355B, S355JR, A572, and SM490A require filler metals that achieve base-metal strength and impact toughness standards, which steer contractors to qualified electrodes and wires. Developers also weigh the life cycle and carbon profile upside of steel structures in markets where green building certification is gaining traction. Fabrication workflows mix flux-cored wires for submerged arc processes with stick electrodes for positional welds that resist automation. As urbanization continues, this trend supports ongoing consumption for certified electrodes in commercial towers and transport hubs within the welding electrodes market.

Railway Infrastructure and Rolling Stock Manufacturing

U.S. and European rail programs are refreshing track, rolling stock, and intermodal capacity, and these upgrades require welding solutions that address pearlitic rail steels and in-depot fabrication. BNSF’s 2026 program covers extensive track maintenance and capacity expansion that depends on qualified consumables and procedures. Italy’s Trenitalia modernization program accelerates regional fleet renewal, where welding spans bogie frames, undercarriage brackets, and interior assemblies subject to EN standards. Defense vehicle contracts like BAE Systems’ ACV production reinforce a base of armored steel welding governed by strict process control. This combination cushions the welding electrodes market from the volatility of building cycles and places a premium on electrodes that meet railway and defense quality regimes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift from Manual Stick Welding to Semi-Automatic Processes | -0.8% | Global, particularly advanced manufacturing hubs in North America, Europe, Asia-Pacific (Japan, South Korea) | Short term (≤ 2 years) |

| Quality Issues with Unbranded and Counterfeit Electrodes | -0.4% | Emerging markets in Asia-Pacific, Middle East, Africa, Latin America | Medium term (2-4 years) |

| Moisture Contamination During Storage and Handling | -0.3% | Global, with higher impact in high-humidity coastal regions (Southeast Asia, Gulf Coast, tropical zones) | Short term (≤ 2 years) |

| Price Erosion Due to Excessive Manufacturing Capacity | -0.6% | Global, driven by Asia-Pacific overcapacity (China), affecting all export markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shift from Manual Stick Welding to Semi-Automatic Processes

Fabricators continue to replace manual SMAW with semi-automatic GMAW and fully automated cells to reduce labor costs and improve quality consistency. In shipbuilding, Korean initiatives to pilot humanoid welding robots illustrate how automation is moving from simple fillet welds toward more complex tasks in constrained spaces. Equipment vendors are bundling pulsed multiprocessor power sources with proprietary consumables to create integrated ecosystems that favor wire-fed processes over stick electrodes. While automation expands steadily, manual processes persist in emergency field repairs and hard-to-access joints where robots are set up and reach limit robots. The net effect is a gradual shift that reduces baseline stick electrode volume but keeps specialty electrodes relevant for critical or remote operations within the welding electrodes market.

Moisture Contamination During Storage and Handling

Moisture pickup in flux coatings remains a primary cause of hydrogen-induced cracking in high-strength steel welds. Low-hydrogen electrodes like E7018-1 H4R are engineered to meet strict diffusible hydrogen thresholds, but field humidity and storage lapses can quickly degrade performance if electrodes are not kept in holding ovens or sealed packaging. Manufacturers and distributors promote vacuum-sealed packs and clear usage windows once opened, yet compliance gaps persist among smaller contractors operating in humid climates. Best-practice guides for pressure vessel welding warn that contaminated electrodes must be pulled from service to avoid unpredictable hydrogen uptake that drives cracking and reworking. Process discipline in storage, handling, and re-baking is therefore as critical as product selection to ensure weld integrity in the welding electrodes market.[3]Adam’s Tarp & Tool, “ESAB Low Hydrogen OK 55.00 E7018-1 H4R,” Adam’s Tarp & Tool, adamstarpntool.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Electrode Type: Stick Electrodes, Anchor, Manual, Precision Welding

Stick electrodes held 41.61% of the welding electrodes market share in 2025, reflecting their versatility for field repair and positional welds in areas with limited access. Within this category, basic and low-hydrogen sticks are projected to grow at 6.23% through 2031 as contractors prioritize diffusible hydrogen limits for critical joints, which supports the welding electrodes market size outlook linked to pressure vessel and pipeline standards. Flux-cored wires are gaining share in shipbuilding for double-hull sections where self-shielding reduces gas logistics, while solid wires align with robotic cells in automotive and wind nacelle fabrication. Bare electrodes remain concentrated in submerged arc lines for pipe mills, and gouging or hard-facing sticks continue to serve high-wear rebuilds in mining and cement. The trajectory is toward greater specialization as end users demand electrodes tuned to specific base metals and hydrogen thresholds rather than broad-spectrum general-purpose products. Certification frameworks across AWS and ISO classes ensure consistent performance and traceability for mission-critical work. Demand for metal-cored electrodes is steady in plants with advanced process control, although their narrower parameter window limits are adopted compared with flux-cored alternatives. Specialty consumables for very thick sections, cryogenic service, or elevated temperature exposure require metallurgical support and testing capacity that favors integrated incumbents. The welding electrodes market continues to bifurcate into high-volume commodity offerings and engineered premium grades with qualification support. As manual stick work in assembly lines recedes with automation, the remaining stick demand concentrates in jobs where human precision, reach, and setup speed are decisive. This concentration strengthens the case for premium, low-hydrogen variants that reduce rework risk and improve compliance in audits of critical infrastructure.

By Coating Type: Rutile Dominates General Fabrication, Low-Hydrogen Accelerates in Critical Applications

Rutile-coated electrodes accounted for 43.62% of the value in 2025 due to forgiving arc behavior and easy slag removal, especially in small shops and repair settings. Basic and low-hydrogen coatings are expected to grow at 6.50% through 2031 as pressure-retaining structures adopt stricter hydrogen and toughness criteria, reinforcing the welding electrodes market size expansion in high-specification projects. Regulatory emphasis and project specifications are narrowing acceptable options for certain work scopes, particularly where documentation of moisture control and hydrogen testing is required. Cellulosic coatings retain influence in pipeline root passes for deep penetration and speed, yet orbital GMAW solutions have begun to displace some legacy SMAW procedures. Iron-oxide and metal-powder coatings serve rapid deposition use cases but face competitive price pressure that shifts margin concentration toward engineered low-hydrogen lines. Companies with packaging that improves moisture resistance are well-positioned as contractors adapt to humid regions and longer site logistics.

As qualification regimes tighten, the welding electrodes industry is seeing stronger demand for documented procedures and batch traceability. This is changing purchase criteria from simple price-per-kilogram comparisons to total risk reduction, including rework avoidance and inspection acceptance rates. The result is a two-speed market where commoditized rutile volume coexists with premium low-hydrogen solutions that command higher margins. Training and field discipline around storage and handling also raise the value of vendor support and packaging innovations that maintain electrode condition after opening. The interplay of quality enforcement and field realities is therefore critical in coating-type choices across contractors and geographies.

By Material: Mild-Steel Dominates Volume, Nickel Alloys Command Premium Growth

Mild-steel electrodes represented 45.12% of revenue in 2025, supported by widespread use across structural steel, line pipe, and general fabrication. Nickel and specialty alloy electrodes are projected to grow at 7.10% by 2031, and this growth contributes to the welding electrodes market size tied to LNG tanks and high-temperature petrochemical vessels. Progress in code approvals, such as ASME Code Case 3111 for VDM Alloy 699 XA, shows how performance in corrosive and hot environments is expanding the qualified alloy base. Stainless steel electrodes remain a mainstay for sanitary and corrosive environments, while cast-iron products focus on repair and transition joints with brittle substrates. Aluminum stick electrodes are mainly for field emergencies when TIG stations are unavailable due to known porosity and inclusion risks. Suppliers with R&D and testing labs are better placed to qualify new alloy formulations that match evolving base metal requirements in energy and process industries.[4]VDM Metals, “New ASME Code Case for VDM Alloy 699 XA Released,” VDM Metals, vdm-metals.com

As LNG-related cryogenic infrastructure advances, demand for nickel-containing consumables grows in parallel with tank and cold box fabrication. Product launches targeting 9% Ni steels illustrate how alloyed filler metals and documented notch toughness are becoming mainstream in project specifications. These materials require careful heat input control and hydrogen management, which increases the value of technical support and procedure development supplied by integrated incumbents. The welding electrodes market increasingly rewards suppliers that can bridge metallurgy, process optimization, and certification. This ecosystem capability helps contractors reduce qualification time and accelerate production starts without compromising inspection outcomes.

Geography Analysis

Asia-Pacific accounted for 45.14% of global revenue in 2025, led by China’s 62% share of global shipbuilding orders and South Korea’s specialized LNG carrier and offshore orders. The region’s defense buildout, including new carrier and combatant classes in China, layers incremental demand beyond commercial cycles and keeps low-hydrogen and nickel-alloy electrodes in regular use. Momentum from 2019-2025 has moderated as Chinese real estate curbs reduce new high-rise starts, though rail electrification and India’s infrastructure pipeline sustain structural steel and pipeline welding activity. Southeast Asia adds capacity in shipbuilding and offshore modules, but outcomes depend on distributor networks and the consistency of moisture-control practices that reduce rework. Asia-Pacific remains the center of gravity for the welding electrodes market due to the combination of commercial yards, energy infrastructure, and defense platforms.

The Middle East and Africa are forecast to grow at 7.90% through 2031, making it the fastest-expanding region as pipeline and LNG export infrastructure scale up to meet diversified import demand in Europe and Asia. Projects like Qatar’s North Field East and additional crude and gas pipelines underpin specifications that mix cellulosic electrodes for root passes with low-hydrogen fill and cap welds under ASME codes. LNG terminals and floating units in countries like Nigeria and Egypt increase the volume and complexity of pressure-retaining welds, which elevates the role of certified low-hydrogen products. Mining maintenance demand in South Africa supports hard-facing and gouging electrodes, even as power shortages create near-term headwinds. These dynamics strengthen the case for specialized consumables and project-level welding procedure documentation in the welding electrodes market.

North America and Europe held smaller shares in 2025 but continue to invest in rail, pipeline looping, and offshore wind that sustain multi-year demand profiles. North American programs include BNSF’s network maintenance plan and Enbridge’s pipeline expansion, while Europe’s offshore wind value chain is adding tower capacity in Poland for upcoming Baltic projects. Suppliers are reallocating commercial focus from subdued European industrial cycles to growth corridors in China, the Middle East, and Africa while maintaining technical and service coverage in mature markets. Defense production and onshoring initiatives in the United States also support stable orders for armor-grade electrodes with documented batch control. The welding electrodes market, therefore, reflects a portfolio of steady infrastructure work in the West alongside high-growth energy infrastructure in the Middle East and Africa.

Competitive Landscape

The market remains moderately fragmented, with vertical integration in metallurgy, flux manufacturing, and wire drawing giving large incumbents an advantage in premium formulations. One strategic path is ecosystem consolidation, where equipment and consumables are bundled to harmonize processes and lock in workflow standards. ESAB’s acquisition of Germany’s EWM broadened access to pulsed multiprocessor equipment and complements a consumables portfolio that supports integrated solutions beyond electrode pricing alone. This approach aims to convert equipment placements into recurring consumables revenue with standardized procedures and quality data integration. It also shifts competition away from price-only dynamics to certified performance and productivity outcomes in the welding electrodes market.

Another path is geographic arbitrage, where capacity in lower-cost locations supports exports while limiting exposure to duties and trade actions. Incumbents with established distribution and qualification support can flex inventory and local service into faster-growing regions like China, the Middle East, and parts of Africa. Packaging advances that mitigate moisture risk, and digital traceability tools linked to batch records, provide value beyond the consumable itself. Partnerships that expand channel reach, such as collaborations to distribute advanced welding systems in North America, also influence the mix between wire-fed processes and stick electrodes. This interplay underscores how product and channel strategies shape share retention in both commodity and premium lines of the welding electrodes market.

Process innovation continues to redefine productivity for thick sections and constrained welds. Methods like vertical electroslag for very thick plates reduce labor hours and interpass cleaning, which shifts the performance frontier toward suppliers with proprietary process IP. Packaging solutions such as vacuum-sealed sticks target field reliability in humid environments, while nickel-alloy consumables qualified for cryogenic service serve LNG tank builders. The welding electrodes market is therefore bifurcating into price-pressured commodity grades and engineered alloys with higher margins, with certification and support capabilities acting as entry barriers. Suppliers that align R&D, packaging, and digital traceability with critical project needs are best placed to defend and grow share.

Welding Electrodes Industry Leaders

Lincoln Electric Holdings, Inc.

ESAB Corporation

voestalpine Böhler Welding

Air Liquide Welding (Oerlikon)

Tianjin Golden Bridge Welding Materials Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: HD Hyundai, HD Korea Shipbuilding & Offshore Engineering, HD Hyundai Robotics, and U.S.-based Persona AI signed a joint development agreement to advance humanoid welding robots for shipyards, building on a May 2025 partnership that produced a successful prototype; the shipyard-specific humanoid aims to perform complex welding tasks autonomously with AI-based control systems, targeting field testing in 2027 to enhance worker safety and production efficiency in Korea's smart shipyards.

- March 2026: Siemens Gamesa ordered wind turbine towers for Poland's Baltica 2 offshore wind project from Baltic Towers, a Gdańsk-based manufacturer established via a EUR 200 million (USD 235.26 million) joint venture between Spain's GRI Renewable Industries and the Polish Industrial Development Agency; the project will feature 107 Siemens Gamesa 14 MW-222 turbines totaling 1.5 gigawatts of capacity, with commissioning expected in 2027, creating sustained demand for welding electrodes in tower section fabrication.

- March 2026: Windar Renovables leased 29,000 square meters of industrial space plus 41,000 square meters of outdoor storage at CTPark Legnica in Poland to construct its second onshore wind turbine tower manufacturing facility, targeting production start in Q4 2026 with annual capacity for 200 towers generating over 1,000 megawatts of clean energy and creating up to 300 new jobs; the facility will serve Polish and German markets with tower sections up to 40 meters long, 80 tons weight, and 6.5 meters diameter, driving electrode consumption in thick-section structural welding.

Global Welding Electrodes Market Report Scope

The Welding Electrodes Market Report is Segmented by Electrode Type (Stick Electrodes (SMAW/Manual Arc Electrodes), Bare Electrodes, and More), by Coating Type (Rutile, Basic/Low-Hydrogen, and More), by Material (Mild-Steel, Stainless-Steel, and More), by End-User Industry (Automotive, Construction, and More), and by Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD Billion).

| Stick Electrodes (SMAW/Manual Arc Electrodes) |

| Coiled Wires (including MIG/MAG and TIG electrodes) |

| Bare Electrodes |

| Flux-cored Wires (FCAW) |

| Metal-cored Electrodes |

| Gouging & Hardfacing Electrodes |

| Others (Light Coated, Non-consumable Electrodes) |

| Rutile |

| Basic / Low-Hydrogen |

| Cellulose |

| Iron-Oxide |

| Metal-Powder |

| Others (Acid-Coated, Special Coating, etc.) |

| Mild-Steel |

| Stainless-Steel |

| Cast-Iron |

| Aluminum & Alloys |

| Nickel & Specialty Alloys |

| Automotive |

| Aerospace and Defense |

| Construction |

| Shipbuilding |

| Energy and Power |

| Electronics |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Peru | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Turkey | |

| Egypt | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Electrode Type | Stick Electrodes (SMAW/Manual Arc Electrodes) | |

| Coiled Wires (including MIG/MAG and TIG electrodes) | ||

| Bare Electrodes | ||

| Flux-cored Wires (FCAW) | ||

| Metal-cored Electrodes | ||

| Gouging & Hardfacing Electrodes | ||

| Others (Light Coated, Non-consumable Electrodes) | ||

| By Coating Type | Rutile | |

| Basic / Low-Hydrogen | ||

| Cellulose | ||

| Iron-Oxide | ||

| Metal-Powder | ||

| Others (Acid-Coated, Special Coating, etc.) | ||

| By Material | Mild-Steel | |

| Stainless-Steel | ||

| Cast-Iron | ||

| Aluminum & Alloys | ||

| Nickel & Specialty Alloys | ||

| By End-User Industry | Automotive | |

| Aerospace and Defense | ||

| Construction | ||

| Shipbuilding | ||

| Energy and Power | ||

| Electronics | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Peru | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Kuwait | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the welding electrodes market to 2031?

The welding electrodes market size was USD 5.67 billion in 2025 and is projected to reach USD 7.98 billion by 2031 at a 5.89% CAGR over 2026-2031.

Which regions lead, and which are growing fastest in welding electrodes?

Asia-Pacific led with 45.14% share in 2025, while the Middle East and Africa are expected to post the fastest growth at 7.90% through 2031.

Which electrode types and coatings are most important right now?

Stick electrodes led with 41.61% share in 2025, and rutile coatings held 43.62%, while basic or low-hydrogen variants are the fastest-growing within their categories.

Which end-use sectors are most supportive of demand resilience?

Construction held 29.32% of demand in 2025, and aerospace and defense are projected to grow at 7.60%, supporting premium, traceable consumables.

How is automation changing the demand for stick electrodes?

Semi-automatic and robotic welding are reducing routine SMAW use, but manual stick remains essential for precision repair, constrained spaces, and critical field work.

What certifications or standards matter most for critical electrode applications?

ASME Section IX, AWS D1.1, and ISO 9606 are central for qualification and inspection, with additional material-specific code cases in advanced alloy applications.

Page last updated on: