Oxygen-Scavenger Paper Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

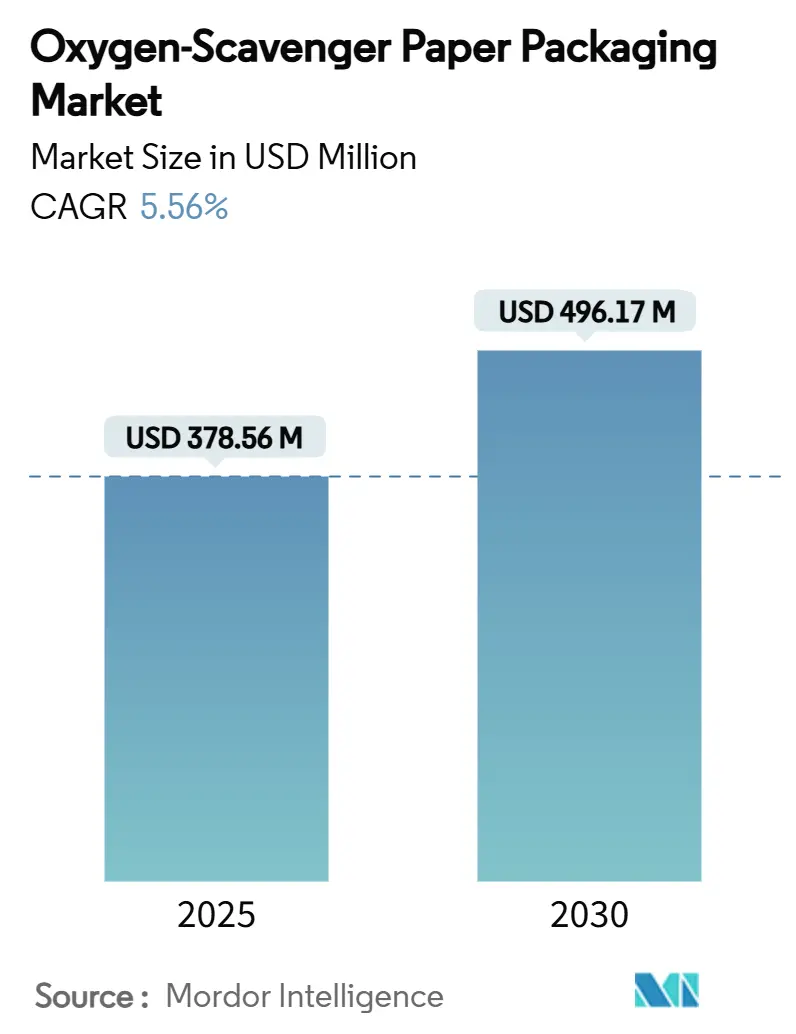

| Market Size (2025) | USD 378.56 Million |

| Market Size (2030) | USD 496.17 Million |

| Growth Rate (2025 - 2030) | 5.56% CAGR |

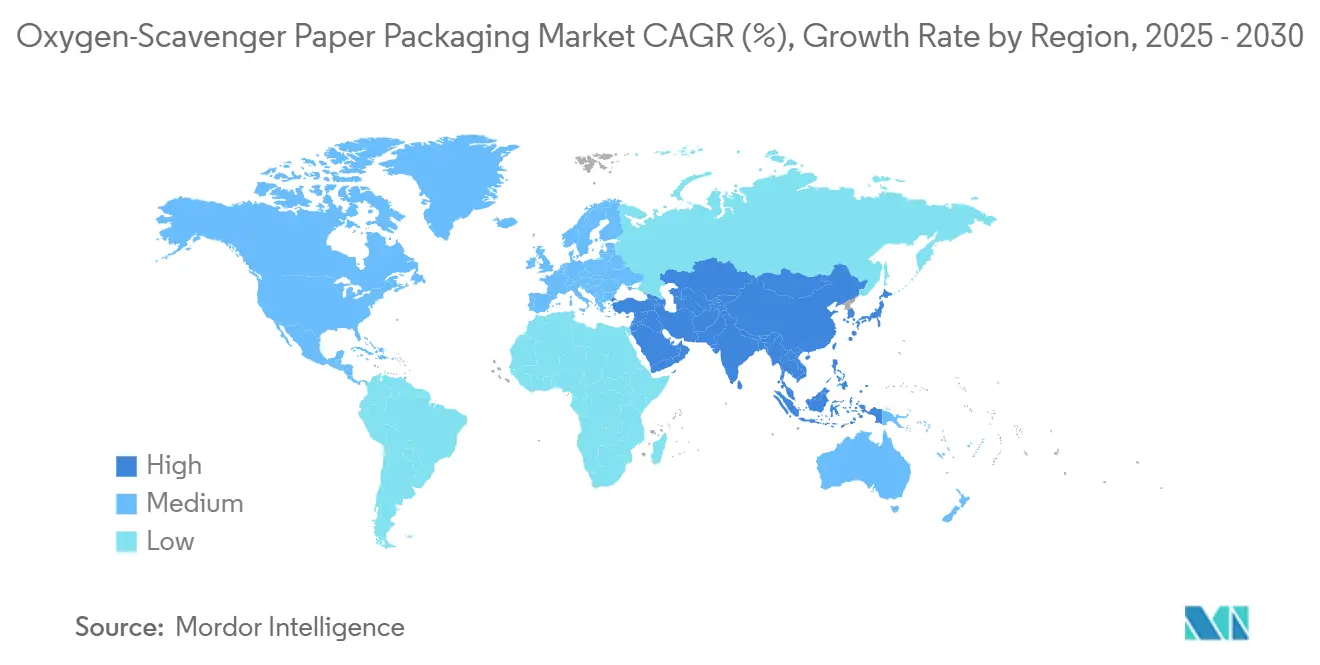

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oxygen-Scavenger Paper Packaging Market Analysis by Mordor Intelligence

The oxygen-scavenger paper packaging market size stands at USD 378.56 million in 2025 and is forecast to reach USD 496.17 million by 2030, registering a 5.56% CAGR. Demand accelerates as regulators tighten rules on single-use plastics, retailers lean into clean-label claims, and brands pursue lower Scope-3 emissions. Iron-based sachets remain the workhorse technology, yet polymer-integrated and bio-scavenger systems are scaling because they combine barrier performance with recyclability. Packaging converters are redesigning flexible formats around mono-material papers that accept scavenger coatings, while e-commerce growth widens the use case for corrugated linerboard containing oxygen absorbers. Competitive intensity is rising as chemical firms, paper mills, and specialty converters race to differentiate through patentable chemistries that unlock premium SKUs.

Key Report Takeaways

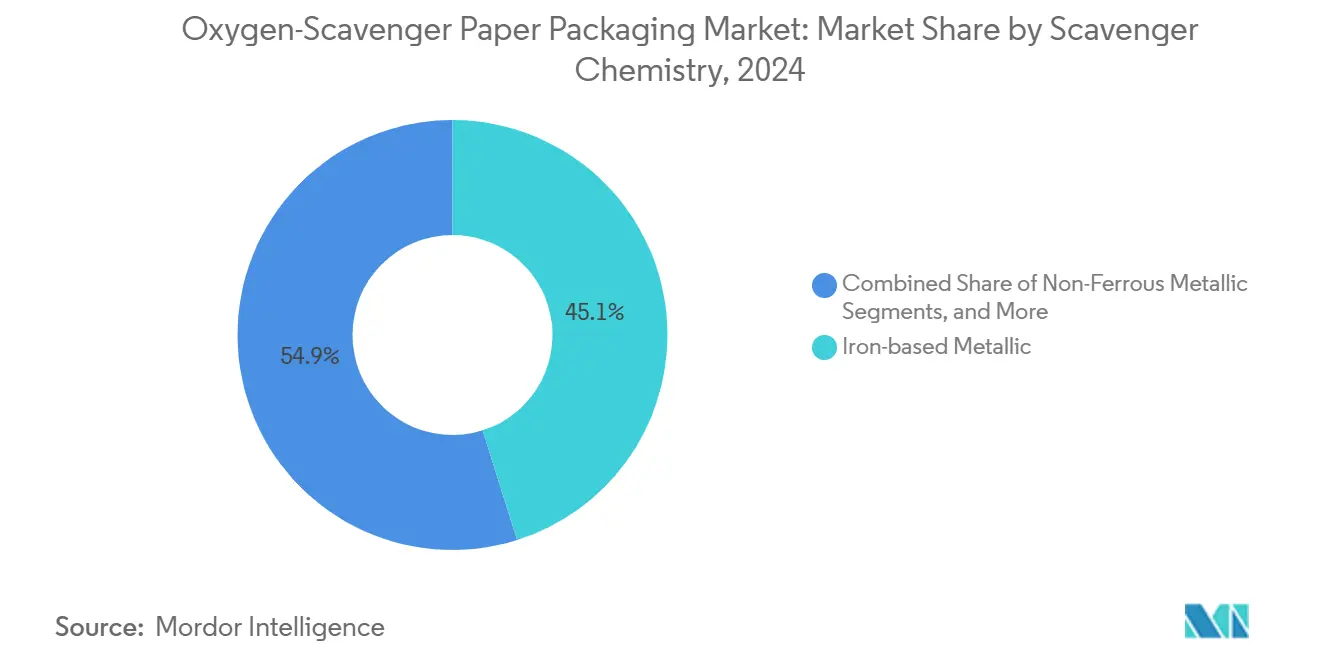

- By scavenger chemistry, iron systems led with 45.13% of the oxygen-scavenger paper packaging market share in 2024.

- By paper substrate, the oxygen-scavenger paper packaging market size for the multilayer bio-papers segment is projected to grow at a 6.84% CAGR between 2025-2030.

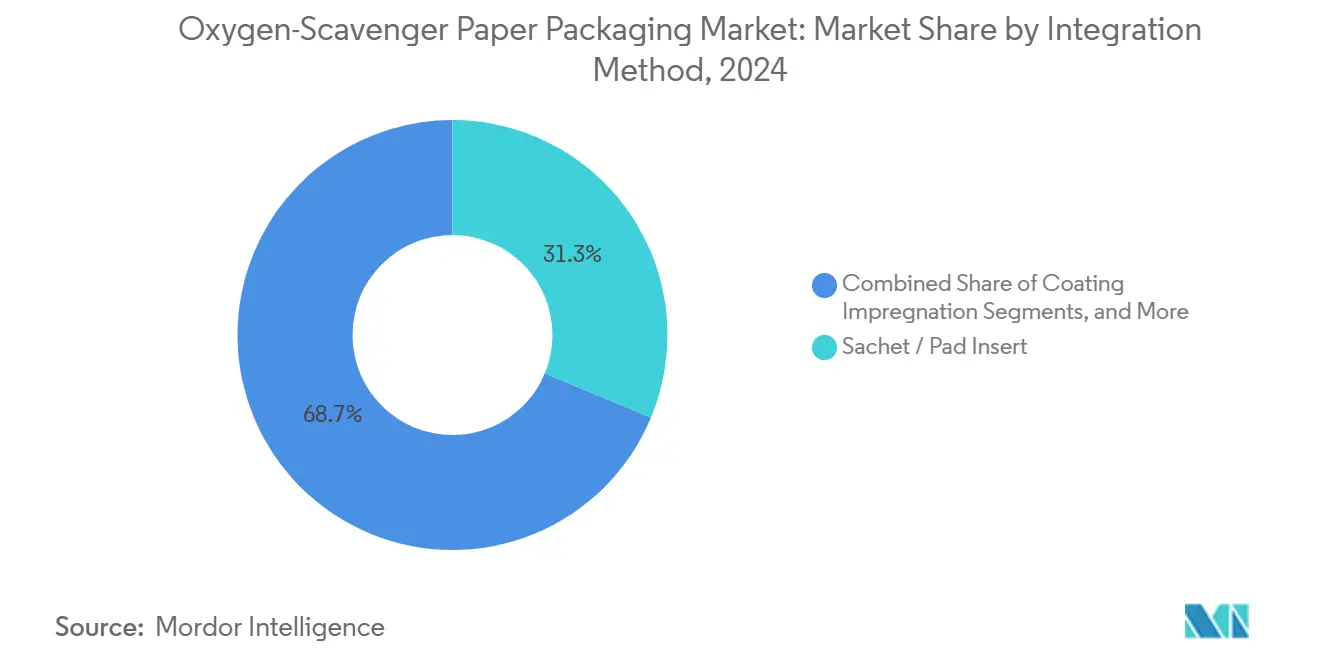

- By integration method, sachet and pad inserts captured a 31.25% share of the oxygen-scavenger paper packaging market size in 2024.

- By end-use industry, the oxygen-scavenger paper packaging market size for the pharmaceuticals and nutraceuticals segment is projected to grow at a 6.93% CAGR between 2025-2030.

- By geography, North America held 33.41% of the oxygen-scavenger paper packaging market share in 2024.

Global Oxygen-Scavenger Paper Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for clean-label shelf-life extension | +1.2% | Global, with premium focus in North America & EU | Medium term (2-4 years) |

| Plastic-to-paper substitution driven by regulation | +1.8% | EU primary, expanding to APAC & North America | Long term (≥ 4 years) |

| Growth of e-commerce and ready-to-eat meals | +0.9% | Global, concentrated in urban centers | Short term (≤ 2 years) |

| Global anti-food-waste legislation momentum | +0.7% | OECD countries, expanding to emerging markets | Long term (≥ 4 years) |

| Light-activated scavenger coatings unlock new SKUs | +0.4% | North America & EU innovation hubs | Medium term (2-4 years) |

| Net-zero Scope-3 targets favour bio-scavenger papers | +0.6% | Global, led by multinational corporations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Clean-Label Shelf-Life Extension

Consumers gravitate toward minimally processed foods, pushing brands to replace synthetic preservatives with oxygen absorbers that work invisibly inside paper packs. National targets aligned to UN SDG 12.3 place policy weight behind shelf-life technologies, and 74% of governments now report formal food-waste goals.[1]Celine Giner, “OECD Food Loss and Waste Policy Analysis,” OECD.ORG Research into essential-oil biopolymer coatings shows antimicrobial action without chemical additives, particularly valuable for meat and poultry. Enzyme systems such as glucose oxidase and laccase maintain 97% activity after lamination yet absorb over 7.6 L/m² of oxygen. Lignin-derived substrates support these enzymes while lowering carbon footprints, enabling converters to market packs as both natural and circular. Collectively, these advances elevate oxygen-scavenger papers from shelf-life tools to clean-label enablers that protect brand equity.

Plastic-to-Paper Substitution Driven by Regulation

The April 2024 EU Packaging Regulation mandates that every pack placed on the bloc’s market must be recyclable by 2030. Paper therefore gains share in barrier-critical categories where plastics previously dominated. Mondi already meets 85% of its packaging revenue with recyclable or compostable designs, channeling capex toward paper-based barrier lines. Academic reviews confirm that current multilayer plastic laminates struggle in mechanical recycling, prompting a redesign toward mono-material papers plus oxygen scavengers. Emerging Asian rules mirror Europe, with Indonesia’s draft food-contact law introducing migration limits that established paper-based scavengers can meet more readily than many polymer systems. The regulatory tide thus leans strongly toward oxygen-scavenger paper packaging market adoption.

Growth of E-Commerce and Ready-to-Eat Meals

Direct-to-consumer supply chains stretch transit times and environmental exposures, elevating the value of in-pack oxygen control. Express delivery in China was already 90.95% paper-based by 2018, creating a vast platform for scavenger-enabled corrugated formats. Ready-to-eat meals likewise benefit from oxygen management without investing in modified-atmosphere machinery. Trials on smart packs for fresh fruit confirm that paper embeds can slow respiration and ethylene, extending freshness in last-mile networks. Urbanization and sustainability converge, positioning the oxygen-scavenger paper packaging market as a dual solution for convenience and waste reduction.

Global Anti-Food-Waste Legislation Momentum

Voluntary rather than punitive, most national food-waste programs still steer procurement toward proven shelf-life technologies. Mitsubishi Gas Chemical’s AGELESS sachets illustrate the legacy of oxygen scavenging in reducing spoilage since 1977. Next-generation systems use palladium nanoparticles in biodegradable matrices to outperform iron while aligning with recycling goals. Policymakers reward such innovations through grants and eco-label privileges, reinforcing demand across regions.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher unit cost versus conventional paper | -1.1% | Global, most pronounced in price-sensitive markets | Short term (≤ 2 years) |

| Moisture-interference lowers scavenger efficacy | -0.8% | High-humidity regions, tropical climates | Medium term (2-4 years) |

| Off-odour / flavour risks in premium foods | -0.6% | Premium food segments globally | Medium term (2-4 years) |

| Recycling challenges of multilayer papers | -0.9% | EU & North America with strict recycling mandates | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Higher Unit Cost Versus Conventional Paper

Scavenger-impregnated papers currently carry a price premium that constrains uptake in commodity channels. Austrian studies show that reaching 38.9% recycling of multilayer films will require capital upgrades that feed into material costs. Enzyme-based laminates also need tighter process control, adding to overheads. However, lifecycle models that account for avoided food waste and spoilage are starting to tilt total-cost-of-ownership analyses in favor of scavenger papers, gradually narrowing the cost gap within the oxygen-scavenger paper packaging market.

Moisture-Interference Lowers Scavenger Efficacy

High ambient humidity, typical in tropical zones, competes with oxygen for iron-based reaction sites, blunting performance. Laccase–lignin systems likewise show sensitivity to water vapor. The answer lies in hydrophobic carriers and moisture-resistant coatings, which are progressing but add complexity to supply chains. Until these formulations scale, efficacy concerns could temper growth in certain climates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Scavenger Chemistry: Iron Leads but Polymers Surge

Iron-based materials held 45.13% oxygen-scavenger paper packaging market share in 2024, anchored by Mitsubishi Gas Chemical’s AGELESS family, which spans 600 SKUs and supports semi-dried noodle and frozen pizza categories. Despite maturity, iron’s limits around moisture and odor drive brands toward alternatives in premium lines. Polymer-integrated films complexed with Fe(II)(salen) reach oxygen uptake of 300 mL/g, propelling a 6.78% CAGR trajectory. Nano-metal composites using TiO₂ enable light-controlled activation that conserves scavenger capacity during distribution. As more CPGs rewrite design briefs around recyclability, polymer and bio-based chemistries are set to erode iron’s share, reshaping the oxygen-scavenger paper packaging market over the forecast horizon.

Second-generation bio-scavengers employ lignin residues from pulping streams, aligning function with circular-economy storytelling. Enzyme systems stitched into the paper matrix provide clean-label appeal and reduce the risk of metallic contamination. Early adopters in organic snacks and baby food segments report marketing upside that offsets incremental cost. With multinational brands chasing net-zero goals, these niche chemistries are likely to graduate into mainstream volume mid-decade.

By Paper Substrate: Conventional Grades Face Bio-Paper Challenge

Coated kraft and SBS papers dominated with 39.62% share in 2024 due to established converters and compatibility with high-speed filling lines. Their clay coatings deliver a smooth surface for ink and barrier layers, essential in branded FMCG cartons. Yet investors are channelling funds into bio-papers that couple compostability with mechanical strength. Palladium-nanoparticle biopapers, produced via electrospinning onto PCL layers, surpass oxygen-permeability targets while remaining heat-sealable. [2]Adriane Cherpinski et al., “Oxygen-Scavenging Biopapers with Palladium Nanoparticles,” NANOMATERIALS.COM This performance underpins a 6.84% CAGR, the fastest among substrates.

Corrugated linerboard, long the backbone of shipping cases, now integrates scavenger intermediates to offset longer e-commerce dwell times. Trials show carton oxygen levels falling below 0.1% for 30 days, protecting nutraceutical pouches in hot climates. As digital grocery expands, linerboard’s functional transformation is set to broaden the oxygen-scavenger paper packaging market footprint across secondary and tertiary packaging tiers.

By Integration Method: Coatings Outpace Sachets

Sachets and pads remain popular, controlling 31.25% of the 2024 oxygen-scavenger paper packaging market size thanks to low-capex retrofit options and familiarity among packers. They also satisfy regulations where direct food contact must be avoided. However, line productivity and packaging aesthetics push converters to embed scavengers directly onto paper. Coating-impregnation technologies now maintain 97% enzyme activity even after exposure to 325 °C during lamination, supporting a 6.52% CAGR.

Label and ink routes provide pinpoint placement for premium chocolates and coffee, while microcapsule coatings activate under defined humidity, preventing early depletion. These methods compress pack thickness, reduce SKUs, and enhance recyclability advantages that compound adoption momentum in the oxygen-scavenger paper packaging market.

By End-Use Industry: Pharmaceuticals Accelerate

Food and beverage absorbed 56.25% of 2024 demand, leveraging scavenger papers across meat, dairy, bakery, and produce. Ready-to-eat meals shipped through urban dark-kitchen networks rely on in-pack oxygen control to preserve taste without recooking. Fruits packed in smart cartons show reduced respiration and extended shelf life, aiding cross-border e-commerce into Southeast Asia.

Compliance-heavy, pharmaceuticals and nutraceuticals clock the quickest 6.93% CAGR through 2030. FDA container-closure guidance emphasises oxygen barrier performance, and scavenger papers enable blister lidding that protects oxidation-sensitive APIs while remaining child-resistant. Brands also deploy them for herbal supplements marketed on “no preservatives” claims. As wellness trends surge, the segment is primed to lift overall oxygen-scavenger paper packaging market revenues.

Geography Analysis

North America controlled 33.41% of 2024 revenue, propelled by stringent food-safety codes and well-capitalised converters that can validate new chemistries swiftly. The US craft-meat sector adds niche demand for clean-label oxygen control, while Canadian seafood exporters adopt scavenger cartons to cut airfreight spoilage. Mexico’s expanding manufacturing base benefits from USMCA duty-free flows, allowing regional brands to source papers locally and feed into continental distribution.

Asia-Pacific will deliver the fastest 7.14% CAGR to 2030. Indonesia’s forthcoming migration-limit rule formalises a compliance pathway for paper-based scavengers. China, already the world’s biggest paper consumer in e-commerce, offers industrial scale: corrugated accounts for close to 91% of express packs, ready for functional upgrades. [3]Xuanyu Ji et al., “Development of Green Packaging,” IOP.ORG India’s packaged-food boom and Japan’s ageing population where small-portion ready meals flourish stimulate demand. South Korea and Australia, both tightening plastic-waste rules, further amplify regional growth prospects for the oxygen-scavenger paper packaging market.

Europe provides regulatory certainty under the 2024 Packaging Regulation. Germany and France spearhead adoption in premium dairy and charcuterie, while Nordic retailers pilot bio-paper solutions aligned with national circular-economy roadmaps. Post-Brexit, the UK mirrors EU rules to ease continental trade, keeping market standards harmonised. In the Middle East and Africa, GCC investments in food-security logistics and South Africa’s growing chilled-food aisles hint at longer-term potential once price points fall.

Competitive Landscape

Market concentration is moderate. Early entrant Mitsubishi Gas Chemical leverages nearly five decades of technical data to defend its AGELESS iron platform, supplying over 600 sachet variants for global meat, bakery, and pharmaceutical packs. Sealed Air’s 2023 acquisition of Liquibox added liquid-pack formats, creating cross-selling opportunities to integrate paper-based scavenger layers across its USD 5.5 billion revenue base.

Integrated paper majors are moving upstream. Stora Enso’s Oulu board mill, ramping toward full capacity by 2027, is engineered to accept functional coatings that include oxygen scavengers. Mondi’s EUR 1.2 billion investment plan channels 80% toward recyclable barrier solutions, directly challenging specialty chemical suppliers. Concurrently, patent activity around light-activated and reusable scavenger composites points to disruptive entrants such as Empire Technology Development, whose porphyrin-metal oxide designs could rewrite material economics.

Strategic play centers on chemistry differentiation and life-cycle credentials. Firms tout bio-based content, light-activation triggers, and recyclability to win sustainability-driven RFQs. Co-development agreements between brand owners and converters shorten validation cycles, embedding suppliers early. This jockeying is set to redefine share positions in the oxygen-scavenger paper packaging market over the next five years.

Oxygen-Scavenger Paper Packaging Industry Leaders

Mitsubishi Gas Chemical Co.

Sealed Air Corp.

Multisorb Technologies (Filtration Grp.)

Mondi Plc

Stora Enso Oyj

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Stora Enso recorded 9% sales growth to EUR 2,362 million in Q1 2025, with its new Oulu consumer board line on track for full output by 2027, expanding feedstock for scavenger-ready papers.

- February 2025: Amcor released a decarbonization roadmap targeting a 32.5% Scope-3 cut by 2033 and 30% recycled content by 2030, signalling increased sourcing of bio-scavenger packaging.

- January 2025: OECD reported that 74% of nations have food-waste reduction targets aligned with SDG 12.3, underpinning policy support for shelf-life technologies.

- October 2024: Indonesia’s food-contact draft law set migration limits for paper and cardboard packs, to be enforced within 12 months.

Global Oxygen-Scavenger Paper Packaging Market Report Scope

| Iron-based Metallic |

| Non-Ferrous Metallic |

| Enzyme-based |

| Polymer-Integrated |

| Natural Bio-based |

| Nano-Metal / Composite |

| Coated Kraft and SBS |

| Greaseproof / Waxed |

| Multilayer Bio-papers |

| Label Stock and Inserts |

| Corrugated Linerboard |

| Sachet / Pad Insert |

| Coating Impregnation |

| Multilayer Laminate |

| Micro-encapsulated Label / Ink |

| Food and Beverage | Meat and Seafood |

| Dairy Products | |

| Bakery and Confectionery | |

| Fruits and Vegetables | |

| Ready-to-Eat Meals | |

| Pharmaceuticals and Nutraceuticals | |

| Industrial and Electronics | |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Thailand | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | GCC |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Scavenger Chemistry | Iron-based Metallic | ||

| Non-Ferrous Metallic | |||

| Enzyme-based | |||

| Polymer-Integrated | |||

| Natural Bio-based | |||

| Nano-Metal / Composite | |||

| By Paper Substrate | Coated Kraft and SBS | ||

| Greaseproof / Waxed | |||

| Multilayer Bio-papers | |||

| Label Stock and Inserts | |||

| Corrugated Linerboard | |||

| By Integration Method | Sachet / Pad Insert | ||

| Coating Impregnation | |||

| Multilayer Laminate | |||

| Micro-encapsulated Label / Ink | |||

| By End-use Industry | Food and Beverage | Meat and Seafood | |

| Dairy Products | |||

| Bakery and Confectionery | |||

| Fruits and Vegetables | |||

| Ready-to-Eat Meals | |||

| Pharmaceuticals and Nutraceuticals | |||

| Industrial and Electronics | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| France | |||

| United Kingdom | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Thailand | |||

| Indonesia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | GCC | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the oxygen-scavenger paper packaging market?

The market is valued at USD 378.56 million in 2025 with a forecast to reach USD 496.17 million by 2030 at a 5.56% CAGR.

Which segment holds the largest market share?

Iron-based scavenger systems account for 45.13% of revenue, maintaining leadership due to proven performance in food preservation.

Which region is growing fastest?

Asia-Pacific is projected to expand at a 7.14% CAGR through 2030, supported by emerging packaging regulations and a surge in e-commerce.

Why are polymer-integrated scavengers gaining traction?

They deliver high oxygen-uptake capacity while enabling mono-material paper designs that meet 2030 recyclability targets.

How do light-activated scavenger coatings work?

They embed photocatalysts like titanium dioxide within the paper matrix, absorbing oxygen when exposed to UV light, preventing premature scavenger exhaustion during storage.

What are the main barriers to wider adoption?

Higher unit costs, moisture sensitivity in tropical climates, potential off-odors in premium foods, and recycling challenges linked to multilayer constructions remain key restraints.

Page last updated on: