Water-Based And Low-Migration Inks For Food Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

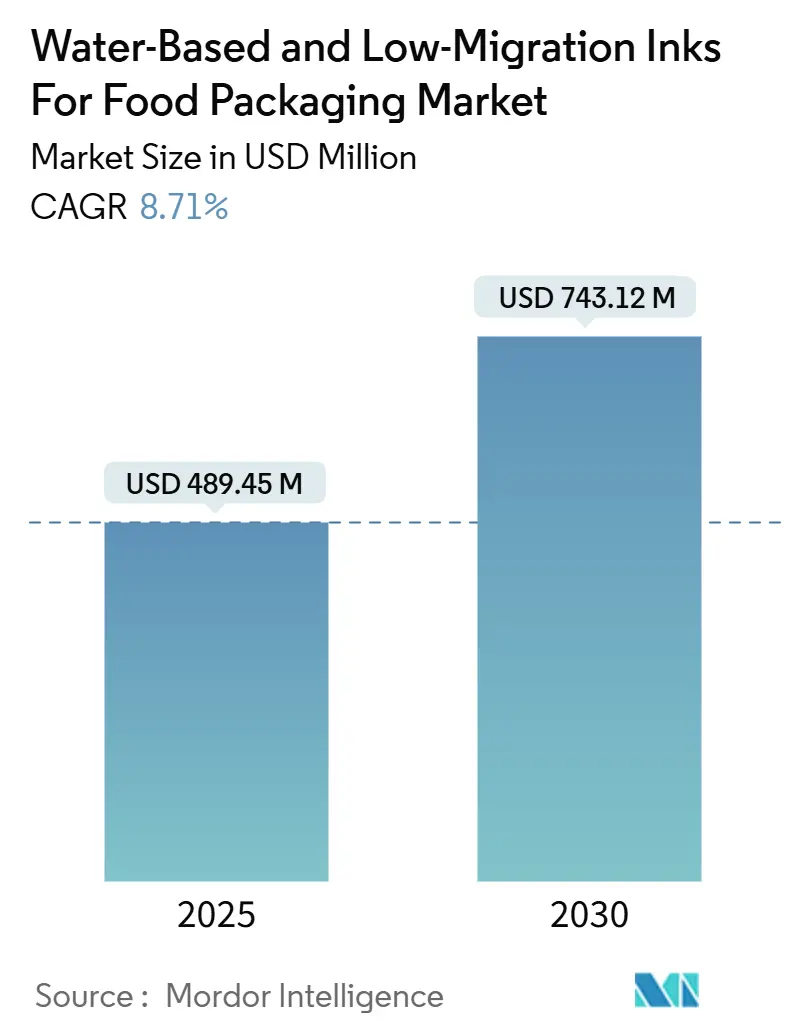

| Market Size (2025) | USD 489.45 Million |

| Market Size (2030) | USD 743.12 Million |

| Growth Rate (2025 - 2030) | 8.71% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Water-Based And Low-Migration Inks For Food Packaging Market Analysis by Mordor Intelligence

The water-based and low-migration inks for food packaging market size is estimated at USD 489.45 million in 2025, and is expected to reach USD 743.12 million by 2030, at a CAGR of 8.71% during the forecast period (2025-2030). Sustained momentum stems from the European MOSH/MOAH regulatory clampdown, rising brand-owner commitments to solvent-free graphics, and recent advances that solve historical adhesion limits on high-barrier substrates. Converter preference continues to favor systems that achieve direct food-contact compliance without sacrificing line speed, giving early adopters a pricing edge with premium food brands. Asia-Pacific’s rapid capacity build-out and Europe’s policy leadership are combining to shift technical standards worldwide, while corporate Scope-3 decarbonization targets cement demand for renewable binder systems that lower cradle-to-gate emissions. Concurrently, LED-UV retrofits and digital workflows shorten run lengths, accelerate artwork changes, and expand addressable spaces for water-based chemistries, further propelling the water-based and low-migration inks market.

Key Report Takeaways

- By ink type, bio-based polyurethane grades are projected to rise at a 10.29% CAGR between 2025-2030.

- By printing process, flexographic printing accounted for 51.29% of the water-based and low-migration inks for food packaging market share in 2024.

- By substrate, the water-based and low-migration inks for food packaging market size for the compostable PLA films segment is projected to increase at a 11.28% CAGR between 2025-2030.

- By end-use food industry, bakery and confectionery captured 27.02% of the water-based and low-migration inks for food packaging market share in 2024.

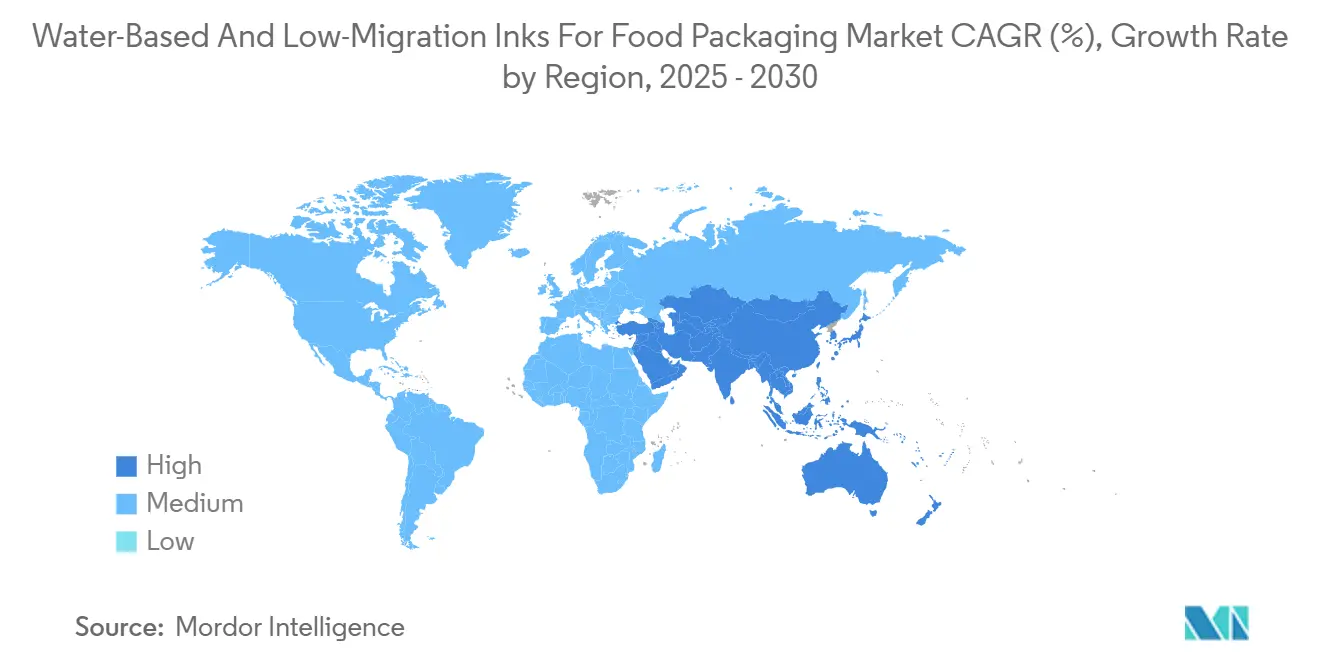

- By geography, the water-based and low-migration inks for food packaging market size for the Asia-Pacific segment is forecast to expand at a 10.19% CAGR through 2030.

Global Water-Based And Low-Migration Inks For Food Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in brand-owner pledges for solvent-free printing | +2.1% | Global, early adoption in North America and Europe | Medium term (2-4 years) |

| EU MOSH/MOAH crackdown accelerating low-migration adoption | +2.8% | Europe core, spill-over to North America and Asia-Pacific | Short term (≤2 years) |

| Brand shift to mono-material recyclables demanding water-based inks | +1.9% | Europe and North America, expanding to Asia-Pacific | Long term (≥4 years) |

| Retailer private-label mandates on VOC thresholds | +1.2% | Global, stricter enforcement in Europe | Medium term (2-4 years) |

| Rapid LED-UV retrofits boosting hybrid water-based lines | +1.4% | Global, manufacturing concentration in Asia-Pacific | Short term (≤2 years) |

| Corporate Scope-3 decarbonization targets | +0.8% | Global, multinational brand leadership | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Surge in Brand-Owner Pledges for Solvent-Free Printing

Major food companies now embed solvent-free requirements in supplier contracts, linking compliance to corporate sustainability metrics and investor disclosure frameworks. This structural shift raises switching costs once converters certify water-based chemistries, producing stable revenue streams and favoring early movers who can validate cradle-to-gate carbon savings.

EU MOSH/MOAH Crackdown Accelerating Low-Migration Adoption

France banned mineral-oil aromatic hydrocarbons in printing inks effective January 2025, imposing 0.1% content limits, while Germany’s voluntary roadmap phases out mineral-oil news inks by 2028. The regulatory urgency anchors Europe as the reference market for low-migration performance and sparks copy-cat policy drafts in Indonesia, Canada, and Mexico.[1]De Clercq, “Information Note on French Order on Mineral Oils in Printing Inks,” EuPIA, eupia.org

Brand Shift to Mono-Material Recyclables Demanding Water-Based Inks

The EU Packaging and Packaging Waste Regulation grades recyclability and modulates producer fees, rewarding packaging that de-inks easily during flotation and reenters fiber loops at high yield. Water-based inks meet these criteria, delivering economics that offset the modest price premium of food-grade resins and compelling adoption in private-label programs.[2]Publications Office of the European Union, “Regulation (EU) 2025/40 on Packaging and Packaging Waste,” eur-lex.europa.eu

Rapid LED-UV Retrofits Boosting Hybrid Water-Based Lines

LED-UV lamps cure at lower temperatures, enabling hybrid emulsions that combine water-based binders with energy-curable oligomers. Production speeds up to 300 m/min are now documented while still satisfying 10 ppb migration thresholds, solving the long-standing trade-off between throughput and compliance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Poor adhesion on high-barrier films without plasma treatment | -1.8% | Global, acute in Asia-Pacific flexible packaging | Short term (≤2 years) |

| Cost premium of food-grade resin systems | -1.3% | Global, price sensitivity highest in emerging markets | Medium term (2-4 years) |

| Supply risk for bio-based binders | -0.9% | Global, supply concentration in Northern Europe and North America | Long term (≥4 years) |

| Anilox wear and cleaning downtime on changeovers | -0.7% | Global, operational impact highest in high-mix plants | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Poor Adhesion on High-Barrier Films Without Plasma Treatment

Metallized PET or SiOx-coated substrates exhibit low surface energy, forcing converters to invest in plasma units that lift per-line capital outlays by 12-18%. Adhesion failure risk deters smaller players from entering premium meat or retort pouch niches despite growing customer demand.

Cost Premium of Food-Grade Resin Systems

Food-contact polyurethanes cost 15-25% more than commodity acrylics, and bio-based grades widen that delta to 30-35%, eroding margins for converters operating in markets where solvent-based products still evade enforcement.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ink Type: Bio-Based Binders Accelerate Premium Uptake

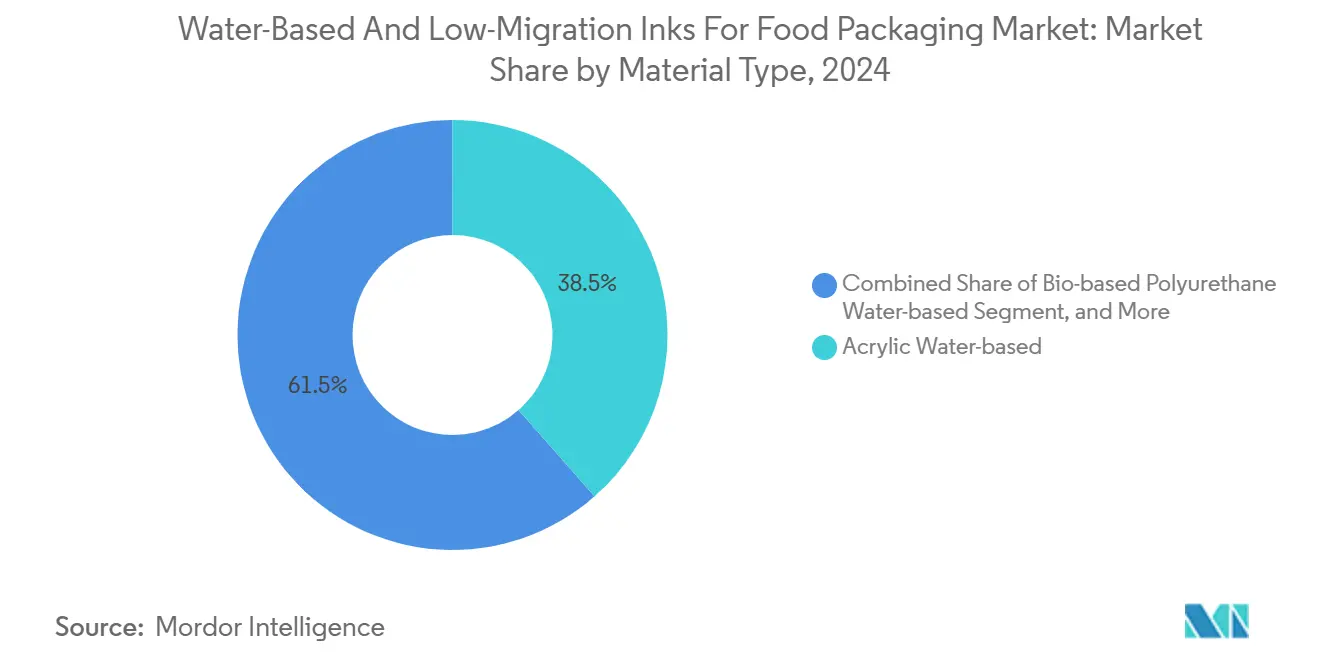

Bio-based polyurethane grades are projected to rise at a 10.29% CAGR, outpacing the trajectory of conventional acrylics, which retained a 38.51% share in 2024. Early adopters highlight Scope 3 emission reductions of up to 35 kg CO₂-eq per tonne of printed packaging, offering tangible metrics for ESG reports. Maleic resins retain relevance in price-sensitive labels, while shellac blends address organic-certified confectionery where migration and allergen profiles demand natural inputs.

Hybrid LED-curable emulsions, although niche today, are experiencing the fastest numerical growth, supported by grant-funded pilots in Germany and Japan. Over the forecast horizon, the water-based and low-migration inks market size for hybrid chemistries is projected to expand at a low double-digit pace, limited only by challenges related to pigment dispersion stability.

By Printing Process: Digital Inkjet Presses Capture High-Mix Volumes

Digital inkjet volumes are growing at an 11.49% CAGR, aligned with e-commerce-driven SKU proliferation that requires short runs and real-time code customization. Xeikon’s toner platform withstands 260 °C oven cycles without auxiliary varnish, unlocking ready-meal trays and shelf-stable soups formerly dominated by gravure.[3]Grania Jain, “Xeikon and Sappi partner for resource-saving packaging,” Packaging Connections, packagingconnections.com

Flexography retains 51.29% market share due to plate efficiency on bread bags and snack liners, yet faces migration to hybrid LED flexo units that offer instant cure and reduced substrate waste. Gravure persists for >300 m/min pasta wrap lines but is declining in Western Europe as toluene restrictions tighten.

By Packaging Substrate: Compostable Films Challenge Conventional Mixes

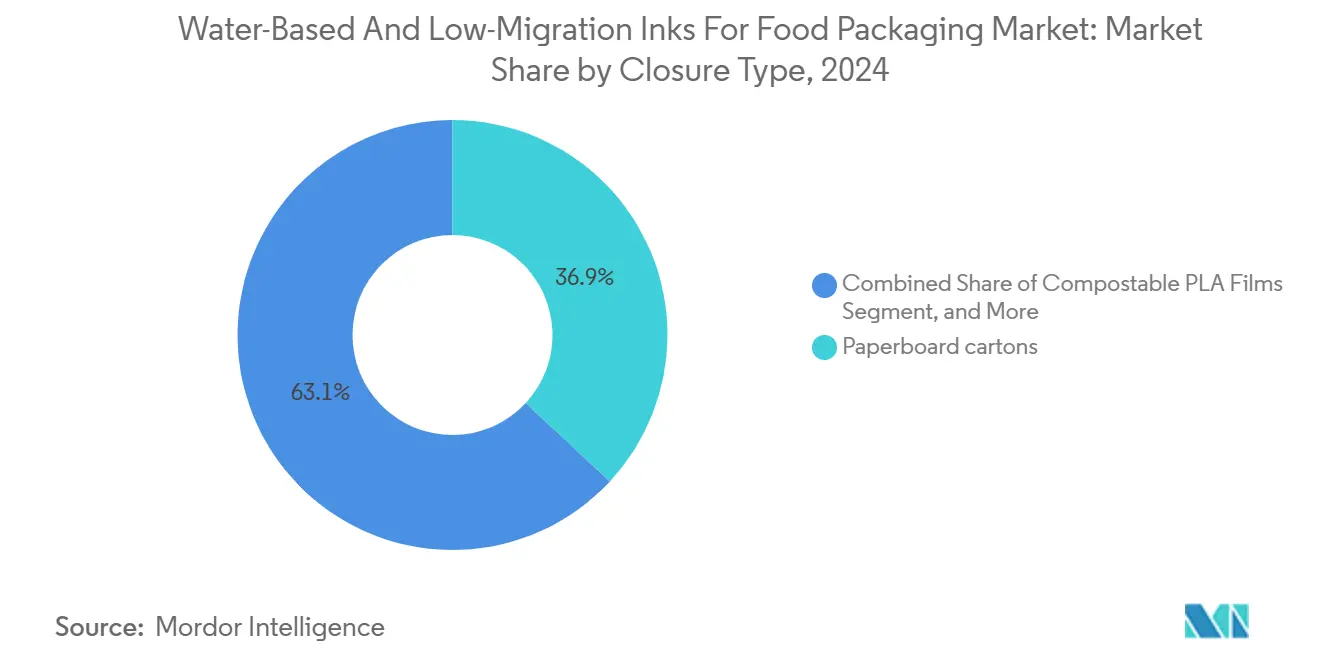

Paperboard cartons still hold 36.92% of global demand, buoyed by barrier-enhanced iterations that displace plastic sleeves for frozen bakery goods. Compostable PLA films grow at 11.28% CAGR, with chilled produce brands applying industrial composting logos that boost consumer uptake. High-barrier multilayers, essential for meat and seafood, remain constrained by adhesion limitations of aqueous inks, slowing their conversion despite regulatory pressure.

Flexible mono-material PE structures gain ground in cereal liners where recyclability fees are lowest under the EU’s eco-modulation schedule. Metal cans emerge as a nascent user of LED-curable water-based systems, aided by ongoing PFAS phase-outs in traditional epoxy coatings.

By End-Use Food Segment: Plant-Based Foods Drive Innovation

Bakery and confectionery kept a 27.02% revenue share in 2024 on the back of high graphics volume. Plant-based foods, however, deliver a 10.97% CAGR by linking vegan positioning with fully recyclable or compostable packs. Ready-to-eat meals benefit from the tailwinds of extended shelf-life retort pouches, prompting R&D into water-based adhesion promoters that are resistant to 121 °C sterilization.

Dairy firms adopt mono-material PP pots with in-mold labels printed in water-based inkjet, cutting delamination waste by 15%. The infant nutrition channel insists on migration limits one order of magnitude stricter than EU thresholds, stimulating demand for shellac-based solutions vetted through in vitro toxicology.

Geography Analysis

Europe accounts for 33.59% of 2024 revenue, propelled by the mineral-oil ban in France and Germany’s voluntary phase-out program. Siegwerk’s 2025 acquisition of Allinova enhances dispersion capabilities in Germany’s “chemical triangle,” shortening lead times for custom food-contact blends. In parallel, PFAS-free mandates effective as of August 2026 necessitate a technology refresh that favors water-based platforms.

Asia-Pacific, posting a 10.19% CAGR, benefits from DIC’s Indonesian plant for food-contact coatings and SAKATA INX’s USD 8.1 million Shanghai pilot line for aqueous dispersions. India’s first direct food-contact ink facility, opened by Hubergroup in June 2025, illustrates the knowledge transfer from Europe to emerging hubs. Indonesia’s draft food packaging law mirrors EU migration metrics, accelerating regional alignment.

North America leverages a robust bio-based raw material supply from corn and tall-oil streams, although currency-adjusted resin costs remain 12% higher than those in the Asia-Pacific region. The FDA’s bolstered post-market surveillance increases testing stringency, motivating mid-tier converters to modernize. South America, Middle East and Africa show early adoption in premium SKUs but overall penetration is tempered by resin cost premiums and limited recycling infrastructure.

Competitive Landscape

Market concentration stands moderate as the top five suppliers control roughly 55% of 2024 revenue. Siegwerk, Sun Chemical and Flint Group continue acquisition-driven expansion, with Siegwerk integrating Allinova’s dispersion technology to bolster low-migration credentials. Sun Chemical’s SunPak FSP EcoPace rollout delivers higher mileage on anilox rolls, trimming ink consumption by 8% and appealing to high-run bakery converters. Flint Group advances Flexocure Leap, a LED-curable flexo line that meets 10 ppb migration limits at 250 m/min press speeds.

Rising challengers target compostable packaging and digital inkjet niches. Epple Druckfarben launches shellac-rich inks for organic chocolate wrappers, while Nazdar Ink Technologies develops aqueous pigment dispersions compatible with Kyocera piezo heads. Competitive edge increasingly hinges on regulatory affairs depth, as converters rely on suppliers for toxicological dossiers and NIAS risk assessments. Overall, technology differentiation now centers on adhesion promoters, renewable content, and energy-curable hybrids that deliver competitive press productivity without compromising safety thresholds.

Water-Based And Low-Migration Inks For Food Packaging Industry Leaders

Sun Chemical (DIC Corporation)

Flint Group

Siegwerk Druckfarben AG & Co. KGaA

Sakata INX Corporation

Huber Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Borouge, Siegwerk and TPN Food Packaging unveiled a mono-material flexible pouch that eliminates adhesive layers, showing converter alignment with circular economy targets.

- September 2025: Mondi introduced a white water-based ink for digital corrugated printing, meeting e-commerce aesthetic demands while maintaining recyclability.

- August 2025: Siegwerk finalized the acquisition of Allinova, deepening its dispersion expertise for food-contact aqueous formulations.

- July 2025: Hubergroup Print Solutions released a water-based ink and varnish set certified for direct food contact.

Global Water-Based And Low-Migration Inks For Food Packaging Market Report Scope

| Acrylic Water-based |

| Maleic Resin Water-based |

| Bio-based Polyurethane Water-based |

| Shellac / Natural-based |

| Hybrid UV / Aqueous (LED-curable) |

| Latex Dispersion Water-based |

| Flexographic |

| Gravure |

| Digital Inkjet |

| Offset Lithography |

| Screen Printing |

| Hybrid LED Flexo |

| Paperboard Cartons |

| Corrugated and Linerboard |

| Flexible Plastic Films |

| High-barrier Multilayer Films |

| Rigid Plastic Containers |

| Metal Cans and Closures |

| Glass Jars and Bottles |

| Molded Fibre and Compostable Materials |

| Bakery and Confectionery |

| Dairy Products |

| Ready-to-eat Meals and Meal Kits |

| Meat, Poultry and Seafood |

| Fruits and Vegetables |

| Other End-user food Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Ink Type | Acrylic Water-based | ||

| Maleic Resin Water-based | |||

| Bio-based Polyurethane Water-based | |||

| Shellac / Natural-based | |||

| Hybrid UV / Aqueous (LED-curable) | |||

| Latex Dispersion Water-based | |||

| By Printing Process | Flexographic | ||

| Gravure | |||

| Digital Inkjet | |||

| Offset Lithography | |||

| Screen Printing | |||

| Hybrid LED Flexo | |||

| By Packaging Substrate | Paperboard Cartons | ||

| Corrugated and Linerboard | |||

| Flexible Plastic Films | |||

| High-barrier Multilayer Films | |||

| Rigid Plastic Containers | |||

| Metal Cans and Closures | |||

| Glass Jars and Bottles | |||

| Molded Fibre and Compostable Materials | |||

| By End-use Food Industry | Bakery and Confectionery | ||

| Dairy Products | |||

| Ready-to-eat Meals and Meal Kits | |||

| Meat, Poultry and Seafood | |||

| Fruits and Vegetables | |||

| Other End-user food Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What revenue will the water-based and low-migration inks market reach by 2030?

The market is projected to grow to USD 743.12 million by 2030, expanding at an 8.71% CAGR from its 2025 base.

Which printing process is growing fastest for food-contact aqueous inks?

Digital inkjet is rising at an 11.49% CAGR through 2030, fueled by demand for short runs and variable data.

Why is Europe the largest regional user of low-migration inks?

Europe leads due to strict MOSH/MOAH limits, France’s mineral-oil ban, and PFAS phase-outs that make water-based systems the default for compliance.

What impedes wider adoption on high-barrier films?

Water-based inks often require costly plasma treatment to achieve adhesion on metallized or SiOx-coated films, raising capex for converters.

How do brand-owner sustainability pledges influence ink selection?

Pledges to eliminate solvents align with Scope-3 emission cuts, pushing converters toward water-based chemistries that provide measurable carbon reductions.

Which ink chemistry is growing quickest?

Bio-based polyurethane formulations post a 10.29% CAGR as brands seek renewable content that meets food-contact safety norms.

Page last updated on: