Water-Based Barrier Paper Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

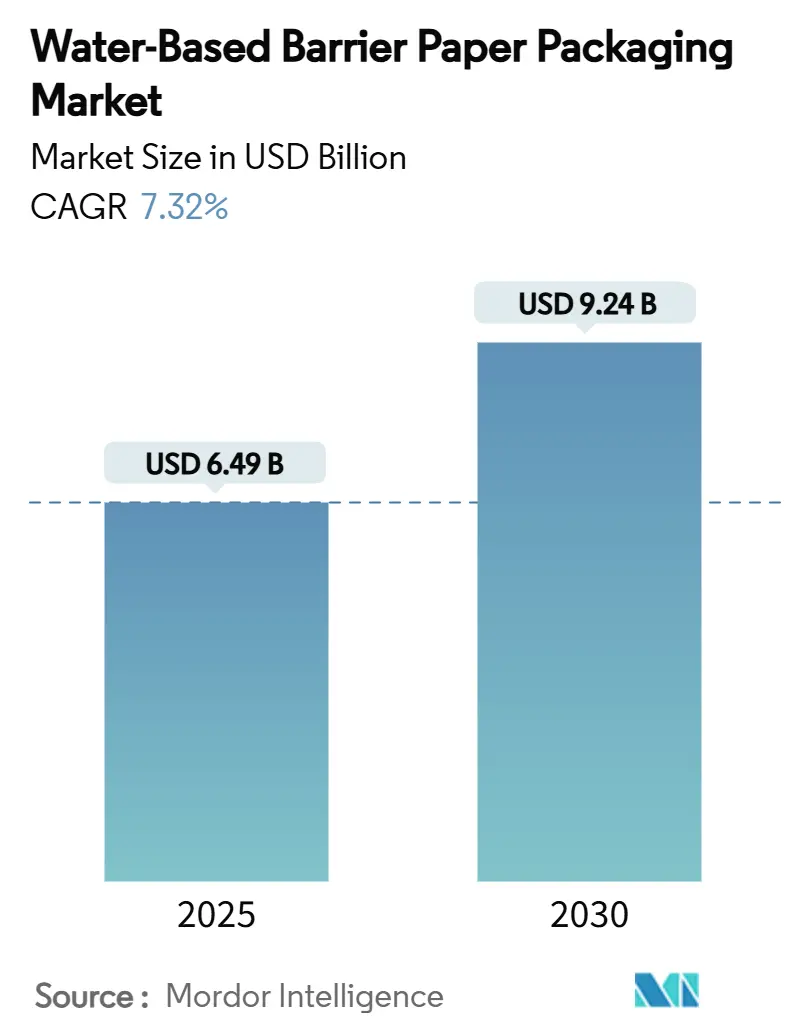

| Market Size (2025) | USD 6.49 Billion |

| Market Size (2030) | USD 9.24 Billion |

| Growth Rate (2025 - 2030) | 7.32% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

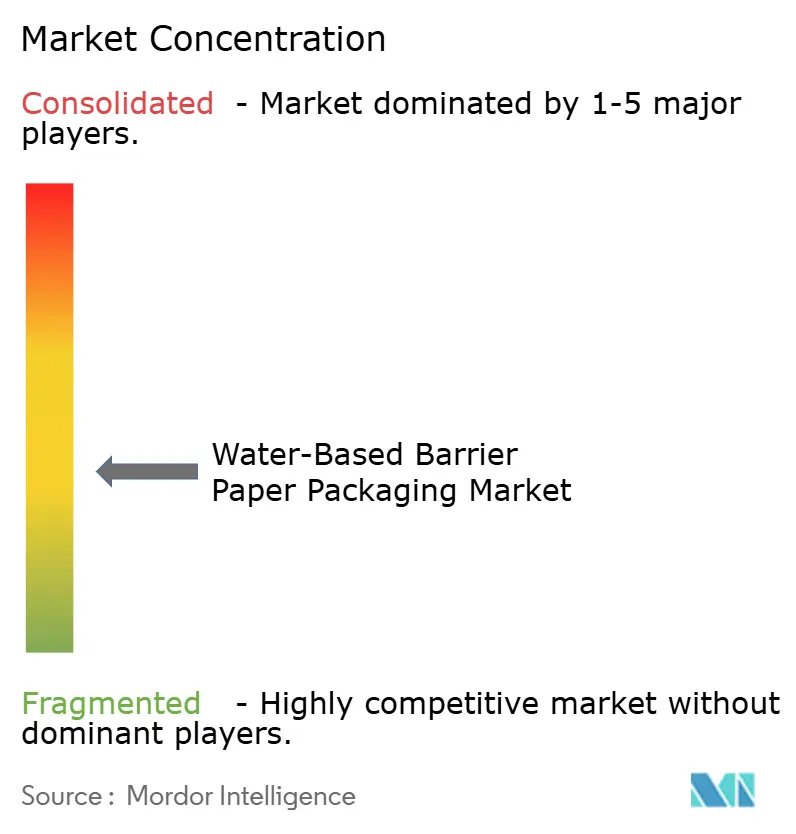

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Water-Based Barrier Paper Packaging Market Analysis by Mordor Intelligence

The water-based barrier paper packaging market size stands at USD 6.49 billion in 2025 and is forecast to reach USD 9.24 billion by 2030, advancing at a 7.32% CAGR over the period. This trajectory is underpinned by mounting plastic-ban legislation, rapid brand adoption of 2025 recyclability pledges, and fast-emerging high-speed dispersion-coating lines that collectively improve cost-performance parity with polyethylene board.[1]European Parliament, “Packaging and Packaging Waste,” europarl.europa.eu Large consumer packaged-goods companies are accelerating material changeovers to meet Extended Producer Responsibility fees and PFAS phase-outs, while e-commerce operators demand curbside-recyclable mailers compatible with automated fulfillment. Market expansion is especially pronounced in Asia-Pacific, where China’s mandatory express-packaging standard GB 43352-2023 imposes heavy-metal limits that push converters toward water-based alternatives. European investments in low-carbon capacity, such as BASF’s new dispersion line and Stora Enso’s Oulu board machine, are boosting regional supply resilience. However, unit-cost gaps versus PE board, specialty-resin bottlenecks, and regulatory ambiguity over novel bio-coatings still temper near-term adoption in price-sensitive food segments.

Key Report Takeaways

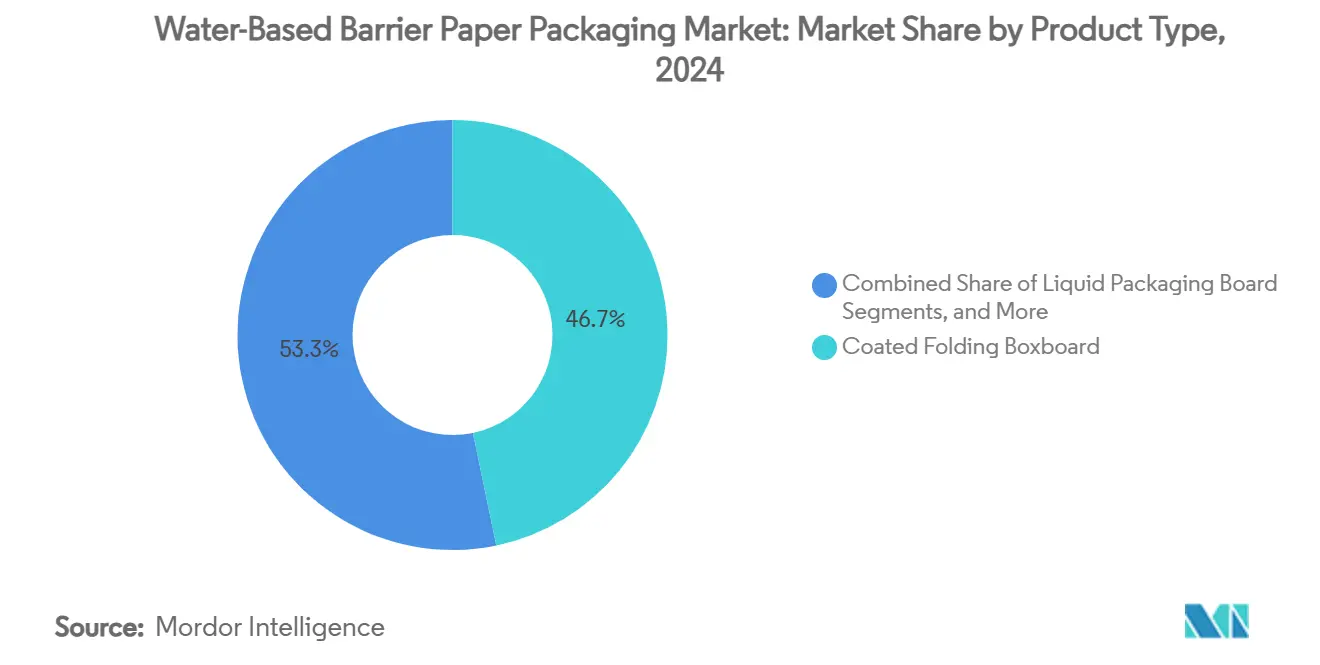

- By product type, coated folding boxboard captured 46.73% of the water-based barrier paper packaging market share in 2024.

- By end-user industry, the water-based barrier paper packaging market size for the healthcare and pharma segment is projected to grow at a 9.82% CAGR between 2025-2030.

- By Geography, Asia-Pacific captured a 35.29% of the water-based barrier paper packaging market share in 2024.

Global Water-Based Barrier Paper Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Plastic-ban legislation momentum | +1.8% | Global, early adoption in EU, North America, APAC | Medium term (2-4 years) |

| Brand 2025 recyclability pledges | +1.2% | Global, concentrated in North America and EU | Short term (≤ 2 years) |

| Advances in dispersion-coating lines | +0.9% | Global, led by Europe and North America | Long term (≥ 4 years) |

| Surge in food-service sustainability demand | +1.1% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Automated e-commerce pack formats | +0.7% | APAC core, spill-over to North America | Medium term (2-4 years) |

| Nordic low-carbon CAPEX incentives | +0.4% | Nordic countries, expanding to broader EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Plastic-ban Legislation Momentum

Governments on three continents have moved from voluntary guidelines to enforceable bans, compelling producers to replace plastic-lined substrates with recyclable fiber-based formats that comply with 2030 recyclability mandates. Australia’s reform package, California’s Extended Producer Responsibility law and New South Wales’ food-packaging ban have tightened timelines, while China’s GB 43352-2023 creates immediate express-sector compliance targets. These synchronized policies are triggering retrofit projects on coating lines, driving new orders for dispersion systems and elevating demand for water-based barrier paper packaging market solutions. Converters unable to prove recyclability now face fee escalations that erode the historical cost advantage of PE board. As a result, procurement teams increasingly treat fiber alternatives as the default specification rather than a niche premium.

Brand 2025 Recyclability Pledges

Publicly tracked ESG scorecards have pushed CPG multinationals to guarantee that their entire packaging portfolios will be recyclable or reusable by 2025, compressing material-switch timelines to less than one major planning cycle.[2]Amcor, “Amcor Sustainability Report,” amcor.com Amcor, WestRock, and the 4evergreen alliance report recyclability levels above 94% for core lines, yet they still depend on scaling water-based barrier technologies to close the final compliance gaps. Investor pressure links executive compensation to near-term milestones, so procurement teams tolerate modest cost premiums for proven solutions. Demand visibility is high; suppliers with validated dispersion coatings are locking in multiyear offtake contracts, accelerating volume ramps, and narrowing cost spreads. The corporate pledge cascade, therefore, magnifies baseline regulatory demand, adding roughly 1.2 percentage points to forecast CAGR for the water-based barrier paper packaging market.

Advances in Dispersion-coating Lines

Second-generation aqueous dispersions such as BASF’s Joncryl and Acronal Pro families now match PE substrates in moisture, oxygen and mineral-oil barrier performance at coating weights 15% lower than 2023 incumbents. Precision metering heads, inline IR drying and closed-loop viscosity control raise line speeds above 800 m/min, reducing variable costs per m². UPM’s co-creation projects demonstrate sealability on conventional FFS machines and validated performance for coffee and confectionery wrappers. Nanocellulose additives further enhance grease resistance, expanding the candidate set for fatty snacking applications. These breakthroughs extend the addressable universe of the water-based barrier paper packaging market, particularly in segments once deemed technologically out of reach, and they cut the price-gap headwind identified under the key restraint.

Surge in Food-service Sustainability Demand

Quick-service restaurants, stadium caterers and meal-delivery firms have become early adopters because packaging visibility directly influences customer perceptions of sustainability. NISSIN FOODS’ ECO Cup changeover and Sonoco’s EnviroFlex Paper illustrate how operators integrate barrier paper into flagship SKUs to reinforce brand environmental credentials. Municipal bans on coated take-out containers in California and EU PFAS restrictions escalate compliance urgency. Food-service volume growth creates scale economies that lower coating-resin unit costs, indirectly benefiting adjacent retail categories. Consequently, food-service adoption adds tangible momentum to the water-based barrier paper packaging market, particularly in North America and Europe where quick-service chains drive high turnover.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher unit cost vs PE board | -1.4% | Global, most pronounced in price-sensitive markets | Short term (≤ 2 years) |

| Sub-optimal barrier for fatty foods | -0.8% | Global, concentrated in food packaging applications | Medium term (2-4 years) |

| Specialty resin feedstock bottlenecks | -0.6% | Global, supply concentrated in North America and Europe | Medium term (2-4 years) |

| Regulatory uncertainty over novel bio-coatings | -0.5% | Global, most acute in North America and EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Higher Unit Cost vs PE Board

Water-based dispersion substrates are still price at 15-25% above PE-lined board, reflecting smaller production runs, capex amortization on new coaters, and specialty-resin premiums. This gap is most painful in commodity food categories where margins are thin. However, Extended Producer Responsibility fees and plastic taxes raise the fully-loaded cost of legacy packaging, narrowing the differential each fiscal year. Chemical producers are scaling bio-based dispersions, and KPMG forecasts capacity additions that should soften resin pricing by late 2026. Converters, therefore, view the cost challenge as transitory, but it remains the single largest negative drag on the water-based barrier paper packaging market CAGR through 2027.

Sub-optimal Barrier for Fatty Foods

Grease penetration compromises shelf life for high-fat products such as bakery items and ready-to-eat meals. Traditional fluorochemical solutions are exiting the market as the FDA nullifies 35 PFAS food-contact notifications by June 2025. Paper converters must reinvent coatings that balance lipophobicity with recyclability. Amcor’s AmFiber Performance Paper and nanocellulose-enhanced layers show progress, yet most offerings require thicker coats that raise grammage and cost. Until food manufacturers validate next-gen chemistries at commercial scale, uptake in this sub-segment will lag, shaving 0.8 percentage points off the global water-based barrier paper packaging market CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Flexible Formats Power Growth

Coated folding boxboard generated 46.73% of 2024 revenue, confirming its entrenched role in branded retail displays where printability and stiffness are vital.[3]UPM, “UPM Annual Report 2024,” upm.com The segment benefited from established coating assets and brand familiarity, yet its growth rate trails the overall water-based barrier paper packaging market because performance thresholds were already adequate for moderate-barrier use cases. Liquid packaging board maintains steady demand from dairy and juice cartons as resin supply constraints gradually relax, while cupstock gains incremental share from quick-service chains shifting away from PE-lined cups.

Flexible barrier paper is the clear innovation engine, recording an 11.43% CAGR through 2030 on the back of automated e-commerce mailers and high-barrier snack formats. Its lightweight profile lowers postage costs, and dispersion-treated kraft withstands automated pick-and-place without tearing. Asia-Pacific fulfillment centers lead adoption, yet European converters are fast-tracking installs to capture the Extended Producer Responsibility fee relief. Performance advances in moisture vapor transmission rate and grease resistance have allowed flexible grades to encroach on polymer film territory, expanding the total addressable water-based barrier paper packaging market size for high-growth SKUs.

By End-user Industry: Pharma Becomes a Catalyst

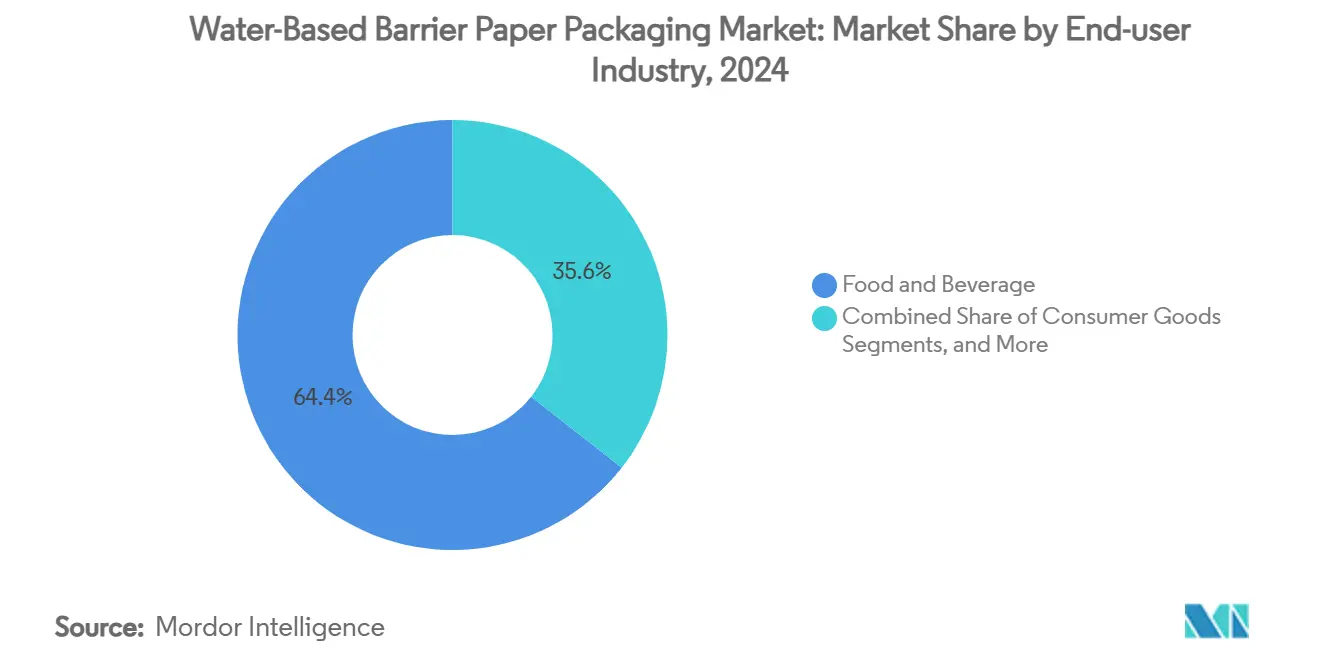

Food and beverage commanded 64.42% of 2024 demand thanks to regulatory PFAS bans, quick-service container swaps and supermarket chains’ private-label sustainability targets. Brands exploit the recyclability narrative to differentiate on-shelf, driving cartonboard retrofits and flexible flow-wrap pilots. Petrochemical cost volatility further motivates substitution toward fiber formats with more predictable pricing trajectories.

Healthcare and pharma, though smaller in absolute terms, is tracking a 9.82% CAGR, the fastest within the water-based barrier paper packaging market. EU exemptions acknowledge sterility requirements yet still incentivize recyclable solutions, prompting pharmaceutical companies to fund barrier-paper trials for blister overwraps and unit-dose sachets. Compliance with medical-device sterilization protocols requires ultra-low extractables, an area where advanced dispersions now meet ISO 11607 norms. Success in this segment signals technical maturity and unlocks premium pricing that can subsidize broader cost reductions across mass-market categories.

Geography Analysis

Asia-Pacific delivered 35.29% of global revenue in 2024 and is projected to advance at a 10.61% CAGR through 2030, the steepest regional climb in the water-based barrier paper packaging market. China’s GB 43352-2023 expresses clear heavy-metal thresholds that disqualify many PE laminates, and domestic parcel volume exceeds 100 billion units annually, creating unrivaled scale for dispersion-coated kraft mailers. Japan’s corporate reporting reforms embed climate metrics into annual reports, causing brands to evaluate packaging footprint as a financial disclosure variable. South-East Asian converters follow suit, lured by supply-chain onshoring and surging regional e-commerce.

Europe ranks second by value owing to the Packaging and Packaging Waste Regulation that mandates recyclability by 2030 and restricts PFAS content from August 2026. Nordic clean-tech incentives mitigate capex hurdles, exemplified by Norway’s NOK 60 billion green-industry roadmap and Finland’s heavy investment in Stora Enso’s 750,000-tonne Oulu board line. Western European quick-service chains, pressed by municipal plastic bans, accelerate fiber conversion, while pharmaceutical clusters in Germany and Switzerland pilot high-barrier medical wraps.

North America combines federal recycling targets with a patchwork of state-level EPR laws, most notably California’s statute that obliges all packaging to be recyclable or compostable by 2032. Corporate pledges translate into USD 100 million annual R&D budgets at players like Amcor, and International Paper’s Pennsylvania corrugated investment expands local supply of dispersion-ready substrates. Rising landfill-gate fees and consumer activism around PFAS propel grocery retailers to list recyclable criteria in supplier scorecards, lifting adoption rates despite inflationary headwinds.

Competitive Landscape

Industry leadership rests with Smurfit Westrock, Mondi Group and International Paper, whose combined presence controls roughly 35% of the water-based barrier paper packaging market share. Their vertical integration spans timber, pulp, converting and recycling, enabling cost optimization and fast scale-up of new dispersion recipes. Consolidation momentum is high: the USD 34 billion Smurfit Kappa-WestRock merger realized USD 400 million in projected synergies by the end of 2024, while International Paper closed the USD 9.9 billion DS Smith acquisition after agreeing to divest five European plants to satisfy regulators.

Technology differentiation now outweighs sheer tonnage as converters demand coatings that survive form-fill-seal speeds, freezer cycles and grease loads. UPM collaborates directly with brand owners on co-creation pilots, pairing chemists with pack-line engineers to tune seal windows and coefficient of friction parameters. BASF’s Heerenveen expansion secures upstream resin supply for partners, lowering risk around specialty-polymer shortages. These advances raise switching costs for brand owners, locking in multi-year contracts that stabilize order books.

Disruptors focus on nanocellulose, chitosan and algae-derived binders that claim end-of-life compostability and tailored barrier functions. Venture-funded start-ups leverage empty pulp mill capacity in Scandinavia, using Nordic green-CAPEX subsidies to prototype micro-coating units that retrofit onto legacy machines. OEMs, in turn, integrate AI-powered process control to guarantee uniform coat-weights, reducing resin waste and enabling competitive pricing. As patent portfolios expand, the competitive frontier shifts toward Intellectual Property, testing the negotiating leverage of incumbents versus agile niche specialists.

Water-Based Barrier Paper Packaging Industry Leaders

Mondi Group

Nippon Paper Group

Metsä Board

Smurfit Westrock PLC

Amcor PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Stora Enso began operating a EUR 1 billion consumer board line in Oulu, Finland, adding 750,000 tonnes of folding boxboard and coated unbleached kraft capacity.

- February 2025: The European Commission cleared International Paper’s USD 9.9 billion acquisition of DS Smith, conditioned on divesting five plants in Portugal, Spain and France.

- February 2025: Smurfit Westrock reported USD 7.5 billion Q4 2024 sales and highlighted USD 400 million synergy capture from its mega-merger.

- January 2025: California appointed the Circular Action Alliance as the state’s first Producer Responsibility Organization to implement its plastics packaging law.

Global Water-Based Barrier Paper Packaging Market Report Scope

| Coated Folding Boxboard |

| Liquid Packaging Board |

| Cupstock and Food-service Board |

| Flexible Barrier Paper |

| Food and Beverage |

| Consumer Goods |

| Healthcare and Pharma |

| Industrial and Electronics |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Malaysia | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Product Type | Coated Folding Boxboard | ||

| Liquid Packaging Board | |||

| Cupstock and Food-service Board | |||

| Flexible Barrier Paper | |||

| By End-user Industry | Food and Beverage | ||

| Consumer Goods | |||

| Healthcare and Pharma | |||

| Industrial and Electronics | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Malaysia | |||

| Singapore | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the water-based barrier paper packaging market?

The market is valued at USD 6.49 billion in 2025 and is projected to reach USD 9.24 billion by 2030.

How fast is the water-based barrier paper packaging market growing?

It is forecast to expand at a 7.32% CAGR between 2025 and 2030.

Which region is expected to post the highest growth?

Asia-Pacific leads growth with a 10.61% CAGR through 2030, supported by China’s express-packaging standards and rising e-commerce volumes.

Who are the leading companies in this market?

Smurfit Westrock, Mondi Group and International Paper together account for roughly 35% of global revenue, reflecting a moderately consolidated landscape.

What are the main factors driving adoption of water-based barrier paper packaging?

Plastic-ban legislation, brand recyclability pledges and advances in aqueous dispersion-coating lines are the primary demand catalysts.

Page last updated on: