Market Overview

| Study Period | 2020 - 2031 |

|---|---|

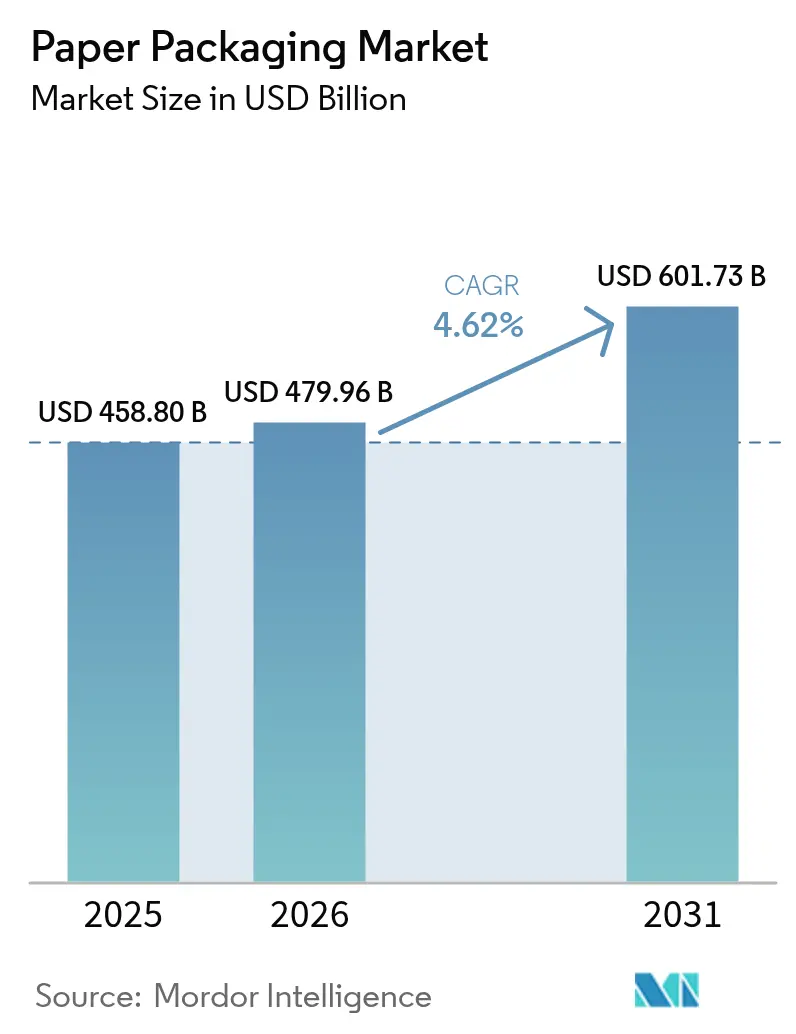

| Market Size (2026) | USD 479.96 Billion |

| Market Size (2031) | USD 601.73 Billion |

| Growth Rate (2026 - 2031) | 4.62% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Paper Packaging Market Analysis by Mordor Intelligence

The paper packaging market size was valued at USD 458.8 billion in 2025 and estimated to grow from USD 479.96 billion in 2026 to reach USD 601.73 billion by 2031, at a CAGR of 4.62% during the forecast period (2026-2031). This expansion is propelled by environmental regulations that reward recyclable substrates, the continued rise of online retail, and rapid progress in bio-based barrier coatings that let paper compete with plastics on moisture and grease resistance. Producers benefit from Extended Producer Responsibility fee schedules that lower compliance costs for fiber-based materials relative to multilayer plastics. At the same time, investments in nano-cellulose technology promise PFAS-free performance that aligns with looming U.S. and EU chemical phase-outs. Supply-side flexibility, powered by digital printing and smaller batch economics, is enabling converters to serve short-run, highly customized campaigns at attractive margins, expanding addressable volume for the paper packaging market.

Key Report Takeaways

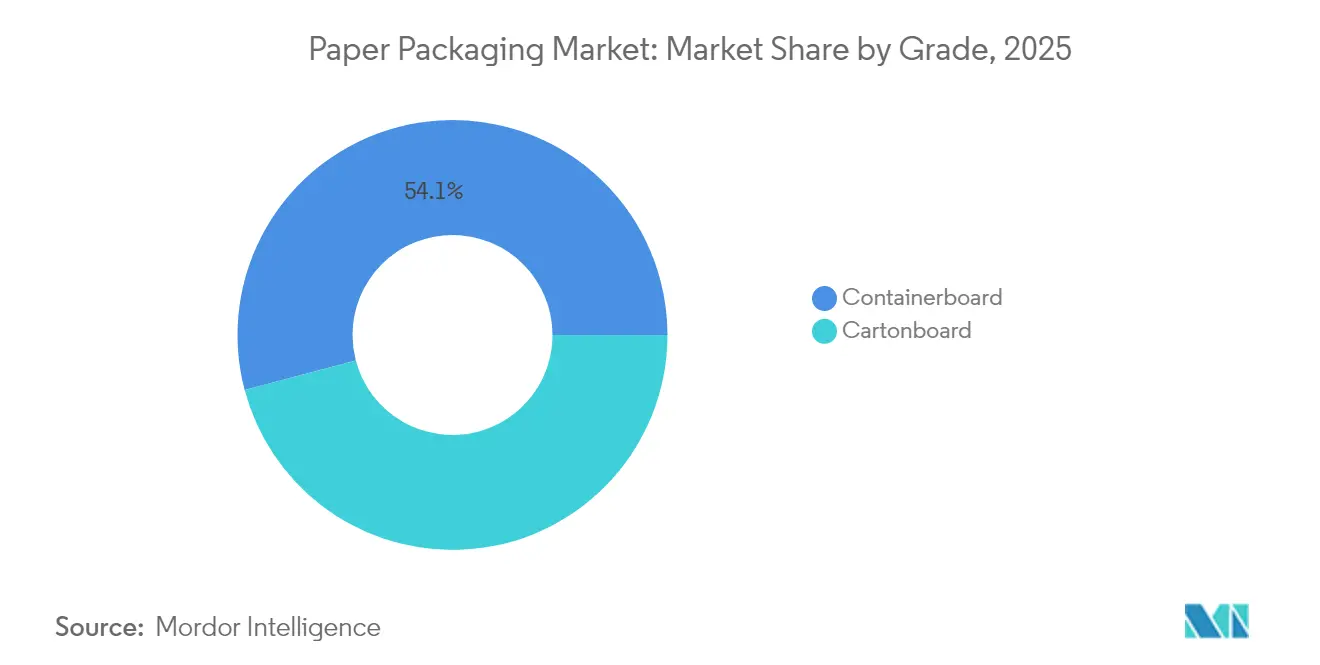

- By grade, containerboard captured 54.12% of the paper packaging market share in 2025.

- By product, the paper packaging market size for folding cartons is projected to grow at a 5.12% CAGR between 2026-2031.

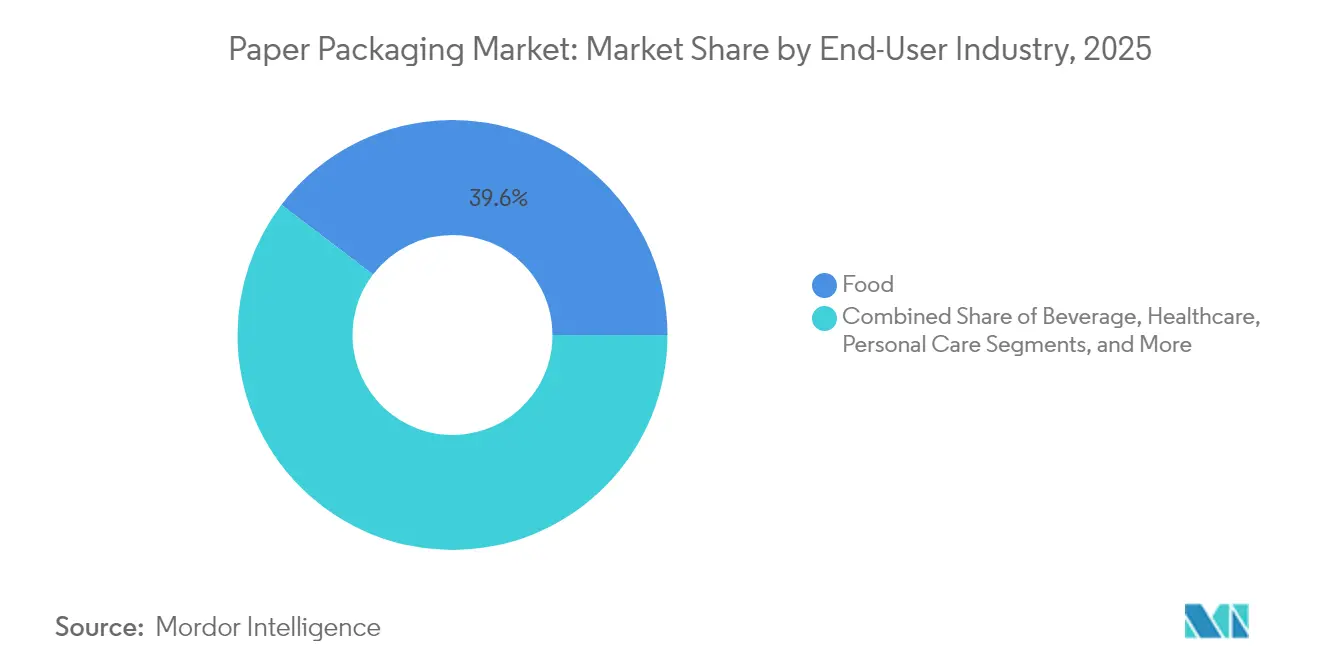

- By end-user, food captured 39.64% of the paper packaging market share in 2025.

- By packaging format, the market size for molded fibre and pulp is projected to grow at a 6.62% CAGR between 2026-2031.

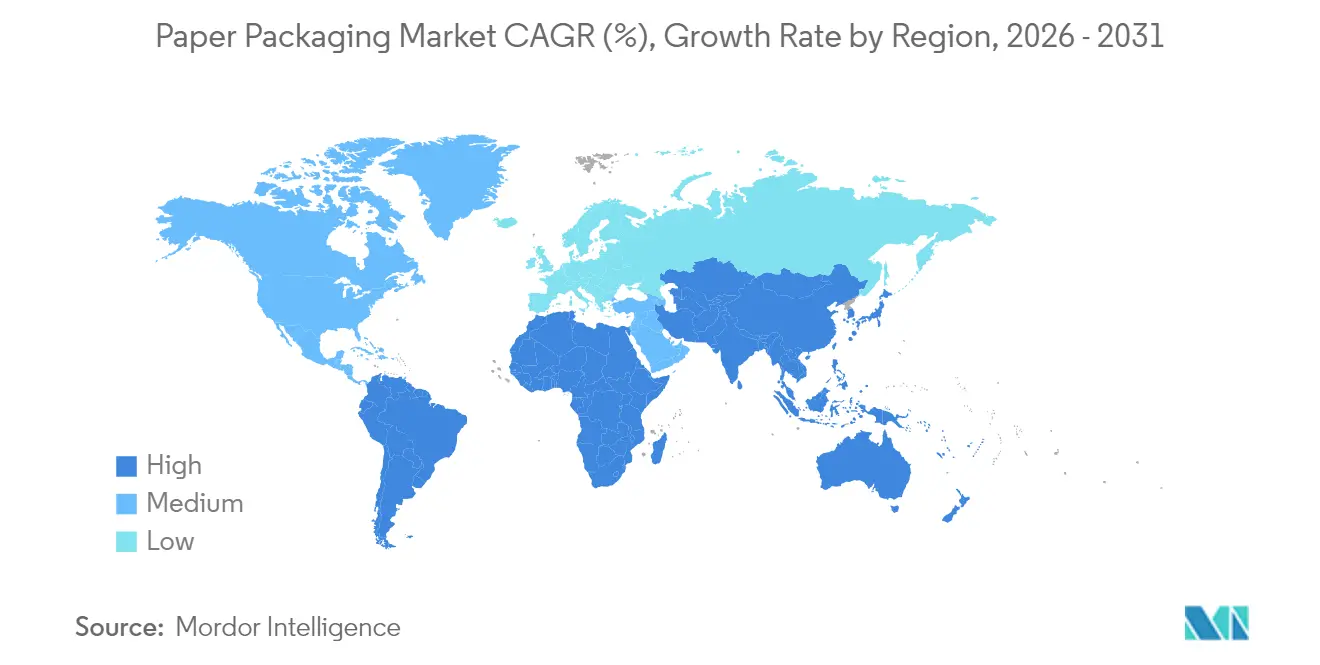

- By geography, the Asia-Pacific captured 47.62% of the paper packaging market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Paper Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Development of barrier-coated paperboard solutions | +1.2% | Global; early adoption in North America and EU | Medium term (2-4 years) |

| Rise in e-commerce corrugated demand | +1.8% | Global; strongest in Asia-Pacific and North America | Short term (≤ 2 years) |

| Brand-owner shift toward mono-material packs | +0.9% | EU and North America, expanding to APAC | Medium term (2-4 years) |

| Extended Producer Responsibility mandates | +1.1% | EU, UK, select U.S. states, expanding globally | Long term (≥ 4 years) |

| Nano-cellulose barrier breakthroughs | +0.7% | North America and Nordic countries; pilot in Asia | Long term (≥ 4 years) |

| Converting-plant on-site digital printing economics | +0.6% | Global; premium applications in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Development of Barrier-Coated Paperboard Solutions Drive Premium Applications

Advanced water-, oxygen-, and grease-barrier coatings based on bio-polymers and nano-cellulose are elevating paper’s performance while preserving its recyclability. Laboratory trials show that cellulose nanofibril coatings can reduce oxygen transmission by more than 90% and double folding endurance compared with uncoated board.[1]“Blending of cellulose nanofibers with cotton linter pulp to enhance the mechanical and barrier properties of paper,” Nature, nature.com The U.S. Food & Drug Administration confirmed that grease-proofing agents containing PFAS have exited the food-contact market, shifting demand toward safer chemistries. In Europe, several converters are fast-tracking industrial runs of boric-acid-cross-linked poly(vinyl alcohol) coatings that deliver robust water vapor protection and meet compostability standards. As brand owners pursue plastic replacement without compromising shelf life, premium barrier-coated board is becoming the default for ready-to-eat foods, frozen meals, and personal-care gift packs, boosting value growth in the paper packaging market.

E-Commerce Corrugated Demand Surge Reshapes Production Priorities

Global online retail continues to outperform brick-and-mortar channels, and each parcel requires protective, stackable outer packaging that can withstand automated handling. Corrugated cases now account for an estimated 80% of e-commerce shipments, cementing their role as the workhorse for last-mile logistics. Asian mega-markets led by China and India added double-digit billions of parcels in 2024, prompting box-plant expansions and high-speed digital print lines dedicated to web-shop volumes. The production mix is shifting toward lightweight fluting profiles that cut freight costs yet retain compression strength, and integrated producers are prioritizing incremental containerboard tonnage over graphic paper grades to keep pace with e-commerce pull-through. This demand foundation underpins steady volume growth for the paper packaging market in both mature and emerging economies.

Brand-Owner Migration Toward Mono-Material Packaging Architectures

Consumer-product companies are redesigning packs to meet the EU Packaging and Packaging Waste Regulation target of universal recyclability by 2030. Eliminating multilayer laminates reduces separation complexity in material-recovery facilities and lowers EPR fees. Mono-material paper solutions now cover dry foods, household powders, and certain confectionery lines, using dispersion or polymer-based barriers that remain compatible with standard paper recycling loops. The design shift also simplifies communication of sustainability credentials on pack and supports carbon-footprint reporting. These dynamics channel incremental volumes toward the paper packaging market and reward converters that can certify fiber provenance and recyclability.

Extended Producer Responsibility Mandates Accelerate Market Transformation

The United Kingdom’s fee schedule, already live, charges brand owners higher rates for hard-to-recycle plastics than for readily recyclable fiber. February 2025 marks the synchronized launch of harmonized EPR across the EU, followed by a wave of U.S. state programs. Differential pricing immediately improves the total cost of ownership for recyclable paper formats, prompting pack-switch roadmaps in grocery, foodservice, and personal care. Converters are investing in material-identification printing and QR code tracking to document collection performance, an emerging requirement for next-generation EPR compliance. The result is an institutional tailwind that sustains the long-run CAGR of the paper packaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Deforestation and fibre-supply scrutiny | -0.8% | Global, particularly affecting U.S.–EU trade | Medium term (2-4 years) |

| Volatile recycled-fibre pricing | -1.1% | Global; acute impact in Europe and North America | Short term (≤ 2 years) |

| PFAS “forever-chemicals” phase-out costs | -0.6% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| Limited recovery logistics in emerging markets | -0.9% | Asia-Pacific, Latin America, Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Deforestation Scrutiny Challenges Traditional Supply-Chain Structures

The EU Deforestation Regulation obliges importers to demonstrate plot-level traceability for all wood-based inputs by the end of 2025. U.S. Kraft pulp, representing 60% of EU specialty-grade imports, must now carry geo-coordinates verified by third parties.[2]American Forest & Paper Association, “Why the EU Needs to Reconsider Their Deforestation Law,” afandpa.org Implementing satellite monitoring and chain-of-custody audits raises procurement costs and risks of shipment delays. Smaller mills lacking sophisticated data systems may cede share to vertically integrated majors with certified forests, altering competitive balances within the paper packaging market. Over time, tighter provenance rules could squeeze supply and curb the sector’s growth potential in markets that rely on imported fiber.

Volatile Recycled-Fiber Pricing Creates Margin Compression Pressures

Recovered-fiber indices in Europe swung more than USD 50 per ton between Q1 2024 and Q4 2024 as containerboard capacity additions outpaced collection growth. Converters chasing lightweight grades are particularly exposed to price spikes, while contracts indexed to virgin kraft pulp offer limited offset. Short-cycle cost inflation challenges pass-through to end users, eroding EBITDA margins for integrated players. Hedging strategies and inventory buffers mitigate volatility but tie up working capital. Persistent price swings could temper the otherwise steady trajectory of the paper packaging market unless collection rates improve and export restrictions on waste paper ease.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: Cartonboard Innovation Accelerates Despite Containerboard Dominance

Containerboard held a 54.12% paper packaging market share in 2025, supported by deep corrugated infrastructure and its central role in e-commerce shipping. Meanwhile, cartonboard is registering a 7.05% CAGR, the fastest among fiber grades. The paper packaging market size for cartonboard applications is projected to rise, reflecting premium penetration in food and personal-care sleeves. Converters are refitting idle graphic-paper machines with coating heads suited to Solid Bleached Sulfate and Folding Boxboard production, improving asset utilization. Folding Boxboard’s compatibility with high-definition digital print elevates shelf appeal, while dispersion-barrier upgrades enable chilled-food entry. At the same time, containerboard producers are investing in lightweight kraftliner to cut shipping mass, enhancing sustainability credentials. Virgin-recycled blends optimize strength-to-weight ratios and keep containerboard competitive, ensuring it remains the volume backbone of the paper packaging market.

Cartonboard’s growth profile attracts capital for rapid European and North American capacity expansions, with start-ups exceeding 1 million tons by 2026. Food-contact certification and pharmaceutical clean-room compliance boost value per ton, particularly for solid-bleached grades. Regulatory bans on black plastics in several EU countries redirect premium confectionery and cosmetic packs to white cartonboard formats, lifting demand further. Performance-enhancing additives such as nano-clays deliver moisture barriers without compromising recyclability, reducing reliance on plastic films. As retail brands demand mono-material packs that convey quality and sustainability, cartonboard emerges as the prime beneficiary within the paper packaging market.

By Product: Folding Cartons Gain Momentum Through Digital Printing Capabilities

Corrugated boxes occupied 61.48% of the paper packaging market in 2025 owing to their unmatched protective strength and versatility across shipping, industrial, and grocery channels. Folding cartons, however, are forecast to outpace overall growth, expanding at a 5.12% CAGR on the back of personalized graphics, quick-response seasonal campaigns, and smaller lot sizes. Digital printheads integrated into die-cutters reduce changeover times, paving the way for mass-customization without costly inventories. Premium beauty, nutraceuticals, and plant-based foods all favor folding cartons for their aesthetic flexibility and shelf-ready formats.

Corrugated producers respond with inside-print and high-color capabilities to keep hold of branding real estate, but folding cartons maintain an edge in tactile finishes and embossing. Consumer-electronics accessories increasingly shift from plastic clamshells to reinforced cartons married with molded-fiber inserts, capturing sustainability-minded shoppers. Novel tear-strip opening features borrowed from flexible pouches further boost convenience. These design and technology advances underpin steady share migration within the broader paper packaging market.

By End-User Industry: Personal Care Emerges as Premium Growth Driver

Food applications provided 39.64% of paper packaging market revenue in 2025, spanning corrugated produce crates, cartonboard cereal boxes, and molded-fiber takeaway containers. Despite its maturity, the segment adds incremental volume thanks to PFAS-free grease barriers compliant with FDA guidance and single-use plastic bans in quick-service dining. The personal-care segment, while smaller, will post a 7.08% CAGR to 2031 as brands converge on sustainable, Instagram-worthy packs that align with clean-beauty messaging. Folding cartons with metallic foils swapped for recyclable dispersion coatings preserve luxury cues while meeting recycling guidelines.

E-commerce beauty subscription services demand robust yet elegant shippers, stimulating hybrid formats that pair lightweight corrugated outers with cartonboard inner trays. Meanwhile, the beverage, healthcare, and electronics sectors adopt molded-fiber bottle carriers, blister replacements, and cushioned trays, respectively, to meet corporate carbon budgets. This multi-industry uptake cements the growth runway for the paper packaging market.

By Packaging Format: Molded Fiber Technologies Challenge Traditional Hierarchies

Rigid formats, chiefly corrugated cases and solid board, accounted for 45.71% of 2025 revenue, reflecting legacy dominance in shipping and bulk retail. Molded-fiber solutions, historically limited to egg cartons, are scaling rapidly with a forecast 6.62% CAGR as press-form tooling and dry-molded processes deliver crisp geometry and smooth surfaces. Rapid-cycle hot-press lines slash water usage by up to 70% compared with conventional slurry methods, and in-mold barrier sprays confer splash resistance suitable for quick-service beverage lids.

Semi-rigid folding cartons continue to exploit digital upgrades and barrier lamination for frozen-food and ready-meal categories, whereas flexible paper wraps fill niche needs for sugar sachets and instant soup pouches. With regulators tightening compostability and plastic-tax thresholds, molded fiber stands to capture incremental share, aided by lignin-reinforced formulations that elevate wet tensile strength. Together, these format innovations expand the addressable universe for the paper packaging market.

Geography Analysis

Asia-Pacific led the paper packaging market with a 47.62% revenue share in 2025 and is projected to record a 5.51% CAGR to 2031. Rapid urbanization, expanding middle-class purchasing power, and large-scale food-delivery ecosystems underpin fiber demand in South and Southeast Asia. Regional players leverage cost-efficient integrated mills that pair plantation forests with in-house converting, shortening lead times for export-oriented customers. Local governments incentivize sustainable-pack investments through duty rebates on energy-efficient machinery, further accelerating capacity additions.

North America remains an innovation nucleus, driving digital-print adoption and spearheading nano-cellulose pilot commercialization. Tightening landfill legislation in several states spurs demand for curbside-recyclable packs, bolstering domestic containerboard offtake. The United States also benefits from abundant softwood resources, ensuring steady virgin-fiber availability to blend with imported OCC. Meanwhile, Europe’s stringent recyclability targets and EPR rollouts create a predictable policy environment that favors continuous equipment upgrades. German and Scandinavian mills transition from fossil to biomass boilers, reducing Scope 1 emissions and sharpening cost competitiveness despite high energy prices.

Latin America and the Middle East and Africa collectively hold modest shares today, yet both regions register above-global average growth. Brazilian pulp producers integrate downstream into cartonboard to mitigate commodity cycles, while Gulf Cooperation Council economies add corrugated capacity to serve expanding e-commerce hubs. Africa’s underdeveloped collection network hinders recycled-fiber supply, but international development programs are funding pilot materials-recovery facilities, laying groundwork for future circularity. Collectively, these regional trajectories reinforce the diversified demand base that supports the long-term resilience of the paper packaging market.

Competitive Landscape

The sector exhibits moderate concentration, with the top five companies controlling roughly 45% of global revenue. The newly formed Smurfit WestRock immediately became the largest integrated player, operating more than 500 converting sites worldwide and focusing on containerboard synergies.[3]Smurfit WestRock, “Merger Completion Announcement,” smurfitwestrock.com International Paper, Mondi, and Graphic Packaging extend vertical control from certified forests through high-graphic folding cartons, while investing heavily in barrier science and digital workflows. Geographic diversification shields majors from regional demand shocks, yet exposes them to varying regulatory regimes and fiber-price volatility.

Strategic maneuvers center on portfolio re-mix: International Paper’s agreed divestiture of several European plants cleared antitrust hurdles and unlocked USD 1.1 billion for North American corrugated upgrades. Suzano’s 2024 acquisition of two U.S. mills marked a downstream push that secures offtake for its Brazilian hardwood pulp. On the technology front, Mondi’s Austrian facility commissioned a pilot nano-cellulose coater capable of 220 m/min, targeting snack-food liners that conform to EU PFAS restrictions. Graphic Packaging’s Better, Every Day roadmap commits to net-zero greenhouse-gas emissions by 2050, aligning capital allocation with decarbonization.

Mid-tier independents differentiate through specialty niches such as grease-resistant wraps or molded-fiber wine shippers. Licensing deals with university spin-offs accelerate the commercialization of lignin-enhanced boards, while joint ventures with chemical suppliers secure access to compostable barrier polymers. Competitive intensity remains high in mature regions, but disciplined capital expenditure and disciplined price-setting maintain rational margins, sustaining investor confidence in the paper packaging market.

Paper Packaging Industry Leaders

International Paper Company

Smurfit Westrock plc

Mondi plc

Packaging Corporation of America

Stora Enso Oyj

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: European Commission approves International Paper’s acquisition of DS Smith conditional on divesting five European plants to address competition concerns in corrugated sheets and cases markets across Portugal, Spain, and France.

- August 2024: Graphic Packaging announces 2050 net-zero greenhouse-gas-emissions goal as part of its Better, Every Day sustainability program aligned with Paris Agreement objectives.

- July 2024: Suzano completes acquisition of two U.S. industrial facilities from Pactiv Evergreen for USD 110 million, adding 420,000 metric-ton annual paperboard capacity in Arkansas and North Carolina.

- July 2024: Smurfit Kappa and WestRock finalize merger to form Smurfit WestRock, a combined entity with more than USD 34 billion in revenues.

Global Paper Packaging Market Report Scope

Paper is frequently used to package products in several end-user industries. There are numerous grades of paperboard packaging. Paperboard, like folding cartons, is the most common material used in the manufacturing of containers. In the manufacturing process, the paperboard requires pulping, bleaching (optional), refining, sheet forming, drying, calendaring, and winding. Paper packaging materials can be efficiently reused and recycled compared to other materials, such as metals and plastics. This is why paper packaging is considered an eco-friendly and economical form of packaging.

- The paper packaging market is segmented by grade (carton board [solid bleached sulfate (SBS), solid unbleached sulfate (SUS), folding boxboard (FBB), coated recycled board (CRB), uncoated recycled board (URB)] and containerboard [white-top kraft-liner, other kraft-liners, white top test-liner, other test-liners, semi-chemical fluting, and recycled fluting]), product type (folding cartons and corrugated boxes), end-user industry (food, beverage, healthcare, personal care, household care, and electrical products) and geography (North America [United States and Canada], Europe [Germany, United Kingdom, Italy, France, and Rest of Europe], Asia-Pacific [China, Japan, India, and Rest of Asia-Pacific], Latin America [Brazil, Mexico, and Rest of Latin America], and Middle East and Africa [United Arab Emirates, Saudi Arabia, South Africa, and Rest of Middle East and Africa]). The market size and forecasts are provided in terms of value (USD) for all the above segments.

By Grade

| Cartonboard | Solid Bleached Sulphate (SBS) |

| Solid Unbleached Sulphate (SUS) | |

| Folding Boxboard (FBB) | |

| Coated Recycled Board (CRB) | |

| Uncoated Recycled Board (URB) | |

| Other Cartonboard Grades | |

| Containerboard | White-top Kraftliner |

| Other Kraftliners | |

| White-top Testliner | |

| Other Testliners | |

| Semi-chemical Fluting | |

| Recycled Fluting |

By Product

| Folding Cartons |

| Corrugated Boxes |

| Other Products |

By End-User Industry

| Food |

| Beverage |

| Healthcare |

| Personal Care |

| Household Care |

| Electrical and Electronics |

| Other End-User Industries |

By Packaging Format

| Rigid (Corrugated, Solid Board) |

| Semi-rigid (Folding Cartons) |

| Flexible Paper (Sachets, Wraps) |

| Molded Fibre and Pulp |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Grade | Cartonboard | Solid Bleached Sulphate (SBS) | |

| Solid Unbleached Sulphate (SUS) | |||

| Folding Boxboard (FBB) | |||

| Coated Recycled Board (CRB) | |||

| Uncoated Recycled Board (URB) | |||

| Other Cartonboard Grades | |||

| Containerboard | White-top Kraftliner | ||

| Other Kraftliners | |||

| White-top Testliner | |||

| Other Testliners | |||

| Semi-chemical Fluting | |||

| Recycled Fluting | |||

| By Product | Folding Cartons | ||

| Corrugated Boxes | |||

| Other Products | |||

| By End-User Industry | Food | ||

| Beverage | |||

| Healthcare | |||

| Personal Care | |||

| Household Care | |||

| Electrical and Electronics | |||

| Other End-User Industries | |||

| By Packaging Format | Rigid (Corrugated, Solid Board) | ||

| Semi-rigid (Folding Cartons) | |||

| Flexible Paper (Sachets, Wraps) | |||

| Molded Fibre and Pulp | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the global paper packaging market in 2026?

The paper packaging market size is valued at USD 479.96 billion in 2026.

What CAGR is projected for paper-based packs between 2026 and 2031?

The market is forecast to expand at a 4.62% CAGR through 2031.

Which region contributes the highest revenue?

Asia-Pacific delivers 47.62% of global sales and is also the fastest-growing region.

Which product category is gaining the most momentum?

Folding cartons are advancing at a 5.12% CAGR due to digital printing and premium branding demands.

Why are barrier-coated boards important?

Next-generation coatings replace PFAS, offer superior moisture and oxygen resistance, and keep packs fully recyclable, satisfying brand and regulatory expectations.

How are Extended Producer Responsibility fees influencing material choice?

EPR schemes charge lower rates for recyclable fiber than for difficult-to-recycle plastics, tilting economic advantage toward paper packaging.

Page last updated on: