Sensor-Enabled Paper Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

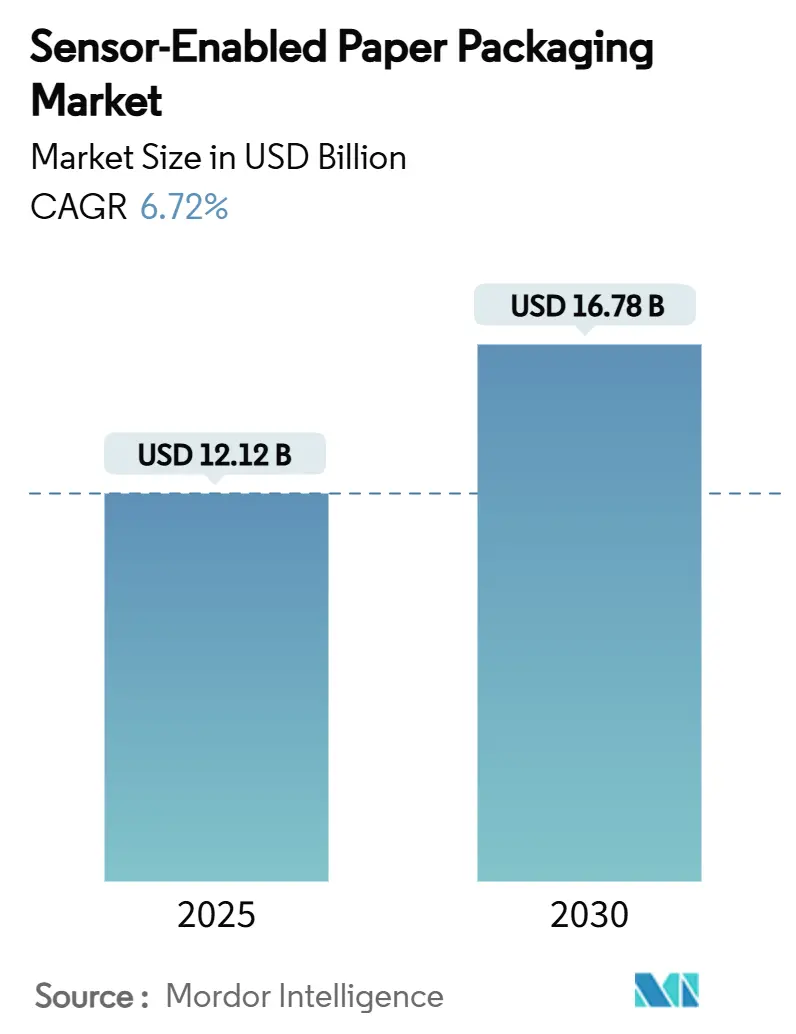

| Market Size (2025) | USD 12.12 Billion |

| Market Size (2030) | USD 16.78 Billion |

| Growth Rate (2025 - 2030) | 6.72% CAGR |

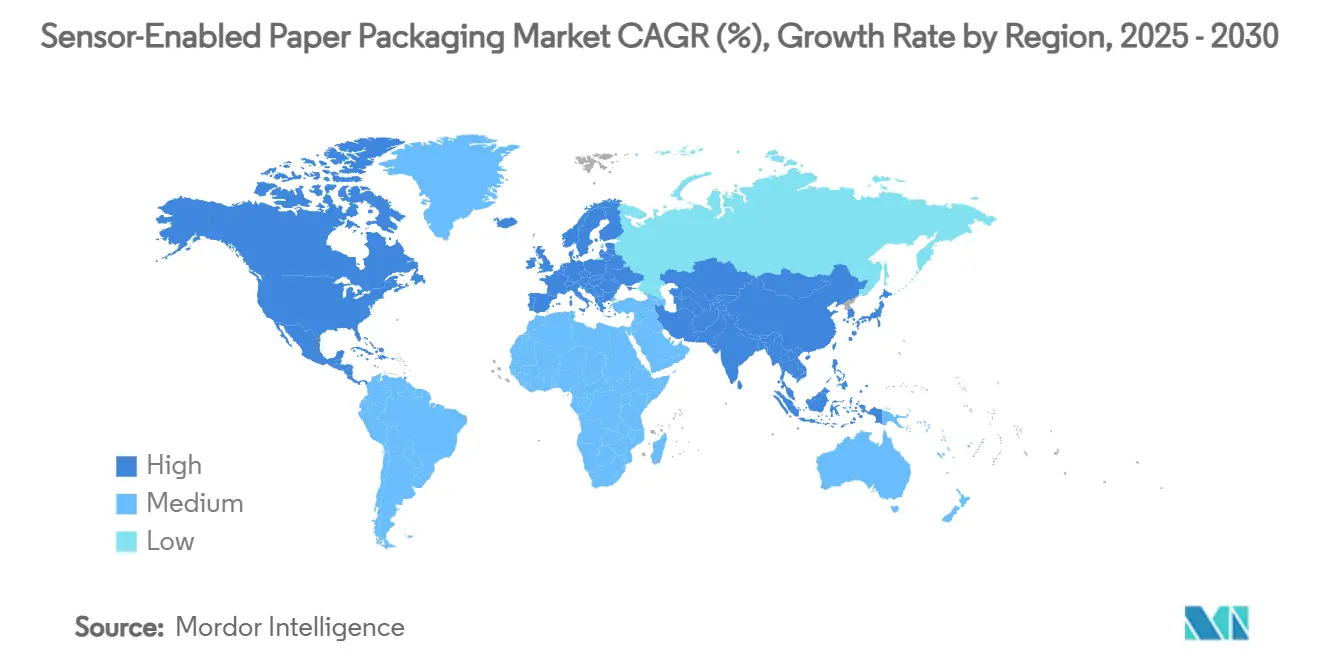

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sensor-Enabled Paper Packaging Market Analysis by Mordor Intelligence

The sensor-enabled paper packaging market size is valued at USD 12.12 billion in 2025 and is forecast to reach USD 16.78 billion by 2030, registering a 6.72% CAGR over the period. This outlook reflects accelerating regulatory mandates such as FSMA 204 in the United States and the European Union’s Digital Product Passport coupled with brand commitments to plastic reduction, which collectively push fiber-based packs toward embedded sensing functions. E-commerce volume growth, especially in Asia-Pacific, intensifies demand for real-time shipment visibility, while rapid advances in printed electronics continue lowering tag costs and broadening viable use cases. Cold-chain integrity failures in food and pharmaceuticals highlight unmet needs for continuous temperature monitoring, positioning sensor-enabled paper packaging as a cost-effective alternative to plastic-based smart packs. Venture funding into bio-based inks and NFC-in-paper start-ups strengthens the innovation pipeline, even as recycling-stream contamination concerns and cost premiums remain short-term headwinds.

Key Report Takeaways

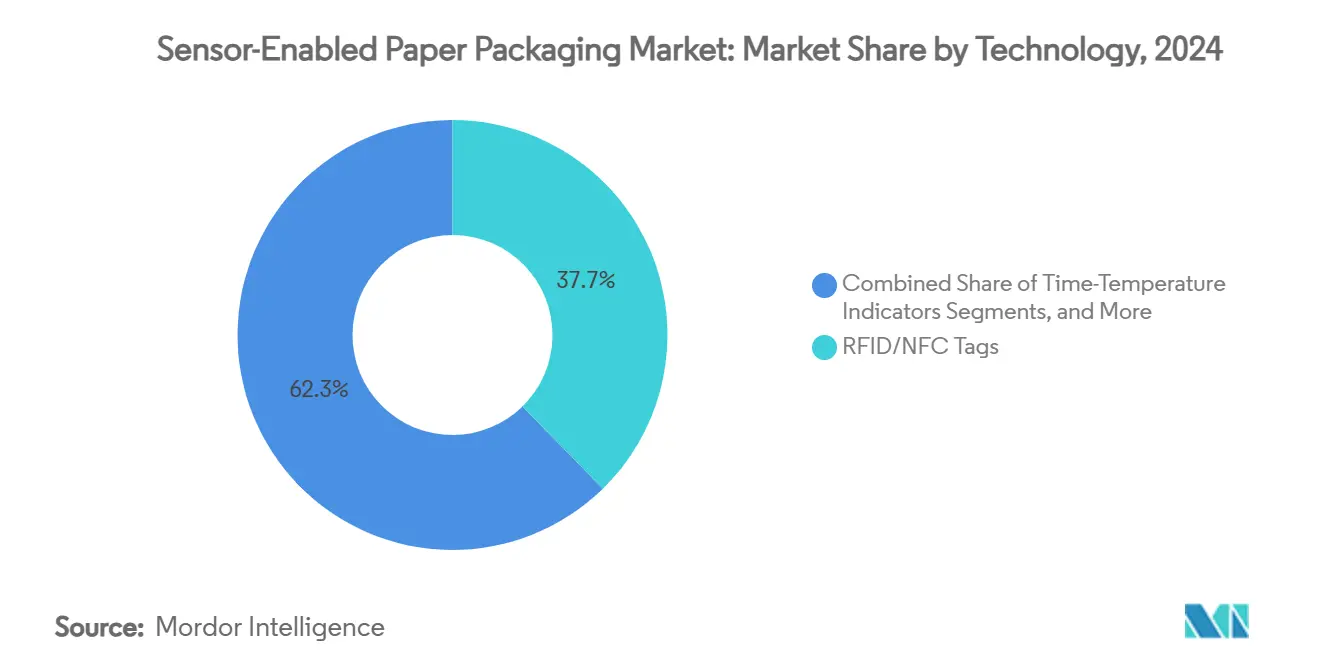

- By technology, RFID/NFC tags led with 37.67% of the sensor-enabled paper packaging market share in 2024.

- By packaging type, the sensor-enabled paper packaging market size for the labels and tags segment is projected to grow at a 16.75% CAGR between 2025-2030.

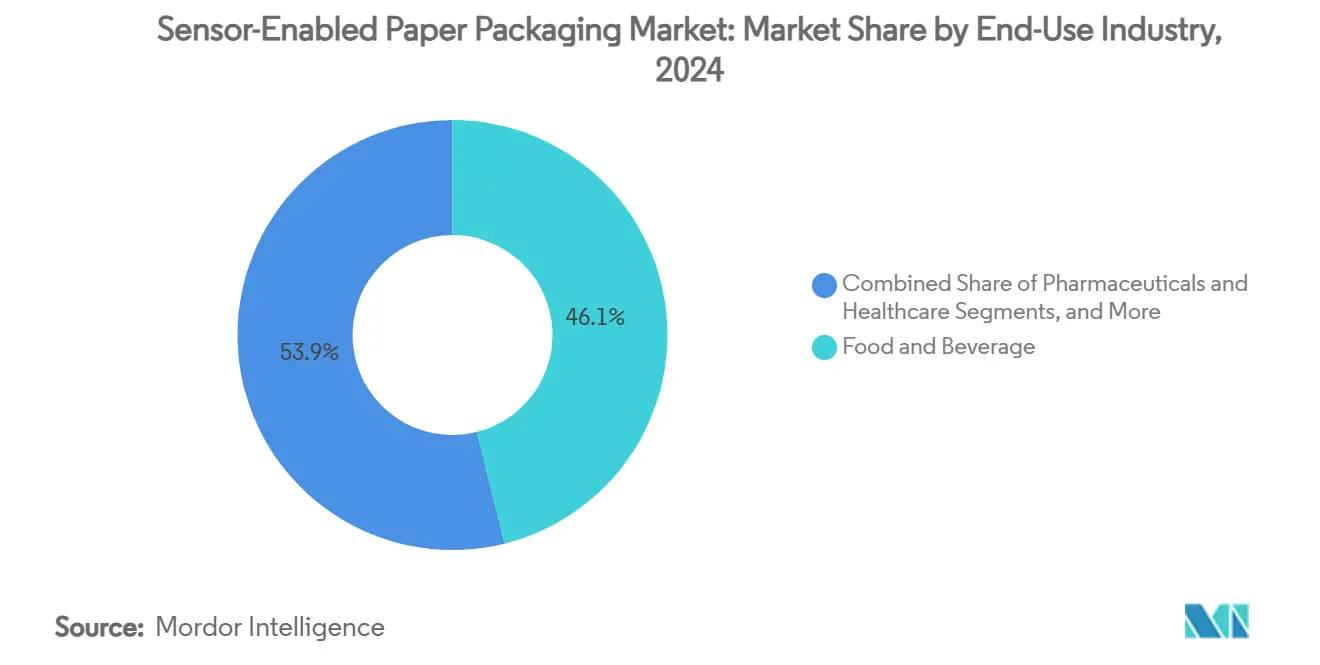

- By end-use industry, food and beverage held 46.12% of the sensor-enabled paper packaging market share in 2024.

- By geography, the sensor-enabled paper packaging market size for the Asia-Pacific region is projected to grow at a 6.12% CAGR between 2025-2030.

Global Sensor-Enabled Paper Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| End-to-end cold-chain traceability in perishable food shipments | +1.8% | Global, concentrated in North America and EU | Medium term (2-4 years) |

| Stricter food-safety and serialization regulations (FSMA 204, EU Digital Product Passport) | +1.5% | North America and EU primary, spillover to Asia-Pacific | Short term (≤2 years) |

| Surge in e-commerce and omnichannel logistics demanding track-and-trace solutions | +1.2% | Global, led by APAC and North America | Medium term (2-4 years) |

| Brand commitments to plastic reduction driving fiber-based smart packaging adoption | +0.9% | Global, strongest in EU and North America | Long term (≥4 years) |

| Rapid advances in printed electronics enabling low-cost chipless RFID on paper | +0.7% | Global, manufacturing concentrated in APAC | Medium term (2-4 years) |

| Venture funding into bio-based sensor inks and NFC-in-paper start-ups | +0.4% | North America and EU venture ecosystems | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Need for End-to-End Cold-Chain Traceability in Perishable Food Shipments

Cold-chain failures cost the global food industry USD 35 billion annually, with temperature excursions affecting 30% of pharmaceutical and 25% of fresh-produce shipments. Sensor-enabled paper packaging market solutions embed time-temperature indicators and gas sensors into fiber substrates, delivering continuous data that traditional packs lack. Japan’s METI spearheaded 2024 RFID pilots in convenience stores to automate inventory of short-shelf-life goods, cutting waste and boosting freshness compliance[1]Ministry of Economy, Trade and Industry, “Demonstration Tests to be Held for Food Waste Reduction Taking Advantage of Electronic Tags,” meti.go.jp. Paper-based pH sensors have demonstrated 95% accuracy in seafood freshness monitoring, underscoring commercial readiness . As GDP guidelines tighten temperature-documentation rules, pharmaceutical shippers increasingly specify fiber-based smart cartons to unify compliance and sustainability goals. Consequently, cold-chain traceability remains the single largest incremental driver of the sensor-enabled paper packaging market through 2030.

Stricter Food-Safety and Serialization Regulations (FSMA 204, EU Digital Product Passport)

The FDA’s FSMA 204 rule mandates traceability lot codes and key data elements for 16 high-risk food categories beginning January 2026, pushing suppliers to embed automatic data-capture technologies at the package level. In parallel, the EU’s Digital Product Passport requires lifecycle transparency for nearly all products sold in the bloc starting 2024, creating a contiguous compliance framework that favors sensor integration. GS1 standards have emerged as the interoperability backbone, standardizing RFID and NFC data structures across borders. Early adopters report faster recalls and lower labor costs due to automated record generation, offsetting sensor premiums. Because regulations are phased in over the next two years, adoption curves steepen rapidly in North America and Europe before diffusing to Asia-Pacific exporters serving those markets. Compliance assurance, therefore, becomes a core value proposition within the sensor-enabled paper packaging market.

Surge in E-Commerce and Omnichannel Logistics Demanding Track-and-Trace Solutions

Global parcel volume surpassed 100 billion units in 2024, with 40% requiring temperature control and 60% needing real-time tracking . Omnichannel retailers now expect item-level visibility from distribution center to doorstep, placing unprecedented stress on legacy barcodes. Avery Dennison’s Intelligent Labels platform gained a major U.S. grocery account in 2024, enhancing inventory accuracy and reducing shrinkage through paper-based UHF RFID tags . In Asia-Pacific, smartphone-readable NFC in folded cartons enables post-purchase engagement and warranty activation, aligning with markets where mobile commerce penetration exceeds 25%. The resulting data granularity feeds predictive analytics that optimize routing and replenishment, unlocking total-cost savings that outweigh incremental packaging spend. Consequently, omnichannel logistics represents a rapidly scaling revenue pool for the sensor-enabled paper packaging market.

Brand Commitments to Plastic Reduction Driving Fiber-Based Smart Packaging Adoption

More than 400 global brands have pledged to eliminate single-use plastics by 2030, prompting a pivot toward recyclable fiber packs that still deliver the interactive functions historically provided by plastics. The EU’s Packaging and Packaging Waste Regulation enforces recyclability and minimum recycled-content thresholds, making sensor-ready paper formats a compliance shortcut. Amcor’s AmFiber Performance Paper, granted a European patent in January 2025, demonstrates that high-barrier recyclable substrates can securely host printed antennas and humidity sensors without compromising fiber recovery rates. Consumer electronics and cosmetics brands use these packs to couple tamper evidence with digital storytelling via smartphone-tap experiences. Sustainability metrics from CO₂ reduction to curb-side recyclability thereby converge with digital-engagement KPIs, reinforcing adoption momentum across premium categories.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High unit costs of embedded sensors vs. razor-thin packaging margins | -1.1% | Global, most acute in price-sensitive APAC markets | Short term (≤2 years) |

| Recycling-stream contamination risk from electronic components | -0.8% | EU and North America with advanced recycling infrastructure | Medium term (2-4 years) |

| Lack of global interoperability standards for sensor data platforms | -0.6% | Global, particularly affecting cross-border supply chains | Medium term (2-4 years) |

| Data-privacy & cybersecurity concerns in consumer-facing smart packs | -0.4% | EU and North America with strict data-protection regulations | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Unit Costs of Embedded Sensors vs. Razor-Thin Packaging Margins

Traditional fiber packs cost USD 0.02–0.05 per unit, whereas sensor-integrated versions range from USD 0.15–0.50, representing up to a 1,000% premium that many low-margin goods cannot absorb. Gross margins for converters hover at 8–15%, so widespread adoption depends on either high-value products or ROI from waste reduction and theft prevention. Tetra Pak’s smart-carton pilot showed a 38.66% production-cost increase balanced by shelf-life gains in dairy products. APAC manufacturers feel the squeeze most acutely, given competitive pricing and limited willingness to pay for traceability. Market participants, therefore, focus on chipless RFID and printed indicators that bypass silicon costs, but serious price parity remains at least two years away.

Recycling-Stream Contamination Risk from Electronic Components

Embedded circuitry threatens fiber purity during pulping, jeopardizing the circular-economy rationale that underpins paper-based substitution[2]European Union, “Regulation (EU) 2025/40 on Packaging and Packaging Waste,” europa.eu . Regulation (EU) 2025/40 sets tight contamination thresholds, compelling producers to prove full recyclability. Existing mills cannot separate metallic antenna residues or polymer substrates, raising costs for specialty reclamation. Research into water-soluble conductors and cellulose-based boards offers potential relief, but commercial-scale trials remain limited. Until end-of-life solutions mature, buyers in Europe and North America may restrict sensor-enabled formats to closed-loop supply chains, capping near-term growth in those regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: RFID/NFC Dominance Amid Colorimetric Innovation

RFID/NFC tags captured 37.67% of the sensor-enabled paper packaging market share in 2024, supported by mature reader infrastructure across retail and logistics channels. Colorimetric and thermochromic inks, however, are forecast to log a 15.62% CAGR through 2030, driven by cost-effective spoilage indicators that require no electronics or special readers.

The sensor-enabled paper packaging industry increasingly pairs chipless RFID with gas-sensing overlays to meet dual goals of authentication and freshness monitoring. Time-temperature indicators remain essential in pharma and seafood exports, while emerging biosensors detect ethylene for produce shelf-life extension. Printed-electronics IP expansion signals ongoing cost compression, sustaining RFID/NFC leadership yet broadening the competitive set.

By Packaging Type: Corrugated Leadership with Labels Acceleration

Corrugated cartons commanded 41.23% of the sensor-enabled paper packaging market size in 2024 thanks to e-commerce’s preference for durable outer packs that house antennas without structural compromise. Labels and tags often applied post-conversion are projected to accelerate at 16.75% CAGR because brands want item-level analytics without overhauling primary packaging lines.

Carton board retains traction in fast-moving consumer goods where graphics matter, and flexible pouches integrate humidity spots for snack freshness cues. Specialty liquid boards add temperature strips to dairy and juice boxes. These hybrid paths illustrate how sensor-enabled paper packaging market solutions adapt form factors to diverse product geometries.

By End-Use Industry: Food Dominance with Cold-Chain Surge

Food and beverage held 46.12% of the sensor-enabled paper packaging market share in 2024 as FSMA 204 compliance and consumer demand for shelf-life data converged. Logistics and dedicated cold-chain applications are projected to register a 17.80% CAGR through 2030, reflecting pharmaceutical biologics growth and global vaccine distribution protocols.

Pharma packs embed serialized UHF tags and time-temperature strips to satisfy GDP guidelines, while consumer-electronics brands embed NFC for anti-counterfeit verification. Cosmetics leverage tap-to-reorder features, and industrial users monitor humidity for sensitive components. This breadth underscores the sensor-enabled paper packaging market’s cross-sector relevance.

Geography Analysis

Asia-Pacific leads both demand and production for the sensor-enabled paper packaging market. China’s integrated supply-chain ecosystem pairs low-cost converting with local printed-electronics fabs, accelerating adoption in cross-border e-commerce parcels. India’s market is expected to hit USD 204.81 billion in overall paper packaging value by 2025, and government incentives for MSME digitalization spur smart-pack trials [3]Invest India, “Paper & Packaging,” investindia.gov.in . Japan’s RFID pilots in convenience chains demonstrate policy-driven scaling models that reduce perishables waste.

North America remains pivotal because FSMA 204 imposes compulsory traceability for high-risk foods from January 2026. Cold-chain infrastructure already employs data-loggers, making the transition to disposable smart cartons seamless. Venture funding concentrates in Silicon Valley and Boston, nurturing biodegradable ink developers that partner with converters for pilot runs.

Europe’s Digital Product Passport and Regulation 2025/40 codify recyclability and transparency, intensifying R&D into detachable or soluble antennas to avoid mill contamination . Nordic and DACH countries pioneer curb-side recycling standards for sensor-enabled packs, while southern Europe focuses on high-value olive-oil and wine exports that justify premium traceability features. Middle East and Africa show nascent uptake, mainly in pharma re-exports through Gulf free zones and temperature-sensitive agrifood shipments to the EU.

Competitive Landscape

The sensor-enabled paper packaging market remains moderately fragmented, with the top five converters and technology providers collectively controlling under 30% of global revenue. International Paper, Smurfit WestRock, and Graphic Packaging leverage mill capacity and brand relationships to integrate sensing layers during corrugating or coating. Technology specialists Avery Dennison, Thinfilm Electronics, Blue Bite focus on printed circuitry, cloud platforms, and smartphone-based consumer experiences.

Strategic collaborations blur boundaries: Amcor partners with start-ups for bio-based inks, while Smurfit WestRock pilots chipless RFID embedded in single-wall liners for parcel post. Patent filings concentrate on flexible conductors, moisture-responsive substrates, and compostable antennas, signaling defensive IP strategies as unit costs drop.

Regulations increasingly shape competition. Converters with ISO 13485 or pharma-grade clean-room capacity secure contracts for vaccine packaging that demands validated sensors. Retailers favor vendors that bundle cloud dashboards with physical tags, accelerating vertical integration between material science and SaaS layers in the sensor-enabled paper packaging market.

Sensor-Enabled Paper Packaging Industry Leaders

Stora Enso Oyj

Avery Dennison Corp. (Smartrac)

Amcor plc

3M Company

Smurfit Westrock Plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Amcor received European patent protection for AmFiber Performance Paper, enabling high-barrier recyclable packs compatible with embedded sensors.

- July 2024: FDA updated food-contact-notification guidance, clarifying revocation procedures and easing approvals for new sensor substrates.

- February 2024: The EU officially launched the Digital Product Passport, mandating lifecycle transparency and spurring demand for smart packs.

- January 2024: Japan’s METI expanded RFID-enabled food-waste-reduction pilots in convenience stores nationwide.

Global Sensor-Enabled Paper Packaging Market Report Scope

| RFID / NFC Tags |

| Time-Temperature Indicators |

| Gas Sensors and Biosensors |

| Moisture and Humidity Sensors |

| Colorimetric and Thermochromic Inks |

| Others (QR / Printed Electronics) |

| Corrugated Boxes |

| Carton Board and Folding Cartons |

| Flexible Paper and Pouches |

| Labels and Tags |

| Others (Liquidboard, Specialty Papers) |

| Food and Beverage |

| Pharmaceuticals and Healthcare |

| Logistics and Cold Chain |

| Consumer Electronics |

| Cosmetics and Personal Care |

| Others (Industrial, Automotive) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Technology | RFID / NFC Tags | ||

| Time-Temperature Indicators | |||

| Gas Sensors and Biosensors | |||

| Moisture and Humidity Sensors | |||

| Colorimetric and Thermochromic Inks | |||

| Others (QR / Printed Electronics) | |||

| By Packaging Type | Corrugated Boxes | ||

| Carton Board and Folding Cartons | |||

| Flexible Paper and Pouches | |||

| Labels and Tags | |||

| Others (Liquidboard, Specialty Papers) | |||

| By End-use Industry | Food and Beverage | ||

| Pharmaceuticals and Healthcare | |||

| Logistics and Cold Chain | |||

| Consumer Electronics | |||

| Cosmetics and Personal Care | |||

| Others (Industrial, Automotive) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the sensor-enabled paper packaging market?

The market is valued at USD 12.12 billion in 2025 and is forecast to grow to USD 16.78 billion by 2030 at a 6.72% CAGR.

Which region leads the sensor-enabled paper packaging market?

Asia-Pacific leads with 37.25% share in 2024 and is projected to maintain the fastest growth at 6.12% CAGR through 2030.

Which technology segment dominates the market?

RFID/NFC tags dominate with 37.67% share in 2024 due to established infrastructure and broad supply-chain adoption.

What end-use industry generates the highest demand?

Food and beverage applications account for 46.12% of 2024 demand, driven by regulatory traceability and freshness-monitoring needs.

Why are brands shifting toward sensor-enabled paper packaging?

Corporate plastic-reduction commitments and strict EU recyclability rules push brands to adopt fiber-based packs that still deliver traceability, anti-counterfeit, and consumer-engagement functions.

Page last updated on: