Silicone-Free Water-Resistant Paper Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

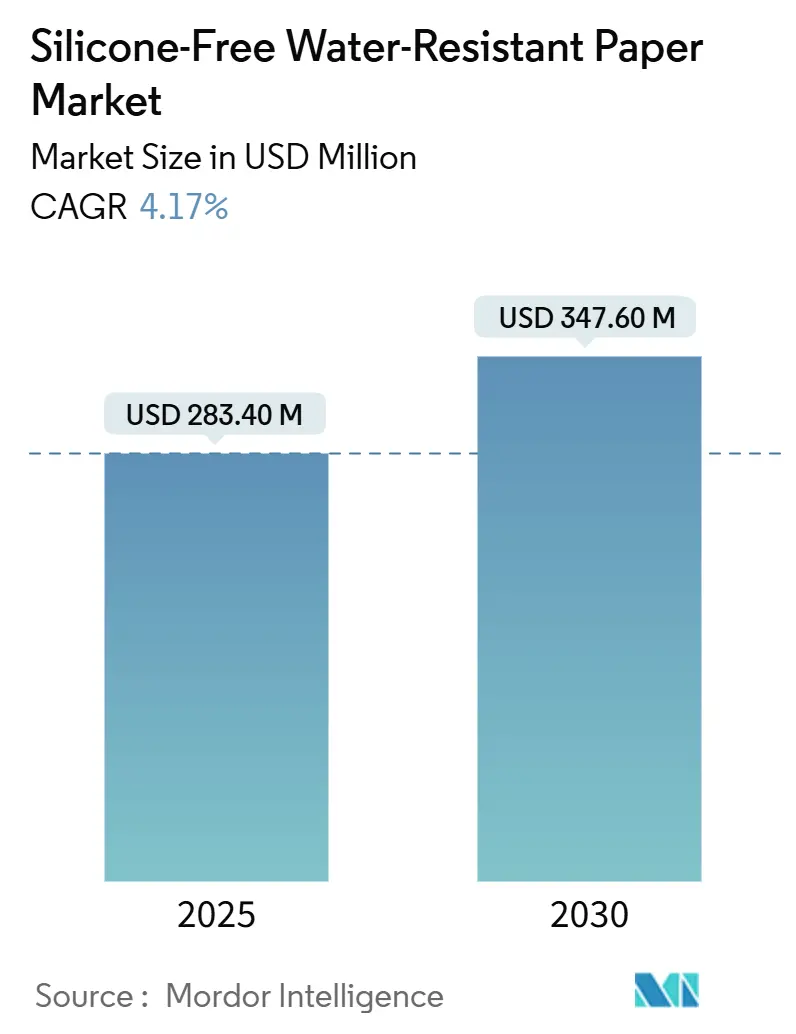

| Market Size (2025) | USD 283.40 Million |

| Market Size (2030) | USD 347.60 Million |

| Growth Rate (2025 - 2030) | 4.17% CAGR |

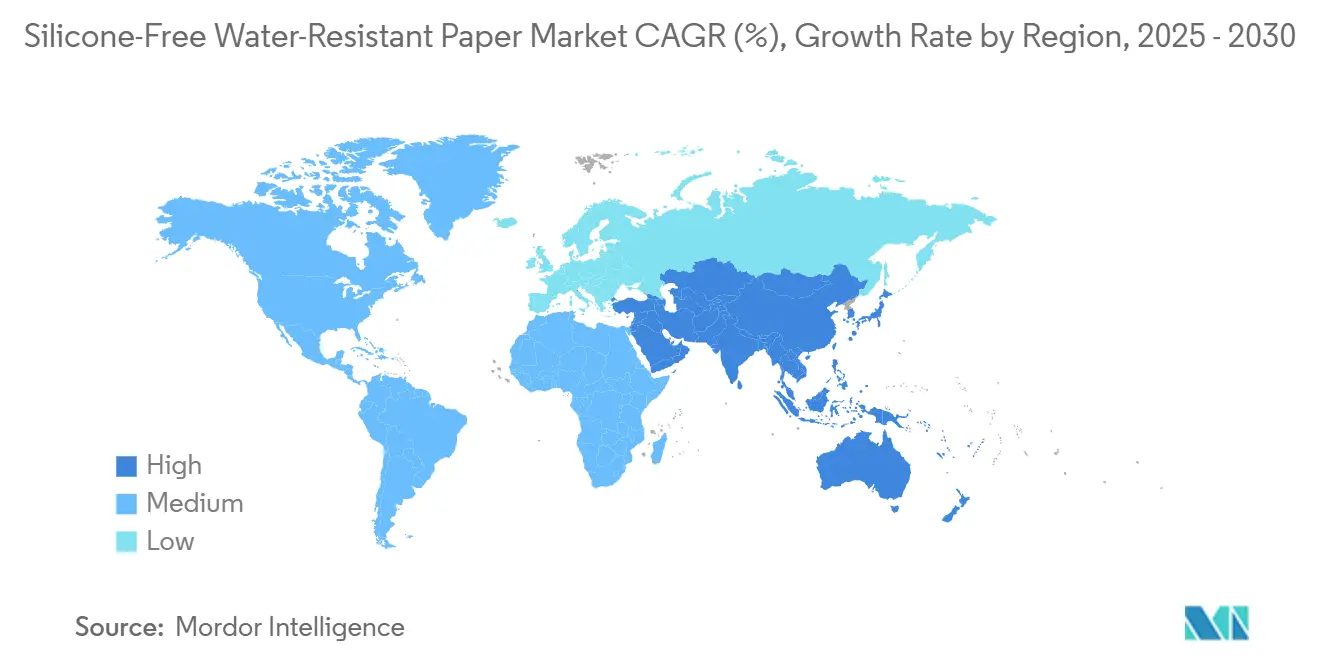

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Silicone-Free Water-Resistant Paper Market Analysis by Mordor Intelligence

The silicone-free water resistant paper market size stands at USD 283.4 million in 2025 and is forecast to reach USD 347.6 million in 2030, reflecting a CAGR of 4.17% over the period. Demand scales quickly as brand owners replace PFAS-based coatings, invest in dispersion and biopolymer barriers, and re-engineer supply chains to satisfy new import regulations and extended-producer-responsibility rules. [1]U.S. Food and Drug Administration, “FDA Determines Authorization for 35 Food Contact Notifications Related to PFAS Are No Longer Effective,” fda.gov Dispersion-coated grades retain cost advantages and wide converting compatibility, yet barrier technology diversification accelerates as hydrogen-peroxide-sterilizable papers gain traction in medical packaging and mono-material mailers grow in e-commerce logistics. Asia-Pacific commands almost half of global consumption because of its large converting base and low-cost operations, whereas Middle East and Africa posts the fastest growth as multinationals build greenfield plants and governments harmonize food-contact laws with EU norms. Strategic projects by Mondi, LINTEC, and Stora Enso underline a shift toward vertical integration, scale economics, and proprietary chemistries that lock in end-user relationships amid tightening regulatory timelines.

Key Report Takeaways

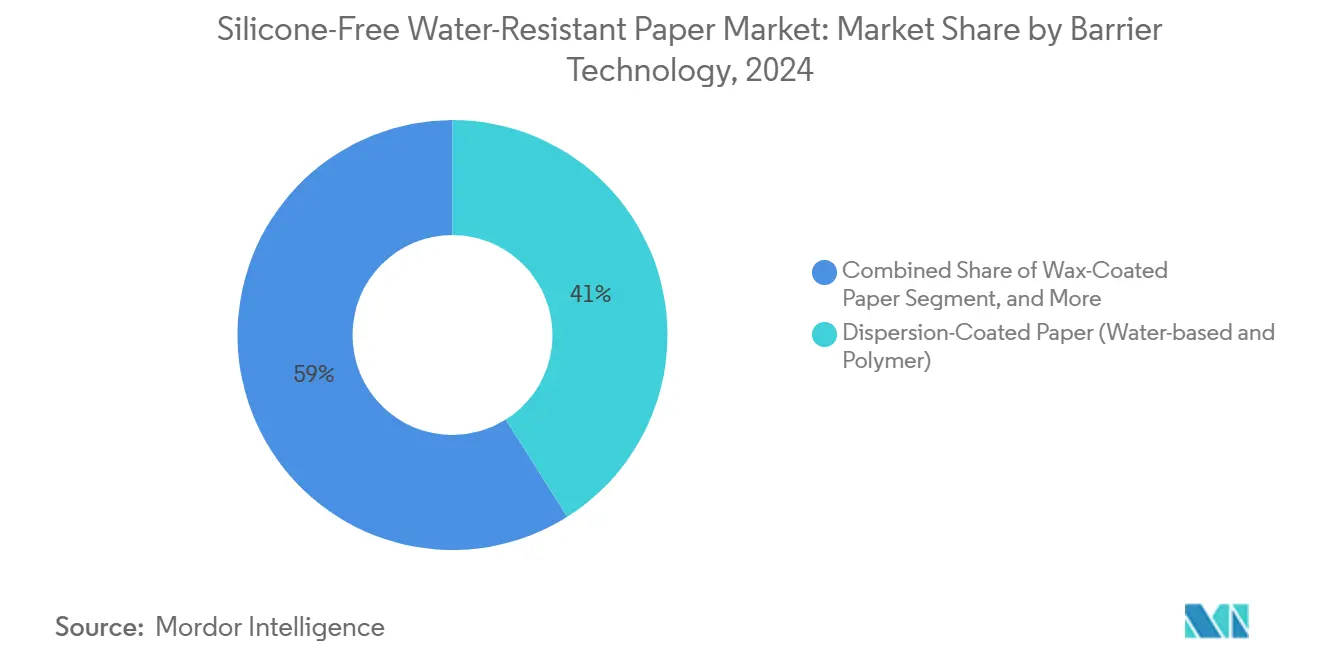

- By barrier technology, dispersion-coated paper captured 41.04% of silicone-free water resistant paper market share in 2024.

- By end-use industry, the silicone-free water resistant paper market size for healthcare and pharmaceuticals packaging segment is projected to expand at a 5.67% CAGR between 2025-2030.

- By geography, Asia-Pacific region held 46.72% of the silicone-free water resistant paper market share in 2024.

Global Silicone-Free Water-Resistant Paper Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift to PFAS-free fluorochemical alternatives | +1.2% | Global, early adoption in North America and EU | Medium term (2-4 years) |

| E-commerce demand for moisture-proof fiber mailers | +0.8% | Global, concentrated in North America and APAC | Short term (≤ 2 years) |

| Food-contact compliance driving polymer-free coatings | +0.6% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| Growth of H₂O₂-sterilizable paper in aseptic packaging | +0.5% | Global, healthcare hubs leading adoption | Long term (≥ 4 years) |

| Craft-beverage boom for wet-strength label stock | +0.4% | North America and EU, emerging in APAC | Short term (≤ 2 years) |

| Circular fiber flexible-packaging initiatives | +0.3% | EU leading, spillover to North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift to PFAS-free Fluorochemical Alternatives

Total removal of PFAS grease-proofing agents under the EPA December 2024 TSCA revision and the FDA March 2025 revocation compels converters to rebuild coating lines, recalibrate quality systems, and qualify dispersion or biopolymer barriers that meet rigorous oil-resistance tests. [2]Federal Register, “Updates to New Chemicals Regulations Under TSCA,” federalregister.gov European mills gained first-mover advantage after earlier REACH actions, whereas Asian suppliers navigate staggered national rules, generating temporary cost asymmetries in global trade flows.

E-commerce Demand for Moisture-proof Fiber Mailers

Parcel volumes rise sharply as cross-border online retail expands, pushing brand owners to replace plastic mailers with fiber formats that survive humidity swings, long transport cycles, and drop impacts. Dispersion-coated and cross-linked PVOH papers meet performance targets while remaining curbside recyclable, yet price differentials versus commodity plastic mailers still constrain penetration outside premium sectors.

Food-contact Compliance Driving Polymer-free Coatings

Strict extractives limits in 21 CFR 176.170 shift purchasing preferences toward mineral-based or natural-polymer coatings that eliminate residual monomer risk for fatty or aqueous foods. Wax blends and cellulose derivatives gain share in chilled bakery wraps and quick-service clamshells where brand owners prioritize consumer safety credentials over incremental costs.

Growth of H₂O₂-Sterilizable Paper in Aseptic Packaging

Sterile barrier systems for syringes, catheters, and diagnostic kits require papers that withstand hydrogen-peroxide vapor without barrier degradation. Cross-linked PVOH and starch-PVOH hybrids show robust performance, maintaining sub-0.1 g/m²·day WVTR after multiple sterilization cycles while meeting ISO 11607-1 tensile and burst requirements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PFAS regulatory clamp-down on legacy coatings | −0.7% | Global, immediate impact in North America and EU | Short term (≤ 2 years) |

| Limited heat-sealability vs. plastic films | −0.5% | Global, especially flexible packaging | Medium term (2-4 years) |

| High CAPEX for curtain-coating retrofits | −0.4% | Global, greater burden on smaller manufacturers | Medium term (2-4 years) |

| Recycling contamination from multilayer laminates | −0.3% | EU and North America, expanding to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

PFAS Regulatory Clamp-down on Legacy Coatings

The June 30 2025 depletion deadline forces converters to exhaust or scrap PFAS-laden inventory. Specialty microwave grease-proof wraps risk temporary shortages as replacement chemistries still await full-scale qualification, creating a drag on near-term volume expansion.

Limited Heat-sealability vs. Plastic Films

Paper lacks the melt-flow behavior of polyethylene; hence hermetic seals rely on dispersion or hot-melt tie layers that may undermine barrier continuity or recyclability. Liquid pouches and portion-control sachets therefore maintain a partial dependency on plastic films, slowing share gains for paper-only formats.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Barrier Technology Biopolymers Narrow the Performance Gap

The silicone-free water resistant paper market size attributed to dispersion-coated grades reached USD 116.3 million in 2024, equal to 41.04% of global revenue. Competitive price points, low coat-weights, and well-understood recycle behavior keep dispersion systems in pole position; however, policy-driven preference for bio-sourced ingredients channels R&D toward starch and PVOH hybrids that now underpin a 6.48% CAGR through 2030.

Emerging formulations cross-linked with boric acid cut oxygen permeability by up to 92% while preserving compostability, enabling snack bars and dried fruit packs to shift away from fluorochemicals without shelf-life trade-offs. [3]Royal Society of Chemistry, “Boric acid-crosslinked poly(vinyl alcohol),” rsc.org Wax-coated grades defend legacy niches in cheese wraps and ice cream cartons though they contend with oil migration limits and consumer backlash against mineral-oil content. Laminated PE/PP-free constructs using heat-reactive dispersions address curbside recycling aims but need further scale to match incumbent cost benchmarks.

By End-Use Industry Healthcare Outpaces Food Packaging

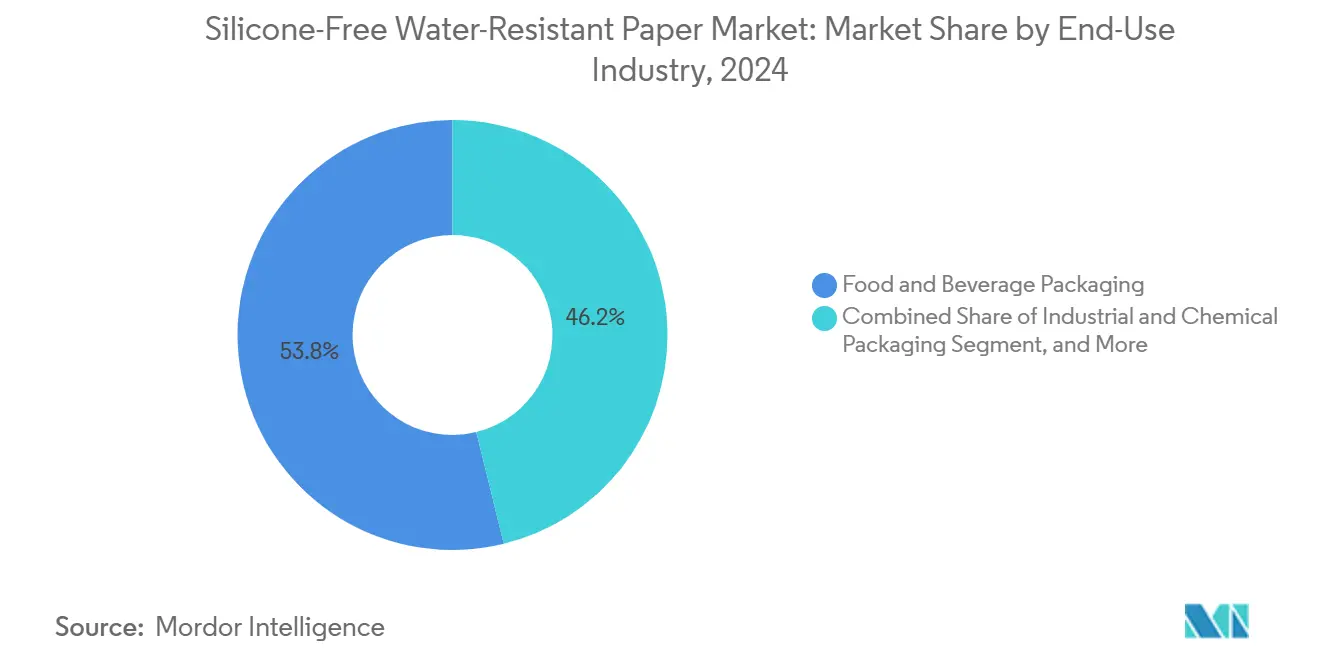

Food and beverage held 53.83% silicone-free water resistant paper market share in 2024 on the back of quick-service restaurant wraps, bakery interleavers, and craft-beer label stock. Growth moderates because brand owners juggle barrier, cost, and recyclability trade-offs amid ongoing substrate trials.

Healthcare and pharmaceuticals advance at a 5.67% CAGR as sterile barrier pouches, SOP compliance paperwork, and blister outserts migrate to hydrogen-peroxide-stable, low-dust substrates that ease clean-room validation burdens. Industrial chemicals adopt silicone-free coatings for desiccant sachets and barrier in-liners while consumer goods ride the e-commerce boom that prizes tough yet recyclable mailers. Printing and graphics remain flat but support higher-margin coated grades for premium catalogs and labels.

Geography Analysis

Asia-Pacific’s dominance rests on integrated pulp supply, dense converter clusters, and favorable duty structures that lower landed costs for regional FMCG brands. Japanese producers front-run innovation within wet-strength label applications, while Chinese mills ramp recycled-fiber lines to meet national 2030 carbon peaking goals. Currency headwinds and shipping-rate volatility prompt some North American buyers to dual-source locally, smoothing volume risk.

North American demand stays firm as state-level PFAS prohibitions align with the federal ruling, compelling immediate reformulation. Cross-border e-commerce accelerates multi-item mailer usage, spurring domestic capacity additions in dispersion coaters. Plastic-tax rollouts in Canada further widen the relative cost gap in favor of recyclable paper barriers.

Europe posts steady gains by embedding recyclability criteria into VAT incentives and grocery private-label standards. High energy prices curtail profit margins, yet access to green electricity certificates supports brand sustainability narratives. Middle East and Africa emerge as the fastest growth pocket; population expansion, quick-service restaurant chains, and new pharma plants underpin rising import volumes of high-barrier paper until local coating capacity matures. South America maintains a niche position where municipal recycling networks lag, but organic-certified agribusiness exports open a channel for silicone-free liners in bulk sacks.

Competitive Landscape

The silicone-free water resistant paper market exhibits moderate fragmentation; top five converters hold roughly 45% global share, reflecting significant but not overwhelming scale advantages. Mondi directs EUR 1.2 billion (USD 1.40 billion) to organic growth, installing high-speed curtain lines that reach 1,000 m/min while halving coat-weight variability. LINTEC focuses on fluorine-free grease barriers for instant noodle lids and oil-resistant tray liners, pledging to lift new-product revenue to 30% of sales by 2030. [4]LINTEC Corporation, “Integrated Report 2024,” lintec-global.com

Stora Enso converts Oulu’s former fine-paper machine into a 750,000 tpa consumer board unit, anchoring European supply security for PFAS-free papers employed in frozen foods and dairy lids. Avery Dennison leverages its USD 5.8 billion Materials Group to extend acrylic-dispersion know-how into water-resistant pressure-sensitive facestocks that meet ice-bath and condensation hurdles for premium beverages.

White-space entrants emphasize biopolymer feedstock integration, pushing algae-based and polysaccharide-rich coatings that promise traceable low-carbon footprints. Conversion cost, line-speed compatibility, and customer validation cycles remain formidable. Smurfit WestRock advances merger synergies that blend kraftliner, sack kraft, and coated-paper portfolios, seeking USD 400 million cost savings to fund new dispersion assets.

Silicone-Free Water-Resistant Paper Industry Leaders

Mondi plc

Nippon Paper Industries Co., Ltd.

LINTEC Corporation

Stora Enso Oyj

Domtar Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: FDA declares 35 PFAS food-contact notifications ineffective, mandating stock depletion by June 30 2025.

- February 2025: Smurfit WestRock posts Q4 2024 net sales of USD 7.5 billion and targets USD 400 million synergy savings.

- February 2025: Stora Enso reports 9% sales growth to EUR 2.362 billion (USD 2.749 billion) and confirms Oulu board line startup schedule.

- December 2024: EPA finalizes TSCA amendments heightening PFAS scrutiny.

Global Silicone-Free Water-Resistant Paper Market Report Scope

| Wax-Coated Paper |

| Fluorochemical-Coated Paper |

| Dispersion-Coated Paper (Water-based and Polymer) |

| Biopolymer and PVOH-Coated Paper |

| Laminated PE/PP-free Paper |

| Food and Beverage Packaging |

| Industrial and Chemical Packaging |

| Consumer Goods Packaging |

| Healthcare and Pharmaceuticals Packaging |

| Writing, Printing, and Graphics |

| Other End-Use Industries (E-commerce, Textile) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Barrier Technology | Wax-Coated Paper | ||

| Fluorochemical-Coated Paper | |||

| Dispersion-Coated Paper (Water-based and Polymer) | |||

| Biopolymer and PVOH-Coated Paper | |||

| Laminated PE/PP-free Paper | |||

| By End-Use Industry | Food and Beverage Packaging | ||

| Industrial and Chemical Packaging | |||

| Consumer Goods Packaging | |||

| Healthcare and Pharmaceuticals Packaging | |||

| Writing, Printing, and Graphics | |||

| Other End-Use Industries (E-commerce, Textile) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| France | |||

| United Kingdom | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the global value of silicone-free water resistant paper in 2025?

It stands at USD 283.4 million, with a forecast to reach USD 347.6 million by 2030.

Which application currently consumes the largest share of silicone-free water resistant paper?

Food and beverage packaging leads with 53.83% of global use in 2024.

How quickly is biopolymer and PVOH-coated paper demand expanding?

This barrier technology is projected to advance at a 6.48% CAGR from 2025 to 2030.

Which regulation triggered the most significant move away from PFAS-based coatings?

The FDA’s March 2025 decision that revoked 35 PFAS food-contact notifications accelerated the transition.

Which region is growing the fastest over the forecast period?

Middle East and Africa posts the highest CAGR at 6.03% between 2025 and 2030.

What is the main technical obstacle to broader use in flexible packaging?

Paper’s limited heat-sealability versus plastic films remains the biggest barrier to wider adoption.

Page last updated on: