Smart Barrier Paper Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

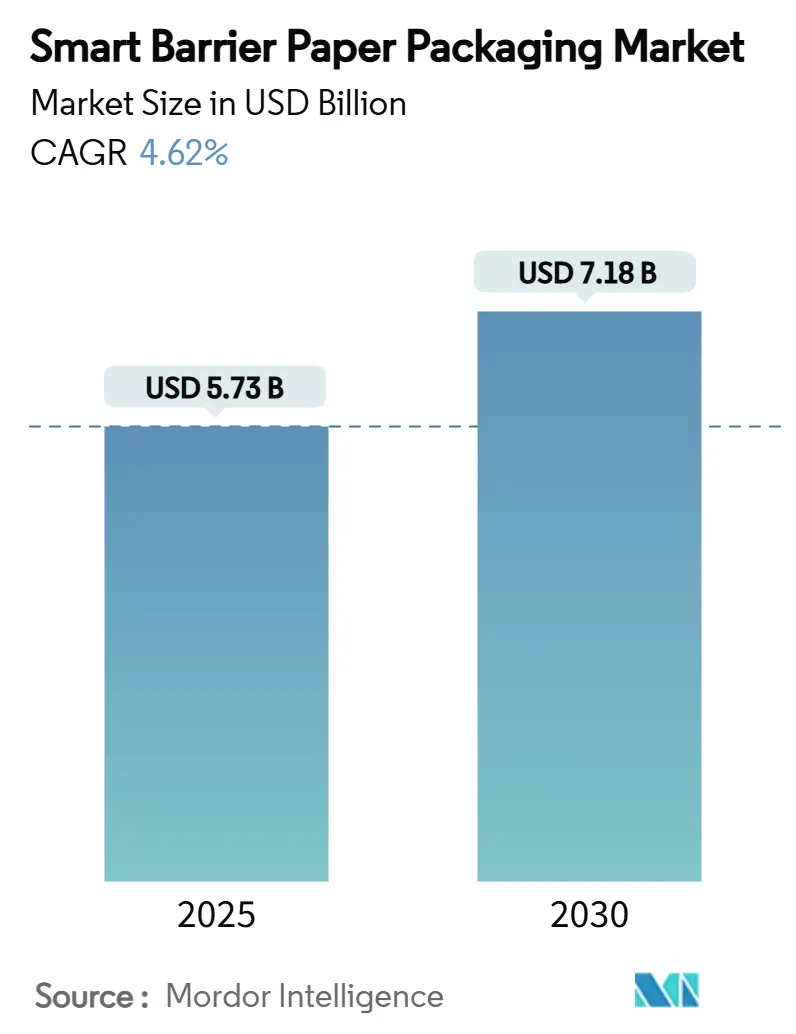

| Market Size (2025) | USD 5.73 Billion |

| Market Size (2030) | USD 7.18 Billion |

| Growth Rate (2025 - 2030) | 4.62% CAGR |

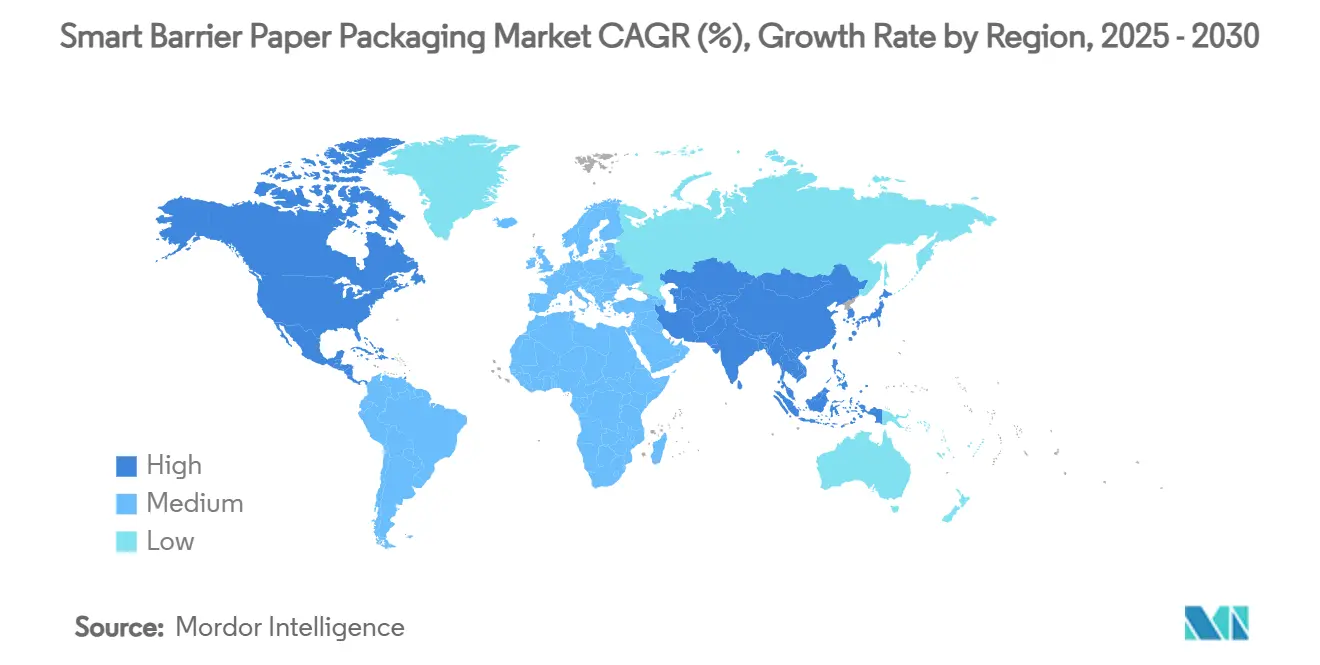

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

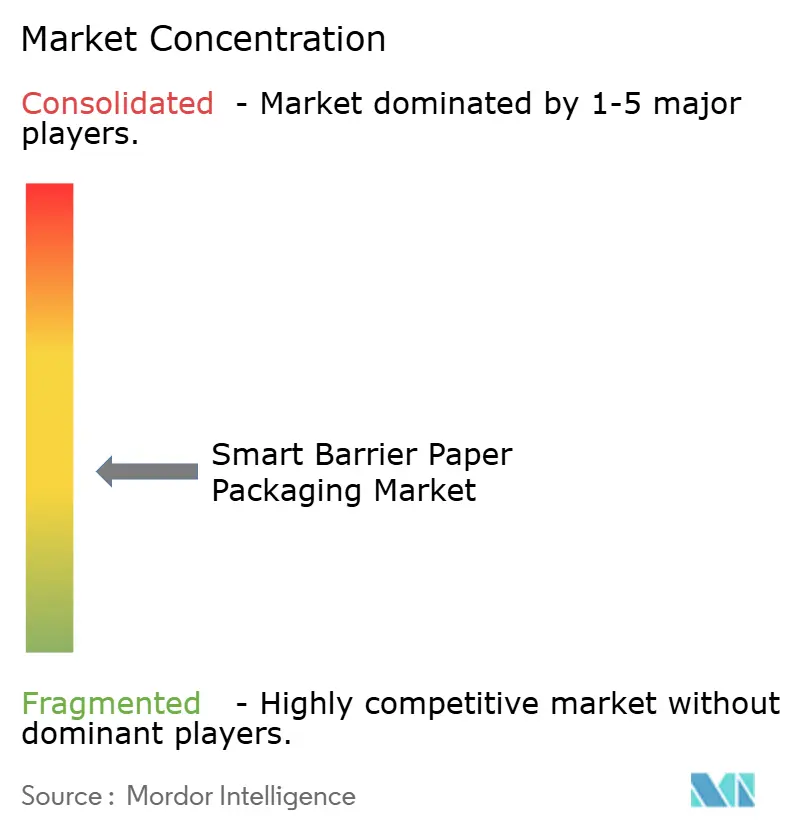

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Barrier Paper Packaging Market Analysis by Mordor Intelligence

The smart barrier paper packaging market size stands at USD 5.73 billion in 2025 and is forecast to reach USD 7.18 billion by 2030, expanding at a CAGR of 4.62% during 2025-2030. This trajectory captures the pivot from petroleum-based substrates toward fiber-based alternatives as policymakers restrict PFAS, tighten recyclability thresholds, and impose extended producer responsibility fees. Multinational brands are redesigning pack formats into mono-material platforms, catalyzing rapid adoption of water-based dispersion coatings that now command 42.23% of the smart barrier paper packaging market. Asia-Pacific holds the strategic lead as the region combines low-cost converting infrastructure with breakthrough coating chemistries such as Japan’s SHIELDPLUS water-soluble system. Moisture-barrier grades dominate demand because water ingress remains the single largest spoilage risk across food, personal-care, and pharmaceutical chains. In parallel, e-commerce cold-chain mailers are opening new revenue pools as online grocery platforms seek thermal liners that are lightweight, curb-side recyclable, and compliant with PFAS bans.

Key Report Takeaways

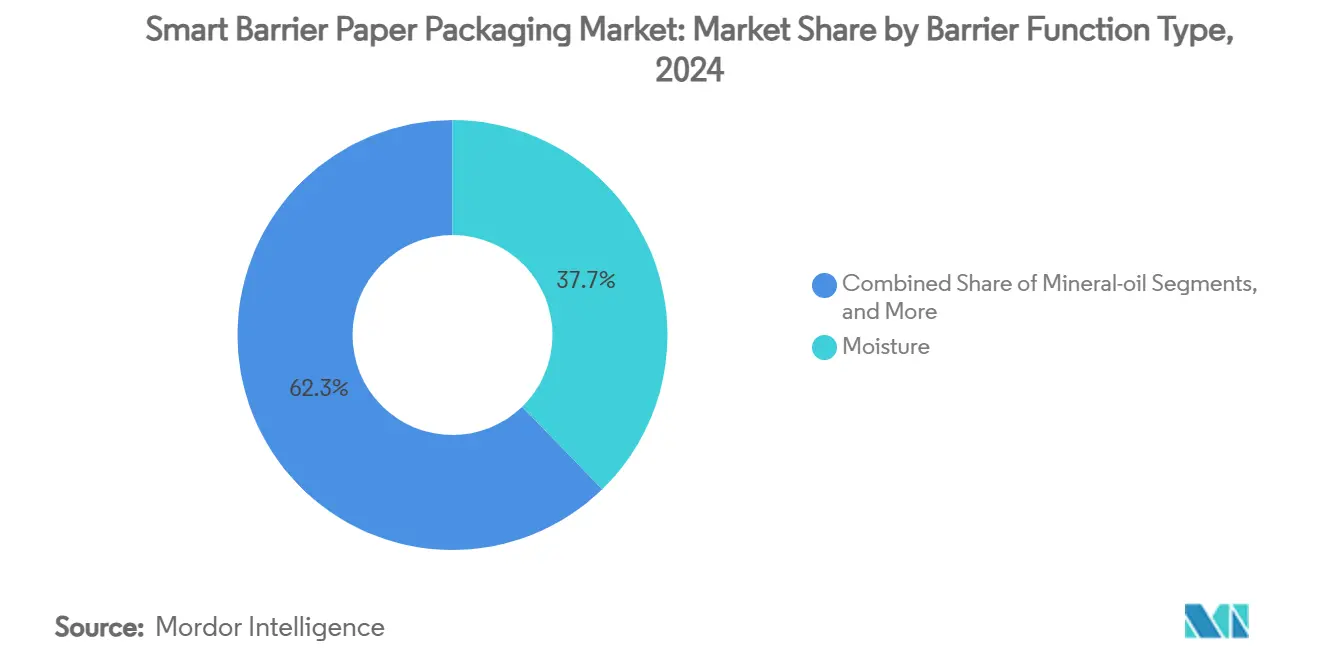

- By barrier function type, moisture grades controlled 37.73% of the smart barrier paper packaging market share in 2024.

- By coating/treatment technology, the smart barrier paper packaging market size for the cellulose-nanofibre (CNF) lamination segment is projected to grow at a 17.40% CAGR between 2025-2030.

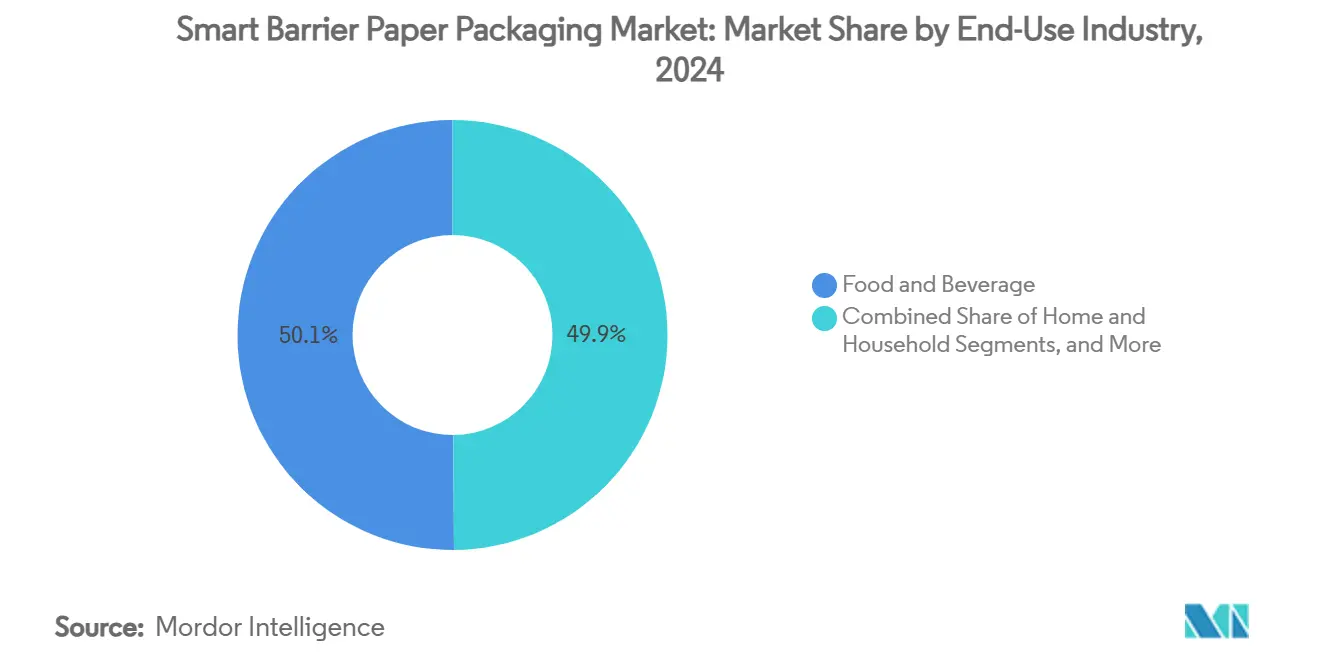

- By end-use industry, food and beverage retained a 50.12% share of the smart barrier paper packaging market size in 2024.

- By geography, the smart barrier paper packaging market size for the Asia-Pacific region is projected to grow at a 11.30% CAGR between 2025-2030.

Global Smart Barrier Paper Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising plastic-replacement regulations | +1.2% | Global; EU and North America lead | Medium term (2-4 years) |

| Brand demand for mono-material paper packs | +0.8% | Global; concentrated in developed markets | Short term (≤ 2 years) |

| Rapid scale-up of water-based dispersion coatings | +0.7% | APAC core; spill-over to North America & EU | Medium term (2-4 years) |

| Food-grade grease-barrier breakthroughs with PFAS-free chemistries | +0.6% | Global; early adoption in EU and North America | Long term (≥ 4 years) |

| Adoption of cellulose-nanofibre (CNF) lamination in Asia | +0.5% | APAC; technology transfer to other regions | Long term (≥ 4 years) |

| Smart barrier papers in e-commerce cold-chain insulation | +0.4% | Global; led by North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Plastic-Replacement Regulations

Global policy action is compressing compliance timelines and transforming specification sheets across consumer and industrial segments. The EU Packaging and Packaging Waste Regulation bans PFAS in food-contact papers from August 2026 and sets a minimum recyclability of 70% by 2030, rising to 80% by 2038. China’s mandatory express-pack standard GB 43352-2023 caps heavy-metal residues and hazardous substances starting June 2024. Australia’s forthcoming extended producer responsibility framework signals similar pressures in Oceania. Such converging rules obligate converters to redesign structures rather than swap films, intensifying demand for integrated moisture-oxygen-grease barriers within a paper substrate. Capital is therefore flowing into coating assets able to toggle between legislative test protocols for North America, Europe, and Asia in the same production campaign.

Brand Demand for Mono-Material Paper Packs

Consumer-product companies view packaging simplicity as a tangible brand differentiator. Mondelēz partnered with Saica to supply heat-sealable paper wraps that run on existing multi-pack lines yet pass CEPI recyclability tests [1]Packaging Europe, “Saica and Mondelēz partner to launch paper-based product for food market,” PACKAGINGEUROPE.COM. Surveys show 62% of shoppers perceive paper as inherently greener than plastic. Mono-material platforms eliminate delamination hurdles and simplify curbside collection, enabling on-pack claims that resonate at the point of sale. Joint-development agreements are replacing transactional sourcing, granting converters longer revenue visibility and a pipeline of customer-funded R&D as they tailor surface chemistries to individual filler speeds and sealing jaws.

Rapid Scale-Up of Water-Based Dispersion Coatings

Water-borne dispersions lower VOC, avoid explosion-proof rooms, and retrofit onto gravure or curtain coaters with minimal downtime, a decisive cost advantage for large mills. TAPPI studies confirm emission reductions while maintaining grease and moisture resistance comparable to solvent-based analogues. Laboratory work shows water-borne polymer-nanoclay layers cut water-vapor transmission from 533 g/m²·day to 1.3 g/m²·day. Asian mills exploit low energy tariffs and government grants to scale these lines, then export reels to converters in Europe and the Americas. With 80% of Sirane’s flexible portfolio now paper-based, the tipping point toward dispersion systems has arrived.

Adoption of Cellulose-Nanofibre (CNF) Lamination in Asia

Japanese and Korean mills pilot multilayer CNF laminates that drive water-vapor transmission below 1 g/m²·day while preserving heat-seal ranges suited to high-speed flow-wrappers. Falling CNF costs, aided by co-product valorization in bio-refineries, are unlocking roll-to-roll lamination at commercial widths. Technology-transfer agreements are now licensing Asian know-how to European converters seeking premium aroma barriers for coffee and nutraceuticals. Long-term, CNF could erode extrusion-coated polyethylene volumes in barrier sacks and sachets.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost premium over commodity plastics | -0.9% | Global; higher in price-sensitive regions | Short term (≤ 2 years) |

| Limited high-speed converting line compatibility | -0.6% | Global; affects large-scale operations | Medium term (2-4 years) |

| Barrier performance loss in humid tropics | -0.4% | Tropical and subtropical zones | Long term (≥ 4 years) |

| Competition from bio-based polymer films | -0.3% | Global; premium niches | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cost Premium Over Commodity Plastics

Smart barrier paper commands higher input and conversion costs than legacy films because specialty coatings, lower production scales, and multi-pass drying inflate per-ton economics. MDPI research notes that biopack solutions often struggle for price parity despite environmental savings[2]MDPI, “Opportunities and Challenges in the Application of Bioplastics,” MDPI.COM. The gap narrows gradually as mills retrofit idle newsprint lines and capitalize on EPR-linked plastic surcharges. Billerud’s SEK 1.2 billion North American upgrade aims to optimize tonne-hour efficiencies and reduce freight overheads, signalling strategic intent to squeeze unit costs. Yet, in lower-income economies, plastic sachets remain irresistible on a cost-per-serve basis, postponing large-scale displacement.

Limited High-Speed Converting Line Compatibility

Papers demand tighter web tension windows, different heat-seal dwell times, and specialized glues compared with biaxially-oriented films. IPPTA studies show that machine-clothing permeability and tension variance can erode efficiency on older corrugators and flow-wrappers. Brand owners with billion-unit filler speeds hesitate to down-rate throughput while qualification trials proceed. Equipment OEMs are engineering hybrid modules, yet upgrade capex remains substantial. Over the medium term, collaborative machinery-material testing cells should broaden compatibility, but the restraint tempers penetration in mass-volume snack and beverage lines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Barrier Function Type: Moisture Dominance Drives Innovation

Moisture grades contributed 37.73% of the smart barrier paper packaging market share in 2024, as desiccation-sensitive products from meat to nutraceutical powders hinge on water-vapor control. CNF-reinforced coatings now deliver 93% reductions in transmission, enabling paper to enter freezer-grade and retort end-uses once monopolized by polyamide laminates. Producers integrate mineral-oil blocks, aroma locks, and anti-oxidation layers into the same pass, aligning with customer demand for fewer SKUs and leaner inventories. Light and UV grades, though smaller, post a 15.20% CAGR by catering to blue-light-sensitive dairy, craft-beer labels, and probiotic capsules. They utilize titanium dioxide micro-layers or lignin-based UV absorbers that remain fully repulpable.

The smart barrier paper packaging market size for oxygen and aroma control rises steadily as single-serve coffee, snack-nuts, and infant-formula players shift away from aluminium foil. Oil/grease resistance platforms are in flux amid PFAS bans, pushing starch-fatty-acid esters and boric-acid-cross-linked PVA into pilot trials. Multilayer hybrid solutions capture customers unwilling to gamble on full mono-transition, balancing incremental compliance with operational risk. Mineral-oil migration concerns after MOAH incidents in Europe stimulate paper grades able to block aromatic hydrocarbons migrating from recycled corrugate, adding a food-safety impetus to the segment mix.

By Coating Technology: Water-Based Systems Lead Transformation

Water-based dispersion lines supplied 42.23% of 2024 revenue, underlining their status as the de facto workhorse for high-volume moisture barriers. Formulators blend styrene-acrylate lattices with nanoclay or alkyl-ketene-dimer to balance sealing windows and shelf-life. Because the chemistries run on existing curtain coaters, mills re-deploy depreciated newsprint machines, accelerating capacity without building green-field assets. The smart barrier paper packaging market size linked to dispersion lines should surpass USD 3 billion by 2030 as brands embed recyclability scorecards into procurement.

CNF laminate technology, expanding at 17.40% CAGR, occupies premium niches such as high-fat confectionery wraps and pharma sachets where pin-hole resistance and flex-crack durability outweigh higher cost. Plasma-treated surfaces exist at the frontier, pre-activating cellulose fibers for superior adhesive wetting and coating anchorage. Bio-derived polymer blends PLA-PHB matrices with cellulose nanocrystals promise compost-ready solutions, yet chill-seal limitations currently corral them into dry-food pouches. Solvent systems fade as occupational-health audits tighten, though they persist for military rations demanding >5-year shelf stability.

By End-Use Industry: Food Dominance with E-Commerce Surge

Food and beverage accounted for 50.12% of global revenue in 2024 because moisture, grease, and aroma integrity directly translate into downgrades and waste. Leading confectionery, bakery, and dairy fillers embed barrier paper into roll stock to hit corporate net-zero targets without revamping pack architecture. Shelf-life modelling illustrates that a switch from oriented polypropylene to dispersion-coated kraft can cut greenhouse-gas emissions 35% cradle-to-gate. The sector’s volume density secures economies of scale that reduce per-pack premiums, encouraging spill-over into adjacent personal-care and pet-food categories.

E-commerce mailers, accelerating at 18.00% CAGR, pull barrier papers into secondary containment where return-ready seals, QR-enabled traceability, and temperature cushioning must coexist. Fashion platforms adopt curb-side recyclable padded mailers to meet upcoming French AGEC and California SB 54 mandates. Healthcare and pharma uptake grows for blister-overwraps and sachets compatible with ISO 11607. Industrial and construction sacks test mineral-oil and moisture barriers for powdered adhesives and grout mixes, while home-care brands pilot grease-barrier liners for detergent pods aimed at eliminating LDPE pouches.

Geography Analysis

Asia-Pacific led with 36.25% revenue share in 2024 and is projected to grow at 11.30% CAGR to 2030 as China, India, and ASEAN nations escalate bans on single-use plastics and incentivize fibre conversion lines. Mandatory express-parcel standards in China, coupled with Japan’s SHIELDPLUS technology, anchor supply-chain depth from pulp to finished pouch. Competitive labour rates and captive pulp availability allow mills to price aggressively, positioning the smart barrier paper packaging market as a strategic export engine for the region.

North America remains a critical revenue pool where PFAS prohibitions across multiple states and the federal EPR debate feed sustained demand for compliant barrier substrates. Billerud’s SEK 1.2 billion Michigan revamp shows how European know-how is localized to shorten lead times and hedge freight volatility. E-commerce cold-chain growth outpaces overall parcel expansion as meal-kit services penetrate secondary cities, reinforcing appetite for thermal liner papers.

Europe exerts regulatory leadership; the Packaging and Packaging Waste Regulation sets recyclability and recycled-content baselines that ripple through global procurement. With 85% of Mondi’s packaging revenue now reusable, recyclable, or compostable, producers embed circularity metrics into product-development charters . Incremental capacity such as Stora Enso’s USD 1 billion Oulu board line ensures domestic supply for Scandinavian converters, mitigating geopolitical supply shocks.[3]Stora Enso, “Stora Enso Interim Report January–March 2025,” STORAENSO.COM

Competitive Landscape

The smart barrier paper packaging market is moderately fragmented, with the top five players accounting for roughly 45% of global revenue. Vertical integration from pulp forests through coating assets confers cost leverage and quality consistency. Stora Enso’s Oulu investment, Mondi’s Kraftliner upgrades, and Amcor’s patent portfolio illustrate the capex-plus-IP strategy defining competitive boundaries.

Technology partnerships eclipse spot sales; converters co-develop chemistries with brands to lock in multi-year offtake and embed exclusivity clauses. White-space opportunities concentrate in high-barrier pharmaceutical sachets and e-commerce thermal liners, where performance thresholds are stringent and ASPs justify premium coatings. New entrants from bio-polymer films attempt crossover plays, yet struggle to match paper’s tactile shelf appeal and curb-side recyclability narrative.

M&A potential centers on specialty-chemical formulators owning PFAS-free grease-barrier IP. Scale-hungry paper majors look to bolt-on these tech shops to accelerate go-to-market while internal R&D focuses on pilot-plant validation. Geographic diversification is another lever; capacity additions in North America reduce currency risk and respond to Buy-American procurement directives in federal nutrition programs.

Smart Barrier Paper Packaging Industry Leaders

Stora Enso Oyj

Smurfit Westrock Plc

Mondi Group

Billerud AB (publ)

Koehler Paper SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Stora Enso reported 9% Q1 sales growth on the ramp-up of its new consumer-board line at Oulu, targeting EBITDA breakeven by end-2025 and full capacity by 2027.

- January 2025: Amcor secured a European patent for AmFiber Performance Paper, integrating high-barrier layers with heat-sealable surfaces for food and healthcare uses

- December 2024: Billerud announced SEK 1.4 billion in North American investments aimed at optimizing liner and paperboard capacity .

- April 2024: Ranpak unveiled climaliner Plus and naturemailer padded mailers, both 100% paper and fully recyclable, targeting cold-chain e-commerce .

Global Smart Barrier Paper Packaging Market Report Scope

| Oxygen and Aroma |

| Moisture |

| Oil / Grease |

| Mineral-oil |

| Light and UV |

| Multilayer Hybrid |

| Water-based Dispersion |

| Extrusion-Coated |

| Plasma-Treated |

| Solvent-Based |

| Bio-derived Polymer Blend |

| CNF Laminated |

| Food and Beverage |

| Personal Care and Cosmetics |

| Home and Household |

| Industrial / Construction |

| Healthcare and Pharma |

| E-commerce Mailers |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Barrier Function Type | Oxygen and Aroma | ||

| Moisture | |||

| Oil / Grease | |||

| Mineral-oil | |||

| Light and UV | |||

| Multilayer Hybrid | |||

| By Coating / Treatment Technology | Water-based Dispersion | ||

| Extrusion-Coated | |||

| Plasma-Treated | |||

| Solvent-Based | |||

| Bio-derived Polymer Blend | |||

| CNF Laminated | |||

| By End-use Industry | Food and Beverage | ||

| Personal Care and Cosmetics | |||

| Home and Household | |||

| Industrial / Construction | |||

| Healthcare and Pharma | |||

| E-commerce Mailers | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the smart barrier paper packaging market?

The smart barrier paper packaging market size is valued at USD 5.73 billion in 2025.

How fast is the market expected to grow over the next five years?

Revenue is projected to rise to USD 7.18 billion by 2030, reflecting a 4.62% CAGR during the forecast period.

Which region holds the largest share of demand?

Asia-Pacific leads with 36.25% of global revenue in 2024, supported by regulatory mandates and competitive manufacturing costs.

What segment is expanding the quickest?

E-commerce mailers show the fastest growth at an 18.00% CAGR as online retail scales cold-chain and return-ready shipping needs.

Why are water-based dispersion coatings so prominent?

These coatings deliver strong moisture and grease barriers without VOC emissions and retrofit onto existing coaters, earning 42.23% share of 2024 revenue.

How are PFAS bans influencing technology choices?

Regulators outlawing fluorochemicals push converters toward PFAS-free grease-barrier chemistries such as CNF composites and boric-acid-cross-linked PVA, accelerating R&D and adoption across food-contact grades.

Page last updated on: