UV-Barrier Paper Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

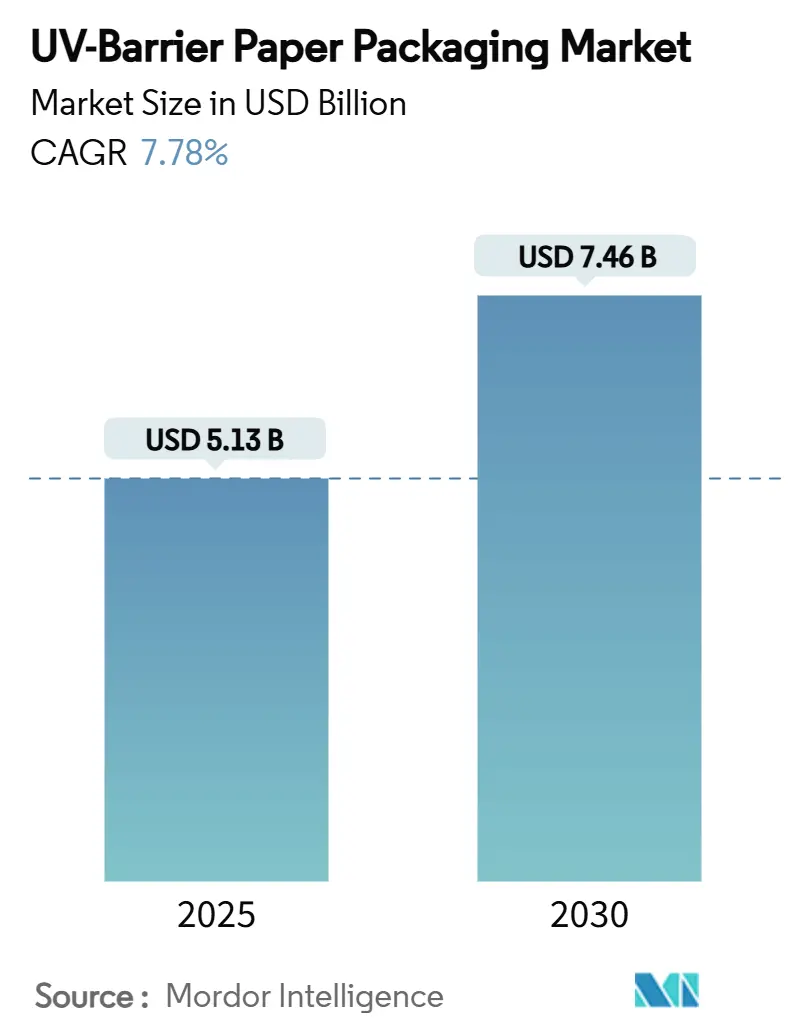

| Market Size (2025) | USD 5.13 Billion |

| Market Size (2030) | USD 7.46 Billion |

| Growth Rate (2025 - 2030) | 7.78% CAGR |

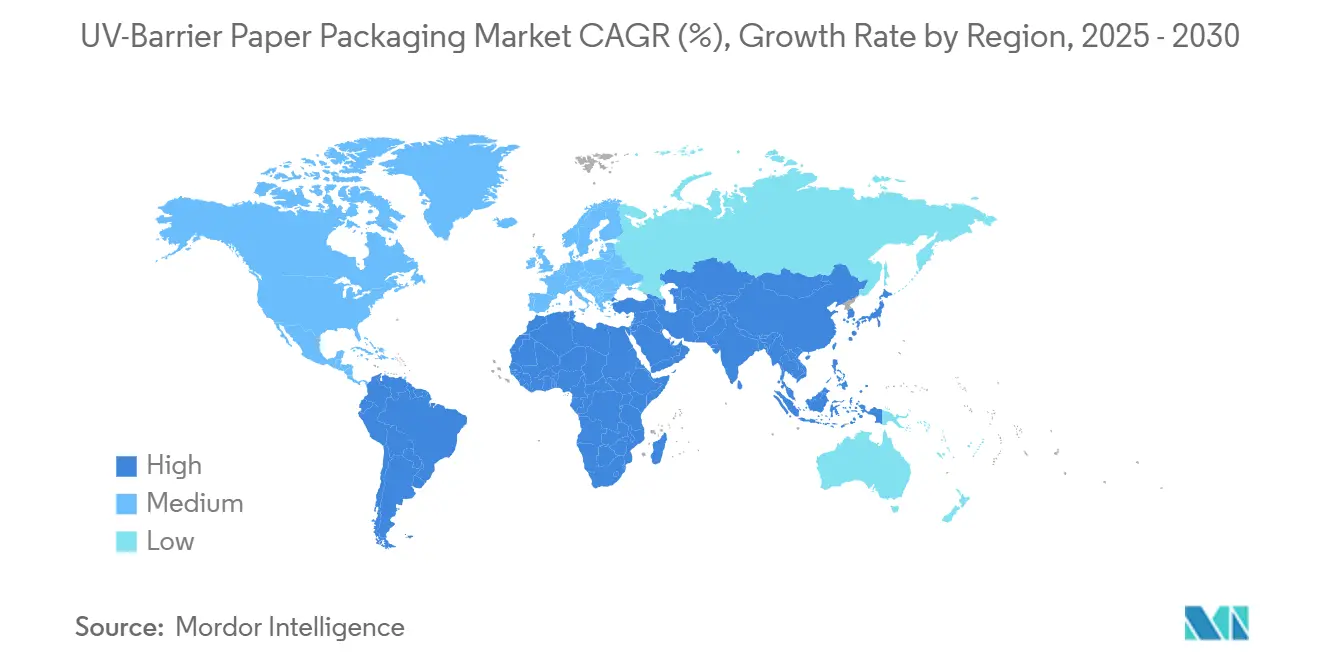

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UV-Barrier Paper Packaging Market Analysis by Mordor Intelligence

The UV-Barrier Paper Packaging market size stood at USD 5.13 billion in 2025 and is forecast to reach USD 7.46 billion by 2030, expanding at a 7.78% CAGR during 2025-2030. Rising regulatory pressure for fully recyclable formats, rapid progress in bio-based barrier coatings, and premiumisation across nutraceutical and cosmetic categories jointly accelerate demand. Consolidation among global suppliers following the International Paper-DS Smith and Smurfit Kappa-WestRock mergers unlocks scale advantages in technology roll-outs, while Europe’s recyclability mandates and Asia–Pacific’s e-commerce boom widen geographic growth fronts. Major retailers’ monomaterial policies, FDA withdrawal of PFAS approvals, and volatile titanium-dioxide pricing further shape the competitive agenda of the UV-Barrier Paper Packaging market.

Key Report Takeaways

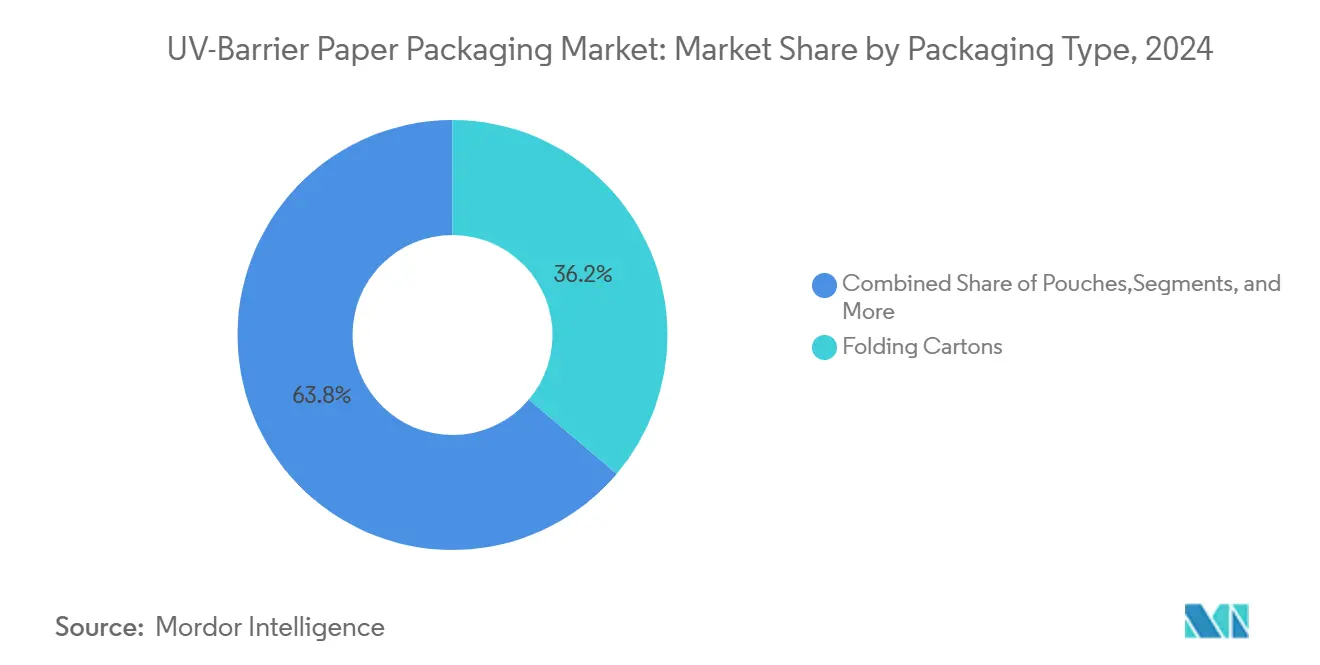

- By packaging type, folding cartons led with 36.17% of the UV-Barrier Paper Packaging market share in 2024.

- By barrier technology, the UV-Barrier Paper Packaging market size for the bio-based coatings segment is projected to grow at an 8.93% CAGR between 2025- 2030.

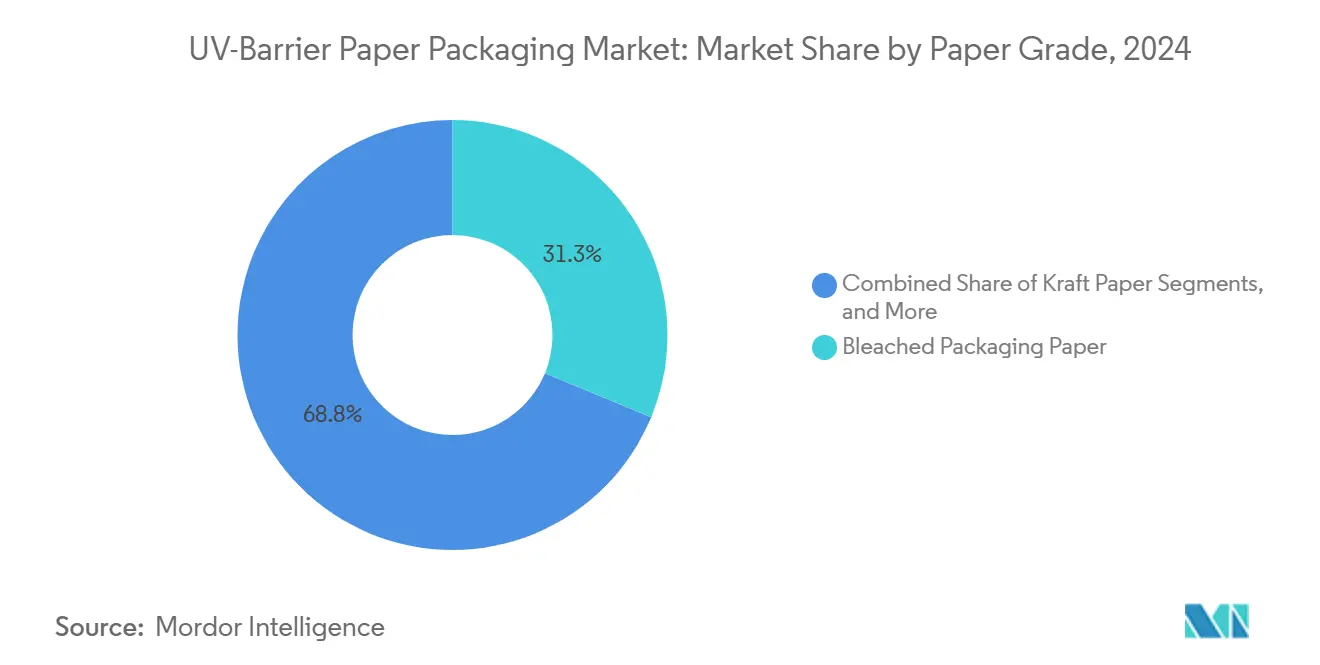

- By paper grade, bleached packaging paper commanded a 31.25% share of the UV-Barrier Paper Packaging market size in 2024.

- By end-user industry, the UV-Barrier Paper Packaging market size for the pharmaceuticals and nutraceuticals segment is projected to grow at an 8.71% CAGR between 2025- 2030.

- By geography, Europe captured 30.12% of the UV-Barrier Paper Packaging market share in 2024.

Global UV-Barrier Paper Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in demand for recyclable UV-protected food packaging | +1.2% | Global (early uptake in Europe, North America) | Medium term (2-4 years) |

| Stringent regulations on photodegradable inks and dyes | +0.9% | Europe, North America expanding to APAC | Short term (≤ 2 years) |

| Premiumisation of nutraceutical and cosmetics formats | +0.8% | Global, focused on developed markets | Long term (≥ 4 years) |

| Retailer shift to monomaterial solutions for curb-side recycling | +0.7% | Europe and North America | Medium term (2-4 years) |

| UV-blocking lignin nanoparticle coatings reaching pilot scale | +0.6% | Nordic region, North America | Long term (≥ 4 years) |

| Growth of e-commerce ambient grocery requiring shelf-stable packs | +0.5% | APAC and North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in demand for recyclable UV-protected food packaging

Food safety standards and circular-economy rules converge to lift demand for recyclable substrates that still block light-induced spoilage. Two-thirds of European packaging tonnage already sits in the fiber segment, yet legacy UV barriers relied on multilayer laminates that hinder recycling. Lignin-based coatings now replicate UV shielding in the 250–400 nm range without plastic layers, letting converters meet 2030 recyclability targets. Mondi channels 85% of its packaging revenue from reusable, recyclable or compostable lines, underpinning volume upside for monomaterial grades. Brands pay a premium for paper structures that move seamlessly through curb-side systems, sustaining revenue growth in the UV-Barrier Paper Packaging market.

Stringent regulations on photodegradable inks and dyes

New FDA interim safety rules for food-contact substances obligate converters to validate ink resistance against UV degradation to avoid chemical migration risks. Parallel European Parliament provisions narrow allowable dye classes in contact with food, pushing brands toward barrier papers that stabilize print layers. Suppliers offering proven UV-shielded surfaces gain an immediate compliance advantage. As certification timelines tighten, adoption of established barrier chemistries accelerates inside the UV-Barrier Paper Packaging market.

Premiumisation of nutraceutical and cosmetics formats

Higher disposable incomes and wellness awareness boost sales of supplements and premium skincare that require strict protection of active ingredients. Pharmaceuticals and nutraceuticals record the fastest 8.71% CAGR, using barrier cartons to preserve potency and signal brand quality. Research confirms lignin nanocomposites impart both UV defense and antioxidant activity, aligning with “clean label” narratives [1]Royal Society of Chemistry, “Overcoming Challenges of Lignin Nanoparticles,” pubs.rsc.org . Willingness to absorb higher material costs supports profitable growth across premium SKUs within the UV-Barrier Paper Packaging market.

Retailer shift to monomaterial solutions for curb-side recycling

European grocers and U.S. big-box chains stipulate monomaterial packaging to simplify consumer sorting. EU rules demand 70% recycling of all packs by 2030. WestRock reached 96% of its 2025 recyclability target by 2024 and now pivots investment to fiber-only alternatives. Converters that deliver UV barriers through coatings rather than laminates secure shelf access, cementing long-run demand in the UV-Barrier Paper Packaging market.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited heat-sealability of high-opacity papers | -0.4% | Global; heavily felt in flexible packaging | Short term (≤ 2 years) |

| Capital-intensive retro-fit of flexo/gravure lines | -0.3% | Regions with aging equipment | Medium term (2-4 years) |

| Volatility of TiO₂ pigment prices | -0.2% | Global | Short term (≤ 2 years) |

| Risk of over-specification vs. actual UV exposure profiles | -0.1% | Premium markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited heat-sealability of high-opacity papers

Opacity-boosting minerals undermine thermal bonding, limiting high-barrier paper use in pouches. TAPPI tests reveal declines in seal integrity as mineral filler ratios rise. [2]TAPPI, “Paper Industry Resources,” tappi.org Brands targeting liquids confront leak-risk trade-offs, delaying substitution and shaving growth from the UV-Barrier Paper Packaging market.

Capital-intensive retro-fit of flexo/gravure lines

Switching to dense barrier grades requires modified drying, ink and tension settings. Upgrades are valued at more than USD 1 million per line, restricting smaller converters’ entry. Larger integrated groups can amortize capex, entrenching competitive advantages in the UV-Barrier Paper Packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Type: Folding Cartons Sustain Premium Use‐Cases

Folding cartons accounted for 36.17% of the UV-Barrier Paper Packaging market in 2024, anchored in pharmaceuticals and prestige cosmetics where surface print quality and barrier reliability are critical. Cartonboard enables monomaterial compliance by embedding UV coatings directly on fiber, eliminating plastic films. Premium brands adopt embossed inserts and metallic inks to enhance shelf appeal without compromising recyclability.

Rapid pouch uptake at an 8.82% CAGR reflects e-commerce driven demand for lightweight, high-volume formats. Progress in seal-assist coatings and fiber orientation lifts seam strength, though heat-sealability remains a bottleneck for liquids. Sachets, wraps and sleeves round out flexible options, serving single-dose nutraceuticals and secondary protection for premium candles or fragrances. The UV-Barrier Paper Packaging market continues to migrate toward hybrid coating recipes that reconcile opacity with seal performance, gradually widening the addressable share of flexible lines.

By Barrier Technology: Bio-based Coatings Gather Momentum

Metallised films preserved 35.69% share of the UV-Barrier Paper Packaging market in 2024 due to proven light-block performance and mature cost curves. High vacuum-metallised layers still dominate pharmaceutical leaflets and OTC cartons.

Bio-based coatings, however, post the fastest 8.93% CAGR on the back of lignin nanoparticle pilots scaling across Nordic sites.[3]Stora Enso, “Interim Report January–March 2025,” storaenso.com Direct lignin use offers cost relief compared with monomer routes, while achieving acceptable gloss and oxygen-barrier metrics. TiO₂ and pigmented formulations face price spikes tied to mineral supply disruptions, underscoring the pivot to renewable chemistries. AlOx/SiOx nano-layers and hybrid stacks remain niche, reserved for nutraceutical powders that demand near-total UV extinction.

By Paper Grade: Specialty Barrier Sheets Capture Value Upside

Bleached packaging paper held 31.25% share of the UV-Barrier Paper Packaging market size in 2024 thanks to FDA food-contact clearance and consistent print surfaces. The grade remains ubiquitous in frozen foods, dairy sticks and confectionery wraps.

Specialty barrier papers deliver the highest 8.64% CAGR, commanding price premiums through engineered porosity, tailored fiber orientation and coating-receptive surfaces. Producers invest in pilot calenders and blade coaters to fine-tune surface energy for lignin dispersion. Kraft variants maintain appeal in hardware wraps where UV protection prevents pigmentation fade of metal fasteners, while recycled board grows selectively as mills improve brightness and reduce odor.

By End-user Industry: Pharmaceuticals Accelerate

Food & beverage represented 39.76% of the UV-Barrier Paper Packaging market in 2024 as ambient grocery channels expand. UV barriers mitigate vitamin oxidation in fruit purées and stabilize colors in plant-based beverages shipped via parcel networks.

Pharmaceuticals and nutraceuticals are projected to increase at an 8.71% CAGR. Regulatory filings now require package-mediated photostability data, favoring validated barrier substrates. Active nutraceutical sachets exploit lignin’s antimicrobial traits to extend shelf life without additional preservatives. Cosmetics and personal care deploy barrier sleeves that guard formulations rich in retinol or natural pigments from photolysis, sustaining demand beyond core healthcare.

Geography Analysis

Europe’s early embrace of recycled-content mandates anchors the region as the policy benchmark, drawing investments into Finnish, German and Spanish mills upgrading to bio-based coatings. Retail chains across France and the Nordics enforce fiber-only shelf requirements, pushing rapid substitution of metalized PET laminates.

Asia-Pacific’s populous consumer base and rising purchasing power spark new demand nodes. Chinese nutraceutical brands package antioxidant tea extracts in high-gloss UV-barrier cartons to reinforce premium cues. Indian personal-care players pivot from opaque PE bottles to paper pouches, leveraging improved lignin-based seal coatings to withstand humid climates.

North America leverages consolidated supply networks of Smurfit WestRock and International Paper to diffuse barrier innovations quickly. The continent’s stringent FDA oversight accelerates commercialization of PFAS-free UV coatings, setting export standards adopted by Latin American co-packers. Middle East & Africa trail in adoption but import UV-barrier sachets for nutrient-dense powdered dairy, hinting at future regional investment.

Competitive Landscape

The UV-Barrier Paper Packaging market shows moderate concentration as newly merged giants integrate board mills, barrier-coating assets and converting plants to serve global FMCG and pharma accounts. International Paper-DS Smith pairs North American kraft supply with European carton converting depth, unlocking cross-regional synergies in bio-based barriers. Smurfit WestRock deploys 459 converting sites that can amortize capital for line retrofits more swiftly than regional independents.

Mondi’s USD 1.3 billion capex program funnels into mono-material projects, including heat-seal assist coatings that resolve opacity-sealability tension. Stora Enso commits EUR 1 billion to a Finnish consumer board line optimized for lignin dispersion layers, aiming to halve fossil-based barrier volumes by 2028.

Specialty challengers such as Finnish nanoparticle start-ups license lignin formulations to mid-tier Asian mills, threatening to erode metallised incumbency in the long run. Equipment vendors market modular plasma coater retrofits that lower the cost hurdle for converters under 10 kt annual throughput, fostering ecosystem dynamism within the UV-Barrier Paper Packaging market.

UV-Barrier Paper Packaging Industry Leaders

Mondi Group

Smurfit Westrock plc

Nippon Paper Industries

International Paper

Stora Enso Oyj

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: International Paper finalised its merger with DS Smith, forming a trans-Atlantic fiber-based packaging leader.

- March 2025: UPM Communication Papers announced the permanent closure of its Ettringen mill to concentrate on profitable specialty grades.

- February 2025: Stora Enso reported 9% Q1 sales growth and confirmed commissioning of its Oulu consumer-board line by 2027.

- January 2025: FDA revoked 35 PFAS food-contact approvals, prompting reformulation of grease-resistant and UV-barrier coatings.

Global UV-Barrier Paper Packaging Market Report Scope

| Pouches |

| Sachets |

| Wraps and Overwraps |

| Folding Cartons |

| Labels and Sleeves |

| Others |

| Metallised Coatings |

| TiO₂ / Pigmented UV-Block Coatings |

| AlOx / SiOx Laminations |

| Bio-based Coatings |

| Hybrid and Multi-layer |

| Kraft Paper |

| Bleached Packaging Paper |

| Recycled Paperboard |

| Specialty Barrier Paper |

| Food and Beverage |

| Cosmetics and Personal Care |

| Pharmaceuticals and Nutraceuticals |

| Industrial and Chemical |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Thailand | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | GCC |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Packaging Type | Pouches | ||

| Sachets | |||

| Wraps and Overwraps | |||

| Folding Cartons | |||

| Labels and Sleeves | |||

| Others | |||

| By Barrier Technology | Metallised Coatings | ||

| TiO₂ / Pigmented UV-Block Coatings | |||

| AlOx / SiOx Laminations | |||

| Bio-based Coatings | |||

| Hybrid and Multi-layer | |||

| By Paper Grade | Kraft Paper | ||

| Bleached Packaging Paper | |||

| Recycled Paperboard | |||

| Specialty Barrier Paper | |||

| By End-user Industry | Food and Beverage | ||

| Cosmetics and Personal Care | |||

| Pharmaceuticals and Nutraceuticals | |||

| Industrial and Chemical | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| France | |||

| United Kingdom | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Thailand | |||

| Indonesia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | GCC | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current UV-Barrier Paper Packaging market size?

The UV-Barrier Paper Packaging market size totaled USD 5.13 billion in 2025.

How fast will the UV-Barrier Paper Packaging market grow?

A 7.78% CAGR is projected from 2025 to 2030.

Which packaging type holds the largest share?

Folding cartons led with 36.17% share in 2024.

Which region will grow the quickest?

Asia-Pacific is expected to post a 9.05% CAGR through 2030.

Why are bio-based coatings gaining ground?

Lignin nanoparticles offer recyclable UV protection, aligning with EU and FDA rules that phase out PFAS and non-recyclable laminates.

What restrains adoption of high-opacity paper pouches?

Reduced heat-sealability demands added coating innovations and costly line retrofits, slowing flexible conversion rates.

Page last updated on: