Edible Coated Paper Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

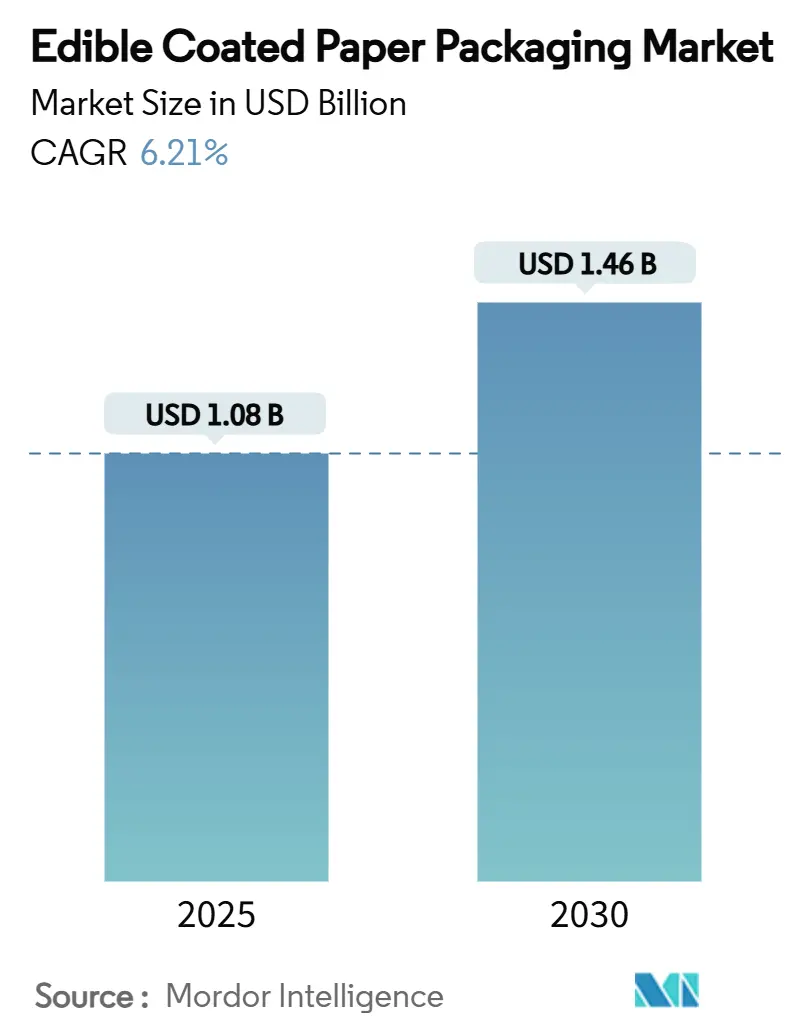

| Market Size (2025) | USD 1.08 Billion |

| Market Size (2030) | USD 1.46 Billion |

| Growth Rate (2025 - 2030) | 6.21% CAGR |

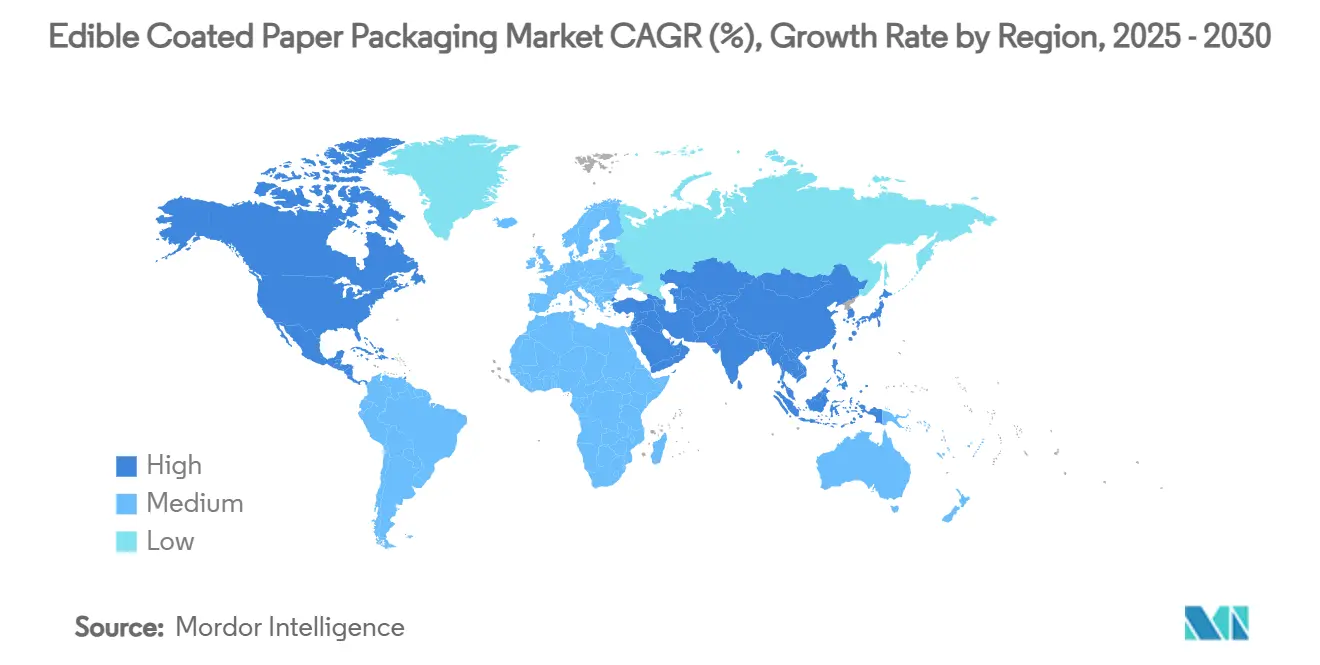

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Edible Coated Paper Packaging Market Analysis by Mordor Intelligence

The edible coated paper packaging market size reached USD 1.08 billion in 2025 and is forecast to expand to USD 1.46 billion by 2030, registering a 6.21% CAGR during the period. Stronger plastic-waste legislation, corporate sustainability mandates, and proven advances in bio-polymer barriers are reshaping material choices across food value chains. Firms that master composite barrier science achieve functional parity with thin plastic laminates, opening new premium channels. Meanwhile, the scale-up of coating lines is helped by lower capital costs due to ESG-linked financing. Europe anchors early adoption because of mandatory recycled-content rules, while Asia-Pacific delivers the steepest growth on the back of regulatory modernization and a rising middle class. Fragmentation persists, yet collaboration between specialized start-ups and global converters is accelerating time-to-market for high-performance formats.

Key Report Takeaways

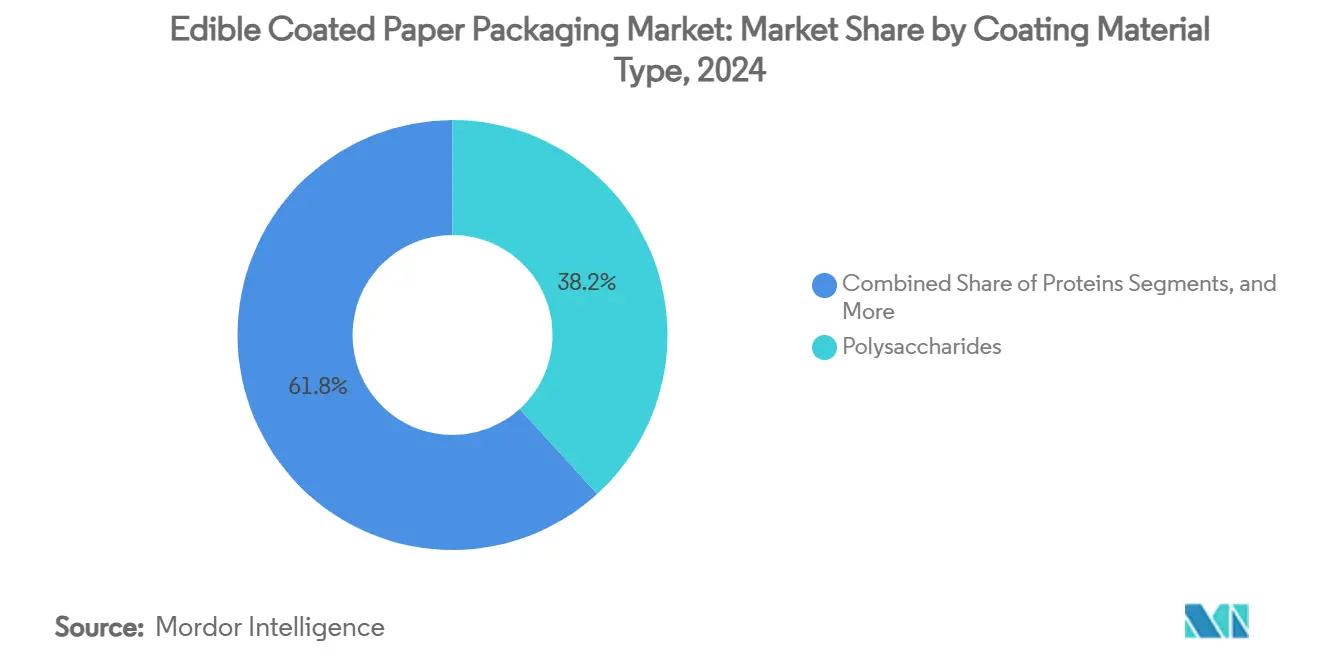

- By coating material, polysaccharides led with 38.24 % of the edible coated paper packaging market share in 2024.

- By application, the edible coated paper packaging market size for the fresh produce and ready-to-eat meals segment is projected to grow at a 7.46 % CAGR between 2025-2030.

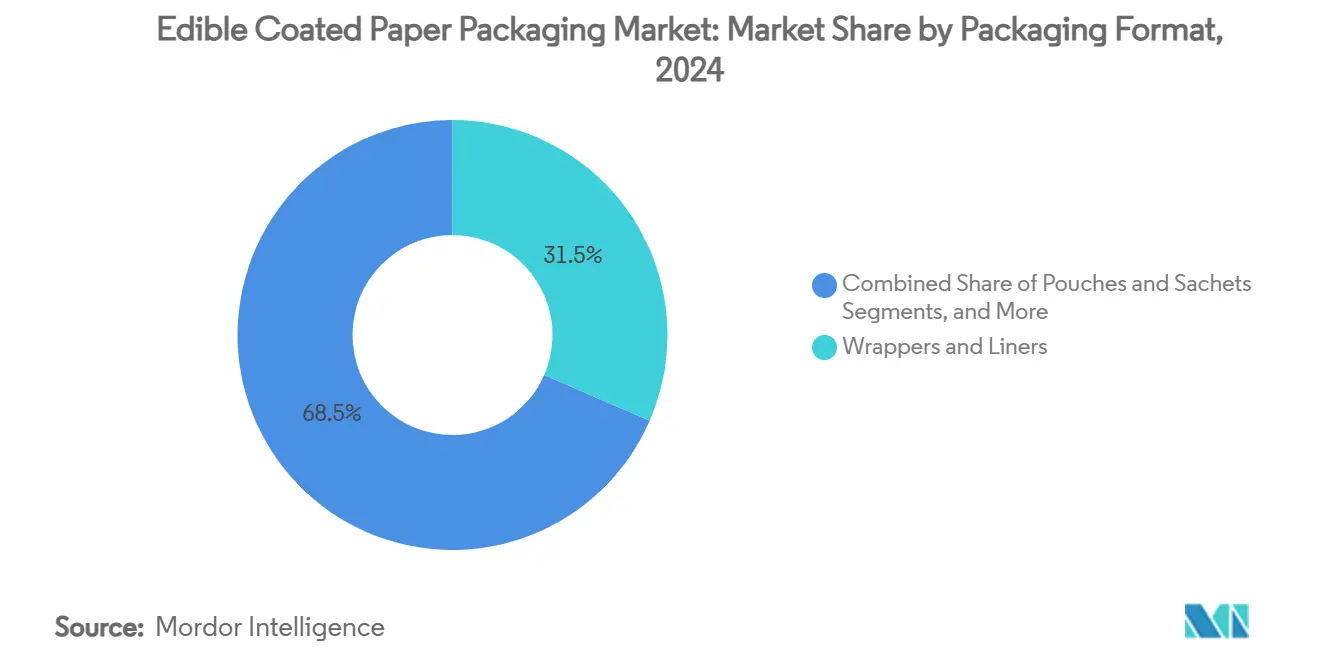

- By packaging format, wrappers and liners held 31.53 % of the edible coated paper packaging market share in 2024.

- By Geography, the edible coated paper packaging market size for the Asia-Pacific region is projected to grow at a 7.28 % CAGR between 2025-2030.

Global Edible Coated Paper Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Plastic-waste legislation accelerates demand for edible coatings | +1.2 % | Europe and North America, expanding to APAC | Medium term (2-4 years) |

| Corporate sustainability pledges move away from single-use plastics | +0.9 % | Global, led by multinational corporations | Short term (≤ 2 years) |

| Performance gains in bio-polymer barrier technologies | +0.8 % | Global, with innovation hubs in Europe and North America | Long term (≥ 4 years) |

| Active ingredients create premium SKUs | +0.6 % | North America and Europe, premium segments | Medium term (2-4 years) |

| Zero-waste grocery and meal-kit channels trial edible wrap formats | +0.4 % | Urban centers in developed markets | Short term (≤ 2 years) |

| ESG-linked financing lowers capital costs for innovators | +0.3 % | Global, concentrated in venture-capital hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Plastic-Waste Legislation Accelerates Demand for Edible Coatings

Governments are tightening plastic-waste rules that directly cut single-use volumes and spur searches for fully compostable or edible options. The EU Regulation 2025/40 mandates all packaging to be recyclable or reusable by 2030 and limits PFAS in food contact materials, driving swift substitution to edible coatings [1]European Commission, “European Union Finalizes New Rules for Packaging and Packaging Waste Reduction,” EUROPA.EU. Similar moves in Japan, China, and Australia standardize bio-based compliance pathways and ensure regulatory clarity that lowers approval risk. These synchronized policies raise baseline demand across multinational supply chains and embed edible formats into long-range capital allocation cycles.

Corporate Sustainability Pledges Move Away from Single-Use Plastics

Large FMCG groups and global converters tie procurement incentives to 2025-2030 public goals that require recyclable, reusable, or compostable designs. Amcor’s global pledge for 100% recyclable or reusable packaging in 2025 anchors predictable volume offtakes for bio-polymer-coated paper. Huhtamaki’s blueloop platform invests in fiber lines that switch customers from multilayer film to paper plus barrier coatings. Meal-kit provider HelloFresh prioritizes edible wrap pilots to help reach its 52 % food-waste reduction pledge. Such mandates create near-term certainty that helps processors amortize line conversions.

Performance Gains in Bio-Polymer Barrier Technologies

Composite chitosan coatings now deliver antimicrobial effects that rival traditional preservatives while holding sensory quality, improving commercial viability for fresh-cut fruit and meat. Starch-PVOH blends reach oxygen transmission below 10,000 cm³/m²/day, approaching the thresholds of metallized film for moderate-shelf-life confectionery. Nano-emulsion techniques lift coating uniformity, reduce additive load, and simplify regulatory approval. These functional leaps close prior performance gaps and broaden the addressable SKU mix.

Active Ingredients Create Premium SKUs

Brands deploy edible barriers infused with essential oils, probiotics, or nutraceuticals to differentiate high-value ranges. Chitosan plus thyme oil films extend strawberry shelf life and cut microbial counts without synthetic preservatives, appealing to clean-label positioning. The United States Department of Agriculture research funds active edible films for fresh produce, underscoring government support. Clear FDA guidance on allergen labeling gives formulators defined paths to compliance for protein coatings. Higher willingness to pay offsets raw material premiums and secures profitable niches.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High unit production cost and limited scale manufacturing | -1.8 % | Global, most acute in emerging markets | Short term (≤ 2 years) |

| Mechanical fragility vs. multi-layer plastic laminates | -1.1 % | Global, critical for industrial applications | Medium term (2-4 years) |

| Allergen-label challenges for protein-based coatings | -0.7 % | Developed markets with strict labeling requirements | Long term (≥ 4 years) |

| Printing-ink incompatibility limits brand graphics | -0.5 % | Global, affecting consumer goods applications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Unit Production Cost and Limited Scale Manufacturing

Capital-intensive drying tunnels, tight humidity control, and specialty feedstocks keep edible coated paper premiums above commodity film. Agricultural-waste pectin extraction shows poor line yields at the pilot level, highlighting process inefficiencies. Chitosan and modified starch cost 200-300 % more than low-density polyethylene per kilogram, squeezing margins in price-sensitive markets. Limited global supply chains for food-grade biopolymers add volatility. These economics are an immediate barrier, especially in emerging economies with limited ESG premiums at the point of sale.

Mechanical Fragility vs. Multi-Layer Plastic Laminates

Creasing, puncture, and tear tests reveal rapid performance decline under rough handling. Starch-PVOH films crack after industrial folding, and protein-based films show elevated water vapor transmission in humid corridors. Biodegradable test films achieve lower tensile strength than polyethylene, limiting their use in heavy items. Ongoing R&D in hybrid composites seeks to lift stress tolerance while keeping edible status, yet near-term applications stay concentrated in low-mechanical-load categories.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Coating Material Type: Composite Adoption Accelerates Regulatory-Ready Polysaccharides

Polysaccharides retained 38.24 % leadership in 2024 because cellulose, starch, and pectin hold GRAS or equivalent approvals across major jurisdictions [2]Food Standards Australia New Zealand, “Food Standards Code Compilation,” FOODSTANDARDS.GOV.AU . This base speeds new SKU roll-outs, minimizing dossier work. However, the composite and multilayer class is forecast to grow at 7.32 % CAGR to 2030 as converters merge polysaccharide matrices with micro-layers of lipids or proteins to narrow oxygen and moisture gaps. The edible coated paper packaging market size for composites will expand as premium formats gain traction in ready meals. Protein coatings lag because allergy labeling raises artwork complexity, yet UK regulators are drafting position papers that could open broader use of chitosan complexes. Nano-emulsion R&D further blends lipid gloss with starch rigidity, fostering formulas that tolerate flexographic inks.

Second-generation formulations employ cross-linkers that keep barrier tightness after heat-seal and cold-chain cycling. Suppliers such as AGRANA scale organic starch lines to capture this shift, integrating GMO-free claims that resonate with European buyers. Overall, material convergence positions composites to displace petroleum-based laminates in snack bars and cereal liners, giving rise to higher volumes and more stable revenue curves.

By Application: Fresh Produce Surges Beyond Legacy Bakery Dominance

Bakery and confectionery held 35.69 % of the edible coated paper packaging market share in 2024, supported by familiar wrapper formats and established supply agreements. Shelf-stable pastries rely on thin polysaccharide layers that prevent sugar bloom without hindering recyclability. Yet the edible coated paper packaging market size attached to fresh produce and ready-to-eat meals is rising fastest at a 7.46 % CAGR on heightened food-waste reduction targets. Chitosan-based skins reduce microbial spoilage on apple slices, extending display life for retailers.

Growth is reinforced by government procurement in school meal programs that prefer compostable or edible wraps to meet zero-waste policies. Meat and seafood remain smaller because USDA FSIS oversight has tightened allergen and sanitation hurdles. Dairy brands evaluate cheese slices wrapped in protein films, seeking plastic-free differentiation. Beverage cups and straws test lipid-starch blends for café chains that phase out coated paperboard. Each new application widens the commercial validation loop and accelerates downstream tooling orders.

By Packaging Format: Three-Dimensional Lines Drive CapEx Upswing

Wrappers and liners commanded 31.53 % share in 2024 because they require thinner coatings and leaner drying equipment. However, three-dimensional trays, cups, and bowls now post a 7.15 % CAGR through 2030 as quick-service dining pivots to fiber molds over polystyrene clamshells. The edible coated paper packaging market size attached to molded formats benefits from ESG-linked financing that subsidizes high-speed vacuum-forming cells. Pouches and sachets address single-serve seasoning and instant-noodle markets, yet sealing temperatures must avoid protein denaturation, adding technical complexity.

Labels, stickers, and cutlery represent early-stage niches that face color-fastness and strength barriers. Printed ink mobility risks migrate brand graphics; thus, research into food-grade solvent-free inks picks up pace. Pilot plant data reveal that format complexity increases film thickness variation, prompting investments in inline optical inspection. Scalability success hinges on balancing geometry, speed, and water removal without compromising edibility.

Geography Analysis

Europe’s leadership stems from binding recycled-content mandates that eliminate regulatory ambiguity for converters. Large retailers demand vendor compliance audits, driving rapid transitions from poly-laminate to edible barriers in ready bakery lines. Germany, the UK, and France introduced supplier scorecards that rank compostability, pushing edible coated paper adoption in private-label SKUs. Southern Europe’s fruit exporters deploy chitosan wraps to slow mold growth during long-haul shipments.

Asia-Pacific showcases the fastest uptake, supported by population density and accelerating cold-chain investment. Japan’s 2025 positive list system approves bio-based coatings for broad use, creating immediate pathways for domestic producers. China’s GB 4806.1 revision emphasizes dual safety and environmental endpoints, opening supply contracts with international QSR chains that expand in Tier-2 cities. India’s organized retail boom and government plastic-ban extensions spur local mills to trial starch-cellulose films.

North America leverages robust R&D ecosystems. University-industry consortia develop nano-fibrillated cellulose blends that can be hot-filled without delamination, offering potential breakthroughs for soup cups. The United States hosts early-stage pilots inside military commissary channels, aligning with federal waste targets. Canada’s shared standards simplify cross-border distribution, while Mexico’s price sensitivity keeps adoption to premium snack and export-oriented orchards.

Competitive Landscape

The market remains fragmented with specialized biotech firms, regional paper mills, and global packaging majors coexisting. Notpla commercializes seaweed film sachets for sauces, while Evoware pilots cassava-based paper in Indonesia. Lactips supplies casein pellets that paper converters extrude into barrier coatings. Large incumbents such as Mondi, International Paper, and Stora Enso retrofit coaters to run bio-polymer dispersions, pairing volume capacity with client trust. Collaboration models prevail: converters license start-up chemistries, and ingredient producers secure off-take agreements to derisk scale-up.

Strategic moves center on joint ventures, line conversions, and patent portfolios. Mondi boosted flexible packaging output after completing a EUR 125 million bio-barrier upgrade in Germany. DuPont invested in photopolymer plate lines that enable high-resolution graphics on coated papers . Closed Loop Partners channel ESG capital into pilot plants that convert agricultural waste into pectin feedstock[3]Closed Loop Partners, “2023 Impact Report,” CLOSEDLOOPPARTNERS.COM . Consolidation is expected as successful chemistries mature and majors seek secure resin inputs.

Startup differentiation increasingly revolves around active-ingredient licensing. Firms that file claims for antimicrobial or nutraceutical payloads can command higher unit value and defend margins. Patent races around nano-emulsion barrier tech drive alliances with academic labs. Competitive intensity remains high, but the absence of a dominant patent pool supports open innovation and multiple parallel pathways to technical success.

Edible Coated Paper Packaging Industry Leaders

Notpla Ltd.

Monosol LLC (Kuraray)

Evoware

Lactips

Stora Enso Oyj

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: The European Union finalized Regulation 2025/40 that mandates 65 % recycled content in plastic packaging by 2040 and restricts PFAS in food-contact materials.

- February 2025: Japan’s Ministry of Health, Labour and Welfare implemented the positive list for food-contact materials, clarifying approval routes for bio-based coatings.

- October 2024: Avery Dennison Investor Day unveiled solvent-free adhesive platforms relevant to edible barrier lamination.

- September 2024: AGRANA showcased organic starch lines positioned for edible coatings within European premium bakery channels.

Global Edible Coated Paper Packaging Market Report Scope

| Polysaccharides (Starch, Cellulose, Pectin, Alginate, Pullulan) |

| Proteins (Whey, Soy, Gelatin, Zein) |

| Lipids and Waxes (Beeswax, Carnauba, Plant-wax) |

| Composite and Multilayer Coatings |

| Bakery and Confectionery |

| Fresh Produce and Ready-to-Eat Meals |

| Meat, Poultry and Seafood |

| Dairy Products |

| Beverage Cups and Straws |

| Other Applications (Spices, Instant-Noodle Wraps) |

| Wrappers and Liners |

| Pouches and Sachets |

| Trays, Cups and Bowls |

| Labels and Stickers |

| Cutlery and Straws |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Thailand | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | GCC |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Coating Material Type | Polysaccharides (Starch, Cellulose, Pectin, Alginate, Pullulan) | ||

| Proteins (Whey, Soy, Gelatin, Zein) | |||

| Lipids and Waxes (Beeswax, Carnauba, Plant-wax) | |||

| Composite and Multilayer Coatings | |||

| By Application | Bakery and Confectionery | ||

| Fresh Produce and Ready-to-Eat Meals | |||

| Meat, Poultry and Seafood | |||

| Dairy Products | |||

| Beverage Cups and Straws | |||

| Other Applications (Spices, Instant-Noodle Wraps) | |||

| By Packaging Format | Wrappers and Liners | ||

| Pouches and Sachets | |||

| Trays, Cups and Bowls | |||

| Labels and Stickers | |||

| Cutlery and Straws | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Thailand | |||

| Indonesia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | GCC | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the edible coated paper packaging market?

The edible coated paper packaging market size reached USD 1.08 billion in 2025 and is forecast to rise to USD 1.46 billion by 2030.

Which region grows fastest between 2025 and 2030?

Asia-Pacific posts the highest 7.28 % CAGR owing to regulatory modernization in Japan, China, and India that supports bio-based packaging adoption.

Which coating material segment expands quickest?

Composite and multilayer coatings are projected to grow at a 7.32 % CAGR as converters combine polysaccharides with lipid or protein layers for stronger barriers.

What are the main restraints facing the market?

High unit production costs and mechanical fragility versus plastic laminates are the strongest restraints, lowering near-term profitability in price-sensitive categories.

How do corporate pledges influence demand?

Global FMCG and packaging majors with 2025-2030 sustainability goals purchase recyclable or edible formats, creating predictable offtake that supports investment in coating capacity.

What premium opportunities exist for manufacturers?

Active ingredient coatings that add antimicrobial or nutraceutical functions allow higher price points and meet clean-label consumer demand, especially in North America and Europe.

Page last updated on: