Flexible Paper Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

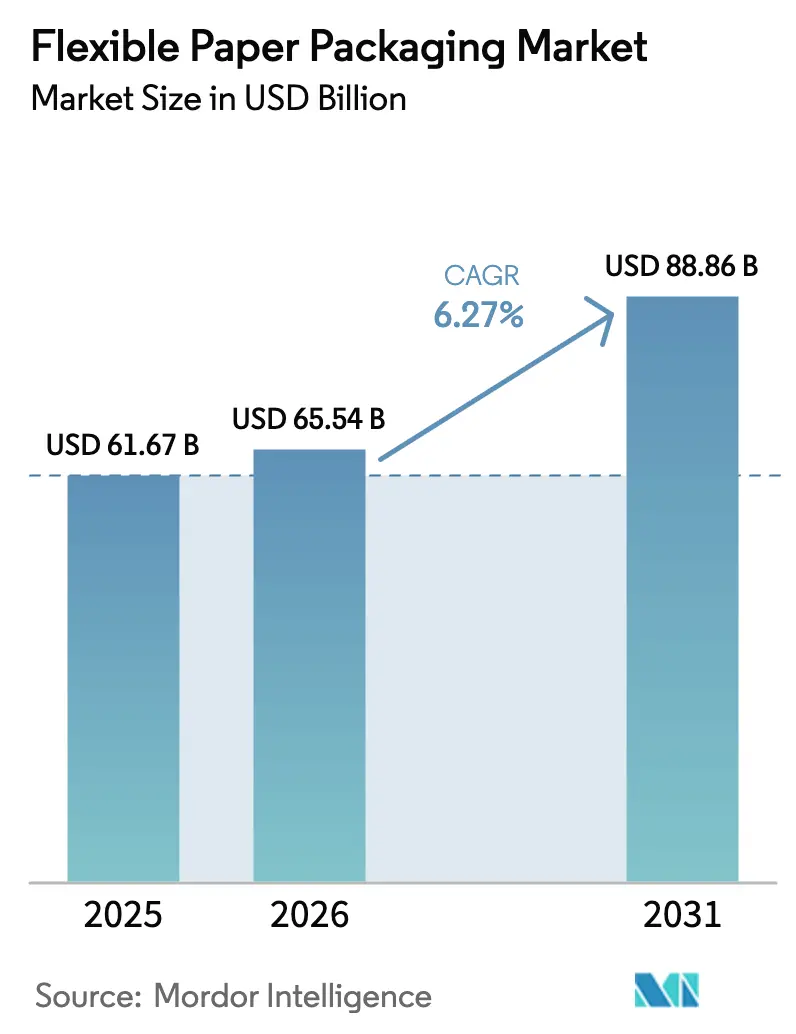

| Market Size (2026) | USD 65.54 Billion |

| Market Size (2031) | USD 88.86 Billion |

| Growth Rate (2026 - 2031) | 6.27% CAGR |

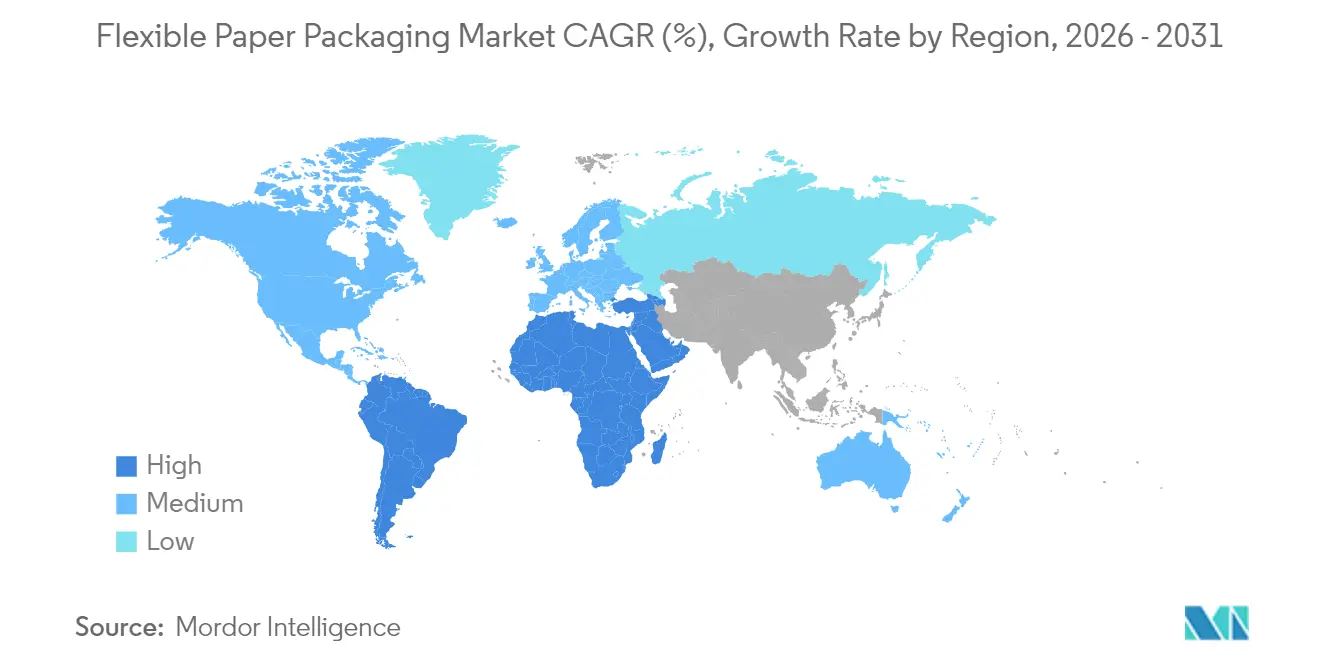

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Flexible Paper Packaging Market Analysis by Mordor Intelligence

The flexible paper packaging market size is expected to grow from USD 61.67 billion in 2025 to USD 65.54 billion in 2026 and is forecast to reach USD 88.86 billion by 2031 at 6.27% CAGR over 2026-2031. The expansion is anchored in regulatory mandates limiting single-use plastics, corporate net-zero targets, and rapid innovation in barrier coatings that let paper substitute plastic in direct-food and e-commerce channels. Converters are modernizing assets with high-speed digital presses and aqueous or bio-polymer coatings that support short runs, variable data printing, and mono-material designs, thereby compressing lead times for brand launches. Large integrated mills leverage pulp backward integration to hedge raw-material volatility, while independent converters differentiate through specialty grease-resistant wraps and meal-kit pouches. Investor appetite remains strong as acquirers pursue scale to negotiate pulp contracts and fund R&D pipelines, with regulatory clarity in the European Union (EU) and Asia-Pacific (APAC) accelerating deal flow.

Key Report Takeaways

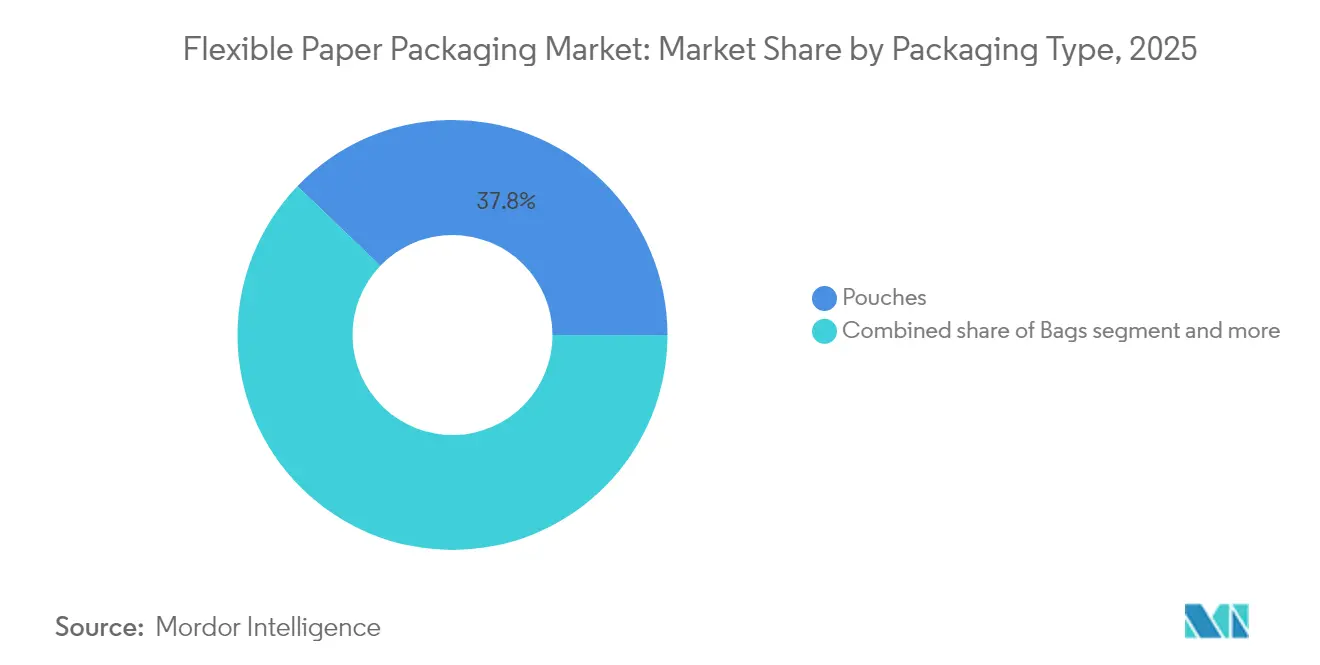

- By packaging type, pouches led with 37.83% of flexible paper packaging market share in 2025; wraps are projected to grow at a 8.78% CAGR through 2031.

- By printing technology, flexography captured 35.02% of revenue in 2025, whereas digital printing exhibit the highest 7.74% CAGR to 2031.

- By paper grade, kraft paper accounted for 44.68% of the flexible paper packaging market size in 2025; laminated paper is expanding at 7.71% CAGR during 2026-2031.

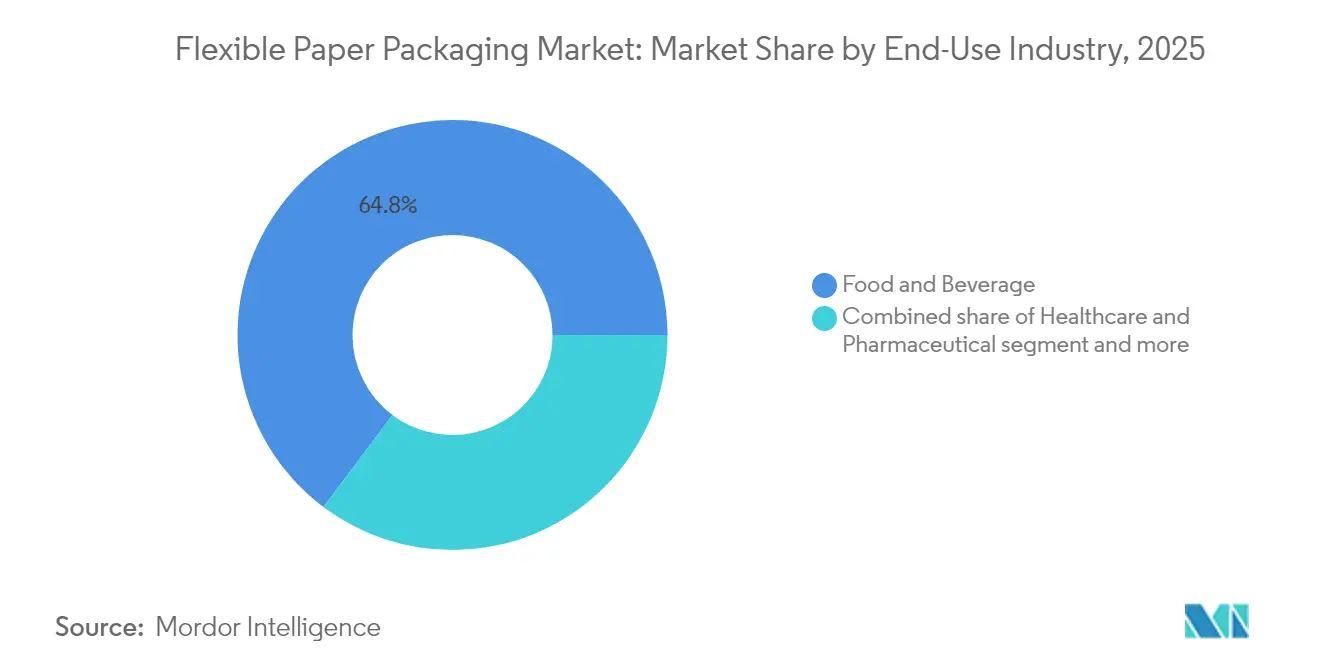

- By end-use industry, food and beverage captured 64.75% of revenue in 2025, whereas healthcare and pharmaceuticals exhibit the highest 8.89% CAGR to 2031.

- By geography, Asia-Pacific commanded 44.56% revenue share in 2025, while the Middle East & Africa region is poised for the fastest 8.92% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Flexible Paper Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory bans on single-use plastics | +1.8% | EU core, spill-over to APAC & North America | Medium term (2-4 years) |

| High-barrier paper for e-commerce meal-kits | +1.2% | North America, expanding to Europe | Short term (≤ 2 years) |

| High-speed digital printing for DTC brands | +0.9% | Europe & North America | Medium term (2-4 years) |

| Grease-resistant pouches for refrigerated Asian foods | +1.1% | APAC core, emerging in MEA | Short term (≤ 2 years) |

| Brand-owner 2025 recyclability commitments in cosmetics packaging | +0.7% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Expansion of aqueous/biopolymer coatings for snack wraps | +0.8% | Latin America, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory bans on single-use plastics

The EU’s Packaging & Packaging Waste Regulation sets a mandatory 65% recycling rate for paper packs by 2025, forcing global FMCG suppliers to redesign multilayer laminates around mono-paper substrates. China’s updated food-contact standard GB 4806 now lists bio-origin coatings, nudging takeaway chains toward fluorine-free wraps. Thailand and Japan adopted similar positive-list schemes in 2024, creating cross-regional scale for compliant grades. Brand owners embed paper-substitution milestones in supplier scorecards, triggering multi-year offtake commitments that underpin capacity expansions by Amcor and Mondi.

High-barrier paper for e-commerce meal-kits

Cold-chain meal-kit vendors require oxygen- and moisture-barrier integrity over 48-hour transit. Solenis teamed with Heidelberg to commercialise aqueous coatings that withstand condensation without polymer lamination, cutting pack weight 18% and maintaining curbside recyclability. [1]Source: Solenis, “Barrier Coatings for Food and Beverage Packaging,” solenis.com Amcor’s AmFiber platform now ships mono-paper mailers rated for −20 °C storage while meeting FDA migration limits. US meal-kit operators report 12% repeat-purchase lifts after switching from PE films to paper mailers that carry “widely recyclable” How2Recycle labels.

High-speed digital printing for DTC brands

European converters deploy industrial inkjet presses capable of 500-unit profit runs, unlocking mass-customised packaging with serialized QR codes, variable loyalty offers, and geo-targeted graphics. New pigment sets bond to grease-resistant and barrier-coated papers without corona treatments, expanding substrate freedom while reducing VOC emissions under Germany’s TA Luft limits. Digital workflows trim plate waste and eliminate chemical wash-ups, aligning with Scope-1 emissions targets published by Huhtamaki.

Grease-resistant pouches for refrigerated Asian foods

Fluorine-free dispersion coatings allow paper pouches to pack oily dim sum, sushi, and noodle bowls for refrigerated shelves. Vietnam’s paper-pack industry, worth USD 2.60 billion in 2025, is forecast to grow 9.73% annually through 2033 as wet-market operators shift from LDPE bags to paper pouches mandated by Decree 45/2024. Nestlé Thailand replaced multi-layer PP pouches with FC-approved kraft, cutting plastic tonnage 28% in its ready-meal range. [2]Source: Nestlé Thailand, “Nestlé Thailand Eliminates Plastic in Ready Meal Lines,” nestle.co.th

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Barrier limits in dairy & beverage applications | −1.4% | Global, especially developed markets | Long term (≥ 4 years) |

| Virgin pulp price volatility | −1.1% | Global, acute in North America & Europe | Short term (≤ 2 years) |

| Weak collection infrastructure for paper-laminates | −0.8% | Emerging markets in Africa & LatAm | Medium term (2-4 years) |

| High capex to retrofit plastic-flexible lines | −0.9% | North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Barrier limits in dairy & beverage applications

Paper’s porosity still compromises flavour and carbonation retention in milk and soft drinks beyond 72 hours, according to controlled storage trials that recorded a 0.2 log CFU microbial uptick in skim-milk cartons after refrigerated hold. Nano-cellulose and biodegradable EVOH replacements remain commercially nascent; Stora Enso targets pilot-scale output only by 2028. As a result, PET and aseptic cartons continue to dominate liquid dairy aisles, capping flexible paper packaging market penetration.

Virgin pulp price volatility compressing converter margins

Benchmark NBSK pulp averaged USD 1,350/tonne in 2024, 15% higher year-over-year after storm damage cut Canadian fiber supply. [3]Source: Forest Products Association Canada, “2024 Market Pulp Outlook,” fpac.ca Currency swings amplify strain; euro-denominated converters paid an effective 19% surcharge due to dollar strength. Integrated majors offset shocks via captive forests and long-term stumpage leases; independents instead blend higher recycled furnish, but tensile loss elevates reject rates 4% and drags OEE metrics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Type: Pouches Consolidate Leadership

Pouches accounted for 37.83% of flexible paper packaging market share in 2025, reflecting cross-category acceptance in snacks, nutraceuticals, and condiments. Their flattened geometry cuts freight emissions by up to 30% versus rigid cans, aligning with retailer scope-3 carbon targets. Brand owners appreciate front-panel real estate that supports storytelling and QR-enabled traceability. Bags persist in industrial seed and pet-food channels where drop-test performance trumps aesthetics. Wraps, although holding a smaller base, post a 8.78% CAGR through 2031 as e-commerce apparel and confectionery shippers pivot from PE mailers to tear-resistant paper wraps that meet mailbox-friendly sizing.

The flexible paper packaging market size is projected to reach USD 88.86 billion by 2031, and wraps could command a doubled share if e-tailers scale mono-material pilots nationwide. Sachets and stick-packs remain niche but vital for powdered electrolytes and cosmetic samplers that exploit new micro-valve fitments compatible with paper laminates. Integrated mills deploy modular pouching lines enabling quick tool changes between stand-up and flat variants, enhancing asset utilisation. Customisable zipper seals, now made from cellulose-based films, advance the circularity narrative without compromising barrier metrics.

By Paper Grade: Kraft Paper Retains Strength Premium

Kraft paper delivered 44.68% of revenue in 2025 due to high tear resistance and excellent machinability on existing form-fill-seal lines. Mills expand bleached and natural kraft SKUs tailored for premium pet-food and organic snack brands seeking earthy aesthetics. Laminated paper, forecast at 7.71% CAGR, exploits water-based adhesive systems that bond thin barrier layers yet allow same-stream repulping. White-top kraft grades gain traction where photo-realistic printing is crucial, bridging the gap between cost and printability.

The flexible paper packaging market size for kraft grades alone translates to USD 27.55 billion in 2025, underscoring their strategic importance to converters. Recycled-content options climb in popularity after consumer-goods companies pledged 30% post-consumer fiber by 2028. Specialty grease-resistant coated papers serve Asian frozen meals, using fluorine-free chemistry validated under FDA and EU food-contact protocols. Research into nano-clay and chitosan coatings promises moisture-barrier lifts without plastic, broadening kraft applicability to bakery and salty snack corridors.

By End-Use Industry: Food & Beverage Drive Volume

Food and beverage relied on paper for 64.75% of sectoral uptake in 2025 as quick-service restaurants replaced waxed boards with PE-free wraps. Shelf-stable cereal brands moved to micro-perforated paper sachets that balance moisture egress and crunch retention. The healthcare vertical, rising at 8.89% CAGR, pilots blister-lidding composites using thin aluminium-oxide coated paper, anticipating EU pharmaceutical EPR enactment in 2026. Personal-care sachets leverage the tactile warmth of paper to signal natural formulations, with line extensions in shampoo bars and serums.

The flexible paper packaging industry taps e-grocery alliances for scale, supplying high-barrier pouch liners that withstand freezer burn for plant-based entrées. Home-care detergents adopt paper refill pods scored for easy tearing, cutting rigid-plastic bottle demand. Pet-food brands trial oxygen-scavenger functional inks printed on kraft, prolonging kibble freshness without multilayer films. Across verticals, universal design for recyclability checklists guide substrate qualification and accelerate cross-segment knowledge transfer.

By Printing Technology: Digital Accelerates Personalisation

Flexography held 35.02% share in 2025, buoyed by continuous-duty reliability on wide-web kraft lines. LED-UV curing lowers energy draw and curbs VOC emissions, helping fleets meet ESG audits. Yet digital inkjet exhibits an 7.74% CAGR as DTC marketing budgets pivot toward limited-edition drops and influencer collaborations. Cloud-native prepress platforms streamline artwork approvals, enabling 72-hour turnaround from file receipt to shipment.

The flexible paper packaging market size allocated to digitally printed formats is expected to surpass USD 11.07 billion by 2031. Hybrid presses merge flexo bases with digital units, allowing cost-optimal versioning within the same pass. Rotogravure remains the choice for premium confectionery wraps needing metallic effects, although solvent-recovery mandates add capex burdens. Offset litho occupies a niche in folded cartons and insert sleeves but informs colour-management protocols adopted by flexo and inkjet workflows, promoting visual consistency across mixed substrates.

Geography Analysis

Asia-Pacific led the flexible paper packaging market with 44.56% revenue share in 2025, supported by competitive fiber sourcing, integrated mill networks, and rising middle-class consumption. China’s updated positive list for food-contact coatings expedites commercial rollout of bio-polymer barriers, shortening regulatory lead times. Vietnam, valued at USD 2.60 billion in 2025, represents a template for export-ready meal-kit pouches that align with European recyclability standards. Japanese converters benefit from government subsidies that offset capital costs for high-speed digital presses, accelerating innovation diffusion. The flexible paper packaging market size is set to expand steadily in the region as cold-chain infrastructure spreads into tier-3 cities, unlocking applications for grease-resistant freezer pouches.

The Middle East & Africa region records the fastest 8.92% CAGR, underpinned by plastic-tax legislation in the Gulf Cooperation Council and infrastructure investments in corrugated and flexible converting. Saudi Arabia’s Vision 2030 allocates land for integrated pulp-to-packaging complexes that reduce import dependency. In Africa, pan-regional supermarket chains mandate recyclable mono-paper wraps for private-label baked goods, triggering capacity additions in Kenya and Nigeria. International brand owners negotiate local sourcing agreements to bypass high freight costs and mitigate currency risk, embedding circular-economy clauses that require in-country recycling audits.

North America and Europe together represent mature, high-value nodes where brand owners demand advanced barrier performance and precision print quality. US e-commerce meal-kit operators adopt porch-friendly pouch formats that maintain freshness through ambient swings, driving R&D in condensation-resistant coatings. In the EU, PPWR recyclability targets continue to pull forward capital expenditure on repulpable laminates. South America leverages abundant plantation forestry in Brazil and Chile to export uncoated kraft reels, while domestic converters in Argentina focus on snack-wrap demand amid rising convenience-food sales. Regional trade pacts streamline movement of jumbo reels, fostering cross-border cooperation among mill and print converters.

Competitive Landscape

The flexible paper packaging market remains moderately fragmented, yet consolidation momentum accelerates as players pursue synergies in pulp procurement, R&D, and cross-selling. International Paper’s USD 7.2 billion acquisition of DS Smith in January 2025 created the world’s largest paper-centric packaging entity, integrating corrugated and flexible portfolios under one sourcing umbrella. Amcor’s merger with Berry Global in February 2025 solidifies a North America-Europe axis that combines polymer know-how with emerging mono-paper lines, while Smurfit Westrock’s USD 34 billion tie-up amplifies bargaining power with supermarket chains.

Strategic emphasis rests on proprietary barrier chemistries that enable mono-material designs. Huhtamaki scales fiber lid output in Northern Ireland, pairing lids with in-house produced grease-resistant pouches for QSR chains. UPM pilots nano-fibrillated cellulose coatings that elevate water vapour barrier without plastic, positioning mills for entry into dairy powdered drink mixes. Integrated players lock pulp supply through sustainable forestry certifications, insulating against raw-material spikes that continue to pressure stand-alone converters.

Mid-cap specialists differentiate via digital-printing agility, offering cosmetic and nutraceutical brands batch sizes as low as 300 units with serialized graphics. Start-ups commercialize chitosan-based barrier dispersions sourced from shrimp-shell waste, attracting venture capital for scale-up reactors. Private-label retailers expand direct sourcing offices in Asia to co-create sustainable paper packs, bypassing legacy procurement intermediaries and compressing time-to-market. Competitive intensity therefore hinges on technical IP, scale advantages, and the capacity to navigate converging global regulations.

Flexible Paper Packaging Industry Leaders

Amcor Plc

Mondi Plc

Smurfit Westrock

Huhtamaki Oyj

International Paper Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Amcor completed its merger with Berry Global, forming a broader platform for paper-based flexible solutions.

- January 2025: Huhtamaki India hosted Think Circle, spotlighting flexible packaging recycling guidance.

- January 2025: International Paper closed the USD 7.2 billion DS Smith acquisition, expanding global reach in corrugated and flexible products.

- December 2024: Stora Enso ramped production at the Oulu mill after a USD 1.13 billion capacity upgrade, boosting European supply of coated kraft.

Global Flexible Paper Packaging Market Report Scope

Flexible packaging paper solutions are low-cost, lightweight, and used to extend product shelf life. The growing demand for environment-friendly and sustainable packaging solutions is a significant driver of the flexible packaging paper market, creating opportunities for manufacturers. Flexible paper packaging is becoming more popular, linked to its high efficiency and low cost. Industries that require flexible packaging, such as food and beverage, personal care, home care, and healthcare, can benefit significantly from it. The scope of the flexible paper packaging market is segmented by packaging type (pouches, roll stock, shrink sleeves, wraps), by end-use (food & beverages, healthcare. beauty & personal care), and by geography (North America, Europe, Asia-Pacific, and Rest of the World). The market is tracked in terms of revenue (USD Billion) for all the reportable segments.

| Pouches |

| Bags |

| Wraps |

| Other Packaging Types |

| Coated Papers |

| Laminated Pape |

| Kraft Paper |

| Other Paper Grades |

| Food and Beverage |

| Healthcare and Pharmaceutical |

| Beauty and Personal Care |

| Home Care and Laundry |

| Pet Food |

| Other End Use Industry |

| Flexography |

| Rotogravure |

| Digital Printing |

| Offset |

| Other Printing Technology |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Packaging Type | Pouches | ||

| Bags | |||

| Wraps | |||

| Other Packaging Types | |||

| By Paper Grade | Coated Papers | ||

| Laminated Pape | |||

| Kraft Paper | |||

| Other Paper Grades | |||

| By End-Use Industry | Food and Beverage | ||

| Healthcare and Pharmaceutical | |||

| Beauty and Personal Care | |||

| Home Care and Laundry | |||

| Pet Food | |||

| Other End Use Industry | |||

| By Printing Technology | Flexography | ||

| Rotogravure | |||

| Digital Printing | |||

| Offset | |||

| Other Printing Technology | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current size of the flexible paper packaging market?

• The flexible paper packaging market size stands at USD 65.54 billion in 2026 and is forecast to hit USD 88.86 billion by 2031.

Which region leads demand for flexible paper packaging?

• Asia-Pacific leads with 44.56% revenue share, driven by manufacturing scale, raw-material availability, and rising consumer-goods output.

Which packaging type dominates the flexible paper packaging market?

• Pouches hold 37.83% market share thanks to their convenience, barrier performance, and freight-efficiency benefits.

What is the fastest-growing end-use sector?

• Healthcare and pharmaceuticals expand at a 8.89% CAGR because of rising unit-dose formats and regulatory acceptance of paper substrates.

How are raw-material price fluctuations affecting the market?

• Virgin pulp volatility, with 15% price swings in 2024, compresses converter margins and incentivizes vertical integration and blended fiber recipes.

Why are regulators accelerating adoption of paper packaging?

• Policies such as the EU PPWR set high recyclability targets and single-use plastic bans, prompting brand owners to swap plastic films for recyclable paper alternatives.

Page last updated on: