Low Carbon Paper Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

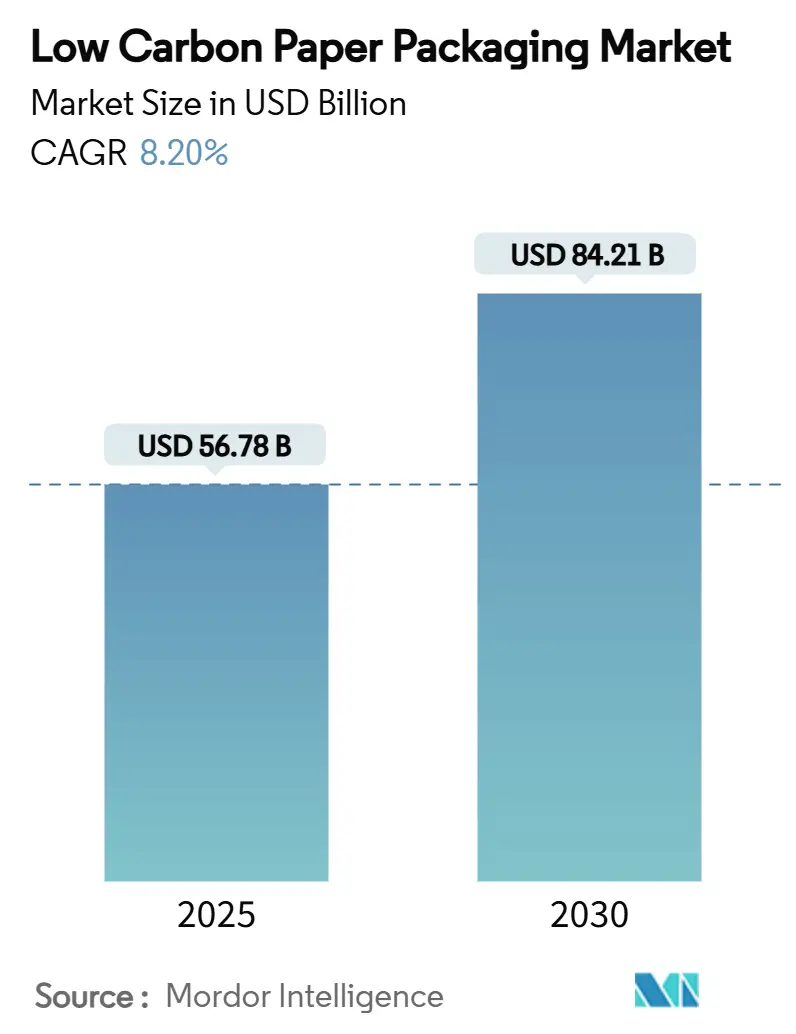

| Market Size (2025) | USD 56.78 Billion |

| Market Size (2030) | USD 84.21 Billion |

| Growth Rate (2025 - 2030) | 8.20% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Low Carbon Paper Packaging Market Analysis by Mordor Intelligence

The low carbon paper packaging market size is USD 56.78 billion in 2025 and is forecast to reach USD 84.21 billion by 2030 at an 8.20% CAGR, underscoring the rapid pivot from petroleum-based substrates to renewable fiber platforms that comply with emerging regulatory mandates.[1]European Commission, “Regulation – EU – 2025/40,” EUROPA.EU Policy momentum, particularly the European Union’s 100%-recyclable packaging requirement effective 2028, is steering procurement toward fiber solutions certified for end-of-life recovery. Brand owners in fast-moving consumer goods (FMCG) are accelerating plastic-to-paper substitution programs that guarantee long-run order volumes for converters. Corrugated formats dominate thanks to their automation compatibility, yet molded fiber designs are scaling quickly as breakthrough dry-forming technology cuts water use by 60% and adds structural strength. Meanwhile, recycled fiber’s cost parity with virgin plastics inside European Union Emissions Trading System (EU ETS) jurisdictions removes the historical price premium barrier and amplifies demand signals across global supply chains.

Key Report Takeaways

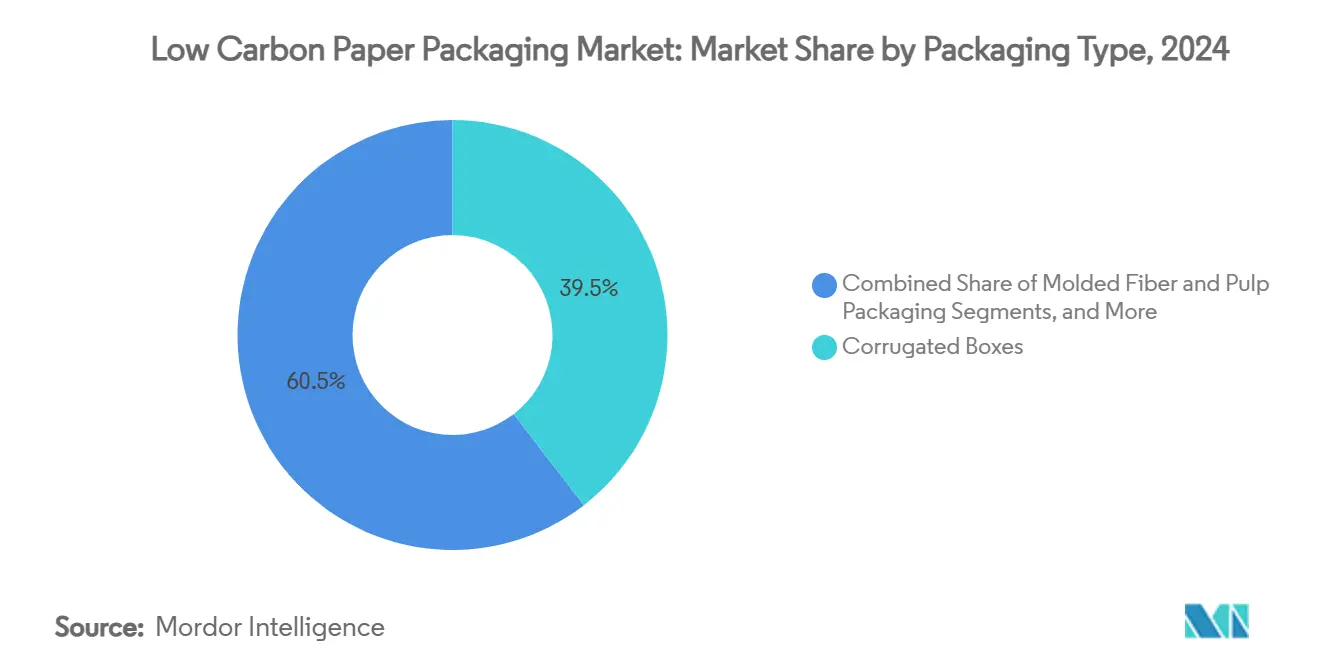

- By packaging type, the low-carbon paper packaging market size for molded fiber and pulp packaging segment is projected to grow at a 9.34% CAGR between 2025-2030.

- By source of fiber, recycled content captured a 57.48% of the low-carbon paper packaging market share in 2024.

- By end-use, the low-carbon paper packaging market size for the e-commerce and retail segment is projected to grow at a 9.83% CAGR between 2025-2030.

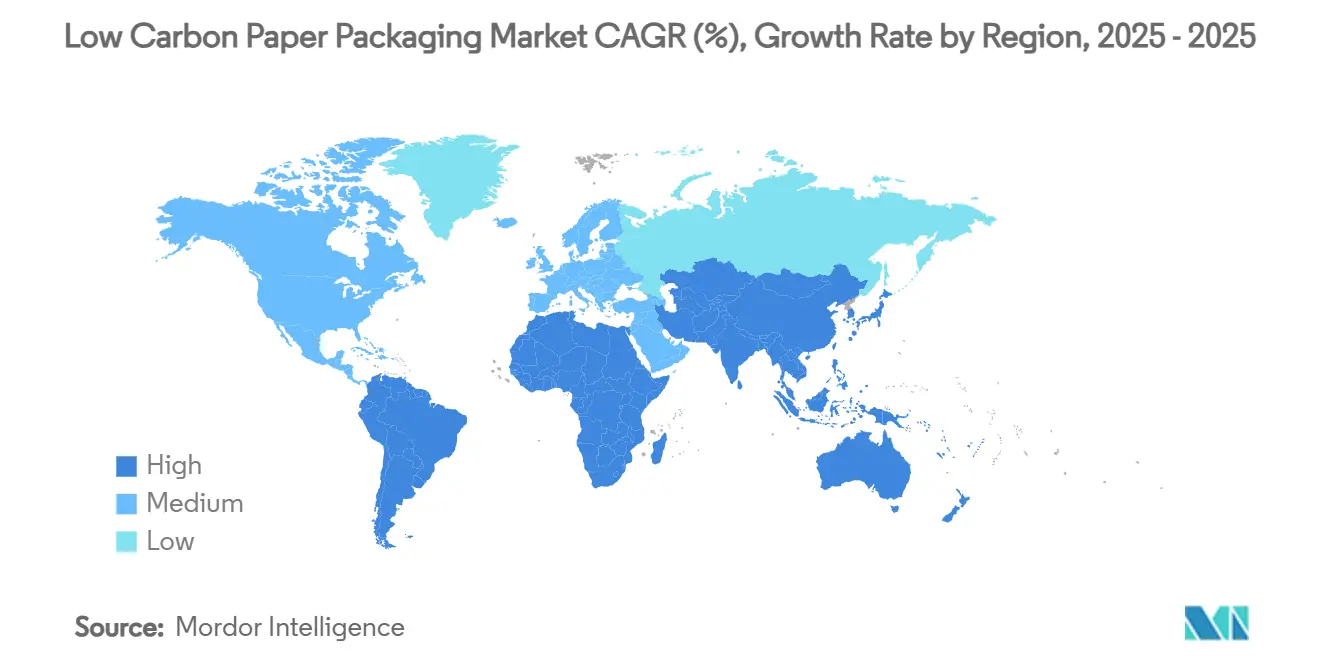

- By region, Europe captured a 31.92% of the low-carbon paper packaging market share in 2024.

Global Low Carbon Paper Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in e-commerce corrugated demand | +1.8% | Global, with concentration in North America and Asia-Pacific | Short term (≤ 2 years) |

| FMCG brand plastic-to-paper substitution mandates | +1.5% | Global, led by Europe and North America | Medium term (2-4 years) |

| Regulatory push for carbon-neutral materials | +2.1% | Europe and North America, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Cost parity reached with virgin plastics in EU ETS markets | +1.2% | Europe, with spillover to other carbon pricing jurisdictions | Medium term (2-4 years) |

| Retailer shift to “frustration-free” fiber packaging | +0.9% | North America and Europe, expanding globally | Short term (≤ 2 years) |

| Agro-residue fiber breakthroughs (bagasse, straw) | +0.7% | Asia-Pacific and emerging markets with agricultural waste | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in E-commerce Corrugated Demand

Global e-commerce fulfillment centers increasingly require packaging that travels through automated sorters without damage while reinforcing brand identity at the doorstep. Packaging Corporation of America posted an 11.1% year-on-year rise in corrugated shipments for Q3 2024, citing record demand from online channels. Amazon’s frustration-free packaging rules, now widely adopted by major retailers, favor right-sized fiber boxes over plastic mailers and enforce detailed design guidelines on strength-to-weight ratios. The requirement for smaller, more frequent shipments raises per-unit board intensity, boosting volumes even in flat finished-goods markets. Digital printing upgrades let converters personalize boxes at production speed, adding marketing value without compromising recyclability. Corrugated’s established curbside recovery network further differentiates it from plastic alternatives under tightening Extended Producer Responsibility (EPR) fee schedules.

FMCG Brand Plastic-to-Paper Substitution Mandates

Multinational consumer-goods firms have adopted binding targets that phase out virgin petroleum plastics, guaranteeing medium-term demand for fiber packaging. Procter & Gamble aims to reach net-zero emissions by 2040 with explicit milestones to reduce virgin plastic, while Coca-Cola commits to 100% recyclable packaging by 2025 and 50% recycled content by 2030.[2]The Coca-Cola Company, “2023 Environmental Update,” COCACOLA.COM Contracts increasingly specify post-consumer recycled (PCR) fiber, supporting converters’ capital investments in recycling capacity. Tata Consumer Products’ pledge for 100% recyclable, compostable, or reusable packaging by 2030 illustrates similar traction in emerging markets. Collaborative innovations such as the Boardio paperboard canister—developed by Graphic Packaging and Mother Parkers—slash plastic usage by 50% while preserving barrier integrity, setting benchmarks for cross-industry uptake.

Regulatory Push for Carbon-Neutral Materials

Government policy frameworks embed carbon accounting into packaging compliance, shifting low-carbon formats from voluntary to compulsory. The EU Packaging and Packaging Waste Regulation makes 100% recyclability mandatory by 2028 and aligns EPR fees with greenhouse-gas intensity, directly monetizing carbon savings. New Jersey’s recycled-content law already obliges 40% PCR in paper carryout bags, a model other U.S. states are evaluating. Australia’s draft reforms propose EPR schemes and minimum recycled thresholds, strengthening Asia-Pacific momentum. The United Kingdom’s updated EPR blueprint similarly ties fee modulation to carbon efficiency, rewarding converters with proven low-carbon footprints. Collectively, these policies generate predictable, jurisdiction-wide demand curves for renewable fiber substrates.

Cost Parity Reached with Virgin Plastics in EU ETS Markets

Rising carbon allowance prices under the EU ETS now offset the historical cost gap between recycled paperboard and virgin polyolefins. The International Monetary Fund notes that cross-border carbon taxes could erode the competitiveness of high-emission packaging exports, amplifying incentives for paper formats. Billerud reports its Scandinavian board mills will remain 98% fossil-free when EU carbon taxation on mill emissions begins in 2026, reinforcing its cost advantage. Life-cycle studies from the Fibre Box Association show corrugated greenhouse-gas intensity fell 50% between 2006 and 2020, compounding the economic crossover when carbon levies are factored. As a result, brands purchasing bulk secondary packaging meet both cost and compliance objectives by specifying recycled paperboard.

Restraints Impact Analysis*

| Restraint | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile OCC (old corrugated container) pricing | -0.8% | Global, with particular impact in North America and Europe | Short term (≤ 2 years) |

| Limited barrier-coating recyclability infrastructure | -0.6% | Global, with infrastructure gaps in emerging markets | Medium term (2-4 years) |

| Water-intensive pulping footprint in water-stressed regions | -0.4% | Water-stressed regions globally, particularly Middle East and parts of Asia | Long term (≥ 4 years) |

| Brand risk from “greenwashing” claims scrutiny | -0.3% | Global, with heightened scrutiny in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile OCC (Old Corrugated Container) Pricing

Fluctuating prices for recovered paper undermine budget certainty for converters negotiating multi-year supply contracts. The U.S. Producer Price Index for corrugated recyclables shows pronounced swings linked to export policy shifts and seasonal collection patterns. July 2024 U.S. countervailing duties on Chinese and Indian paper bags illustrate how trade measures can disrupt supply chains and inflate input costs. Small-to-mid converters lacking hedging tools face margin compression that delays capital spending on sustainable innovation. Variability in OCC quality due to contamination further complicates cost modeling, prompting some brands to retain plastics where price predictability is paramount.

Limited Barrier-Coating Recyclability Infrastructure

High-performance paper often relies on polymer or silicone coatings that most municipal facilities cannot separate, reducing actual recyclability despite material claims. Specialized plants such as Sustana’s Wisconsin unit accept coated liners but remain few, leaving gaps that attract higher EPR fees in several jurisdictions. Research into on-site dry defibration cuts greenhouse-gas emissions by 50% but requires capital scale yet to materialize beyond pilots. As regulators tighten definitions around “recyclable,” coated formats risk reclassification as non-compliant, squeezing high-barrier applications such as frozen foods unless infrastructure rapidly expands.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Type: Corrugated Platforms Sustain Volume Leadership

The corrugated box category held 39.53% of low carbon paper packaging market share in 2024, reflecting widespread utility in e-commerce, industrial, and produce shipping. Corrugated’s mature recycling loops and high stacking strength sustain its value proposition even as material light-weighting progresses. The low carbon paper packaging market size for corrugated formats is forecast to expand in line with e-commerce’s 9.83% CAGR, supported by investments such as Packaging Corporation of America’s USD 221 million quarterly net income reinvested in board machines.[3]Packaging Corporation of America, “Q4 2024 Results,” PACKAGINGCORP.COM Folding cartons remain entrenched in pharmaceuticals and premium personal-care, while paper bags and sacks gain traction in supermarkets responding to single-use plastic bag bans. Specialty wrapping papers grow within quick-service restaurants that need grease-resistant yet recyclable wraps, though digital media curtails legacy print papers.

Molded fiber and pulp products represent the fastest-growing format with a 9.34% CAGR through 2030. Stora Enso’s Skene plant—the world’s largest dry-forming line—demonstrates commercial viability by slashing water consumption and enabling high-precision molding for electronics and cosmetics trays. Adoption by consumer-electronics brands seeking to replace expanded polystyrene bolsters demand. Converters are pairing polymer-free barrier chemistries with molded fiber to unlock frozen-food and liquid applications, though recyclability of barriers remains a limiting factor. Overall, converters are shifting from commodity board production toward specialized, high-margin engineered fiber substrates tailored to end-use requirements.

By Source of Fiber: Circularity Favours Recycled Streams

Recycled pulp supplied 57.48% of low carbon paper packaging market size in 2024, largely because collection systems in Europe and North America deliver steady inflows that lower capital outlays and energy use compared with virgin pulping. Recovered fiber’s greenhouse-gas profile and cost competitiveness under carbon pricing make it the default feedstock in policy-driven procurement contracts. Virgin pulp is still required for strength-critical or direct-food-contact applications where purity standards are stringent. Hybrid recipes—combining fresh and recovered fibers—optimize stiffness while maintaining recycled-content thresholds for EPR fee reductions.

Agro-residue fiber, led by bagasse and straw, is projected to grow at 9.45% CAGR, reflecting technology gains that tackle silica content, odor, and variability. Sodium-carbonate pulping of wheat straw offers European mills relief from tight recycled-paper markets, whereas sugarcane bagasse in India and Brazil provides co-location benefits between sugar mills and molded-fiber operations. Strength data from maize-straw-bagasse bioplastic film experiments show tensile values of 3.8 MPa and water absorption of 33%, comparable to entry-level tray applications. As agricultural supply chains monetize waste, farmers secure an additional revenue stream, and packaging producers diversify feedstock risk.

By End-Use Industry: E-Commerce Reconfigures Design Priorities

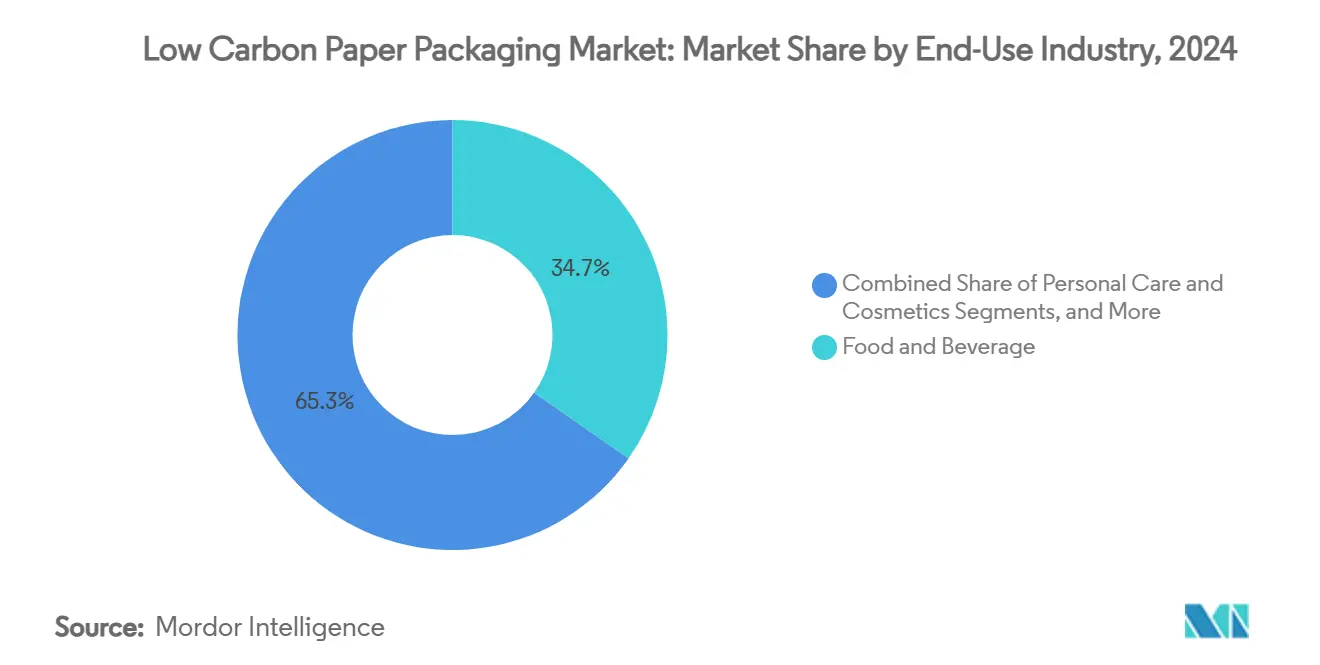

Food and beverage captured 34.74% low carbon paper packaging market share in 2024 via regulatory tailwinds banning single-use plastics in food service across the EU and several U.S. states. Brands value fiber’s printability for on-shelf communication and compliance with migration limits for direct contact. Barrier-coated papers and wet-strength boards find uptake in chilled and frozen segments, though recyclability infrastructure remains a hurdle.

E-commerce and retail represent the fastest-growing demand base at 9.83% CAGR. The low carbon paper packaging market size for this segment benefits from retailer mandates that packages arrive damage-free, right-sized, and curbside-recyclable. Amazon’s hundreds of packaging engineers collaborate with converters to redesign ship-in-own-container solutions, driving board grade diversification. Personal care and cosmetics use molded fiber inserts and premium folding cartons for brand enhancement, whereas consumer electronics adopt molded fiber cushions to replace foamed plastics.

Healthcare and pharmaceuticals adopt traceable packaging certified for chain-of-custody to comply with serialization laws. Industrial goods shift to heavier single-wall corrugated grades as cost-effective substitutes for multi-wall plastics. Cross-sector convergence on recyclability and carbon metrics enables converters to repurpose material innovations across multiple categories.

Geography Analysis

Europe remains the global epicenter, accounting for 31.92% of low carbon paper packaging market share in 2024, underpinned by the EU directive mandating 100% recyclable packaging by 2028. Investments such as Metsä Group’s scale-up to 600,000 tonnes of folding boxboard and Stora Enso’s dry-forming expansion reinforce the region’s technological authority. Carbon-adjusted EPR fees narrow price gaps between sustainable formats and plastics, so brand owners adopt fiber solutions not only for compliance but also to avoid rising levies. The policy environment also standardizes technical specifications, enabling converters to rapidly export proven designs to other regulated markets.

Asia-Pacific delivers the highest growth at 9.71% CAGR through 2030. China’s domestic consumption surge aligns with export customers’ low-carbon requirements, prompting Nine Dragons Paper to install high-speed recycled board machines. Japan’s Nippon Paper Industries targets a 54% greenhouse-gas reduction from 2013 baselines, integrating molded fiber into its daily-life products portfolio. India leverages abundant sugarcane bagasse, with pilot plants demonstrating tableware production that meets municipal composting standards. Regional regulators are drafting plastic-waste legislation mirroring EU templates, providing clear commercialization pathways for agro-residue fiber.

North America retains a strong foothold through entrenched corrugated infrastructure and robust e-commerce penetration. International Paper dedicates USD 100 million to modernize U.S. box plants, while Billerud invests USD 114 million to optimize Michigan and Wisconsin board mills. State-level recycled-content mandates, such as New Jersey’s 40% PCR requirement, foreshadow broader U.S. adoption. Canada’s forthcoming federal plastics ban is expected to divert additional volume toward fiber formats. The continent’s vast forest resource base and high per-capita box consumption sustain steady growth even without Europe-style regulatory acceleration.

Competitive Landscape

The low carbon paper packaging industry features moderate consolidation, with the top five companies controlling roughly 45% of global capacity. Vertical integration—spanning fiber sourcing, pulping, and converting—gives incumbents cost control and carbon-accounting transparency. International Paper focuses on containerboard debottlenecking to secure corrugated feedstock, while Graphic Packaging rationalizes assets, selling its Augusta paperboard mill to Clearwater for USD 700 million to fund recycled-board capacity upgrades. Stora Enso and Metsä leverage Scandinavian access to certified forests and renewable energy, promoting near-fossil-free board portfolios.

Innovation pipelines increasingly revolve around fiber-based replacements for plastic pouches, trays, and barrier cartons. Graphic Packaging filed over 100 patents in 2023, many addressing coating recyclability or fiber cannister structures. White-space entrants such as dry-forming technology startups and agro-fiber processors are attracting venture capital, suggesting potential disruption in niche segments. However, EPR compliance costs and carbon disclosure requirements create barriers to entry, favoring scale players that can amortize auditing, certification, and research expenses.

Brand-converter collaboration is pivotal. The Mother Parkers-Graphic Packaging Boardio project illustrates co-development models wherein converters share technical risk while securing long-term volumes. Similarly, electronics OEMs engage molded-fiber specialists to design protective inserts that outperform expanded polystyrene on drop tests. The shifting basis of competition—from price-per-ton to verified carbon intensity—means converters with auditable data platforms will command premium margins.

Low Carbon Paper Packaging Industry Leaders

Stora Enso Oyj

Nine Dragons Paper (Holdings) Limited

International Paper Company

Mondi PLC

Smurfit Westrock PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: European Union implements Packaging and Packaging Waste Regulation mandating 100% recyclable packaging by 2028 and introducing EPR fee modulation that favors low-carbon materials.

- January 2025: Packaging Corporation of America posts Q4 2024 net income of USD 221 million, citing a 9.1% rise in corrugated shipments on sustained e-commerce demand.

- August 2024: Graphic Packaging International pledges net-zero emissions by 2050 and reports replacing 450 million plastic packages and 665 million foam cups with paper alternatives in 2023.

- January 2024: New Jersey enforces a recycled-content statute requiring 40% PCR in paper carryout bags, with annual certification reports due July 2025.

Global Low Carbon Paper Packaging Market Report Scope

| Corrugated Boxes |

| Folding Cartons |

| Paper Bags and Sacks |

| Wrapping and Specialty Papers |

| Molded Fiber and Pulp Packaging |

| Other Innovative Formats |

| Virgin Fiber |

| Recycled Fiber |

| Hybrid / Mixed Fiber |

| Agro-Residue Fiber |

| Certified Sustainable Fiber |

| Food and Beverage |

| Personal Care and Cosmetics |

| Healthcare and Pharma |

| Consumer Electronics |

| E-commerce and Retail |

| Industrial and Bulk Goods |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Packaging Type | Corrugated Boxes | ||

| Folding Cartons | |||

| Paper Bags and Sacks | |||

| Wrapping and Specialty Papers | |||

| Molded Fiber and Pulp Packaging | |||

| Other Innovative Formats | |||

| By Source of Fiber | Virgin Fiber | ||

| Recycled Fiber | |||

| Hybrid / Mixed Fiber | |||

| Agro-Residue Fiber | |||

| Certified Sustainable Fiber | |||

| By End-use Industry | Food and Beverage | ||

| Personal Care and Cosmetics | |||

| Healthcare and Pharma | |||

| Consumer Electronics | |||

| E-commerce and Retail | |||

| Industrial and Bulk Goods | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the low carbon paper packaging market?

The low carbon paper packaging market size is USD 56.78 billion in 2025 and is projected to reach USD 84.21 billion by 2030.

Which region leads in market share for low carbon paper packaging?

Europe leads with 31.92% market share in 2024 due to stringent recyclable-packaging mandates and carbon pricing mechanisms.

Which packaging type is growing the fastest?

Molded fiber and pulp packaging is forecast to grow at a 9.34% CAGR through 2030, driven by water-saving dry-forming technology.

How important is recycled fiber in the market?

Recycled fiber accounts for 57.48% of the market in 2024, benefiting from established collection systems and cost competitiveness under carbon regulations.

What is driving demand in the e-commerce sector?

Online retailers’ frustration-free packaging standards demand right-sized, curbside-recyclable corrugated boxes, fueling a 9.83% CAGR in e-commerce and retail applications.

Page last updated on: