Vietnam Integrated Facility Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

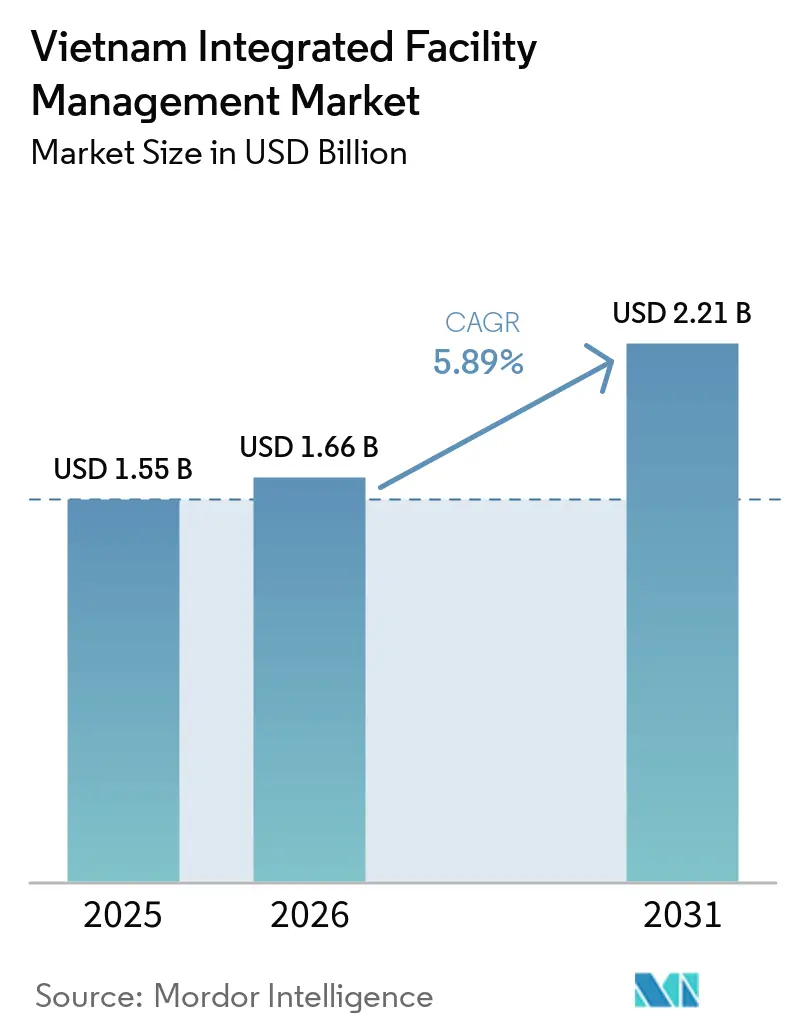

| Base Year Market Size (2025) | USD 1.55 Billion |

| Market Size (2026) | USD 1.66 Billion |

| Market Size (2031) | USD 2.21 Billion |

| Growth Rate (2026 - 2031) | 5.89% CAGR |

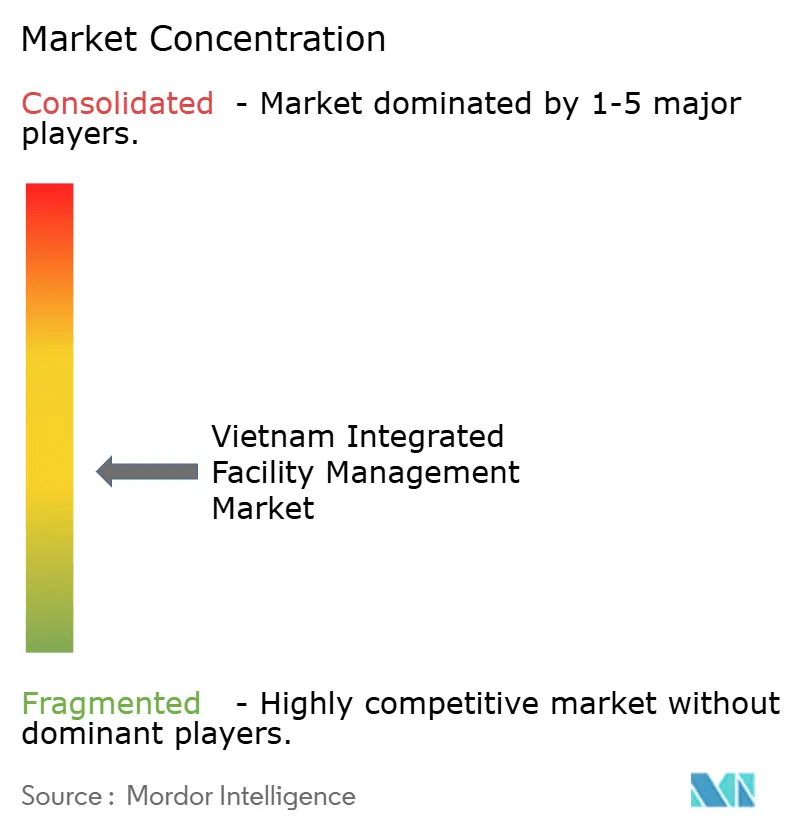

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Integrated Facility Management Market Analysis by Mordor Intelligence

The Vietnam Integrated Facility Management Market size is projected to be USD 1.55 billion in 2025, USD 1.66 billion in 2026, and reach USD 2.21 billion by 2031, growing at a CAGR of 5.89% from 2026 to 2031.

The Vietnam integrated facility management market is benefiting from Vietnam’s role in the China-plus-one production shift, which continues to bring in new factories, logistics assets, and office projects that need coordinated technical and support services. This demand is rising because newer facilities carry more complex operating needs, including MEP uptime, access control, energy tracking, fire safety compliance, and ongoing documentation that single-service outsourcing models cannot manage effectively at scale. Green-certified buildings and smart-enabled properties are also widening the service scope because building owners now need continuous monitoring, preventive maintenance, and reporting to protect asset performance and tenant retention. The Vietnam integrated facility management market is also being shaped by stricter procurement standards from multinational occupiers, who increasingly prefer vendors with structured quality, safety, and ESG delivery capabilities rather than loosely coordinated local subcontracting chains. Domestic competition remains fragmented and price-led in many mid-tier accounts, but that fragmentation is also creating room for integrated providers to consolidate contracts as building complexity and service expectations continue to rise.

Key Report Takeaways

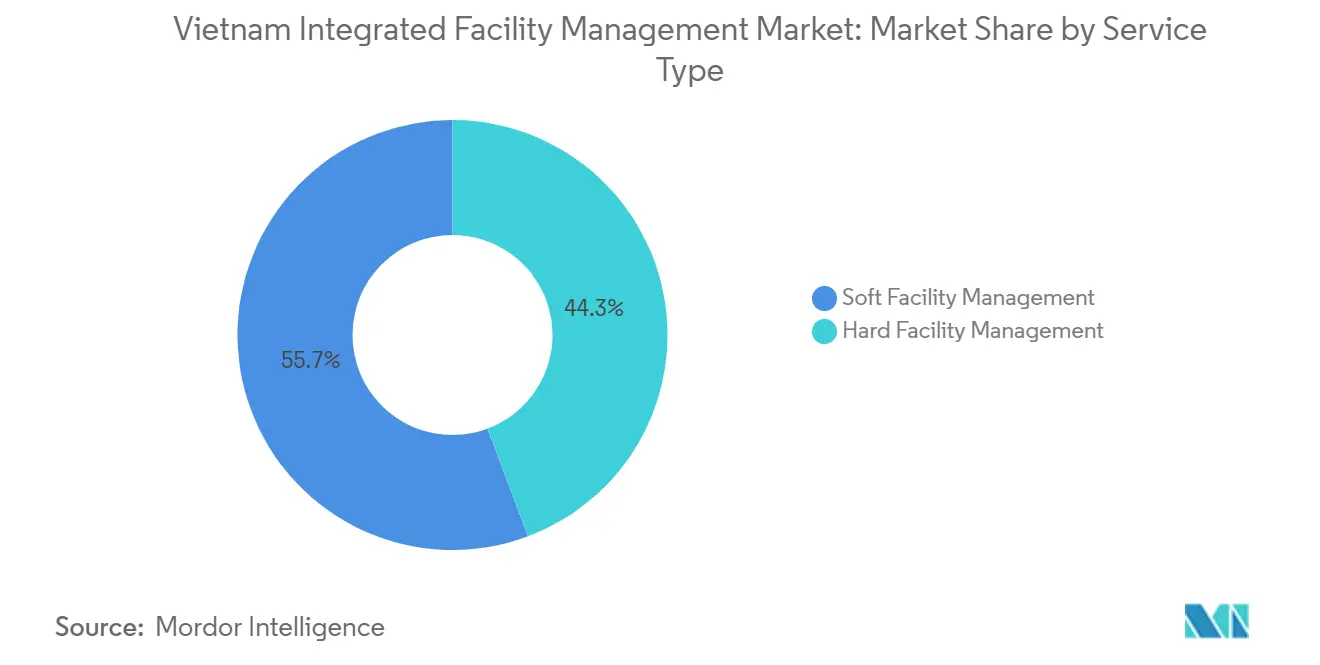

- By service type, Soft facility management led with 55.7% of the Vietnam integrated facility management market revenue share in 2025, while Hard FM is forecast to expand at a 6.4% CAGR through 2031.

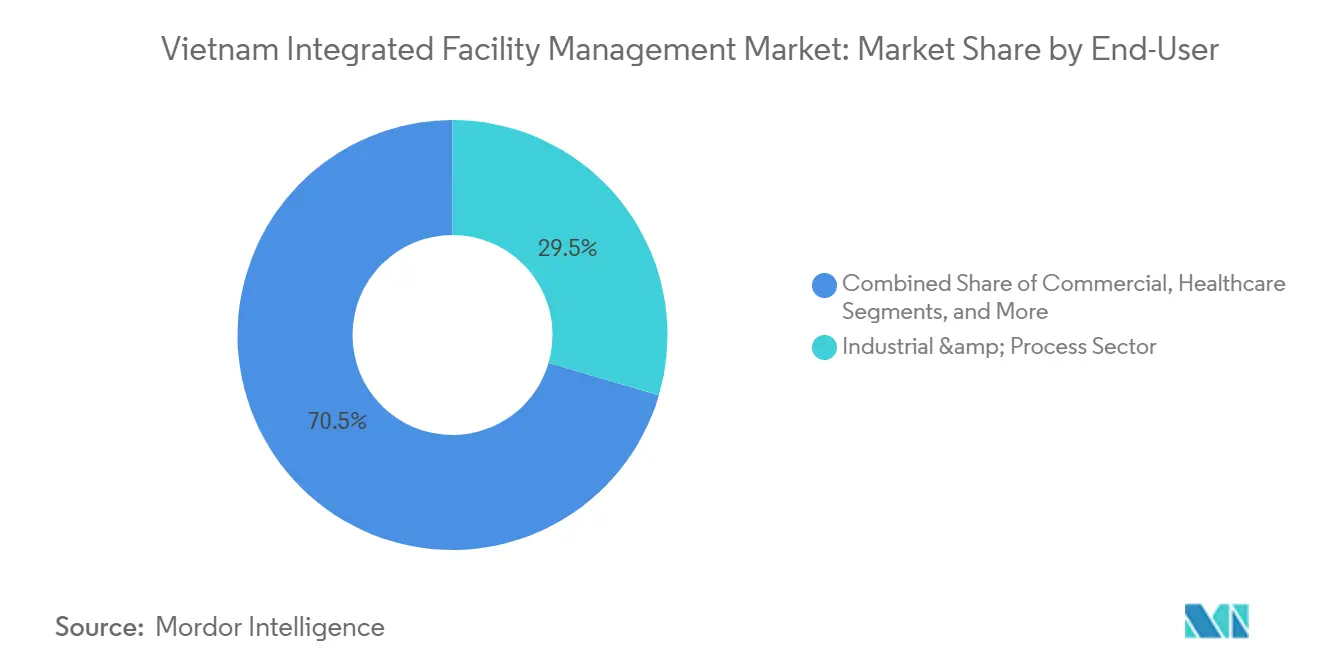

- By end-user, the industrial and process sector held 29.5% of the Vietnam integrated facility management market share in 2025, while the commercial segment is projected to record the highest CAGR at 6.5% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Vietnam Integrated Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising FDI Inflows and Industrial Park Expansion | +1.8% | North Vietnam, including Bac Ninh and Hai Phong, and South Vietnam, including Binh Duong, Dong Nai, and Ho Chi Minh City | Short term (≤ 2 years) |

| Rapid Urbanization and Commercial Real Estate Growth | +1.4% | Primarily Ho Chi Minh City and Hanoi, with secondary gains in Da Nang and Hai Phong | Medium term (2-4 years) |

| Cost Optimization Pressure Driving Outsourcing of Non-Core FM Activities | +0.9% | National, concentrated in Ho Chi Minh City and Hanoi multinational clusters | Short term (≤ 2 years) |

| Digital Transformation and Smart Building Technology Adoption | +0.8% | Ho Chi Minh City and Hanoi Grade A offices, and northern industrial parks in Bac Ninh and Bac Giang | Medium term (2-4 years) |

| Growing ESG Compliance Requirements and Green Building Certification Adoption | +0.7% | National, led by Ho Chi Minh City and Hanoi | Long term (≥ 4 years) |

| Expanding Hospitality, Retail, and Technology Office Sectors Requiring Specialized FM | +0.4% | National, with early gains in Hanoi, Ho Chi Minh City, and Da Nang | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising FDI And Industrial Park Expansion

The Vietnam integrated facility management market is gaining direct support from new industrial park supply and from the steady rise in higher-value manufacturing activity across both the north and the south. New factories, logistics hubs, and supplier campuses not only add floor area but also introduce technical systems, safety procedures, and operating protocols that require a single accountable service model rather than multiple disconnected vendors. This is especially visible in Bac Ninh, Bac Giang, and Hai Phong, where electronics, semiconductor assembly, and precision manufacturing tenants need cleanroom control, uninterrupted utilities, calibrated maintenance schedules, and auditable site security practices. The same pattern is visible in southern corridors such as Binh Duong and Dong Nai, where industrial expansion is creating a pipeline of bundled, technically intensive FM contracts. Savills Vietnam reported 42 newly approved industrial park projects in 2025, adding close to 8,400 hectares of leasable land, which supports a multi-year asset pipeline for the Vietnam integrated facility management market as those parks move toward occupancy.[1]Savills Vietnam, “Vietnam Industrial and Property Management Updates,” Savills Vietnam As Vietnam attracts more process-critical production, the service scope within the Vietnam integrated facility management market shifts upward from reactive site support toward preventive engineering, compliance management, and continuous operations assurance.

Rapid Urbanization and Commercial Real Estate Growth

Vietnam integrated facility management market is also expanding because urban construction in Hanoi and Ho Chi Minh City continues to add a large stock of buildings that need organized lifecycle management. Vietnam Television reported that the two cities had more than 2,870 completed high-rise buildings by late 2024, which shows that the demand base for recurring FM services is broad and still expanding.[2]Vietnam Television, “High-Rise Building Development in Hanoi and Ho Chi Minh City,” VTV The opportunity is strongest in newer Grade A and upper-tier commercial properties because those assets usually include centralized building management systems, HVAC zoning, smart access controls, and energy monitoring tools that require trained operators rather than single-line contractors. Green-certified office development is reinforcing that pattern because owners need maintenance regimes that preserve certification outcomes and support tenant expectations around energy, indoor air quality, and service transparency. West Hanoi and central Ho Chi Minh City are showing this movement most clearly, but the spillover is reaching Da Nang and Hai Phong as office, mixed-use, and logistics projects become more institutional in design. The same urban expansion is also lifting demand from hospitality, retail, and technology office occupiers, which need more specialized cleaning, support, security, and asset-care programs than older buildings typically required.

Cost Optimization Through Outsourcing Non-Core FM Activities

A large part of current demand in the Vietnam integrated facility management market comes from occupiers that want tighter cost control and less administrative friction across multi-site operations. When security, cleaning, MEP maintenance, catering, pest control, and waste management sit under separate contracts, the burden of procurement, performance review, safety coordination, and dispute handling becomes costly for occupiers. A bundled model reduces those coordination costs and gives corporate tenants a clearer line of accountability for service quality, downtime response, and compliance documentation. Savills Vietnam stated that a well-structured integrated FM model can improve operating efficiency by up to 15%, mainly through vendor consolidation, predictive maintenance, and energy savings.[3]VietnamPlus Editorial Team, “Outsourced Integrated Facility Management Growth in Vietnam,” VietnamPlus VietnamPlus also noted that outsourced IFM has been growing faster than the broader FM base, reflecting a formal shift toward tender-led procurement and more structured facility operations among corporate tenants. Vietnam integrated facility management market still faces slower conversion among domestic SMEs, but that segment remains an important medium-term opportunity as buyers become more comfortable with bundled pricing and lifecycle cost management.

Digital Transformation and Smart Building Technology Adoption

Digital capability is no longer optional in the Vietnam integrated facility management market, especially for premium offices, industrial campuses, and certified assets. Building owners increasingly expect service providers to support live dashboards, digital ticketing, energy KPI reporting, predictive maintenance schedules, and mobile workflows that can be audited by asset managers and occupiers. Savills Vietnam stated that its Property Cube platform was being used across more than 22 million m² of managed space in Vietnam, which shows how operational technology is now embedded into service delivery rather than treated as an add-on. This shift became stronger in 2026 when the Vietnam Green Building Council released LOTUS V4 because the updated framework requires more consistent performance monitoring across energy, water, and indoor environmental quality. That requirement matters for the Vietnam integrated facility management market because certified assets now need continuous digital audit trails rather than occasional manual reporting. Providers that cannot demonstrate smart-building capability are therefore less likely to qualify for premium tenders, even when their pricing is competitive.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Highly Fragmented and Unorganized FM Service Provider Landscape | -0.6% | National, most acute in secondary cities and domestic manufacturing clusters | Short term (≤ 2 years) |

| Shortage of Qualified and Skilled FM Professionals | -0.5% | National, particularly severe in northern industrial corridors such as Bac Ninh, Bac Giang, and Hai Phong | Medium term (2-4 years) |

| High Upfront Capital Investment Requirements for Integrated FM Technology Platforms | -0.3% | National, disproportionately affecting domestic mid-market FM providers | Medium term (2-4 years) |

| Low Awareness of Integrated FM Value Proposition Among Domestic SMEs | -0.2% | National, especially prevalent in secondary cities and residential real estate segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented And Unorganized Provider Landscape

The Vietnam integrated facility management market is still held back by a service base that remains highly fragmented across cleaning firms, security companies, maintenance vendors, and small local support providers. Vietnam Television noted that the number of new FM-related businesses has been rising quickly, but this expansion has not created a comparable rise in standardized delivery quality or broad multi-service capability. That makes vendor consolidation harder for occupiers because many domestic operators can manage one or two service lines effectively, but only a limited number can absorb a full IFM mandate with the right staffing depth, documentation discipline, and insurance coverage. Mid-market properties are the most exposed to this issue because they often rely on informal or narrowly scoped subcontracting arrangements that are difficult for integrated providers to displace on price alone. The absence of a compulsory national quality framework for FM keeps underqualified players in the bidding pool and caps average contract value across the Vietnam integrated facility management market. This same landscape also slows the conversion of domestic SMEs, which often remain unconvinced that integrated contracts offer enough value to justify a shift away from low-cost single-service procurement.

Shortage Of Qualified and Skilled FM Workforce

The Vietnam integrated facility management market also faces a structural labour constraint, especially in roles tied to MEP engineering, energy management, cleanroom environments, and smart-building operations. This shortage is most visible in northern industrial clusters, where advanced manufacturers need technicians who can work within strict uptime, safety, and process-control standards, yet providers often struggle to fill even current staffing needs. As Vietnam moves further into semiconductor packaging, EV components, and more complex electronics production, the gap between service needs and available technical labour is likely to remain wide. Wage inflation is a related pressure point because providers that won long-term contracts on older labour assumptions now face rising payroll costs for specialist roles. Another restraint comes from the capital needed to deploy BMS-linked monitoring, energy management software, and digital maintenance systems, which can delay upgrades among domestic providers that want to compete for larger mandates. The Vietnam integrated facility management market also grows more slowly in secondary cities because many local building owners and SMEs still have limited awareness of integrated FM’s lifecycle value, which delays adoption even where the service case is already clear.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard FM Growth Driven by Advanced Manufacturing Requirements

Soft facility management (FM) held 55.7% of Vietnam integrated facility management (IFM) market share in 2025, reflecting the wide use of cleaning, catering, pest control, concierge, and support services across commercial, hospitality, industrial, and residential properties. This segment remains large because labor-intensive environments, including hotels, hospitals, food processing units, and high-traffic office towers, require consistent headcount deployment and service routines that translate into steady contract value. The Vietnam IFM industry also gives Soft FM added weight because hygiene, occupancy support, and front-of-house services remain essential even when technical systems are less advanced. Bundled FM is gaining ground inside this mix, as occupiers prefer one contract that combines site support, asset care, and compliance reporting rather than a patchwork of separate vendors. LOTUS V4 adds another push because certified properties now need more structured performance records and standardized building operations, which fit better with coordinated service models than with fragmented outsourcing.

Hard FM is projected to grow at a 6.4% CAGR from 2026 to 2031, making it the fastest-growing service type in the Vietnam IFM market. The main reason is the technical profile of new assets entering operation, especially factories, ready-built industrial space, premium offices, and data-linked facilities that cannot rely on periodic repair crews alone. Semiconductor assemblers, electronics manufacturers, and EV component producers need planned maintenance, calibrated engineering support, fire system certification, and continuous MEP uptime to protect production quality and avoid shutdown risk. KCN Vietnam highlighted the rise of LEED Gold ready-built factories in locations such as Hai Phong, Dong Nai, and Bac Ninh, which reinforces the movement toward permanent on-site engineering teams and digitally supported maintenance routines. Within the Vietnam IFM industry, this means Hard FM is moving from a support function to a core value driver for contracts tied to advanced manufacturing and institutional-grade real estate.

By End-User Industry: Commercial Segment Accelerates as Green Offices Reshape FM Standards

Industrial and manufacturing accounted for 29.5% of demand in 2025, giving this segment the largest position in the Vietnam integrated facility management market. Its scale comes from the country’s wide network of industrial parks across Binh Duong, Dong Nai, Bac Ninh, Bac Giang, and Hai Phong, where factory construction and supplier clustering have created a deep stock of FM-intensive assets. These sites need a mix of security, technical maintenance, worker support services, waste handling, and HSE-aligned operating routines, which support integrated contracts even when buyers remain price sensitive. The commercial segment is forecast to expand at a 6.5% CAGR through 2031, which makes it the fastest-growing end-user category in the Vietnam integrated facility management market. That growth reflects a broader shift in asset quality because new offices, mixed-use schemes, co-working spaces, data centers, and healthcare facilities require more energy management, indoor environmental monitoring, advanced security, and documentation than older stock.

The remaining demand comes from healthcare, public infrastructure, and institutional buildings, all of which add different service needs to the Vietnam integrated facility management industry. Healthcare sites require infection control discipline and uninterrupted support for medical equipment environments, while public and institutional buildings are placing more attention on energy efficiency and lifecycle upgrades. Hospitality and retail also continue to add specialized demand, especially where tourism recovery and premium urban consumption raise service expectations around cleanliness, guest experience, and uptime. The commercial segment’s projected 6.5% CAGR shows that higher-quality real estate is not only adding floor space but also increasing contract scope and value within the Vietnam integrated facility management market. Providers that can prove green-building maintenance capability and structured compliance delivery are therefore in a stronger position to consolidate mandates that once supported multiple specialist vendors.

Geography Analysis

Southern Vietnam generated the largest share of the Vietnam IFM market in 2025, while Northern Vietnam remained the strongest growth corridor for high-specification industrial and commercial FM demand. In the north, Hanoi anchors demand from Grade A offices, government complexes, hospitals, and new digital infrastructure, while Bac Ninh, Bac Giang, and Hai Phong extend that demand into electronics, logistics, and semiconductor-linked manufacturing environments. These locations are more FM-intensive than conventional industrial zones because occupiers need cleaner production environments, stable utilities, disciplined maintenance cycles, and tighter security procedures. JLL’s engagement with CMC Telecom for a 20-MW Tier III data center in Hanoi illustrates how the Vietnam IFM market is moving into critical-environment mandates that require 24/7 monitoring and very low tolerance for service failure. Hanoi’s residential tower stock adds another layer of volume, and Vietnam Television reported that the city had more than 1,420 completed high-rise buildings by late 2024, which supports broad recurring demand beyond the premium office segment.

Southern Vietnam remains the revenue center of the Vietnam integrated facility management market because Ho Chi Minh City, Binh Duong, and Dong Nai combine the country’s deepest office base with its densest multinational industrial footprint. Ho Chi Minh City’s industrial parks attracted more than USD 5.3 billion of investment in 2025, and ready-built factory supply rose to 492,000 m², which signals a strong pipeline for technical and bundled FM contracts in coming years. This corridor also hosts major fast-moving consumer goods and export-oriented manufacturers whose facilities need strict hygiene, HSE, and support-service standards that favour scaled providers over small local vendors. As green-certified commercial stock and industrial automation both increases, the Vietnam integrated facility management market in the south is likely to remain the most competitive and the most service-diverse part of the country.

Central Vietnam is smaller today, but it is becoming a more visible expansion zone in the Vietnam integrated facility management market. Da Nang is drawing institutional attention as a technology, logistics, and commercial hub, and Savills Vietnam’s addition of Capital Square 3 in April 2026 points to rising demand for professional property management in the corridor. Hue adds a different demand layer through healthcare and education infrastructure, where campus services and hospital FM can create stable contract value even outside the main industrial belts. From a lower base, Central Vietnam is likely to grow faster than the national average through 2031, although absolute market size will remain below the north and the south as the region continues to build scale.

Competitive Landscape

The Vietnam integrated facility management market is moderately fragmented in premium contracts and highly fragmented across mid-market and residential accounts, which creates a clear split between global operators and local price-led providers. Savills Vietnam, CBRE, and JLL remain prominent in upper-tier mandates because they combine multinational client access, digital delivery systems, and stronger compliance infrastructure than most domestic competitors can match. Technology is a major point of differentiation because Savills has expanded the use of Property Cube, CBRE has emphasized IoT-enabled MEP monitoring, and JLL has moved deeper into data center FM, where uptime and critical systems discipline matter more than low headline pricing. Domestic providers such as PMC, G&T Facility Management, and other regional specialists are still gaining traction in second-tier cities and in less complex assets, where local relationships and lower pricing remain important. The white-space opportunity sits in light industrial and mid-tier commercial buildings because many of those properties still rely on multiple single-service contracts that could be consolidated if providers can package integrated services at workable entry prices.

LOTUS V4 is likely to sharpen that divide inside the Vietnam integrated facility management market because certification-linked operating requirements now reward providers that can show organized reporting, energy management discipline, and structured indoor environment controls. As more owners adopt green-certified development strategies, procurement standards become harder for smaller, subscale vendors to meet, even when they remain competitive on cost. That makes contract quality self-reinforcing because certified buildings tend to select providers with stronger systems, and those providers then build a deeper track record that improves their position in future tenders. ATALIAN Global Services’ acquisition of a 60% stake in TKT Cleaning in October 2025 is a useful example because it added workforce scale quickly and strengthened bundled soft-service capacity through one transaction. The Vietnam integrated facility management market is therefore showing early signs of consolidation, especially where international operators want faster access to labour depth, client relationships, and local delivery coverage.

Strategic moves over the past two years show how leading firms are positioning for that shift in the Vietnam integrated facility management market. Savills Vietnam expanded into Central Vietnam with Capital Square 3 in Da Nang, which improved its national management footprint across north, central, and south corridors. JLL’s data center FM engagement in Hanoi shows a push into higher-margin technical environments that smaller providers cannot easily replicate. CBRE’s long-term integrated FM win at Vinhomes Golden River in Ho Chi Minh City also reflects growing demand for technology-enabled and ESG-linked service models in premium mixed-use and residential assets. Taken together, these moves suggest that competition in the Vietnam integrated facility management market is becoming less about basic service line breadth and more about digital systems, specialized engineering, compliance readiness, and the ability to scale reliably across multiple asset classes.

Vietnam Integrated Facility Management Industry Leaders

CBRE Group, Inc.

Jones Lang LaSalle Incorporated

Savills plc

Cushman & Wakefield plc

Sodexo S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Savills Vietnam expanded its property management portfolio to include Capital Square 3 in Da Nang, marking a deliberate strategic extension into Central Vietnam's emerging commercial real estate market and signalling institutional investor confidence in the corridor's long-term FM demand. The addition reinforces Savills' national footprint across North, Central, and South Vietnam.

- February 2026: CBRE Vietnam secured a seven-year integrated FM contract for the 250,000 m² Vinhomes Golden River complex in Ho Chi Minh City, covering IoT-enabled MEP maintenance and ESG performance reporting aligned with LEED Gold certification targets. This represents one of the largest single integrated FM mandates awarded in Vietnam's premium residential segment to date.

- January 2026: Savills Vietnam was appointed as property management operator for Song Da Building in Hanoi, a two-tower, 27-story complex at My Dinh, implementing lifecycle asset management, proactive MEP maintenance, and energy optimization aligned with ESG standards to compete in Hanoi's increasingly green-benchmarked office leasing market.

- January 2026: The Marc 88, a Grade A LEED Silver-certified office development in West Hanoi, was added to Savills Vietnam's management portfolio. The mandate illustrates how institutional-quality assets in Hanoi's emerging office corridor require full-service integrated FM from first occupancy rather than migrating to professional FM post-stabilization.

Vietnam Integrated Facility Management Market Report Scope

The Vietnam Market Report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, Fire Systems and Safety, and Other Hard Facility Management Services], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and Other Soft Facility Management Services]), End User (Commercial (includes BFSI, IT and Telecom, Retail and Warehouses, etc.), Hospitality (includes Eateries, Restaurants and Large-Scale Hotels), Institutional and Public Infrastructure (includes Government Establishments, Education, Transportation such as Airports and Railways, etc.), Healthcare (includes Public and Private Healthcare Facilities), Industrial and Process Sector (includes Manufacturing, Energy including Oil and Gas Exploration, Mining, etc.), and Other End-User Industries (Multi-House Residential, Entertainment, Sports and Leisure)). The Market Forecasts are Provided in Terms of Value (USD).

| Hard Facility Management | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Facility Management Services | |

| Soft Facility Management | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft Facility Management Services |

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process Sector |

| Other End-User Industries |

| By Service Type | Hard Facility Management | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Facility Management Services | ||

| Soft Facility Management | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft Facility Management Services | ||

| By End User Industry | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process Sector | ||

| Other End-User Industries | ||

Key Questions Answered in the Report

What is the current size of the Vietnam integrated facility management space?

It stands at USD 1.66 billion in 2026 and is projected to reach USD 2.21 billion by 2031, growing at a 5.9% CAGR over 2026-2031.

Which service category leads demand in Vietnam?

Soft FM led in 2025 with 55.7% share, supported by cleaning, catering, concierge, pest control, and other labor-intensive support functions across multiple property types.

Which end-user group is growing the fastest through 2031?

Commercial is projected to grow the fastest at a 6.5% CAGR, driven by Grade A offices, mixed-use assets, green-certified buildings, data centers, and healthcare facilities.

Why are integrated contracts gaining traction over single-service outsourcing?

Building owners and occupiers want one accountable partner for MEP uptime, energy reporting, security, compliance, and support services, which helps reduce coordination cost and service gaps.

Which parts of Vietnam are creating the strongest demand?

Southern Vietnam generates the largest revenue base, while northern corridors such as Hanoi, Bac Ninh, Bac Giang, and Hai Phong are driving high-specification industrial and data-led demand.

What is the biggest challenge for providers operating in Vietnam?

The main constraint is the shortage of qualified FM professionals, especially in MEP engineering, cleanroom support, energy management, and smart-building operations.

Page last updated on: